Advantage & Disadvantage of Management Accounting

VerifiedAdded on 2021/02/19

|21

|6035

|116

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Content

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

1 Management Accounting & its requirements..........................................................................1

2 Different types of Management Accounting Reporting...........................................................3

3. Calculation of Cost through different Cost Accounting Techniques......................................5

Annex A......................................................................................................................................6

Annex B......................................................................................................................................6

ACTIVITY 2....................................................................................................................................8

4. Advantage & Disadvantages of planning tools used in Budgetary Control............................8

5. Adaption of Management Accounting System for resolving financial problems.................10

Annex C....................................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

1 Management Accounting & its requirements..........................................................................1

2 Different types of Management Accounting Reporting...........................................................3

3. Calculation of Cost through different Cost Accounting Techniques......................................5

Annex A......................................................................................................................................6

Annex B......................................................................................................................................6

ACTIVITY 2....................................................................................................................................8

4. Advantage & Disadvantages of planning tools used in Budgetary Control............................8

5. Adaption of Management Accounting System for resolving financial problems.................10

Annex C....................................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management Accounting is a method of accounting used by internal managers of

business organisation. Managers of company make various decisions related to cost minimisation

and preparation of future financial plan in accordance with organisations objectives. Different

reports are prepared by managers with the help of management accounting such as Costing

Report and Budgeting Report which in turn helps managers in decision making & formulating

strategies.

This report explain Management Accounting. Further, the below report elaborate various

types of systems used by managers in management accounting. Furthermore, importance of

management accounting systems are discussed in this report. Moreover, this report include

different types of report prepared by managers with the help of management accounting. Further,

this report prepare Income Statement with the help of different management accounting

techniques such as Marginal & Absorption Costing. Furthermore, the below stated report

includes advantages & disadvantages of planning tools used in Budgetary Control. At last, this

report explains application of management accounting in a business organisation with the

purpose of resolving financial problems.

ACTIVITY 1

1 Management Accounting & its requirements

Management Accounting

Financial Accounting & Management Accounting are two accounting methods. Financial

Accounting is used for disclosing financial information of a company to its external users

whereas Management Accounting essential for internal managers of a business firm.

Management Accounting helps managers in managing companies production process by

reducing cost. Further, This cost is also known as Cost Accounting as with this accounting

technique internal managers of company monitors and control cost incurred during

manufacturing process which in turn benefits business organisations in achieving high

profitability and Customer Base(Hague, 2018).

Further, with the help of this accounting method managers of company are able to

compare estimated cost of production with the actual cost and if there is any difference in both

actual & estimated cost than managers make further plans to eliminate unnecessary cost.

1

Management Accounting is a method of accounting used by internal managers of

business organisation. Managers of company make various decisions related to cost minimisation

and preparation of future financial plan in accordance with organisations objectives. Different

reports are prepared by managers with the help of management accounting such as Costing

Report and Budgeting Report which in turn helps managers in decision making & formulating

strategies.

This report explain Management Accounting. Further, the below report elaborate various

types of systems used by managers in management accounting. Furthermore, importance of

management accounting systems are discussed in this report. Moreover, this report include

different types of report prepared by managers with the help of management accounting. Further,

this report prepare Income Statement with the help of different management accounting

techniques such as Marginal & Absorption Costing. Furthermore, the below stated report

includes advantages & disadvantages of planning tools used in Budgetary Control. At last, this

report explains application of management accounting in a business organisation with the

purpose of resolving financial problems.

ACTIVITY 1

1 Management Accounting & its requirements

Management Accounting

Financial Accounting & Management Accounting are two accounting methods. Financial

Accounting is used for disclosing financial information of a company to its external users

whereas Management Accounting essential for internal managers of a business firm.

Management Accounting helps managers in managing companies production process by

reducing cost. Further, This cost is also known as Cost Accounting as with this accounting

technique internal managers of company monitors and control cost incurred during

manufacturing process which in turn benefits business organisations in achieving high

profitability and Customer Base(Hague, 2018).

Further, with the help of this accounting method managers of company are able to

compare estimated cost of production with the actual cost and if there is any difference in both

actual & estimated cost than managers make further plans to eliminate unnecessary cost.

1

Management Accounting Systems

Management Accounting systems are important for managers as with this systems

managers are able evaluated and difference between actual & estimated performance. Managers

of a company are also able to minimise risk associate in production & other business activities

which in turn enhances profitability of company. Thus, this system is having a significant

importance for managers and a business organisation. Different Types of Management

Accounting Systems are discussed below-

Cost Accounting System- This is the most required management accounting system as

with this managers of a company develop a structure through which they can analyse or make an

estimation of cost incurred during manufacturing process. After determining cost with the help of

this system managers are able to decide profit margin. Thus, this system is also important in

analysing profitability of a firm. Further, with this management accounting system managers can

determine value of inventory available for manufacturing process this benefits them in managing

& maintaining cost(Kaplan and Atkinson, 2015).

This system is also advantageous in determining different types of cost & products of

manufacturing such as Direct Cost and Standard Cost. Direct Cost includes Cost of Direct Raw

Material, Direct Overhead and Labour used in production process whereas, Standard cost is

estimated cost required to manufacture a product. Further, this system is also essential for

identifying profitability of different products offered by a business organisation and with that

managers can make decisions related to elimination of a product which is giving loss. This

further helps company in increasing its profits, performance, customer and market share.

Inventory Management System- Inventory is a most essential element without which a

company is note able to start its production process thus, it is necessary for a business

organisation to check availability of stock and determine value of its available stock. This can be

done by managers with the help of Inventory Management System as this system track inventory

level, sales orders and helps in developing different types bills related to material and other

production elements. Thus, this system is beneficial in managing inventory in a manner which

minimises cost.

Further, Managers are able to make decision related to selection of an inventory valuation

methods such as LIFO & FIFO. This cost evaluate cost included in each method and provides an

2

Management Accounting systems are important for managers as with this systems

managers are able evaluated and difference between actual & estimated performance. Managers

of a company are also able to minimise risk associate in production & other business activities

which in turn enhances profitability of company. Thus, this system is having a significant

importance for managers and a business organisation. Different Types of Management

Accounting Systems are discussed below-

Cost Accounting System- This is the most required management accounting system as

with this managers of a company develop a structure through which they can analyse or make an

estimation of cost incurred during manufacturing process. After determining cost with the help of

this system managers are able to decide profit margin. Thus, this system is also important in

analysing profitability of a firm. Further, with this management accounting system managers can

determine value of inventory available for manufacturing process this benefits them in managing

& maintaining cost(Kaplan and Atkinson, 2015).

This system is also advantageous in determining different types of cost & products of

manufacturing such as Direct Cost and Standard Cost. Direct Cost includes Cost of Direct Raw

Material, Direct Overhead and Labour used in production process whereas, Standard cost is

estimated cost required to manufacture a product. Further, this system is also essential for

identifying profitability of different products offered by a business organisation and with that

managers can make decisions related to elimination of a product which is giving loss. This

further helps company in increasing its profits, performance, customer and market share.

Inventory Management System- Inventory is a most essential element without which a

company is note able to start its production process thus, it is necessary for a business

organisation to check availability of stock and determine value of its available stock. This can be

done by managers with the help of Inventory Management System as this system track inventory

level, sales orders and helps in developing different types bills related to material and other

production elements. Thus, this system is beneficial in managing inventory in a manner which

minimises cost.

Further, Managers are able to make decision related to selection of an inventory valuation

methods such as LIFO & FIFO. This cost evaluate cost included in each method and provides an

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

appropriate method to company. This system is an essential requirement of management

accounting as it provides detailed information related to Reorder Point, Lead Demand, Order

Quantity, Stock Cover and Accuracy. This in turn benefits business in optimising cost & level f

inventory. Inventory Management System is applicable in all types of organisations such as

Manufacturing Firm, Retail Companies and other industries(Labro, 2019).

Job Costing System- A Costing System which helps managers in determining cost

involved in a particular job performed by a company is known as Job Costing. This system is

important as with this production managers of a business organisation can assess cost of each job

and make decisions of investment in a job which is more profitable. This system is implemented

in organisations which are introducing more than one product line and job. Further, it is also

beneficial for business ventures which are engaging in a manufacturing activity of unique

products. Event Management Companies and Interior designers most commonly use this system

as they their products & services differs with time.

This system is an essential requirement for companies which are paying high cost in

manufacturing of their products & services(Maas, Schaltegger and Crutzen, 2016).

Price Optimising System- Benefit of this management accounting system is it helps

managers in optimising prices of products & services offered by company according to the

demand & preference of customer which in turn benefits business firms in maximisation of its

customer base. This system enable managers in analysing response of customers at different

price and on that basis managers set a price which is accepted by most of the customers.

This system is applicable on organisations which are distributing their products &

services in more than one market. As individuals of different geographical area are having

different income level and different purchasing power. Further, managers determine price of

products after considering profit margin which in turn increases revenue of business(Advantages

of Benchmarking. 2016).

2 Different types of Management Accounting Reporting

Management Accounting Reports

Management Accounting Reports are prepared by managers which gives detailed

information related to cost, inventory and other elements used in process of product

development. This reports are disclosed to internal managers of company so that they can make

3

accounting as it provides detailed information related to Reorder Point, Lead Demand, Order

Quantity, Stock Cover and Accuracy. This in turn benefits business in optimising cost & level f

inventory. Inventory Management System is applicable in all types of organisations such as

Manufacturing Firm, Retail Companies and other industries(Labro, 2019).

Job Costing System- A Costing System which helps managers in determining cost

involved in a particular job performed by a company is known as Job Costing. This system is

important as with this production managers of a business organisation can assess cost of each job

and make decisions of investment in a job which is more profitable. This system is implemented

in organisations which are introducing more than one product line and job. Further, it is also

beneficial for business ventures which are engaging in a manufacturing activity of unique

products. Event Management Companies and Interior designers most commonly use this system

as they their products & services differs with time.

This system is an essential requirement for companies which are paying high cost in

manufacturing of their products & services(Maas, Schaltegger and Crutzen, 2016).

Price Optimising System- Benefit of this management accounting system is it helps

managers in optimising prices of products & services offered by company according to the

demand & preference of customer which in turn benefits business firms in maximisation of its

customer base. This system enable managers in analysing response of customers at different

price and on that basis managers set a price which is accepted by most of the customers.

This system is applicable on organisations which are distributing their products &

services in more than one market. As individuals of different geographical area are having

different income level and different purchasing power. Further, managers determine price of

products after considering profit margin which in turn increases revenue of business(Advantages

of Benchmarking. 2016).

2 Different types of Management Accounting Reporting

Management Accounting Reports

Management Accounting Reports are prepared by managers which gives detailed

information related to cost, inventory and other elements used in process of product

development. This reports are disclosed to internal managers of company so that they can make

3

decisions & develop strategies related investment, expansion, Increment in employees salary,

Introduction & minimisation of product line and elimination of cost. This reports are prepared

according to the business requirements. IT can be prepared monthly, Quarterly and

Annually(McVay, Kennedy and Fullerton, 2016).

Further, no specific format is used by companies for preparing management accounting

reports. Various types of management accounting reports are explained below-

Cost Managerial Accounting Reports- This report provide information related to cost of

each element used in manufacturing process like Raw Material, Labour and overheads. Further,

this report show amount of selling & manufacturing cost so that managers can identify amount of

profit generated by each unit. This reports are useful for managers as with this they can analyse

expenses done by company and it also provide information related to use of organisational

resources which in turn helps organisations in effective utilisation of their resources. Manager

also makes decisions related to waste management and determining hourly cost of labours on the

basis of this report(Medudula, Sagar and Gandhi, 2016).

Cost Accounting Reports are beneficial for companies a with this managers are able to

estimate future profits & expenses and which further plays a significant role in achieving

business objectives with formulating strategy of minimising cost.

Budget Reports- Budget Report shows future financial plan of a company according to

its future objectives which in turn benefits managers in evaluating performance of a business

firm. Budget is prepared by managers on the basis of historical data and this reports includes

information related to expenses, revenue, income & cost. This report is essential as whole

business operations of a company is decided on the basis of future budget.

Further, this report is an essential requirement for managers as managers decide amount

of incentives for employees and negotiate with suppliers of raw materials on the basis of this

report. A company can also achieve future goals & objectives if it operates its business in

accordance with Budget Reports.

Performance Report- Performance Report gives details of overall business activities

performed by an organisation so that managers of company can review performance of company

and its employees. Further, managers develop plans & policies if performance of company is not

4

Introduction & minimisation of product line and elimination of cost. This reports are prepared

according to the business requirements. IT can be prepared monthly, Quarterly and

Annually(McVay, Kennedy and Fullerton, 2016).

Further, no specific format is used by companies for preparing management accounting

reports. Various types of management accounting reports are explained below-

Cost Managerial Accounting Reports- This report provide information related to cost of

each element used in manufacturing process like Raw Material, Labour and overheads. Further,

this report show amount of selling & manufacturing cost so that managers can identify amount of

profit generated by each unit. This reports are useful for managers as with this they can analyse

expenses done by company and it also provide information related to use of organisational

resources which in turn helps organisations in effective utilisation of their resources. Manager

also makes decisions related to waste management and determining hourly cost of labours on the

basis of this report(Medudula, Sagar and Gandhi, 2016).

Cost Accounting Reports are beneficial for companies a with this managers are able to

estimate future profits & expenses and which further plays a significant role in achieving

business objectives with formulating strategy of minimising cost.

Budget Reports- Budget Report shows future financial plan of a company according to

its future objectives which in turn benefits managers in evaluating performance of a business

firm. Budget is prepared by managers on the basis of historical data and this reports includes

information related to expenses, revenue, income & cost. This report is essential as whole

business operations of a company is decided on the basis of future budget.

Further, this report is an essential requirement for managers as managers decide amount

of incentives for employees and negotiate with suppliers of raw materials on the basis of this

report. A company can also achieve future goals & objectives if it operates its business in

accordance with Budget Reports.

Performance Report- Performance Report gives details of overall business activities

performed by an organisation so that managers of company can review performance of company

and its employees. Further, managers develop plans & policies if performance of company is not

4

favourable according to this report and managers also conduct training & development

programmes for improving employees skills(Modugno and Di Carlo, 2019).

Different Department operated in an organisation also prepare their own performance

report so that managers which in turn helps in improving efficiency & effectiveness of operations

of each department. Managers also develop strategic objectives after reviewing performance

report of business firm.

Account Receivable Reports- If a company is selling its products & services on credit

than there is a requirement of Account Receivable Aging Report. With this report managers are

able to determine amount of bad debts and according to that they formulate their credit policy.

Further, managers can determine liquidity of company with the help of this report.

This report is essential as it gives information related to cash inflows and with this

managers are able to recover due amount from trade debtors.

Integration of Management Accounting Systems & Reports in Organisation Processes

Management Accounting Reports & Systems are inter related with each other. Because,

all the information included in managing accounting reports are abstract through systems of

management accounting. Further, both are an integrated part of organisation process as managers

make future decisions in accordance with results provided by management accounting reports.

Management Accounting System manage inventory level, determine cost of each job and

enhances profits of firm all this activities are part of business an organisation. Thus, management

accounting systems are integrated with operations of companies. Similarly, future estimation of

cost & revenue and analysis of performance is a part of business process as with that only a

company can make improvement in its operational process(Ndemewah, Menges and Hiebl,

2019).

Inventory is something without which a manufacturing process is impossible thus,

Inventory management System is useful and an integrated part of organisations process.

Management of Cost leads to profit maximisation and it is essential for a business. Formulation

of Credit Collection Policy manages cash inflow and cash is necessary for running a business

thus, Account Receivable Reports are also merged in business process.

5

programmes for improving employees skills(Modugno and Di Carlo, 2019).

Different Department operated in an organisation also prepare their own performance

report so that managers which in turn helps in improving efficiency & effectiveness of operations

of each department. Managers also develop strategic objectives after reviewing performance

report of business firm.

Account Receivable Reports- If a company is selling its products & services on credit

than there is a requirement of Account Receivable Aging Report. With this report managers are

able to determine amount of bad debts and according to that they formulate their credit policy.

Further, managers can determine liquidity of company with the help of this report.

This report is essential as it gives information related to cash inflows and with this

managers are able to recover due amount from trade debtors.

Integration of Management Accounting Systems & Reports in Organisation Processes

Management Accounting Reports & Systems are inter related with each other. Because,

all the information included in managing accounting reports are abstract through systems of

management accounting. Further, both are an integrated part of organisation process as managers

make future decisions in accordance with results provided by management accounting reports.

Management Accounting System manage inventory level, determine cost of each job and

enhances profits of firm all this activities are part of business an organisation. Thus, management

accounting systems are integrated with operations of companies. Similarly, future estimation of

cost & revenue and analysis of performance is a part of business process as with that only a

company can make improvement in its operational process(Ndemewah, Menges and Hiebl,

2019).

Inventory is something without which a manufacturing process is impossible thus,

Inventory management System is useful and an integrated part of organisations process.

Management of Cost leads to profit maximisation and it is essential for a business. Formulation

of Credit Collection Policy manages cash inflow and cash is necessary for running a business

thus, Account Receivable Reports are also merged in business process.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

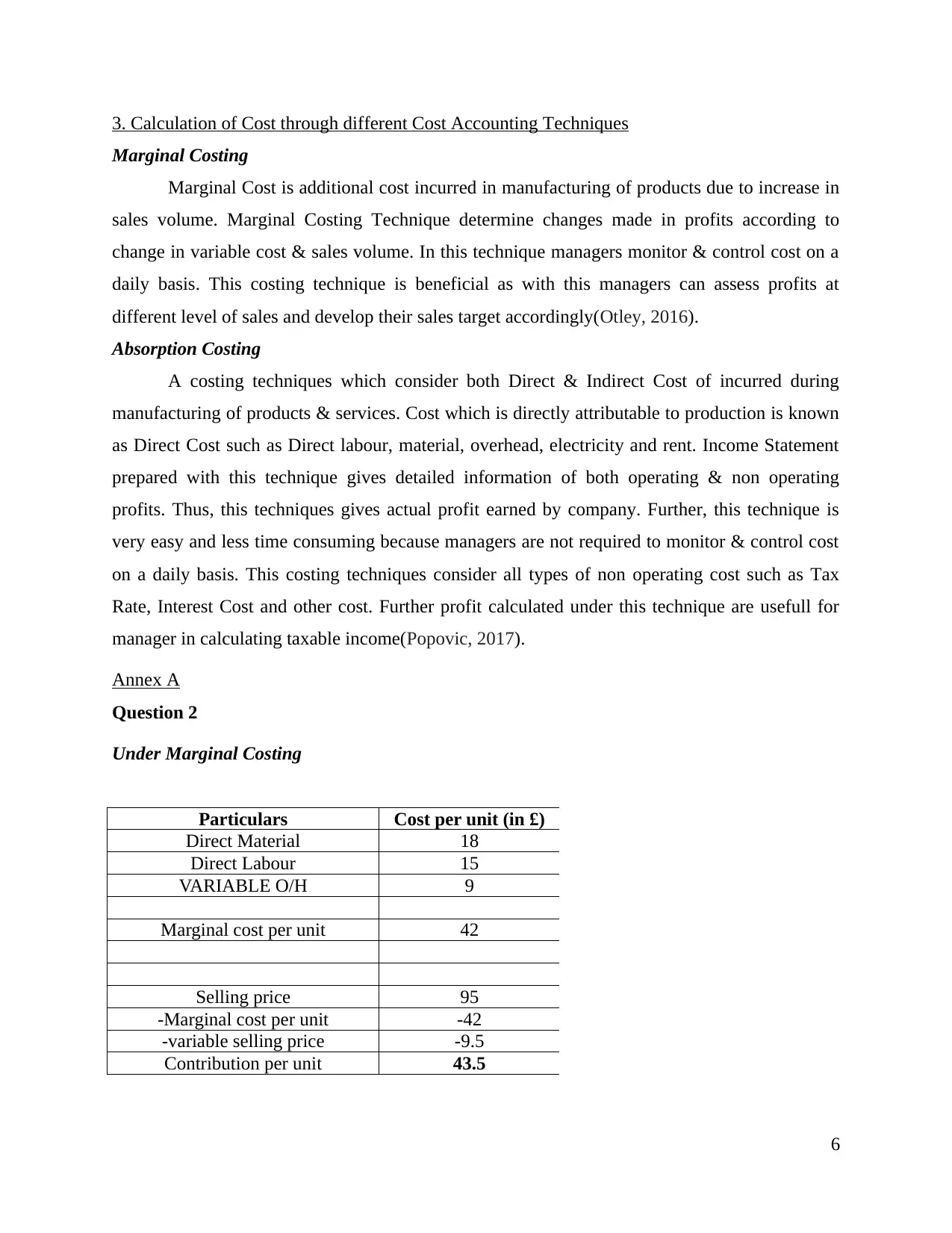

3. Calculation of Cost through different Cost Accounting Techniques

Marginal Costing

Marginal Cost is additional cost incurred in manufacturing of products due to increase in

sales volume. Marginal Costing Technique determine changes made in profits according to

change in variable cost & sales volume. In this technique managers monitor & control cost on a

daily basis. This costing technique is beneficial as with this managers can assess profits at

different level of sales and develop their sales target accordingly(Otley, 2016).

Absorption Costing

A costing techniques which consider both Direct & Indirect Cost of incurred during

manufacturing of products & services. Cost which is directly attributable to production is known

as Direct Cost such as Direct labour, material, overhead, electricity and rent. Income Statement

prepared with this technique gives detailed information of both operating & non operating

profits. Thus, this techniques gives actual profit earned by company. Further, this technique is

very easy and less time consuming because managers are not required to monitor & control cost

on a daily basis. This costing techniques consider all types of non operating cost such as Tax

Rate, Interest Cost and other cost. Further profit calculated under this technique are usefull for

manager in calculating taxable income(Popovic, 2017).

Annex A

Question 2

Under Marginal Costing

Particulars Cost per unit (in £)

Direct Material 18

Direct Labour 15

VARIABLE O/H 9

Marginal cost per unit 42

Selling price 95

-Marginal cost per unit -42

-variable selling price -9.5

Contribution per unit 43.5

6

Marginal Costing

Marginal Cost is additional cost incurred in manufacturing of products due to increase in

sales volume. Marginal Costing Technique determine changes made in profits according to

change in variable cost & sales volume. In this technique managers monitor & control cost on a

daily basis. This costing technique is beneficial as with this managers can assess profits at

different level of sales and develop their sales target accordingly(Otley, 2016).

Absorption Costing

A costing techniques which consider both Direct & Indirect Cost of incurred during

manufacturing of products & services. Cost which is directly attributable to production is known

as Direct Cost such as Direct labour, material, overhead, electricity and rent. Income Statement

prepared with this technique gives detailed information of both operating & non operating

profits. Thus, this techniques gives actual profit earned by company. Further, this technique is

very easy and less time consuming because managers are not required to monitor & control cost

on a daily basis. This costing techniques consider all types of non operating cost such as Tax

Rate, Interest Cost and other cost. Further profit calculated under this technique are usefull for

manager in calculating taxable income(Popovic, 2017).

Annex A

Question 2

Under Marginal Costing

Particulars Cost per unit (in £)

Direct Material 18

Direct Labour 15

VARIABLE O/H 9

Marginal cost per unit 42

Selling price 95

-Marginal cost per unit -42

-variable selling price -9.5

Contribution per unit 43.5

6

1st Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4,500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Labour (5000*15) 75000

Variable O/h (5000*9) 45000

210000

-Closing inventory (500*43.5) -21750

-188250

239250

-Variable selling

cost (4500*9.5) -42750

Contribution 196500

-Fixed costs -75000

-Fixed selling

expenses -45000

Actual Net

profit/(Net Loss) 76500

2nd Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (3000*95) 285000

Cost of sales:

Opening inventory (500*43.5) 21750

Material (5900*18) 106200

Labour (5900*15) 88500

Variable O/h (5900*9) 45000

261450

-Closing inventory (3400*43.5) -147900

-113550

171450

-Variable selling

cost (3000*9.5) -28500

Contribution 142950

-Fixed costs -75000

-Fixed selling

expenses -45000

7

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4,500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Labour (5000*15) 75000

Variable O/h (5000*9) 45000

210000

-Closing inventory (500*43.5) -21750

-188250

239250

-Variable selling

cost (4500*9.5) -42750

Contribution 196500

-Fixed costs -75000

-Fixed selling

expenses -45000

Actual Net

profit/(Net Loss) 76500

2nd Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (3000*95) 285000

Cost of sales:

Opening inventory (500*43.5) 21750

Material (5900*18) 106200

Labour (5900*15) 88500

Variable O/h (5900*9) 45000

261450

-Closing inventory (3400*43.5) -147900

-113550

171450

-Variable selling

cost (3000*9.5) -28500

Contribution 142950

-Fixed costs -75000

-Fixed selling

expenses -45000

7

Actual Net

profit/(Net Loss) 22950

Under Absorption

Costing

1st Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Annex B

Question 5

I.

Income Statement

(Marginal Costing)

FOR 650 UNITS

selling price (650*63) 40950

-Total Cost -29000

Net Profit 11950

Break Even Point (in units) 359.63

Break Even Point (in $) 22656.45

Income Statement

(Marginal Costing)

II.

FOR 400 UNITS

selling price (400*80) 32000

8

profit/(Net Loss) 22950

Under Absorption

Costing

1st Quarter

Particulars

Figures (in

£)

Figures (in

£)

Figures (in

£)

sales (4500*95) 427500

Cost of sales:

Opening inventory 0

Material (5000*18) 90000

Annex B

Question 5

I.

Income Statement

(Marginal Costing)

FOR 650 UNITS

selling price (650*63) 40950

-Total Cost -29000

Net Profit 11950

Break Even Point (in units) 359.63

Break Even Point (in $) 22656.45

Income Statement

(Marginal Costing)

II.

FOR 400 UNITS

selling price (400*80) 32000

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

-Total Cost -23538.46

Net Profit 8461.54

Break Even Point (in units) 254.50

Break Even Point (in $) 20359.79

Income Statement

(Marginal Costing)

III.

For 500 units

selling price (500*70) 35000

-Total Cost -25723.08

Net Profit 9276.92

Break Even Point (in units) 307.35

Break Even Point (in $) 21514.38

I.

Income Statement

(Absorption Costing)

For 650 units

Fixed Variable

Labour 6000 2000

Material 0 12000

Selling Costs 1800 200

Other Costs 7000 0

14800 14200

21.85

II.

Income Statement

9

Net Profit 8461.54

Break Even Point (in units) 254.50

Break Even Point (in $) 20359.79

Income Statement

(Marginal Costing)

III.

For 500 units

selling price (500*70) 35000

-Total Cost -25723.08

Net Profit 9276.92

Break Even Point (in units) 307.35

Break Even Point (in $) 21514.38

I.

Income Statement

(Absorption Costing)

For 650 units

Fixed Variable

Labour 6000 2000

Material 0 12000

Selling Costs 1800 200

Other Costs 7000 0

14800 14200

21.85

II.

Income Statement

9

(Absorption Costing)

For 400 units

Fixed Variable

Labour 6000 1230.77

Material 0 7384.62

Selling Costs 1800 123.08

Other Costs 7000 0.00

14800 8738.46 23538.46

21.85

III.

Income Statement

(Absorption Costing)

For 500 units

Fixed Variable

Labour 6000 1538.46

Material 0 9230.77

Selling Costs 1800 153.85

Other Costs 7000 0.00

14800 10923.08 25723.08

21.85

ACTIVITY 2

4. Advantage & Disadvantages of planning tools used in Budgetary Control

Budgetary Controlling is the process of preparation of budgets for various activities and

comparing the budgeted figures for arriving at certain decisions about the particular area. It is the

continuous process done in order to take best decisions from the available alternatives by

accountants, investors, regulators, auditors etc. There are different planning tools for the

budgetary control such as-

Zero Based Budgeting

Zero Based Budgeting is the process where every expenditure must be justified every

budget cycle. In this process budget starts with zero and every department plans describing

10

For 400 units

Fixed Variable

Labour 6000 1230.77

Material 0 7384.62

Selling Costs 1800 123.08

Other Costs 7000 0.00

14800 8738.46 23538.46

21.85

III.

Income Statement

(Absorption Costing)

For 500 units

Fixed Variable

Labour 6000 1538.46

Material 0 9230.77

Selling Costs 1800 153.85

Other Costs 7000 0.00

14800 10923.08 25723.08

21.85

ACTIVITY 2

4. Advantage & Disadvantages of planning tools used in Budgetary Control

Budgetary Controlling is the process of preparation of budgets for various activities and

comparing the budgeted figures for arriving at certain decisions about the particular area. It is the

continuous process done in order to take best decisions from the available alternatives by

accountants, investors, regulators, auditors etc. There are different planning tools for the

budgetary control such as-

Zero Based Budgeting

Zero Based Budgeting is the process where every expenditure must be justified every

budget cycle. In this process budget starts with zero and every department plans describing

10

which expense has to allocate and what will be benefits the company will be receiving from

it(Imtiaz Ferdous and et.al., 2019).

Advantages of Zero Based Budgeting -

Efficient allocation of resources, as it is based on needs and benefits.

It helps in justifying all the operating expenses spent in every budgeting period and what

are the generating revenues from such operating expenses.

It also helps in knowing in which area revenues are not generated so there is no need to

allocated funds in that particular area.

Disadvantages of Zero Based Budgeting-

It takes lot of time to closely review and justify every budget element rather than modify

an existing budget and review only new elements.

It can be manipulated by mangers to get more resources in their department.

Zero Based Budgeting can be applied by managers where they can identify alternative methods

of performing each activity such as evaluating the costs and benefits of making projects or

outsourcing it , or centralizing versus decentralizing operations.

Incremental Budgeting

Incremental Budgeting is the process where it is assumed that the entire organisation and

all of its departments will continue to operate at a minimum with the same budget used the

previous year. The budget used from the current fiscal year becomes the base for incremental

distribution for the next fiscal year(Dekker 2016).

Advantages of Incremental Budgeting-

Incremental Budgeting requires limited fluctuations in the allocation of the funds.

It is simple because it is based recent financial years or recent budget.

If any project requires funding for multiple years in order to achieve a certain outcome,

this budget will ensure that funds will keep flowing to the program.

Disadvantages of Incremental Budgeting-

It only assumes minor changes from the preceding period and does not take into account

major changes such as inflation rates, interest rates.

Managers tend to build too little revenue growth and excessive expenses into incremental

budgets so as to bring favourable variance.

11

it(Imtiaz Ferdous and et.al., 2019).

Advantages of Zero Based Budgeting -

Efficient allocation of resources, as it is based on needs and benefits.

It helps in justifying all the operating expenses spent in every budgeting period and what

are the generating revenues from such operating expenses.

It also helps in knowing in which area revenues are not generated so there is no need to

allocated funds in that particular area.

Disadvantages of Zero Based Budgeting-

It takes lot of time to closely review and justify every budget element rather than modify

an existing budget and review only new elements.

It can be manipulated by mangers to get more resources in their department.

Zero Based Budgeting can be applied by managers where they can identify alternative methods

of performing each activity such as evaluating the costs and benefits of making projects or

outsourcing it , or centralizing versus decentralizing operations.

Incremental Budgeting

Incremental Budgeting is the process where it is assumed that the entire organisation and

all of its departments will continue to operate at a minimum with the same budget used the

previous year. The budget used from the current fiscal year becomes the base for incremental

distribution for the next fiscal year(Dekker 2016).

Advantages of Incremental Budgeting-

Incremental Budgeting requires limited fluctuations in the allocation of the funds.

It is simple because it is based recent financial years or recent budget.

If any project requires funding for multiple years in order to achieve a certain outcome,

this budget will ensure that funds will keep flowing to the program.

Disadvantages of Incremental Budgeting-

It only assumes minor changes from the preceding period and does not take into account

major changes such as inflation rates, interest rates.

Managers tend to build too little revenue growth and excessive expenses into incremental

budgets so as to bring favourable variance.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

When the incremental budget is based on a prior budget, there tends to be a growing

disconnect between the budget and actual results.

This technique can be applied where managers wants to take certain decisions related to expense

for future projects based on the previous budgets.

Cash Based Budgeting

Cash Budget is a budget or plan of expected cash receipts an disbursements during the

period. These cash inflows and outflows include revenues collected, expenses paid, and loan

receipts and payments. In other words, a Cash budget is an projection of the company's cash

position in the future(Tappura and et.al., 2015).

Advantages of Cash Based Budgeting are-

It helps in minimizing the cost and profit maximization.

It helps the management to coordinate the activities of all the department in an

organisation

It helps in forecasting the future needs of funds, its time and the amount well in advance.

Thus, it helps in raising the funds through the most profitable sources at reasonable terms

and cost.

Disadvantages of Cash Based Budgeting-

Estimates limit the effectiveness of the cash budget because factual knowledge is not

available.

Managers with ulterior motives manipulate budget numbers to reflect well on themselves.

When using a cash budget to analyse financing needs and financing options, non-

financial factors are omitted.

Cash Based Budgeting can be applied to know what is minimum cash required by the company

so their will be no liquidity crunch in the organisation. Also, it helps in the controlling the extra

cost and helps in increasing the maximum profits for the company.

5. Adaption of Management Accounting System for resolving financial problems

Financial Problems such as lot of spendings, less profit making, lack of cash in the

organisation etc. Managing Financial Problems through management accounting systems involve

identification of the problems and then applying techniques like benchmarking, forecasting and

budgets, key performance indicators etc. to generate solutions(Chiwamit and et.al., 2017).

12

disconnect between the budget and actual results.

This technique can be applied where managers wants to take certain decisions related to expense

for future projects based on the previous budgets.

Cash Based Budgeting

Cash Budget is a budget or plan of expected cash receipts an disbursements during the

period. These cash inflows and outflows include revenues collected, expenses paid, and loan

receipts and payments. In other words, a Cash budget is an projection of the company's cash

position in the future(Tappura and et.al., 2015).

Advantages of Cash Based Budgeting are-

It helps in minimizing the cost and profit maximization.

It helps the management to coordinate the activities of all the department in an

organisation

It helps in forecasting the future needs of funds, its time and the amount well in advance.

Thus, it helps in raising the funds through the most profitable sources at reasonable terms

and cost.

Disadvantages of Cash Based Budgeting-

Estimates limit the effectiveness of the cash budget because factual knowledge is not

available.

Managers with ulterior motives manipulate budget numbers to reflect well on themselves.

When using a cash budget to analyse financing needs and financing options, non-

financial factors are omitted.

Cash Based Budgeting can be applied to know what is minimum cash required by the company

so their will be no liquidity crunch in the organisation. Also, it helps in the controlling the extra

cost and helps in increasing the maximum profits for the company.

5. Adaption of Management Accounting System for resolving financial problems

Financial Problems such as lot of spendings, less profit making, lack of cash in the

organisation etc. Managing Financial Problems through management accounting systems involve

identification of the problems and then applying techniques like benchmarking, forecasting and

budgets, key performance indicators etc. to generate solutions(Chiwamit and et.al., 2017).

12

Management Accounting uses different types of planning tools through which

performance of a business can be evaluated and which in turn benefits them in resolving

financial problems. If managers follow effective & appropriate systems & techniques of

management accounting than production manager are able to develop products at a lower cost

which resolves problem of profitability and with this company can maximise its sales volume.

Further, with management accounting a business organisation can compare cost, sales and other

variables which in turn maximises market share of company. With cost minimisation a company

is able to compete with its competitors as it can offer products at an affordable price which

attracts customers. Planning tolls through which financial problem of a company can be resolved

are discussed below-

Benchmarking

Benchmarking is setting up performance targets which a company should achieve to

excel in the industry I which it operates. These set benchmarks are then compared with the actual

achieved figures and the reasons due to which deviation arises a re studied with the aim of

minimizing them. This benchmarking technique helps in identifying the points at which a

company is lacking, improving, internal processes of a company, opportunities for growth,

identifying key competencies and gaining through competitive advantage(Renz, 2016).

A company can do either continuous improvement i.e. regular updating and improvement

in the processes or dramatic improvement which involves changing the entire internal working

system. This tool helps in resolving the problem by benchmarking any other companies profits

for our company in the same industry and same sector. In addition, it is about how certain

features can be realized better, faster and cheaper. There are various types of benchmarking such

as Process Benchmarking, Benchmarking from Investor Perspective, Product Benchmarking and

Strategic Benchmarking(Tucker and et.al., 2016).

Benchmarking resolves financial problems as it improves performance by influencing

organisations to adapt new and innovative technologies with that customers gets attracted and

that has a positive impact on financial of a company.

Pros

Benchmarking improves leaning capabilities & skills of employees of an organisation

which in turn improves over all operational efficiency of a company.

13

performance of a business can be evaluated and which in turn benefits them in resolving

financial problems. If managers follow effective & appropriate systems & techniques of

management accounting than production manager are able to develop products at a lower cost

which resolves problem of profitability and with this company can maximise its sales volume.

Further, with management accounting a business organisation can compare cost, sales and other

variables which in turn maximises market share of company. With cost minimisation a company

is able to compete with its competitors as it can offer products at an affordable price which

attracts customers. Planning tolls through which financial problem of a company can be resolved

are discussed below-

Benchmarking

Benchmarking is setting up performance targets which a company should achieve to

excel in the industry I which it operates. These set benchmarks are then compared with the actual

achieved figures and the reasons due to which deviation arises a re studied with the aim of

minimizing them. This benchmarking technique helps in identifying the points at which a

company is lacking, improving, internal processes of a company, opportunities for growth,

identifying key competencies and gaining through competitive advantage(Renz, 2016).

A company can do either continuous improvement i.e. regular updating and improvement

in the processes or dramatic improvement which involves changing the entire internal working

system. This tool helps in resolving the problem by benchmarking any other companies profits

for our company in the same industry and same sector. In addition, it is about how certain

features can be realized better, faster and cheaper. There are various types of benchmarking such

as Process Benchmarking, Benchmarking from Investor Perspective, Product Benchmarking and

Strategic Benchmarking(Tucker and et.al., 2016).

Benchmarking resolves financial problems as it improves performance by influencing

organisations to adapt new and innovative technologies with that customers gets attracted and

that has a positive impact on financial of a company.

Pros

Benchmarking improves leaning capabilities & skills of employees of an organisation

which in turn improves over all operational efficiency of a company.

13

A company using Benchmarking is able to offer better quality product than its

competitors.

Cons

Benchmarking only focuses on operational activities it does not consider all functions of

an organisation. Thus, it is not efficient in resolving overall financial problem.

This tool is very expensive & time consuming. Companies are getting dependent upon strategies formulated its competitors which

effects a companies Brand Image in a Negative Manner.

Key Performance Indicator

A KPI is a performance measurement technique useful in identifying those activities

which contribute mainly in the successful operation of the business activities. High level KPIs

may focus on the overall performance of the business, while low level KPIs may focus on

processes in departments such as sales, marketing, HR, support and others. Identification and

selection of the correct KPI's is a very crucial decision as different sectors and activities had

different performance indicators i.e. KPI can be financial as well as Non-Financial. KPI of

finance department (ratios, liquidity etc.) will be different from the one assigned to sales

department or an HR department (product/service quality, brand awareness etc.) this helps the

company in improving itself and increases the sustainability of the company. This tool resolves

problems by overviewing one particular area such as expenses of the company and how reduce

those expenses.

Pros

KPI provide Quantifiable results which helps in assessing profitability and other business

performance. For Example- A Hotel Industry can determine revenue generated from each

room by calculating RaVpar and if it is low than managers make plans so that it can be

improved.

A company can achieve its goals & objectives easily with the help of KPI which in turn

eliminate financial problems. Managers also decide incentives for employees as with KPI individuals performance can

be assessed.

14

competitors.

Cons

Benchmarking only focuses on operational activities it does not consider all functions of

an organisation. Thus, it is not efficient in resolving overall financial problem.

This tool is very expensive & time consuming. Companies are getting dependent upon strategies formulated its competitors which

effects a companies Brand Image in a Negative Manner.

Key Performance Indicator

A KPI is a performance measurement technique useful in identifying those activities

which contribute mainly in the successful operation of the business activities. High level KPIs

may focus on the overall performance of the business, while low level KPIs may focus on

processes in departments such as sales, marketing, HR, support and others. Identification and

selection of the correct KPI's is a very crucial decision as different sectors and activities had

different performance indicators i.e. KPI can be financial as well as Non-Financial. KPI of

finance department (ratios, liquidity etc.) will be different from the one assigned to sales

department or an HR department (product/service quality, brand awareness etc.) this helps the

company in improving itself and increases the sustainability of the company. This tool resolves

problems by overviewing one particular area such as expenses of the company and how reduce

those expenses.

Pros

KPI provide Quantifiable results which helps in assessing profitability and other business

performance. For Example- A Hotel Industry can determine revenue generated from each

room by calculating RaVpar and if it is low than managers make plans so that it can be

improved.

A company can achieve its goals & objectives easily with the help of KPI which in turn

eliminate financial problems. Managers also decide incentives for employees as with KPI individuals performance can

be assessed.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cons

Only short term goals can be achieved with this Key Performance Indicator. Different measures are required to be used under different situations thus, this tool is time

consuming and effective only when appropriate measures are used.

Variance Analysis

Variance Analysis is the quantitative analysis of the difference between actual and

planned behaviour. Variance Analysis is effective when the reviews are made on the amount of a

variance on a trend line, so that sudden changes in the variance level from month to month are

more readily apparent. Variance Analysis also involves the analysis of these differences, so that

the outcome is a statement of the difference from expectations, and an interpretation of why the

variance occurred. This level of detailed variance analysis allows management to understand

why fluctuations occur in its company and what it can do to change the situation.

There are various types of Variance analysis such as Purchase Price Variance, Labour

rate Variance, Variance Overhead Spending variance, Fixed Overhead spending variance,

Selling Price Variance, Material Yield Variance, Labour Efficiency Variance and Variable

Overhead Efficiency Variance. It is not necessary tot rack all the preceding variances. It may be

sufficient to review just one or two variances(Englund and et.al., 2018.).

Pros

Variance Analysis enable managers in evaluating their business performance and if there

is any variance than managers find out reasons for variance with this tool and take action

of resolving that problem.

This analysis control over cost of manufacturing and with this tool managers can set

target related to future sales volume & profits. Any defect in operational performance can be highlighted with this analysis which further

improves efficiency(Types of Managerial Accounting Reports. 2017).

Cons This tool of management accounting is not suitable for all organisation, it is useful only

for manufacturing companies. Thus, every company cannot achieve their objectives with

this planning tool of management accounting.

15

Only short term goals can be achieved with this Key Performance Indicator. Different measures are required to be used under different situations thus, this tool is time

consuming and effective only when appropriate measures are used.

Variance Analysis

Variance Analysis is the quantitative analysis of the difference between actual and

planned behaviour. Variance Analysis is effective when the reviews are made on the amount of a

variance on a trend line, so that sudden changes in the variance level from month to month are

more readily apparent. Variance Analysis also involves the analysis of these differences, so that

the outcome is a statement of the difference from expectations, and an interpretation of why the

variance occurred. This level of detailed variance analysis allows management to understand

why fluctuations occur in its company and what it can do to change the situation.

There are various types of Variance analysis such as Purchase Price Variance, Labour

rate Variance, Variance Overhead Spending variance, Fixed Overhead spending variance,

Selling Price Variance, Material Yield Variance, Labour Efficiency Variance and Variable

Overhead Efficiency Variance. It is not necessary tot rack all the preceding variances. It may be

sufficient to review just one or two variances(Englund and et.al., 2018.).

Pros

Variance Analysis enable managers in evaluating their business performance and if there

is any variance than managers find out reasons for variance with this tool and take action

of resolving that problem.

This analysis control over cost of manufacturing and with this tool managers can set

target related to future sales volume & profits. Any defect in operational performance can be highlighted with this analysis which further

improves efficiency(Types of Managerial Accounting Reports. 2017).

Cons This tool of management accounting is not suitable for all organisation, it is useful only

for manufacturing companies. Thus, every company cannot achieve their objectives with

this planning tool of management accounting.

15

Balanced Score Card

A balance scorecard is used to identify and improve various internal functions of a

business and their resulting external outcomes. It is used to measure and provide feedback to

organisations. Data collection is crucial to providing quantitative results because the information

collected is interpreted by managers and executives and used to make better decisions for the

organisation. There are four areas under Balance Scorecard such as involve learning and growth,

business processes, customers and finance.

Learning growth focuses on how effectively employees utilize the information to convert

it to a competitive advantage over the industry. Business Processes analyses to track any gaps,

delays, shortages or waste. Customer provides feedback abut their satisfaction with current

products. Financial Data includes financial ratios, budget variances, income targets etc. The

Balanced Scorecard is used to attain objectives, measurements, initiatives and goals that result

from these four primary functions of a business. Thus, Balanced Scorecard is referred as a

management tool rather than a measurement tool(Coad and et.al., 2015).

Pros Performance of an organisation is evaluated by managers according to goals & objectives

of company. Further, Financial, operational, Customer Base and growth of a company

can be assessed by managers with this tool which in turn benefits companies achievement

of organisational goals.

Cons

This tool does not use any standard method or & approach for measuring performance

which sometimes does not give accurate results(Talley, 2017).

Annex C

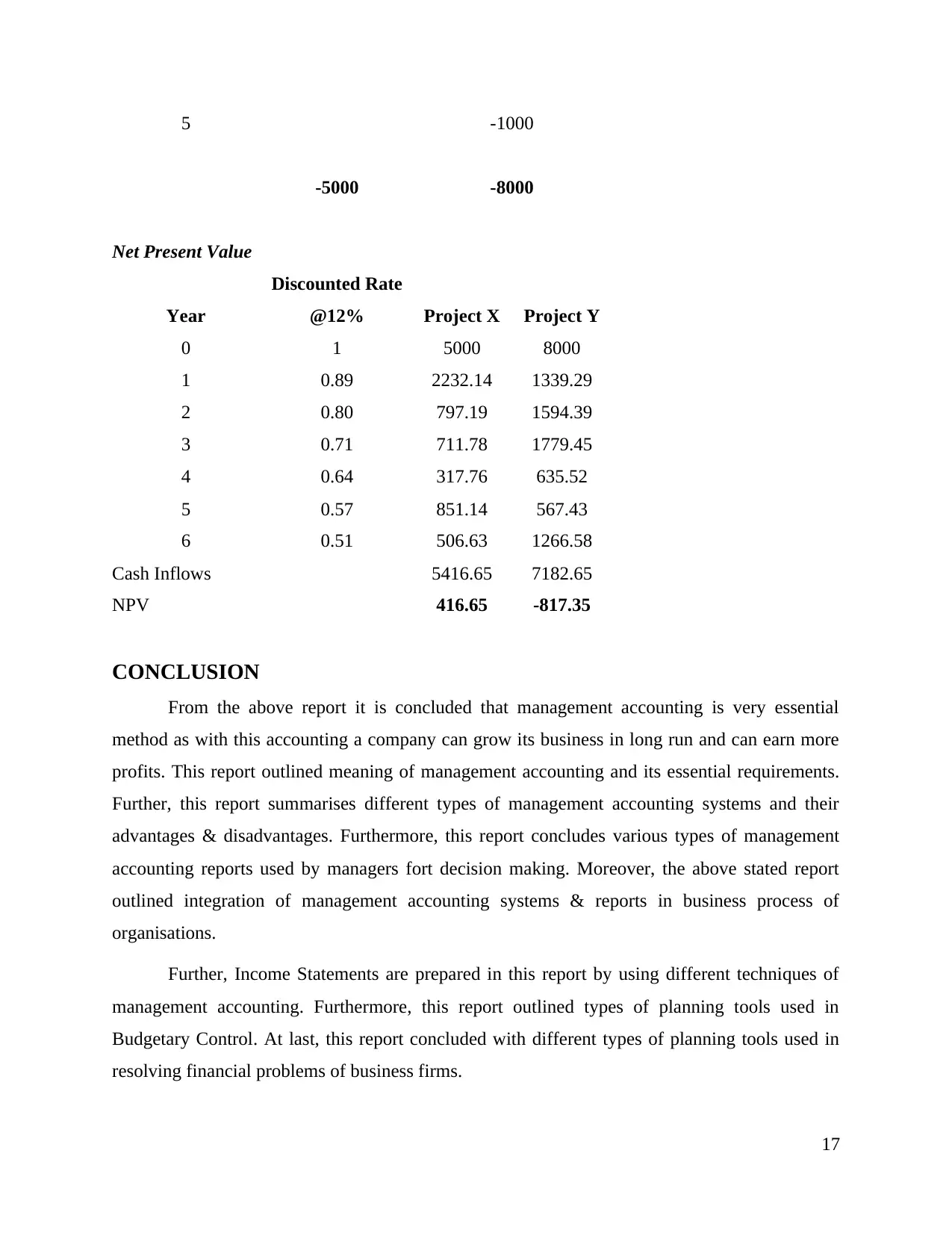

Payback Period Method

Year Project X Project Y

0 5000 8000

1 -2500 -1500

2 -1000 -2000

3 -1000 -2500

4 -500 -1000

16

A balance scorecard is used to identify and improve various internal functions of a

business and their resulting external outcomes. It is used to measure and provide feedback to

organisations. Data collection is crucial to providing quantitative results because the information

collected is interpreted by managers and executives and used to make better decisions for the

organisation. There are four areas under Balance Scorecard such as involve learning and growth,

business processes, customers and finance.

Learning growth focuses on how effectively employees utilize the information to convert

it to a competitive advantage over the industry. Business Processes analyses to track any gaps,

delays, shortages or waste. Customer provides feedback abut their satisfaction with current

products. Financial Data includes financial ratios, budget variances, income targets etc. The

Balanced Scorecard is used to attain objectives, measurements, initiatives and goals that result

from these four primary functions of a business. Thus, Balanced Scorecard is referred as a

management tool rather than a measurement tool(Coad and et.al., 2015).

Pros Performance of an organisation is evaluated by managers according to goals & objectives

of company. Further, Financial, operational, Customer Base and growth of a company

can be assessed by managers with this tool which in turn benefits companies achievement

of organisational goals.

Cons

This tool does not use any standard method or & approach for measuring performance

which sometimes does not give accurate results(Talley, 2017).

Annex C

Payback Period Method

Year Project X Project Y

0 5000 8000

1 -2500 -1500

2 -1000 -2000

3 -1000 -2500

4 -500 -1000

16

5 -1000

-5000 -8000

Net Present Value

Year

Discounted Rate

@12% Project X Project Y

0 1 5000 8000

1 0.89 2232.14 1339.29

2 0.80 797.19 1594.39

3 0.71 711.78 1779.45

4 0.64 317.76 635.52

5 0.57 851.14 567.43

6 0.51 506.63 1266.58

Cash Inflows 5416.65 7182.65

NPV 416.65 -817.35

CONCLUSION

From the above report it is concluded that management accounting is very essential

method as with this accounting a company can grow its business in long run and can earn more

profits. This report outlined meaning of management accounting and its essential requirements.

Further, this report summarises different types of management accounting systems and their

advantages & disadvantages. Furthermore, this report concludes various types of management

accounting reports used by managers fort decision making. Moreover, the above stated report

outlined integration of management accounting systems & reports in business process of

organisations.

Further, Income Statements are prepared in this report by using different techniques of

management accounting. Furthermore, this report outlined types of planning tools used in

Budgetary Control. At last, this report concluded with different types of planning tools used in

resolving financial problems of business firms.

17

-5000 -8000

Net Present Value

Year

Discounted Rate

@12% Project X Project Y

0 1 5000 8000

1 0.89 2232.14 1339.29

2 0.80 797.19 1594.39

3 0.71 711.78 1779.45

4 0.64 317.76 635.52

5 0.57 851.14 567.43

6 0.51 506.63 1266.58

Cash Inflows 5416.65 7182.65

NPV 416.65 -817.35

CONCLUSION

From the above report it is concluded that management accounting is very essential

method as with this accounting a company can grow its business in long run and can earn more

profits. This report outlined meaning of management accounting and its essential requirements.

Further, this report summarises different types of management accounting systems and their

advantages & disadvantages. Furthermore, this report concludes various types of management

accounting reports used by managers fort decision making. Moreover, the above stated report

outlined integration of management accounting systems & reports in business process of

organisations.

Further, Income Statements are prepared in this report by using different techniques of

management accounting. Furthermore, this report outlined types of planning tools used in

Budgetary Control. At last, this report concluded with different types of planning tools used in

resolving financial problems of business firms.

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Chenhall, R. H. and et.al., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Chiwamit, P. and et.al., 2017. Regulation and adaptation of management accounting innovations:

The case of economic value added in Thai state-owned enterprises. Management

Accounting Research. 37. pp.30-48.

Coad, A., Jack and et.al., 2015. Structuration theory: reflections on its further potential for

management accounting research. Qualitative Research in Accounting &

Management,. 12(2). pp.153-171.

Englund, H. and et.al., 2018. Management accounting and the paradox of embedded agency: A

framework for analyzing sources of structural change.

Hague, D., 2018. Pricing in business. Routledge.

Imtiaz Ferdous, M. and et.al., 2019. Institutional drivers of environmental management

accounting adoption in public sector water organisations. Accounting, Auditing &

Accountability Journal.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Labro, E., 2019. Costing Systems. Foundations and Trends® in Accounting. 13(3-4). pp.267-

404.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

McVay, G., Kennedy, F. and Fullerton, R., 2016. Accounting in the lean enterprise: providing

simple, practical, and decision-relevant information. Productivity Press.

Medudula, M.K., Sagar, M. and Gandhi, R.P., 2016. Costing and Pricing Mechanism of Telecom

Services. In Telecom Management in Emerging Economies (pp. 119-149). Springer, New

Delhi.

Modugno, G. and Di Carlo, F., 2019. Financial Sustainability of Higher Education Institutions:

A Challenge for the Accounting System. In Financial Sustainability of Public Sector

Entities(pp. 165-184). Palgrave Macmillan, Cham.

18

Books and Journals

Chenhall, R. H. and et.al., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Chiwamit, P. and et.al., 2017. Regulation and adaptation of management accounting innovations:

The case of economic value added in Thai state-owned enterprises. Management

Accounting Research. 37. pp.30-48.

Coad, A., Jack and et.al., 2015. Structuration theory: reflections on its further potential for

management accounting research. Qualitative Research in Accounting &

Management,. 12(2). pp.153-171.

Englund, H. and et.al., 2018. Management accounting and the paradox of embedded agency: A

framework for analyzing sources of structural change.

Hague, D., 2018. Pricing in business. Routledge.

Imtiaz Ferdous, M. and et.al., 2019. Institutional drivers of environmental management

accounting adoption in public sector water organisations. Accounting, Auditing &

Accountability Journal.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Labro, E., 2019. Costing Systems. Foundations and Trends® in Accounting. 13(3-4). pp.267-

404.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

McVay, G., Kennedy, F. and Fullerton, R., 2016. Accounting in the lean enterprise: providing

simple, practical, and decision-relevant information. Productivity Press.

Medudula, M.K., Sagar, M. and Gandhi, R.P., 2016. Costing and Pricing Mechanism of Telecom

Services. In Telecom Management in Emerging Economies (pp. 119-149). Springer, New

Delhi.

Modugno, G. and Di Carlo, F., 2019. Financial Sustainability of Higher Education Institutions:

A Challenge for the Accounting System. In Financial Sustainability of Public Sector

Entities(pp. 165-184). Palgrave Macmillan, Cham.

18

Ndemewah, S.R., Menges, K. and Hiebl, M.R., 2019. Management accounting research on

farms: what is known and what needs knowing?. Journal of Accounting & Organizational

Change. 15(1). pp.58-86.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Popovic, N., 2017. Review of Costing Tools Health System in Liberia. South Eastern European

Journal of Public Health.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Talley, W.K., 2017. Transport carrier costing. Routledge.

Online

Advantages of Benchmarking, 2016. [Online]. Available through:

<https://theinvestorsbook.com/benchmarking.html>

Managerial Accounting. 2019. [Online]. Available through

<https://xplaind.com/180841/managerial-accounting>

Types of Managerial Accounting Reports, 2017. [Online]. Available through:

<https://smallbusiness.chron.com/types-managerial-accounting-reports-58384.html>

19

farms: what is known and what needs knowing?. Journal of Accounting & Organizational

Change. 15(1). pp.58-86.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Popovic, N., 2017. Review of Costing Tools Health System in Liberia. South Eastern European

Journal of Public Health.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Talley, W.K., 2017. Transport carrier costing. Routledge.

Online

Advantages of Benchmarking, 2016. [Online]. Available through:

<https://theinvestorsbook.com/benchmarking.html>

Managerial Accounting. 2019. [Online]. Available through

<https://xplaind.com/180841/managerial-accounting>

Types of Managerial Accounting Reports, 2017. [Online]. Available through:

<https://smallbusiness.chron.com/types-managerial-accounting-reports-58384.html>

19

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.