Report on Management Accounting: Cost Allocation and Ethical Dilemmas

VerifiedAdded on 2023/01/05

|13

|2374

|48

Report

AI Summary

This report provides a detailed analysis of management accounting principles and techniques. It begins with an introduction to management accounting and then delves into various costing methods, including job costing, unit costing, and break-even analysis. The report explores different cost allocation methods such as direct, step-down, and reciprocal methods, comparing their application and accuracy. It examines break-even analysis, calculating break-even points under different sales mixes and considering operational income. The report also addresses an ethical dilemma faced by a sales manager in the context of budgeting, evaluating the implications of unethical behavior. The conclusion summarizes the key findings, emphasizing the importance of cost accounting in management decision-making. References to relevant literature are also provided.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Question 1...............................................................................................................................3

Question 2...............................................................................................................................6

Question 3...............................................................................................................................7

Question 4...............................................................................................................................9

Question 5.............................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Question 1...............................................................................................................................3

Question 2...............................................................................................................................6

Question 3...............................................................................................................................7

Question 4...............................................................................................................................9

Question 5.............................................................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

Introduction

Management accounting is that stream of accounting which is concerned with only internal

management of the company (Datar and Rajan, 2018). This report has been prepared to assess

various concepts of costing – job costing, unit costing, break even analysis and ethical dilemma

faced by managers while preparing various budgets.

Main Body

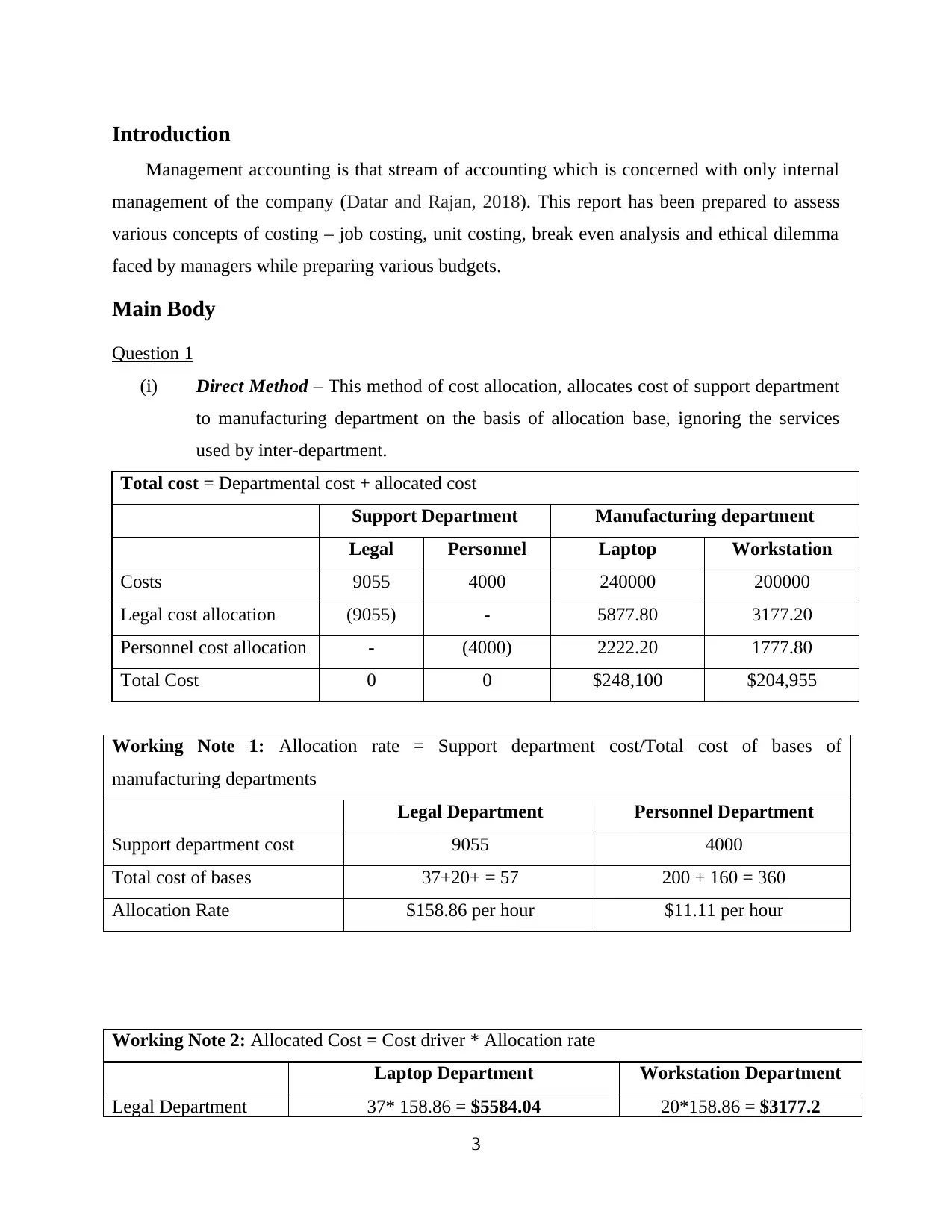

Question 1

(i) Direct Method – This method of cost allocation, allocates cost of support department

to manufacturing department on the basis of allocation base, ignoring the services

used by inter-department.

Total cost = Departmental cost + allocated cost

Support Department Manufacturing department

Legal Personnel Laptop Workstation

Costs 9055 4000 240000 200000

Legal cost allocation (9055) - 5877.80 3177.20

Personnel cost allocation - (4000) 2222.20 1777.80

Total Cost 0 0 $248,100 $204,955

Working Note 1: Allocation rate = Support department cost/Total cost of bases of

manufacturing departments

Legal Department Personnel Department

Support department cost 9055 4000

Total cost of bases 37+20+ = 57 200 + 160 = 360

Allocation Rate $158.86 per hour $11.11 per hour

Working Note 2: Allocated Cost = Cost driver * Allocation rate

Laptop Department Workstation Department

Legal Department 37* 158.86 = $5584.04 20*158.86 = $3177.2

3

Management accounting is that stream of accounting which is concerned with only internal

management of the company (Datar and Rajan, 2018). This report has been prepared to assess

various concepts of costing – job costing, unit costing, break even analysis and ethical dilemma

faced by managers while preparing various budgets.

Main Body

Question 1

(i) Direct Method – This method of cost allocation, allocates cost of support department

to manufacturing department on the basis of allocation base, ignoring the services

used by inter-department.

Total cost = Departmental cost + allocated cost

Support Department Manufacturing department

Legal Personnel Laptop Workstation

Costs 9055 4000 240000 200000

Legal cost allocation (9055) - 5877.80 3177.20

Personnel cost allocation - (4000) 2222.20 1777.80

Total Cost 0 0 $248,100 $204,955

Working Note 1: Allocation rate = Support department cost/Total cost of bases of

manufacturing departments

Legal Department Personnel Department

Support department cost 9055 4000

Total cost of bases 37+20+ = 57 200 + 160 = 360

Allocation Rate $158.86 per hour $11.11 per hour

Working Note 2: Allocated Cost = Cost driver * Allocation rate

Laptop Department Workstation Department

Legal Department 37* 158.86 = $5584.04 20*158.86 = $3177.2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

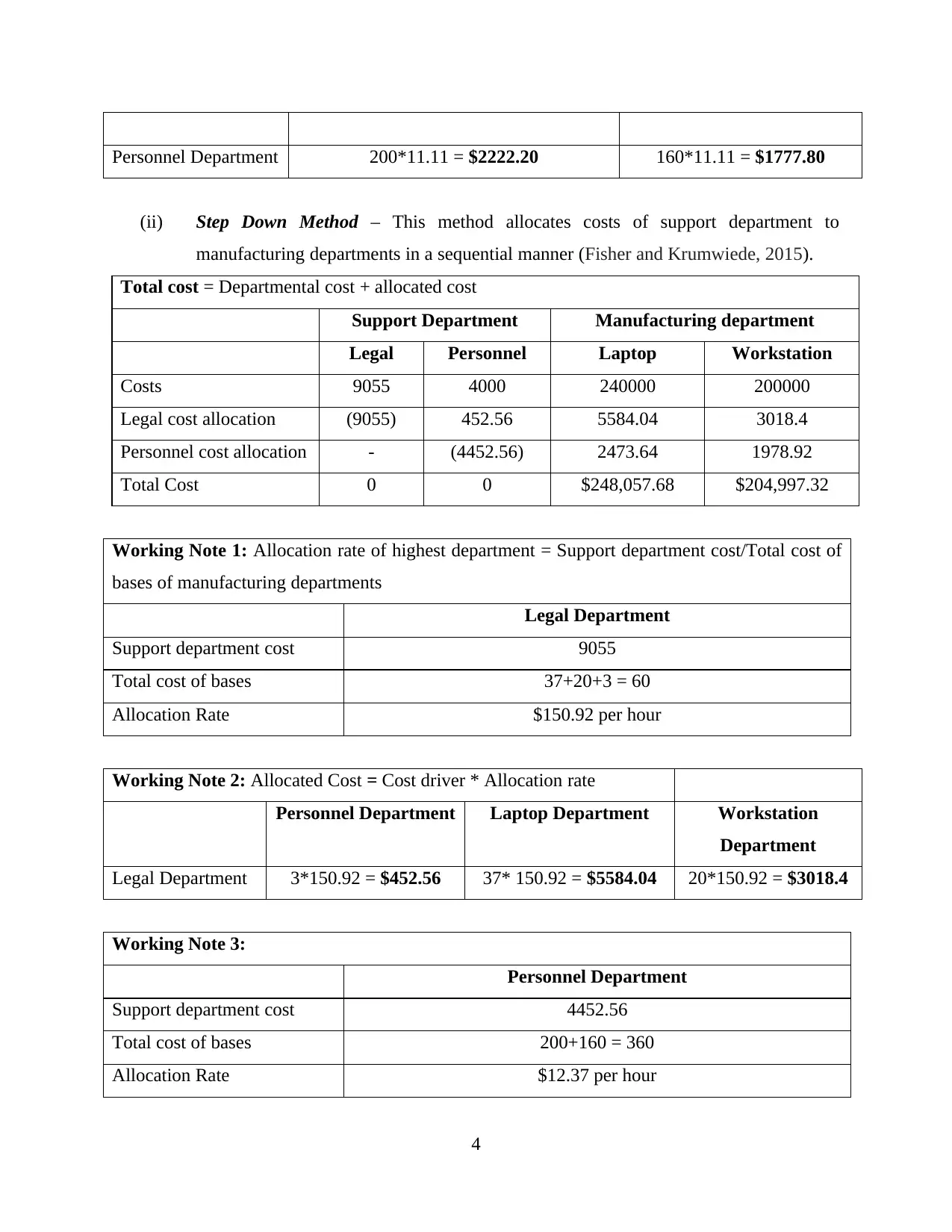

Personnel Department 200*11.11 = $2222.20 160*11.11 = $1777.80

(ii) Step Down Method – This method allocates costs of support department to

manufacturing departments in a sequential manner (Fisher and Krumwiede, 2015).

Total cost = Departmental cost + allocated cost

Support Department Manufacturing department

Legal Personnel Laptop Workstation

Costs 9055 4000 240000 200000

Legal cost allocation (9055) 452.56 5584.04 3018.4

Personnel cost allocation - (4452.56) 2473.64 1978.92

Total Cost 0 0 $248,057.68 $204,997.32

Working Note 1: Allocation rate of highest department = Support department cost/Total cost of

bases of manufacturing departments

Legal Department

Support department cost 9055

Total cost of bases 37+20+3 = 60

Allocation Rate $150.92 per hour

Working Note 2: Allocated Cost = Cost driver * Allocation rate

Personnel Department Laptop Department Workstation

Department

Legal Department 3*150.92 = $452.56 37* 150.92 = $5584.04 20*150.92 = $3018.4

Working Note 3:

Personnel Department

Support department cost 4452.56

Total cost of bases 200+160 = 360

Allocation Rate $12.37 per hour

4

(ii) Step Down Method – This method allocates costs of support department to

manufacturing departments in a sequential manner (Fisher and Krumwiede, 2015).

Total cost = Departmental cost + allocated cost

Support Department Manufacturing department

Legal Personnel Laptop Workstation

Costs 9055 4000 240000 200000

Legal cost allocation (9055) 452.56 5584.04 3018.4

Personnel cost allocation - (4452.56) 2473.64 1978.92

Total Cost 0 0 $248,057.68 $204,997.32

Working Note 1: Allocation rate of highest department = Support department cost/Total cost of

bases of manufacturing departments

Legal Department

Support department cost 9055

Total cost of bases 37+20+3 = 60

Allocation Rate $150.92 per hour

Working Note 2: Allocated Cost = Cost driver * Allocation rate

Personnel Department Laptop Department Workstation

Department

Legal Department 3*150.92 = $452.56 37* 150.92 = $5584.04 20*150.92 = $3018.4

Working Note 3:

Personnel Department

Support department cost 4452.56

Total cost of bases 200+160 = 360

Allocation Rate $12.37 per hour

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

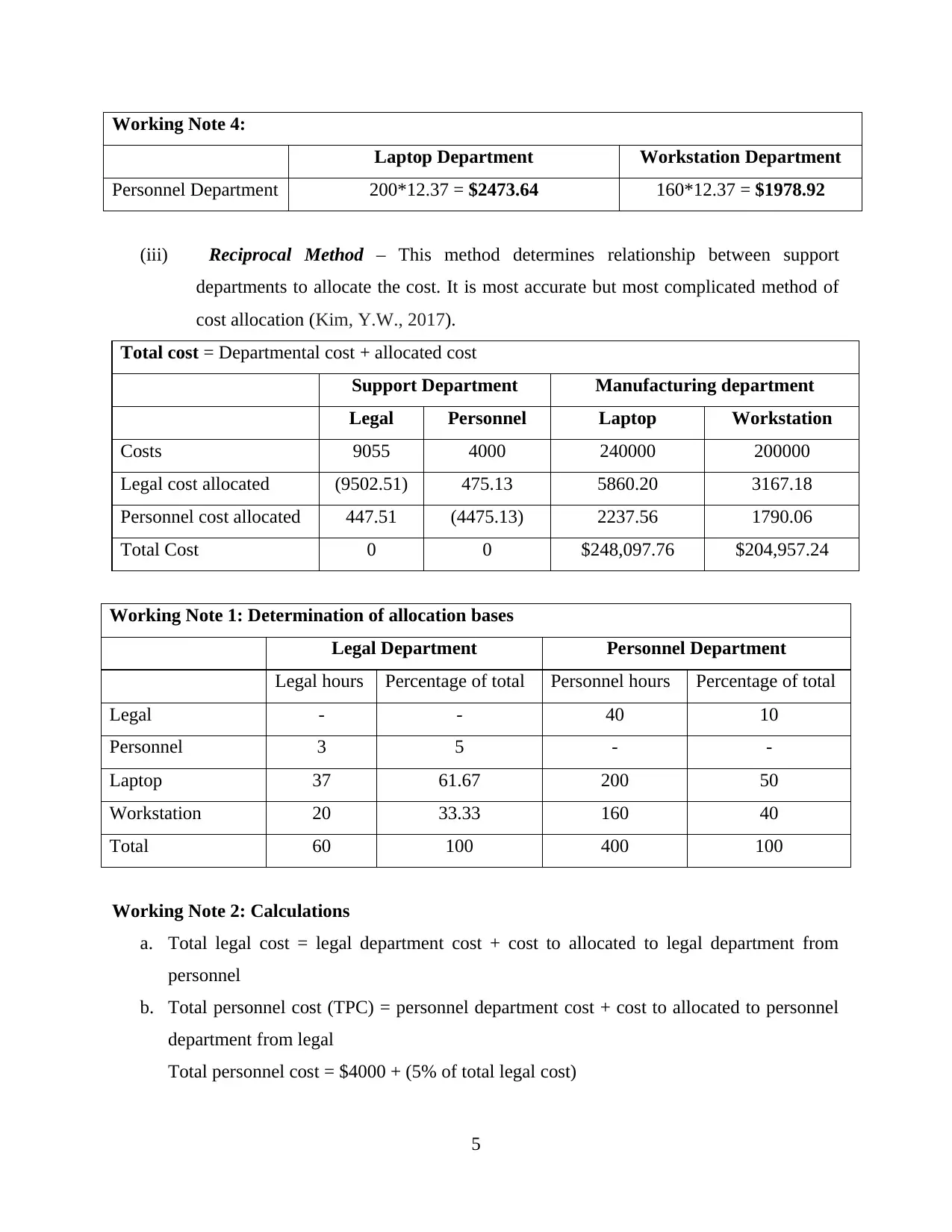

Working Note 4:

Laptop Department Workstation Department

Personnel Department 200*12.37 = $2473.64 160*12.37 = $1978.92

(iii) Reciprocal Method – This method determines relationship between support

departments to allocate the cost. It is most accurate but most complicated method of

cost allocation (Kim, Y.W., 2017).

Total cost = Departmental cost + allocated cost

Support Department Manufacturing department

Legal Personnel Laptop Workstation

Costs 9055 4000 240000 200000

Legal cost allocated (9502.51) 475.13 5860.20 3167.18

Personnel cost allocated 447.51 (4475.13) 2237.56 1790.06

Total Cost 0 0 $248,097.76 $204,957.24

Working Note 1: Determination of allocation bases

Legal Department Personnel Department

Legal hours Percentage of total Personnel hours Percentage of total

Legal - - 40 10

Personnel 3 5 - -

Laptop 37 61.67 200 50

Workstation 20 33.33 160 40

Total 60 100 400 100

Working Note 2: Calculations

a. Total legal cost = legal department cost + cost to allocated to legal department from

personnel

b. Total personnel cost (TPC) = personnel department cost + cost to allocated to personnel

department from legal

Total personnel cost = $4000 + (5% of total legal cost)

5

Laptop Department Workstation Department

Personnel Department 200*12.37 = $2473.64 160*12.37 = $1978.92

(iii) Reciprocal Method – This method determines relationship between support

departments to allocate the cost. It is most accurate but most complicated method of

cost allocation (Kim, Y.W., 2017).

Total cost = Departmental cost + allocated cost

Support Department Manufacturing department

Legal Personnel Laptop Workstation

Costs 9055 4000 240000 200000

Legal cost allocated (9502.51) 475.13 5860.20 3167.18

Personnel cost allocated 447.51 (4475.13) 2237.56 1790.06

Total Cost 0 0 $248,097.76 $204,957.24

Working Note 1: Determination of allocation bases

Legal Department Personnel Department

Legal hours Percentage of total Personnel hours Percentage of total

Legal - - 40 10

Personnel 3 5 - -

Laptop 37 61.67 200 50

Workstation 20 33.33 160 40

Total 60 100 400 100

Working Note 2: Calculations

a. Total legal cost = legal department cost + cost to allocated to legal department from

personnel

b. Total personnel cost (TPC) = personnel department cost + cost to allocated to personnel

department from legal

Total personnel cost = $4000 + (5% of total legal cost)

5

= $4000 + (5% * [legal department cost + cost to allocated to legal

department from personnel])

TPC = 4000 + (5% * [9055 + 10%] TPC)

Solving the above equation, we get: Total personnel cost = $4475.13

Total legal cost = $9055 + (4475.13*10%) = $9502.51

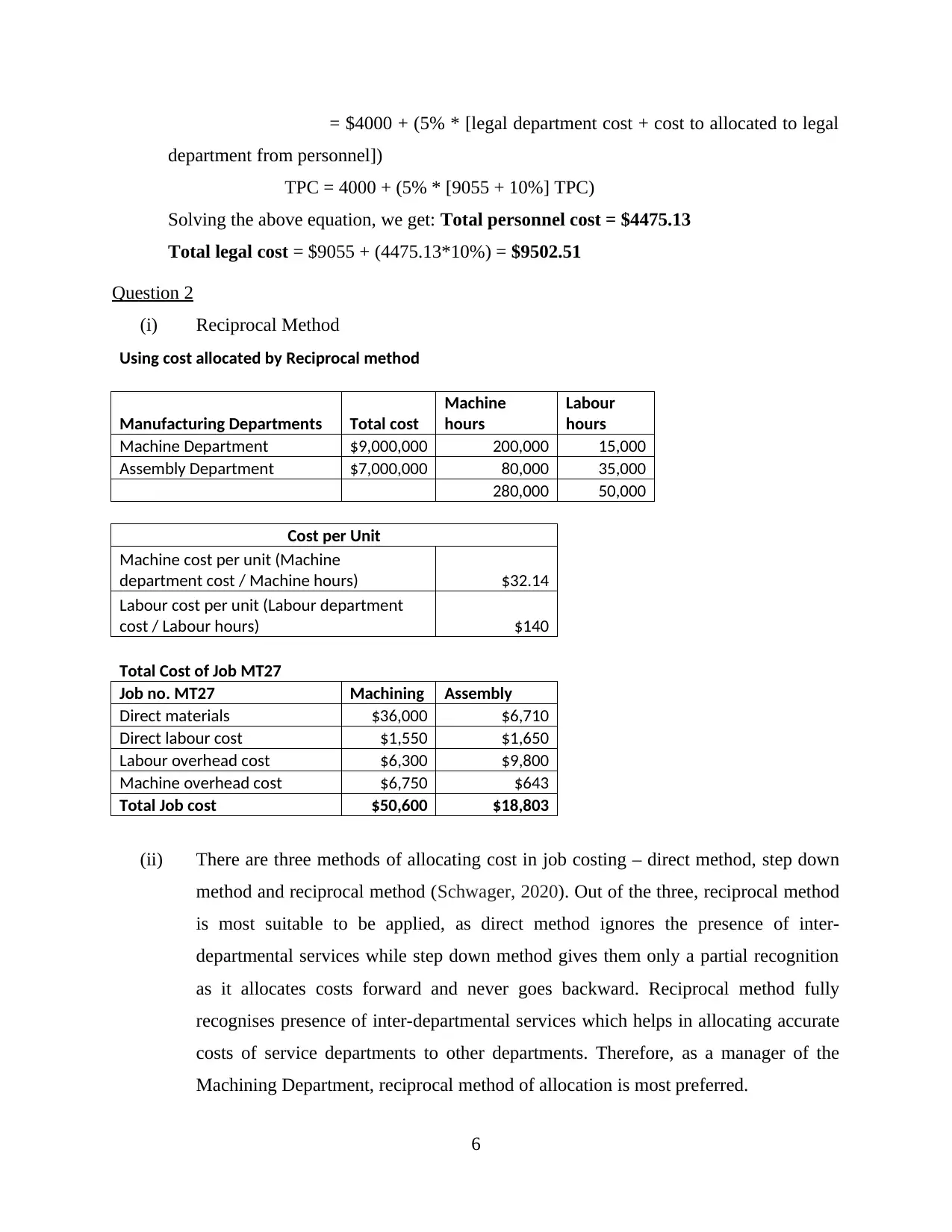

Question 2

(i) Reciprocal Method

Using cost allocated by Reciprocal method

Manufacturing Departments Total cost

Machine

hours

Labour

hours

Machine Department $9,000,000 200,000 15,000

Assembly Department $7,000,000 80,000 35,000

280,000 50,000

Cost per Unit

Machine cost per unit (Machine

department cost / Machine hours) $32.14

Labour cost per unit (Labour department

cost / Labour hours) $140

Total Cost of Job MT27

Job no. MT27 Machining Assembly

Direct materials $36,000 $6,710

Direct labour cost $1,550 $1,650

Labour overhead cost $6,300 $9,800

Machine overhead cost $6,750 $643

Total Job cost $50,600 $18,803

(ii) There are three methods of allocating cost in job costing – direct method, step down

method and reciprocal method (Schwager, 2020). Out of the three, reciprocal method

is most suitable to be applied, as direct method ignores the presence of inter-

departmental services while step down method gives them only a partial recognition

as it allocates costs forward and never goes backward. Reciprocal method fully

recognises presence of inter-departmental services which helps in allocating accurate

costs of service departments to other departments. Therefore, as a manager of the

Machining Department, reciprocal method of allocation is most preferred.

6

department from personnel])

TPC = 4000 + (5% * [9055 + 10%] TPC)

Solving the above equation, we get: Total personnel cost = $4475.13

Total legal cost = $9055 + (4475.13*10%) = $9502.51

Question 2

(i) Reciprocal Method

Using cost allocated by Reciprocal method

Manufacturing Departments Total cost

Machine

hours

Labour

hours

Machine Department $9,000,000 200,000 15,000

Assembly Department $7,000,000 80,000 35,000

280,000 50,000

Cost per Unit

Machine cost per unit (Machine

department cost / Machine hours) $32.14

Labour cost per unit (Labour department

cost / Labour hours) $140

Total Cost of Job MT27

Job no. MT27 Machining Assembly

Direct materials $36,000 $6,710

Direct labour cost $1,550 $1,650

Labour overhead cost $6,300 $9,800

Machine overhead cost $6,750 $643

Total Job cost $50,600 $18,803

(ii) There are three methods of allocating cost in job costing – direct method, step down

method and reciprocal method (Schwager, 2020). Out of the three, reciprocal method

is most suitable to be applied, as direct method ignores the presence of inter-

departmental services while step down method gives them only a partial recognition

as it allocates costs forward and never goes backward. Reciprocal method fully

recognises presence of inter-departmental services which helps in allocating accurate

costs of service departments to other departments. Therefore, as a manager of the

Machining Department, reciprocal method of allocation is most preferred.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

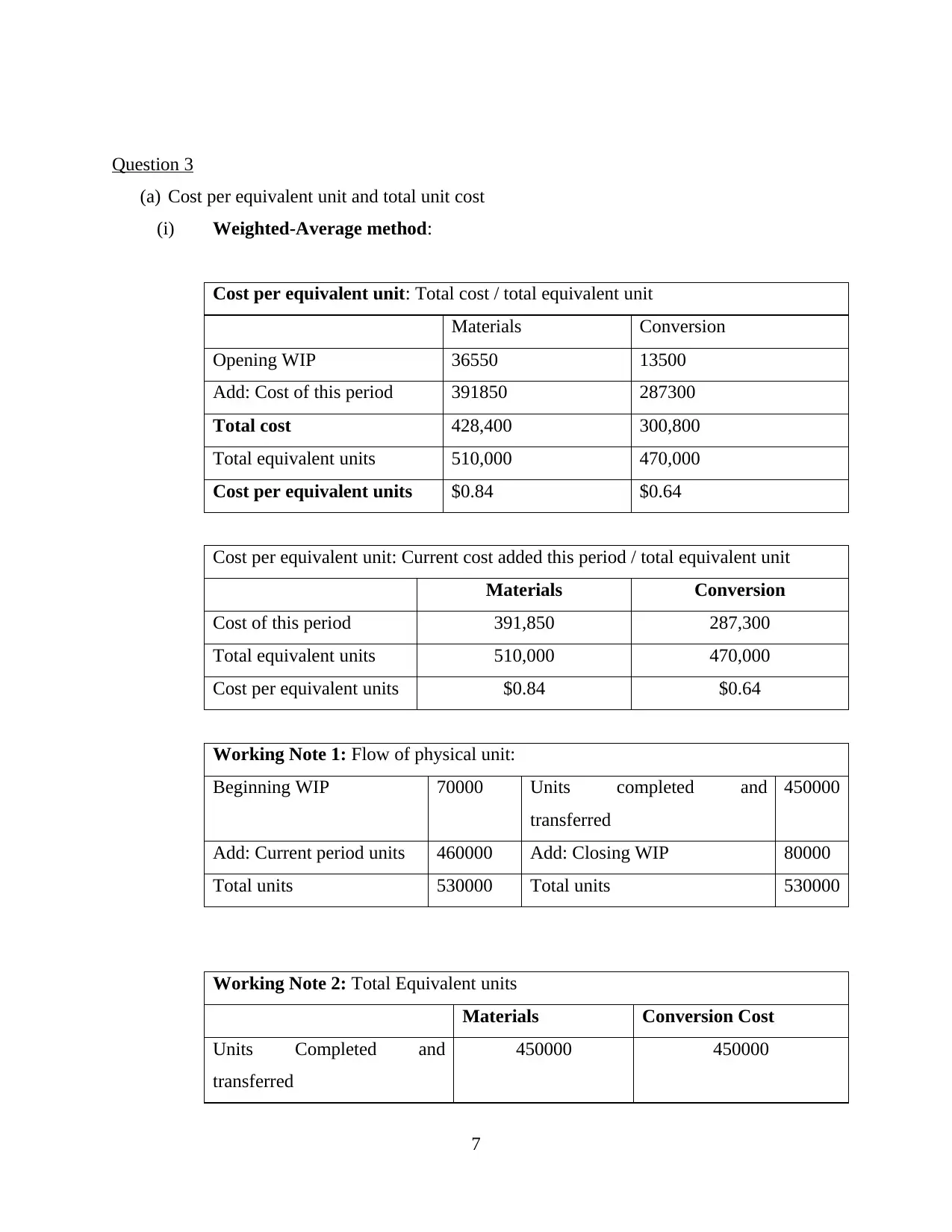

Question 3

(a) Cost per equivalent unit and total unit cost

(i) Weighted-Average method:

Cost per equivalent unit: Total cost / total equivalent unit

Materials Conversion

Opening WIP 36550 13500

Add: Cost of this period 391850 287300

Total cost 428,400 300,800

Total equivalent units 510,000 470,000

Cost per equivalent units $0.84 $0.64

Cost per equivalent unit: Current cost added this period / total equivalent unit

Materials Conversion

Cost of this period 391,850 287,300

Total equivalent units 510,000 470,000

Cost per equivalent units $0.84 $0.64

Working Note 1: Flow of physical unit:

Beginning WIP 70000 Units completed and

transferred

450000

Add: Current period units 460000 Add: Closing WIP 80000

Total units 530000 Total units 530000

Working Note 2: Total Equivalent units

Materials Conversion Cost

Units Completed and

transferred

450000 450000

7

(a) Cost per equivalent unit and total unit cost

(i) Weighted-Average method:

Cost per equivalent unit: Total cost / total equivalent unit

Materials Conversion

Opening WIP 36550 13500

Add: Cost of this period 391850 287300

Total cost 428,400 300,800

Total equivalent units 510,000 470,000

Cost per equivalent units $0.84 $0.64

Cost per equivalent unit: Current cost added this period / total equivalent unit

Materials Conversion

Cost of this period 391,850 287,300

Total equivalent units 510,000 470,000

Cost per equivalent units $0.84 $0.64

Working Note 1: Flow of physical unit:

Beginning WIP 70000 Units completed and

transferred

450000

Add: Current period units 460000 Add: Closing WIP 80000

Total units 530000 Total units 530000

Working Note 2: Total Equivalent units

Materials Conversion Cost

Units Completed and

transferred

450000 450000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

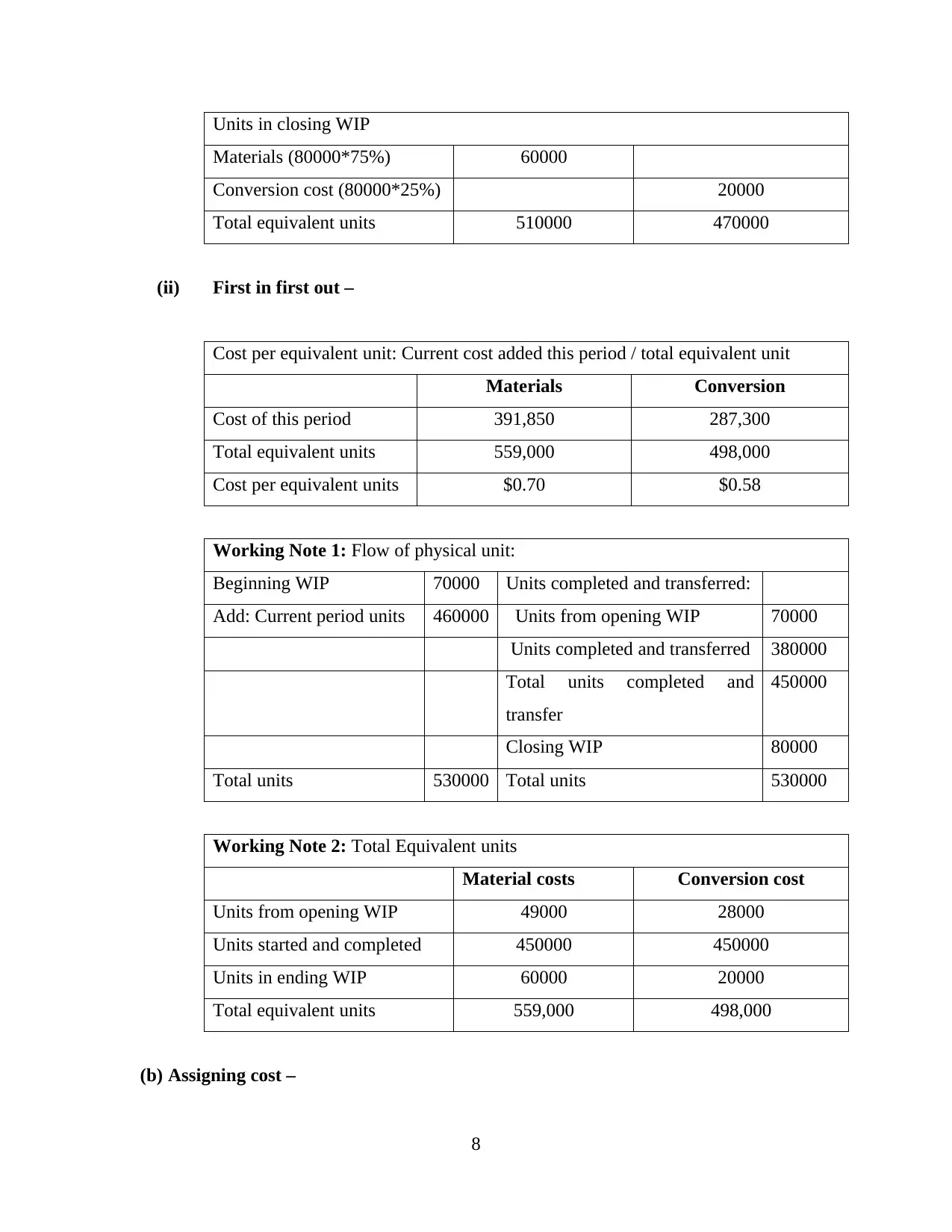

Units in closing WIP

Materials (80000*75%) 60000

Conversion cost (80000*25%) 20000

Total equivalent units 510000 470000

(ii) First in first out –

Cost per equivalent unit: Current cost added this period / total equivalent unit

Materials Conversion

Cost of this period 391,850 287,300

Total equivalent units 559,000 498,000

Cost per equivalent units $0.70 $0.58

Working Note 1: Flow of physical unit:

Beginning WIP 70000 Units completed and transferred:

Add: Current period units 460000 Units from opening WIP 70000

Units completed and transferred 380000

Total units completed and

transfer

450000

Closing WIP 80000

Total units 530000 Total units 530000

Working Note 2: Total Equivalent units

Material costs Conversion cost

Units from opening WIP 49000 28000

Units started and completed 450000 450000

Units in ending WIP 60000 20000

Total equivalent units 559,000 498,000

(b) Assigning cost –

8

Materials (80000*75%) 60000

Conversion cost (80000*25%) 20000

Total equivalent units 510000 470000

(ii) First in first out –

Cost per equivalent unit: Current cost added this period / total equivalent unit

Materials Conversion

Cost of this period 391,850 287,300

Total equivalent units 559,000 498,000

Cost per equivalent units $0.70 $0.58

Working Note 1: Flow of physical unit:

Beginning WIP 70000 Units completed and transferred:

Add: Current period units 460000 Units from opening WIP 70000

Units completed and transferred 380000

Total units completed and

transfer

450000

Closing WIP 80000

Total units 530000 Total units 530000

Working Note 2: Total Equivalent units

Material costs Conversion cost

Units from opening WIP 49000 28000

Units started and completed 450000 450000

Units in ending WIP 60000 20000

Total equivalent units 559,000 498,000

(b) Assigning cost –

8

(i) Since, no information was provided about the method to be used, total cost

assigned has been under weighted Average Method:

Cost assigned to units completed and transferred

Direct Material (450000*$0.84) 378,000

Conversion (450000*$0.64) 288,000

Total cost assigned to completed units 666,000

Cost assigned to closing WIP

Direct materials (60000*$0.84) 50400

Conversion (20000*$0.64) 12800

Total cost assigned to closing WIP 63200

Question 4

(a) Break Even point in units: Fixed cost/ contribution per unit

Sales of three are in ratio of 1:4:2.

Hence, contribution margin of bundle = (1*5) + (4*4) + (2*3) = 5 + 16 + 6 = $27

Breakeven point of bundle = 35,100/27 = 1300

Breakeven point in units:

PC case = 1300*1 = 1300

S Case = 1300*4 = 5200

TPU Case = 1300*2 = 2600

Total number of units for breakeven = 9100 units

Working Note:

Fixed Cost = $35,100

Contribution per unit = Sales price per unit – Variable cost per unit

PC Case S Case TPU Case

Sales price per unit 50 65 90

Variable cost per unit 45 61 87

Contribution 5 4 3

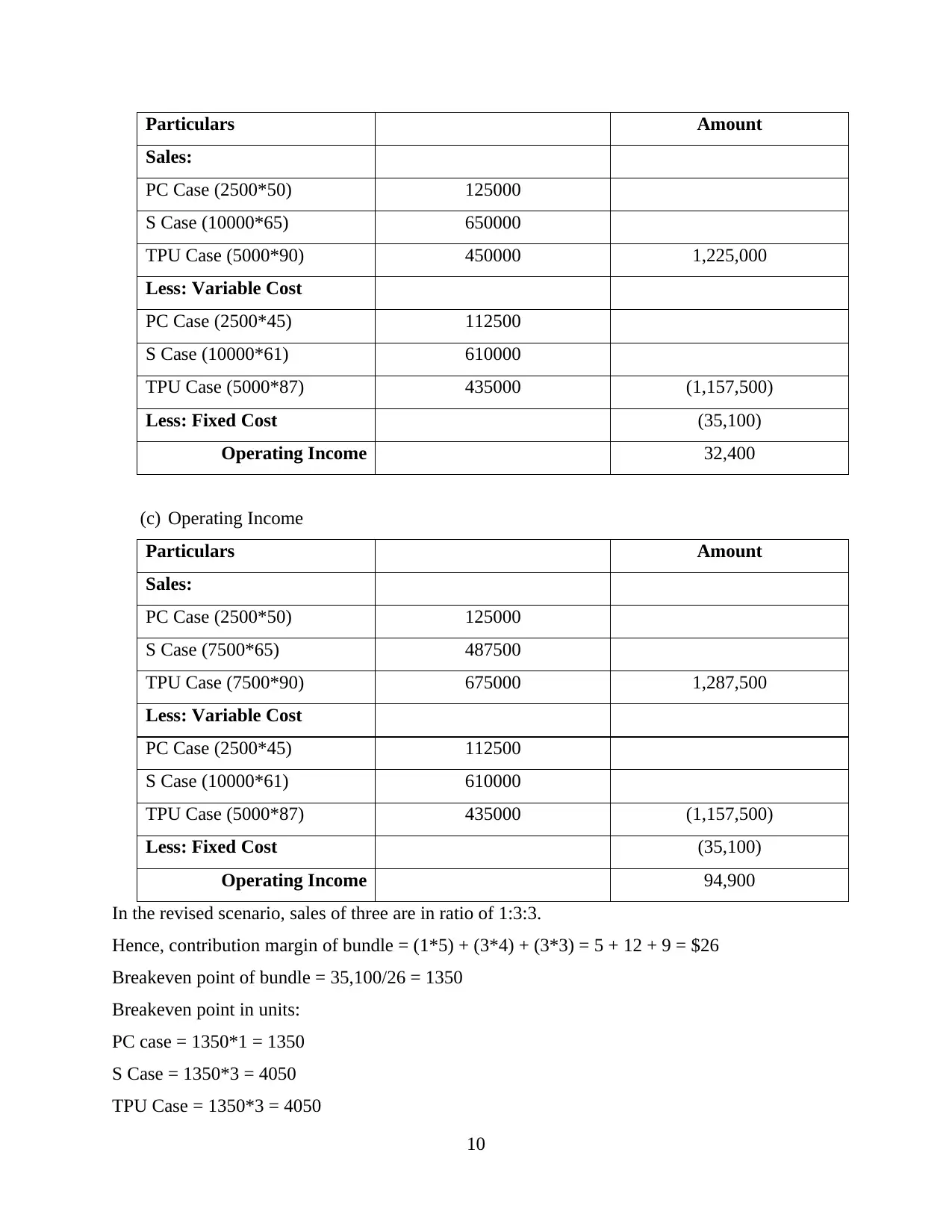

(b) Operating Income –

9

assigned has been under weighted Average Method:

Cost assigned to units completed and transferred

Direct Material (450000*$0.84) 378,000

Conversion (450000*$0.64) 288,000

Total cost assigned to completed units 666,000

Cost assigned to closing WIP

Direct materials (60000*$0.84) 50400

Conversion (20000*$0.64) 12800

Total cost assigned to closing WIP 63200

Question 4

(a) Break Even point in units: Fixed cost/ contribution per unit

Sales of three are in ratio of 1:4:2.

Hence, contribution margin of bundle = (1*5) + (4*4) + (2*3) = 5 + 16 + 6 = $27

Breakeven point of bundle = 35,100/27 = 1300

Breakeven point in units:

PC case = 1300*1 = 1300

S Case = 1300*4 = 5200

TPU Case = 1300*2 = 2600

Total number of units for breakeven = 9100 units

Working Note:

Fixed Cost = $35,100

Contribution per unit = Sales price per unit – Variable cost per unit

PC Case S Case TPU Case

Sales price per unit 50 65 90

Variable cost per unit 45 61 87

Contribution 5 4 3

(b) Operating Income –

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount

Sales:

PC Case (2500*50) 125000

S Case (10000*65) 650000

TPU Case (5000*90) 450000 1,225,000

Less: Variable Cost

PC Case (2500*45) 112500

S Case (10000*61) 610000

TPU Case (5000*87) 435000 (1,157,500)

Less: Fixed Cost (35,100)

Operating Income 32,400

(c) Operating Income

Particulars Amount

Sales:

PC Case (2500*50) 125000

S Case (7500*65) 487500

TPU Case (7500*90) 675000 1,287,500

Less: Variable Cost

PC Case (2500*45) 112500

S Case (10000*61) 610000

TPU Case (5000*87) 435000 (1,157,500)

Less: Fixed Cost (35,100)

Operating Income 94,900

In the revised scenario, sales of three are in ratio of 1:3:3.

Hence, contribution margin of bundle = (1*5) + (3*4) + (3*3) = 5 + 12 + 9 = $26

Breakeven point of bundle = 35,100/26 = 1350

Breakeven point in units:

PC case = 1350*1 = 1350

S Case = 1350*3 = 4050

TPU Case = 1350*3 = 4050

10

Sales:

PC Case (2500*50) 125000

S Case (10000*65) 650000

TPU Case (5000*90) 450000 1,225,000

Less: Variable Cost

PC Case (2500*45) 112500

S Case (10000*61) 610000

TPU Case (5000*87) 435000 (1,157,500)

Less: Fixed Cost (35,100)

Operating Income 32,400

(c) Operating Income

Particulars Amount

Sales:

PC Case (2500*50) 125000

S Case (7500*65) 487500

TPU Case (7500*90) 675000 1,287,500

Less: Variable Cost

PC Case (2500*45) 112500

S Case (10000*61) 610000

TPU Case (5000*87) 435000 (1,157,500)

Less: Fixed Cost (35,100)

Operating Income 94,900

In the revised scenario, sales of three are in ratio of 1:3:3.

Hence, contribution margin of bundle = (1*5) + (3*4) + (3*3) = 5 + 12 + 9 = $26

Breakeven point of bundle = 35,100/26 = 1350

Breakeven point in units:

PC case = 1350*1 = 1350

S Case = 1350*3 = 4050

TPU Case = 1350*3 = 4050

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total number of units for breakeven = 9450 units

(d) No, it is not always better to choose the sales mix that yields the lower break-even point

because the above situation has ignored many aspects like demand for the product. The

company shall focus on maximising its sales of all three products and resultingly,

improving its operating income, even if it happens with sales mix with a higher

breakeven point (Batkovskiy and et.al., 2017).

Question 5

(a) In the given problem, a scenario is presented in which there is a slowdown in logistics

and supply chain process due to pandemic lockdown. CFO of the company is preparing

a master budget and has asked for sales estimates from manager of sales department,

Mr. John. Mr. John knows that due to pandemic not only supply slumps but also,

demand falls. He must have revised figures of demands of the company’s products for

current year. He can face a dilemma over estimating next year’s sales figure

considering uncertain market situation as well as he can have a dilemma over

deliberately reducing the demand figures considering the company’s policy that if

actual sales exceed budgeted sales, sales managers are rewarded. He has to choose

between his personal profit for a short term or cheating company which might result in

obstructing company’s operations in long run.

(b) If John chooses to behave unethically, CFO will end making up an incorrect budget. As

a consequence, there are two possibilities: first, demand actually shows up at lower

side and second, if actual demand exceeds the estimated and he gets rewarded,

company will suffer additional cost of bonus which is not actually due. Also, if demand

estimates are highly deflated, company might increase promotional efforts like offering

more discounts, which might be in favour of customers but not in the favour of the

company. All this will put additional stress on the company in the times when already

it is facing extra pressure from elongated supply chain and reduced demand (Weimer

and Vining, 2017).

11

(d) No, it is not always better to choose the sales mix that yields the lower break-even point

because the above situation has ignored many aspects like demand for the product. The

company shall focus on maximising its sales of all three products and resultingly,

improving its operating income, even if it happens with sales mix with a higher

breakeven point (Batkovskiy and et.al., 2017).

Question 5

(a) In the given problem, a scenario is presented in which there is a slowdown in logistics

and supply chain process due to pandemic lockdown. CFO of the company is preparing

a master budget and has asked for sales estimates from manager of sales department,

Mr. John. Mr. John knows that due to pandemic not only supply slumps but also,

demand falls. He must have revised figures of demands of the company’s products for

current year. He can face a dilemma over estimating next year’s sales figure

considering uncertain market situation as well as he can have a dilemma over

deliberately reducing the demand figures considering the company’s policy that if

actual sales exceed budgeted sales, sales managers are rewarded. He has to choose

between his personal profit for a short term or cheating company which might result in

obstructing company’s operations in long run.

(b) If John chooses to behave unethically, CFO will end making up an incorrect budget. As

a consequence, there are two possibilities: first, demand actually shows up at lower

side and second, if actual demand exceeds the estimated and he gets rewarded,

company will suffer additional cost of bonus which is not actually due. Also, if demand

estimates are highly deflated, company might increase promotional efforts like offering

more discounts, which might be in favour of customers but not in the favour of the

company. All this will put additional stress on the company in the times when already

it is facing extra pressure from elongated supply chain and reduced demand (Weimer

and Vining, 2017).

11

Conclusion

From the above report, this can be concluded that cost accounting is one of the integral parts

of management accounting. It is used by different managers in different methods to find out

various results required. For example, in the above report, it can be concluded that reciprocal

method is most preferred method of cost allocation in job costing while also, realising that it is

not necessary to choose sales mix with lower break-even point.

12

From the above report, this can be concluded that cost accounting is one of the integral parts

of management accounting. It is used by different managers in different methods to find out

various results required. For example, in the above report, it can be concluded that reciprocal

method is most preferred method of cost allocation in job costing while also, realising that it is

not necessary to choose sales mix with lower break-even point.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.