Excite Entertainment Ltd: Management Accounting Report

VerifiedAdded on 2023/01/19

|14

|5043

|73

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on Excite Entertainment Ltd. It begins by defining management accounting and its essential requirements, contrasting it with financial accounting. The report then delves into various management accounting systems, including cost accounting, inventory management (LIFO, FIFO), job costing, and price optimization systems. It explores different reporting methods such as budget, cost, execution, and inventory reports. The study further examines cost calculation techniques using absorption and marginal costing, along with an analysis of planning tools for monetary control. Finally, the report discusses how companies adapt management accounting systems to address financial issues, providing a well-rounded overview of the subject matter.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P1 Management accounting and essential requirements of different management accounting

systems.........................................................................................................................................3

P2 Different methods used for management accounting reporting.............................................5

P3 Calculation cost using absorption and marginal cost method................................................7

LO 3.................................................................................................................................................8

P4 Diverse types of planning tools used for monetary control..........................................8

LO 4...............................................................................................................................................10

Management accounting systems adapt by Excite entertainment Ltd...........................10

CONCLUSION.............................................................................................................................12

REFERENCES............................................................................................................................13

2

INTRODUCTION...........................................................................................................................3

P1 Management accounting and essential requirements of different management accounting

systems.........................................................................................................................................3

P2 Different methods used for management accounting reporting.............................................5

P3 Calculation cost using absorption and marginal cost method................................................7

LO 3.................................................................................................................................................8

P4 Diverse types of planning tools used for monetary control..........................................8

LO 4...............................................................................................................................................10

Management accounting systems adapt by Excite entertainment Ltd...........................10

CONCLUSION.............................................................................................................................12

REFERENCES............................................................................................................................13

2

INTRODUCTION

Management accounting defined as procedure of providing financial resources

and information to company manager in decision taking. It is only used by internal team

of company, and this is the best thing that makes it unique from financial accounting. In

this procedure, info about financial budget and reports such as invoice, monetary

balance statement is transferred by finance administration with organization

management team. Management accounting objective is to use statistical data and take

the accurate and better decision, business activities, controlling enterprise and business

development. In other words, this is the profession that add incorporation of non-

financial and financial statements to cater effective info to management so that

department take appropriate decision for company well fare. The present report is

based on Excite Entertainment Ltd; they provide variety of content including weather

and news, a web-based email and a metasearch engine. It explains management

accounting, requirement of various types of MA systems and various methods used for

MA reporting. It justifies correct techniques of cost analysis to made an income

statement using absorption and marginal costs. Furthermore, this study clarifies benefits

and disadvantages of several types of planning tools used for monetary control. It

explains ways used by companies for adapting management accounting systems to

reply to financial issues.

P1 Management accounting and essential requirements of different management accounting

systems

In current time period business firms are facing competition on number of fronts

and it become difficult for them to compete with them. Firms do lot of research and

identify areas where they need to work in order to solve their business problem. Cost is

one of the main focus area where most of the business firms pay due attention in order

to control cost of production and operations. There are number of approaches that are

used by the firms to control. Important point to note is that in order to control cost it is

very important to identify areas from where higher amount of cost is generated. In this

regard, big data system is developed by the firms specially those working in

manufacturing industry. These firms adopt management accounting system under which

in specific manner cost of production is computed and then analyzed. Number of

techniques like variance analysis and budgeting are used to find out whether firm

successfully control its production cost or there is need to take specific action to handle

situation (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil, 2015). Most commonly in

case of few expenses actual value surpassed projected value and in that case negative

variance comes in existence. Varied sort of management accounting systems are

3

Management accounting defined as procedure of providing financial resources

and information to company manager in decision taking. It is only used by internal team

of company, and this is the best thing that makes it unique from financial accounting. In

this procedure, info about financial budget and reports such as invoice, monetary

balance statement is transferred by finance administration with organization

management team. Management accounting objective is to use statistical data and take

the accurate and better decision, business activities, controlling enterprise and business

development. In other words, this is the profession that add incorporation of non-

financial and financial statements to cater effective info to management so that

department take appropriate decision for company well fare. The present report is

based on Excite Entertainment Ltd; they provide variety of content including weather

and news, a web-based email and a metasearch engine. It explains management

accounting, requirement of various types of MA systems and various methods used for

MA reporting. It justifies correct techniques of cost analysis to made an income

statement using absorption and marginal costs. Furthermore, this study clarifies benefits

and disadvantages of several types of planning tools used for monetary control. It

explains ways used by companies for adapting management accounting systems to

reply to financial issues.

P1 Management accounting and essential requirements of different management accounting

systems

In current time period business firms are facing competition on number of fronts

and it become difficult for them to compete with them. Firms do lot of research and

identify areas where they need to work in order to solve their business problem. Cost is

one of the main focus area where most of the business firms pay due attention in order

to control cost of production and operations. There are number of approaches that are

used by the firms to control. Important point to note is that in order to control cost it is

very important to identify areas from where higher amount of cost is generated. In this

regard, big data system is developed by the firms specially those working in

manufacturing industry. These firms adopt management accounting system under which

in specific manner cost of production is computed and then analyzed. Number of

techniques like variance analysis and budgeting are used to find out whether firm

successfully control its production cost or there is need to take specific action to handle

situation (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil, 2015). Most commonly in

case of few expenses actual value surpassed projected value and in that case negative

variance comes in existence. Varied sort of management accounting systems are

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

explained below.

Cost accounting system: Cost accounting system is one of the common

management accounting system that is used by the business firms. Under this

system entire product costing is done altogether. Specifically this accounting

system is not used by the firms that are producing multiple products. Opposite to

this it can be said that cost accounting system is used by the firms that have

single product. This system cannot be used for the multiple products because in

this there is not a provision to do accounting for each product individually. If firm

produce multiple products and cost accounting system is used then in that case it

cannot obtain information about overall cost of each product line individually. This

is one of the major limitations of the cost accounting system. Main importance of

cost accounting system is that by using cost accounting system for single product

manager can identify expenses whose value is high and over expenses made. In

cost accounting system entire database is maintained and due to this reason by

comparing current value with past one business firm easily identify area where

extravagance is made. By taking corrective actions situation is handle and it is

ensured that in future time period expenses will remain in control at facility.

Inventory management system: Inventory management system is the one of

the main system under which entire data related to the inventory is saved by the

business firms. Firms operating in manufacturing sector usually place an order

to purchase a raw material. They need data to make decisions about quantity of

raw material that must be purchased and time on which order must be placed to

purchase an order (Wouters and Kirchberger, 2015). Thus, it can be said that

inventory management system has huge benefit for the business firms because

by using it firm managers can determine time by which order must be placed so

that unused inventory does not remain in the warehouse. Important point to note

is that in inventory every year higher amount of money get stuck because

sometimes due to interruption in production process inventory remain unused at

workforce. In such situation heavy loss is faced by the firms. Use of inventory

management system ensured that everything will be fine and according to

requirement order will be placed. All these things lead to cost saving in the

business. Best techniques of inventory management that are used by the firm are

given below.

LIFO: Under LIFO units that are produced recently are sold first and those who

were produced earlier are sold later. Now some days many firms are using this

approach because USA income tax rules permit firms to do so. This approach is

4

Cost accounting system: Cost accounting system is one of the common

management accounting system that is used by the business firms. Under this

system entire product costing is done altogether. Specifically this accounting

system is not used by the firms that are producing multiple products. Opposite to

this it can be said that cost accounting system is used by the firms that have

single product. This system cannot be used for the multiple products because in

this there is not a provision to do accounting for each product individually. If firm

produce multiple products and cost accounting system is used then in that case it

cannot obtain information about overall cost of each product line individually. This

is one of the major limitations of the cost accounting system. Main importance of

cost accounting system is that by using cost accounting system for single product

manager can identify expenses whose value is high and over expenses made. In

cost accounting system entire database is maintained and due to this reason by

comparing current value with past one business firm easily identify area where

extravagance is made. By taking corrective actions situation is handle and it is

ensured that in future time period expenses will remain in control at facility.

Inventory management system: Inventory management system is the one of

the main system under which entire data related to the inventory is saved by the

business firms. Firms operating in manufacturing sector usually place an order

to purchase a raw material. They need data to make decisions about quantity of

raw material that must be purchased and time on which order must be placed to

purchase an order (Wouters and Kirchberger, 2015). Thus, it can be said that

inventory management system has huge benefit for the business firms because

by using it firm managers can determine time by which order must be placed so

that unused inventory does not remain in the warehouse. Important point to note

is that in inventory every year higher amount of money get stuck because

sometimes due to interruption in production process inventory remain unused at

workforce. In such situation heavy loss is faced by the firms. Use of inventory

management system ensured that everything will be fine and according to

requirement order will be placed. All these things lead to cost saving in the

business. Best techniques of inventory management that are used by the firm are

given below.

LIFO: Under LIFO units that are produced recently are sold first and those who

were produced earlier are sold later. Now some days many firms are using this

approach because USA income tax rules permit firms to do so. This approach is

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

used to move cost from inventory to COGS. It can be said that LIFO help a lot to

firms to manage inventory at workplace.

FIFO: In FIFO items that are produced first are sold in the market as soon as

possible. This approach is just inverse of LIFO. This method is used by those

firms that prepare and sale perishable goods.

Job costing system: It is another accounting system that is widely used by the

business firms. This accounting system is used when firm have multiple product

lines. Most of business firms are always interested in knowing which product line

is profitable for them. Hence, business firms use job costing system, as under

this system for each product line cost is computed individually. Thus, a business

firm comes to know that which product is generating better and worst results.

Time to time analysis of data is done and on that basis area where action need to

be taken are identified. In this way in better way cost is controlled at the

workplace (Pavlatos, 2015). Job cost system is adopted now some days by most

of large size business firms because it assists them to analyze cost at granular

level which ultimately lead to making better decisions at the workplace. This is

one of the major benefit of job costing system. Business firms maintain entire

database where record of long time period is maintained. Analysis of data reflect

history of performance which ultimately help managers in identifying trends that

persist in past time period. Consistent origination of same trend reflect a lot about

a problem and indicate manager that there is need to take immediate action to

handle situation.

Price optimization system: In today era cost is one of the major focal point

of the business firms. Now days most of companies are focusing on

optimizing their product price. In this regard number of approaches is used

by the business firms like linear programming etc. By using these

approaches best allocation of resources is done among products and cost

is controlled in proper manner. Thus, it can be said that there is huge

significance of the price optimization system for the business firms. It not

only helps them to control cost of production but also assist them to make

best use of available resources (Bobryshev and et.al., 2015). Firms

according to their requirement use varied price optimization system. Every

business firm has experts that have knowledge of the specific tools.

Because of this reason in few firms linear programming is used and in

other firms other methods are used. It can be said that scope of price

optimization system is wide.

5

firms to manage inventory at workplace.

FIFO: In FIFO items that are produced first are sold in the market as soon as

possible. This approach is just inverse of LIFO. This method is used by those

firms that prepare and sale perishable goods.

Job costing system: It is another accounting system that is widely used by the

business firms. This accounting system is used when firm have multiple product

lines. Most of business firms are always interested in knowing which product line

is profitable for them. Hence, business firms use job costing system, as under

this system for each product line cost is computed individually. Thus, a business

firm comes to know that which product is generating better and worst results.

Time to time analysis of data is done and on that basis area where action need to

be taken are identified. In this way in better way cost is controlled at the

workplace (Pavlatos, 2015). Job cost system is adopted now some days by most

of large size business firms because it assists them to analyze cost at granular

level which ultimately lead to making better decisions at the workplace. This is

one of the major benefit of job costing system. Business firms maintain entire

database where record of long time period is maintained. Analysis of data reflect

history of performance which ultimately help managers in identifying trends that

persist in past time period. Consistent origination of same trend reflect a lot about

a problem and indicate manager that there is need to take immediate action to

handle situation.

Price optimization system: In today era cost is one of the major focal point

of the business firms. Now days most of companies are focusing on

optimizing their product price. In this regard number of approaches is used

by the business firms like linear programming etc. By using these

approaches best allocation of resources is done among products and cost

is controlled in proper manner. Thus, it can be said that there is huge

significance of the price optimization system for the business firms. It not

only helps them to control cost of production but also assist them to make

best use of available resources (Bobryshev and et.al., 2015). Firms

according to their requirement use varied price optimization system. Every

business firm has experts that have knowledge of the specific tools.

Because of this reason in few firms linear programming is used and in

other firms other methods are used. It can be said that scope of price

optimization system is wide.

5

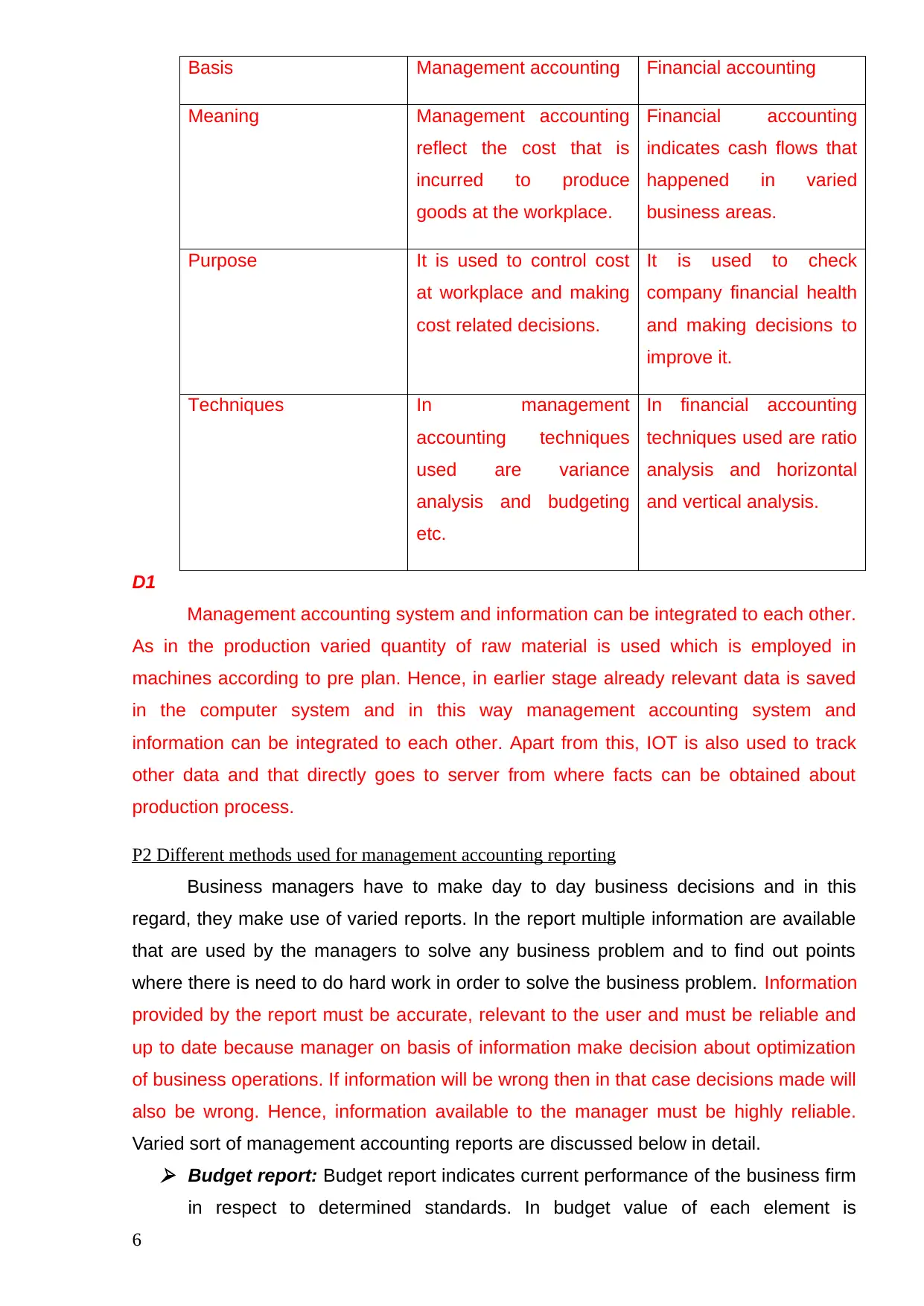

Basis Management accounting Financial accounting

Meaning Management accounting

reflect the cost that is

incurred to produce

goods at the workplace.

Financial accounting

indicates cash flows that

happened in varied

business areas.

Purpose It is used to control cost

at workplace and making

cost related decisions.

It is used to check

company financial health

and making decisions to

improve it.

Techniques In management

accounting techniques

used are variance

analysis and budgeting

etc.

In financial accounting

techniques used are ratio

analysis and horizontal

and vertical analysis.

D1

Management accounting system and information can be integrated to each other.

As in the production varied quantity of raw material is used which is employed in

machines according to pre plan. Hence, in earlier stage already relevant data is saved

in the computer system and in this way management accounting system and

information can be integrated to each other. Apart from this, IOT is also used to track

other data and that directly goes to server from where facts can be obtained about

production process.

P2 Different methods used for management accounting reporting

Business managers have to make day to day business decisions and in this

regard, they make use of varied reports. In the report multiple information are available

that are used by the managers to solve any business problem and to find out points

where there is need to do hard work in order to solve the business problem. Information

provided by the report must be accurate, relevant to the user and must be reliable and

up to date because manager on basis of information make decision about optimization

of business operations. If information will be wrong then in that case decisions made will

also be wrong. Hence, information available to the manager must be highly reliable.

Varied sort of management accounting reports are discussed below in detail.

Budget report: Budget report indicates current performance of the business firm

in respect to determined standards. In budget value of each element is

6

Meaning Management accounting

reflect the cost that is

incurred to produce

goods at the workplace.

Financial accounting

indicates cash flows that

happened in varied

business areas.

Purpose It is used to control cost

at workplace and making

cost related decisions.

It is used to check

company financial health

and making decisions to

improve it.

Techniques In management

accounting techniques

used are variance

analysis and budgeting

etc.

In financial accounting

techniques used are ratio

analysis and horizontal

and vertical analysis.

D1

Management accounting system and information can be integrated to each other.

As in the production varied quantity of raw material is used which is employed in

machines according to pre plan. Hence, in earlier stage already relevant data is saved

in the computer system and in this way management accounting system and

information can be integrated to each other. Apart from this, IOT is also used to track

other data and that directly goes to server from where facts can be obtained about

production process.

P2 Different methods used for management accounting reporting

Business managers have to make day to day business decisions and in this

regard, they make use of varied reports. In the report multiple information are available

that are used by the managers to solve any business problem and to find out points

where there is need to do hard work in order to solve the business problem. Information

provided by the report must be accurate, relevant to the user and must be reliable and

up to date because manager on basis of information make decision about optimization

of business operations. If information will be wrong then in that case decisions made will

also be wrong. Hence, information available to the manager must be highly reliable.

Varied sort of management accounting reports are discussed below in detail.

Budget report: Budget report indicates current performance of the business firm

in respect to determined standards. In budget value of each element is

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determined and within that performance need to be made in order to control cost

of the production in the business. Budgets are prepared in respect to production,

sales and marketing etc. Time to time actual performance is compared with the

budget performance and variance is identified. If variance is negative then in that

case steps are taken to handle situation.

Cost report: In this report expenses are recorded in respect to varied business

operations and points where cost suddenly rise and decline are identified. If

trends are normal then management does not make change in its strategy.

Opposite to this, If it is identified that results will be opposite to the expectation

then in that case changes are made to course of action to handle current

situation.

Execution report: It is prepared when firm operate specific project. Under the

project multiple activities are performed together and their completion time period

is also determined. In case firm failed to complete activities on time cost increase

sharply. Thus, execution report is prepared time to time because it reflects

percentage of task that completed and percentage that remain to be performed.

If it is identified that more time will be required to perform task then in that case

additional resources are used to finish that task on time (Collis and Hussey,

2017). In this cost elevation is controlled to some extent which ultimately lead to

increase in business profit.

Inventory report: It is the report where information about inventory use and

quantity stored in the warehouse is available. In the inventory report data related

to previous months is also available. Manager by comparing current performance

with previous one identified whether performance is good or bad and accordingly

take step to handle situation.

Manufacturing report: It is the report in which record related to number of units

produced within specific time period is available. Like inventory report in

manufacturing report also record is available about number of units produced in

earlier months. Thus, manager easily obtains information about progress made

towards target.

Job costing report: In the job cost report cost of each of product line is given

and along with this cost classification in varied expenses is also given. By

analyzing elements of overall cost managers come to know about item where

heavy expenses are made. Manager evaluate that item previous month expense

to identify whether extravagance made or value of expense is in control

7

of the production in the business. Budgets are prepared in respect to production,

sales and marketing etc. Time to time actual performance is compared with the

budget performance and variance is identified. If variance is negative then in that

case steps are taken to handle situation.

Cost report: In this report expenses are recorded in respect to varied business

operations and points where cost suddenly rise and decline are identified. If

trends are normal then management does not make change in its strategy.

Opposite to this, If it is identified that results will be opposite to the expectation

then in that case changes are made to course of action to handle current

situation.

Execution report: It is prepared when firm operate specific project. Under the

project multiple activities are performed together and their completion time period

is also determined. In case firm failed to complete activities on time cost increase

sharply. Thus, execution report is prepared time to time because it reflects

percentage of task that completed and percentage that remain to be performed.

If it is identified that more time will be required to perform task then in that case

additional resources are used to finish that task on time (Collis and Hussey,

2017). In this cost elevation is controlled to some extent which ultimately lead to

increase in business profit.

Inventory report: It is the report where information about inventory use and

quantity stored in the warehouse is available. In the inventory report data related

to previous months is also available. Manager by comparing current performance

with previous one identified whether performance is good or bad and accordingly

take step to handle situation.

Manufacturing report: It is the report in which record related to number of units

produced within specific time period is available. Like inventory report in

manufacturing report also record is available about number of units produced in

earlier months. Thus, manager easily obtains information about progress made

towards target.

Job costing report: In the job cost report cost of each of product line is given

and along with this cost classification in varied expenses is also given. By

analyzing elements of overall cost managers come to know about item where

heavy expenses are made. Manager evaluate that item previous month expense

to identify whether extravagance made or value of expense is in control

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance report: Performance report reflects overall performance of the

business firm. In the report varied issues related to business firm are explained in

detail. These issues are taken in to account in order to determine future course

of action (Armitage, Webb and Glynn, 2016).

Account receivable report: Account receivable report reflects status of varied

account receivables. In the report information about amount need to be received

is given and along with this, duration for which account receivable is allowed is

also given. Those receivables which must be received till the date but not

received are also given in the account receivable report. Thus, this report assist

managers in maintain current asset to some extent.

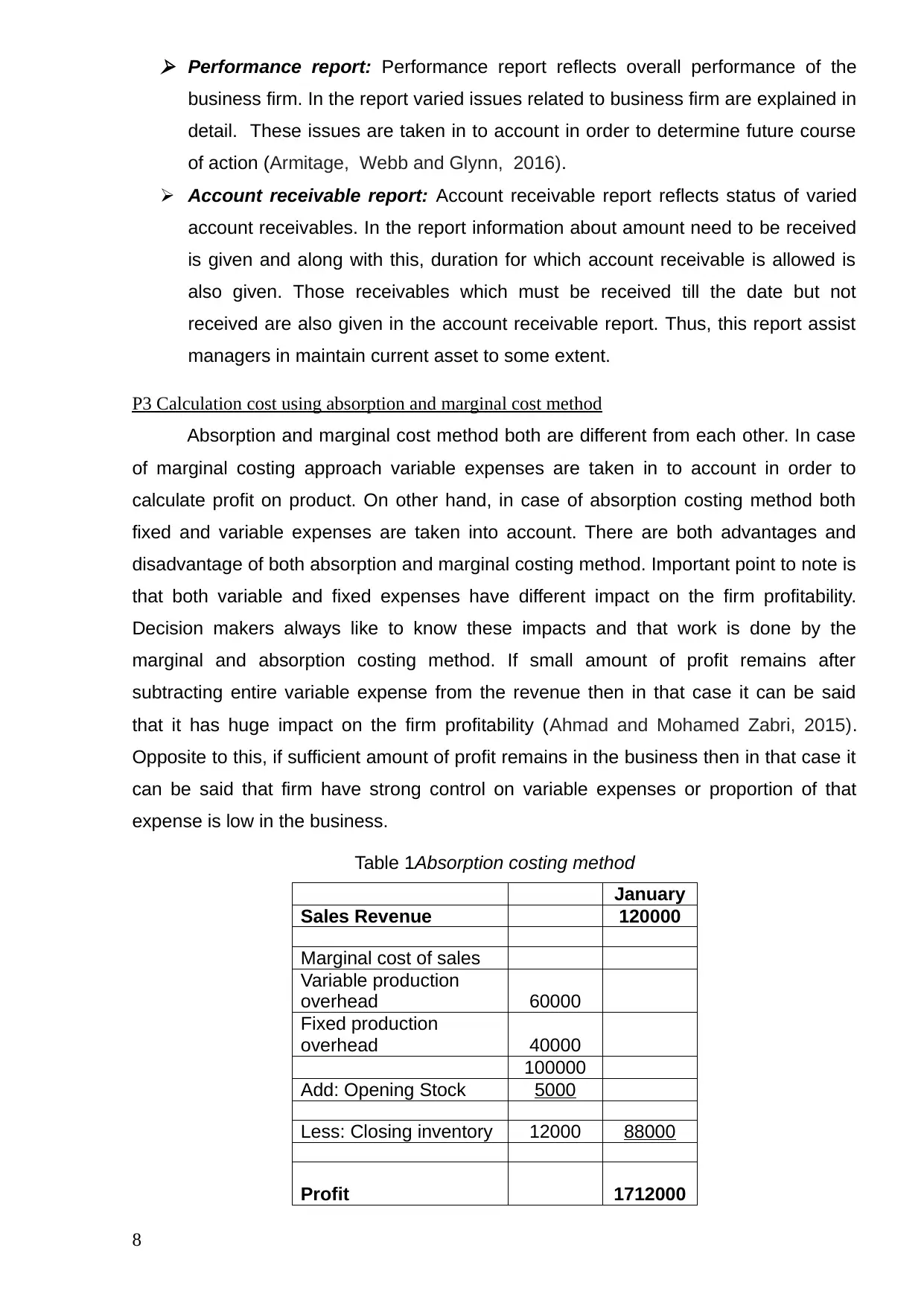

P3 Calculation cost using absorption and marginal cost method

Absorption and marginal cost method both are different from each other. In case

of marginal costing approach variable expenses are taken in to account in order to

calculate profit on product. On other hand, in case of absorption costing method both

fixed and variable expenses are taken into account. There are both advantages and

disadvantage of both absorption and marginal costing method. Important point to note is

that both variable and fixed expenses have different impact on the firm profitability.

Decision makers always like to know these impacts and that work is done by the

marginal and absorption costing method. If small amount of profit remains after

subtracting entire variable expense from the revenue then in that case it can be said

that it has huge impact on the firm profitability (Ahmad and Mohamed Zabri, 2015).

Opposite to this, if sufficient amount of profit remains in the business then in that case it

can be said that firm have strong control on variable expenses or proportion of that

expense is low in the business.

Table 1Absorption costing method

January

Sales Revenue 120000

Marginal cost of sales

Variable production

overhead 60000

Fixed production

overhead 40000

100000

Add: Opening Stock 5000

Less: Closing inventory 12000 88000

Profit 1712000

8

business firm. In the report varied issues related to business firm are explained in

detail. These issues are taken in to account in order to determine future course

of action (Armitage, Webb and Glynn, 2016).

Account receivable report: Account receivable report reflects status of varied

account receivables. In the report information about amount need to be received

is given and along with this, duration for which account receivable is allowed is

also given. Those receivables which must be received till the date but not

received are also given in the account receivable report. Thus, this report assist

managers in maintain current asset to some extent.

P3 Calculation cost using absorption and marginal cost method

Absorption and marginal cost method both are different from each other. In case

of marginal costing approach variable expenses are taken in to account in order to

calculate profit on product. On other hand, in case of absorption costing method both

fixed and variable expenses are taken into account. There are both advantages and

disadvantage of both absorption and marginal costing method. Important point to note is

that both variable and fixed expenses have different impact on the firm profitability.

Decision makers always like to know these impacts and that work is done by the

marginal and absorption costing method. If small amount of profit remains after

subtracting entire variable expense from the revenue then in that case it can be said

that it has huge impact on the firm profitability (Ahmad and Mohamed Zabri, 2015).

Opposite to this, if sufficient amount of profit remains in the business then in that case it

can be said that firm have strong control on variable expenses or proportion of that

expense is low in the business.

Table 1Absorption costing method

January

Sales Revenue 120000

Marginal cost of sales

Variable production

overhead 60000

Fixed production

overhead 40000

100000

Add: Opening Stock 5000

Less: Closing inventory 12000 88000

Profit 1712000

8

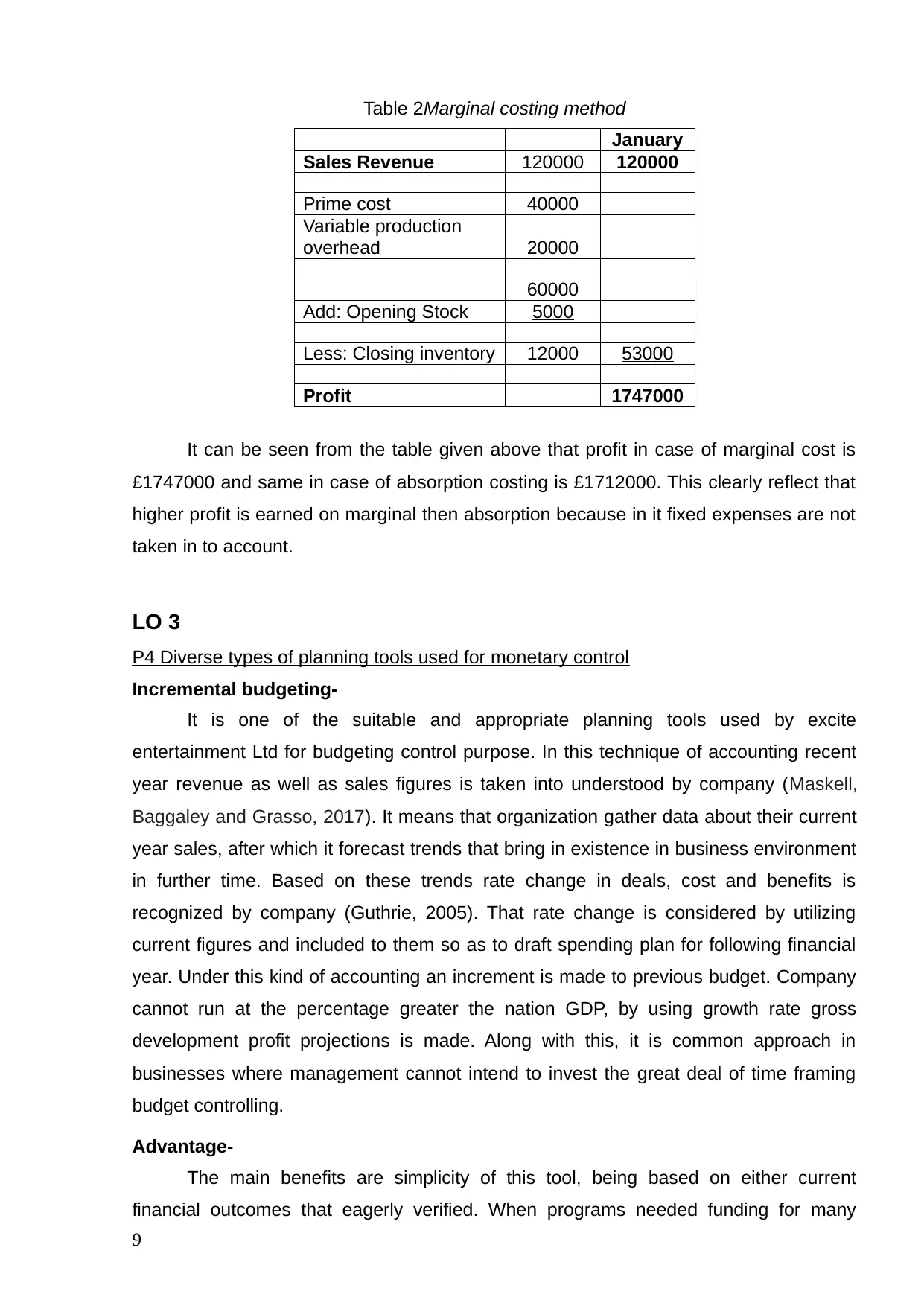

Table 2Marginal costing method

January

Sales Revenue 120000 120000

Prime cost 40000

Variable production

overhead 20000

60000

Add: Opening Stock 5000

Less: Closing inventory 12000 53000

Profit 1747000

It can be seen from the table given above that profit in case of marginal cost is

£1747000 and same in case of absorption costing is £1712000. This clearly reflect that

higher profit is earned on marginal then absorption because in it fixed expenses are not

taken in to account.

LO 3

P4 Diverse types of planning tools used for monetary control

Incremental budgeting-

It is one of the suitable and appropriate planning tools used by excite

entertainment Ltd for budgeting control purpose. In this technique of accounting recent

year revenue as well as sales figures is taken into understood by company (Maskell,

Baggaley and Grasso, 2017). It means that organization gather data about their current

year sales, after which it forecast trends that bring in existence in business environment

in further time. Based on these trends rate change in deals, cost and benefits is

recognized by company (Guthrie, 2005). That rate change is considered by utilizing

current figures and included to them so as to draft spending plan for following financial

year. Under this kind of accounting an increment is made to previous budget. Company

cannot run at the percentage greater the nation GDP, by using growth rate gross

development profit projections is made. Along with this, it is common approach in

businesses where management cannot intend to invest the great deal of time framing

budget controlling.

Advantage-

The main benefits are simplicity of this tool, being based on either current

financial outcomes that eagerly verified. When programs needed funding for many

9

January

Sales Revenue 120000 120000

Prime cost 40000

Variable production

overhead 20000

60000

Add: Opening Stock 5000

Less: Closing inventory 12000 53000

Profit 1747000

It can be seen from the table given above that profit in case of marginal cost is

£1747000 and same in case of absorption costing is £1712000. This clearly reflect that

higher profit is earned on marginal then absorption because in it fixed expenses are not

taken in to account.

LO 3

P4 Diverse types of planning tools used for monetary control

Incremental budgeting-

It is one of the suitable and appropriate planning tools used by excite

entertainment Ltd for budgeting control purpose. In this technique of accounting recent

year revenue as well as sales figures is taken into understood by company (Maskell,

Baggaley and Grasso, 2017). It means that organization gather data about their current

year sales, after which it forecast trends that bring in existence in business environment

in further time. Based on these trends rate change in deals, cost and benefits is

recognized by company (Guthrie, 2005). That rate change is considered by utilizing

current figures and included to them so as to draft spending plan for following financial

year. Under this kind of accounting an increment is made to previous budget. Company

cannot run at the percentage greater the nation GDP, by using growth rate gross

development profit projections is made. Along with this, it is common approach in

businesses where management cannot intend to invest the great deal of time framing

budget controlling.

Advantage-

The main benefits are simplicity of this tool, being based on either current

financial outcomes that eagerly verified. When programs needed funding for many

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

years in order to gain certain outcome, this tool is best structured help to assure that

funds can hold flowing to program. It helps to assure that accounting department are

effectively operated in stable and consistent manner for long period of time.

Disadvantage-

Incremental budgeting undertakes only minor changes from earlier period, when

in fact there are major structural changes in firm. Its outcomes in conservative mindset

in firm that actually noticeable force in destroying overall business over long term.

Top down budgeting-

This is the second planning tool or type of budgeting in which two level of

management perform together and work on budget, these stages are middles & top

level of accounting department. According to this tool, top management make a budget

and interact same to all level of financing management. After that manager at middle

level allocate budget cost among all management levels and these distributions is

communicated to middles one of top stage of administration for approval. After final

approval from supervision budget amount is assigned all sections in organization

effectively. In simple words, in top down budgeting method first of all higher cost

elements is being determined in budget at primary stage.

Advantage-

The benefits of using top down budgeting tool is that is allow company to do not

depend on lower level managers in firm to come up with budgeting data. Organization

with this method permit manager to only centring on its department and focus on what

they do best. When Excite entertainment Ltd, use this method, they have to wait for

each department to bring with budgets and after that compile them into firm broad

budget.

Disadvantage-

On the other hand, top down budgeting also has some drawbacks that impact on

accounting management. By using this technique is not always good choice as it does

have some disadvantages. For example, high level executives of organization not have

much knowledge about each department to come up with effective budget.

Zero based budgeting-

In this planning tool budgeting old value has not been used, in this method

budget is prepared by determined all activities of company (Walsh, 2016). Then assets

are assigned to these activities in order to make budget. Inputs is taken from all

department, until they cannot direct projected expense statement to top level of

management no amount is allocated to particular department. Resources values in this

10

funds can hold flowing to program. It helps to assure that accounting department are

effectively operated in stable and consistent manner for long period of time.

Disadvantage-

Incremental budgeting undertakes only minor changes from earlier period, when

in fact there are major structural changes in firm. Its outcomes in conservative mindset

in firm that actually noticeable force in destroying overall business over long term.

Top down budgeting-

This is the second planning tool or type of budgeting in which two level of

management perform together and work on budget, these stages are middles & top

level of accounting department. According to this tool, top management make a budget

and interact same to all level of financing management. After that manager at middle

level allocate budget cost among all management levels and these distributions is

communicated to middles one of top stage of administration for approval. After final

approval from supervision budget amount is assigned all sections in organization

effectively. In simple words, in top down budgeting method first of all higher cost

elements is being determined in budget at primary stage.

Advantage-

The benefits of using top down budgeting tool is that is allow company to do not

depend on lower level managers in firm to come up with budgeting data. Organization

with this method permit manager to only centring on its department and focus on what

they do best. When Excite entertainment Ltd, use this method, they have to wait for

each department to bring with budgets and after that compile them into firm broad

budget.

Disadvantage-

On the other hand, top down budgeting also has some drawbacks that impact on

accounting management. By using this technique is not always good choice as it does

have some disadvantages. For example, high level executives of organization not have

much knowledge about each department to come up with effective budget.

Zero based budgeting-

In this planning tool budgeting old value has not been used, in this method

budget is prepared by determined all activities of company (Walsh, 2016). Then assets

are assigned to these activities in order to make budget. Inputs is taken from all

department, until they cannot direct projected expense statement to top level of

management no amount is allocated to particular department. Resources values in this

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

method is estimated as well as by using these value company budgets is finally

prepared.

Advantage-

The advantage of this method is that it assures manager to think about how

every dollar or pound is spent and how every budgeting period. This procedure forces

manger to justify all functioning expenses and focusing which areas of firm is generating

revenue. With using traditional budgeting, organization cannot be examined legacy

costs for years until there is some sort of economic shock that pressure business to

take extreme actions. This approach leads to important misallocation of all resource,

when done effectively zero-based budgeting prevent misallocation from happening.

Disadvantage-

With this method high chances of presence of impractical values in budget

impact on business performance, it not used by company sometimes. One of the major

disadvantages of this method is that it can return short term thinking by moving

resources towards filed of organizations that generate revenue over further time period.

As outcomes, some areas of firms that is usually viewed as long term investments that

is not directly tied to revenue such as development and research or employees training,

left with smaller budgets which they actually need. It would possibly harm firm because

although these areas cannot be generating revenue, it is also considered as key to

remaining competitive for longer period of time.

LO 4

Management accounting systems adapt by Excite entertainment Ltd

Identifying financial issue with benchmarking-

Organizations can use benchmark, budgetary targets and key performance

indicators that helps to identify financial issue. Benchmark is the best procedure of

measuring performance of organization services, products or processes as opposite

those of other companies considered to be best in sector, in short, this method helps to

identify internal opportunities of business for financial improvement (Kruger and

Hancke, 2014). Business conditions has included over past few years where financial

information is considered as one of the most essential resource for measuring business

performance identifying financial issues related to alterations found in standardised set

of recital indicators. It led to use of different management accounting systems that set

benchmarks to analyse performance of business reflecting way it tends to focus on long

term sustainability features. Benchmarking is appropriate practice of comparing existing

business performance and procedures metrics to industry best and bests practice from

11

prepared.

Advantage-

The advantage of this method is that it assures manager to think about how

every dollar or pound is spent and how every budgeting period. This procedure forces

manger to justify all functioning expenses and focusing which areas of firm is generating

revenue. With using traditional budgeting, organization cannot be examined legacy

costs for years until there is some sort of economic shock that pressure business to

take extreme actions. This approach leads to important misallocation of all resource,

when done effectively zero-based budgeting prevent misallocation from happening.

Disadvantage-

With this method high chances of presence of impractical values in budget

impact on business performance, it not used by company sometimes. One of the major

disadvantages of this method is that it can return short term thinking by moving

resources towards filed of organizations that generate revenue over further time period.

As outcomes, some areas of firms that is usually viewed as long term investments that

is not directly tied to revenue such as development and research or employees training,

left with smaller budgets which they actually need. It would possibly harm firm because

although these areas cannot be generating revenue, it is also considered as key to

remaining competitive for longer period of time.

LO 4

Management accounting systems adapt by Excite entertainment Ltd

Identifying financial issue with benchmarking-

Organizations can use benchmark, budgetary targets and key performance

indicators that helps to identify financial issue. Benchmark is the best procedure of

measuring performance of organization services, products or processes as opposite

those of other companies considered to be best in sector, in short, this method helps to

identify internal opportunities of business for financial improvement (Kruger and

Hancke, 2014). Business conditions has included over past few years where financial

information is considered as one of the most essential resource for measuring business

performance identifying financial issues related to alterations found in standardised set

of recital indicators. It led to use of different management accounting systems that set

benchmarks to analyse performance of business reflecting way it tends to focus on long

term sustainability features. Benchmarking is appropriate practice of comparing existing

business performance and procedures metrics to industry best and bests practice from

11

other organizations. Dimensions usually measured cost, quality and time. With the help

of comparing business performance against other companies’ performance, excite

entertainment Ltd can improve their financial problems.

Management accounting skill sets-

Company know features of effective and efficient managerial accountant, that

helps to improve financial issues and reduce it effectively. Firm understand how skills is

applied to prevent issues and to deal with misappropriation of assets meant to grow

business. Planning and reporting, decision making, technology, operations and

leadership is included in set of management accounting skills that provide many

benefits to company when they used it efficiently. Competencies needed to envision

future, evaluate report financial outcomes and measure performance. Manager is able

with management accounting skill is to guide decisions, established the ethical

environment and mange risk that is beneficial for overall business. Company manage

information systems and technology to enable effective operations that also support to

solve financial issues. By contributing as cross functional partner of business it helps to

transform organization wide operations that increase financial budgets. Furthermore,

firm also respond to financial problems when they collaborate with its team member in

good manner which inspire group of people to achieve their common goals and

objectives.

Financial governance-

It is another way can used by company in which they collect data, monitor and

control in business. Along with this, day to day data is measured and decision made by

manager in respect to manufacturing of products in workplace and buying of raw

materials. These kinds of practices are assured that condition further remain in control

which is typically lead to earning or gaining of appropriate amount of profit in company.

Through this procedure organization track financial transactions effectively, control data

and manage performance of business which is one of the best respond to financial

issue. With the help of these activities they can consider the major things which affects

productivity and profitability of firm. Financial governance allows businesses to monitor

their current monetary controlling strategy that identifies any barriers in effective

financial management process. It is the best action of company in which they made

different policies as well as processes that is used by firm to manage business data and

assure that data is suitable for them.

Key performance indictor-

This is the anther method or way that is highly used by companies to make

appropriate decisions. In this procedure for several items standards is identified, this is

12

of comparing business performance against other companies’ performance, excite

entertainment Ltd can improve their financial problems.

Management accounting skill sets-

Company know features of effective and efficient managerial accountant, that

helps to improve financial issues and reduce it effectively. Firm understand how skills is

applied to prevent issues and to deal with misappropriation of assets meant to grow

business. Planning and reporting, decision making, technology, operations and

leadership is included in set of management accounting skills that provide many

benefits to company when they used it efficiently. Competencies needed to envision

future, evaluate report financial outcomes and measure performance. Manager is able

with management accounting skill is to guide decisions, established the ethical

environment and mange risk that is beneficial for overall business. Company manage

information systems and technology to enable effective operations that also support to

solve financial issues. By contributing as cross functional partner of business it helps to

transform organization wide operations that increase financial budgets. Furthermore,

firm also respond to financial problems when they collaborate with its team member in

good manner which inspire group of people to achieve their common goals and

objectives.

Financial governance-

It is another way can used by company in which they collect data, monitor and

control in business. Along with this, day to day data is measured and decision made by

manager in respect to manufacturing of products in workplace and buying of raw

materials. These kinds of practices are assured that condition further remain in control

which is typically lead to earning or gaining of appropriate amount of profit in company.

Through this procedure organization track financial transactions effectively, control data

and manage performance of business which is one of the best respond to financial

issue. With the help of these activities they can consider the major things which affects

productivity and profitability of firm. Financial governance allows businesses to monitor

their current monetary controlling strategy that identifies any barriers in effective

financial management process. It is the best action of company in which they made

different policies as well as processes that is used by firm to manage business data and

assure that data is suitable for them.

Key performance indictor-

This is the anther method or way that is highly used by companies to make

appropriate decisions. In this procedure for several items standards is identified, this is

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.