Management Accounting Techniques and Budgetary Control

Added on 2023-01-13

20 Pages4629 Words57 Views

B07929

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Table of Contents

TASK 2...........................................................................................................................3

Introduction........................................................................................................................3

L.O.2: Apply a range of management accounting techniques..........................................3

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs................................................................3

M2. Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents........................................................................8

L.O.3: Explain the use of planning tools used in management accounting Using budgets

for planning and control:..................................................................................................11

P4. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control........................................................................................................11

M3. Use of different planning tools and their application for preparing and forecasting

budgets:...........................................................................................................................13

L. O. 4: Compare ways in which organizations could use management accounting to

respond to financial problems..........................................................................................14

P5. Compare how organizations are adapting management accounting systems to

respond to financial problems..........................................................................................14

M4. Analyze how, in responding to financial problems, management accounting can

lead organizations to sustainable success......................................................................17

Conclusion.......................................................................................................................19

REFERENCES________________________________________............................20

TASK 2...........................................................................................................................3

Introduction........................................................................................................................3

L.O.2: Apply a range of management accounting techniques..........................................3

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs................................................................3

M2. Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents........................................................................8

L.O.3: Explain the use of planning tools used in management accounting Using budgets

for planning and control:..................................................................................................11

P4. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control........................................................................................................11

M3. Use of different planning tools and their application for preparing and forecasting

budgets:...........................................................................................................................13

L. O. 4: Compare ways in which organizations could use management accounting to

respond to financial problems..........................................................................................14

P5. Compare how organizations are adapting management accounting systems to

respond to financial problems..........................................................................................14

M4. Analyze how, in responding to financial problems, management accounting can

lead organizations to sustainable success......................................................................17

Conclusion.......................................................................................................................19

REFERENCES________________________________________............................20

TASK 2

Introduction

Management accounting evolved before the Industrial Revolution. It is important for

the organisational people; it introduces specific information even for non-accountants

anytime, and observes present firm’s finances and helps creating actual professional

way out. In my words, Management accounting is accounting for managers to set up

reports using financial information to achieve business objectives, planning, control and

decision making. It mixes accounting, finance and management with the business skills

and techniques (What Is a Management Accounting System?, 2020). The scope of it is:

Cost Accounting, Tools and technique of management control, Tax accounting and

Statistical and quantitative techniques.

Managerial accounting is carrying out by identifying, measuring, analyzing,

interpreting, and communicating financial information to line managers for chase of an

organizational goal (What Is a Management Accounting System?, 2020).

L.O.2: Apply a range of management accounting techniques.

P3. Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption

costs

Costs: Costs are the expenses of business which is to be reduced from sales

revenue to get net profit earn by company during year.

Different costs and cost analysis:

There are mainly two types of costs; fixed and variable. Fixed costs are constant

over year and contains fixed amount paid by business for entire year; while on the

Introduction

Management accounting evolved before the Industrial Revolution. It is important for

the organisational people; it introduces specific information even for non-accountants

anytime, and observes present firm’s finances and helps creating actual professional

way out. In my words, Management accounting is accounting for managers to set up

reports using financial information to achieve business objectives, planning, control and

decision making. It mixes accounting, finance and management with the business skills

and techniques (What Is a Management Accounting System?, 2020). The scope of it is:

Cost Accounting, Tools and technique of management control, Tax accounting and

Statistical and quantitative techniques.

Managerial accounting is carrying out by identifying, measuring, analyzing,

interpreting, and communicating financial information to line managers for chase of an

organizational goal (What Is a Management Accounting System?, 2020).

L.O.2: Apply a range of management accounting techniques.

P3. Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption

costs

Costs: Costs are the expenses of business which is to be reduced from sales

revenue to get net profit earn by company during year.

Different costs and cost analysis:

There are mainly two types of costs; fixed and variable. Fixed costs are constant

over year and contains fixed amount paid by business for entire year; while on the

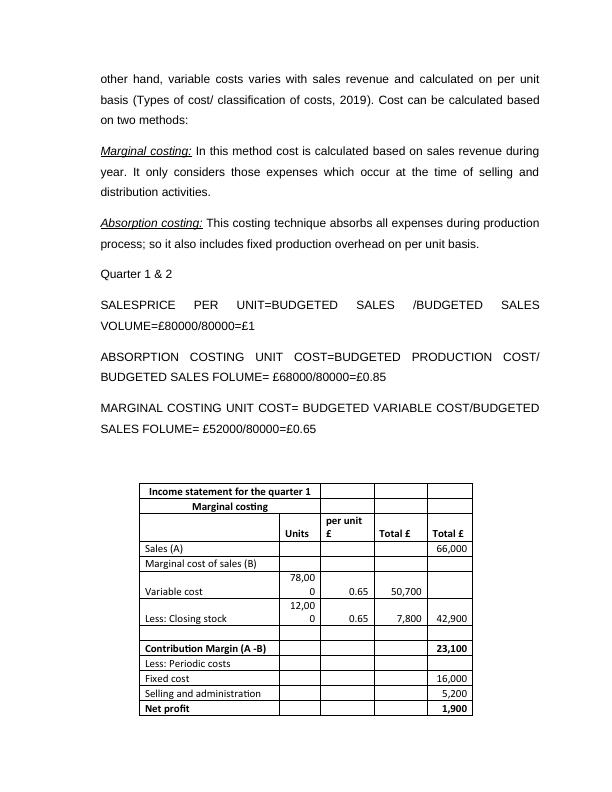

other hand, variable costs varies with sales revenue and calculated on per unit

basis (Types of cost/ classification of costs, 2019). Cost can be calculated based

on two methods:

Marginal costing: In this method cost is calculated based on sales revenue during

year. It only considers those expenses which occur at the time of selling and

distribution activities.

Absorption costing: This costing technique absorbs all expenses during production

process; so it also includes fixed production overhead on per unit basis.

Quarter 1 & 2

SALESPRICE PER UNIT=BUDGETED SALES /BUDGETED SALES

VOLUME=£80000/80000=£1

ABSORPTION COSTING UNIT COST=BUDGETED PRODUCTION COST/

BUDGETED SALES FOLUME= £68000/80000=£0.85

MARGINAL COSTING UNIT COST= BUDGETED VARIABLE COST/BUDGETED

SALES FOLUME= £52000/80000=£0.65

Income statement for the quarter 1

Marginal costing

Units

per unit

£ Total £ Total £

Sales (A) 66,000

Marginal cost of sales (B)

Variable cost

78,00

0 0.65 50,700

Less: Closing stock

12,00

0 0.65 7,800 42,900

Contribution Margin (A -B) 23,100

Less: Periodic costs

Fixed cost 16,000

Selling and administration 5,200

Net profit 1,900

basis (Types of cost/ classification of costs, 2019). Cost can be calculated based

on two methods:

Marginal costing: In this method cost is calculated based on sales revenue during

year. It only considers those expenses which occur at the time of selling and

distribution activities.

Absorption costing: This costing technique absorbs all expenses during production

process; so it also includes fixed production overhead on per unit basis.

Quarter 1 & 2

SALESPRICE PER UNIT=BUDGETED SALES /BUDGETED SALES

VOLUME=£80000/80000=£1

ABSORPTION COSTING UNIT COST=BUDGETED PRODUCTION COST/

BUDGETED SALES FOLUME= £68000/80000=£0.85

MARGINAL COSTING UNIT COST= BUDGETED VARIABLE COST/BUDGETED

SALES FOLUME= £52000/80000=£0.65

Income statement for the quarter 1

Marginal costing

Units

per unit

£ Total £ Total £

Sales (A) 66,000

Marginal cost of sales (B)

Variable cost

78,00

0 0.65 50,700

Less: Closing stock

12,00

0 0.65 7,800 42,900

Contribution Margin (A -B) 23,100

Less: Periodic costs

Fixed cost 16,000

Selling and administration 5,200

Net profit 1,900

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Techniques and Planning Toolslg...

|19

|3950

|63

Management Accounting Fundamentals and Techniqueslg...

|22

|4158

|72

Management Accounting Techniques and Budgetary Controllg...

|16

|3499

|49

Management Accounting Techniques and Budgetary Controllg...

|15

|3492

|91

Management Accounting Techniques and Planning Toolslg...

|13

|3081

|86

MANAGEMENT ACCOUNTINGlg...

|9

|498

|72