Management Accounting: Costing Analysis and Profit Reconciliation

VerifiedAdded on 2022/12/23

|11

|417

|50

Report

AI Summary

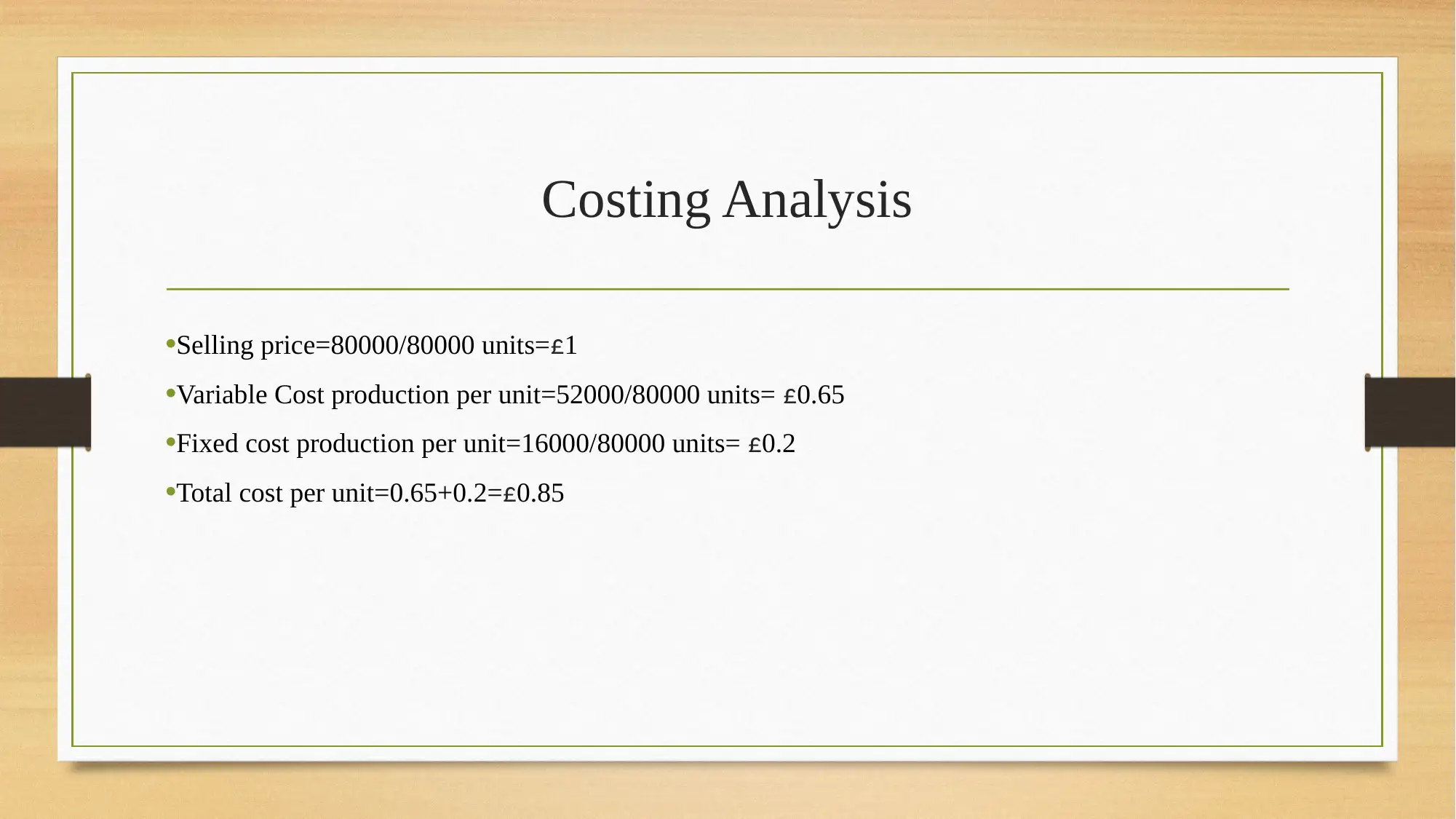

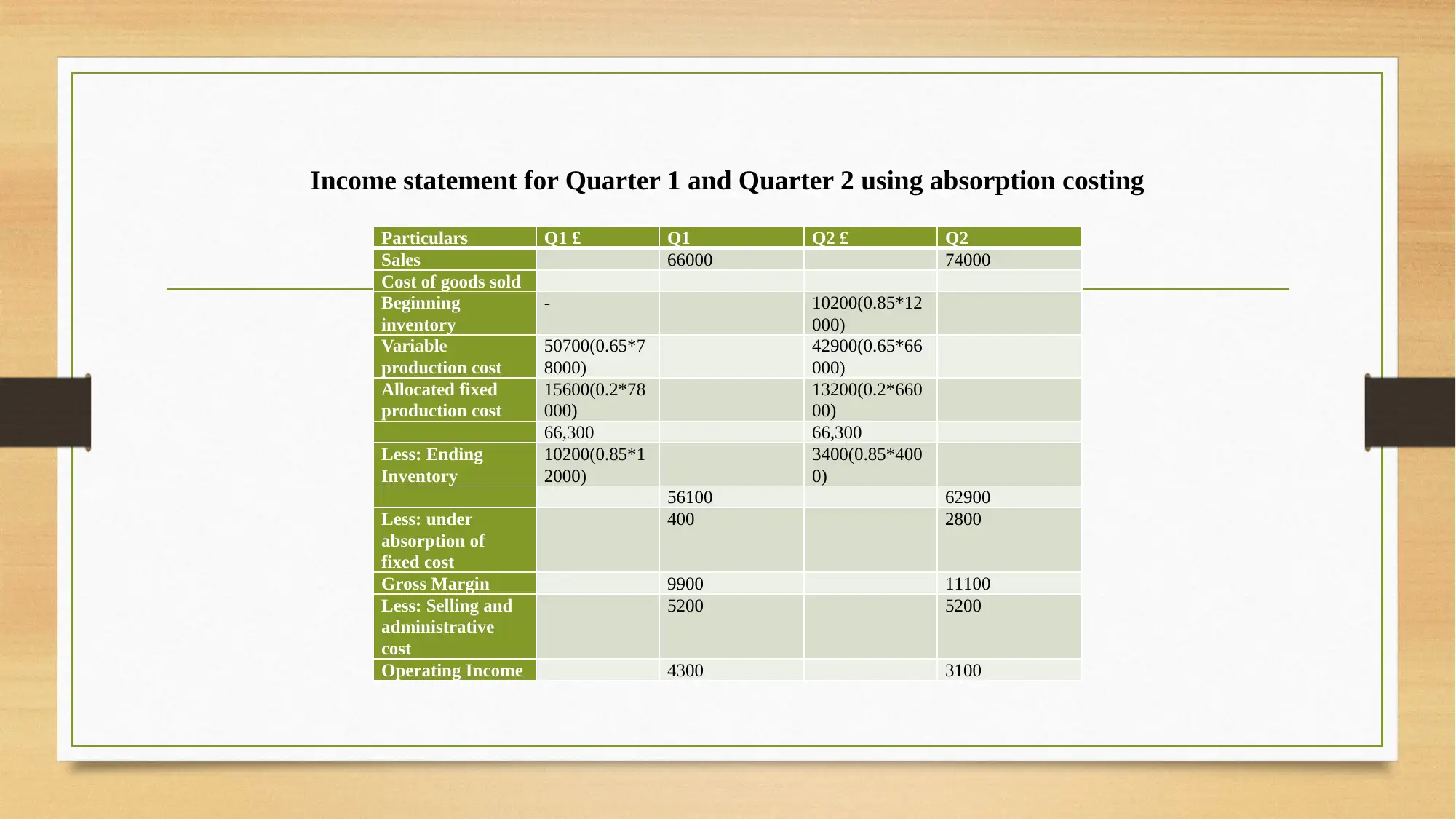

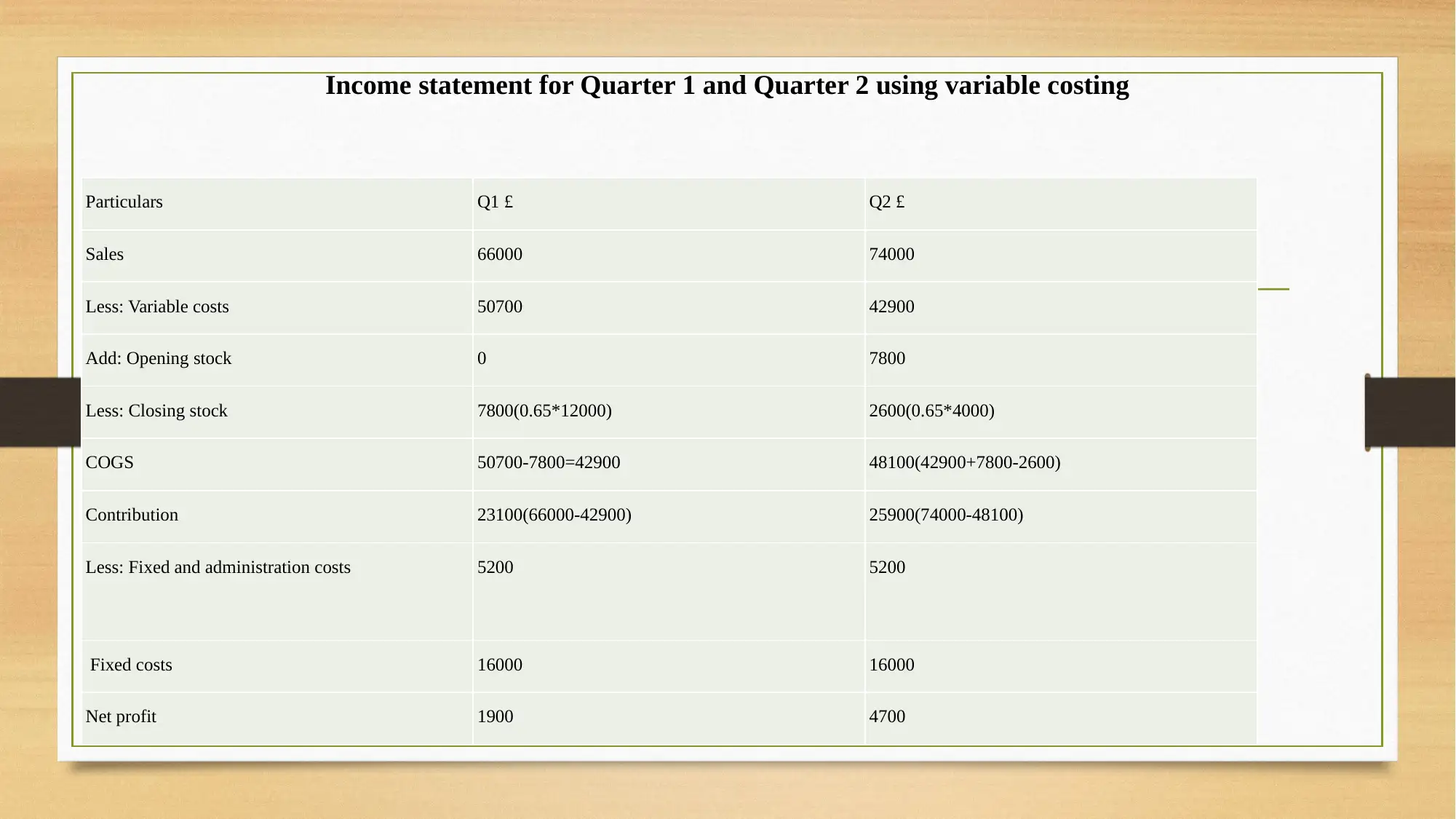

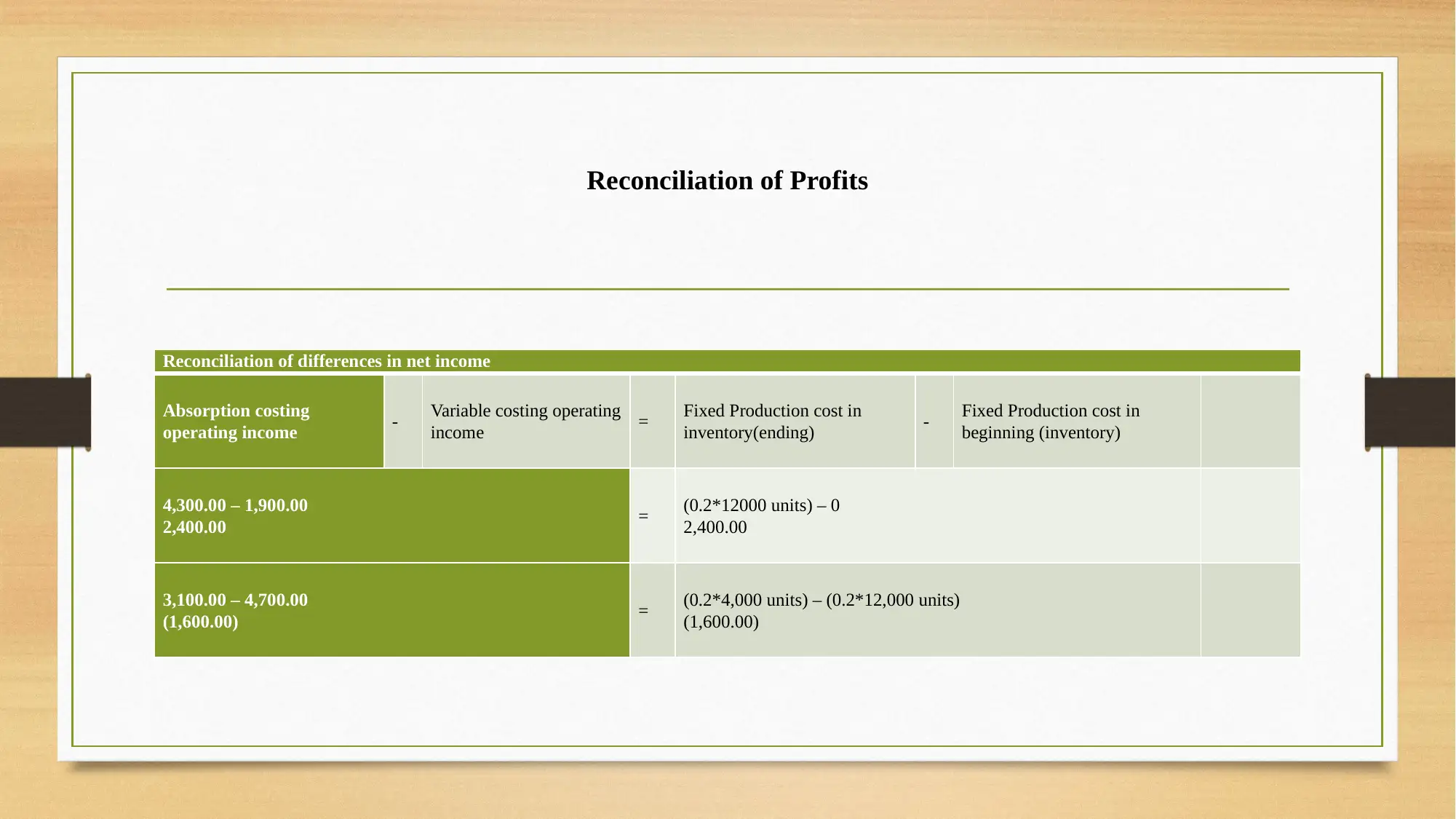

This report conducts a costing analysis comparing absorption and marginal costing methods. It utilizes income statements to analyze the different costing types and their impact on profit. The analysis includes calculations of selling price, variable and fixed costs, and the preparation of income statements for both absorption and marginal costing for two quarters. The report then reconciles the profits generated under each method, highlighting the differences and explaining the reasons behind them. The analysis section discusses the implications of each costing method, emphasizing their respective uses for internal and external reporting. Finally, the report concludes by acknowledging the significance of both costing approaches and their applicability in various management accounting functions. References are provided at the end of the report.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.