Financial Analysis: Cost Structure of Global Manufacturing Firms

VerifiedAdded on 2021/12/20

|11

|1256

|74

Report

AI Summary

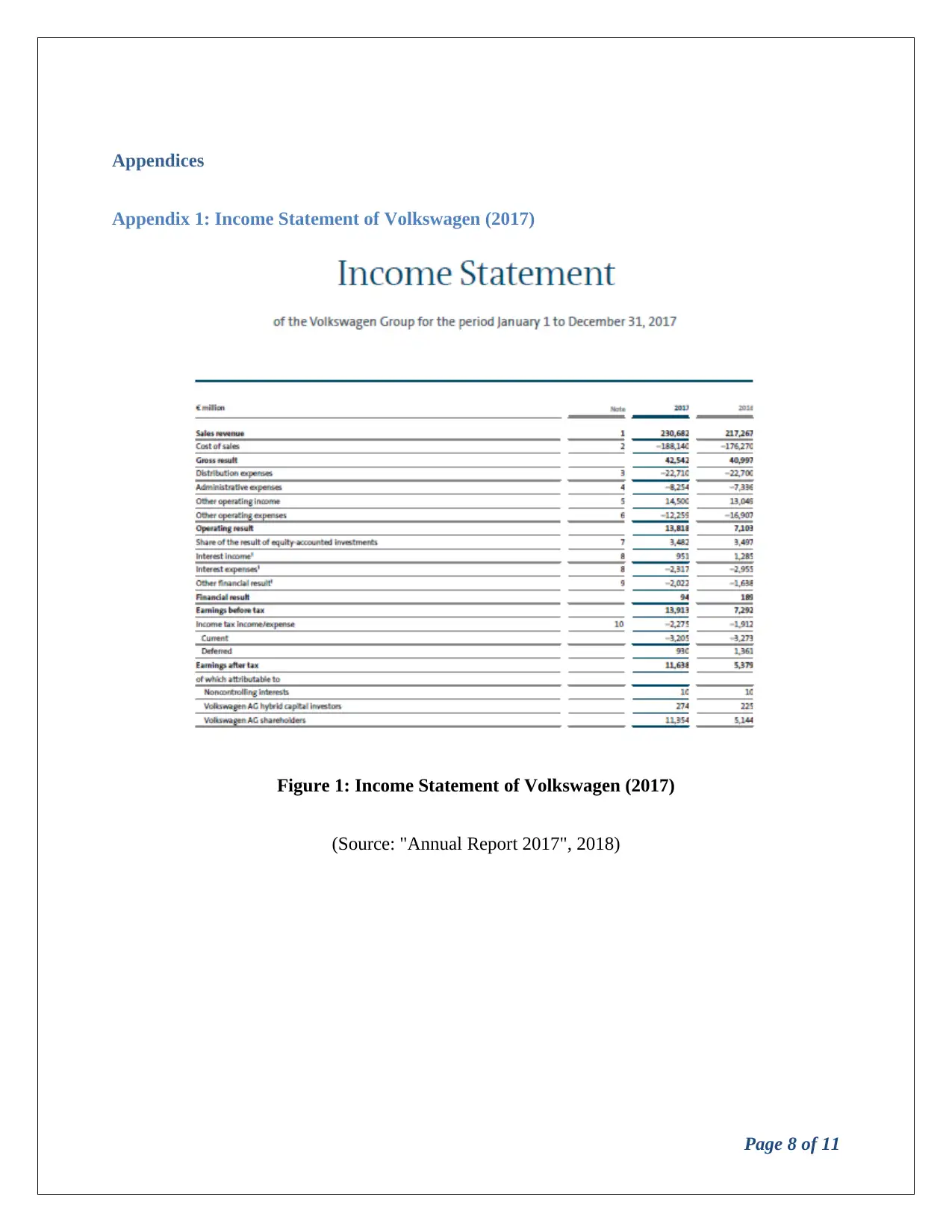

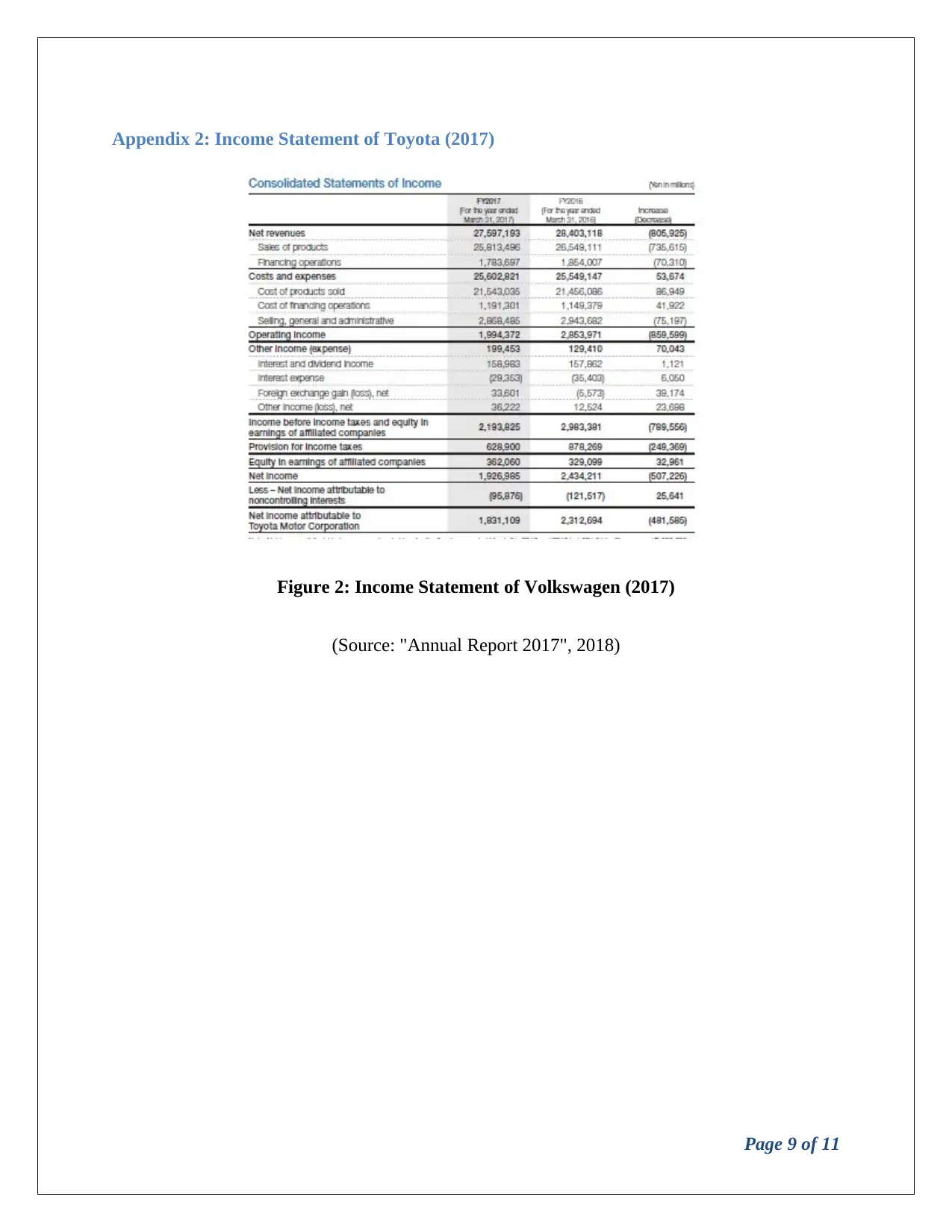

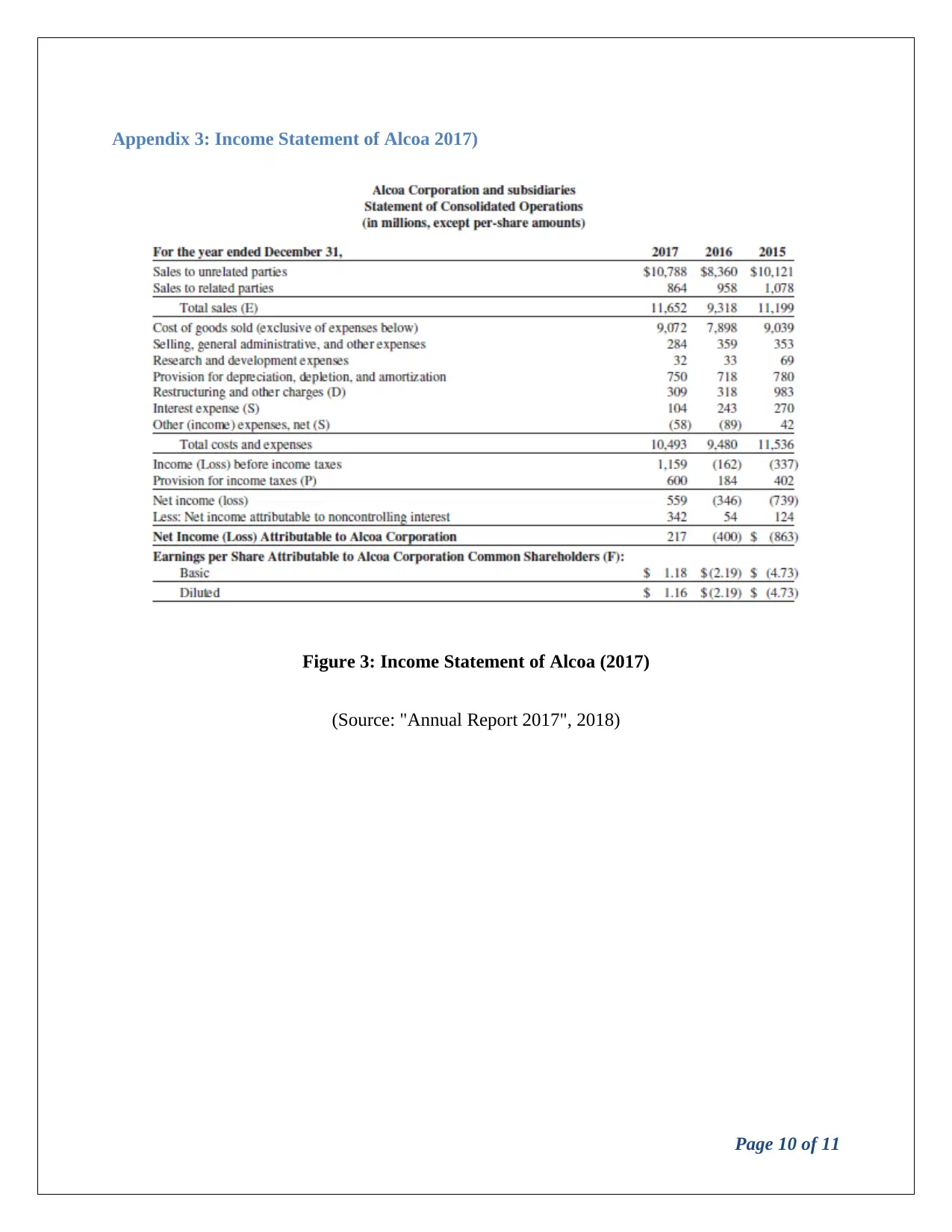

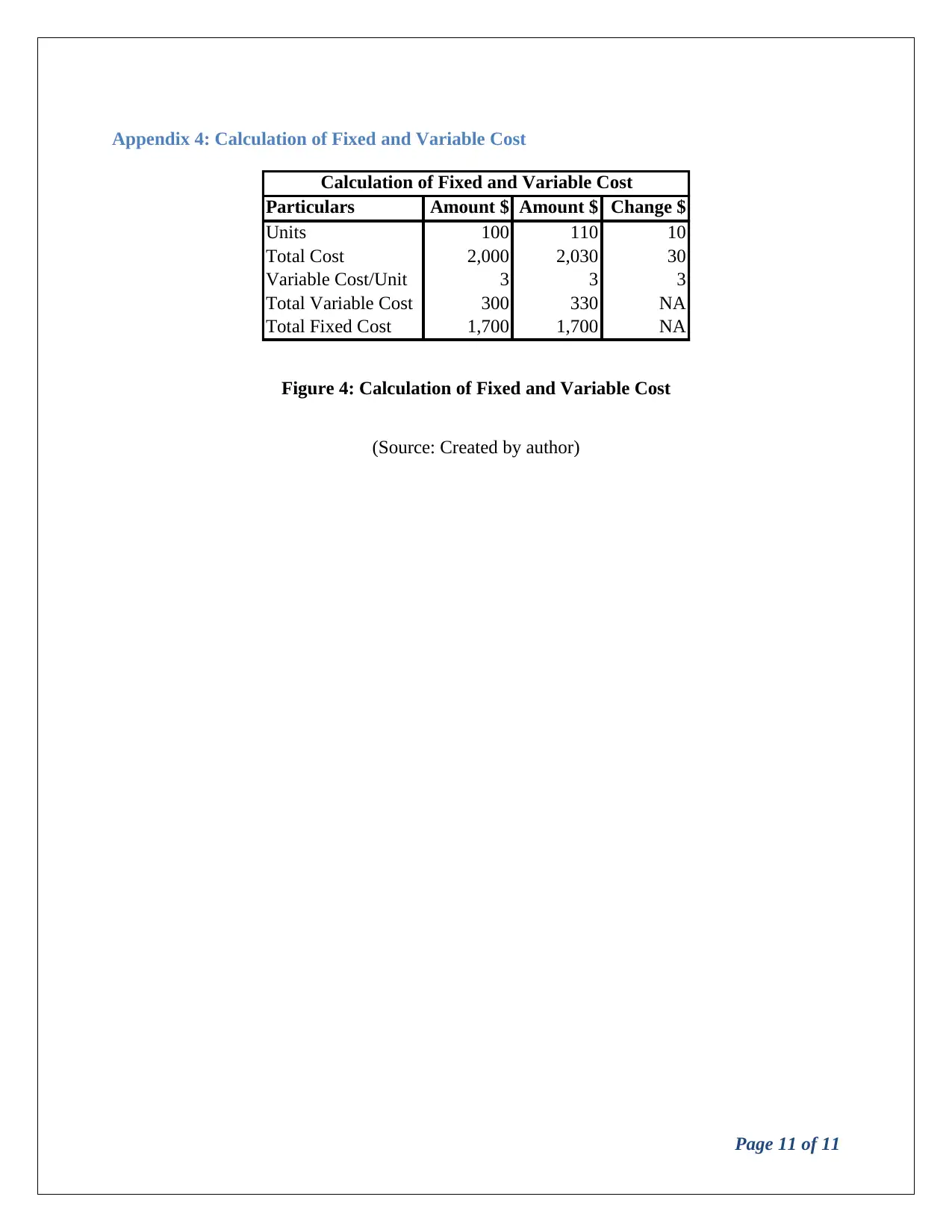

This report provides an in-depth analysis of the cost structures of three global companies: Volkswagen, Toyota, and Alcoa. The report examines the companies' financial data, focusing on the identification and classification of fixed and variable costs. It explores the impact of various factors, such as expansion, investment, and technological advancements, on the cost structures. The analysis includes a detailed overview of the companies' backgrounds, revenue, and expenses, drawing insights from their 2017 annual reports. The report also explains the methodology for calculating fixed and variable costs using hypothetical examples and data extracted from the annual reports. The conclusion emphasizes the challenges in accurately categorizing costs based on financial data alone and highlights the importance of understanding cost behavior for effective management accounting practices.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.