Management Accounting: Job Order Costing and ABC System Analysis

VerifiedAdded on 2020/06/04

|8

|1172

|185

Homework Assignment

AI Summary

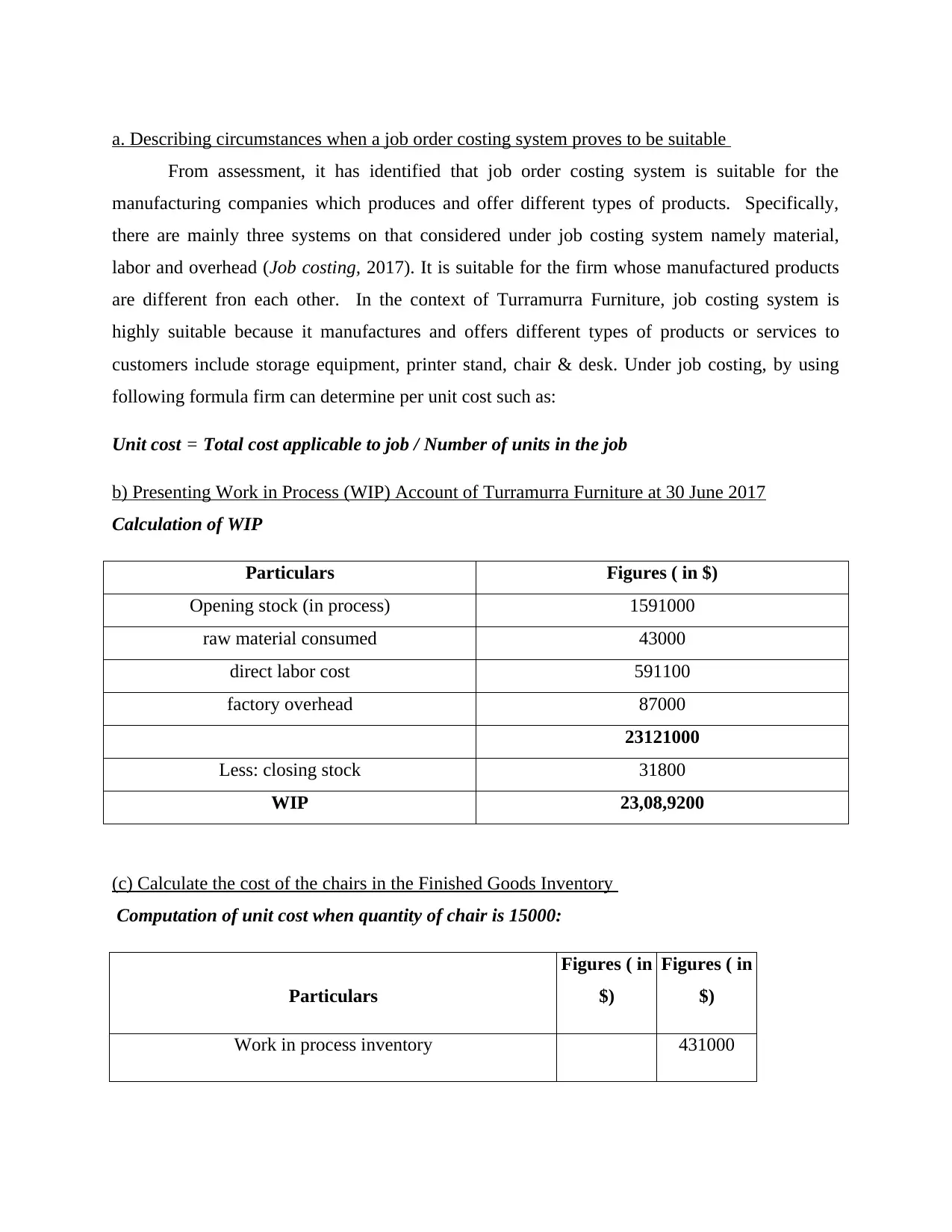

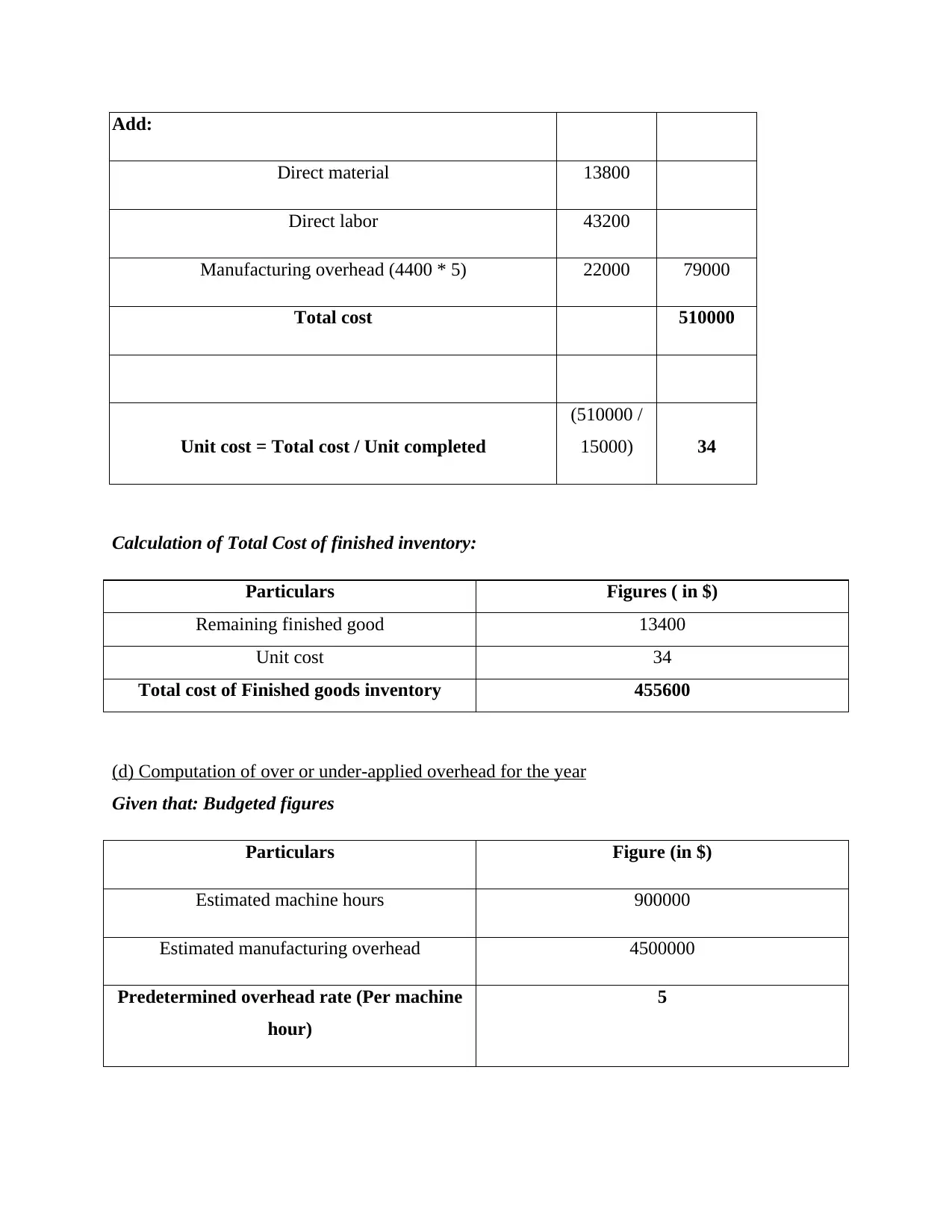

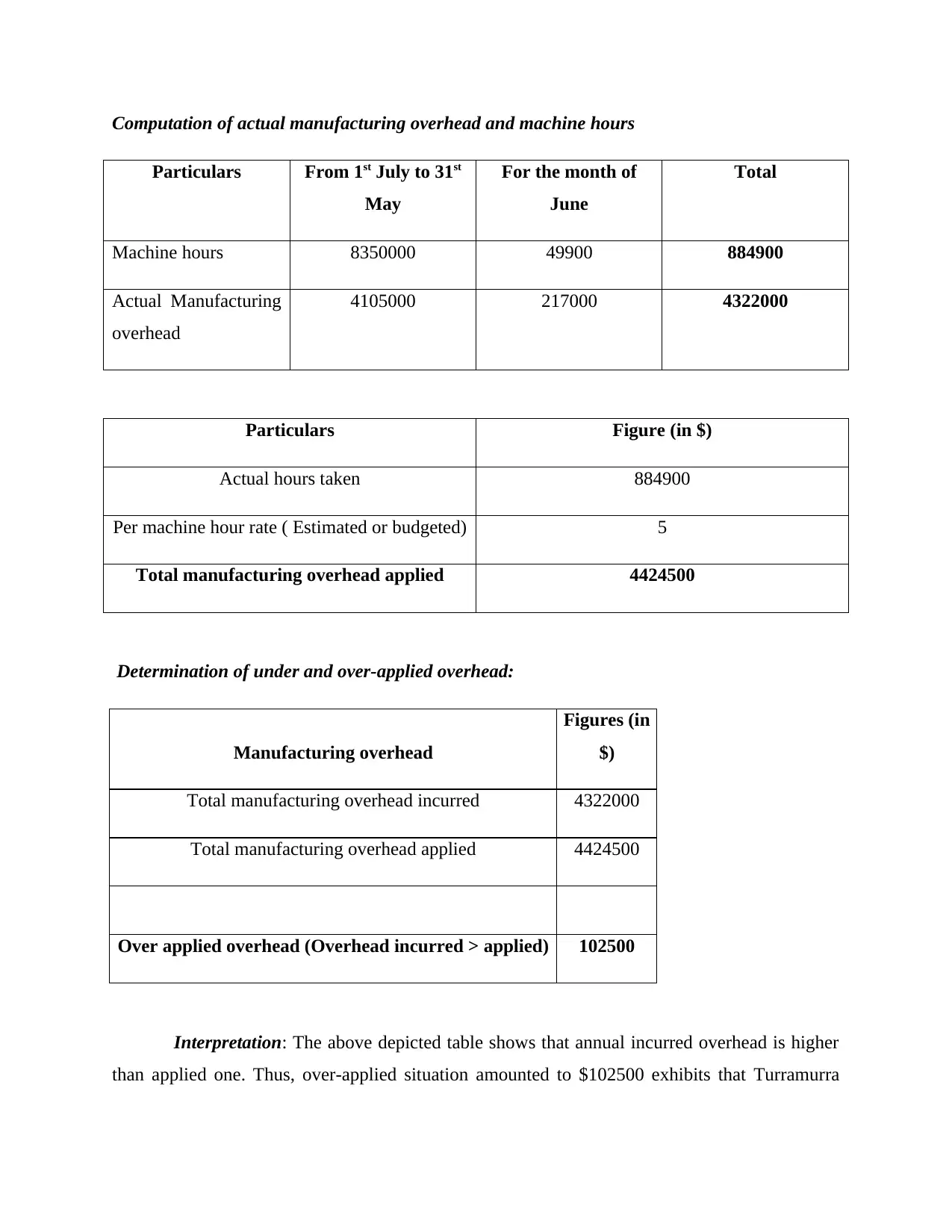

This document presents a comprehensive solution to a management accounting assignment focused on job order costing. The assignment analyzes the suitability of job order costing for Turramurra Furniture, detailing the calculation of Work in Process (WIP) and the cost of finished goods inventory. It includes a computation of over or under-applied overhead, outlining different treatments for the balances and actions to be taken when the over/under-application is material. The solution also provides a recommendation on whether the firm should undertake an Activity-Based Costing (ABC) system, weighing its advantages and disadvantages. The assignment covers key concepts like overhead allocation, cost accounting, and the application of different costing systems, making it a valuable resource for students studying management accounting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.