Detailed Analysis of Management Accounting for Fenner Plc

VerifiedAdded on 2021/02/19

|15

|4226

|170

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the case of Fenner Plc, a British industrial belting and polymer-based products manufacturer. The report begins by defining management accounting and explores the essential needs of various management accounting systems, including inventory management, price optimization, cost accounting, and job costing systems. It then details several methods utilized for management accounting reporting, such as performance reports, inventory management reports, and accounts receivable reports. Furthermore, the report delves into cost analysis techniques, specifically marginal costing and absorption costing, and demonstrates their application with examples. The report also examines the advantages and disadvantages of different budgetary control planning tools and compares how firms utilize management accounting systems to address financial problems. The report concludes with a discussion of how Fenner Plc uses management accounting to monitor, control, and analyze its operations, and how these systems are crucial for strategic decision-making and financial health.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential needs of various kinds of management accounting

systems...................................................................................................................................1

P2. Several methods utilised for management accounting reporting.....................................3

TASK 2............................................................................................................................................4

P3. Calculation of cost with the help of cost analysis techniques..........................................4

TASK 3............................................................................................................................................7

P4. Advantage and disadvantage of several kinds of budgetary control planning tools........7

TASK 4............................................................................................................................................9

P5. Comparison of way through which firms are utilising management accounting system to

respond financial problems.....................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential needs of various kinds of management accounting

systems...................................................................................................................................1

P2. Several methods utilised for management accounting reporting.....................................3

TASK 2............................................................................................................................................4

P3. Calculation of cost with the help of cost analysis techniques..........................................4

TASK 3............................................................................................................................................7

P4. Advantage and disadvantage of several kinds of budgetary control planning tools........7

TASK 4............................................................................................................................................9

P5. Comparison of way through which firms are utilising management accounting system to

respond financial problems.....................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is considered as the systematised procedures of identifying,

gathering , measuring, interpreting preparing as well as communicating financial data. This is

utilised through management for formulating plans in order to organise and control firms

(Anessi-Pessina and et.al., 2016). For this report, the chosen company is Fenner Plc which is the

fastest growing British industrial belting as well as another polymer based products

manufacturer. Its headquarters is in Hessele, England, UK. The purpose of this report is to

describe management accounting and essential needs of various management accounting system

types. Several methods that are utilised for management accounting reporting as well as different

planning tools for budgetary control. Apart from this, calculation of cost with the help of cost

analysis techniques and how that aids to resolve financial problems are also mentioned in this

report.

TASK 1

P1. Management accounting and essential needs of various kinds of management accounting

systems.

Management accounting is refers as the methods of that is utilise through company for

managing, monitoring, controlling and analysing their whole operative as well as executional

activities effectively. Therefore, managers of the Fenner Plc utilise this for the intent to formulate

strategic decision for the effectiveness of their business. Management accounting system is

considered as the system that is applied through managers for analysing as well as monitoring

financial data of organisation on time in order to develop decisions for regular activities. Fenner

Plc utilise some of its types of management accounting system so that they can keep the

information about actual performance of their business. Moreover, with the assistance of these

their managers can maintain appropriate records so that can be utilise in future for effectiveness

of business. All the types are mentioned below:

Inventory management system: This kind of system are mostly utilised into

manufacturing firm in order to keep inventory records that are used in production

activities. This aids manager for examining that stock of raw material are available in its

warehouse or not (Ashraf and Uddin, 2015). Fenner Plc can applied his particular system

so that they get to know that sufficient raw material are their to manufacture polymer

1

Management accounting is considered as the systematised procedures of identifying,

gathering , measuring, interpreting preparing as well as communicating financial data. This is

utilised through management for formulating plans in order to organise and control firms

(Anessi-Pessina and et.al., 2016). For this report, the chosen company is Fenner Plc which is the

fastest growing British industrial belting as well as another polymer based products

manufacturer. Its headquarters is in Hessele, England, UK. The purpose of this report is to

describe management accounting and essential needs of various management accounting system

types. Several methods that are utilised for management accounting reporting as well as different

planning tools for budgetary control. Apart from this, calculation of cost with the help of cost

analysis techniques and how that aids to resolve financial problems are also mentioned in this

report.

TASK 1

P1. Management accounting and essential needs of various kinds of management accounting

systems.

Management accounting is refers as the methods of that is utilise through company for

managing, monitoring, controlling and analysing their whole operative as well as executional

activities effectively. Therefore, managers of the Fenner Plc utilise this for the intent to formulate

strategic decision for the effectiveness of their business. Management accounting system is

considered as the system that is applied through managers for analysing as well as monitoring

financial data of organisation on time in order to develop decisions for regular activities. Fenner

Plc utilise some of its types of management accounting system so that they can keep the

information about actual performance of their business. Moreover, with the assistance of these

their managers can maintain appropriate records so that can be utilise in future for effectiveness

of business. All the types are mentioned below:

Inventory management system: This kind of system are mostly utilised into

manufacturing firm in order to keep inventory records that are used in production

activities. This aids manager for examining that stock of raw material are available in its

warehouse or not (Ashraf and Uddin, 2015). Fenner Plc can applied his particular system

so that they get to know that sufficient raw material are their to manufacture polymer

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

products or not. Moreover, this is needed by respective company to observe actual status

of inventory.

Price optimisation system: Price-optimisation is crucial for attaining competitive

advantages. This system is applied by management of organisation to set appropriate

price for whole products for accomplishing the requirements of customers. With the

assistance of this firms try to develop the goods pocket friendly for its target market place

(Ball, Grubnicand Birchall, 2014). Fenner Plc can applied this system for examining the

consumer response upon various prices that are set through them for its industrial belting

and other polymers based products. Moreover, this is also helpful to set effective

products price in order to accomplish organisational goals and clients needs. For it,

respective firm select the appropriate pricing strategy for the business success. Cost accounting system: This is considered as the system that is mostly utilise through

firms for estimating the cost of various goods that are manufactured by organisation. This

directs the them know about the approximation of accurate expenditure that are incurred

during manufacturing. Fenner Plc applied this to examine the cost that is related to all

manufacture polymer based product, belting etc. It is needed in respective company as

this aids their manager to find out actual manufacturing cost. Initially, they measure as

well as records overall expenses separately then compare the outcomes with exact output

so that their business performance can be measured.

Job costing system: This is considered as the costing system that is applied for gathering

as well as assigning overall manufacturing costs that incurred during business activities

(Christ, urritt and Varsei, 2016). Fenner Plc can used this particular system for assessing

the cost of whole procedures that are performed as per the specification of customers.

This is essential for firms to apply this as it aids them to ascertain actual cost of each job

that is done through company. This system is mostly utilised through organisations that

performs their business operations as per particular clients orders.

From the above mentioned management accounting system are applied by the Fenner Plc

manager so that they can analyses their organisational performance as well as develop strategic

decisions for the effectiveness of business.

2

of inventory.

Price optimisation system: Price-optimisation is crucial for attaining competitive

advantages. This system is applied by management of organisation to set appropriate

price for whole products for accomplishing the requirements of customers. With the

assistance of this firms try to develop the goods pocket friendly for its target market place

(Ball, Grubnicand Birchall, 2014). Fenner Plc can applied this system for examining the

consumer response upon various prices that are set through them for its industrial belting

and other polymers based products. Moreover, this is also helpful to set effective

products price in order to accomplish organisational goals and clients needs. For it,

respective firm select the appropriate pricing strategy for the business success. Cost accounting system: This is considered as the system that is mostly utilise through

firms for estimating the cost of various goods that are manufactured by organisation. This

directs the them know about the approximation of accurate expenditure that are incurred

during manufacturing. Fenner Plc applied this to examine the cost that is related to all

manufacture polymer based product, belting etc. It is needed in respective company as

this aids their manager to find out actual manufacturing cost. Initially, they measure as

well as records overall expenses separately then compare the outcomes with exact output

so that their business performance can be measured.

Job costing system: This is considered as the costing system that is applied for gathering

as well as assigning overall manufacturing costs that incurred during business activities

(Christ, urritt and Varsei, 2016). Fenner Plc can used this particular system for assessing

the cost of whole procedures that are performed as per the specification of customers.

This is essential for firms to apply this as it aids them to ascertain actual cost of each job

that is done through company. This system is mostly utilised through organisations that

performs their business operations as per particular clients orders.

From the above mentioned management accounting system are applied by the Fenner Plc

manager so that they can analyses their organisational performance as well as develop strategic

decisions for the effectiveness of business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2. Several methods utilised for management accounting reporting.

Within all firms, management is divided into various levels so that all the things can be

managed in effective manner but communication is considered as the essential aspects which

ascertain the management chain appropriately. In order to communicate the financial

information, firm used the several types of management accounting reports. Management

accounting reporting is considered as the procedures where carious reports are formulated for

assessing the organisation's performance (Cooper, 2017). This is very crucial for managers to

utilise effective methods for it in order to get the accurate as well as detailed information about

company's internal performance. This reports are prepared by Fenner Plc on yearly basis to keep

the records of whole operative as well as executional activities which are performed by them.

There are several methods that are utilise by respective firm are explained below:

Performance report: This is considered as the report which is prepared by organisation

to keep performance records of business and staff. This is utilised by various firms in

order to provides bonus, incentives and many more to their employees as per its efforts

that are done by them to accomplish their goals. Fenner Plc managers can prepare this

report for monitoring the activities of staff whether they are performing in positive or

negative manner. This is advantageous for business as it aids to keep workers encouraged

because they obtain some rewards for its better performance. Moreover, it directs their

managers to make fast as well as strategic decisions when firm or employees do not

perform effectively.

Inventory management report: For keeping the records of goods that are utilised

through business enterprises to perform manufacturing activities, managers prepare the

inventory management report. Moreover, this aids them to examine that sufficient funds

are available for performing the activities (Evans, Burritt and Guthrie, 2013). Fenner Plc

manager's can prepare this [articular rep[rot so that they can able to know about the

inventory availability that are utilise to manufacture belting and other polymers products.

This advantageous for respective firm as this assists them to order inventory before it

goes out of stock. In case firm is not capable to record exact data then this will become

tough for them to implement operative activities in effectual way.

3

Within all firms, management is divided into various levels so that all the things can be

managed in effective manner but communication is considered as the essential aspects which

ascertain the management chain appropriately. In order to communicate the financial

information, firm used the several types of management accounting reports. Management

accounting reporting is considered as the procedures where carious reports are formulated for

assessing the organisation's performance (Cooper, 2017). This is very crucial for managers to

utilise effective methods for it in order to get the accurate as well as detailed information about

company's internal performance. This reports are prepared by Fenner Plc on yearly basis to keep

the records of whole operative as well as executional activities which are performed by them.

There are several methods that are utilise by respective firm are explained below:

Performance report: This is considered as the report which is prepared by organisation

to keep performance records of business and staff. This is utilised by various firms in

order to provides bonus, incentives and many more to their employees as per its efforts

that are done by them to accomplish their goals. Fenner Plc managers can prepare this

report for monitoring the activities of staff whether they are performing in positive or

negative manner. This is advantageous for business as it aids to keep workers encouraged

because they obtain some rewards for its better performance. Moreover, it directs their

managers to make fast as well as strategic decisions when firm or employees do not

perform effectively.

Inventory management report: For keeping the records of goods that are utilised

through business enterprises to perform manufacturing activities, managers prepare the

inventory management report. Moreover, this aids them to examine that sufficient funds

are available for performing the activities (Evans, Burritt and Guthrie, 2013). Fenner Plc

manager's can prepare this [articular rep[rot so that they can able to know about the

inventory availability that are utilise to manufacture belting and other polymers products.

This advantageous for respective firm as this assists them to order inventory before it

goes out of stock. In case firm is not capable to record exact data then this will become

tough for them to implement operative activities in effectual way.

3

Accounting receivables reports: This is considered as the report that is prepared though

managers of the firm to keep records of whole sales that are done on credit basis on

specified time. This reports are mostly formulate by those firm whose customer

purchases their products on credit (Goodman and et.al., 2013). This assists them to list

out overall activities unused credit memos as well as unpaid consumer invoices as per the

due date. Fenner Plc manager's can prepare this particular report in order to examine the

amount that is purchase y consumers on credit. The main aim of account receivable

report is to trace data of that clients who buy the products on credit and promise to pay

that amount on specified time. This report is advantageous for respective company as

through it they can able to ascertain the outstanding amount of various customers with

date and time.

From the above mentioned management accounting reporting help Fenner Plc manager to

keep all the data regarding staff and company performance, availability and usages of inventory

and many more.

TASK 2

P3. Calculation of cost with the help of cost analysis techniques.

Cost is includes the price that is obtained through individuals for generating,

accomplishing as well as selling something. It is considered as the monetary valuation of

resources, materials, efforts as well as opportunity into manufacturing as well as delivering

products or services.

Marginal costing:

Marginal costing is considered as the most essential technique that is required to prepare

income statements or profits and loss statements. Herein, accountants focused upon systematic

classification of expenditure into variable and fixed (Grossi and Steccolini, 2014). Fixed costs

are consider as the period cost. Where as overall variables manufacturing expenditure are allotted

to specific units. This ascertains the impact of variable expenses upon net income or per unit

product cost.

Absorption costing:

This is refers as the costing techniques which consider both fixed and variable cost as

product costs. The main aim of it is to provide the report as well as compute accurate

4

managers of the firm to keep records of whole sales that are done on credit basis on

specified time. This reports are mostly formulate by those firm whose customer

purchases their products on credit (Goodman and et.al., 2013). This assists them to list

out overall activities unused credit memos as well as unpaid consumer invoices as per the

due date. Fenner Plc manager's can prepare this particular report in order to examine the

amount that is purchase y consumers on credit. The main aim of account receivable

report is to trace data of that clients who buy the products on credit and promise to pay

that amount on specified time. This report is advantageous for respective company as

through it they can able to ascertain the outstanding amount of various customers with

date and time.

From the above mentioned management accounting reporting help Fenner Plc manager to

keep all the data regarding staff and company performance, availability and usages of inventory

and many more.

TASK 2

P3. Calculation of cost with the help of cost analysis techniques.

Cost is includes the price that is obtained through individuals for generating,

accomplishing as well as selling something. It is considered as the monetary valuation of

resources, materials, efforts as well as opportunity into manufacturing as well as delivering

products or services.

Marginal costing:

Marginal costing is considered as the most essential technique that is required to prepare

income statements or profits and loss statements. Herein, accountants focused upon systematic

classification of expenditure into variable and fixed (Grossi and Steccolini, 2014). Fixed costs

are consider as the period cost. Where as overall variables manufacturing expenditure are allotted

to specific units. This ascertains the impact of variable expenses upon net income or per unit

product cost.

Absorption costing:

This is refers as the costing techniques which consider both fixed and variable cost as

product costs. The main aim of it is to provide the report as well as compute accurate

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

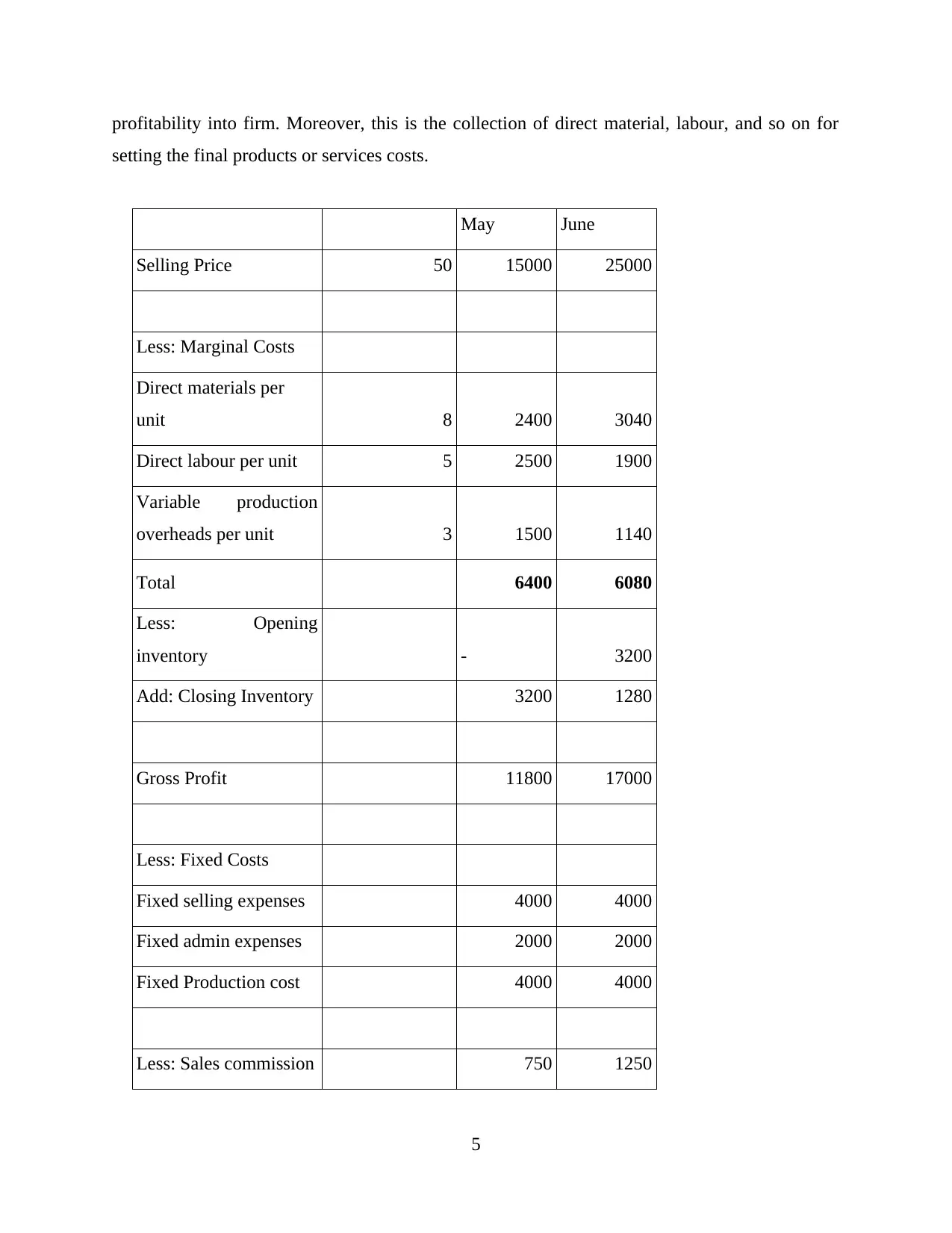

profitability into firm. Moreover, this is the collection of direct material, labour, and so on for

setting the final products or services costs.

May June

Selling Price 50 15000 25000

Less: Marginal Costs

Direct materials per

unit 8 2400 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Total 6400 6080

Less: Opening

inventory - 3200

Add: Closing Inventory 3200 1280

Gross Profit 11800 17000

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Fixed Production cost 4000 4000

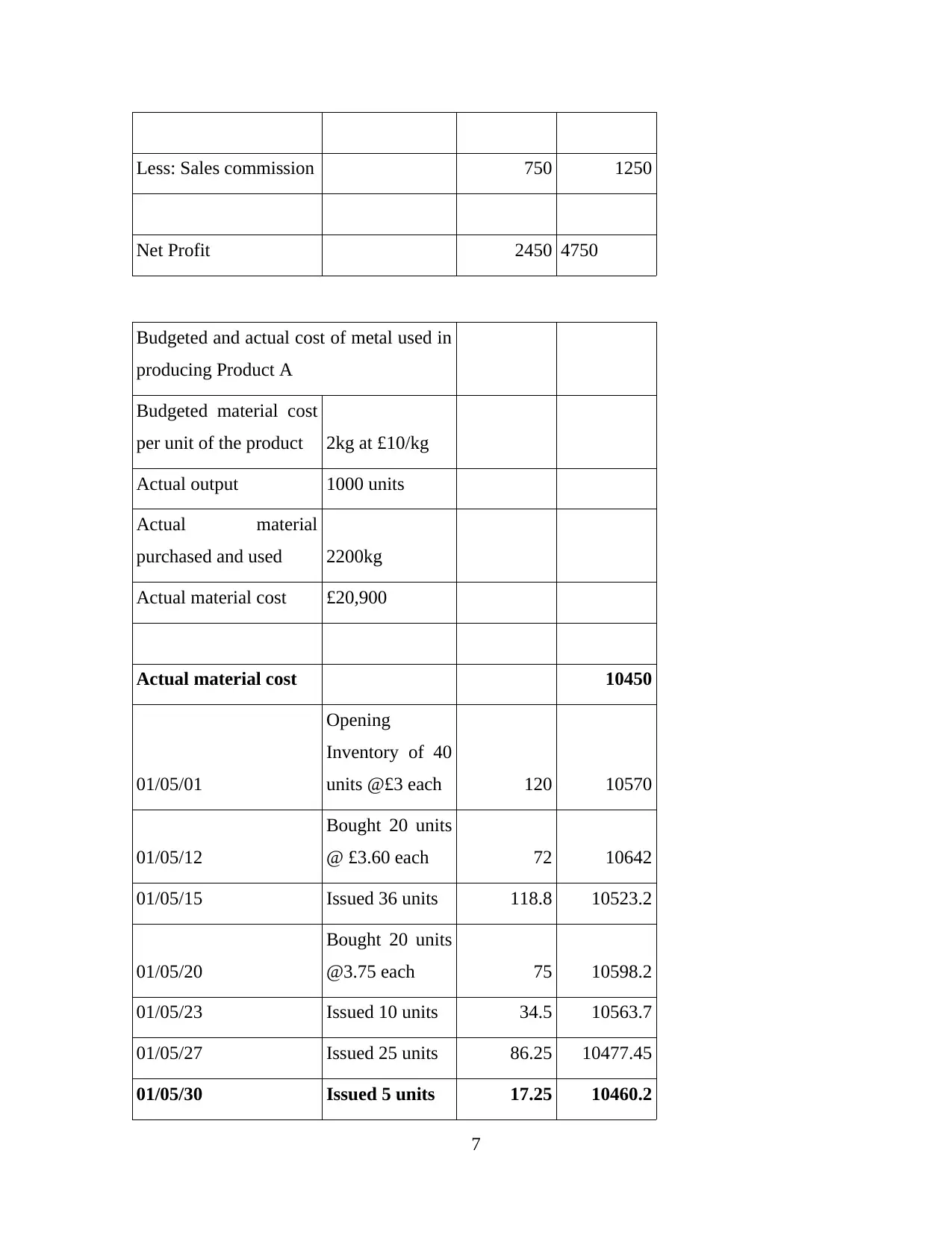

Less: Sales commission 750 1250

5

setting the final products or services costs.

May June

Selling Price 50 15000 25000

Less: Marginal Costs

Direct materials per

unit 8 2400 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Total 6400 6080

Less: Opening

inventory - 3200

Add: Closing Inventory 3200 1280

Gross Profit 11800 17000

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Fixed Production cost 4000 4000

Less: Sales commission 750 1250

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

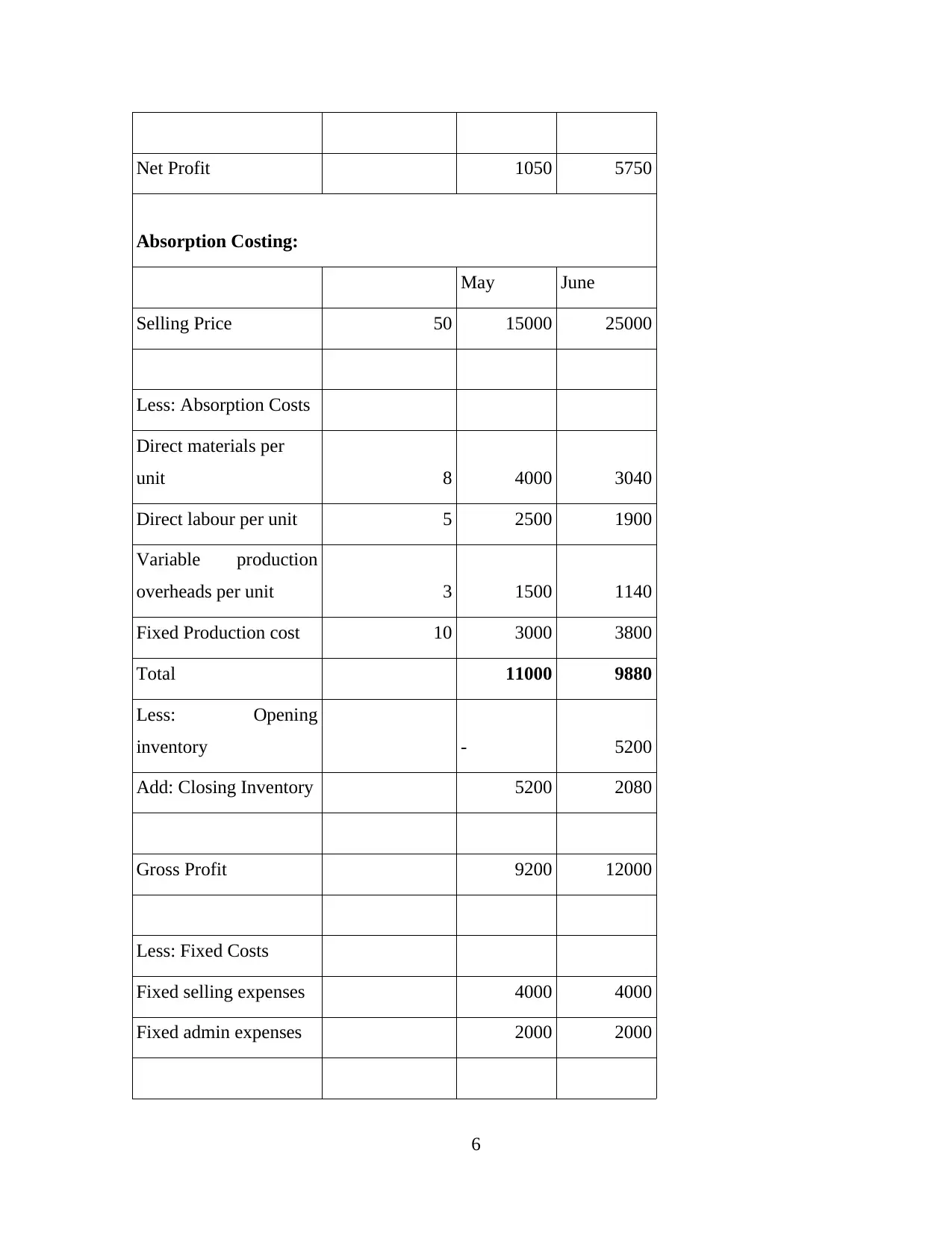

Net Profit 1050 5750

Absorption Costing:

May June

Selling Price 50 15000 25000

Less: Absorption Costs

Direct materials per

unit 8 4000 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Fixed Production cost 10 3000 3800

Total 11000 9880

Less: Opening

inventory - 5200

Add: Closing Inventory 5200 2080

Gross Profit 9200 12000

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

6

Absorption Costing:

May June

Selling Price 50 15000 25000

Less: Absorption Costs

Direct materials per

unit 8 4000 3040

Direct labour per unit 5 2500 1900

Variable production

overheads per unit 3 1500 1140

Fixed Production cost 10 3000 3800

Total 11000 9880

Less: Opening

inventory - 5200

Add: Closing Inventory 5200 2080

Gross Profit 9200 12000

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

6

Less: Sales commission 750 1250

Net Profit 2450 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Actual material cost 10450

01/05/01

Opening

Inventory of 40

units @£3 each 120 10570

01/05/12

Bought 20 units

@ £3.60 each 72 10642

01/05/15 Issued 36 units 118.8 10523.2

01/05/20

Bought 20 units

@3.75 each 75 10598.2

01/05/23 Issued 10 units 34.5 10563.7

01/05/27 Issued 25 units 86.25 10477.45

01/05/30 Issued 5 units 17.25 10460.2

7

Net Profit 2450 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Actual material cost 10450

01/05/01

Opening

Inventory of 40

units @£3 each 120 10570

01/05/12

Bought 20 units

@ £3.60 each 72 10642

01/05/15 Issued 36 units 118.8 10523.2

01/05/20

Bought 20 units

@3.75 each 75 10598.2

01/05/23 Issued 10 units 34.5 10563.7

01/05/27 Issued 25 units 86.25 10477.45

01/05/30 Issued 5 units 17.25 10460.2

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4. Advantage and disadvantage of several kinds of budgetary control planning tools.

Budget is considered as the written document that shows the financial plan in business

enterprises. This is essential for firms for preparing budget to attain the objectives. In simple

terms, budget is the rough framework of income and expenses that is required to set objectives

and develop plans consequently (Harrison and Lock, 2017). This aids Fenner Plc to to examine

the requirements as well as arranging funds for attaining objectives.

Budgetary control is considered as the systematized procedures that assists managers to

decide performance and monetary objectives with approximation as well as compare it with

actual expenditures for gaining profitability. Moreover, this means that how accountant or

managers utilise budget for observing as well as controlling operations and business cost within

accounting period. So, the managers of Fenner Plc set objective and compare it with exact

budget which aids them to control their performance of enterprises. Also, it assists them to

enhance productivity as well as profit through concentrating upon approximated and actual

budget. This includes several kinds of planning tools that are used by for controlling budget are

mentioned below:

Master Budget: This is considered as the superior business document which includes sales,

production level, capital investment and many more for determining the profit (Hutton, Lee and

Shu, 2012). Moreover, this involves several transactions data in enterprise which assists to

maintain enterprises. Fenner Plc can utilise this particular budget as this aids them to maintain

transaction in order to gain more profit as well as productivity. Advantages: This aids in maximising profit as well as productivity as this involves

overall data that is relate to the transaction of business. So, with the assistance of this

Fenner Plc can concentrate upon objectives as all the transactions are recorded

maintained properly.

Disadvantages: This particular budget is time taking as it includes various number of

transactions. It can not provide accurate outcomes as result profitability margin is low

because of having more chances fraud or errors.

8

P4. Advantage and disadvantage of several kinds of budgetary control planning tools.

Budget is considered as the written document that shows the financial plan in business

enterprises. This is essential for firms for preparing budget to attain the objectives. In simple

terms, budget is the rough framework of income and expenses that is required to set objectives

and develop plans consequently (Harrison and Lock, 2017). This aids Fenner Plc to to examine

the requirements as well as arranging funds for attaining objectives.

Budgetary control is considered as the systematized procedures that assists managers to

decide performance and monetary objectives with approximation as well as compare it with

actual expenditures for gaining profitability. Moreover, this means that how accountant or

managers utilise budget for observing as well as controlling operations and business cost within

accounting period. So, the managers of Fenner Plc set objective and compare it with exact

budget which aids them to control their performance of enterprises. Also, it assists them to

enhance productivity as well as profit through concentrating upon approximated and actual

budget. This includes several kinds of planning tools that are used by for controlling budget are

mentioned below:

Master Budget: This is considered as the superior business document which includes sales,

production level, capital investment and many more for determining the profit (Hutton, Lee and

Shu, 2012). Moreover, this involves several transactions data in enterprise which assists to

maintain enterprises. Fenner Plc can utilise this particular budget as this aids them to maintain

transaction in order to gain more profit as well as productivity. Advantages: This aids in maximising profit as well as productivity as this involves

overall data that is relate to the transaction of business. So, with the assistance of this

Fenner Plc can concentrate upon objectives as all the transactions are recorded

maintained properly.

Disadvantages: This particular budget is time taking as it includes various number of

transactions. It can not provide accurate outcomes as result profitability margin is low

because of having more chances fraud or errors.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

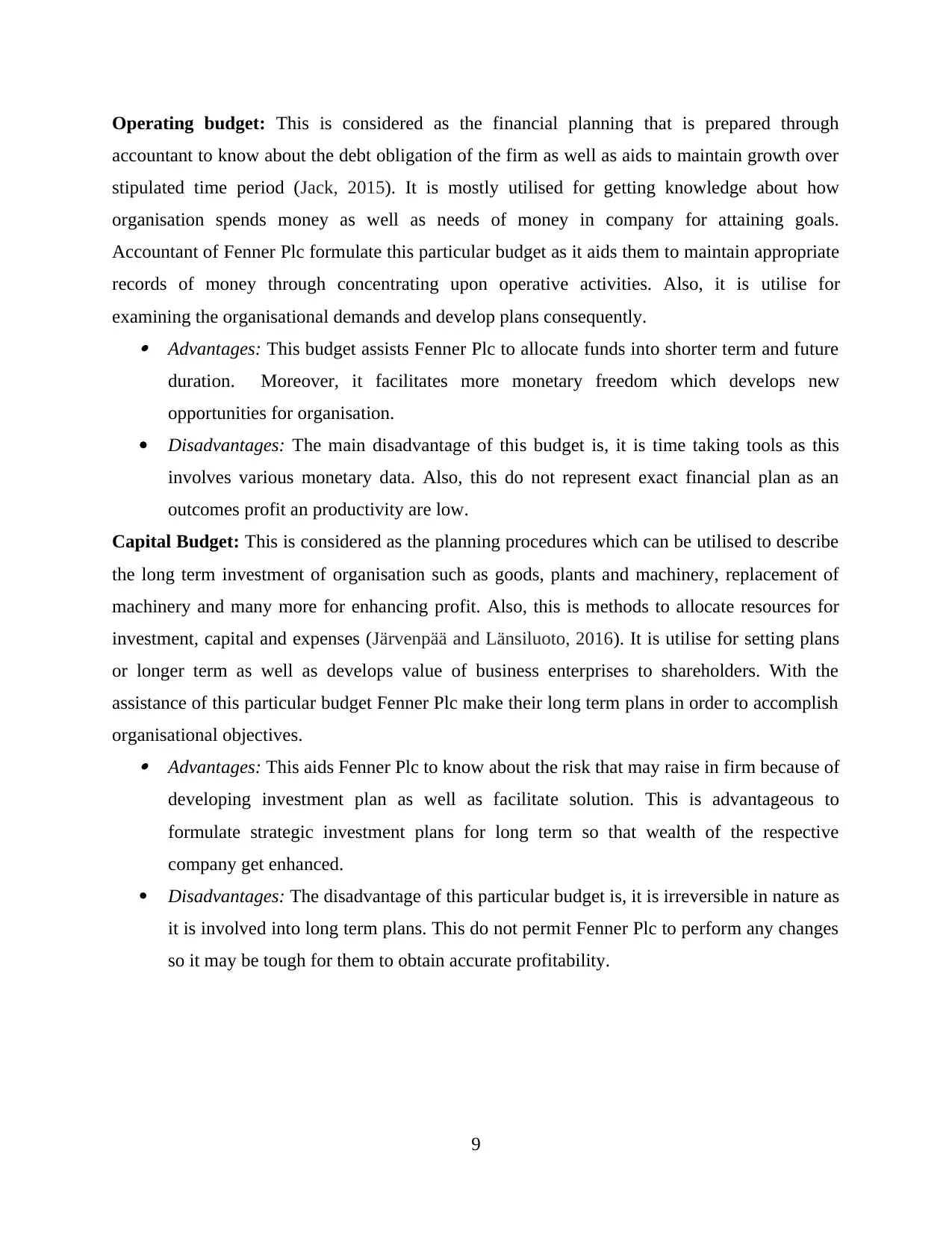

Operating budget: This is considered as the financial planning that is prepared through

accountant to know about the debt obligation of the firm as well as aids to maintain growth over

stipulated time period (Jack, 2015). It is mostly utilised for getting knowledge about how

organisation spends money as well as needs of money in company for attaining goals.

Accountant of Fenner Plc formulate this particular budget as it aids them to maintain appropriate

records of money through concentrating upon operative activities. Also, it is utilise for

examining the organisational demands and develop plans consequently. Advantages: This budget assists Fenner Plc to allocate funds into shorter term and future

duration. Moreover, it facilitates more monetary freedom which develops new

opportunities for organisation.

Disadvantages: The main disadvantage of this budget is, it is time taking tools as this

involves various monetary data. Also, this do not represent exact financial plan as an

outcomes profit an productivity are low.

Capital Budget: This is considered as the planning procedures which can be utilised to describe

the long term investment of organisation such as goods, plants and machinery, replacement of

machinery and many more for enhancing profit. Also, this is methods to allocate resources for

investment, capital and expenses (Järvenpää and Länsiluoto, 2016). It is utilise for setting plans

or longer term as well as develops value of business enterprises to shareholders. With the

assistance of this particular budget Fenner Plc make their long term plans in order to accomplish

organisational objectives. Advantages: This aids Fenner Plc to know about the risk that may raise in firm because of

developing investment plan as well as facilitate solution. This is advantageous to

formulate strategic investment plans for long term so that wealth of the respective

company get enhanced.

Disadvantages: The disadvantage of this particular budget is, it is irreversible in nature as

it is involved into long term plans. This do not permit Fenner Plc to perform any changes

so it may be tough for them to obtain accurate profitability.

9

accountant to know about the debt obligation of the firm as well as aids to maintain growth over

stipulated time period (Jack, 2015). It is mostly utilised for getting knowledge about how

organisation spends money as well as needs of money in company for attaining goals.

Accountant of Fenner Plc formulate this particular budget as it aids them to maintain appropriate

records of money through concentrating upon operative activities. Also, it is utilise for

examining the organisational demands and develop plans consequently. Advantages: This budget assists Fenner Plc to allocate funds into shorter term and future

duration. Moreover, it facilitates more monetary freedom which develops new

opportunities for organisation.

Disadvantages: The main disadvantage of this budget is, it is time taking tools as this

involves various monetary data. Also, this do not represent exact financial plan as an

outcomes profit an productivity are low.

Capital Budget: This is considered as the planning procedures which can be utilised to describe

the long term investment of organisation such as goods, plants and machinery, replacement of

machinery and many more for enhancing profit. Also, this is methods to allocate resources for

investment, capital and expenses (Järvenpää and Länsiluoto, 2016). It is utilise for setting plans

or longer term as well as develops value of business enterprises to shareholders. With the

assistance of this particular budget Fenner Plc make their long term plans in order to accomplish

organisational objectives. Advantages: This aids Fenner Plc to know about the risk that may raise in firm because of

developing investment plan as well as facilitate solution. This is advantageous to

formulate strategic investment plans for long term so that wealth of the respective

company get enhanced.

Disadvantages: The disadvantage of this particular budget is, it is irreversible in nature as

it is involved into long term plans. This do not permit Fenner Plc to perform any changes

so it may be tough for them to obtain accurate profitability.

9

TASK 4

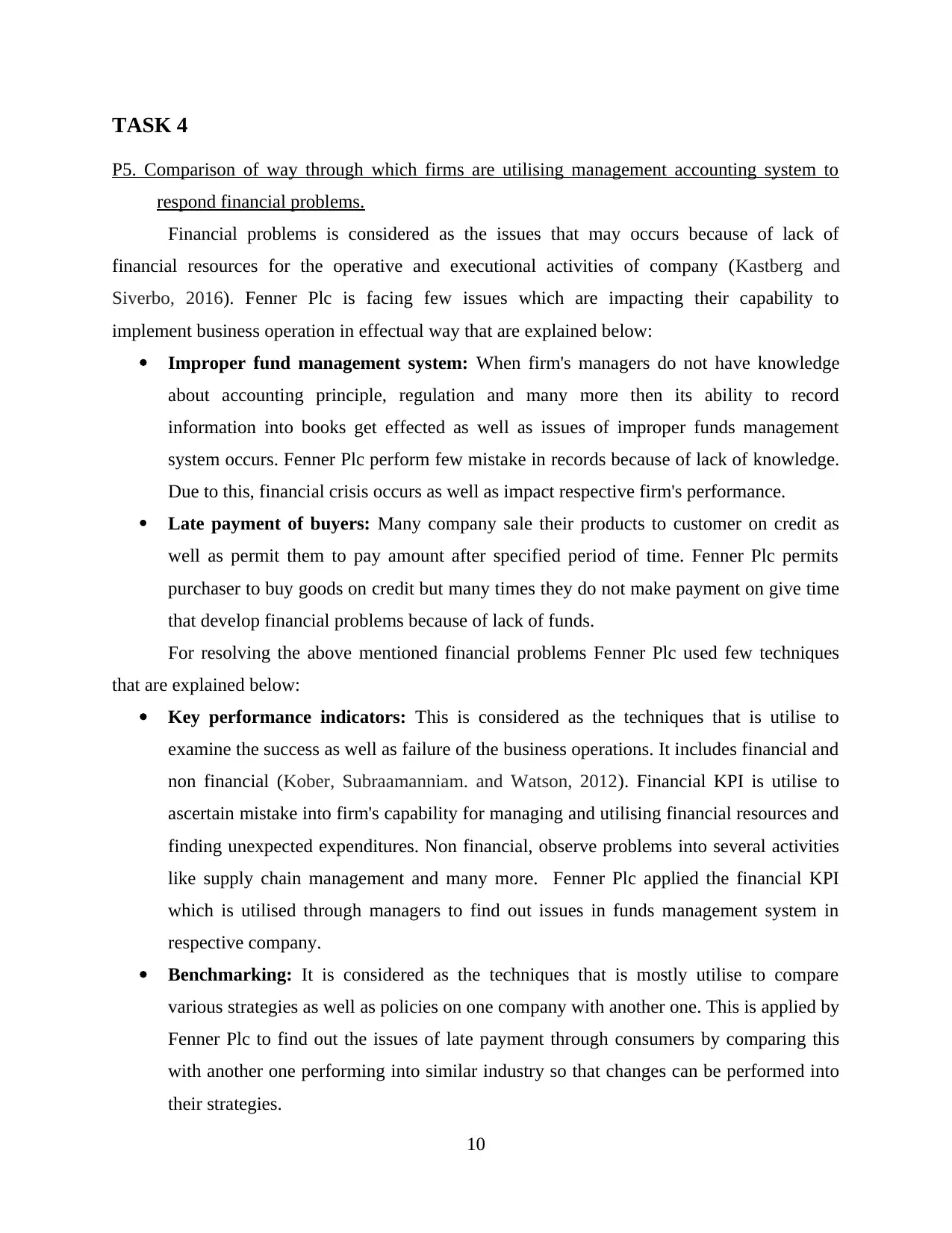

P5. Comparison of way through which firms are utilising management accounting system to

respond financial problems.

Financial problems is considered as the issues that may occurs because of lack of

financial resources for the operative and executional activities of company (Kastberg and

Siverbo, 2016). Fenner Plc is facing few issues which are impacting their capability to

implement business operation in effectual way that are explained below:

Improper fund management system: When firm's managers do not have knowledge

about accounting principle, regulation and many more then its ability to record

information into books get effected as well as issues of improper funds management

system occurs. Fenner Plc perform few mistake in records because of lack of knowledge.

Due to this, financial crisis occurs as well as impact respective firm's performance.

Late payment of buyers: Many company sale their products to customer on credit as

well as permit them to pay amount after specified period of time. Fenner Plc permits

purchaser to buy goods on credit but many times they do not make payment on give time

that develop financial problems because of lack of funds.

For resolving the above mentioned financial problems Fenner Plc used few techniques

that are explained below:

Key performance indicators: This is considered as the techniques that is utilise to

examine the success as well as failure of the business operations. It includes financial and

non financial (Kober, Subraamanniam. and Watson, 2012). Financial KPI is utilise to

ascertain mistake into firm's capability for managing and utilising financial resources and

finding unexpected expenditures. Non financial, observe problems into several activities

like supply chain management and many more. Fenner Plc applied the financial KPI

which is utilised through managers to find out issues in funds management system in

respective company.

Benchmarking: It is considered as the techniques that is mostly utilise to compare

various strategies as well as policies on one company with another one. This is applied by

Fenner Plc to find out the issues of late payment through consumers by comparing this

with another one performing into similar industry so that changes can be performed into

their strategies.

10

P5. Comparison of way through which firms are utilising management accounting system to

respond financial problems.

Financial problems is considered as the issues that may occurs because of lack of

financial resources for the operative and executional activities of company (Kastberg and

Siverbo, 2016). Fenner Plc is facing few issues which are impacting their capability to

implement business operation in effectual way that are explained below:

Improper fund management system: When firm's managers do not have knowledge

about accounting principle, regulation and many more then its ability to record

information into books get effected as well as issues of improper funds management

system occurs. Fenner Plc perform few mistake in records because of lack of knowledge.

Due to this, financial crisis occurs as well as impact respective firm's performance.

Late payment of buyers: Many company sale their products to customer on credit as

well as permit them to pay amount after specified period of time. Fenner Plc permits

purchaser to buy goods on credit but many times they do not make payment on give time

that develop financial problems because of lack of funds.

For resolving the above mentioned financial problems Fenner Plc used few techniques

that are explained below:

Key performance indicators: This is considered as the techniques that is utilise to

examine the success as well as failure of the business operations. It includes financial and

non financial (Kober, Subraamanniam. and Watson, 2012). Financial KPI is utilise to

ascertain mistake into firm's capability for managing and utilising financial resources and

finding unexpected expenditures. Non financial, observe problems into several activities

like supply chain management and many more. Fenner Plc applied the financial KPI

which is utilised through managers to find out issues in funds management system in

respective company.

Benchmarking: It is considered as the techniques that is mostly utilise to compare

various strategies as well as policies on one company with another one. This is applied by

Fenner Plc to find out the issues of late payment through consumers by comparing this

with another one performing into similar industry so that changes can be performed into

their strategies.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.