Management Accounting Report: Financial Analysis of Trust Ford

VerifiedAdded on 2021/02/19

|17

|5288

|62

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the case of Trust Ford, a UK-based medium-sized retail company. It begins by defining management accounting and exploring various systems, including inventory management, cost accounting, job order costing, and price optimization. The report delves into different types of management accounting reports, such as budget reports, performance reports, accounts receivable aging reports, and inventory management reports. It highlights the benefits of these systems for Trust Ford, including cost savings, flexibility, and improved pricing strategies. Furthermore, the report examines the integration of management accounting systems with reporting, emphasizing how these elements work together to provide valuable financial insights. The report also explores costing techniques to calculate profit, planning tools for budgetary control, and the use of management accounting systems to address financial problems, ultimately leading organizations towards sustainable success. Finally, the report concludes with a summary of the key findings and their implications for the company's financial health and strategic decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and different types of system:........................................................3

P2 Management accounting reports and types:...........................................................................5

M1 Benefits of management accounting systems:.......................................................................6

D1 Integration of management accounting system with reporting:.............................................7

TASK 2............................................................................................................................................8

P3 & D3 Costing technique used to calculate profit with its interpretation:...............................8

M2 Application of management accounting techniques:...........................................................11

TASK 3..........................................................................................................................................11

P4 Planning tools used for budgetary control:...........................................................................11

M3 Use of planning tools and their application for preparing and forecasting budgets:...........13

TASK 4..........................................................................................................................................14

P5. Management accounting systems to respond to financial problems:..................................14

M4 Management accounting leads organisations to gain sustainable success:.........................16

D3 Planning tools to solve financial problems to lead organisations to sustainable success:...16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and different types of system:........................................................3

P2 Management accounting reports and types:...........................................................................5

M1 Benefits of management accounting systems:.......................................................................6

D1 Integration of management accounting system with reporting:.............................................7

TASK 2............................................................................................................................................8

P3 & D3 Costing technique used to calculate profit with its interpretation:...............................8

M2 Application of management accounting techniques:...........................................................11

TASK 3..........................................................................................................................................11

P4 Planning tools used for budgetary control:...........................................................................11

M3 Use of planning tools and their application for preparing and forecasting budgets:...........13

TASK 4..........................................................................................................................................14

P5. Management accounting systems to respond to financial problems:..................................14

M4 Management accounting leads organisations to gain sustainable success:.........................16

D3 Planning tools to solve financial problems to lead organisations to sustainable success:...16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is a process of preparing management reports and accounting

records that provide accurate, relevant, timely etc. financial & statistical information. It is

required by managers to make short as well as long term decisions. This is a strategic tool which

helps the directors in taking effective decisions regarding different activities of an organisation.

It is a provision of financial data & advice to a company that is used by firms to develop the

business (Management accounting, 2019). With the use of this tool a firm can improve its

liquidity and profitability position. Also, it can provide monetary benefits to employees on the

basis of their performance. For this report, Trust Ford has been selected which is owned by Ford

Motor Company and is a UK based medium sized retail company that sell new and used cars.

This report outlines on different types of management accounting system and reports

used by managers to assess performance of company (Ainsworth and Deines, 2019). It also uses

costing techniques to estimate net profit during an accounting year. The below document also

consider techniques in which organisations adapt management accounting system to resolve

financial problems.

TASK 1

P1 Management accounting and different types of system:

Management accounting: This can be defined as an application of applying professional

skill, knowledge in the preparation of financial statements. It is a practice of distinguishing,

measuring, examining, explaining, communicating information to managers for the pursuit of

organisational goals and objectives. The tool helps in maintaining a balance among different

functional units of an organisation by ensuring that targets & objectives have been achieved.

There is a requirement of analysing business cost & operations for preparing internal financial

reports which assist directors in decision-making process (Ali and et.al., 2016). Trust Ford uses

management accounting to prepare statement of accounts which help the company in evaluating

Management accounting is a process of preparing management reports and accounting

records that provide accurate, relevant, timely etc. financial & statistical information. It is

required by managers to make short as well as long term decisions. This is a strategic tool which

helps the directors in taking effective decisions regarding different activities of an organisation.

It is a provision of financial data & advice to a company that is used by firms to develop the

business (Management accounting, 2019). With the use of this tool a firm can improve its

liquidity and profitability position. Also, it can provide monetary benefits to employees on the

basis of their performance. For this report, Trust Ford has been selected which is owned by Ford

Motor Company and is a UK based medium sized retail company that sell new and used cars.

This report outlines on different types of management accounting system and reports

used by managers to assess performance of company (Ainsworth and Deines, 2019). It also uses

costing techniques to estimate net profit during an accounting year. The below document also

consider techniques in which organisations adapt management accounting system to resolve

financial problems.

TASK 1

P1 Management accounting and different types of system:

Management accounting: This can be defined as an application of applying professional

skill, knowledge in the preparation of financial statements. It is a practice of distinguishing,

measuring, examining, explaining, communicating information to managers for the pursuit of

organisational goals and objectives. The tool helps in maintaining a balance among different

functional units of an organisation by ensuring that targets & objectives have been achieved.

There is a requirement of analysing business cost & operations for preparing internal financial

reports which assist directors in decision-making process (Ali and et.al., 2016). Trust Ford uses

management accounting to prepare statement of accounts which help the company in evaluating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance of staff members. It also aids Trust Ford in interpreting conduct of used cars by

client feedback.

Management accounting systems: This can be defined as a system which records all the

activities, functions performed by an organisation. It consists of internal systems that a company

uses to measure and evaluate its processes by fulfilling organisational goals & objectives. There

is always a requirement of tracking inventory so it does not get finished, allocating cost to

various functional units, optimising price levels by choosing the appropriate pricing strategy etc.

Trust Ford exercises management accounting system to maintain quality of its new & used cars

by repair & maintenance of parts. The company also believes in providing best quality vehicles

to the customers so uses reliable oil & equipment which are free from any defect.

Inventory management system: It refers to a system which carries information about

how much goods are present at the warehouse. To optimize inventory levels, companies use

different software to record stock like Tally ERP that gives an updated information about how

much/when goods are needed. With the help of inventory management system, managers are not

required to order excess levels of stock (Atrill, McLaney and Harvey, 2014). Also, valuation

methods are used to track stock levels i.e. LIFO- Last in, first out system records inventory that

is recently produced by selling it first. FIFO- First in, first out method records asset which is

produced or acquired first by selling or disposing it first. Weighted average cost method- This

method uses weighted-average of all inventory purchased during a period to assign value to cost

of goods sold (COGS) as well as those which are still available for sale.

Trust Ford values its inventory by using FIFO method as the cars that are acquired or

produced first are the first ones that are sold to the customer. It helps the company in tracking

down the number of cars easily by following the above mentioned costing method.

Cost accounting system: It is a method that aims to capture a company's cost at each

level of production i.e. direct material, labour overhead. This can be classified further into fixed

& variable cost. Trust Ford values its cars as per variable cost because that can change according

to bargaining power of the customer. However, price of equipments like tyres, accessories, seat

covers remain fixed throughout (Boden and Yassia Paul, 2014). There is a severe requirement of

cost accounting system in Trust Ford as company offers a fixed percentage of cash discount on

used cars. Since they are old driven vehicles, the company can offer some trade discount on

client feedback.

Management accounting systems: This can be defined as a system which records all the

activities, functions performed by an organisation. It consists of internal systems that a company

uses to measure and evaluate its processes by fulfilling organisational goals & objectives. There

is always a requirement of tracking inventory so it does not get finished, allocating cost to

various functional units, optimising price levels by choosing the appropriate pricing strategy etc.

Trust Ford exercises management accounting system to maintain quality of its new & used cars

by repair & maintenance of parts. The company also believes in providing best quality vehicles

to the customers so uses reliable oil & equipment which are free from any defect.

Inventory management system: It refers to a system which carries information about

how much goods are present at the warehouse. To optimize inventory levels, companies use

different software to record stock like Tally ERP that gives an updated information about how

much/when goods are needed. With the help of inventory management system, managers are not

required to order excess levels of stock (Atrill, McLaney and Harvey, 2014). Also, valuation

methods are used to track stock levels i.e. LIFO- Last in, first out system records inventory that

is recently produced by selling it first. FIFO- First in, first out method records asset which is

produced or acquired first by selling or disposing it first. Weighted average cost method- This

method uses weighted-average of all inventory purchased during a period to assign value to cost

of goods sold (COGS) as well as those which are still available for sale.

Trust Ford values its inventory by using FIFO method as the cars that are acquired or

produced first are the first ones that are sold to the customer. It helps the company in tracking

down the number of cars easily by following the above mentioned costing method.

Cost accounting system: It is a method that aims to capture a company's cost at each

level of production i.e. direct material, labour overhead. This can be classified further into fixed

& variable cost. Trust Ford values its cars as per variable cost because that can change according

to bargaining power of the customer. However, price of equipments like tyres, accessories, seat

covers remain fixed throughout (Boden and Yassia Paul, 2014). There is a severe requirement of

cost accounting system in Trust Ford as company offers a fixed percentage of cash discount on

used cars. Since they are old driven vehicles, the company can offer some trade discount on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

those which are not in high demand. By following cost accounting system, Trust Ford can

maintain its liquidity as well as profitability position.

Job order costing system: This is defined as a system which is used to record different

activities related to an organisation. It uses job cost sheets, overhead costs to track production

activities at a job. The managers of Trust Ford interprets and considers various needs and

requirement of the client and make changes in the cars accordingly. It can be choice of number

plate, fog lamp, colour & model of car etc. There is a requirement of job order costing system as

it helps is estimating cost of each product as well as service offered by the company.

Management team of Trust Ford designs & develops minor specifications as per want and desire

of the client.

Price optimisation system: It is a technique which uses different pricing strategies to

evaluate cost of products & services like penetration, price skimming, complementary etc. This

includes use of mathematical analysis by a company to determine consumer response on its

goods. It also considers impact of demand & supply factors by which value of goods can be

determined. The managers are required to predict behaviour of potential buyers to different

prices of products. In Trust Ford, price optimisation system is used to get an estimate of used

cars in terms of how many kilometres it has driven, if there are any dents or scratches on the

external body of vehicle etc.

P2 Management accounting reports and types:

Management accounting reporting: It is a process of reporting where forecasts are

prepared by internal management for estimating income & expenses during an accounting year.

This involves analysing, interpreting, evaluating different set of reports for identifying cash

expenses and defaulters etc. in an organisation which are produced by higher authorities. These

are required to carry financial information related to a company's business transactions. In Trust

Ford, management accounting reports are prepared to track inventory of cars which are in high

demand while stocking up those that are not available at the store (Boyns, Anderson and

Edwards, 2014).

Budget report: It is a report which is used to estimate earnings & expenditure of an

organisation during the forthcoming year. This involves assigning & allocating finances to

different functional units in a firm by which they can perform several activities on a day-to-day

basis. The managers are required to compare actual figures with budgeted data while evaluating

maintain its liquidity as well as profitability position.

Job order costing system: This is defined as a system which is used to record different

activities related to an organisation. It uses job cost sheets, overhead costs to track production

activities at a job. The managers of Trust Ford interprets and considers various needs and

requirement of the client and make changes in the cars accordingly. It can be choice of number

plate, fog lamp, colour & model of car etc. There is a requirement of job order costing system as

it helps is estimating cost of each product as well as service offered by the company.

Management team of Trust Ford designs & develops minor specifications as per want and desire

of the client.

Price optimisation system: It is a technique which uses different pricing strategies to

evaluate cost of products & services like penetration, price skimming, complementary etc. This

includes use of mathematical analysis by a company to determine consumer response on its

goods. It also considers impact of demand & supply factors by which value of goods can be

determined. The managers are required to predict behaviour of potential buyers to different

prices of products. In Trust Ford, price optimisation system is used to get an estimate of used

cars in terms of how many kilometres it has driven, if there are any dents or scratches on the

external body of vehicle etc.

P2 Management accounting reports and types:

Management accounting reporting: It is a process of reporting where forecasts are

prepared by internal management for estimating income & expenses during an accounting year.

This involves analysing, interpreting, evaluating different set of reports for identifying cash

expenses and defaulters etc. in an organisation which are produced by higher authorities. These

are required to carry financial information related to a company's business transactions. In Trust

Ford, management accounting reports are prepared to track inventory of cars which are in high

demand while stocking up those that are not available at the store (Boyns, Anderson and

Edwards, 2014).

Budget report: It is a report which is used to estimate earnings & expenditure of an

organisation during the forthcoming year. This involves assigning & allocating finances to

different functional units in a firm by which they can perform several activities on a day-to-day

basis. The managers are required to compare actual figures with budgeted data while evaluating

spending power of each department. Trust Ford assigns limited funds to the workers for repair &

maintenance of old vehicles. The company prepares budget report so that any extra expenses are

not incurred on used cars as if that is the case then the vehicle is disposed off.

Performance report: This is a report which addresses performance outcome of any

activity or work done by the employees at an organisation. With the help of this, managers are

able to achieve organisational targets & objectives for the overall development of a company. It

is required to assess as well as evaluate conduct of workers by providing them with additional

benefits which can motivate them into giving better results. Trust Ford measures performance of

vehicles with the help of this report. The company can also evaluate it by customer experience

with the used cars which can help to attain a high market share.

Accounts receivable aging report: It is a report which records outstanding amount owed

by customers and the duration of time in which they pay it. This report tracks amount of money

that is owed from a debtor by calculating accounts receivable collection period as it gives an idea

about the number of days remaining with the consumer. It is required by management for

providing extended credit policies to defaulters so they are able to pay before time. Trust Ford

prepares accounts receivable aging report to analyse its debtors which may arise during an

accounting year. The managers of the company ensures that bad debts are recovered by offering

them some cash benefits which will help to improve the liquidity position (Chambers, 2014)

(Choi, Mao and Upadhyay, 2014).

Inventory management report: It is a report which is used by management to record,

track inventory at the warehouse. This ensures that proper stock count has been done so that it

remains available when the need arises. It also involves calculation of inventory turnover period

which checks the duration of time in which goods should be ordered. Managers are required to

order & stock up raw material or equipment before lead time to avoid stock-outs. With the help

of inventory management report, Trust Ford makes sure that the cars which are in high demand

should be available at the workshop especially during festive time. The company first evaluates

if any parts or equipment are needed in updating the vehicles and then places order from

suppliers.

M1 Benefits of management accounting systems:

Management accounting system Benefits

maintenance of old vehicles. The company prepares budget report so that any extra expenses are

not incurred on used cars as if that is the case then the vehicle is disposed off.

Performance report: This is a report which addresses performance outcome of any

activity or work done by the employees at an organisation. With the help of this, managers are

able to achieve organisational targets & objectives for the overall development of a company. It

is required to assess as well as evaluate conduct of workers by providing them with additional

benefits which can motivate them into giving better results. Trust Ford measures performance of

vehicles with the help of this report. The company can also evaluate it by customer experience

with the used cars which can help to attain a high market share.

Accounts receivable aging report: It is a report which records outstanding amount owed

by customers and the duration of time in which they pay it. This report tracks amount of money

that is owed from a debtor by calculating accounts receivable collection period as it gives an idea

about the number of days remaining with the consumer. It is required by management for

providing extended credit policies to defaulters so they are able to pay before time. Trust Ford

prepares accounts receivable aging report to analyse its debtors which may arise during an

accounting year. The managers of the company ensures that bad debts are recovered by offering

them some cash benefits which will help to improve the liquidity position (Chambers, 2014)

(Choi, Mao and Upadhyay, 2014).

Inventory management report: It is a report which is used by management to record,

track inventory at the warehouse. This ensures that proper stock count has been done so that it

remains available when the need arises. It also involves calculation of inventory turnover period

which checks the duration of time in which goods should be ordered. Managers are required to

order & stock up raw material or equipment before lead time to avoid stock-outs. With the help

of inventory management report, Trust Ford makes sure that the cars which are in high demand

should be available at the workshop especially during festive time. The company first evaluates

if any parts or equipment are needed in updating the vehicles and then places order from

suppliers.

M1 Benefits of management accounting systems:

Management accounting system Benefits

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system Inventory management system is applied in Trust Ford

as it helps in saving cost by ordering cars from the

factory before lead time. It also help the managers in

tracking down the goods by use of different inventory

management software like barcode readers, Tally ERP

etc.

Job order costing system Job order costing system is used by Trust Ford to

maintain flexibility, accuracy in determining cost for

cars. It is beneficial in identifying any needs or

requirements of the customer in designing the vehicle

which can be a particular number plate or colour of

vehicle (Sugahara, Daidj and Ushio, 2017).

Price optimisation system It helps in optimising price levels with the use of

different pricing strategies like penetration,

complementary etc. Price optimisation system is applied

by Trust Ford in analysing customer responses on price

of cars set by the company.

Cost accounting system Cost accounting system is used by Trust Ford to analyse

liquidity and profitability position of income &

expenditure. It also helps it appointing high skilled

labour who can design or develop any up-gradations

required in the cars.

D1 Integration of management accounting system with reporting:

Both management accounting system and reporting are integrated with each other in such

a way that a need of one affects in the preparation of another. The inventory management system

ensures that proper stock count is done at the warehouse to avoid any stock-outs whereas

inventory management report tracks down the goods when they are shipped from the place of

manufacturing till thy are delivered to the customer. On the other hand, job order costing ensures

that products are made as per needs and requirements of the client (Collis, Holt and Hussey,

as it helps in saving cost by ordering cars from the

factory before lead time. It also help the managers in

tracking down the goods by use of different inventory

management software like barcode readers, Tally ERP

etc.

Job order costing system Job order costing system is used by Trust Ford to

maintain flexibility, accuracy in determining cost for

cars. It is beneficial in identifying any needs or

requirements of the customer in designing the vehicle

which can be a particular number plate or colour of

vehicle (Sugahara, Daidj and Ushio, 2017).

Price optimisation system It helps in optimising price levels with the use of

different pricing strategies like penetration,

complementary etc. Price optimisation system is applied

by Trust Ford in analysing customer responses on price

of cars set by the company.

Cost accounting system Cost accounting system is used by Trust Ford to analyse

liquidity and profitability position of income &

expenditure. It also helps it appointing high skilled

labour who can design or develop any up-gradations

required in the cars.

D1 Integration of management accounting system with reporting:

Both management accounting system and reporting are integrated with each other in such

a way that a need of one affects in the preparation of another. The inventory management system

ensures that proper stock count is done at the warehouse to avoid any stock-outs whereas

inventory management report tracks down the goods when they are shipped from the place of

manufacturing till thy are delivered to the customer. On the other hand, job order costing ensures

that products are made as per needs and requirements of the client (Collis, Holt and Hussey,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017). In relation to this, Trust Ford makes changes in its used or new cars according to the

specifications given by the consumer. It can be a particular number plate, colour or model of a

car etc. For this purpose, the company allocates limited funds to the workers with the help of

budget report.

TASK 2

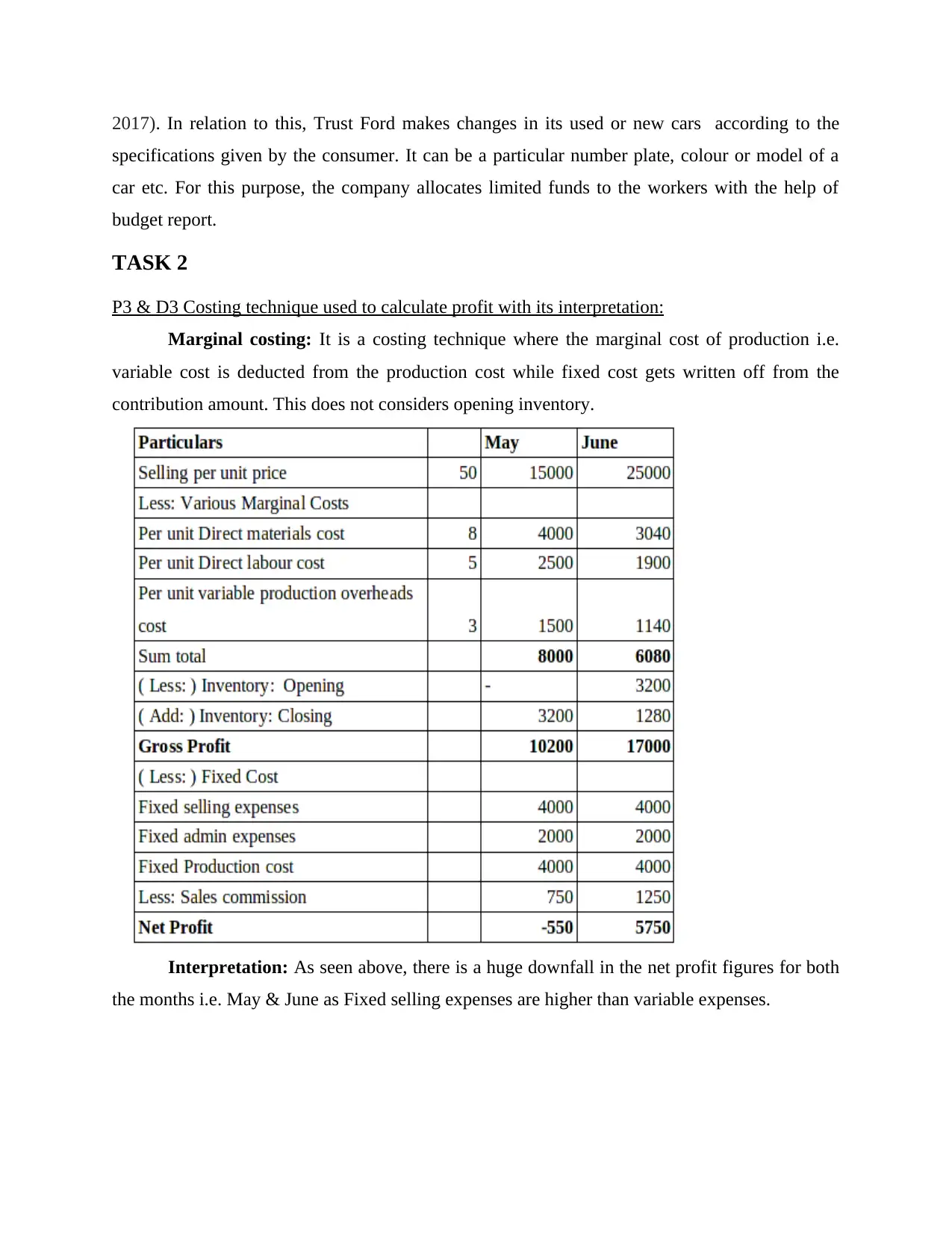

P3 & D3 Costing technique used to calculate profit with its interpretation:

Marginal costing: It is a costing technique where the marginal cost of production i.e.

variable cost is deducted from the production cost while fixed cost gets written off from the

contribution amount. This does not considers opening inventory.

Interpretation: As seen above, there is a huge downfall in the net profit figures for both

the months i.e. May & June as Fixed selling expenses are higher than variable expenses.

specifications given by the consumer. It can be a particular number plate, colour or model of a

car etc. For this purpose, the company allocates limited funds to the workers with the help of

budget report.

TASK 2

P3 & D3 Costing technique used to calculate profit with its interpretation:

Marginal costing: It is a costing technique where the marginal cost of production i.e.

variable cost is deducted from the production cost while fixed cost gets written off from the

contribution amount. This does not considers opening inventory.

Interpretation: As seen above, there is a huge downfall in the net profit figures for both

the months i.e. May & June as Fixed selling expenses are higher than variable expenses.

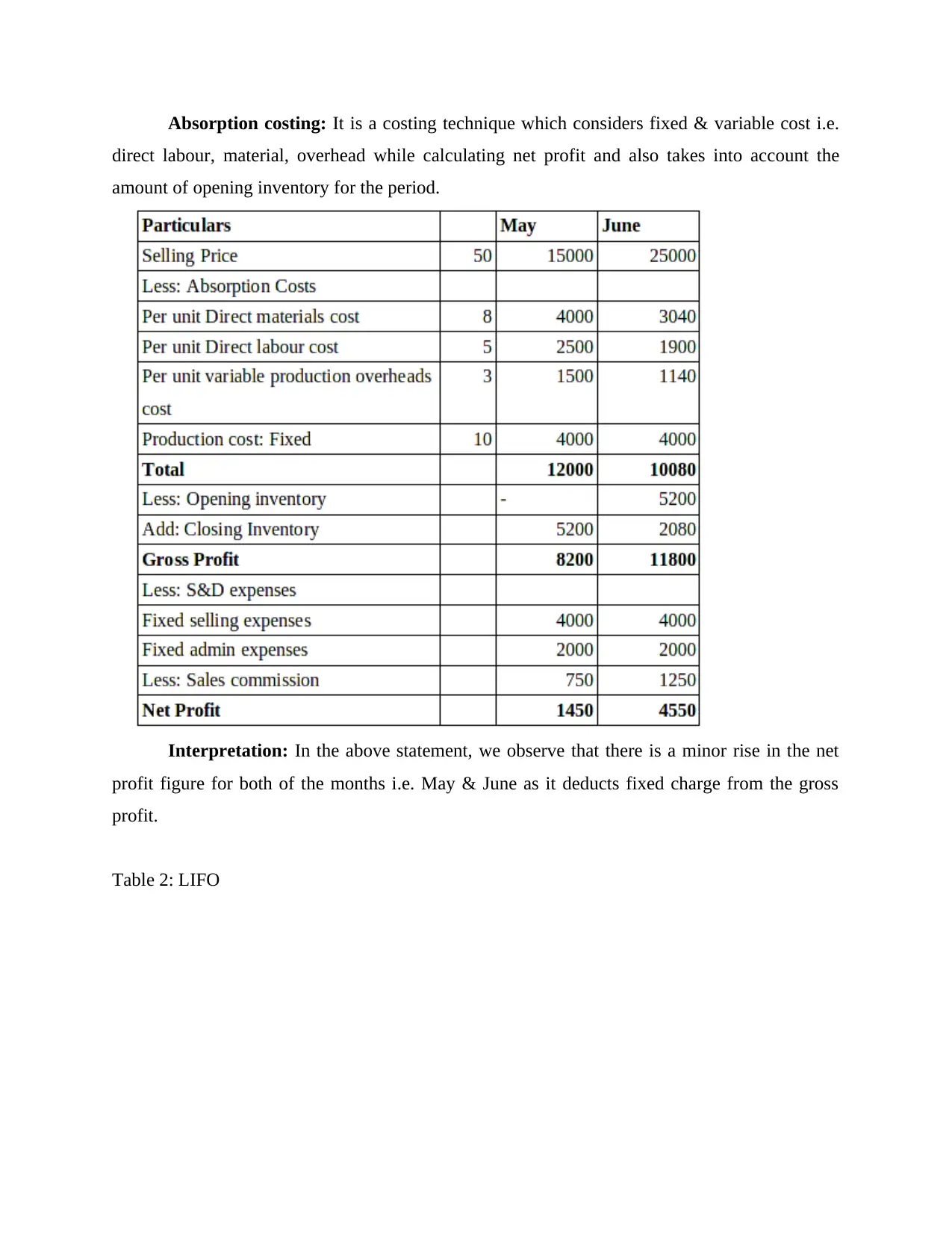

Absorption costing: It is a costing technique which considers fixed & variable cost i.e.

direct labour, material, overhead while calculating net profit and also takes into account the

amount of opening inventory for the period.

Interpretation: In the above statement, we observe that there is a minor rise in the net

profit figure for both of the months i.e. May & June as it deducts fixed charge from the gross

profit.

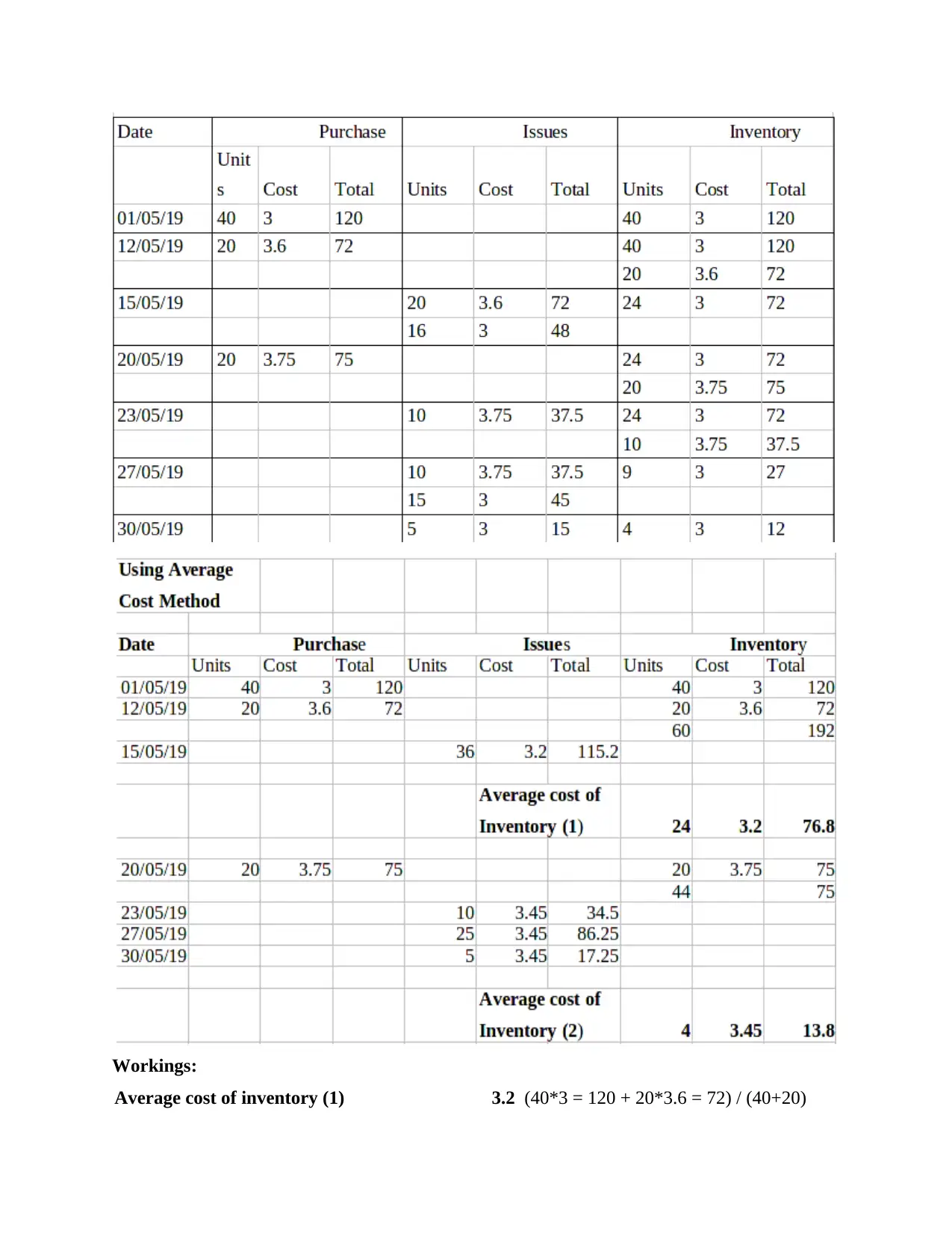

Table 2: LIFO

direct labour, material, overhead while calculating net profit and also takes into account the

amount of opening inventory for the period.

Interpretation: In the above statement, we observe that there is a minor rise in the net

profit figure for both of the months i.e. May & June as it deducts fixed charge from the gross

profit.

Table 2: LIFO

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Workings:

Average cost of inventory (1) 3.2 (40*3 = 120 + 20*3.6 = 72) / (40+20)

Average cost of inventory (1) 3.2 (40*3 = 120 + 20*3.6 = 72) / (40+20)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Average cost of inventory (2) 3.45 (24*3.2 = 76.8 + 20*3.75 = 75) / (20+24)

M2 Application of management accounting techniques:

Normal costing: It is a costing technique by which cost for a product can be determined.

In this approach, direct cost as well as standard overhead rate is applied.

Standard costing: It is a costing technique which substitutes an expected cost for actual

output. This includes calculation of different type of variances.

TASK 3

P4 Planning tools used for budgetary control:

Budget: A budget can be described as a list of estimated revenues as well as estimated

expenditures for a specific time period which is generally a financial year. Budget is a tool that

helps the managers in setting organizational objectives and goals. This tool is used for measuring

outcomes and planning contingencies hence it provides help in operating at highest efficiency.

Budgets are the planning tools which are used in budgetary control process.

Budgetary Control: Budgetary control is a controlling process that utilize various

estimated budgets in order to compare them with actual outcomes so that variances can be find

out. Variances may be adverse or favourable in nature. Further this process includes to find out

reasons behind variances and planning and implementing remedial activities for reducing the

unfavourable situations accordingly. It also examine if estimations are corrupted or wrongly

estimated. The internal management of TrustFord prepares various budgets and follows

budgetary control techniques so that planning and decision making process can be developed for

objectives and goals. Some of the budgets that are generated by the administration defined as

under:

Sales Budget: Sales budget is an estimation of sale of the products during a particular

time in both the units and the value terms (Gago and Macias, 2014). This budget is also

connected with determining appropriate estimated profits after the pre-determined time period.

The sales management team of TrustFord research on and analyse previous year sale, market

competition, economic condition, product quality, selling expenses and customers need before

planning and estimating sales for specific time period. It also assist the management to derive

M2 Application of management accounting techniques:

Normal costing: It is a costing technique by which cost for a product can be determined.

In this approach, direct cost as well as standard overhead rate is applied.

Standard costing: It is a costing technique which substitutes an expected cost for actual

output. This includes calculation of different type of variances.

TASK 3

P4 Planning tools used for budgetary control:

Budget: A budget can be described as a list of estimated revenues as well as estimated

expenditures for a specific time period which is generally a financial year. Budget is a tool that

helps the managers in setting organizational objectives and goals. This tool is used for measuring

outcomes and planning contingencies hence it provides help in operating at highest efficiency.

Budgets are the planning tools which are used in budgetary control process.

Budgetary Control: Budgetary control is a controlling process that utilize various

estimated budgets in order to compare them with actual outcomes so that variances can be find

out. Variances may be adverse or favourable in nature. Further this process includes to find out

reasons behind variances and planning and implementing remedial activities for reducing the

unfavourable situations accordingly. It also examine if estimations are corrupted or wrongly

estimated. The internal management of TrustFord prepares various budgets and follows

budgetary control techniques so that planning and decision making process can be developed for

objectives and goals. Some of the budgets that are generated by the administration defined as

under:

Sales Budget: Sales budget is an estimation of sale of the products during a particular

time in both the units and the value terms (Gago and Macias, 2014). This budget is also

connected with determining appropriate estimated profits after the pre-determined time period.

The sales management team of TrustFord research on and analyse previous year sale, market

competition, economic condition, product quality, selling expenses and customers need before

planning and estimating sales for specific time period. It also assist the management to derive

profitability of the establishment. This budget has its own merits and demerits which have to be

bared by respective firm:

Advantages:

Sales budget is helpful in controlling costs and expenditures so that desired profit can be

achieved.

This budget helps in finding out the areas or products which needs to be updated or

improved.

Disadvantages:

The biggest disadvantage of sales budget is that it is unable to forecast future sales and

other estimates effectively.

Generally sales budget eliminates the estimation of that expenditures which takes long

time in revenue generation.

Flexible Budget: A flexible budget is a technique of planning for approximated income

and expenditures based on the actual current amount of results. It is also known as variable

budget because flexible budget exercise the revenues and expenses generated in the real time

production as a standard and estimates that how the incomes and expenses may change in

relation with changes in the production (Gersonius and et.al., 2015). Selected firm's management

creates flexible budget so that evaluation of the the performance and success can be done on the

basis of previous standards and budgets. The advantages and disadvantages of this budget can be

compared by the respective company as given below:

Advantages:

Flexible budget helps in estimation of seasonal costs and requirements so that production

can be done accordingly.

This budget helps the Trust Ford in integrated irregular receipts and payments so that

funds can be utilised when needed.

Disadvantages:

Separate clarification or notes are required with every activity otherwise it will become

very confusing.

Flexible budget includes so much elasticity in rules that it invites fraud and cheating

practices within the firm.

bared by respective firm:

Advantages:

Sales budget is helpful in controlling costs and expenditures so that desired profit can be

achieved.

This budget helps in finding out the areas or products which needs to be updated or

improved.

Disadvantages:

The biggest disadvantage of sales budget is that it is unable to forecast future sales and

other estimates effectively.

Generally sales budget eliminates the estimation of that expenditures which takes long

time in revenue generation.

Flexible Budget: A flexible budget is a technique of planning for approximated income

and expenditures based on the actual current amount of results. It is also known as variable

budget because flexible budget exercise the revenues and expenses generated in the real time

production as a standard and estimates that how the incomes and expenses may change in

relation with changes in the production (Gersonius and et.al., 2015). Selected firm's management

creates flexible budget so that evaluation of the the performance and success can be done on the

basis of previous standards and budgets. The advantages and disadvantages of this budget can be

compared by the respective company as given below:

Advantages:

Flexible budget helps in estimation of seasonal costs and requirements so that production

can be done accordingly.

This budget helps the Trust Ford in integrated irregular receipts and payments so that

funds can be utilised when needed.

Disadvantages:

Separate clarification or notes are required with every activity otherwise it will become

very confusing.

Flexible budget includes so much elasticity in rules that it invites fraud and cheating

practices within the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.