Management Accounting: Systems, Benefits, and Reporting

VerifiedAdded on 2023/01/17

|23

|5558

|41

AI Summary

This document provides an overview of management accounting systems, their benefits, and methods used for managerial reporting. It also explains the computation of net profit using absorption and marginal costing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Explaining management accounting systems along with its benefits of different systems.........3

Presenting methods used for managerial reporting aspects.........................................................4

Critically evaluating how management accounting systems and reporting is integrated within

organizational process.................................................................................................................5

LO2..................................................................................................................................................6

Computation of net profit by employing absorption and marginal costing.................................6

LO3..................................................................................................................................................9

Explaining the advantages and disadvantages of different planning tools used in budgetary

control..........................................................................................................................................9

Analyzing the usage and application of different planning tools used in budgetary control....11

Exhibits the manner in which financial problems can be responded.........................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Explaining management accounting systems along with its benefits of different systems.........3

Presenting methods used for managerial reporting aspects.........................................................4

Critically evaluating how management accounting systems and reporting is integrated within

organizational process.................................................................................................................5

LO2..................................................................................................................................................6

Computation of net profit by employing absorption and marginal costing.................................6

LO3..................................................................................................................................................9

Explaining the advantages and disadvantages of different planning tools used in budgetary

control..........................................................................................................................................9

Analyzing the usage and application of different planning tools used in budgetary control....11

Exhibits the manner in which financial problems can be responded.........................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting emphasizes on analysing business cost and operations with the

motive to prepare appropriate financial reports. In the recent times, business unit lays high level

of emphasis on undertaking management accounting tools with the motive to manage internal

financial operations effectually. By undertaking MA tools firm can develop competent strategic

and policy framework for the upcoming time period. This report is based on the case scenario of

KEF Ltd which is involved in UK manufacturing sector. In this, report will provide deeper

insight about management accounting tools and techniques that can be undertaken by KEF Ltd.

Further, it also presents how managerial reporting can be used for the purpose of decision

making. Report will develop understanding about how absorption and marginal costing system

can be used for analysing profitability aspects. It also entails how MA tools can be employed for

the purpose of planning and budgetary control. Besides this, it will shed light on the manner in

which monetary problems can be responded using management accounting tools.

LO1

Explaining management accounting systems along with its benefits of different systems

Management accounting (MA) can be defined as a technique or a process which is used

by organisations in order to facilitate their business in the aspect of recording the transactions

that are taking place and the other activities that facilitate the operational activities in an

organisation (Agrawal and Cooper, 2017). Management accounting helps the accountants,

mangers and other financiers working in a business in ascertaining the costs that are incurred or

will be incurred in the business by using various tools and techniques and further, management

accounting also assists in controlling or minimising such costs that are pre-determined so that

unnecessary expenditure can be avoided.

Purpose of MA

It helps in doing planning about future with regards to setting budget that contributes in

cost reduction and profit maximization.

MA also provides high level of assistance in identifying gaps that take place in existing

performance and thereby helps in taking appropriate actions for improvement.

Management accounting emphasizes on analysing business cost and operations with the

motive to prepare appropriate financial reports. In the recent times, business unit lays high level

of emphasis on undertaking management accounting tools with the motive to manage internal

financial operations effectually. By undertaking MA tools firm can develop competent strategic

and policy framework for the upcoming time period. This report is based on the case scenario of

KEF Ltd which is involved in UK manufacturing sector. In this, report will provide deeper

insight about management accounting tools and techniques that can be undertaken by KEF Ltd.

Further, it also presents how managerial reporting can be used for the purpose of decision

making. Report will develop understanding about how absorption and marginal costing system

can be used for analysing profitability aspects. It also entails how MA tools can be employed for

the purpose of planning and budgetary control. Besides this, it will shed light on the manner in

which monetary problems can be responded using management accounting tools.

LO1

Explaining management accounting systems along with its benefits of different systems

Management accounting (MA) can be defined as a technique or a process which is used

by organisations in order to facilitate their business in the aspect of recording the transactions

that are taking place and the other activities that facilitate the operational activities in an

organisation (Agrawal and Cooper, 2017). Management accounting helps the accountants,

mangers and other financiers working in a business in ascertaining the costs that are incurred or

will be incurred in the business by using various tools and techniques and further, management

accounting also assists in controlling or minimising such costs that are pre-determined so that

unnecessary expenditure can be avoided.

Purpose of MA

It helps in doing planning about future with regards to setting budget that contributes in

cost reduction and profit maximization.

MA also provides high level of assistance in identifying gaps that take place in existing

performance and thereby helps in taking appropriate actions for improvement.

In addition to this, the main motive of MA is to ensure liaison between personnel and

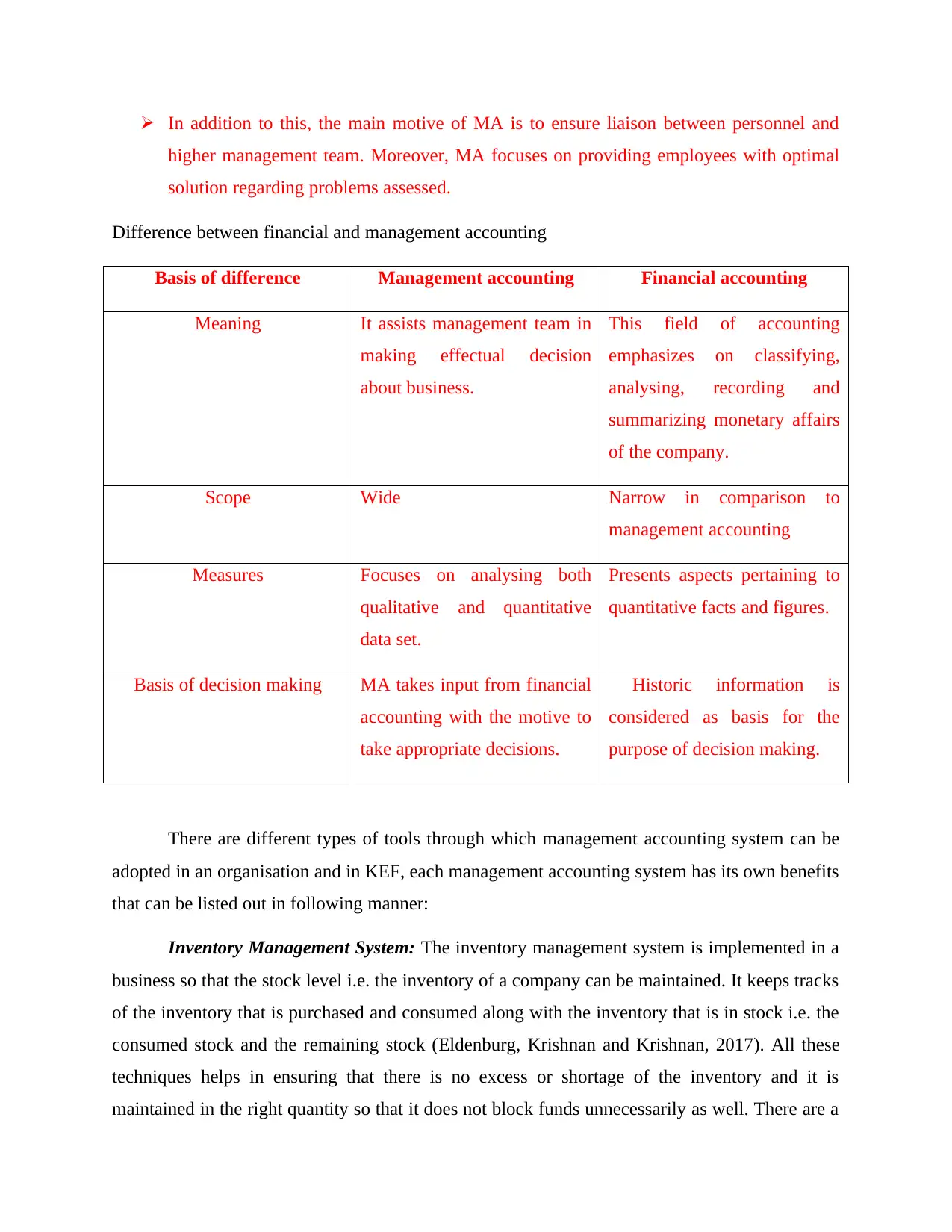

higher management team. Moreover, MA focuses on providing employees with optimal

solution regarding problems assessed.

Difference between financial and management accounting

Basis of difference Management accounting Financial accounting

Meaning It assists management team in

making effectual decision

about business.

This field of accounting

emphasizes on classifying,

analysing, recording and

summarizing monetary affairs

of the company.

Scope Wide Narrow in comparison to

management accounting

Measures Focuses on analysing both

qualitative and quantitative

data set.

Presents aspects pertaining to

quantitative facts and figures.

Basis of decision making MA takes input from financial

accounting with the motive to

take appropriate decisions.

Historic information is

considered as basis for the

purpose of decision making.

There are different types of tools through which management accounting system can be

adopted in an organisation and in KEF, each management accounting system has its own benefits

that can be listed out in following manner:

Inventory Management System: The inventory management system is implemented in a

business so that the stock level i.e. the inventory of a company can be maintained. It keeps tracks

of the inventory that is purchased and consumed along with the inventory that is in stock i.e. the

consumed stock and the remaining stock (Eldenburg, Krishnan and Krishnan, 2017). All these

techniques helps in ensuring that there is no excess or shortage of the inventory and it is

maintained in the right quantity so that it does not block funds unnecessarily as well. There are a

higher management team. Moreover, MA focuses on providing employees with optimal

solution regarding problems assessed.

Difference between financial and management accounting

Basis of difference Management accounting Financial accounting

Meaning It assists management team in

making effectual decision

about business.

This field of accounting

emphasizes on classifying,

analysing, recording and

summarizing monetary affairs

of the company.

Scope Wide Narrow in comparison to

management accounting

Measures Focuses on analysing both

qualitative and quantitative

data set.

Presents aspects pertaining to

quantitative facts and figures.

Basis of decision making MA takes input from financial

accounting with the motive to

take appropriate decisions.

Historic information is

considered as basis for the

purpose of decision making.

There are different types of tools through which management accounting system can be

adopted in an organisation and in KEF, each management accounting system has its own benefits

that can be listed out in following manner:

Inventory Management System: The inventory management system is implemented in a

business so that the stock level i.e. the inventory of a company can be maintained. It keeps tracks

of the inventory that is purchased and consumed along with the inventory that is in stock i.e. the

consumed stock and the remaining stock (Eldenburg, Krishnan and Krishnan, 2017). All these

techniques helps in ensuring that there is no excess or shortage of the inventory and it is

maintained in the right quantity so that it does not block funds unnecessarily as well. There are a

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

variety of techniques that can be used such as FIFO (First In First Out), LIFO (Last In First Out),

EOQ (Economic Order quantity) etc. LIFO deals with the earliest of consumption of the latest

stock that is in the warehouse and FIFO uses the older stock first and then the latest one. EOQ on

the other hand deduces a reorder level or point at which a particular quantity of goods should be

reordered so that the production of the company can keep running. For KEF, the best strategy

would be EOQ method since it ensures that the funds i.e. the working capital of the company

does not gets blocked unnecessarily and the stock is made available at all times.

Advantages Disadvantages

Ensures uninterrupted production

activities

It also helps in reducing storage as well

as ordering cost and thereby increases

profitability

For dealing with inventory

management systems business unit

needs to conduct training session. This

in turn imposes cost in front of the

company.

Time consuming process

Cost Accounting System: This technique of cost management helps the management in

ascertaining the cost that will be incurred on order to manufacture a particular product and also

determines whether it will be profitable or not to manufacture this product (Lopez-Valeiras,

Gomez-Conde and Naranjo-Gil, 2015).

Advantages Disadvantages

Helps in avoiding wastage, losses and

inefficiencies

Assists in identifying reason related to

profit or loss generated

Ensures cost reduction and profit

maximization

This accounting system leads problem

related to under or over absorption

Time consuming exercise as it requires

maintenance of many costing records

EOQ (Economic Order quantity) etc. LIFO deals with the earliest of consumption of the latest

stock that is in the warehouse and FIFO uses the older stock first and then the latest one. EOQ on

the other hand deduces a reorder level or point at which a particular quantity of goods should be

reordered so that the production of the company can keep running. For KEF, the best strategy

would be EOQ method since it ensures that the funds i.e. the working capital of the company

does not gets blocked unnecessarily and the stock is made available at all times.

Advantages Disadvantages

Ensures uninterrupted production

activities

It also helps in reducing storage as well

as ordering cost and thereby increases

profitability

For dealing with inventory

management systems business unit

needs to conduct training session. This

in turn imposes cost in front of the

company.

Time consuming process

Cost Accounting System: This technique of cost management helps the management in

ascertaining the cost that will be incurred on order to manufacture a particular product and also

determines whether it will be profitable or not to manufacture this product (Lopez-Valeiras,

Gomez-Conde and Naranjo-Gil, 2015).

Advantages Disadvantages

Helps in avoiding wastage, losses and

inefficiencies

Assists in identifying reason related to

profit or loss generated

Ensures cost reduction and profit

maximization

This accounting system leads problem

related to under or over absorption

Time consuming exercise as it requires

maintenance of many costing records

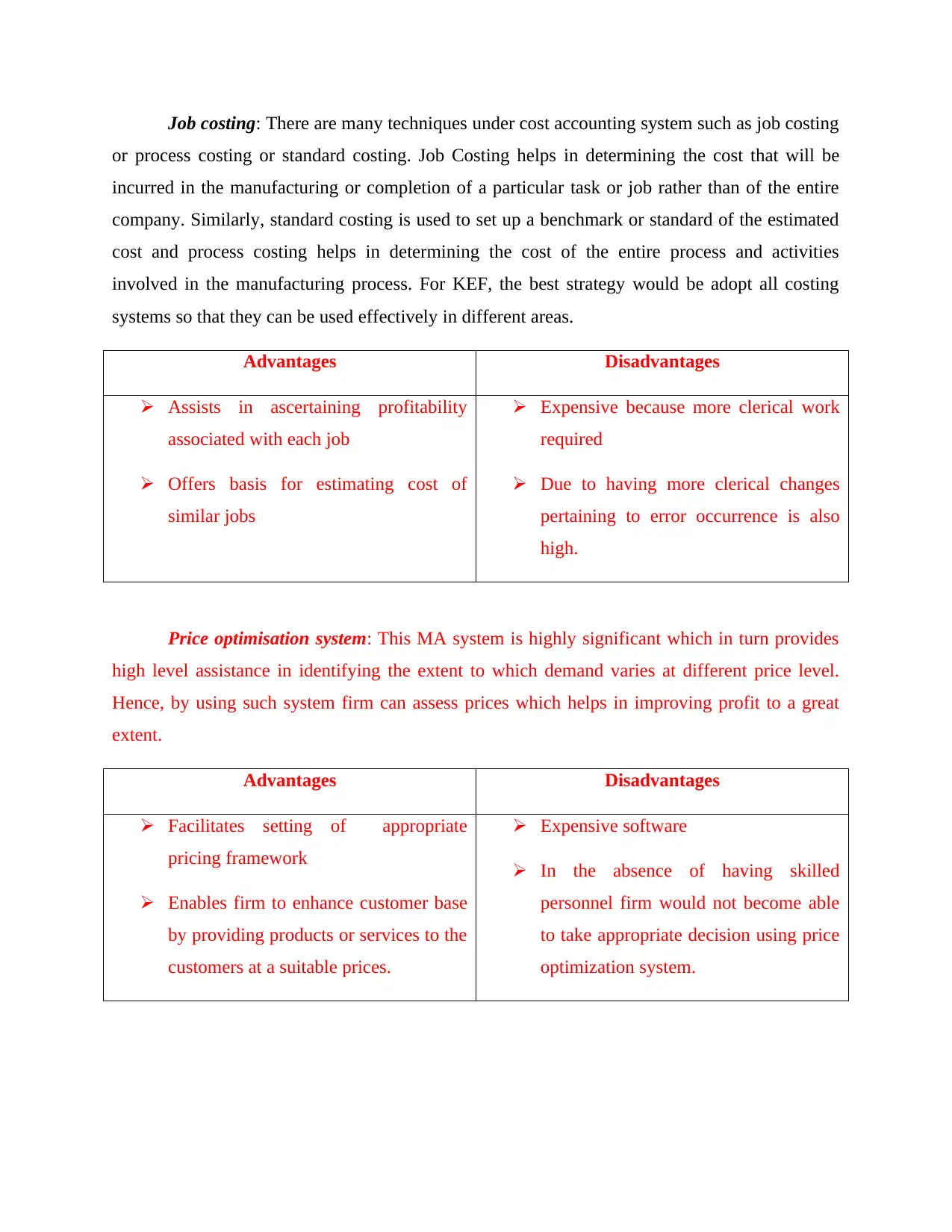

Job costing: There are many techniques under cost accounting system such as job costing

or process costing or standard costing. Job Costing helps in determining the cost that will be

incurred in the manufacturing or completion of a particular task or job rather than of the entire

company. Similarly, standard costing is used to set up a benchmark or standard of the estimated

cost and process costing helps in determining the cost of the entire process and activities

involved in the manufacturing process. For KEF, the best strategy would be adopt all costing

systems so that they can be used effectively in different areas.

Advantages Disadvantages

Assists in ascertaining profitability

associated with each job

Offers basis for estimating cost of

similar jobs

Expensive because more clerical work

required

Due to having more clerical changes

pertaining to error occurrence is also

high.

Price optimisation system: This MA system is highly significant which in turn provides

high level assistance in identifying the extent to which demand varies at different price level.

Hence, by using such system firm can assess prices which helps in improving profit to a great

extent.

Advantages Disadvantages

Facilitates setting of appropriate

pricing framework

Enables firm to enhance customer base

by providing products or services to the

customers at a suitable prices.

Expensive software

In the absence of having skilled

personnel firm would not become able

to take appropriate decision using price

optimization system.

or process costing or standard costing. Job Costing helps in determining the cost that will be

incurred in the manufacturing or completion of a particular task or job rather than of the entire

company. Similarly, standard costing is used to set up a benchmark or standard of the estimated

cost and process costing helps in determining the cost of the entire process and activities

involved in the manufacturing process. For KEF, the best strategy would be adopt all costing

systems so that they can be used effectively in different areas.

Advantages Disadvantages

Assists in ascertaining profitability

associated with each job

Offers basis for estimating cost of

similar jobs

Expensive because more clerical work

required

Due to having more clerical changes

pertaining to error occurrence is also

high.

Price optimisation system: This MA system is highly significant which in turn provides

high level assistance in identifying the extent to which demand varies at different price level.

Hence, by using such system firm can assess prices which helps in improving profit to a great

extent.

Advantages Disadvantages

Facilitates setting of appropriate

pricing framework

Enables firm to enhance customer base

by providing products or services to the

customers at a suitable prices.

Expensive software

In the absence of having skilled

personnel firm would not become able

to take appropriate decision using price

optimization system.

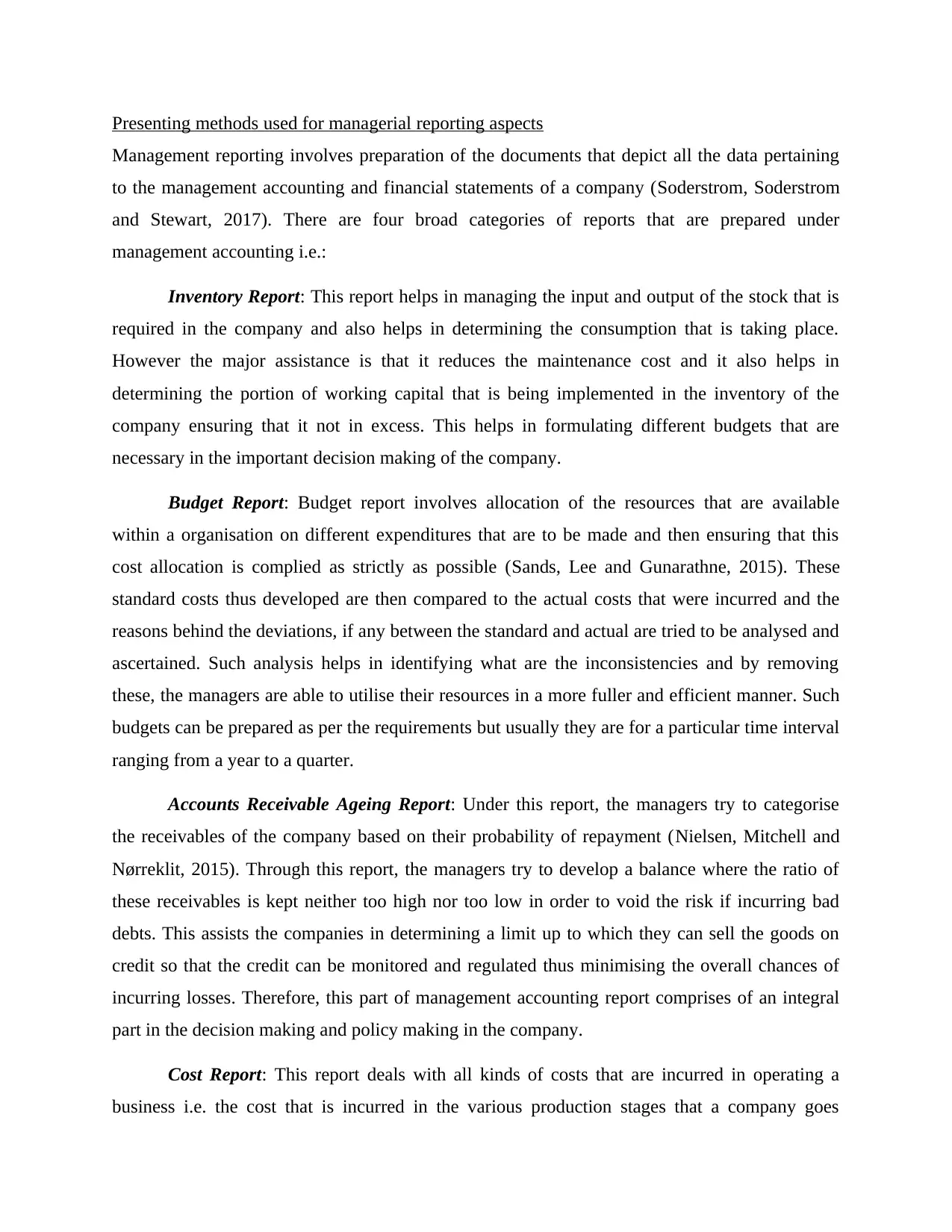

Presenting methods used for managerial reporting aspects

Management reporting involves preparation of the documents that depict all the data pertaining

to the management accounting and financial statements of a company (Soderstrom, Soderstrom

and Stewart, 2017). There are four broad categories of reports that are prepared under

management accounting i.e.:

Inventory Report: This report helps in managing the input and output of the stock that is

required in the company and also helps in determining the consumption that is taking place.

However the major assistance is that it reduces the maintenance cost and it also helps in

determining the portion of working capital that is being implemented in the inventory of the

company ensuring that it not in excess. This helps in formulating different budgets that are

necessary in the important decision making of the company.

Budget Report: Budget report involves allocation of the resources that are available

within a organisation on different expenditures that are to be made and then ensuring that this

cost allocation is complied as strictly as possible (Sands, Lee and Gunarathne, 2015). These

standard costs thus developed are then compared to the actual costs that were incurred and the

reasons behind the deviations, if any between the standard and actual are tried to be analysed and

ascertained. Such analysis helps in identifying what are the inconsistencies and by removing

these, the managers are able to utilise their resources in a more fuller and efficient manner. Such

budgets can be prepared as per the requirements but usually they are for a particular time interval

ranging from a year to a quarter.

Accounts Receivable Ageing Report: Under this report, the managers try to categorise

the receivables of the company based on their probability of repayment (Nielsen, Mitchell and

Nørreklit, 2015). Through this report, the managers try to develop a balance where the ratio of

these receivables is kept neither too high nor too low in order to void the risk if incurring bad

debts. This assists the companies in determining a limit up to which they can sell the goods on

credit so that the credit can be monitored and regulated thus minimising the overall chances of

incurring losses. Therefore, this part of management accounting report comprises of an integral

part in the decision making and policy making in the company.

Cost Report: This report deals with all kinds of costs that are incurred in operating a

business i.e. the cost that is incurred in the various production stages that a company goes

Management reporting involves preparation of the documents that depict all the data pertaining

to the management accounting and financial statements of a company (Soderstrom, Soderstrom

and Stewart, 2017). There are four broad categories of reports that are prepared under

management accounting i.e.:

Inventory Report: This report helps in managing the input and output of the stock that is

required in the company and also helps in determining the consumption that is taking place.

However the major assistance is that it reduces the maintenance cost and it also helps in

determining the portion of working capital that is being implemented in the inventory of the

company ensuring that it not in excess. This helps in formulating different budgets that are

necessary in the important decision making of the company.

Budget Report: Budget report involves allocation of the resources that are available

within a organisation on different expenditures that are to be made and then ensuring that this

cost allocation is complied as strictly as possible (Sands, Lee and Gunarathne, 2015). These

standard costs thus developed are then compared to the actual costs that were incurred and the

reasons behind the deviations, if any between the standard and actual are tried to be analysed and

ascertained. Such analysis helps in identifying what are the inconsistencies and by removing

these, the managers are able to utilise their resources in a more fuller and efficient manner. Such

budgets can be prepared as per the requirements but usually they are for a particular time interval

ranging from a year to a quarter.

Accounts Receivable Ageing Report: Under this report, the managers try to categorise

the receivables of the company based on their probability of repayment (Nielsen, Mitchell and

Nørreklit, 2015). Through this report, the managers try to develop a balance where the ratio of

these receivables is kept neither too high nor too low in order to void the risk if incurring bad

debts. This assists the companies in determining a limit up to which they can sell the goods on

credit so that the credit can be monitored and regulated thus minimising the overall chances of

incurring losses. Therefore, this part of management accounting report comprises of an integral

part in the decision making and policy making in the company.

Cost Report: This report deals with all kinds of costs that are incurred in operating a

business i.e. the cost that is incurred in the various production stages that a company goes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through. Under this, a comparison is made between the past and current costs that were incurred

so that a trend analysis can be established which assists the managers in deciding whether such

increase or decrease in cost is beneficial or not (Endrikat, Hartmann and Schreck, 2017). This

also points out if there is need of any specific policies that are to be implemented and there are

various techniques such as Job Costing etc. that can be used in these report’s preparation.

Critically evaluating how management accounting systems and reporting is integrated within

organizational process

From evaluation, it has identified that aspects of management accounting and reporting

are highly integrated with each other. Moreover, management accounting systems clearly entails

the manner through business unit can ensure effectual management of costing, stock and

profitability aspects (Otley, 2016). Further, report furnishes information about the extent to

which each department is performing in a well manner. Thus, by making assessment of reporting

aspect management team of KEF ltd can ascertain areas where extra efforts need to be made.

Thus, by taking significant measure on the basis of reporting management of KEF ltd can

achieve organizational goals and objectives.

LO2

Computation of net profit by employing absorption and marginal costing

Marginal costing- It means ascertainment through differentiating in between the fixed

and the variable cost of the marginal cost and an effect of the profit changes in respect of type

and the volume of an output (Ray and Gramlich, 2015). Marginal costing method is been used

for analyzing and interpreting cost data in order to determine product’s profitability, department,

process and the cost centre.

Absorption costing- It is referred to the method of accumulating cost attached with the

process of production and in apportioning them to the individual product (Konopczak and Welfe,

2017). It is the costing technique that is needed by an accounting standard for creating valuation

of an inventory which is stated in the balance sheet of an enterprise.

Difference between marginal and absorption costing

so that a trend analysis can be established which assists the managers in deciding whether such

increase or decrease in cost is beneficial or not (Endrikat, Hartmann and Schreck, 2017). This

also points out if there is need of any specific policies that are to be implemented and there are

various techniques such as Job Costing etc. that can be used in these report’s preparation.

Critically evaluating how management accounting systems and reporting is integrated within

organizational process

From evaluation, it has identified that aspects of management accounting and reporting

are highly integrated with each other. Moreover, management accounting systems clearly entails

the manner through business unit can ensure effectual management of costing, stock and

profitability aspects (Otley, 2016). Further, report furnishes information about the extent to

which each department is performing in a well manner. Thus, by making assessment of reporting

aspect management team of KEF ltd can ascertain areas where extra efforts need to be made.

Thus, by taking significant measure on the basis of reporting management of KEF ltd can

achieve organizational goals and objectives.

LO2

Computation of net profit by employing absorption and marginal costing

Marginal costing- It means ascertainment through differentiating in between the fixed

and the variable cost of the marginal cost and an effect of the profit changes in respect of type

and the volume of an output (Ray and Gramlich, 2015). Marginal costing method is been used

for analyzing and interpreting cost data in order to determine product’s profitability, department,

process and the cost centre.

Absorption costing- It is referred to the method of accumulating cost attached with the

process of production and in apportioning them to the individual product (Konopczak and Welfe,

2017). It is the costing technique that is needed by an accounting standard for creating valuation

of an inventory which is stated in the balance sheet of an enterprise.

Difference between marginal and absorption costing

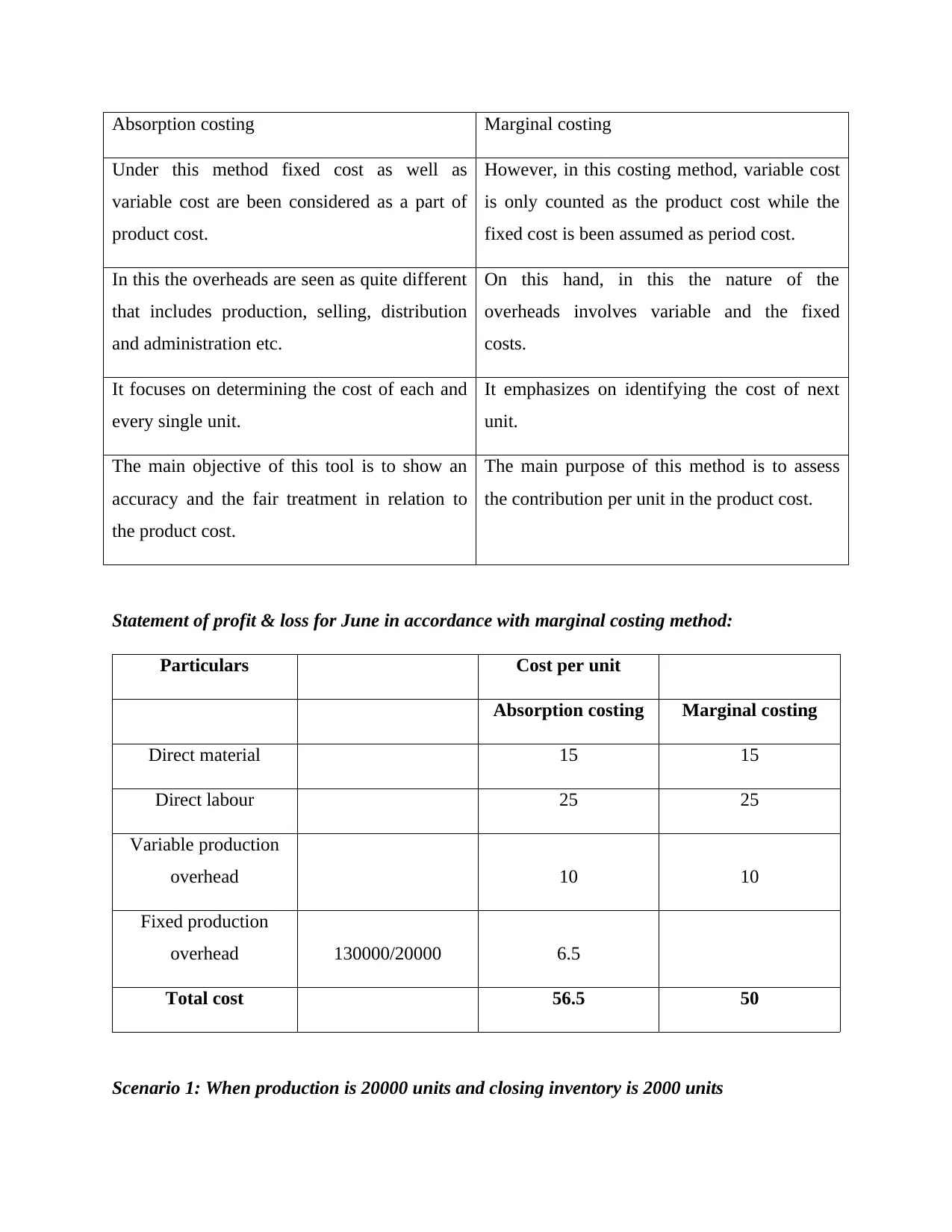

Absorption costing Marginal costing

Under this method fixed cost as well as

variable cost are been considered as a part of

product cost.

However, in this costing method, variable cost

is only counted as the product cost while the

fixed cost is been assumed as period cost.

In this the overheads are seen as quite different

that includes production, selling, distribution

and administration etc.

On this hand, in this the nature of the

overheads involves variable and the fixed

costs.

It focuses on determining the cost of each and

every single unit.

It emphasizes on identifying the cost of next

unit.

The main objective of this tool is to show an

accuracy and the fair treatment in relation to

the product cost.

The main purpose of this method is to assess

the contribution per unit in the product cost.

Statement of profit & loss for June in accordance with marginal costing method:

Particulars Cost per unit

Absorption costing Marginal costing

Direct material 15 15

Direct labour 25 25

Variable production

overhead 10 10

Fixed production

overhead 130000/20000 6.5

Total cost 56.5 50

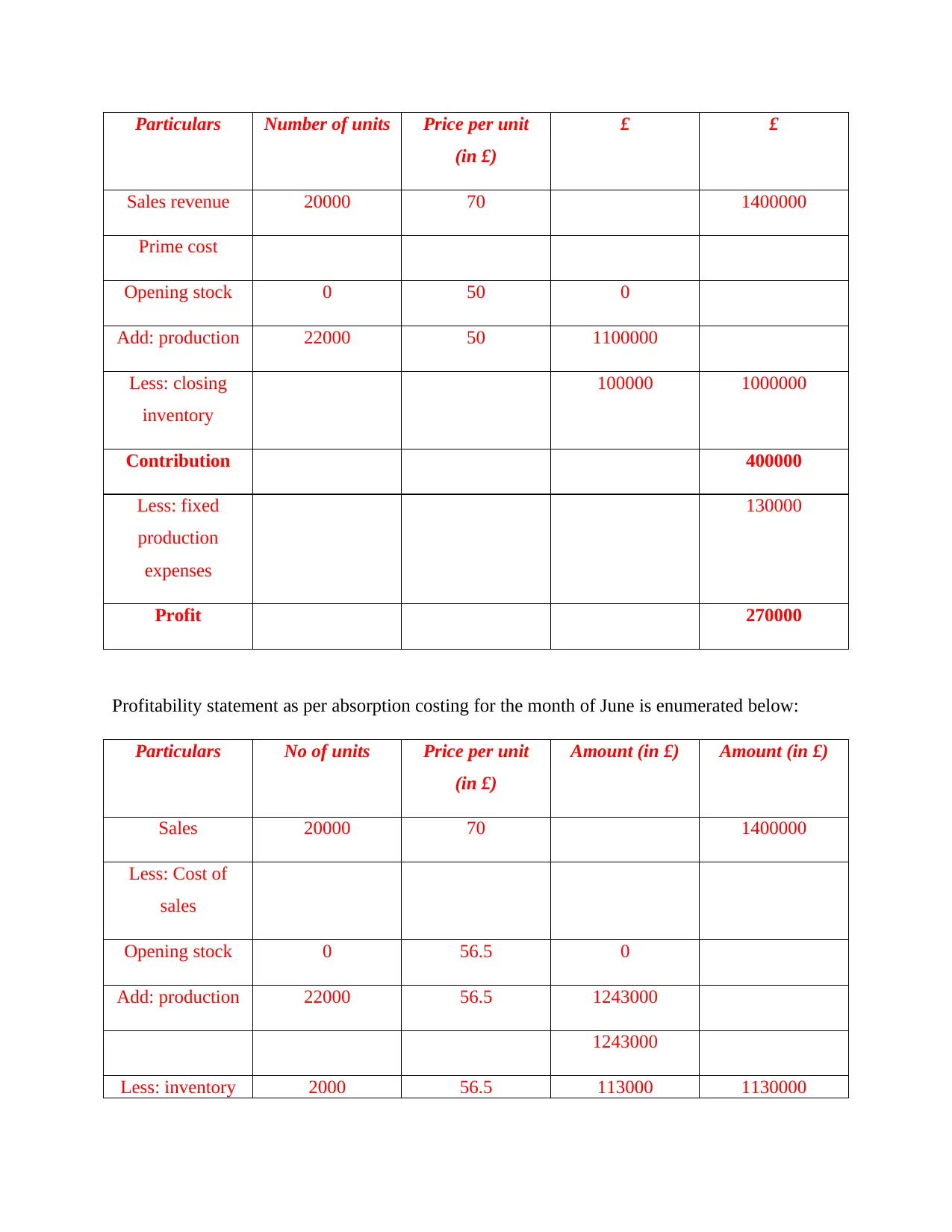

Scenario 1: When production is 20000 units and closing inventory is 2000 units

Under this method fixed cost as well as

variable cost are been considered as a part of

product cost.

However, in this costing method, variable cost

is only counted as the product cost while the

fixed cost is been assumed as period cost.

In this the overheads are seen as quite different

that includes production, selling, distribution

and administration etc.

On this hand, in this the nature of the

overheads involves variable and the fixed

costs.

It focuses on determining the cost of each and

every single unit.

It emphasizes on identifying the cost of next

unit.

The main objective of this tool is to show an

accuracy and the fair treatment in relation to

the product cost.

The main purpose of this method is to assess

the contribution per unit in the product cost.

Statement of profit & loss for June in accordance with marginal costing method:

Particulars Cost per unit

Absorption costing Marginal costing

Direct material 15 15

Direct labour 25 25

Variable production

overhead 10 10

Fixed production

overhead 130000/20000 6.5

Total cost 56.5 50

Scenario 1: When production is 20000 units and closing inventory is 2000 units

Particulars Number of units Price per unit

(in £)

£ £

Sales revenue 20000 70 1400000

Prime cost

Opening stock 0 50 0

Add: production 22000 50 1100000

Less: closing

inventory

100000 1000000

Contribution 400000

Less: fixed

production

expenses

130000

Profit 270000

Profitability statement as per absorption costing for the month of June is enumerated below:

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 20000 70 1400000

Less: Cost of

sales

Opening stock 0 56.5 0

Add: production 22000 56.5 1243000

1243000

Less: inventory 2000 56.5 113000 1130000

(in £)

£ £

Sales revenue 20000 70 1400000

Prime cost

Opening stock 0 50 0

Add: production 22000 50 1100000

Less: closing

inventory

100000 1000000

Contribution 400000

Less: fixed

production

expenses

130000

Profit 270000

Profitability statement as per absorption costing for the month of June is enumerated below:

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 20000 70 1400000

Less: Cost of

sales

Opening stock 0 56.5 0

Add: production 22000 56.5 1243000

1243000

Less: inventory 2000 56.5 113000 1130000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

at the end of

period

Profit 270000

Scenario 2:

Production = 19000 units

Closing inventory = 1000 units

P&L for June as per absorption costing method

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 18000 70 1260000

Less: COGS

Inventory at the

beginning of

period

0 56.5 0

Add: production 19000 56.5 1073500

Less: closing

stock

1000 56.5 56500 1017000

Profit 243000

Less: under

absorption

13000

Reconciled

profit with

marginal

230000

period

Profit 270000

Scenario 2:

Production = 19000 units

Closing inventory = 1000 units

P&L for June as per absorption costing method

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 18000 70 1260000

Less: COGS

Inventory at the

beginning of

period

0 56.5 0

Add: production 19000 56.5 1073500

Less: closing

stock

1000 56.5 56500 1017000

Profit 243000

Less: under

absorption

13000

Reconciled

profit with

marginal

230000

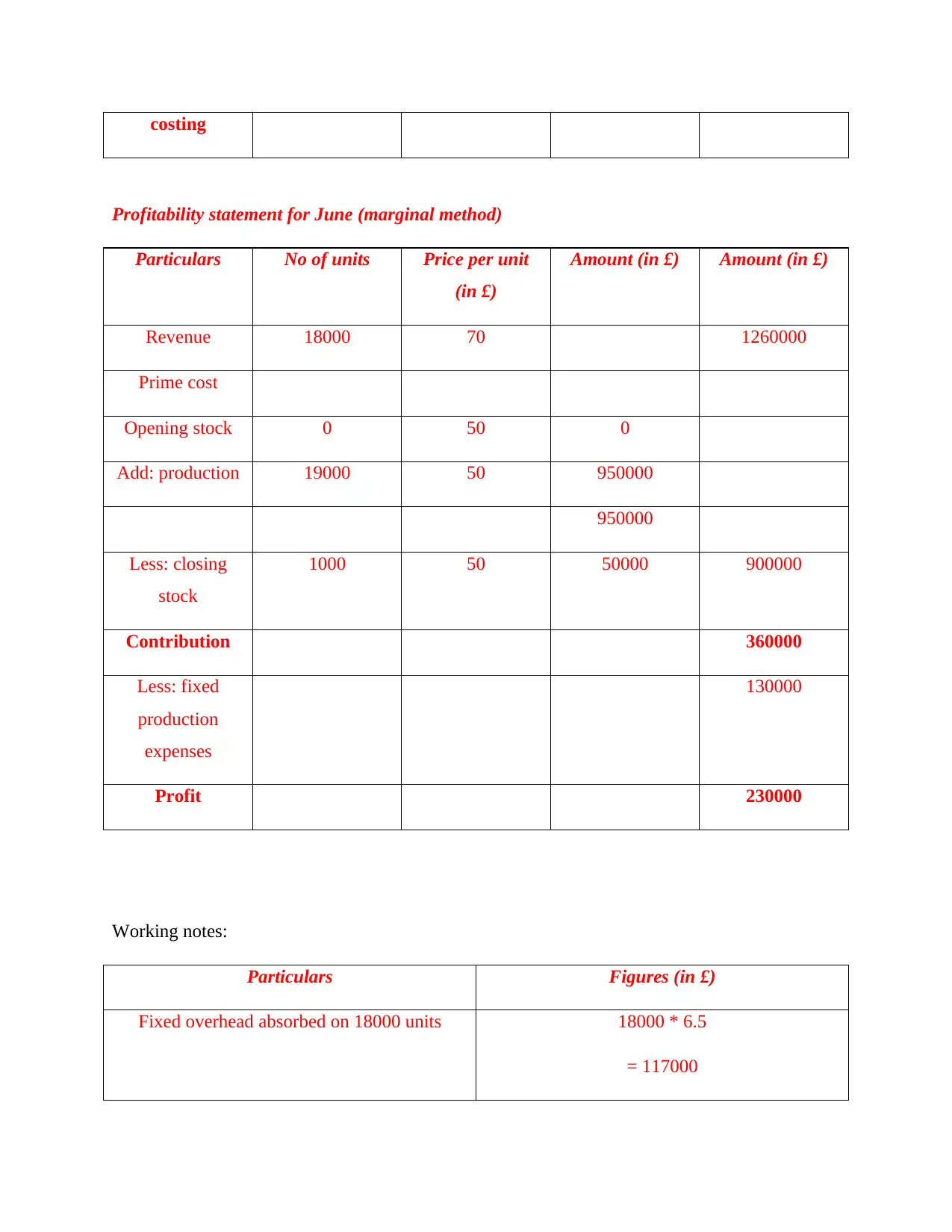

costing

Profitability statement for June (marginal method)

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Revenue 18000 70 1260000

Prime cost

Opening stock 0 50 0

Add: production 19000 50 950000

950000

Less: closing

stock

1000 50 50000 900000

Contribution 360000

Less: fixed

production

expenses

130000

Profit 230000

Working notes:

Particulars Figures (in £)

Fixed overhead absorbed on 18000 units 18000 * 6.5

= 117000

Profitability statement for June (marginal method)

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Revenue 18000 70 1260000

Prime cost

Opening stock 0 50 0

Add: production 19000 50 950000

950000

Less: closing

stock

1000 50 50000 900000

Contribution 360000

Less: fixed

production

expenses

130000

Profit 230000

Working notes:

Particulars Figures (in £)

Fixed overhead absorbed on 18000 units 18000 * 6.5

= 117000

Fixed production overhead 130000

Under absorbed fixed cost (13000)

Interpretation- From the above assessment, it has been reflected that net profit resulted

by application of absorption and marginal costing resulted as 256000 and 230000. This variation

in the profit shows that absorption costing is the better approach in evaluating the profits as

compared to marginal costing because it provides an accurate figure of profit by considering both

variable and the fixed cost in the product cost. Absorption costing presented as the most

conventional technique in context tax and the financial reporting, however, marginal costing

outline the overall contribution.

LO3

Explaining the advantages and disadvantages of different planning tools used in budgetary

control

Budgeting implies for the process which gives clear indication about the manner in which

money should be spent. It contains information about estimated income and expenditure that

associated with near future (Maas, Schaltegger and Crutzen, 2016). With regards to KEF Ltd

budgeting is highly significant for doing panning about upcoming time frame. Along with this, it

offers input to the management team in relation to doing comparison of current aspects over

planned budget and thereby indicates areas for improvement.

There are several tools which KEF Ltd can undertake for the purpose of budgetary

control such as:

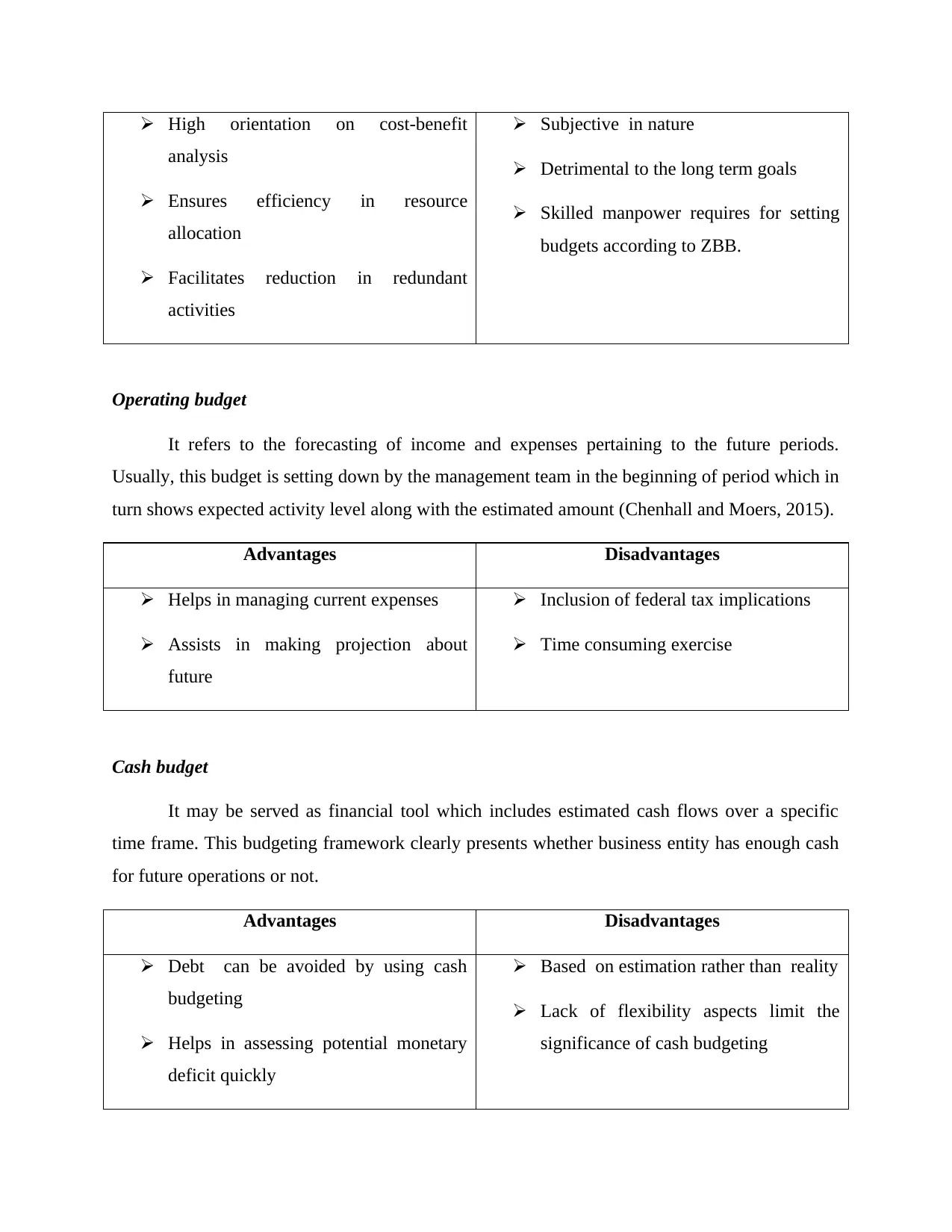

Zero based budgeting

This method emphasizes on justifying every line of item that associated with new period.

As per this, every function within an organization is analyzed for assessing needs and costs

associated with it (Zero Based Budgeting – Advantages and Disadvantages, 2019). All such

aspects clearly exhibits that zero based budget starts from scratch for while drafting the new one.

Advantages Disadvantages

Under absorbed fixed cost (13000)

Interpretation- From the above assessment, it has been reflected that net profit resulted

by application of absorption and marginal costing resulted as 256000 and 230000. This variation

in the profit shows that absorption costing is the better approach in evaluating the profits as

compared to marginal costing because it provides an accurate figure of profit by considering both

variable and the fixed cost in the product cost. Absorption costing presented as the most

conventional technique in context tax and the financial reporting, however, marginal costing

outline the overall contribution.

LO3

Explaining the advantages and disadvantages of different planning tools used in budgetary

control

Budgeting implies for the process which gives clear indication about the manner in which

money should be spent. It contains information about estimated income and expenditure that

associated with near future (Maas, Schaltegger and Crutzen, 2016). With regards to KEF Ltd

budgeting is highly significant for doing panning about upcoming time frame. Along with this, it

offers input to the management team in relation to doing comparison of current aspects over

planned budget and thereby indicates areas for improvement.

There are several tools which KEF Ltd can undertake for the purpose of budgetary

control such as:

Zero based budgeting

This method emphasizes on justifying every line of item that associated with new period.

As per this, every function within an organization is analyzed for assessing needs and costs

associated with it (Zero Based Budgeting – Advantages and Disadvantages, 2019). All such

aspects clearly exhibits that zero based budget starts from scratch for while drafting the new one.

Advantages Disadvantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

High orientation on cost-benefit

analysis

Ensures efficiency in resource

allocation

Facilitates reduction in redundant

activities

Subjective in nature

Detrimental to the long term goals

Skilled manpower requires for setting

budgets according to ZBB.

Operating budget

It refers to the forecasting of income and expenses pertaining to the future periods.

Usually, this budget is setting down by the management team in the beginning of period which in

turn shows expected activity level along with the estimated amount (Chenhall and Moers, 2015).

Advantages Disadvantages

Helps in managing current expenses

Assists in making projection about

future

Inclusion of federal tax implications

Time consuming exercise

Cash budget

It may be served as financial tool which includes estimated cash flows over a specific

time frame. This budgeting framework clearly presents whether business entity has enough cash

for future operations or not.

Advantages Disadvantages

Debt can be avoided by using cash

budgeting

Helps in assessing potential monetary

deficit quickly

Based on estimation rather than reality

Lack of flexibility aspects limit the

significance of cash budgeting

analysis

Ensures efficiency in resource

allocation

Facilitates reduction in redundant

activities

Subjective in nature

Detrimental to the long term goals

Skilled manpower requires for setting

budgets according to ZBB.

Operating budget

It refers to the forecasting of income and expenses pertaining to the future periods.

Usually, this budget is setting down by the management team in the beginning of period which in

turn shows expected activity level along with the estimated amount (Chenhall and Moers, 2015).

Advantages Disadvantages

Helps in managing current expenses

Assists in making projection about

future

Inclusion of federal tax implications

Time consuming exercise

Cash budget

It may be served as financial tool which includes estimated cash flows over a specific

time frame. This budgeting framework clearly presents whether business entity has enough cash

for future operations or not.

Advantages Disadvantages

Debt can be avoided by using cash

budgeting

Helps in assessing potential monetary

deficit quickly

Based on estimation rather than reality

Lack of flexibility aspects limit the

significance of cash budgeting

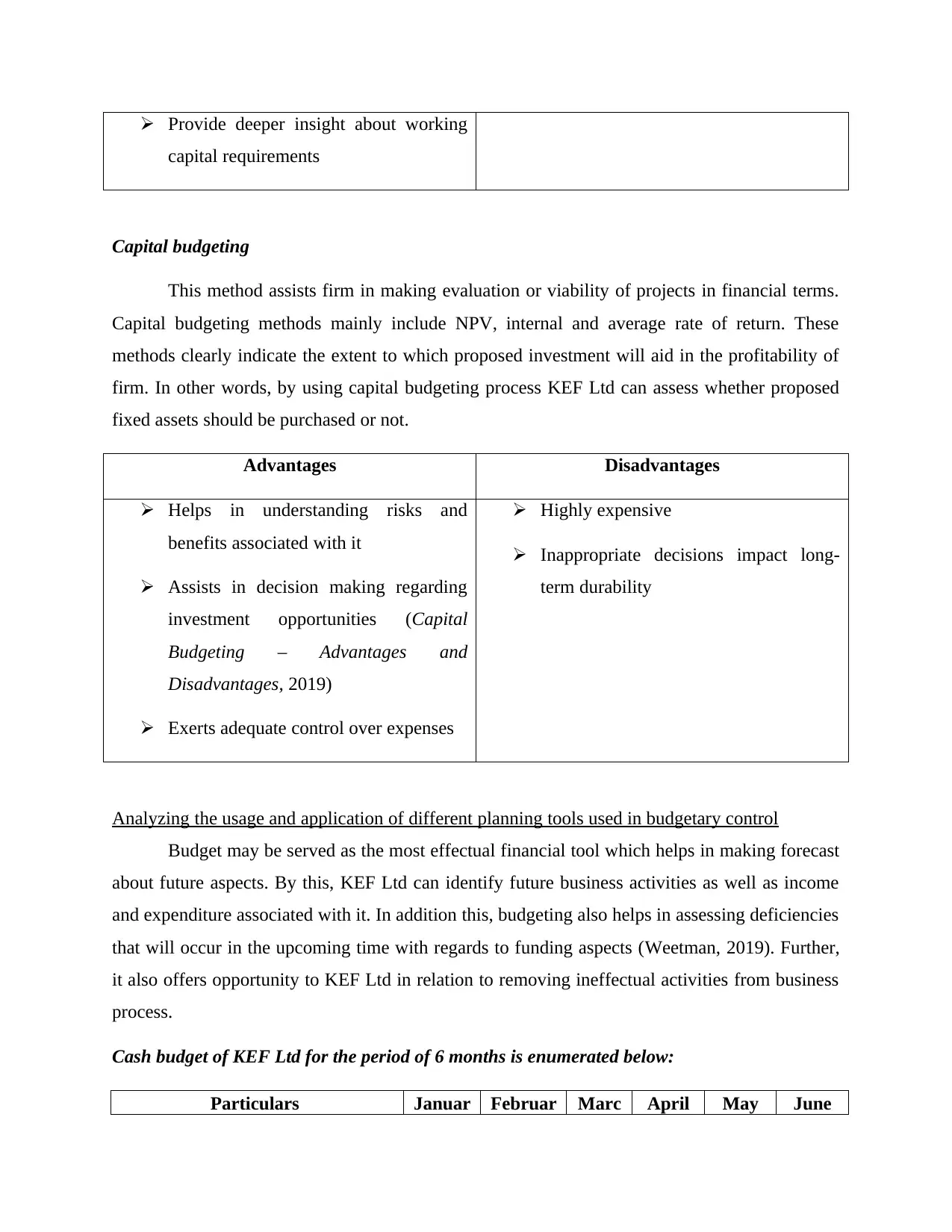

Provide deeper insight about working

capital requirements

Capital budgeting

This method assists firm in making evaluation or viability of projects in financial terms.

Capital budgeting methods mainly include NPV, internal and average rate of return. These

methods clearly indicate the extent to which proposed investment will aid in the profitability of

firm. In other words, by using capital budgeting process KEF Ltd can assess whether proposed

fixed assets should be purchased or not.

Advantages Disadvantages

Helps in understanding risks and

benefits associated with it

Assists in decision making regarding

investment opportunities (Capital

Budgeting – Advantages and

Disadvantages, 2019)

Exerts adequate control over expenses

Highly expensive

Inappropriate decisions impact long-

term durability

Analyzing the usage and application of different planning tools used in budgetary control

Budget may be served as the most effectual financial tool which helps in making forecast

about future aspects. By this, KEF Ltd can identify future business activities as well as income

and expenditure associated with it. In addition this, budgeting also helps in assessing deficiencies

that will occur in the upcoming time with regards to funding aspects (Weetman, 2019). Further,

it also offers opportunity to KEF Ltd in relation to removing ineffectual activities from business

process.

Cash budget of KEF Ltd for the period of 6 months is enumerated below:

Particulars Januar Februar Marc April May June

capital requirements

Capital budgeting

This method assists firm in making evaluation or viability of projects in financial terms.

Capital budgeting methods mainly include NPV, internal and average rate of return. These

methods clearly indicate the extent to which proposed investment will aid in the profitability of

firm. In other words, by using capital budgeting process KEF Ltd can assess whether proposed

fixed assets should be purchased or not.

Advantages Disadvantages

Helps in understanding risks and

benefits associated with it

Assists in decision making regarding

investment opportunities (Capital

Budgeting – Advantages and

Disadvantages, 2019)

Exerts adequate control over expenses

Highly expensive

Inappropriate decisions impact long-

term durability

Analyzing the usage and application of different planning tools used in budgetary control

Budget may be served as the most effectual financial tool which helps in making forecast

about future aspects. By this, KEF Ltd can identify future business activities as well as income

and expenditure associated with it. In addition this, budgeting also helps in assessing deficiencies

that will occur in the upcoming time with regards to funding aspects (Weetman, 2019). Further,

it also offers opportunity to KEF Ltd in relation to removing ineffectual activities from business

process.

Cash budget of KEF Ltd for the period of 6 months is enumerated below:

Particulars Januar Februar Marc April May June

y (in £) y (in £)

h (in

£) (in £) (in £) (in £)

Cash inflows

Opening cash balance 10000 17500 25200 33110 41240 49602

Sales 25000 26000 27040

28121.

6

29246.

5

30416.

3

Other income 5000 5000 5000 5000 5000 5000

Total cash inflows 40000 48500 57240

66231

6

75486.

9

85018.

5

cash outflows

Material 3750 3900 4056 4218 4387 4562

Labour 6250 6500 6760 7030 7312 7604

Overheads 7500 7800 8112 8436 8774 9125

Other expenses 5000 5100 5202

5306.0

4

5412.1

6 5520.4

Total cash outflows 22500 23300 24130

24991.

2

25884.

7

26811.

8

Cash (Deficit / surplus) or closing

cash balance 17500 25200 33110 41240 49602 58207

The above depicted cash budget shows that closing cash balance will increase over the

time frame. Moreover, in the month of January, closing cash balance implies for £17500

respectively, whereas at the end of June it reached on £58207 significantly. Considering this, it

can be mentioned that KEF Ltd is performing well.

Usage and application of capital budgeting

Computation of NPV

Year

Cash

inflows

(Projec

t A)

(in £)

Cash

inflows

(Projec

t B)

(in £)

PV

@

10%

Discounted

cash flows

(Project A)

(in £)

Discounted

cash flows

(Project B)

(in £)

1 45000 49000 0.909 40909 44545

2 56000 59000 0.826 46281 48760

3 48000 53000 0.751 36063 39820

4 64000 69000 0.683 43713 47128

5 76000 84000 0.621 47190 52157

h (in

£) (in £) (in £) (in £)

Cash inflows

Opening cash balance 10000 17500 25200 33110 41240 49602

Sales 25000 26000 27040

28121.

6

29246.

5

30416.

3

Other income 5000 5000 5000 5000 5000 5000

Total cash inflows 40000 48500 57240

66231

6

75486.

9

85018.

5

cash outflows

Material 3750 3900 4056 4218 4387 4562

Labour 6250 6500 6760 7030 7312 7604

Overheads 7500 7800 8112 8436 8774 9125

Other expenses 5000 5100 5202

5306.0

4

5412.1

6 5520.4

Total cash outflows 22500 23300 24130

24991.

2

25884.

7

26811.

8

Cash (Deficit / surplus) or closing

cash balance 17500 25200 33110 41240 49602 58207

The above depicted cash budget shows that closing cash balance will increase over the

time frame. Moreover, in the month of January, closing cash balance implies for £17500

respectively, whereas at the end of June it reached on £58207 significantly. Considering this, it

can be mentioned that KEF Ltd is performing well.

Usage and application of capital budgeting

Computation of NPV

Year

Cash

inflows

(Projec

t A)

(in £)

Cash

inflows

(Projec

t B)

(in £)

PV

@

10%

Discounted

cash flows

(Project A)

(in £)

Discounted

cash flows

(Project B)

(in £)

1 45000 49000 0.909 40909 44545

2 56000 59000 0.826 46281 48760

3 48000 53000 0.751 36063 39820

4 64000 69000 0.683 43713 47128

5 76000 84000 0.621 47190 52157

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

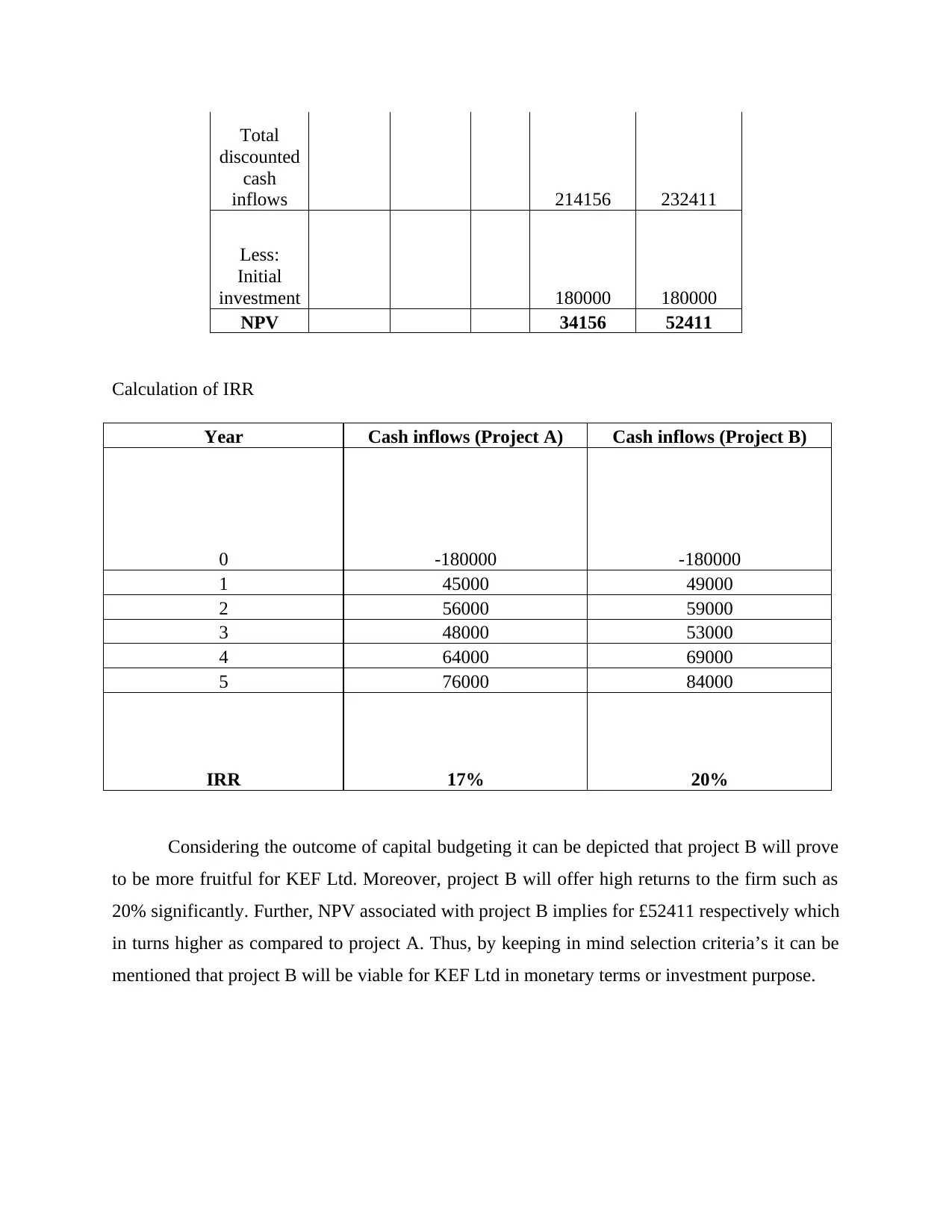

Total

discounted

cash

inflows 214156 232411

Less:

Initial

investment 180000 180000

NPV 34156 52411

Calculation of IRR

Year Cash inflows (Project A) Cash inflows (Project B)

0 -180000 -180000

1 45000 49000

2 56000 59000

3 48000 53000

4 64000 69000

5 76000 84000

IRR 17% 20%

Considering the outcome of capital budgeting it can be depicted that project B will prove

to be more fruitful for KEF Ltd. Moreover, project B will offer high returns to the firm such as

20% significantly. Further, NPV associated with project B implies for £52411 respectively which

in turns higher as compared to project A. Thus, by keeping in mind selection criteria’s it can be

mentioned that project B will be viable for KEF Ltd in monetary terms or investment purpose.

discounted

cash

inflows 214156 232411

Less:

Initial

investment 180000 180000

NPV 34156 52411

Calculation of IRR

Year Cash inflows (Project A) Cash inflows (Project B)

0 -180000 -180000

1 45000 49000

2 56000 59000

3 48000 53000

4 64000 69000

5 76000 84000

IRR 17% 20%

Considering the outcome of capital budgeting it can be depicted that project B will prove

to be more fruitful for KEF Ltd. Moreover, project B will offer high returns to the firm such as

20% significantly. Further, NPV associated with project B implies for £52411 respectively which

in turns higher as compared to project A. Thus, by keeping in mind selection criteria’s it can be

mentioned that project B will be viable for KEF Ltd in monetary terms or investment purpose.

LO4

Exhibits the manner in which financial problems can be responded

There are several tools that can be undertaken by the firm for deriving suitable solution of

financial problems. Moreover, in order to ensure smooth functioning of business operations and

function company is required to take appropriate measure or tool within the suitable time frame.

Balance scorecard:

This is one of the most effectual tools which helps company in resolving both monetary

and non-monetary issues effectually. Moreover, it emphasizes on measuring performance from

several perspectives including financial, customer, internal process and organizational capacity

(Cooper, Ezzamel and Qu, 2017). Thus, by making evaluation of performance in against to such

four aspects KEF Ltd can assess areas where improvements are required and drives overall

business performance.

Advantages Disadvantages

Clearly indicates company’s

performance and areas for improvement

Helps in setting appropriate goals in

line with company’s vision and

mission

Highly time consuming

Expensive in nature

Financial governance:

It implies for the ways in which organization gathers, manages, monitors and control

monetary information. In other words, by using this technique management team can assess the

manner in which business unit is tracking monetary and other aspects. Besides this, compliance

with disclosure aspects can also be monitored using financial governance tool (Malmi, 2016).

Hence, with the help of financial governance tool KEF Ltd can identify loopholes in the existing

operational aspect and thereby takes measure for improvement.

Advantages Disadvantages

Exhibits the manner in which financial problems can be responded

There are several tools that can be undertaken by the firm for deriving suitable solution of

financial problems. Moreover, in order to ensure smooth functioning of business operations and

function company is required to take appropriate measure or tool within the suitable time frame.

Balance scorecard:

This is one of the most effectual tools which helps company in resolving both monetary

and non-monetary issues effectually. Moreover, it emphasizes on measuring performance from

several perspectives including financial, customer, internal process and organizational capacity

(Cooper, Ezzamel and Qu, 2017). Thus, by making evaluation of performance in against to such

four aspects KEF Ltd can assess areas where improvements are required and drives overall

business performance.

Advantages Disadvantages

Clearly indicates company’s

performance and areas for improvement

Helps in setting appropriate goals in

line with company’s vision and

mission

Highly time consuming

Expensive in nature

Financial governance:

It implies for the ways in which organization gathers, manages, monitors and control

monetary information. In other words, by using this technique management team can assess the

manner in which business unit is tracking monetary and other aspects. Besides this, compliance

with disclosure aspects can also be monitored using financial governance tool (Malmi, 2016).

Hence, with the help of financial governance tool KEF Ltd can identify loopholes in the existing

operational aspect and thereby takes measure for improvement.

Advantages Disadvantages

Facilitates better access to capital and

profit maximization

Enhances managerial efficiency and

ensures maintenance of financial

stability

Rigid in nature

High cost is associated with the usage

of financial governance tool which in

turn limits its significance.

Key performance indicators:

In the context of KEF Ltd, management team can evaluate and control business

performance using KPI tool. With regards to the firm, there are several KPI’s such as sales,

profit, market share etc. Accordingly, by doing comparison of performance in against to the

predetermined KPI’s and over rivals firm can determine the extent to which goals are met

(Granlund and Lukka, 2017). Referring this, management team can do suitable modifications in

the existing strategic framework and thereby gets the desired level of outcome or success.

Advantages Disadvantages

Offers clear framework for rewarding

employees

Helps in tracking organizational

progress

Offers appropriate results in terms of

numbers

Aligned with traditional working

practices which in turn results into lack

of innovative practices

KPI results into decrease in quality

work

Benchmarking:

With the motive to attain goals and making optimum utilization of funds company sets

specific benchmarks in relation to income and expenditure. On the basis of this, management

team can assess issues take place in the monetary performance by comparing actual figures in

against to the benchmarks (Latan and et.al., 2018). Thus, by investing causes due to which

profit maximization

Enhances managerial efficiency and

ensures maintenance of financial

stability

Rigid in nature

High cost is associated with the usage

of financial governance tool which in

turn limits its significance.

Key performance indicators:

In the context of KEF Ltd, management team can evaluate and control business

performance using KPI tool. With regards to the firm, there are several KPI’s such as sales,

profit, market share etc. Accordingly, by doing comparison of performance in against to the

predetermined KPI’s and over rivals firm can determine the extent to which goals are met

(Granlund and Lukka, 2017). Referring this, management team can do suitable modifications in

the existing strategic framework and thereby gets the desired level of outcome or success.

Advantages Disadvantages

Offers clear framework for rewarding

employees

Helps in tracking organizational

progress

Offers appropriate results in terms of

numbers

Aligned with traditional working

practices which in turn results into lack

of innovative practices

KPI results into decrease in quality

work

Benchmarking:

With the motive to attain goals and making optimum utilization of funds company sets

specific benchmarks in relation to income and expenditure. On the basis of this, management

team can assess issues take place in the monetary performance by comparing actual figures in

against to the benchmarks (Latan and et.al., 2018). Thus, by investing causes due to which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business unit failed to achieve set benchmarks appropriate modifications can be done in the

existing strategies.

Advantages Disadvantages

Facilitates performance improvement

by inspiring creativity

Motivates towards quality work as

emphasis is placed on doing

comparison of strength and weakness in

against to the rest of the company

Provides insufficient information for

future

It may results into lack of customer

satisfaction

By doing analysis, it has assessed that KEF Ltd uses balance scorecard tool because it

assists in making evaluation of business performance from all perspectives. It clearly indicates

areas, financial and non-financial, whereas changes need to be done for achieving success. In

comparison to this, Corus Ltd employs variance analysis tool for identifying problems take place

in business operations. However, such technique sometimes places negative impact on employee

motivation. Moreover, when firm fails to sets appropriate standards then it may result into high

deviations. Thus, it can be mentioned that techniques undertaken by KEF Ltd are highly effectual

over Corus Ltd.

STRATEGIC PLANNING

a. Assessing applicability of strategic planning tools

There are mainly two tools which can be used by KEF Ltd for the purpose of strategic

planning such as:

SWOT analysis: This tool of strategic planning is highly prominent which assists

company in identifying areas where effectual measure need tobe undertaken for the

purpose of performance improvement.

Balance scorecard: In the context of KEF Ltd performance of business unit can be

evaluated from the perspective of both financial and non-financial. Thus, by using this

firm can take appropriate measure for future growth.

existing strategies.

Advantages Disadvantages

Facilitates performance improvement

by inspiring creativity

Motivates towards quality work as

emphasis is placed on doing

comparison of strength and weakness in

against to the rest of the company

Provides insufficient information for

future

It may results into lack of customer

satisfaction

By doing analysis, it has assessed that KEF Ltd uses balance scorecard tool because it

assists in making evaluation of business performance from all perspectives. It clearly indicates

areas, financial and non-financial, whereas changes need to be done for achieving success. In

comparison to this, Corus Ltd employs variance analysis tool for identifying problems take place

in business operations. However, such technique sometimes places negative impact on employee

motivation. Moreover, when firm fails to sets appropriate standards then it may result into high

deviations. Thus, it can be mentioned that techniques undertaken by KEF Ltd are highly effectual

over Corus Ltd.

STRATEGIC PLANNING

a. Assessing applicability of strategic planning tools

There are mainly two tools which can be used by KEF Ltd for the purpose of strategic

planning such as:

SWOT analysis: This tool of strategic planning is highly prominent which assists

company in identifying areas where effectual measure need tobe undertaken for the

purpose of performance improvement.

Balance scorecard: In the context of KEF Ltd performance of business unit can be

evaluated from the perspective of both financial and non-financial. Thus, by using this

firm can take appropriate measure for future growth.

B. Explaining how companies are using strategic planning tools for performance improvement

and future planning

In the context of KEF Ltd, management team develops strategic and policy framework by

taking into account into account weaknesses, threats and opportunities identified. Moreover, by

using existing strengths KEF Ltd would become able to capitalize opportunities available. In

addition to this, SWOT analysis tool also enables firm to take suitable measure in relation to

overcoming weaknesses and reducing threat level imposed. Thus, it can be presented that SWOT

analysis tool is highly significant which help in improving overall business performance and

profitability as well.

Further, company is also undertaking balance scorecard tool for ensuring alignment of

strategies with organizational vision and mission. As, such tool helps in evaluating performance

from several perspectives such learning& growth, development, customers and financial. In this

way, balance scorecard tool helps company in taking appropriate decision for performance

improvement.

CONCLUSION

By summing up this report, it can be concluded that by employing inventory

management, cost accounting and job costing system KEF Ltd can do effectual monetary

planning. Besides this, it can be inferred from the evaluation that through the means of

managerial report KEF Ltd can take appropriate decision about near future. Further, it has been

articulated that business unit should focus on undertaking absorption costing system over

marginal. The rationale behind this, absorption costing method presents suitable view of cost by

considering both fixed and variable production expenses. Along with this, it can be seen in the

report that activity based, capital budgeting, operating budget etc provides high level of

assistance in exerting control over undesirable activities. Thus, by removing redundant activities

from operations KEF Ltd can ensure optimum usage of funds. It can be summarized from the

report that by employing MA tools business unit can deal with monetary problems prominently.

and future planning

In the context of KEF Ltd, management team develops strategic and policy framework by

taking into account into account weaknesses, threats and opportunities identified. Moreover, by

using existing strengths KEF Ltd would become able to capitalize opportunities available. In

addition to this, SWOT analysis tool also enables firm to take suitable measure in relation to

overcoming weaknesses and reducing threat level imposed. Thus, it can be presented that SWOT

analysis tool is highly significant which help in improving overall business performance and

profitability as well.

Further, company is also undertaking balance scorecard tool for ensuring alignment of

strategies with organizational vision and mission. As, such tool helps in evaluating performance

from several perspectives such learning& growth, development, customers and financial. In this

way, balance scorecard tool helps company in taking appropriate decision for performance

improvement.

CONCLUSION

By summing up this report, it can be concluded that by employing inventory

management, cost accounting and job costing system KEF Ltd can do effectual monetary

planning. Besides this, it can be inferred from the evaluation that through the means of

managerial report KEF Ltd can take appropriate decision about near future. Further, it has been

articulated that business unit should focus on undertaking absorption costing system over

marginal. The rationale behind this, absorption costing method presents suitable view of cost by

considering both fixed and variable production expenses. Along with this, it can be seen in the

report that activity based, capital budgeting, operating budget etc provides high level of

assistance in exerting control over undesirable activities. Thus, by removing redundant activities

from operations KEF Ltd can ensure optimum usage of funds. It can be summarized from the

report that by employing MA tools business unit can deal with monetary problems prominently.

REFERENCES

Books and Journals

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance. 7(01). p.1650014.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-1025.

Eldenburg, L.G., Krishnan, H.A. and Krishnan, R., 2017. Management accounting and control in

the hospital industry: A review. Journal of Governmental & Nonprofit Accounting. 6(1).

pp.52-91

Endrikat, J., Hartmann, F. and Schreck, P., 2017. Social and ethical issues in management

accounting and control: an editorial.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting

research. Critical Perspectives on Accounting. 45. pp.63-80.

Konopczak, K. and Welfe, A., 2017. Convergence-driven inflation and the channels of its

absorption. Journal of Policy Modeling. 39(6). pp.1019-1034.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of cleaner production. 180. pp.297-306.

Lopez-Valeiras, E., Gomez-Conde, J. and Naranjo-Gil, D., 2015. Sustainable innovation,

management accounting and control systems, and international performance.

Sustainability. 7(3). pp.3479-3492.

Books and Journals

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance. 7(01). p.1650014.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-1025.

Eldenburg, L.G., Krishnan, H.A. and Krishnan, R., 2017. Management accounting and control in

the hospital industry: A review. Journal of Governmental & Nonprofit Accounting. 6(1).

pp.52-91

Endrikat, J., Hartmann, F. and Schreck, P., 2017. Social and ethical issues in management

accounting and control: an editorial.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting

research. Critical Perspectives on Accounting. 45. pp.63-80.

Konopczak, K. and Welfe, A., 2017. Convergence-driven inflation and the channels of its

absorption. Journal of Policy Modeling. 39(6). pp.1019-1034.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of cleaner production. 180. pp.297-306.

Lopez-Valeiras, E., Gomez-Conde, J. and Naranjo-Gil, D., 2015. Sustainable innovation,

management accounting and control systems, and international performance.

Sustainability. 7(3). pp.3479-3492.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136. pp.237-

248.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research. 31. pp.31-44.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and decision

making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1, pp. 66-

82). Taylor & Francis.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Ray, K. and Gramlich, J., 2015. Reconciling full-cost and marginal-cost pricing. Journal of

Management Accounting Research. 28(1). pp.27-37.

Sands, J., Lee, K.H. and Gunarathne, N., 2015. Environmental Management Accounting (EMA)

for environmental management and organizational change. Journal of Accounting &

Organizational Change.

Soderstrom, K.M., Soderstrom, N.S. and Stewart, C.R., 2017. Sustainability/CSR Research in

Management Accounting: A Review of the Literature', Advances in Management

Accounting (Advances in Management Accounting, Volume 28).

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online

Capital Budgeting – Advantages and Disadvantages. 2019. Online. Available through: <

https://efinancemanagement.com/investment-decisions/capital-budgeting-advantages-and-

disadvantages>.

Zero Based Budgeting – Advantages and Disadvantages. 2019. Online. Available through: <

https://efinancemanagement.com/budgeting/zero-based>.

management accounting, control, and reporting. Journal of Cleaner Production. 136. pp.237-

248.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research. 31. pp.31-44.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and decision

making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1, pp. 66-

82). Taylor & Francis.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Ray, K. and Gramlich, J., 2015. Reconciling full-cost and marginal-cost pricing. Journal of

Management Accounting Research. 28(1). pp.27-37.

Sands, J., Lee, K.H. and Gunarathne, N., 2015. Environmental Management Accounting (EMA)

for environmental management and organizational change. Journal of Accounting &

Organizational Change.

Soderstrom, K.M., Soderstrom, N.S. and Stewart, C.R., 2017. Sustainability/CSR Research in

Management Accounting: A Review of the Literature', Advances in Management

Accounting (Advances in Management Accounting, Volume 28).

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online

Capital Budgeting – Advantages and Disadvantages. 2019. Online. Available through: <

https://efinancemanagement.com/investment-decisions/capital-budgeting-advantages-and-

disadvantages>.

Zero Based Budgeting – Advantages and Disadvantages. 2019. Online. Available through: <

https://efinancemanagement.com/budgeting/zero-based>.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.