Comprehensive Management Accounting and Budgeting Report - Analysis

VerifiedAdded on 2020/06/04

|16

|4380

|33

Report

AI Summary

This report provides a comprehensive overview of Management Accounting Systems, focusing on their functions and importance in decision-making. It explores the differences between management and financial accounting, emphasizing the role of management accounting information as a decision-making tool for department managers. The report delves into various costing systems, including actual, normal, and standard costing, and discusses inventory and job costing systems. It presents different types of managerial accounting reports, such as accounts receivable aging reports and budget reports, highlighting the importance of presenting information in an understandable format. The report further analyzes costing methods, including absorption and marginal costing, and examines different kinds of budgets, their advantages, and disadvantages, including incremental and zero-based budgeting. The report also discusses the budget preparation process, determination of pricing, and the importance of budgets for planning and control purposes, as well as the role of management accounting in addressing organizational financial problems. The report is aimed at providing a thorough understanding of the key concepts and applications of management accounting within the context of Tech (UK) Limited.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Report.....................................................................................................................................1

(a) Management accounting and essential requirements of management accounting system:1

(b) Presenting financial information.......................................................................................4

TASK 2............................................................................................................................................5

a) Absorption Costing.............................................................................................................5

b) Marginal Costing................................................................................................................5

TASK 3............................................................................................................................................6

(a) Different kinds of budgets and their advantages and disadvantages................................6

(b) Budget preparation process – determination of pricing and different costing systems....8

(c) Importance of budget as a tool for planning and control purposes...................................9

TASK 4..........................................................................................................................................10

Management accounting system subject to respond financial problems of organisation. . .10

CONCLUSION.............................................................................................................................11

REFERENCES..............................................................................................................................12

.......................................................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Report.....................................................................................................................................1

(a) Management accounting and essential requirements of management accounting system:1

(b) Presenting financial information.......................................................................................4

TASK 2............................................................................................................................................5

a) Absorption Costing.............................................................................................................5

b) Marginal Costing................................................................................................................5

TASK 3............................................................................................................................................6

(a) Different kinds of budgets and their advantages and disadvantages................................6

(b) Budget preparation process – determination of pricing and different costing systems....8

(c) Importance of budget as a tool for planning and control purposes...................................9

TASK 4..........................................................................................................................................10

Management accounting system subject to respond financial problems of organisation. . .10

CONCLUSION.............................................................................................................................11

REFERENCES..............................................................................................................................12

.......................................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is used by managers for taking guidance from the provisions of

information to get support while taking decisions for an organisation. Overall, it is a profession

that involves partnership in management's division planning, performance management and

decision-making systems (Anandarajan and Srinivasan, 2012). It also provides expertise in the

financial reporting to support management in implementation of organisational strategies.

In this report, income of Tech (UK) limited which produces special charger will be

identified on marginal and absorption costing methods. There are four tasks discussed in this

report out of which in Task 1, a report is written to Director of Finance to explain the functions

of Management Accounting Systems. Task 3 consists of calculation of marginal and absorption

costing to find income of a company. Final task consists of balanced score card of company. The

main objective of this report is to explain learning outcomes of Management Accounting Reports

and Budgeting Systems.

TASK 1

Report

From: Trainee Management Accountant

To: Director of Finance

Subject: Functions of Management Accounting Systems

This Report is based on the concept of functions of Management Accounting Systems.

Discussions on improvement of decision-making through proper utilisation of financial

information has been discussed in this report.

(a) Management accounting and essential requirements of management accounting system:

Management accounting provides financial information to every organisation to help them in

decision-making process (Bac, 2013). It also provides guidelines which are related to the

explanation about how to utilise financial data properly.

1. Management Accounting Vs. Financial Accounting:

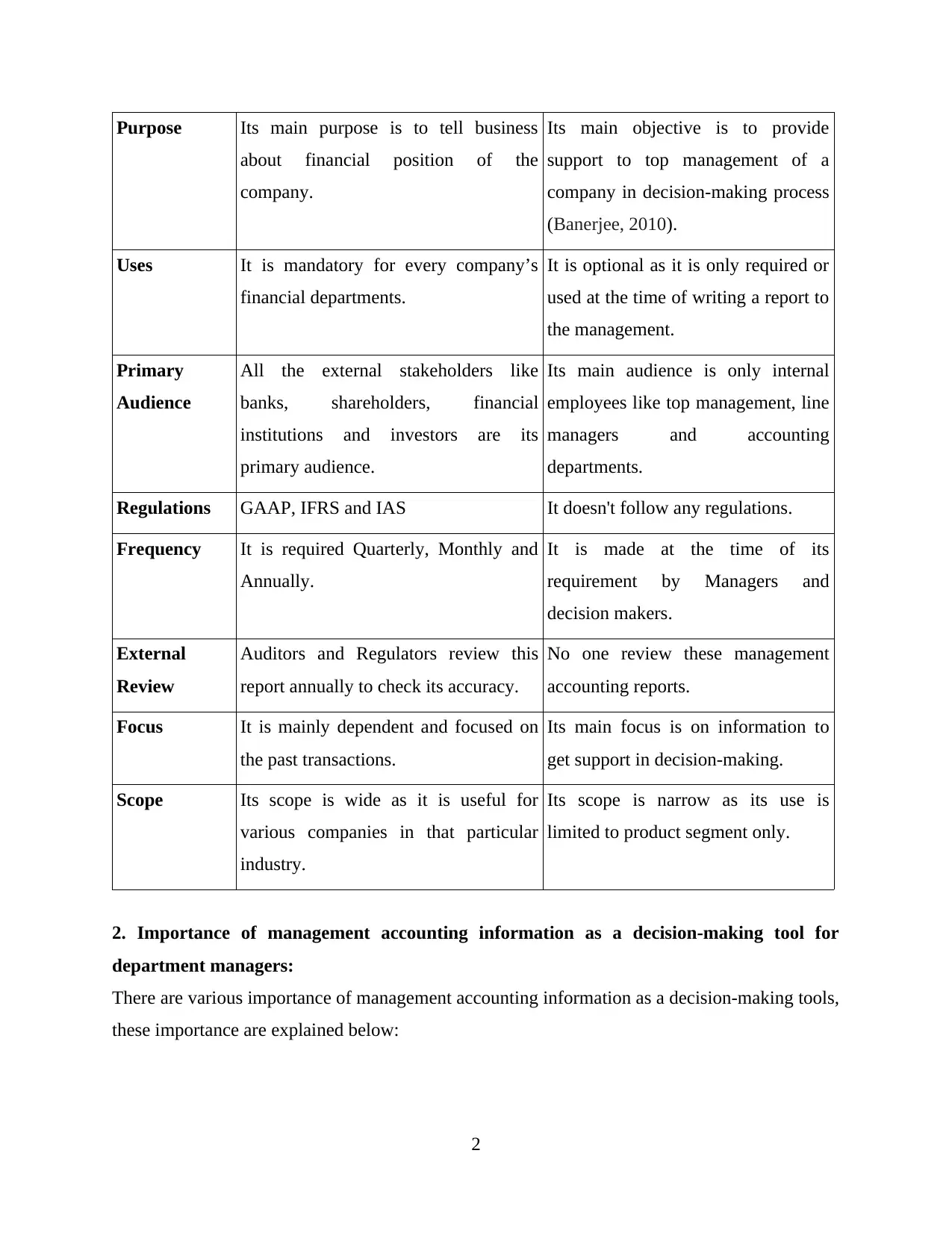

Management accounting is different from financial Standard. Some of the basic differences have

been discussed as below:

Basis Financial Accounting Management Accounting

1

Management accounting is used by managers for taking guidance from the provisions of

information to get support while taking decisions for an organisation. Overall, it is a profession

that involves partnership in management's division planning, performance management and

decision-making systems (Anandarajan and Srinivasan, 2012). It also provides expertise in the

financial reporting to support management in implementation of organisational strategies.

In this report, income of Tech (UK) limited which produces special charger will be

identified on marginal and absorption costing methods. There are four tasks discussed in this

report out of which in Task 1, a report is written to Director of Finance to explain the functions

of Management Accounting Systems. Task 3 consists of calculation of marginal and absorption

costing to find income of a company. Final task consists of balanced score card of company. The

main objective of this report is to explain learning outcomes of Management Accounting Reports

and Budgeting Systems.

TASK 1

Report

From: Trainee Management Accountant

To: Director of Finance

Subject: Functions of Management Accounting Systems

This Report is based on the concept of functions of Management Accounting Systems.

Discussions on improvement of decision-making through proper utilisation of financial

information has been discussed in this report.

(a) Management accounting and essential requirements of management accounting system:

Management accounting provides financial information to every organisation to help them in

decision-making process (Bac, 2013). It also provides guidelines which are related to the

explanation about how to utilise financial data properly.

1. Management Accounting Vs. Financial Accounting:

Management accounting is different from financial Standard. Some of the basic differences have

been discussed as below:

Basis Financial Accounting Management Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purpose Its main purpose is to tell business

about financial position of the

company.

Its main objective is to provide

support to top management of a

company in decision-making process

(Banerjee, 2010).

Uses It is mandatory for every company’s

financial departments.

It is optional as it is only required or

used at the time of writing a report to

the management.

Primary

Audience

All the external stakeholders like

banks, shareholders, financial

institutions and investors are its

primary audience.

Its main audience is only internal

employees like top management, line

managers and accounting

departments.

Regulations GAAP, IFRS and IAS It doesn't follow any regulations.

Frequency It is required Quarterly, Monthly and

Annually.

It is made at the time of its

requirement by Managers and

decision makers.

External

Review

Auditors and Regulators review this

report annually to check its accuracy.

No one review these management

accounting reports.

Focus It is mainly dependent and focused on

the past transactions.

Its main focus is on information to

get support in decision-making.

Scope Its scope is wide as it is useful for

various companies in that particular

industry.

Its scope is narrow as its use is

limited to product segment only.

2. Importance of management accounting information as a decision-making tool for

department managers:

There are various importance of management accounting information as a decision-making tools,

these importance are explained below:

2

about financial position of the

company.

Its main objective is to provide

support to top management of a

company in decision-making process

(Banerjee, 2010).

Uses It is mandatory for every company’s

financial departments.

It is optional as it is only required or

used at the time of writing a report to

the management.

Primary

Audience

All the external stakeholders like

banks, shareholders, financial

institutions and investors are its

primary audience.

Its main audience is only internal

employees like top management, line

managers and accounting

departments.

Regulations GAAP, IFRS and IAS It doesn't follow any regulations.

Frequency It is required Quarterly, Monthly and

Annually.

It is made at the time of its

requirement by Managers and

decision makers.

External

Review

Auditors and Regulators review this

report annually to check its accuracy.

No one review these management

accounting reports.

Focus It is mainly dependent and focused on

the past transactions.

Its main focus is on information to

get support in decision-making.

Scope Its scope is wide as it is useful for

various companies in that particular

industry.

Its scope is narrow as its use is

limited to product segment only.

2. Importance of management accounting information as a decision-making tool for

department managers:

There are various importance of management accounting information as a decision-making tools,

these importance are explained below:

2

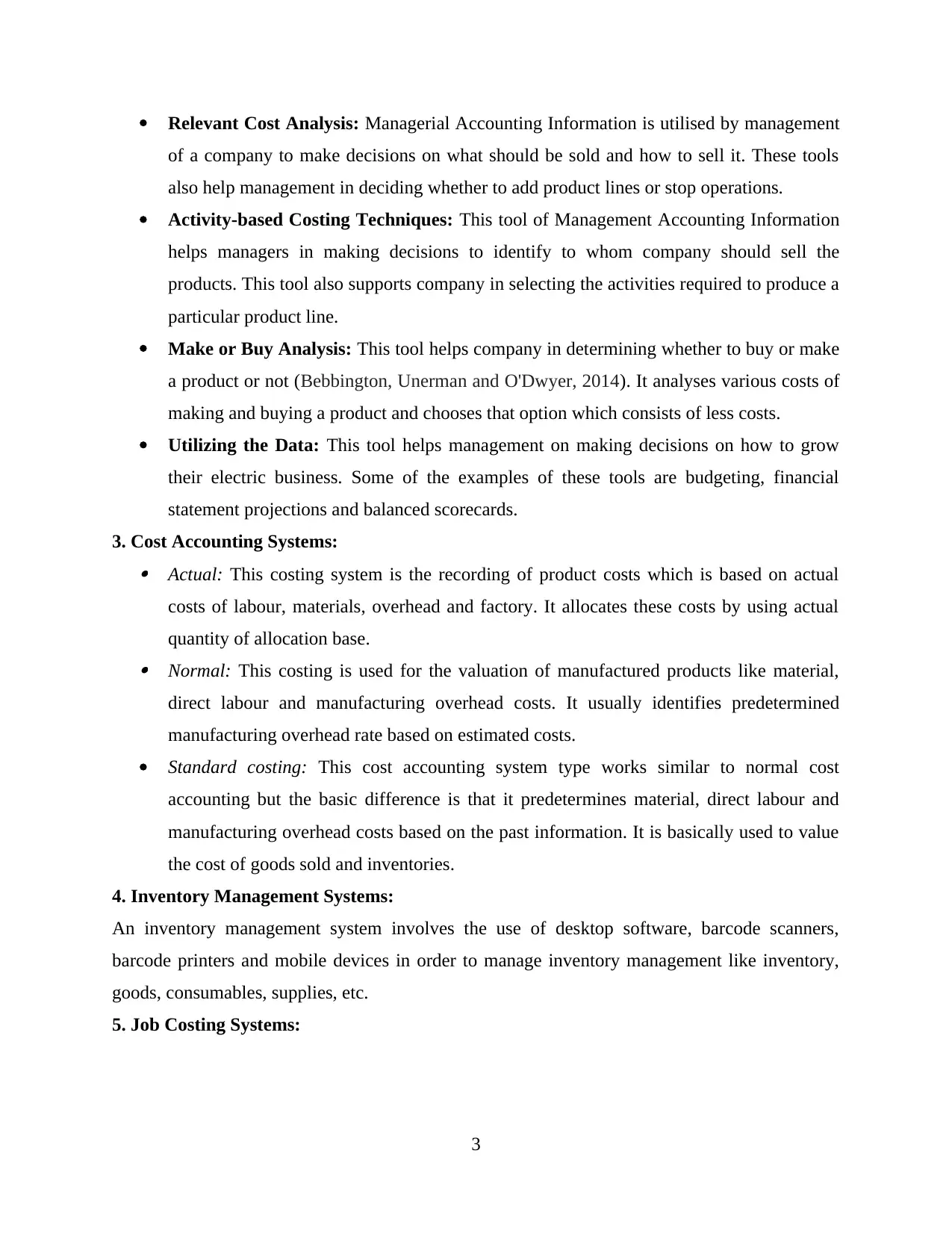

Relevant Cost Analysis: Managerial Accounting Information is utilised by management

of a company to make decisions on what should be sold and how to sell it. These tools

also help management in deciding whether to add product lines or stop operations.

Activity-based Costing Techniques: This tool of Management Accounting Information

helps managers in making decisions to identify to whom company should sell the

products. This tool also supports company in selecting the activities required to produce a

particular product line.

Make or Buy Analysis: This tool helps company in determining whether to buy or make

a product or not (Bebbington, Unerman and O'Dwyer, 2014). It analyses various costs of

making and buying a product and chooses that option which consists of less costs.

Utilizing the Data: This tool helps management on making decisions on how to grow

their electric business. Some of the examples of these tools are budgeting, financial

statement projections and balanced scorecards.

3. Cost Accounting Systems: Actual: This costing system is the recording of product costs which is based on actual

costs of labour, materials, overhead and factory. It allocates these costs by using actual

quantity of allocation base. Normal: This costing is used for the valuation of manufactured products like material,

direct labour and manufacturing overhead costs. It usually identifies predetermined

manufacturing overhead rate based on estimated costs.

Standard costing: This cost accounting system type works similar to normal cost

accounting but the basic difference is that it predetermines material, direct labour and

manufacturing overhead costs based on the past information. It is basically used to value

the cost of goods sold and inventories.

4. Inventory Management Systems:

An inventory management system involves the use of desktop software, barcode scanners,

barcode printers and mobile devices in order to manage inventory management like inventory,

goods, consumables, supplies, etc.

5. Job Costing Systems:

3

of a company to make decisions on what should be sold and how to sell it. These tools

also help management in deciding whether to add product lines or stop operations.

Activity-based Costing Techniques: This tool of Management Accounting Information

helps managers in making decisions to identify to whom company should sell the

products. This tool also supports company in selecting the activities required to produce a

particular product line.

Make or Buy Analysis: This tool helps company in determining whether to buy or make

a product or not (Bebbington, Unerman and O'Dwyer, 2014). It analyses various costs of

making and buying a product and chooses that option which consists of less costs.

Utilizing the Data: This tool helps management on making decisions on how to grow

their electric business. Some of the examples of these tools are budgeting, financial

statement projections and balanced scorecards.

3. Cost Accounting Systems: Actual: This costing system is the recording of product costs which is based on actual

costs of labour, materials, overhead and factory. It allocates these costs by using actual

quantity of allocation base. Normal: This costing is used for the valuation of manufactured products like material,

direct labour and manufacturing overhead costs. It usually identifies predetermined

manufacturing overhead rate based on estimated costs.

Standard costing: This cost accounting system type works similar to normal cost

accounting but the basic difference is that it predetermines material, direct labour and

manufacturing overhead costs based on the past information. It is basically used to value

the cost of goods sold and inventories.

4. Inventory Management Systems:

An inventory management system involves the use of desktop software, barcode scanners,

barcode printers and mobile devices in order to manage inventory management like inventory,

goods, consumables, supplies, etc.

5. Job Costing Systems:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

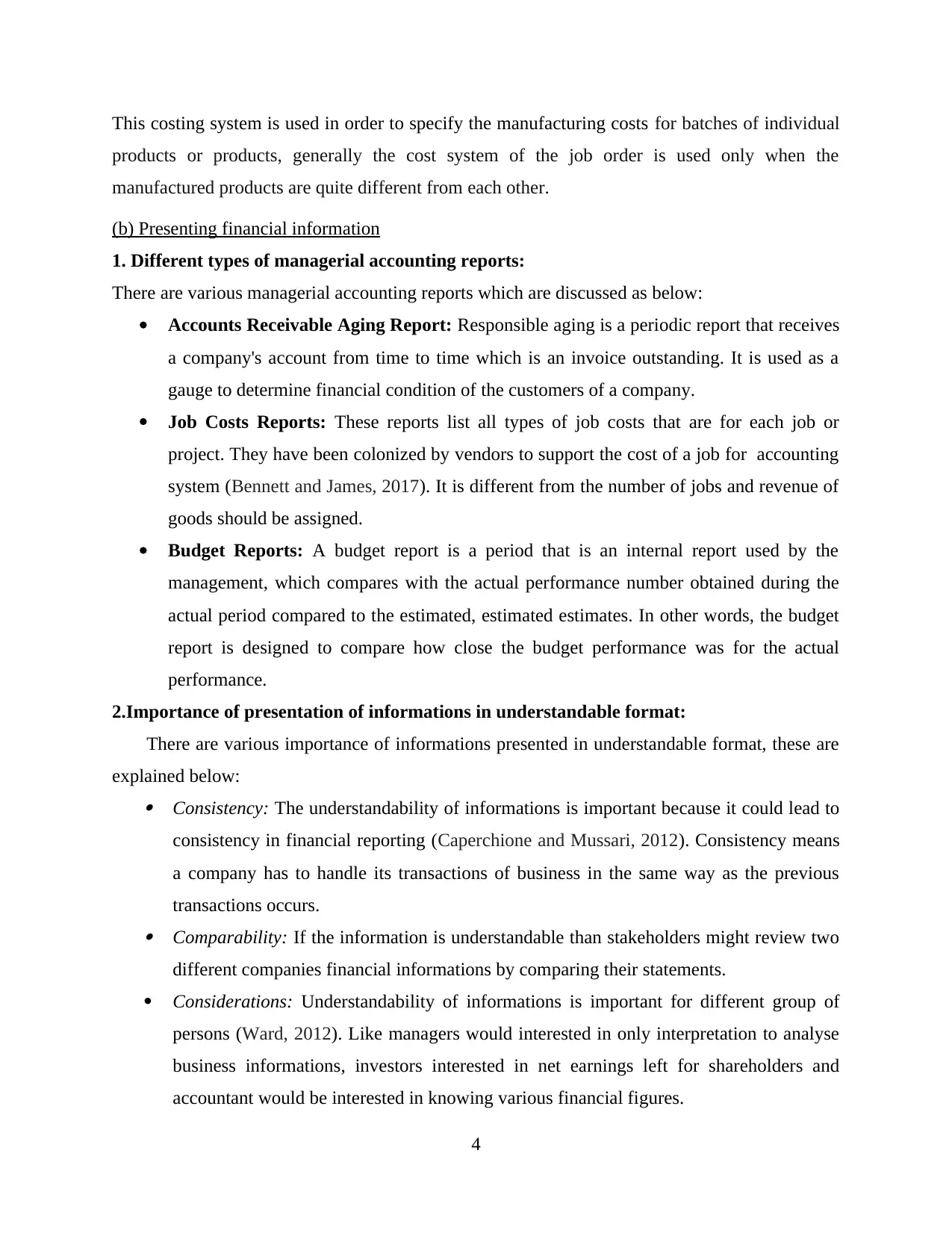

This costing system is used in order to specify the manufacturing costs for batches of individual

products or products, generally the cost system of the job order is used only when the

manufactured products are quite different from each other.

(b) Presenting financial information

1. Different types of managerial accounting reports:

There are various managerial accounting reports which are discussed as below:

Accounts Receivable Aging Report: Responsible aging is a periodic report that receives

a company's account from time to time which is an invoice outstanding. It is used as a

gauge to determine financial condition of the customers of a company.

Job Costs Reports: These reports list all types of job costs that are for each job or

project. They have been colonized by vendors to support the cost of a job for accounting

system (Bennett and James, 2017). It is different from the number of jobs and revenue of

goods should be assigned.

Budget Reports: A budget report is a period that is an internal report used by the

management, which compares with the actual performance number obtained during the

actual period compared to the estimated, estimated estimates. In other words, the budget

report is designed to compare how close the budget performance was for the actual

performance.

2.Importance of presentation of informations in understandable format:

There are various importance of informations presented in understandable format, these are

explained below: Consistency: The understandability of informations is important because it could lead to

consistency in financial reporting (Caperchione and Mussari, 2012). Consistency means

a company has to handle its transactions of business in the same way as the previous

transactions occurs. Comparability: If the information is understandable than stakeholders might review two

different companies financial informations by comparing their statements.

Considerations: Understandability of informations is important for different group of

persons (Ward, 2012). Like managers would interested in only interpretation to analyse

business informations, investors interested in net earnings left for shareholders and

accountant would be interested in knowing various financial figures.

4

products or products, generally the cost system of the job order is used only when the

manufactured products are quite different from each other.

(b) Presenting financial information

1. Different types of managerial accounting reports:

There are various managerial accounting reports which are discussed as below:

Accounts Receivable Aging Report: Responsible aging is a periodic report that receives

a company's account from time to time which is an invoice outstanding. It is used as a

gauge to determine financial condition of the customers of a company.

Job Costs Reports: These reports list all types of job costs that are for each job or

project. They have been colonized by vendors to support the cost of a job for accounting

system (Bennett and James, 2017). It is different from the number of jobs and revenue of

goods should be assigned.

Budget Reports: A budget report is a period that is an internal report used by the

management, which compares with the actual performance number obtained during the

actual period compared to the estimated, estimated estimates. In other words, the budget

report is designed to compare how close the budget performance was for the actual

performance.

2.Importance of presentation of informations in understandable format:

There are various importance of informations presented in understandable format, these are

explained below: Consistency: The understandability of informations is important because it could lead to

consistency in financial reporting (Caperchione and Mussari, 2012). Consistency means

a company has to handle its transactions of business in the same way as the previous

transactions occurs. Comparability: If the information is understandable than stakeholders might review two

different companies financial informations by comparing their statements.

Considerations: Understandability of informations is important for different group of

persons (Ward, 2012). Like managers would interested in only interpretation to analyse

business informations, investors interested in net earnings left for shareholders and

accountant would be interested in knowing various financial figures.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

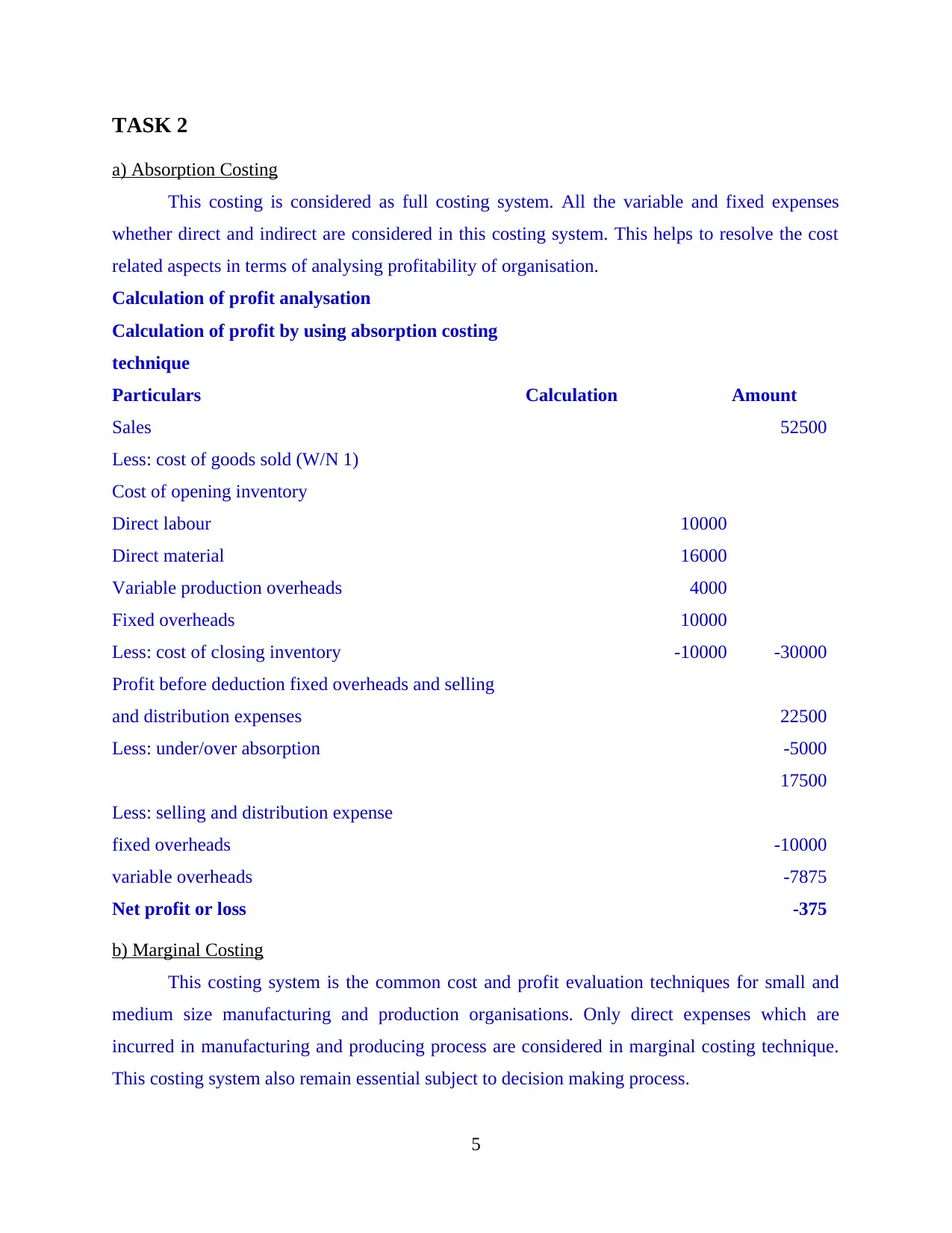

a) Absorption Costing

This costing is considered as full costing system. All the variable and fixed expenses

whether direct and indirect are considered in this costing system. This helps to resolve the cost

related aspects in terms of analysing profitability of organisation.

Calculation of profit analysation

Calculation of profit by using absorption costing

technique

Particulars Calculation Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling

and distribution expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

b) Marginal Costing

This costing system is the common cost and profit evaluation techniques for small and

medium size manufacturing and production organisations. Only direct expenses which are

incurred in manufacturing and producing process are considered in marginal costing technique.

This costing system also remain essential subject to decision making process.

5

a) Absorption Costing

This costing is considered as full costing system. All the variable and fixed expenses

whether direct and indirect are considered in this costing system. This helps to resolve the cost

related aspects in terms of analysing profitability of organisation.

Calculation of profit analysation

Calculation of profit by using absorption costing

technique

Particulars Calculation Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling

and distribution expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

b) Marginal Costing

This costing system is the common cost and profit evaluation techniques for small and

medium size manufacturing and production organisations. Only direct expenses which are

incurred in manufacturing and producing process are considered in marginal costing technique.

This costing system also remain essential subject to decision making process.

5

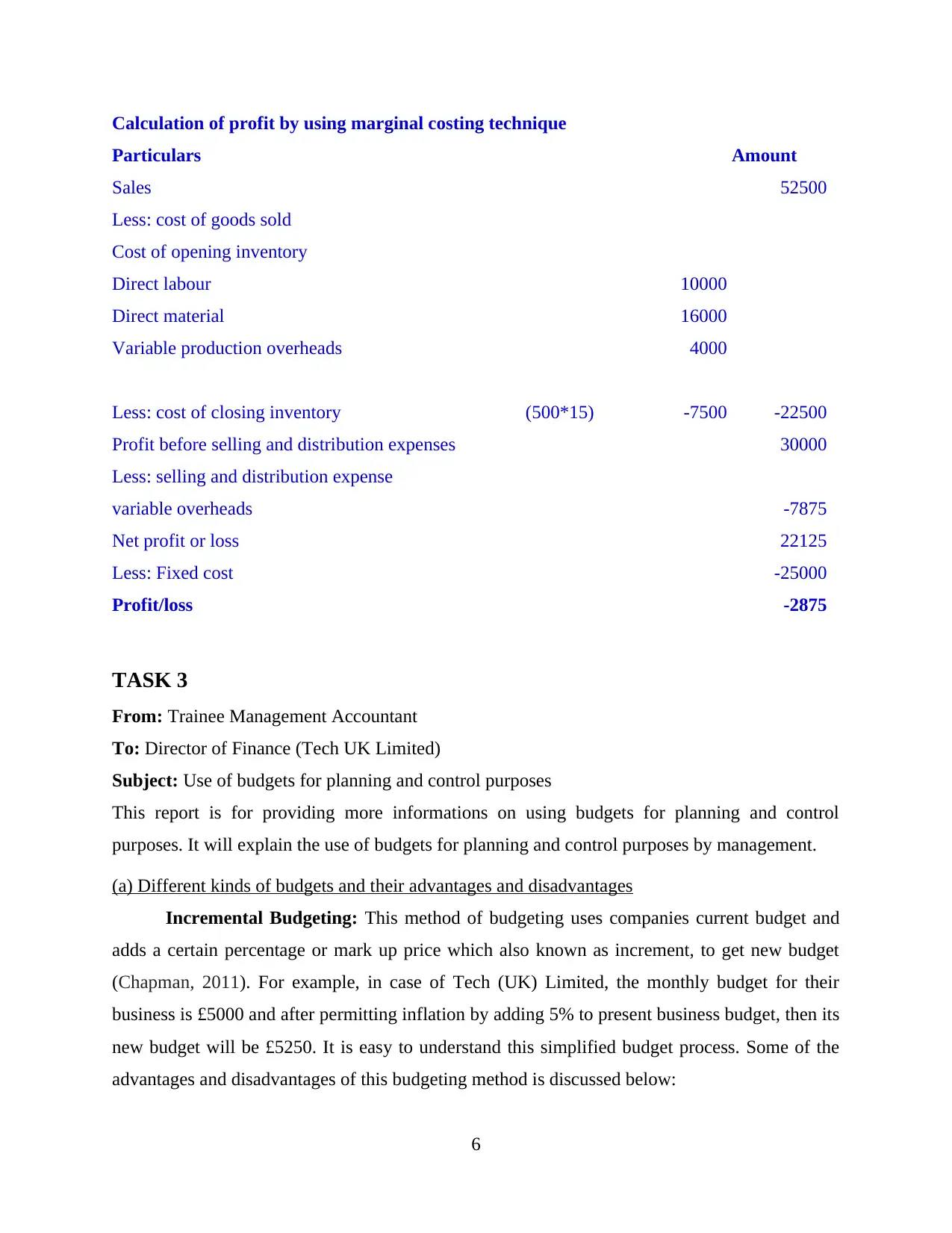

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory (500*15) -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

TASK 3

From: Trainee Management Accountant

To: Director of Finance (Tech UK Limited)

Subject: Use of budgets for planning and control purposes

This report is for providing more informations on using budgets for planning and control

purposes. It will explain the use of budgets for planning and control purposes by management.

(a) Different kinds of budgets and their advantages and disadvantages

Incremental Budgeting: This method of budgeting uses companies current budget and

adds a certain percentage or mark up price which also known as increment, to get new budget

(Chapman, 2011). For example, in case of Tech (UK) Limited, the monthly budget for their

business is £5000 and after permitting inflation by adding 5% to present business budget, then its

new budget will be £5250. It is easy to understand this simplified budget process. Some of the

advantages and disadvantages of this budgeting method is discussed below:

6

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory (500*15) -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

TASK 3

From: Trainee Management Accountant

To: Director of Finance (Tech UK Limited)

Subject: Use of budgets for planning and control purposes

This report is for providing more informations on using budgets for planning and control

purposes. It will explain the use of budgets for planning and control purposes by management.

(a) Different kinds of budgets and their advantages and disadvantages

Incremental Budgeting: This method of budgeting uses companies current budget and

adds a certain percentage or mark up price which also known as increment, to get new budget

(Chapman, 2011). For example, in case of Tech (UK) Limited, the monthly budget for their

business is £5000 and after permitting inflation by adding 5% to present business budget, then its

new budget will be £5250. It is easy to understand this simplified budget process. Some of the

advantages and disadvantages of this budgeting method is discussed below:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages:

It is easy to prepare and generalised a budget.

The costs of preparing budget of this method of budgeting is usually low.

It is easy to understand by every one.

It can reduce conflicts between various staffs because all departments of a company have

equal amount of money to spend on their business activities.

Disadvantage:

The budget made through this method is not accurate, as only adding some value to a

budget is not enough.

This budget is rigid, because this method doesn't allow any further changes after the

preparation of a budget.

There's no incentives given to employees who is putting their efforts in reducing costs of

production, increasing profits and improving productivity of a business.

Zero-based Budgeting: A zero-based budget or zero-sum is a popular method that gives

people a budget for their own personal and home expenses, but it can also be used for business

budgets (Chiarini and Vagnoni, 2015). In this method, the budget examines the value of a

business in order to ensure that they are necessary.

Zero-based budget is created in following three steps given below: Step 1: Activities are determined by managers. There activities are later utilises in

decision-making process. Step 2: In this step management gives ranks to each processes in order, this order later

sort in descending formats of benefits.

Step 3: Here in this final stage, funds are allocated to different budget proposals based on

their priorities.

Advantages:

Resource and funds are efficiently allocated.

It helps managers in driving cost reduction methods.

It recognizes wasteful activities and later eliminates such activities.

Disadvantages:

It is not an easy method, it contains complex steps and consumes lots of manpower and

time.

7

It is easy to prepare and generalised a budget.

The costs of preparing budget of this method of budgeting is usually low.

It is easy to understand by every one.

It can reduce conflicts between various staffs because all departments of a company have

equal amount of money to spend on their business activities.

Disadvantage:

The budget made through this method is not accurate, as only adding some value to a

budget is not enough.

This budget is rigid, because this method doesn't allow any further changes after the

preparation of a budget.

There's no incentives given to employees who is putting their efforts in reducing costs of

production, increasing profits and improving productivity of a business.

Zero-based Budgeting: A zero-based budget or zero-sum is a popular method that gives

people a budget for their own personal and home expenses, but it can also be used for business

budgets (Chiarini and Vagnoni, 2015). In this method, the budget examines the value of a

business in order to ensure that they are necessary.

Zero-based budget is created in following three steps given below: Step 1: Activities are determined by managers. There activities are later utilises in

decision-making process. Step 2: In this step management gives ranks to each processes in order, this order later

sort in descending formats of benefits.

Step 3: Here in this final stage, funds are allocated to different budget proposals based on

their priorities.

Advantages:

Resource and funds are efficiently allocated.

It helps managers in driving cost reduction methods.

It recognizes wasteful activities and later eliminates such activities.

Disadvantages:

It is not an easy method, it contains complex steps and consumes lots of manpower and

time.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Employees and managers requires necessary training to implement such a budget.

It is not suitable for large organisations, as large amount of informations are there. Using

these informations may requires critical details of it (Chiarini, 2012).

Due to the situation of over budget, internal conflicts between different employees might

rises.

Top Down Budgeting: Under this budgeting method, the highest level of business is done

within the business, you can work with any overhead management, spend estimates and the

estimated profit of your business and create a budget accordingly (Damodaran, 2012).

The main advantage of this method is that, a manager does not need to trust others to give

budget information and it can save time. But, if managers are not well-involved in the day-to-day

company's business, then they might not have all the information needed to use this budget

method. This may result in the allocation of resources in some areas and the allocation of

resources in others.

Advantages:

It takes less time to make a budget.

This method promotes upper-level delegation of authorities.

It helps management in addressing organisational objectives.

Disadvantages:

The major disadvantage of this method might be rises due to inaccurate decisions of

upper managers because of incomplete knowledge (Shields, 2015). This could result in

insufficient allocation of budgeted funds among various departments and their

performance might also decrease.

Due to eliminating involvement of subordinates, it can lower their morales.

Bottom-up budgeting: This method starts with determination of all the available risks that

are involved and effecting during implementation of a project. It raises the chances of working

out of resources and requirements of fund.

Advantages:

It provides clear and detailed informations to top management.

All employees are involved which increases their morale and motivation level.

Disadvantages:

Top management has a less control over whole budgeting process of this method.

8

It is not suitable for large organisations, as large amount of informations are there. Using

these informations may requires critical details of it (Chiarini, 2012).

Due to the situation of over budget, internal conflicts between different employees might

rises.

Top Down Budgeting: Under this budgeting method, the highest level of business is done

within the business, you can work with any overhead management, spend estimates and the

estimated profit of your business and create a budget accordingly (Damodaran, 2012).

The main advantage of this method is that, a manager does not need to trust others to give

budget information and it can save time. But, if managers are not well-involved in the day-to-day

company's business, then they might not have all the information needed to use this budget

method. This may result in the allocation of resources in some areas and the allocation of

resources in others.

Advantages:

It takes less time to make a budget.

This method promotes upper-level delegation of authorities.

It helps management in addressing organisational objectives.

Disadvantages:

The major disadvantage of this method might be rises due to inaccurate decisions of

upper managers because of incomplete knowledge (Shields, 2015). This could result in

insufficient allocation of budgeted funds among various departments and their

performance might also decrease.

Due to eliminating involvement of subordinates, it can lower their morales.

Bottom-up budgeting: This method starts with determination of all the available risks that

are involved and effecting during implementation of a project. It raises the chances of working

out of resources and requirements of fund.

Advantages:

It provides clear and detailed informations to top management.

All employees are involved which increases their morale and motivation level.

Disadvantages:

Top management has a less control over whole budgeting process of this method.

8

Lower level managers might not capable to cover all essential areas.

This method could exaggerated some parts of budget.

It is time consuming and costly method.

(b) Budget preparation process – determination of pricing and different costing systems

Below is the steps of budget preparation process: Obtaining Estimates: Departmental heads or managers need to estimate future

conditions and activities, which have an impact on the company. This step includes

estimates of sales, production levels, expected costs, and availability of resources from

each sub-unit/division/department. Here pricing and different costing methods will be

determined.

◦ Determination of Pricing: In this step, the cost of selling per item should include a

high profit margin. Order, while selling large quantities, the profit margin should be

less than the margin by selling per item. The reason for this is that the profit from sale

of many items will increase.

◦ Determination of different costing systems: Two types of costing systems are used in

the manufacturing sector. First is the cost of the process, it is a cost system which is

used in most public-production settings, analyses the net cost of the manufacturing

process (Renz, 2016). The second costing method is job-order costing, which is

concerned with tracking all the costs on an individual product basis.

Coordinating estimates: In this step, the Budget Committee evaluates the various

schemes offered by various organizational units, which determines the capacity of the

scheme in the overall interest of the company and estimates what the resources are

available and can be allocated a lot in different units of the organization.

Communicating Budget: At this stage, changes and modifications included in the final

budget should be known to managers for their support and effort for the budget.

Implementing the Budget Plan: After completing all above steps, the final budget is

then presented to top authorities which adopts these plans of operations for the future

budgets.

Feedback on progress towards budgeted objectives: As a feedback in the budget

process, performance reports are prepared to inform departmental managers and top

management about the performance received in the context of the budget report.

9

This method could exaggerated some parts of budget.

It is time consuming and costly method.

(b) Budget preparation process – determination of pricing and different costing systems

Below is the steps of budget preparation process: Obtaining Estimates: Departmental heads or managers need to estimate future

conditions and activities, which have an impact on the company. This step includes

estimates of sales, production levels, expected costs, and availability of resources from

each sub-unit/division/department. Here pricing and different costing methods will be

determined.

◦ Determination of Pricing: In this step, the cost of selling per item should include a

high profit margin. Order, while selling large quantities, the profit margin should be

less than the margin by selling per item. The reason for this is that the profit from sale

of many items will increase.

◦ Determination of different costing systems: Two types of costing systems are used in

the manufacturing sector. First is the cost of the process, it is a cost system which is

used in most public-production settings, analyses the net cost of the manufacturing

process (Renz, 2016). The second costing method is job-order costing, which is

concerned with tracking all the costs on an individual product basis.

Coordinating estimates: In this step, the Budget Committee evaluates the various

schemes offered by various organizational units, which determines the capacity of the

scheme in the overall interest of the company and estimates what the resources are

available and can be allocated a lot in different units of the organization.

Communicating Budget: At this stage, changes and modifications included in the final

budget should be known to managers for their support and effort for the budget.

Implementing the Budget Plan: After completing all above steps, the final budget is

then presented to top authorities which adopts these plans of operations for the future

budgets.

Feedback on progress towards budgeted objectives: As a feedback in the budget

process, performance reports are prepared to inform departmental managers and top

management about the performance received in the context of the budget report.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.