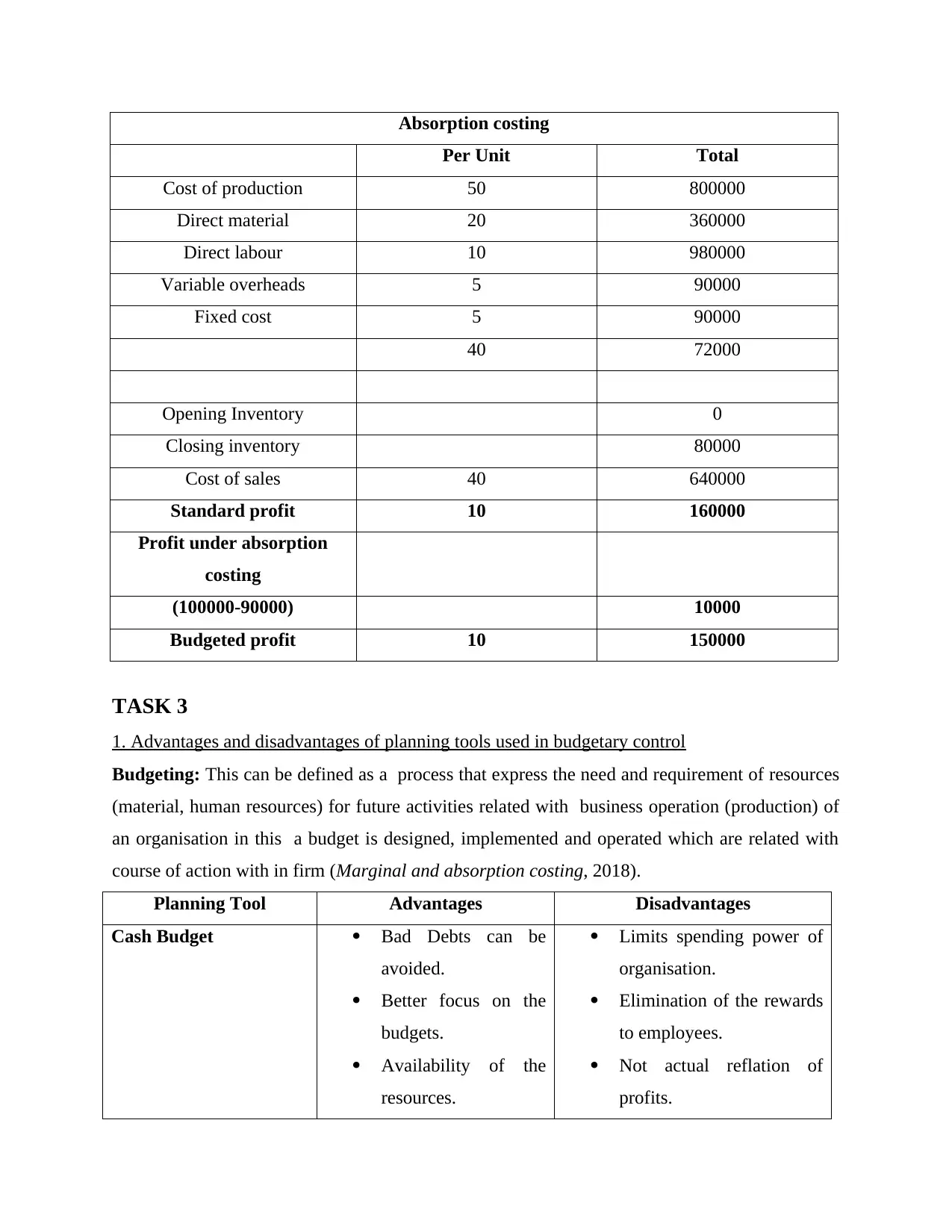

Management Accounting System Techniques and Reports for Jupiter Plc

VerifiedAdded on 2021/01/02

Accounting

Feedback

Paraphrase This Document

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1. Understanding of management accounting system................................................................1

2. Methods of management counting reporting..........................................................................2

3.Benefits of management accounting system and theirs application in Jupiter plc...................3

4. Integration of Managing accounting system and management accounting of reporting........5

TASK 2 ...........................................................................................................................................5

a) Marginal costing.....................................................................................................................5

b)Absorption costing...................................................................................................................5

TASK 3............................................................................................................................................6

1. Advantages and disadvantages of planning tools used in budgetary control..........................6

2. Use of different planning tools and their application in for preparation and forecasting

budget..........................................................................................................................................7

TASK 4............................................................................................................................................8

1.Adoption of management accounting system to respond to financial problems.....................8

2. Use of planning tools to respond and solve financial problems..............................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

REFERENCES................................................................................................................................2

Management accounting can be defined as tat branch of account in an organisation

which deal with presenting information to aid managers in the decision making processes. It

takes into consideration both financial information as well data related with other activities

occurred in business. With taking into consideration all these information reports are prepared

by which assist the decision making process of the organisation. In the present report an

application of different management accounting system techniques and reports are applied along

with their advantages and disadvantages for Jupiter Plc.

TASK 1

1. Understanding of management accounting system

Accounting: this can be defined as language of the business through which the

organisation speaks about its growth and profitability. This is a process of summarizing,

analysing and reporting of transactions to determine profits and to evaluate taxation liability of

the business.

Financials accounting: Under this a comprehensive record of financial transaction

pertaining to a financial year are kept which include both monitory and accrual transaction to

determined actual profits earned by the organisation.

Management accounting: This can be defined as preparation and providing on time

financial and statistical information to the management of Jupiter PLC to assize them in decision

making process. The decision are generally short term in nature. This is different from

financial accounting as in it financial reports are presented to internal stakeholders of the Jupiter

Plc as opposed to external stakeholder. The result of this system can be undertaken as

formulation of reports of the company, its different departments, mangers and CEO.

Essential requirements of different types of management accounting system:

Job costing: this is a method under which manufacturing cost related to a particular job

carried out in Jupiter Plc is recorded. With job costing system a project manager keeps track of

the cost related with every job. This aids them in evaluation of working capital requirement as

well as the amount that is spent on a particular job. Eg:

Inventory management system: this is a mathematical analytical tool which is used by

the management of the organisation for determination of how consumer will respond to different

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a price band is selected so that a price can be offered to consumer which is acceptable to them.

Inventory management: this can be defined as supervision of non capitalized assets and

stoke items that are used in production of articles in Jupiter Plc under this then the flow of raw

material from warehouse to production unit is supervised along with determination of future

requirement to produce estimate budgets units. Inventory method used in business are LIFO-

last in first out this method is banned by HMRC. Another method used id FIFO first in first out,

this means inventory winch came first shall be issues first in production line over the

inventories which comers at later dates.

Cost accounting: this can be defined as a frame work which is used by Jupiter plc to

estimate the cost of production of its article. This estimation aids the management in analysing

the profitability, inventory valuation and cost control of the organisation. Accurate estimation of

the cost related with production of a unit is a sign of profitable organisations.

Actual costing: This can be defined as recording the cost of product which is actually incurred

on its production. Such as actual cost of labour, material and overhead incurred in production.

Standard costing: Standard costing is an accounting technique that some manufacturers used to

identify the differences or variances between 1) the actual costs of the goods that were produced,

and 2) the costs that should have occurred for those goods

Normal costing: this is used for valuation of manufactured products with the actual material,

labour and overhead cost which is based on a predetermined rate.

2. Methods of management counting reporting

Management accounting reports are based on the information need of the management

and these are prepared by taking in to financial as well as statistical data from all the departments

of the Jupiter Plc. The reports prepared are very useful for the management of the organisation as

this helps them in deciding future action plan for the business (Van Helden and Uddin, 2016).

Different types of reports prepared under this system is:

Cost reporting: under this, profits margins are estimated and with this it is evaluated that

what is the actual cost that has been incurred on production and procurement of a unit of article.

Under this material expenses, labour cost, overhead cost and expenses related with each activity

undertaken in the organisation.

2

Paraphrase This Document

expenses etc are forecasted for future period. These are set as targets for the organisation which

it must have to accomplish with given budget and in stipulated time. Budgets are prepared for

almost every activity performed in organisation and is considered as important tool for

managerial control.

Performance report: this can be referred as performance evaluation of all the activities

as well as human resource of the Jupiter Plc. Under this actual performances is compared with

budgets or forecasted and the degree of deviation is determined and sections are taken to correct

the deviation to reach the actual results which were estimated before time.

Inventory management report:

3. Benefits of management accounting system and theirs application in Jupiter plc

Cost accounting system:

Advantages:

Elimination of waste, losses and inefficiency from the production and management.

Reduction in cost of production.

Identification of reason for profit and loss in the organisation,

Significant advice on make and buy decision as what will be more beneficial for the company

with to make the article or to buy the same from outside.

Disadvantages:

Consideration of past performance for making report on the basis of which future

decision are taken.

Previous year cost ado not remain dame in subsequent years so coat data are not so

useful.

Cost estimation is done on full utilization capacity and data for partiality used capacity

cannot be used in its true sense.

Job costing methodologies:

Advantages:

Calculation of the profits earned on each job performed in the organisation.

Provide manager detailed information on production statistics of individual departments.

3

and efficiency.

Disadvantages:

Detailed records related with labour and material used must be kept on order to assist in

calculations and determination of statistical data and actual output.

A close watch on records must be kept in order to determine actual cost and expenses

incurred on specific job and activity related with production.

Inventory management system:

Advantages:

Keeps a record of the available inventory in the stock.

Estimation of the future need of raw material require which is based on budgeted

production.

Evaluation of the stock which s used by each department separately which is determined

as the items issued to particular department.

Disadvantages:

Records cannot be kept for same inventories units such as nut, bolt etc.

using different method gives different results, and a change in the method of inventory

keeping in between an accounting periods can not give correct results.

Price optimisation:

Advantages:

this helps in determination of rate of return as with optimization of price cost is

controlled hence profits are enhanced.

Helps in controlling the cost.

This help in forecasting the cash flows and fund flows.

Disadvantages:

Difficult to determine the reaction that will be given by consumers on the prices of

products of the organisation.

Selectivity of consumers to price fluctuation can not betaken as a major factor to

determine the price.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Both management accounting system and management accounting reports are interrelated

with each other and it can be stated that both care non separable as with the use of different

methods of accounting system and assistance in reporting is taken. In preparation of the budgets

present and past data from the job and costing is taken and a future forecast and estimation is

prepared (Otley, 2016). With the accounting tools price of the product is estimated along with

analysing of data and information of production and related activities.

With the techniques of management accounting cost and expenses related with a

particular job and specific activities aid determine and this helps in preparation of costing report

as this taken into consideration expenses allocated and done by each department in Jupiter plc.

The organisation cab use both accounting system and report techniques to produces data and

information that can help the management in development of accurate plans and assist them in

taking short as well as long term decision.

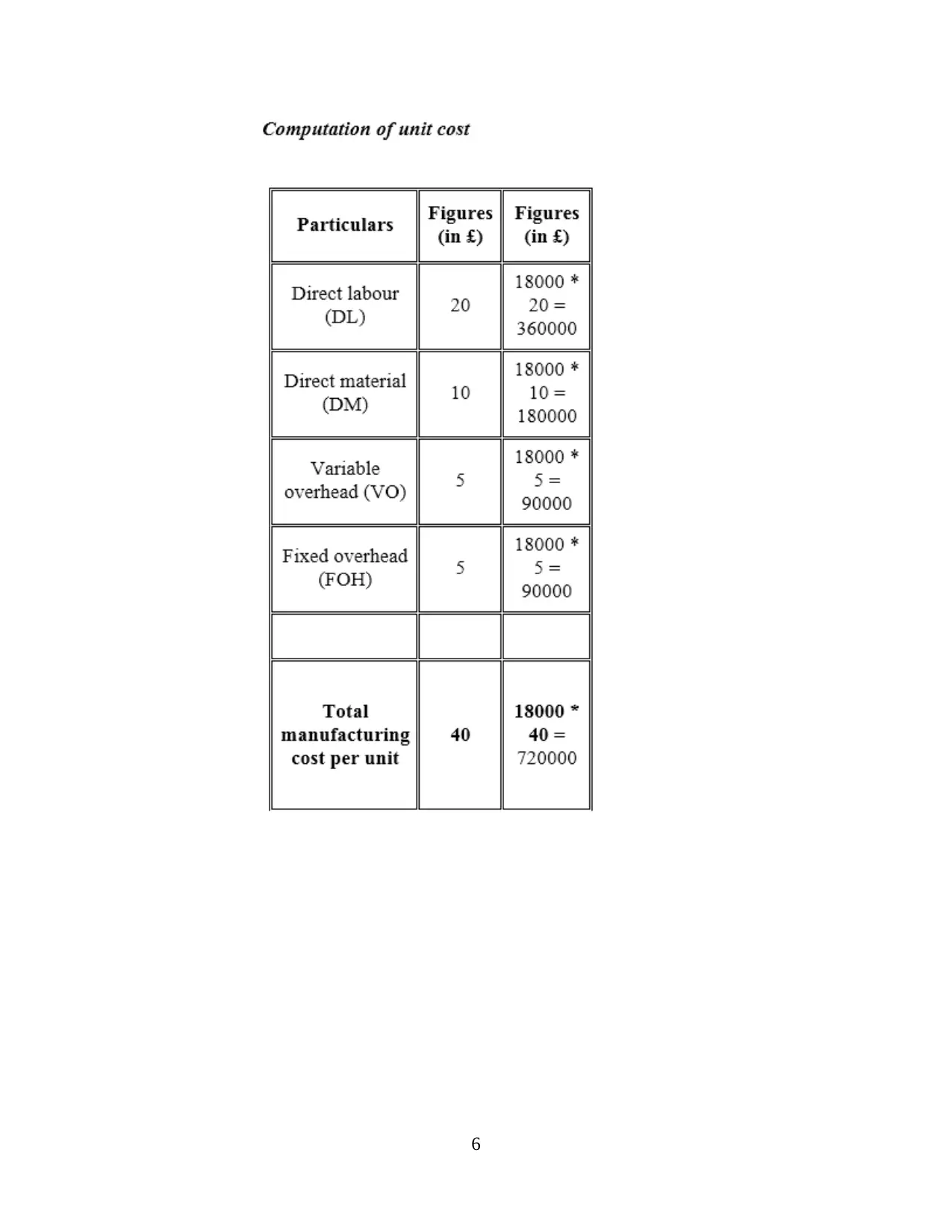

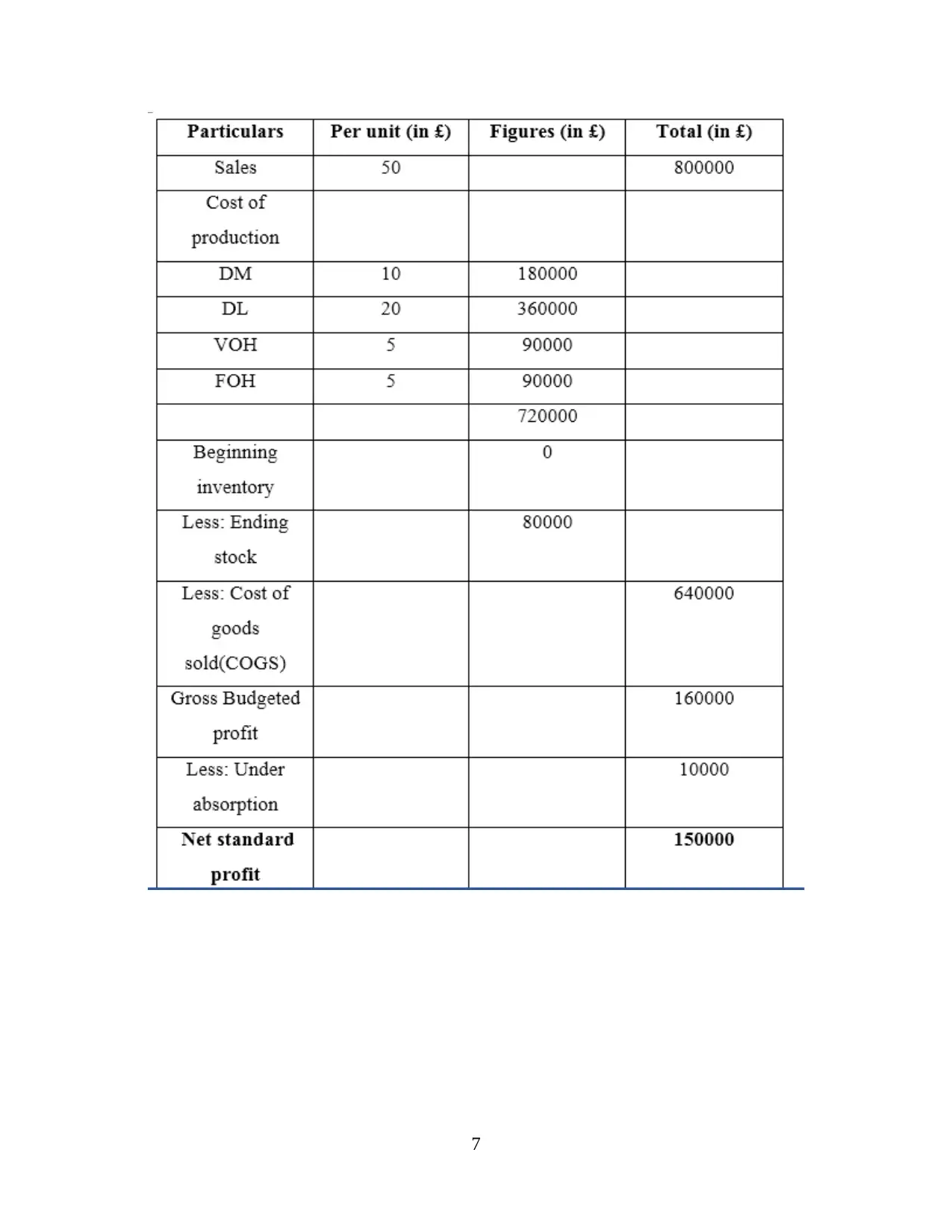

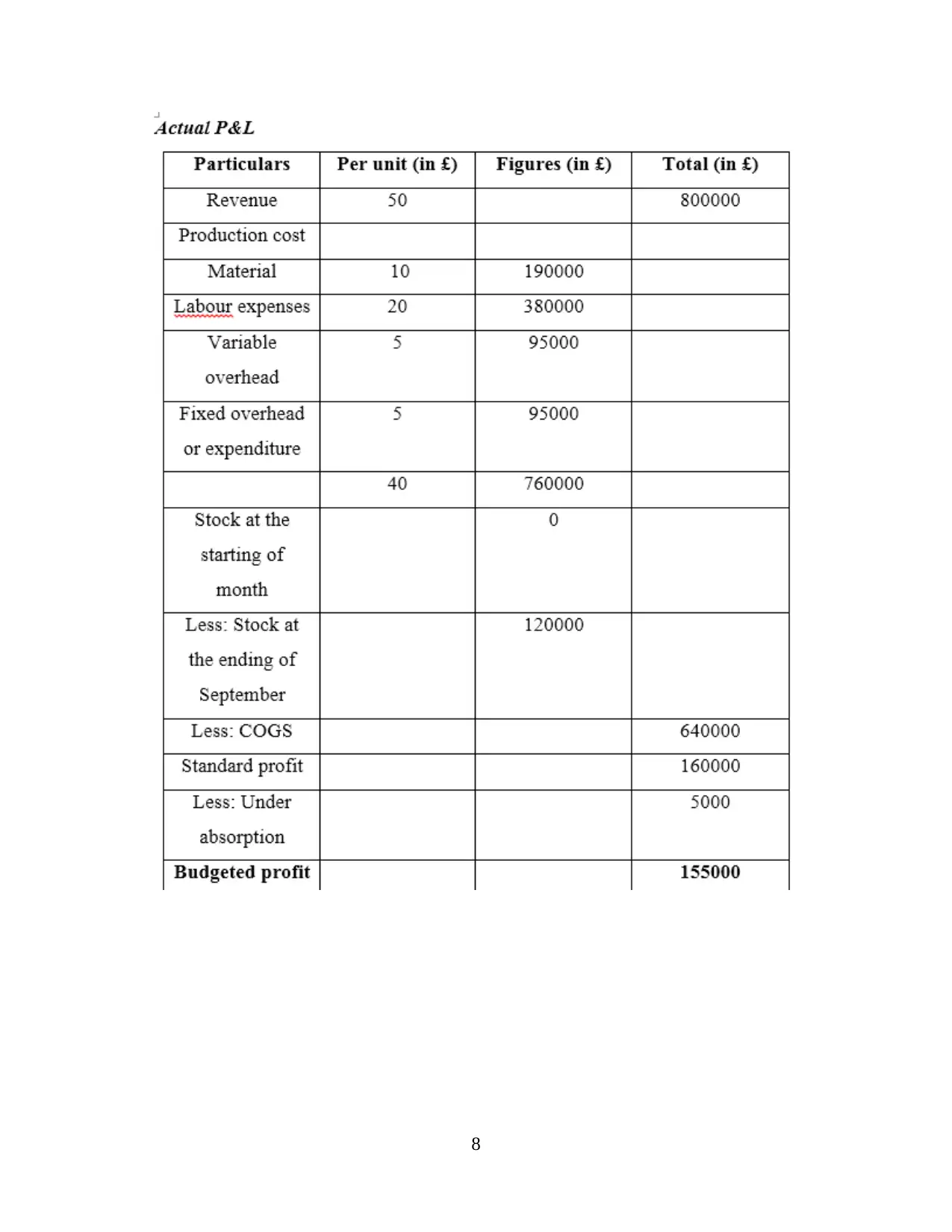

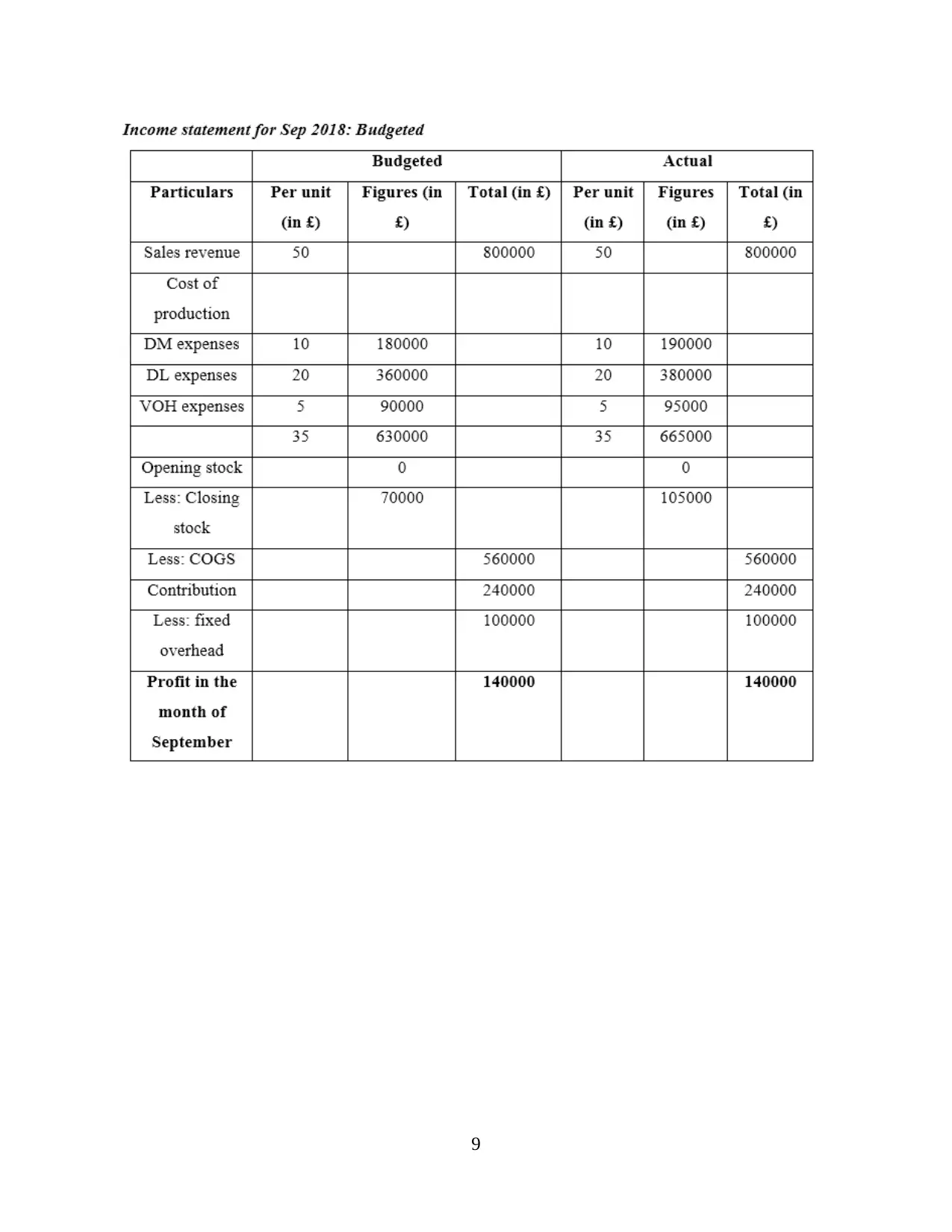

TASK 2

Application of manageable accounting techniques

a) Marginal costing

This is a method of accounting in which variable cost are charged to cost of production and all

fixed whether administrative or other overhead in period cost. Fixed cost is written off in ful

against contribution.

Marginal costing:

b)Absorption costing

Absorption costing: this can be defined as that method of costing which takes into

consideration all coast associated with manufacturing and production of a product. Under this

fixed overhead charges are take as part of production cots.

5

Paraphrase This Document

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Per Unit Total

Cost of production 50 800000

Direct material 20 360000

Direct labour 10 980000

Variable overheads 5 90000

Fixed cost 5 90000

40 72000

Opening Inventory 0

Closing inventory 80000

Cost of sales 40 640000

Standard profit 10 160000

Profit under absorption

costing

(100000-90000) 10000

Budgeted profit 10 150000

TASK 3

1. Advantages and disadvantages of planning tools used in budgetary control

Budgeting: This can be defined as a process that express the need and requirement of resources

(material, human resources) for future activities related with business operation (production) of

an organisation in this a budget is designed, implemented and operated which are related with

course of action with in firm (Marginal and absorption costing, 2018).

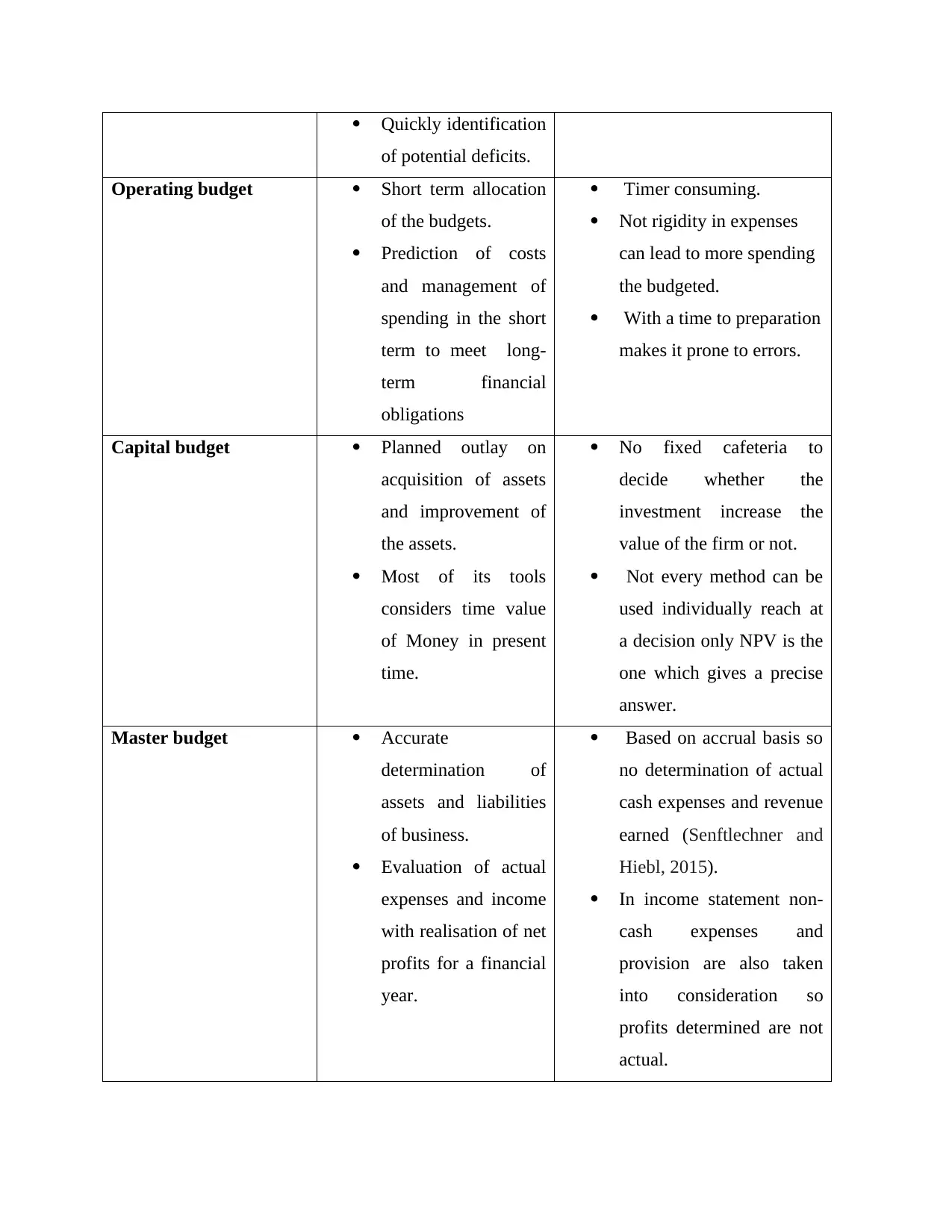

Planning Tool Advantages Disadvantages

Cash Budget Bad Debts can be

avoided.

Better focus on the

budgets.

Availability of the

resources.

Limits spending power of

organisation.

Elimination of the rewards

to employees.

Not actual reflation of

profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of potential deficits.

Operating budget Short term allocation

of the budgets.

Prediction of costs

and management of

spending in the short

term to meet long-

term financial

obligations

Timer consuming.

Not rigidity in expenses

can lead to more spending

the budgeted.

With a time to preparation

makes it prone to errors.

Capital budget Planned outlay on

acquisition of assets

and improvement of

the assets.

Most of its tools

considers time value

of Money in present

time.

No fixed cafeteria to

decide whether the

investment increase the

value of the firm or not.

Not every method can be

used individually reach at

a decision only NPV is the

one which gives a precise

answer.

Master budget Accurate

determination of

assets and liabilities

of business.

Evaluation of actual

expenses and income

with realisation of net

profits for a financial

year.

Based on accrual basis so

no determination of actual

cash expenses and revenue

earned (Senftlechner and

Hiebl, 2015).

In income statement non-

cash expenses and

provision are also taken

into consideration so

profits determined are not

actual.

Paraphrase This Document

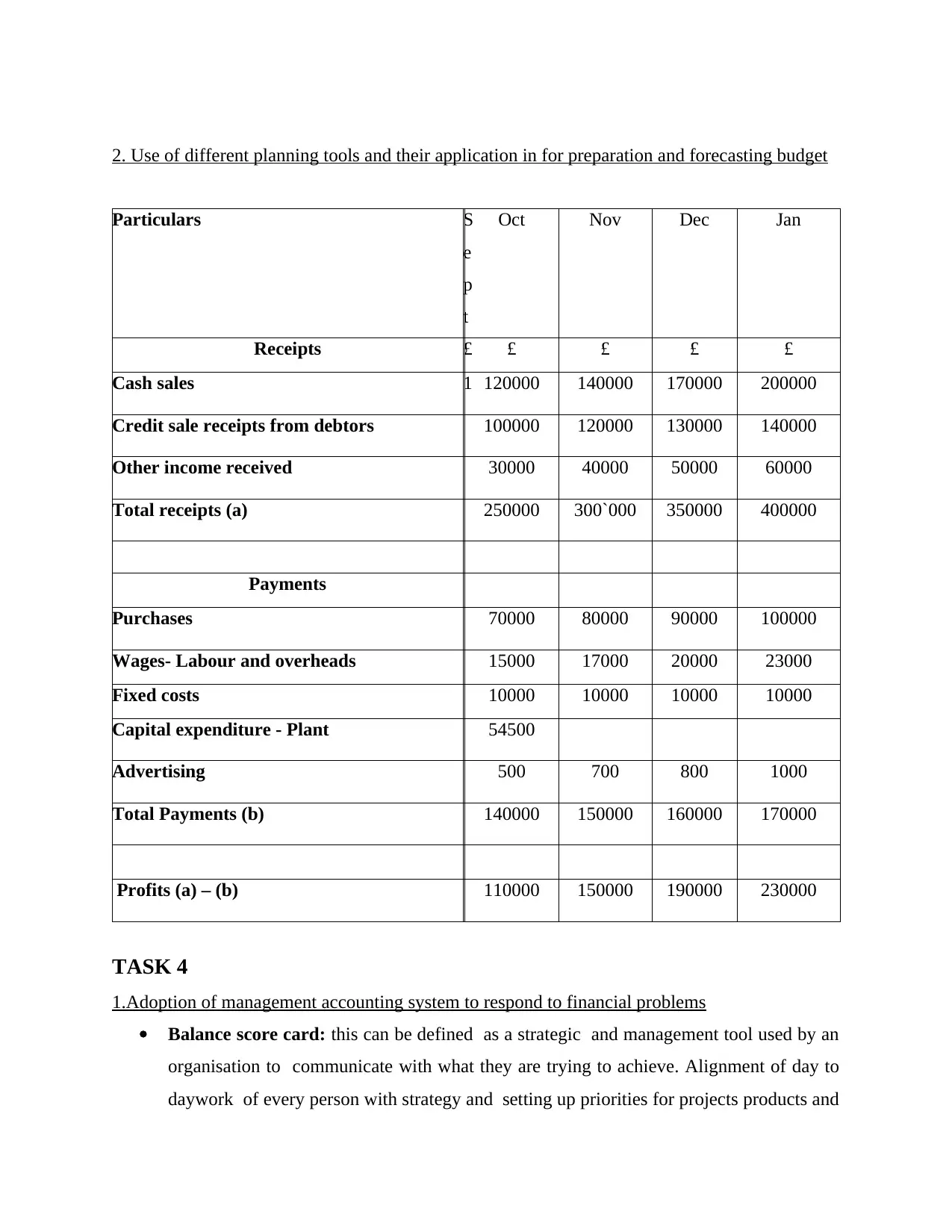

Particulars S

e

p

t

Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 1 120000 140000 170000 200000

Credit sale receipts from debtors 100000 120000 130000 140000

Other income received 30000 40000 50000 60000

Total receipts (a) 250000 300`000 350000 400000

Payments

Purchases 70000 80000 90000 100000

Wages- Labour and overheads 15000 17000 20000 23000

Fixed costs 10000 10000 10000 10000

Capital expenditure - Plant 54500

Advertising 500 700 800 1000

Total Payments (b) 140000 150000 160000 170000

Profits (a) – (b) 110000 150000 190000 230000

TASK 4

1.Adoption of management accounting system to respond to financial problems

Balance score card: this can be defined as a strategic and management tool used by an

organisation to communicate with what they are trying to achieve. Alignment of day to

daywork of every person with strategy and setting up priorities for projects products and

determined before their occurrence and measures can be taken to avoid them.

Financial governance: this can be defined as tools used for managing the risk. In this ,

methods certain tools and techniques are used to determine the risk and then evaluation is

done on how to address those risks (Granlund and Lukka, 2017). The techniques used

under this tool are CIMA strategic scorecard, Enterprisers risk management and CGMA

Ethical Management reflection checklist.

Management accounting skill set: it is a model that enables management of an

organisation to improve its performance, assist in decision making, aids strategic goals

and objectives and add value to the business. With all this an organisation ascertain the

future tasks to be accomplished and planing in advance on how to deal with a situation

that may arise in between attainment of task.

With using all these or any one of the planning tool in the organisation financial

problems can be avoided as this assist in early determination of any issue that can be faced by

firm in near future, it also aids and assist in preparation of plans and measurement techniques

thorough which these upcoming threats can be addressed and avoided (Essential-tools-for-

management-accountants, 2018).

2. Use of planning tools to respond and solve financial problems

Key performance indicator: this can be defined as a value measurement tool which

demonstrate How effectively an organisation is attaining its main business goal. With

this the management evaluate the performances at each level with measurement

indicators as success in reaching the targets. This helps in addressing financial

problems with each level of performance evaluation a lag can be find easily and a

corrective measures can be taken immediately so problem is detected at early stage and

resolved effectively at the same time, hence future uncertainties are avoided.

Ratio analysis: this can be defined as a tool which is used by an organisation to evaluate

its financial performance with calculation of financial ratios. This includes profitability,

liquidity, efficiency and investment ratio which indicates its performances at different

financial level a business with high liquidity and optimal capital structures survive in

long run (Tappura and et.al., 2015). With comparison of the past and present ratio along

with comparing with business of same industry a firm can easily determine its actual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

seen the immediate action are taken to rectify those lags.

Benchmarking: Benchmarking is a process of measuring the performance of a

company’s products, services, or processes against those of another business considered

to be the best in the industry. Internal opportunities for improvement are identified

through benchmarking. In this, companies with superior performance is done along with

breaking down the criteria as what makes the superior performance the best and then

planning is done to meet that benchmark. With this planning tool every organisation in

the industry try to match the benchmark and with reaching that level it is ascertained that

they have touched the peak of the growth with that benchmark as they are set at very

high level.

Swot analysis: this is the best method through which present and future decision are

taken in an organisation. With this tool strengthen, weakness, opportunities and threats

of business are determined. Internal strengths are used to maximum in order to give the

best performance and use it is to gain competitive advantages. Planning and decision are

taken to overcome the weakness prevailing in the organisation. Along with this, plans

are made to grab any opportunity prevailing in external market. To avoid future threat

planning and forecasting is done.

A comparison of Jupiter Plc and Healthcare Pvt Ltd is done regarding the use of planning

tool used be respective organisation to deal with financial problem and ensuring sustainable

growth. Jupiter Plc uses SWOT analysis to address and determine the future financial problems

and with this tool only it gets its answer on how to address such problem. The solution is found

under SWOT as strength and new opportunities are determined and this help in addressing those

future uncertainties.

As far a Healthcare Pvt Ltd this organisation uses benchmarking planning tool to

determine and address any future financial problems as with a set target it set plans on how to

reach Upton that mark and for those forecast and budget are made. With preparation of these

reports upcoming financial problem are determined and immediately actions are taken to rectify

them.

Paraphrase This Document

From the above report it can be concluded that accounting is an important part of a

Jupiter Plc and both branches of it i.e. financial and management accounts are unessential for

Jupiter Plc. Management accounting system techniques and tools helps its organisation in

determination of a cost and preparation of budgets. With this organisation knows the actual cost

incurred and profits that is expected to earn at the end of budgeted period. Further it can be

articulate that with Jupiter Plc uses SWOT analysis as planning tool to react to the future

financial problem as compared to Healthcare Pvt Ltd.

Lastly it can be concluded that an organisation use of planning tool is very essential as it

help in determination of solution for forthcoming financial problem and to address them. In the

above report a budget plans is also prepared for future sales, purchase and profits earned by

Jupiter Plc.

Books and Journals

Andersén, J. and Samuelsson, J., 2016. Resource organization and firm performance: How

entrepreneurial orientation and management accounting influence the profitability of growing

and non-growing SMEs. International Journal of Entrepreneurial Behavior & Research. 22(4).

pp.466-484.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting Review. 49(1).

pp.4-24.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research.34(2). pp.991-1025.

Fullerton, R .R., Kennedy, F .A. and Widener, S .K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management. 32(7-8). pp.414-428.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research. Critical

Perspectives on Accounting. 45. pp.63-80.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Senftlechner, D. and Hiebl, M. R., 2015. Management accounting and management control in

family businesses: Past accomplishments and future opportunities. Journal of Accounting &

Organizational Change. 11(4). pp.573-606.

Tappura, S and et.al., 2015. A management accounting perspective on safety. Safety science. 71.

pp.151-159.

van Helden, J. and Uddin, S., 2016. Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting, 41, pp.34-62.

Online

Marginal and absorption costing. 2018. [Online]. Available through

:<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and%20absorption

%20costing.aspx>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

:<https://www.cgma.org/content/dam/cgma/resources/tools/essential-tools/

downloadabledocuments/essential-tools-for-management-accountants.pdf>.

Paraphrase This Document

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Books and journals

2

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.