Management Accounting Assignment: Tax Implications for NOSA

VerifiedAdded on 2022/11/09

|8

|1568

|437

Homework Assignment

AI Summary

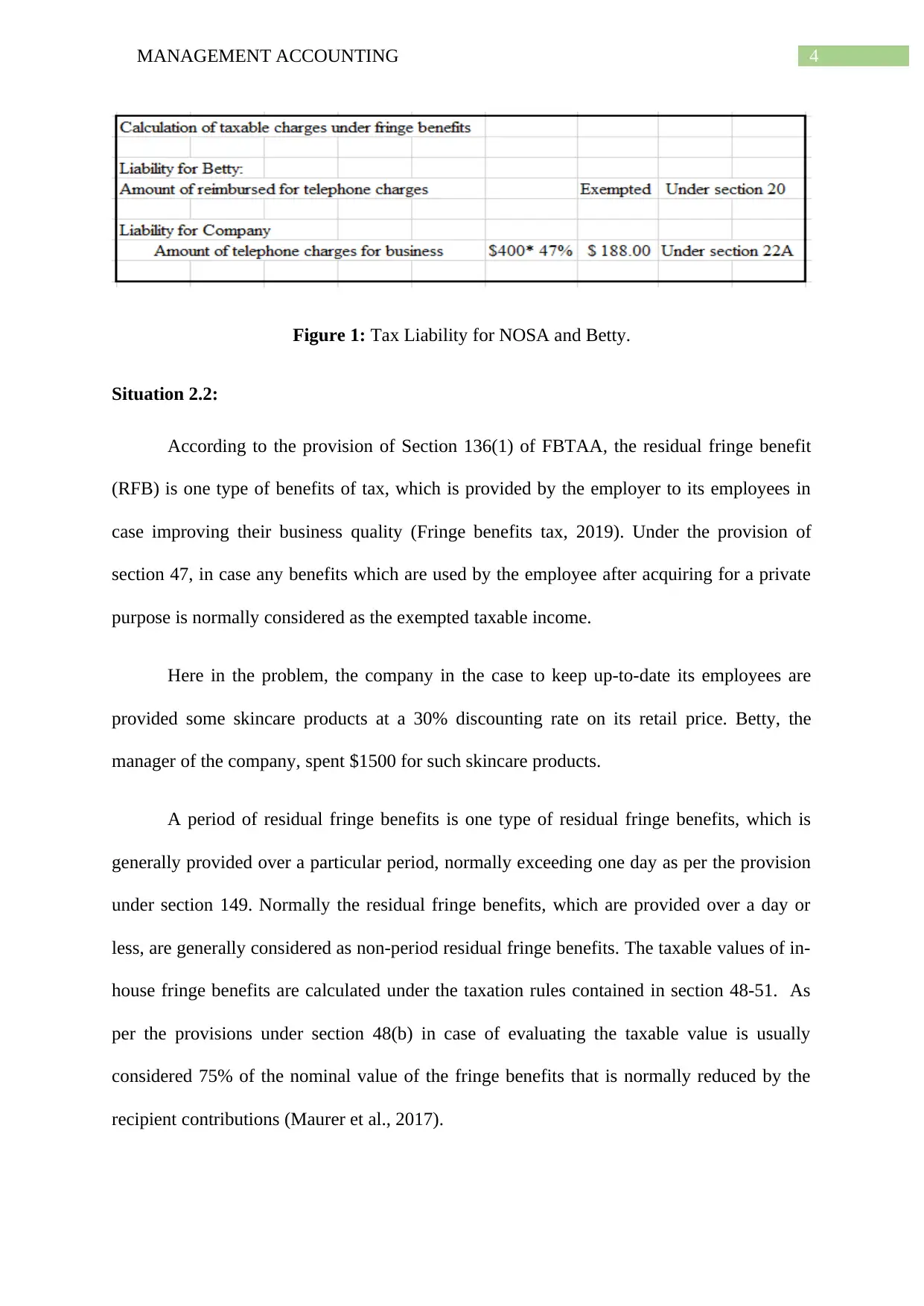

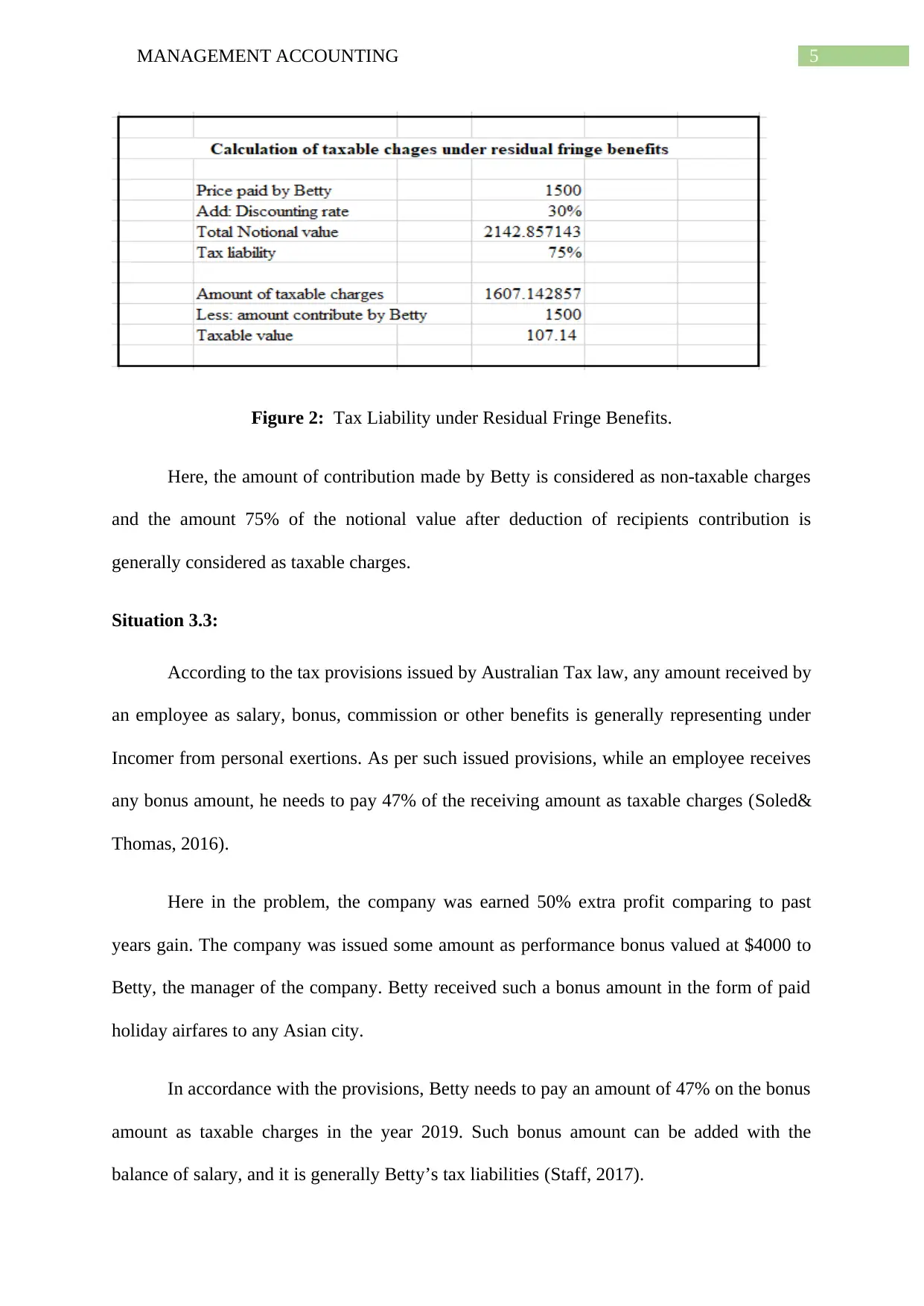

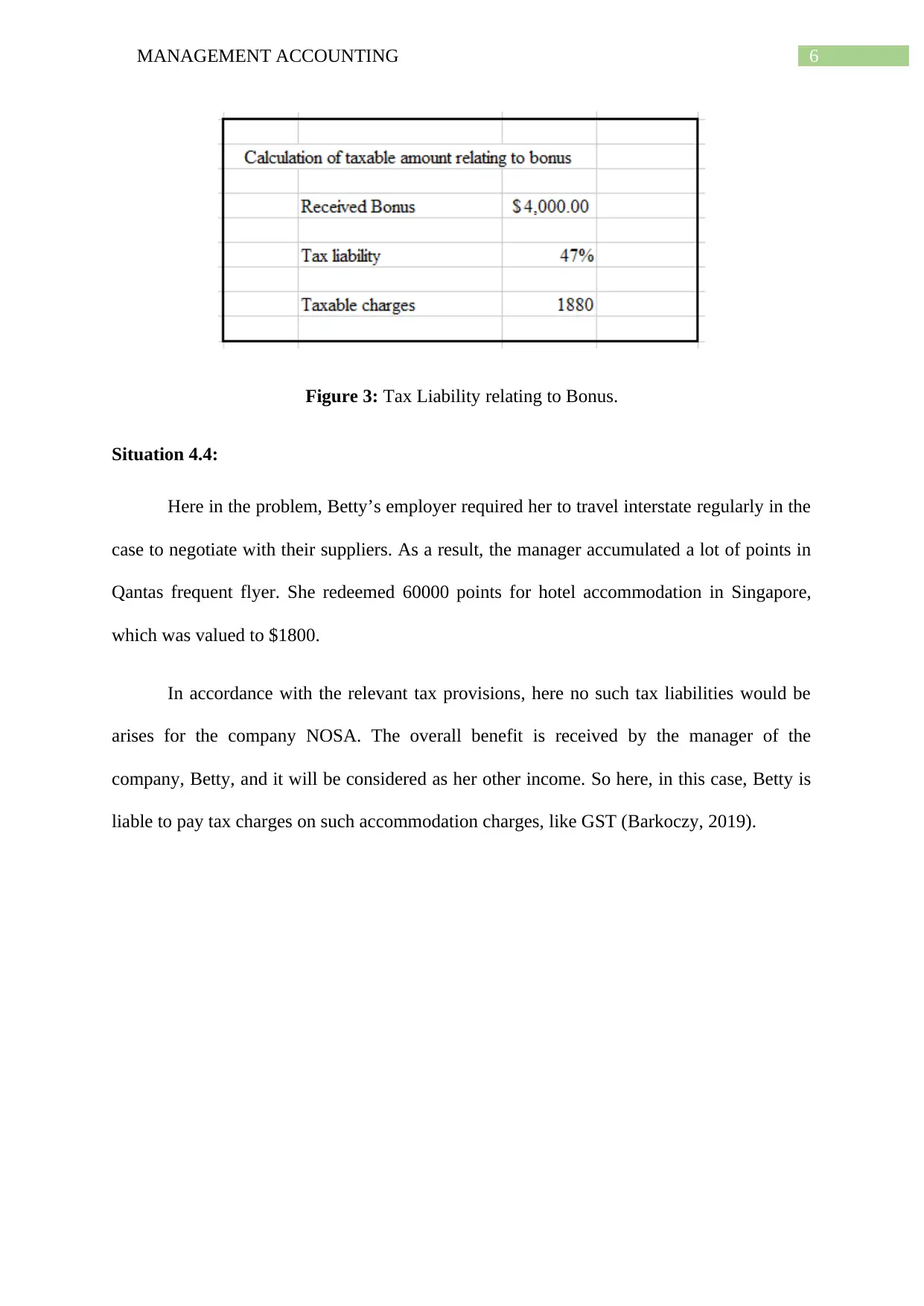

This assignment solution delves into the intricacies of management accounting, specifically focusing on the tax implications faced by Nourished Organic Skincare of Australia Pty Ltd (NOSA). The solution addresses various scenarios, including expense payment benefits, residual fringe benefits, and bonus taxation, all within the framework of Australian tax law. The assignment analyzes the tax consequences for Betty, the purchasing manager, considering fringe benefits tax (FBT) regulations. The solution provides detailed explanations, calculations, and figure representations of tax liabilities arising from telephone reimbursements, discounted skincare products, performance bonuses, and frequent flyer point redemptions. The document references relevant sections of the FBTAA and other tax provisions, offering a comprehensive understanding of the tax implications for both the company and the employee.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.