Management Accounting Report: Krishnamurti Pty Ltd Case Study Analysis

VerifiedAdded on 2021/06/17

|12

|1259

|64

Report

AI Summary

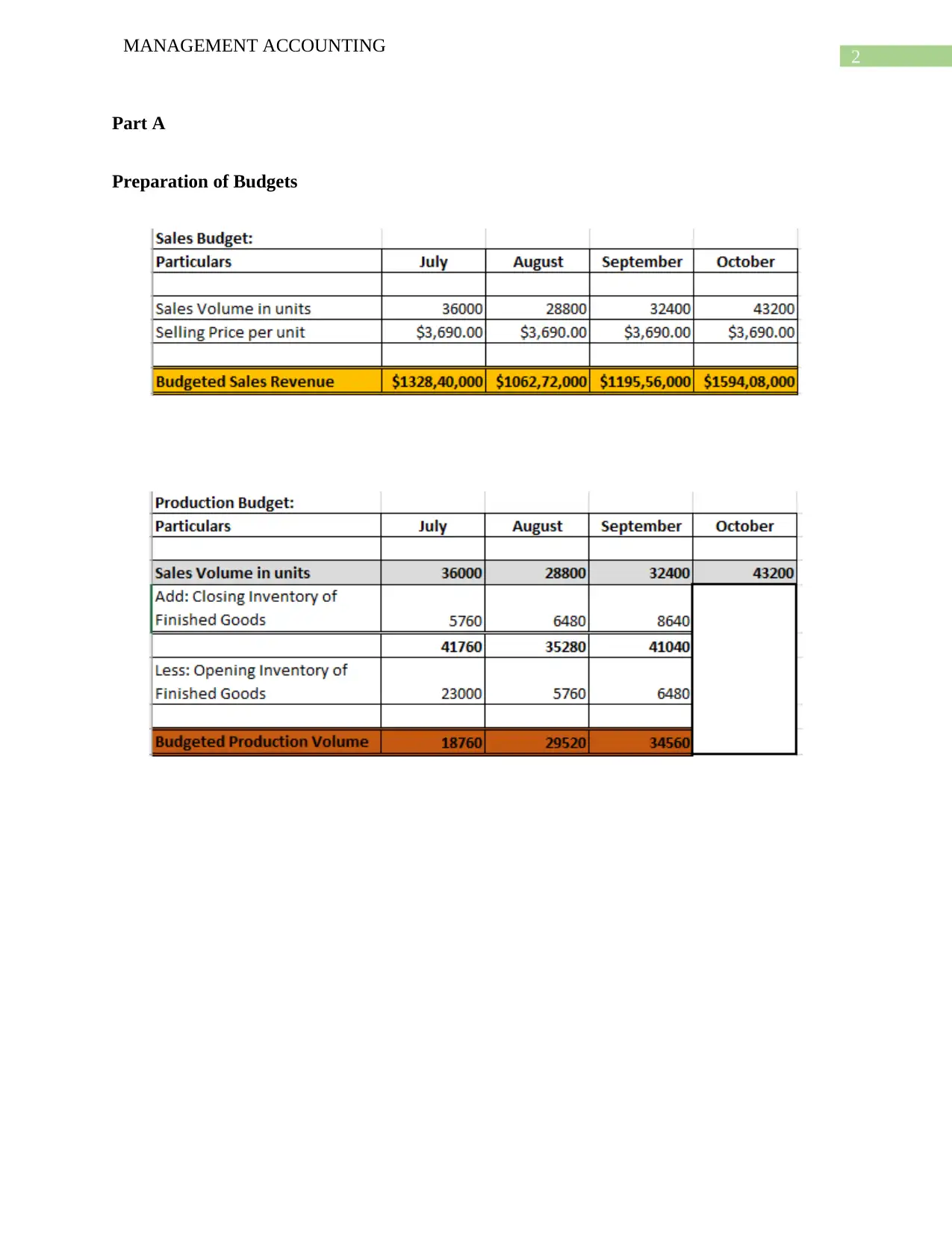

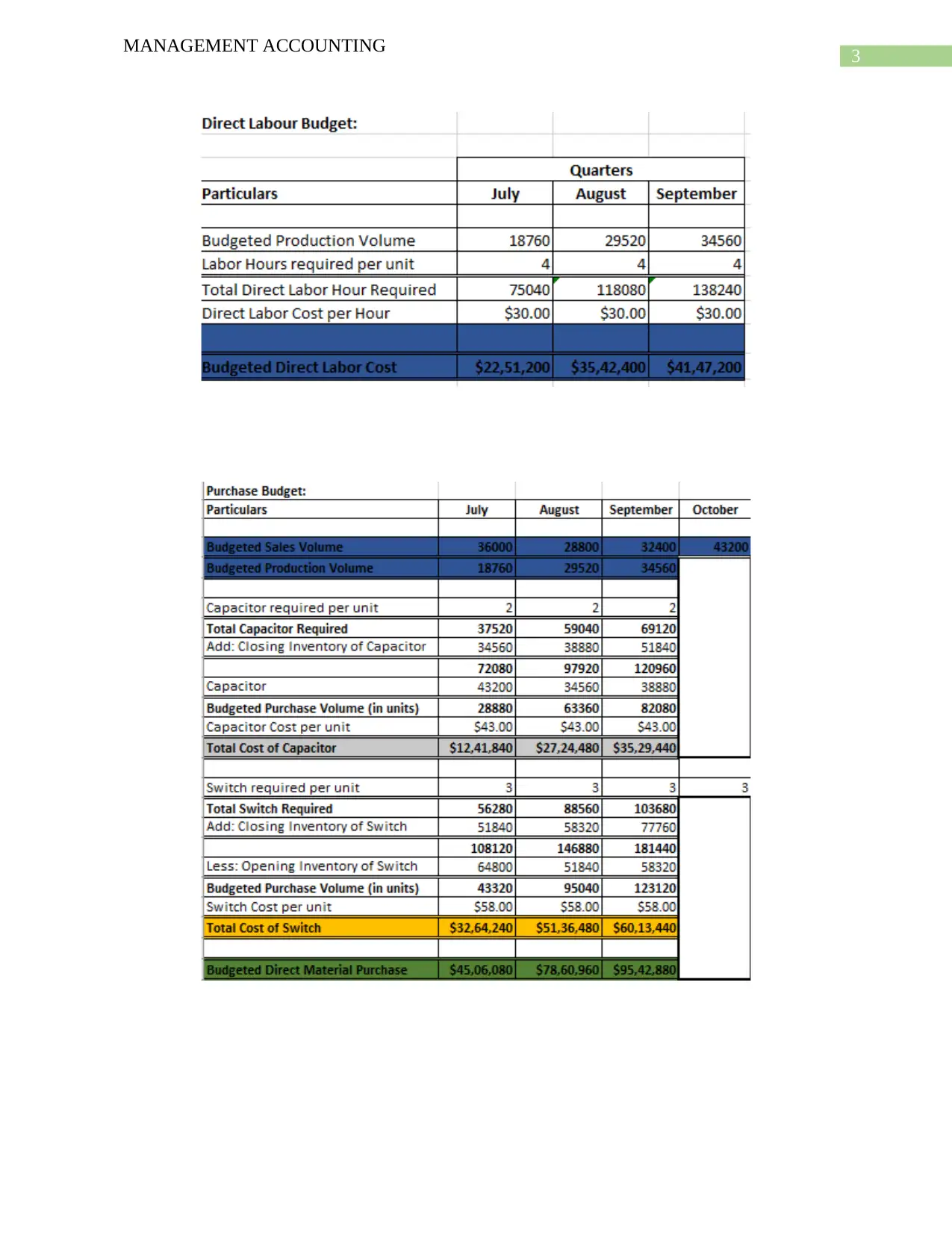

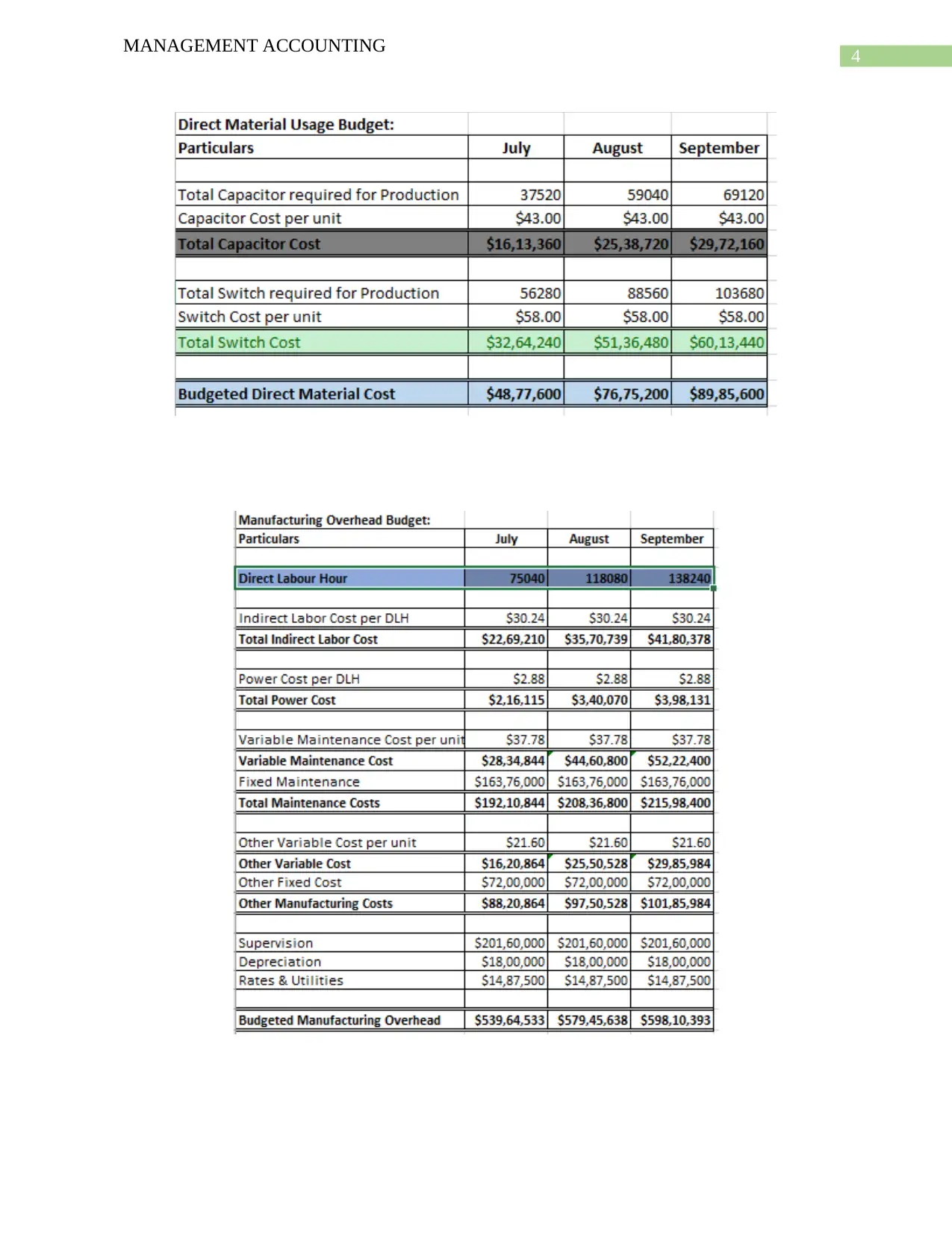

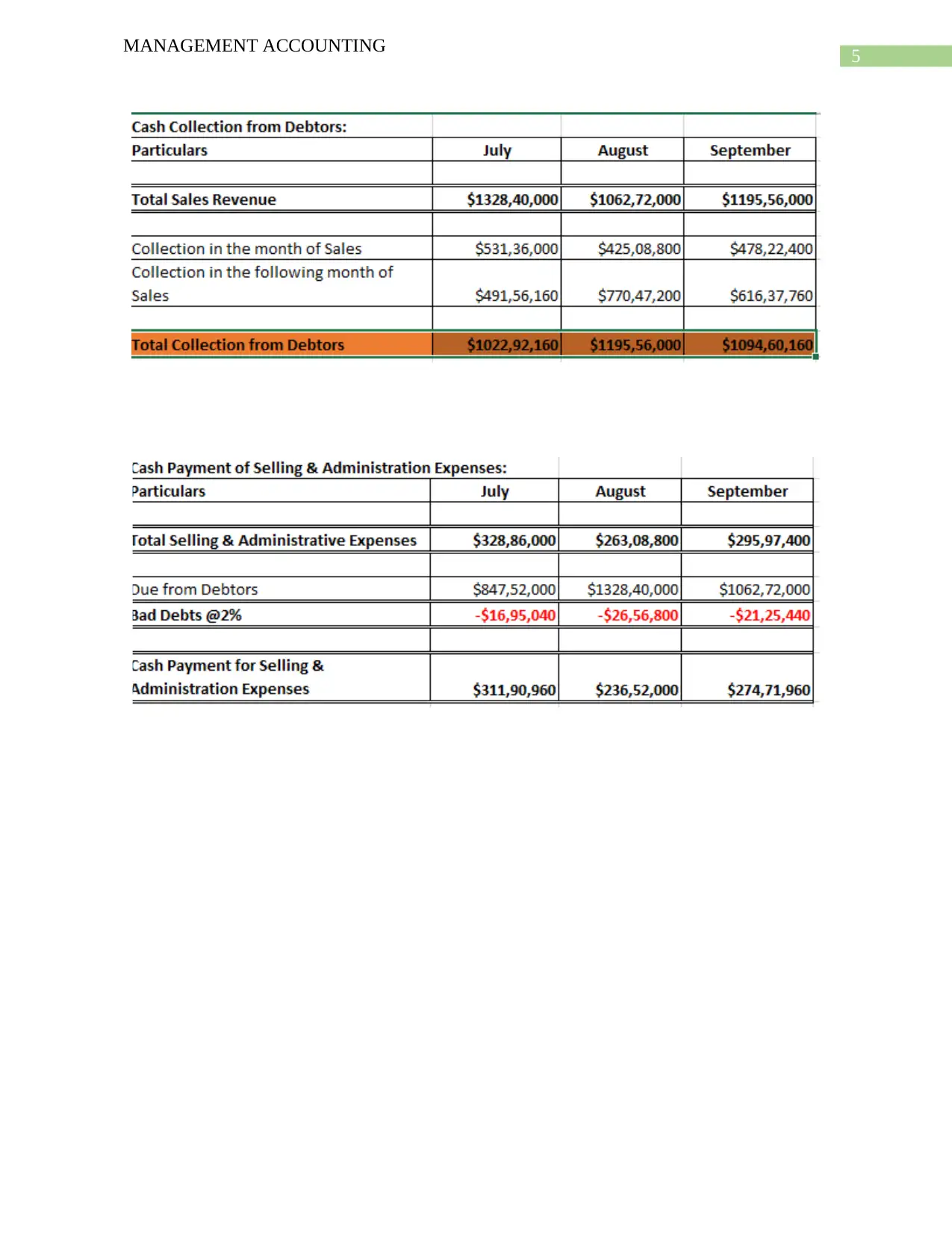

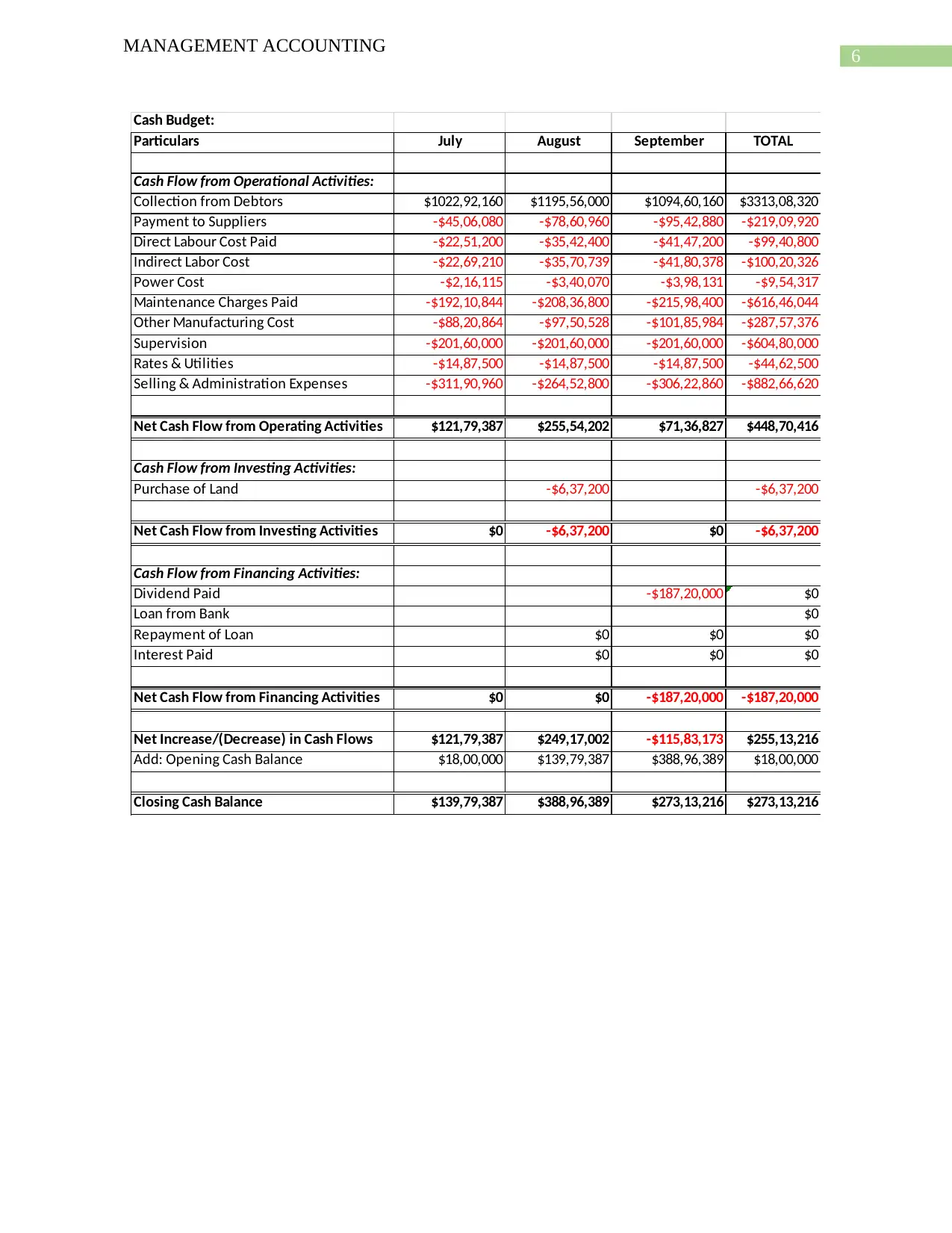

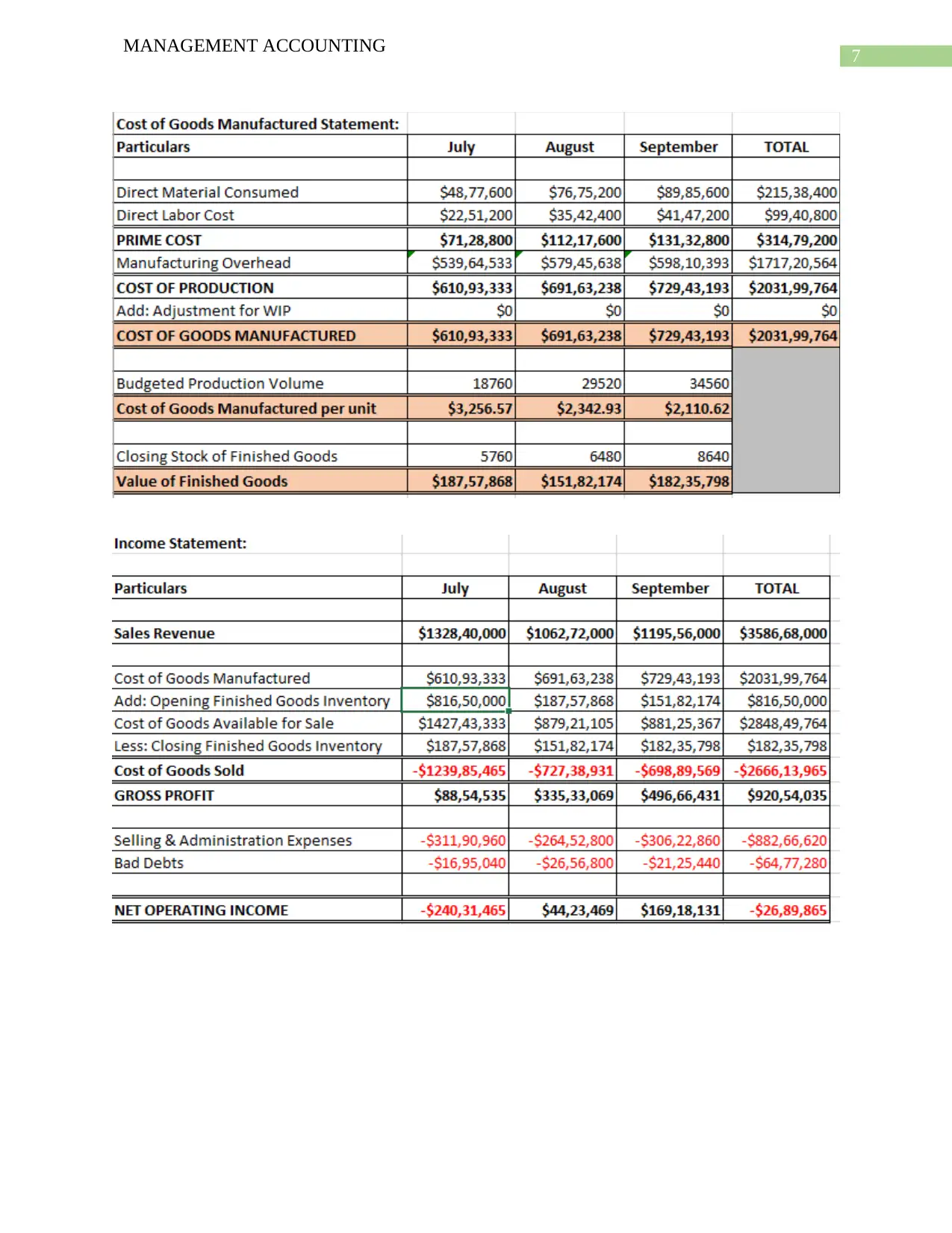

This report analyzes a management accounting case study for Krishnamurti Pty Ltd, focusing on the production of AC/DC switches. The report examines the preparation of budgets, including sales, production, direct labor, purchase, and cash budgets. It evaluates a new production plan, highlighting the impact on costs and revenues. The analysis includes a master budgeting approach and assesses the viability of the production plan. Furthermore, the report differentiates between participative and imposed budgets, advocating for a participative approach in the case study to facilitate collaborative decision-making and improve cash flow management. The report concludes with a list of references used in the analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.