Management Accounting Systems and Planning Tools

VerifiedAdded on 2023/01/11

|22

|6302

|52

AI Summary

This document provides an overview of management accounting systems and planning tools used in organizations. It explains the essential requirements and different methods used for management accounting reporting. It also discusses the use of planning tools in management accounting and provides examples of cost analysis techniques. The document is relevant for students studying management accounting or related subjects.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

| P a g e

ACCOUNTING

| P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

LO1. Demonstrate an understanding of management accounting systems.....................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2. Explain different methods used for management accounting reporting................................6

M1. Evaluate the benefits of management accounting systems and their application within an

organizational context..................................................................................................................7

LO2. Explain the use of planning tools used in Management Accounting.....................................8

P3. Calculate costs using appropriate techniques of cost analysis to prepare income statement

using marginal and absorption costs............................................................................................8

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents...................................................................................................11

LO3. Explain the use of planning tools used in Management Accounting...................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

M3. Analyze the use of different planning tools and their application for preparing budgets

and forecasts..............................................................................................................................15

LO4. Compare ways in which organizations could use Management Accounting to respond to

Financial Problems........................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................16

M4. Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

| P a g e

INTRODUCTION...........................................................................................................................3

LO1. Demonstrate an understanding of management accounting systems.....................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2. Explain different methods used for management accounting reporting................................6

M1. Evaluate the benefits of management accounting systems and their application within an

organizational context..................................................................................................................7

LO2. Explain the use of planning tools used in Management Accounting.....................................8

P3. Calculate costs using appropriate techniques of cost analysis to prepare income statement

using marginal and absorption costs............................................................................................8

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents...................................................................................................11

LO3. Explain the use of planning tools used in Management Accounting...................................12

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

M3. Analyze the use of different planning tools and their application for preparing budgets

and forecasts..............................................................................................................................15

LO4. Compare ways in which organizations could use Management Accounting to respond to

Financial Problems........................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................16

M4. Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

| P a g e

| P a g e

INTRODUCTION

The Management accounting is an arrangement of bookkeeping that causes the board to play out their

capacities all the more productively. At the end of the day, the term the executives bookkeeping is utilized

to give bookkeeping data to the board exercises, for example, arranging, association, administration,

control and dynamic, and so on. Along these lines, the administration account is centered on improving

the productivity of the administration. It does this by furnishing various degrees of the board with the data

required for good dynamic.

This task report dependent on better comprehension of the idea Management bookkeeping; the different

fundamental apparatuses of the executives bookkeeping strategies will investigate the extent of this most

recent money related idea. Estimation of pay proclamation through negligible and retention costing

techniques will upgrade the fundamental contrast among two and furthermore uncovers the purpose for

distinction in both net benefit figure. The chosen organization for this particular project is Cream

Ltd. which sells ice creams, doughnuts and waffles.

| P a g e

The Management accounting is an arrangement of bookkeeping that causes the board to play out their

capacities all the more productively. At the end of the day, the term the executives bookkeeping is utilized

to give bookkeeping data to the board exercises, for example, arranging, association, administration,

control and dynamic, and so on. Along these lines, the administration account is centered on improving

the productivity of the administration. It does this by furnishing various degrees of the board with the data

required for good dynamic.

This task report dependent on better comprehension of the idea Management bookkeeping; the different

fundamental apparatuses of the executives bookkeeping strategies will investigate the extent of this most

recent money related idea. Estimation of pay proclamation through negligible and retention costing

techniques will upgrade the fundamental contrast among two and furthermore uncovers the purpose for

distinction in both net benefit figure. The chosen organization for this particular project is Cream

Ltd. which sells ice creams, doughnuts and waffles.

| P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

LO1. Demonstrate an understanding of management accounting systems

P1. Explain management accounting and give the essential requirements of

different types of management accounting systems

Management accounting: In management accounting or managerial accounting, managers use provisions

of accounting information to better inform themselves before making decisions in the affairs of their

organizations, which assist in the performance of their management and control functions; calculating

techniques to provide effective accounting information for business managers inside the company. For

financial accounting this includes management planning, adjustments between departments, corporate

budgets used for control activities, direct cost accounting, standard cost calculations, and more. It is being

reorganized under Management Information System (MIS) with the introduction of computers (Kaplan

and Atkinson, 2015).

Benefits of management accounting to an organization:

Management accounting has many benefits. Through an effective management accounting system, it is

possible to enhance the overall performance of the company (Burns and Vaivio, 2001). These benefits are

discussed below:

Advanced technology and features:

Cost Transparency

Flexibility and independence

Marginal Cost

Company efficiency

Bar of profitability

Different types of management accounting:

Managerial accountant uses different types of management accounting techniques to solve financial

problems of an organization; these techniques are discussed below:

Cost accounting system: The cost accounting system is only a part of the full accounting system. This

method is established to obtain cost related information. With this help the cost of product services and

various processes can be controlled. At present, cost accounting has become so important that it is not

possible to develop in this era of competition. Every producer must have knowledge about cost

| P a g e

P1. Explain management accounting and give the essential requirements of

different types of management accounting systems

Management accounting: In management accounting or managerial accounting, managers use provisions

of accounting information to better inform themselves before making decisions in the affairs of their

organizations, which assist in the performance of their management and control functions; calculating

techniques to provide effective accounting information for business managers inside the company. For

financial accounting this includes management planning, adjustments between departments, corporate

budgets used for control activities, direct cost accounting, standard cost calculations, and more. It is being

reorganized under Management Information System (MIS) with the introduction of computers (Kaplan

and Atkinson, 2015).

Benefits of management accounting to an organization:

Management accounting has many benefits. Through an effective management accounting system, it is

possible to enhance the overall performance of the company (Burns and Vaivio, 2001). These benefits are

discussed below:

Advanced technology and features:

Cost Transparency

Flexibility and independence

Marginal Cost

Company efficiency

Bar of profitability

Different types of management accounting:

Managerial accountant uses different types of management accounting techniques to solve financial

problems of an organization; these techniques are discussed below:

Cost accounting system: The cost accounting system is only a part of the full accounting system. This

method is established to obtain cost related information. With this help the cost of product services and

various processes can be controlled. At present, cost accounting has become so important that it is not

possible to develop in this era of competition. Every producer must have knowledge about cost

| P a g e

accounting and must keep the cost accounts systematically in order to maintain his accountability, as a

result of which he can make maximum profit on the goods he produces in the era of competition.

Job costing system: A job costing system includes the way to collect cost data associated with a

particular production or administration operation. This data may be required to present cost data to a

customer under an agreement in which expenses are reimbursed. Likewise, the data is useful for

determining the accuracy of an organization's scoreboard, which should include an option to provide cost

estimates that take reasonable advantage into account. The data can be used in the same way to calculate

the deductible costs for manufactured products (Horngren, Sundem, Elliott and Philbrick, 2002).

Inventory management system: An inventory management system is the combination of innovation

(equipment and programming) and methods and strategies that monitor the monitoring and support of

uploaded items, regardless of organizational resources, raw materials and a supply of these or complete

items suitable for transmission to final or final buyers.

Price optimization: The price optimization system is a scientific project that reveals how demand

changes at different levels of value and subsequently combines this information with cost data and

inventory levels to suggest costs which will improve the benefits. Presentation allows organizations to use

evaluation as a dramatic, often unusual, benefit change. Value optimization models can be used to

customize customer portfolio estimates by replicating the way focused customers manage value changes

with information-based scenarios. Given the multidimensional nature of predicting large numbers of

things in extremely powerful economic conditions, the emergence of results and knowledge helps drive

demand, generate and maintain demand creation of evaluation and promotion procedures, control of stock

levels and improvement of customer loyalty.

Explain the essential requirements associated with different management accounting systems

The main aim of the management accounting information is to use internal information’s available

through various accounting documents to support managerial accountants. Some of the essential

requirements associated with different management accounting systems have been discussed below:

1) Management style: Management style is the strategy adopted by manager or leader according to

essential requirement and situation face by business. Different circumstances require applying different

management style.

2) Organization structure: Organization structure refers to the arrangement of interrelations and

functions throughout the organization. The organization's management is determined overall based on the

| P a g e

result of which he can make maximum profit on the goods he produces in the era of competition.

Job costing system: A job costing system includes the way to collect cost data associated with a

particular production or administration operation. This data may be required to present cost data to a

customer under an agreement in which expenses are reimbursed. Likewise, the data is useful for

determining the accuracy of an organization's scoreboard, which should include an option to provide cost

estimates that take reasonable advantage into account. The data can be used in the same way to calculate

the deductible costs for manufactured products (Horngren, Sundem, Elliott and Philbrick, 2002).

Inventory management system: An inventory management system is the combination of innovation

(equipment and programming) and methods and strategies that monitor the monitoring and support of

uploaded items, regardless of organizational resources, raw materials and a supply of these or complete

items suitable for transmission to final or final buyers.

Price optimization: The price optimization system is a scientific project that reveals how demand

changes at different levels of value and subsequently combines this information with cost data and

inventory levels to suggest costs which will improve the benefits. Presentation allows organizations to use

evaluation as a dramatic, often unusual, benefit change. Value optimization models can be used to

customize customer portfolio estimates by replicating the way focused customers manage value changes

with information-based scenarios. Given the multidimensional nature of predicting large numbers of

things in extremely powerful economic conditions, the emergence of results and knowledge helps drive

demand, generate and maintain demand creation of evaluation and promotion procedures, control of stock

levels and improvement of customer loyalty.

Explain the essential requirements associated with different management accounting systems

The main aim of the management accounting information is to use internal information’s available

through various accounting documents to support managerial accountants. Some of the essential

requirements associated with different management accounting systems have been discussed below:

1) Management style: Management style is the strategy adopted by manager or leader according to

essential requirement and situation face by business. Different circumstances require applying different

management style.

2) Organization structure: Organization structure refers to the arrangement of interrelations and

functions throughout the organization. The organization's management is determined overall based on the

| P a g e

organization's structure. The entire organizational system of an organization is the organization structure

that displays the relationships of the employees working in it.

3) Information: Information for management is mainly obtained from financial accounting and cost

accounting which helps managers to make budget, assess profit, determine value, decide capital

expenditure, etc. The administration must choose which data to use. Who requests the data and how it

will be necessary to negotiate the choice. As a result of these studies, data is collected. Source: Another

important fact is where the data will be collected. This can come from internal or external sources.

It is measured solely on light. Allocator: Not all policy data. Distinguish the law and provide another way;

Cc Accuracy: The amount of data is data. It gives any idea an idea. A policy that can recover the burden

of common law from the fact that stocking does not result (Bromwich and Bhimani, 2005).

P2. Explain different methods used for management accounting reporting

Management accounting reporting: The head of the company, from time to time, faces the problem of the

profitability of the company and decides for itself the question: is it profitable and should it continue. To

find answers to them, manager is engaged in the creation of cost and sales prices of goods, budget

planning, scheduling of responsibility centers, analysis of external environment and many other functions

designed to provide complete and transparent control over the organization; this practice is known as

management accounting reporting (Libby and Waterhouse, 1996).

Different methods of management accounting reports:

Management accounting reporting is not the concept which can apply by organization individually; it

requires application of different reporting methods according to requirements. These methods are

discussed below:

Debtors/Accounts receivable aging reports: Accounts receivable aging (sometimes called an account

receivable reconciliation) is the process of categorizing the amount owed by all customers, including the

period of time the unpaid balance is due (unpaid), thus your age, or Consider this information "old age"

(Hansen, Mowen and Guan, 2007). The standard categories for this type of report are:

Departmental reports: These reports are generated by different departments of the company according

to various product segments. This report consists of revenue and expenses of each department separately

and also shows any increase or decrease in total sales compare to previous session.

| P a g e

that displays the relationships of the employees working in it.

3) Information: Information for management is mainly obtained from financial accounting and cost

accounting which helps managers to make budget, assess profit, determine value, decide capital

expenditure, etc. The administration must choose which data to use. Who requests the data and how it

will be necessary to negotiate the choice. As a result of these studies, data is collected. Source: Another

important fact is where the data will be collected. This can come from internal or external sources.

It is measured solely on light. Allocator: Not all policy data. Distinguish the law and provide another way;

Cc Accuracy: The amount of data is data. It gives any idea an idea. A policy that can recover the burden

of common law from the fact that stocking does not result (Bromwich and Bhimani, 2005).

P2. Explain different methods used for management accounting reporting

Management accounting reporting: The head of the company, from time to time, faces the problem of the

profitability of the company and decides for itself the question: is it profitable and should it continue. To

find answers to them, manager is engaged in the creation of cost and sales prices of goods, budget

planning, scheduling of responsibility centers, analysis of external environment and many other functions

designed to provide complete and transparent control over the organization; this practice is known as

management accounting reporting (Libby and Waterhouse, 1996).

Different methods of management accounting reports:

Management accounting reporting is not the concept which can apply by organization individually; it

requires application of different reporting methods according to requirements. These methods are

discussed below:

Debtors/Accounts receivable aging reports: Accounts receivable aging (sometimes called an account

receivable reconciliation) is the process of categorizing the amount owed by all customers, including the

period of time the unpaid balance is due (unpaid), thus your age, or Consider this information "old age"

(Hansen, Mowen and Guan, 2007). The standard categories for this type of report are:

Departmental reports: These reports are generated by different departments of the company according

to various product segments. This report consists of revenue and expenses of each department separately

and also shows any increase or decrease in total sales compare to previous session.

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance reports: These reports uses financial KPIs that are ration analyses to compare its present

performance by taking either its own previous year report or by considering competitors performance

report.

Operating budget report: This budget report is based on the estimation cost of operating overheads and

expenses required for running the business. Working capital expenditures are considered in such type of

report of an organization.

M1. Evaluate the benefits of management accounting systems and their

application within an organizational context

Cost accounting system:

Benefit: Cost bookkeeping can be increasingly adaptable and explicit, particularly as far as cost sharing

and rundown estimating. Tragically, this review chance that expands multifaceted nature is getting

progressively costly and its viability is constrained to the ability and accuracy of the organization's

experts.

Application: Cost accounting can be applied in Creams Ltd. for the estimation of cost control, inventory,

and profits throughout the year.

Job costing system:

Benefit: The cost is collected by number in the package to determine the unit cost for each item; the cores

are separated by numbers. Common designs are average incubation costs for manufacturing plants that

produce residency packages, roll production lines, heating products, and components in pharmaceutical

companies.

Application: It applied by Creams Ltd. usually done within the factory. Each function behaves as a

separate entity, and the associated costs are recorded separately. This type of cost is suitable for printers,

machine tool makers, job casting, furniture manufacturing etc.

Inventory management system:

Benefit: The significance of stock administration, particularly for internet business and online deals logos,

can't be satisfactorily affirmed. Appropriate stock following permits the logo to finish arranges on

schedule and accurately. Record the executives is required to develop in organizations as the business

grows. With a vital arrangement that smoothes out the venture the executives and the board procedure,

| P a g e

performance by taking either its own previous year report or by considering competitors performance

report.

Operating budget report: This budget report is based on the estimation cost of operating overheads and

expenses required for running the business. Working capital expenditures are considered in such type of

report of an organization.

M1. Evaluate the benefits of management accounting systems and their

application within an organizational context

Cost accounting system:

Benefit: Cost bookkeeping can be increasingly adaptable and explicit, particularly as far as cost sharing

and rundown estimating. Tragically, this review chance that expands multifaceted nature is getting

progressively costly and its viability is constrained to the ability and accuracy of the organization's

experts.

Application: Cost accounting can be applied in Creams Ltd. for the estimation of cost control, inventory,

and profits throughout the year.

Job costing system:

Benefit: The cost is collected by number in the package to determine the unit cost for each item; the cores

are separated by numbers. Common designs are average incubation costs for manufacturing plants that

produce residency packages, roll production lines, heating products, and components in pharmaceutical

companies.

Application: It applied by Creams Ltd. usually done within the factory. Each function behaves as a

separate entity, and the associated costs are recorded separately. This type of cost is suitable for printers,

machine tool makers, job casting, furniture manufacturing etc.

Inventory management system:

Benefit: The significance of stock administration, particularly for internet business and online deals logos,

can't be satisfactorily affirmed. Appropriate stock following permits the logo to finish arranges on

schedule and accurately. Record the executives is required to develop in organizations as the business

grows. With a vital arrangement that smoothes out the venture the executives and the board procedure,

| P a g e

remembering continuous information for stock terms and conditions, organizations can recover the

advantages of stock administration.

Application: Creams Ltd can apply this techniques to reach at Economic Order Quantity (EOQ) which is

optimized cost paid by company to manage inventories.

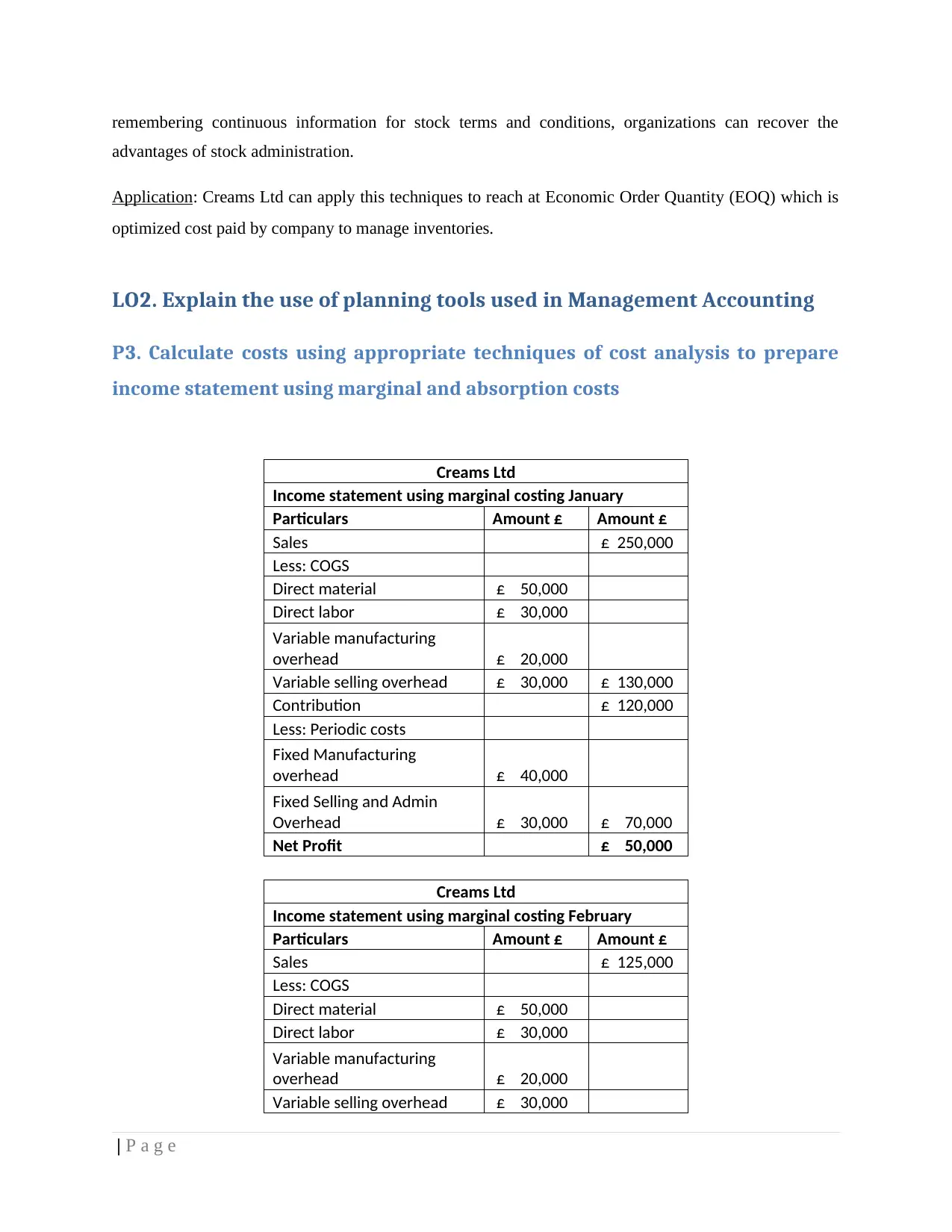

LO2. Explain the use of planning tools used in Management Accounting

P3. Calculate costs using appropriate techniques of cost analysis to prepare

income statement using marginal and absorption costs

Creams Ltd

Income statement using marginal costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000 £ 130,000

Contribution £ 120,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Profit £ 50,000

Creams Ltd

Income statement using marginal costing February

Particulars Amount £ Amount £

Sales £ 125,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000

| P a g e

advantages of stock administration.

Application: Creams Ltd can apply this techniques to reach at Economic Order Quantity (EOQ) which is

optimized cost paid by company to manage inventories.

LO2. Explain the use of planning tools used in Management Accounting

P3. Calculate costs using appropriate techniques of cost analysis to prepare

income statement using marginal and absorption costs

Creams Ltd

Income statement using marginal costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000 £ 130,000

Contribution £ 120,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Profit £ 50,000

Creams Ltd

Income statement using marginal costing February

Particulars Amount £ Amount £

Sales £ 125,000

Less: COGS

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Variable selling overhead £ 30,000

| P a g e

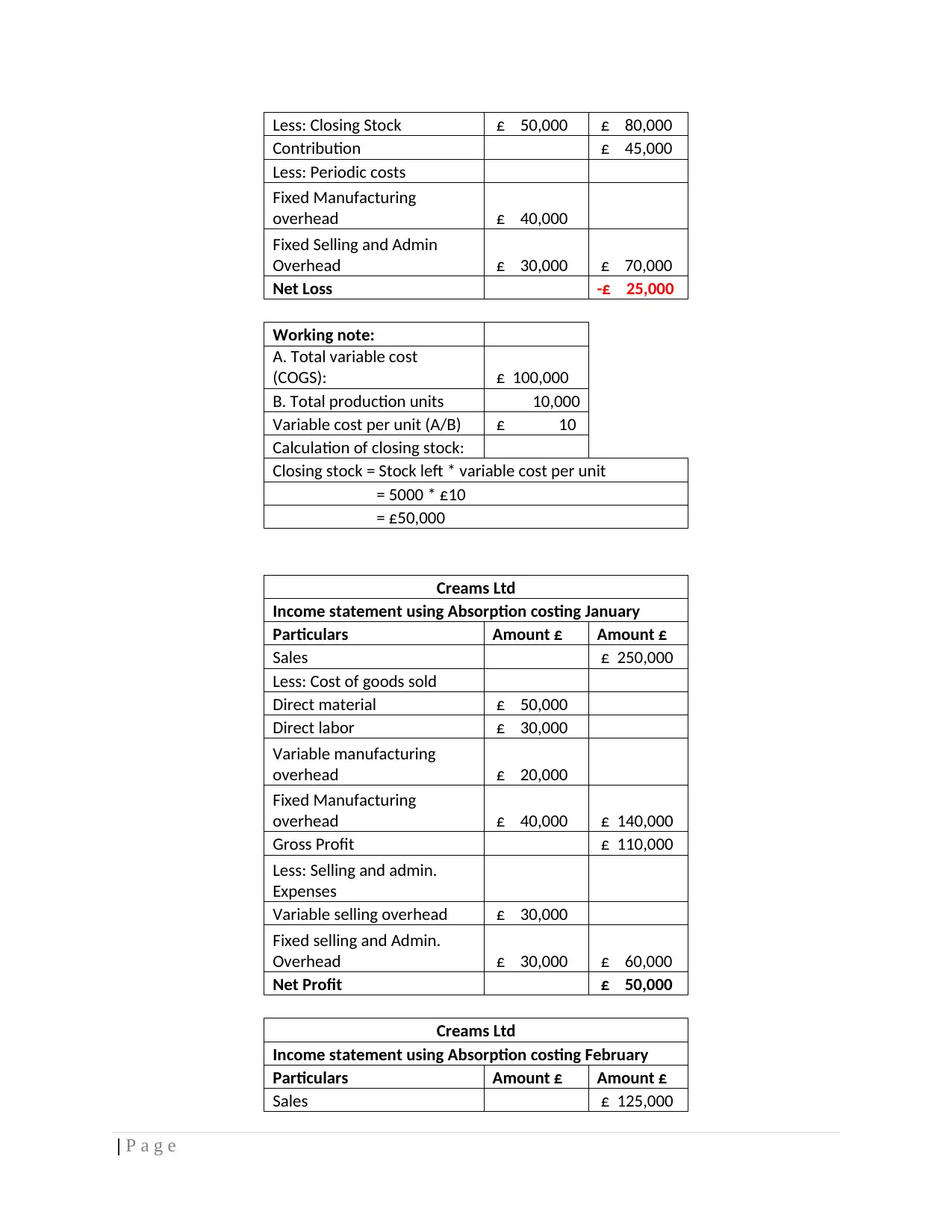

Less: Closing Stock £ 50,000 £ 80,000

Contribution £ 45,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Loss -£ 25,000

Working note:

A. Total variable cost

(COGS): £ 100,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 10

Calculation of closing stock:

Closing stock = Stock left * variable cost per unit

= 5000 * £10

= £50,000

Creams Ltd

Income statement using Absorption costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: Cost of goods sold

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000 £ 140,000

Gross Profit £ 110,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Profit £ 50,000

Creams Ltd

Income statement using Absorption costing February

Particulars Amount £ Amount £

Sales £ 125,000

| P a g e

Contribution £ 45,000

Less: Periodic costs

Fixed Manufacturing

overhead £ 40,000

Fixed Selling and Admin

Overhead £ 30,000 £ 70,000

Net Loss -£ 25,000

Working note:

A. Total variable cost

(COGS): £ 100,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 10

Calculation of closing stock:

Closing stock = Stock left * variable cost per unit

= 5000 * £10

= £50,000

Creams Ltd

Income statement using Absorption costing January

Particulars Amount £ Amount £

Sales £ 250,000

Less: Cost of goods sold

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000 £ 140,000

Gross Profit £ 110,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Profit £ 50,000

Creams Ltd

Income statement using Absorption costing February

Particulars Amount £ Amount £

Sales £ 125,000

| P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

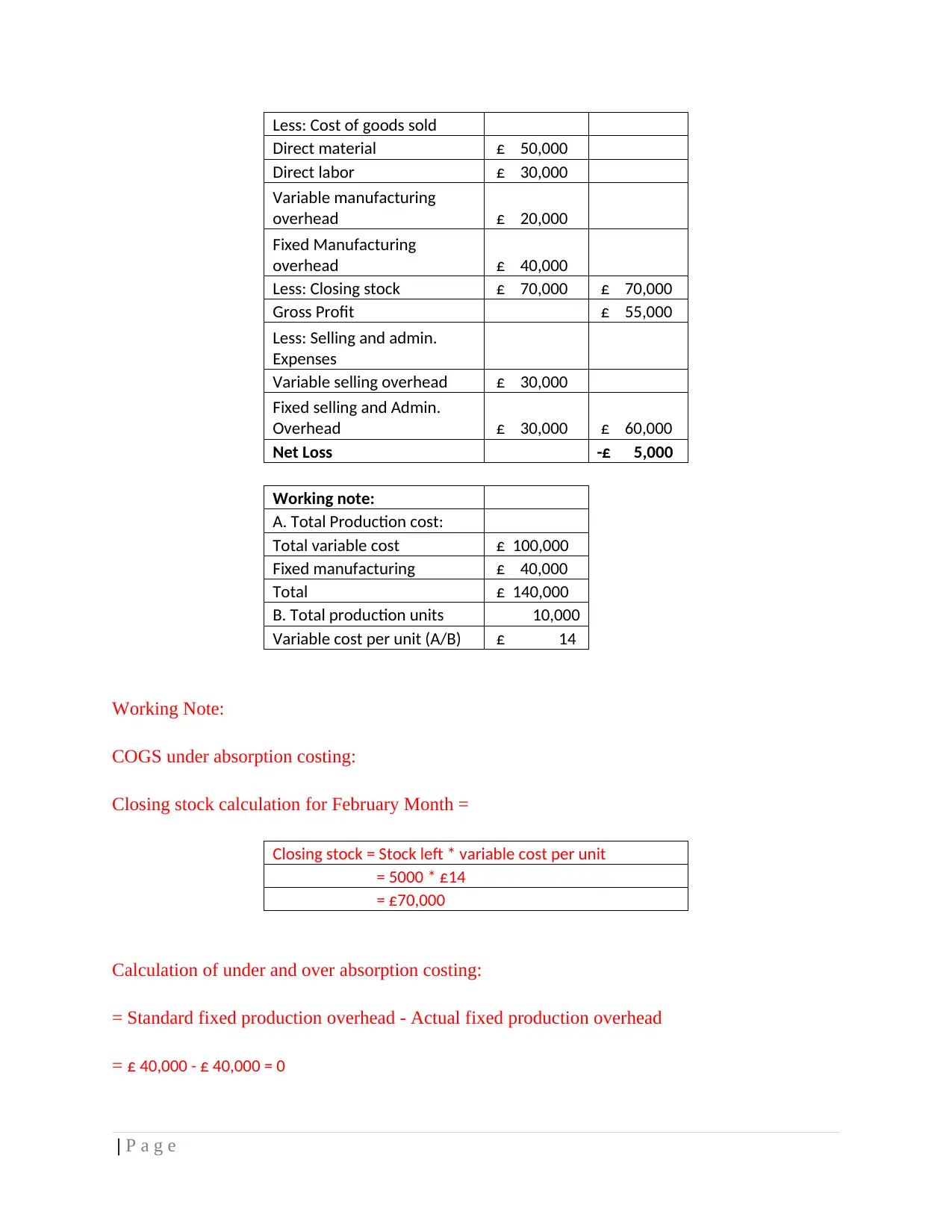

Less: Cost of goods sold

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000

Less: Closing stock £ 70,000 £ 70,000

Gross Profit £ 55,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Loss -£ 5,000

Working note:

A. Total Production cost:

Total variable cost £ 100,000

Fixed manufacturing £ 40,000

Total £ 140,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 14

Working Note:

COGS under absorption costing:

Closing stock calculation for February Month =

Closing stock = Stock left * variable cost per unit

= 5000 * £14

= £70,000

Calculation of under and over absorption costing:

= Standard fixed production overhead - Actual fixed production overhead

= £ 40,000 - £ 40,000 = 0

| P a g e

Direct material £ 50,000

Direct labor £ 30,000

Variable manufacturing

overhead £ 20,000

Fixed Manufacturing

overhead £ 40,000

Less: Closing stock £ 70,000 £ 70,000

Gross Profit £ 55,000

Less: Selling and admin.

Expenses

Variable selling overhead £ 30,000

Fixed selling and Admin.

Overhead £ 30,000 £ 60,000

Net Loss -£ 5,000

Working note:

A. Total Production cost:

Total variable cost £ 100,000

Fixed manufacturing £ 40,000

Total £ 140,000

B. Total production units 10,000

Variable cost per unit (A/B) £ 14

Working Note:

COGS under absorption costing:

Closing stock calculation for February Month =

Closing stock = Stock left * variable cost per unit

= 5000 * £14

= £70,000

Calculation of under and over absorption costing:

= Standard fixed production overhead - Actual fixed production overhead

= £ 40,000 - £ 40,000 = 0

| P a g e

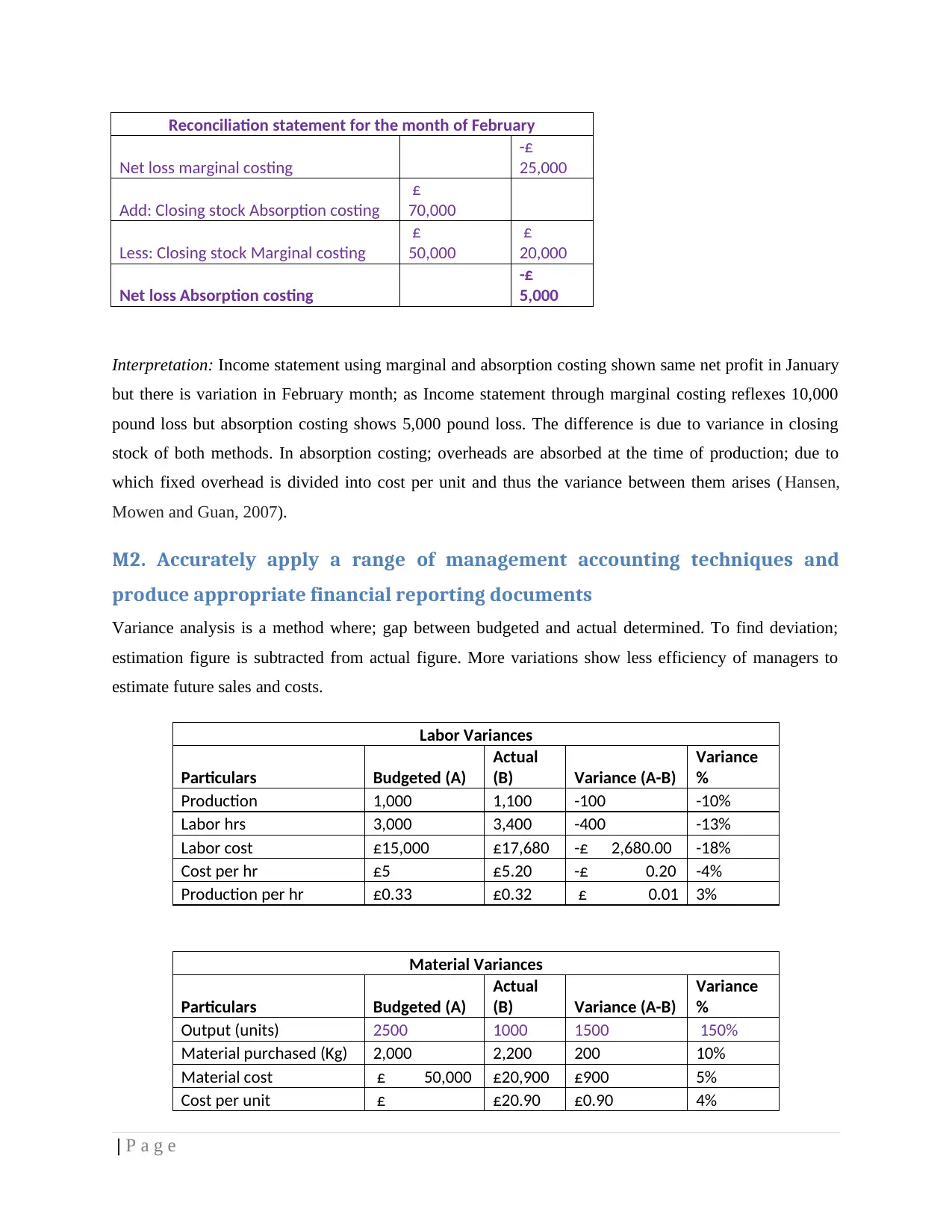

Reconciliation statement for the month of February

Net loss marginal costing

-£

25,000

Add: Closing stock Absorption costing

£

70,000

Less: Closing stock Marginal costing

£

50,000

£

20,000

Net loss Absorption costing

-£

5,000

Interpretation: Income statement using marginal and absorption costing shown same net profit in January

but there is variation in February month; as Income statement through marginal costing reflexes 10,000

pound loss but absorption costing shows 5,000 pound loss. The difference is due to variance in closing

stock of both methods. In absorption costing; overheads are absorbed at the time of production; due to

which fixed overhead is divided into cost per unit and thus the variance between them arises ( Hansen,

Mowen and Guan, 2007).

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Variance analysis is a method where; gap between budgeted and actual determined. To find deviation;

estimation figure is subtracted from actual figure. More variations show less efficiency of managers to

estimate future sales and costs.

Labor Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Production 1,000 1,100 -100 -10%

Labor hrs 3,000 3,400 -400 -13%

Labor cost £15,000 £17,680 -£ 2,680.00 -18%

Cost per hr £5 £5.20 -£ 0.20 -4%

Production per hr £0.33 £0.32 £ 0.01 3%

Material Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Output (units) 2500 1000 1500 150%

Material purchased (Kg) 2,000 2,200 200 10%

Material cost £ 50,000 £20,900 £900 5%

Cost per unit £ £20.90 £0.90 4%

| P a g e

Net loss marginal costing

-£

25,000

Add: Closing stock Absorption costing

£

70,000

Less: Closing stock Marginal costing

£

50,000

£

20,000

Net loss Absorption costing

-£

5,000

Interpretation: Income statement using marginal and absorption costing shown same net profit in January

but there is variation in February month; as Income statement through marginal costing reflexes 10,000

pound loss but absorption costing shows 5,000 pound loss. The difference is due to variance in closing

stock of both methods. In absorption costing; overheads are absorbed at the time of production; due to

which fixed overhead is divided into cost per unit and thus the variance between them arises ( Hansen,

Mowen and Guan, 2007).

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Variance analysis is a method where; gap between budgeted and actual determined. To find deviation;

estimation figure is subtracted from actual figure. More variations show less efficiency of managers to

estimate future sales and costs.

Labor Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Production 1,000 1,100 -100 -10%

Labor hrs 3,000 3,400 -400 -13%

Labor cost £15,000 £17,680 -£ 2,680.00 -18%

Cost per hr £5 £5.20 -£ 0.20 -4%

Production per hr £0.33 £0.32 £ 0.01 3%

Material Variances

Particulars Budgeted (A)

Actual

(B) Variance (A-B)

Variance

%

Output (units) 2500 1000 1500 150%

Material purchased (Kg) 2,000 2,200 200 10%

Material cost £ 50,000 £20,900 £900 5%

Cost per unit £ £20.90 £0.90 4%

| P a g e

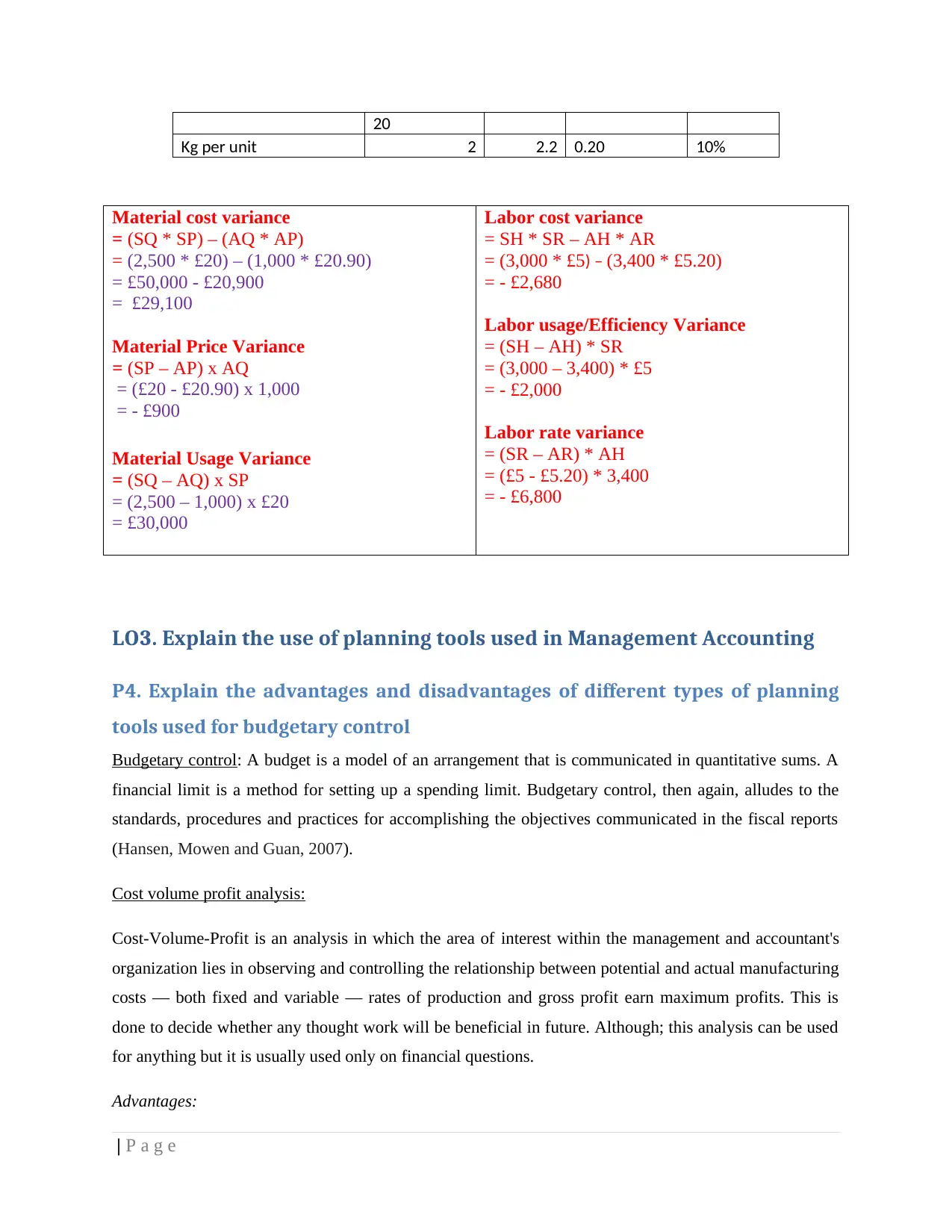

20

Kg per unit 2 2.2 0.20 10%

Material cost variance

= (SQ * SP) – (AQ * AP)

= (2,500 * £20) – (1,000 * £20.90)

= £50,000 - £20,900

= £29,100

Material Price Variance

= (SP – AP) x AQ

= (£20 - £20.90) x 1,000

= - £900

Material Usage Variance

= (SQ – AQ) x SP

= (2,500 – 1,000) x £20

= £30,000

Labor cost variance

= SH * SR – AH * AR

= (3,000 * £5) – (3,400 * £5.20)

= - £2,680

Labor usage/Efficiency Variance

= (SH – AH) * SR

= (3,000 – 3,400) * £5

= - £2,000

Labor rate variance

= (SR – AR) * AH

= (£5 - £5.20) * 3,400

= - £6,800

LO3. Explain the use of planning tools used in Management Accounting

P4. Explain the advantages and disadvantages of different types of planning

tools used for budgetary control

Budgetary control: A budget is a model of an arrangement that is communicated in quantitative sums. A

financial limit is a method for setting up a spending limit. Budgetary control, then again, alludes to the

standards, procedures and practices for accomplishing the objectives communicated in the fiscal reports

(Hansen, Mowen and Guan, 2007).

Cost volume profit analysis:

Cost-Volume-Profit is an analysis in which the area of interest within the management and accountant's

organization lies in observing and controlling the relationship between potential and actual manufacturing

costs — both fixed and variable — rates of production and gross profit earn maximum profits. This is

done to decide whether any thought work will be beneficial in future. Although; this analysis can be used

for anything but it is usually used only on financial questions.

Advantages:

| P a g e

Kg per unit 2 2.2 0.20 10%

Material cost variance

= (SQ * SP) – (AQ * AP)

= (2,500 * £20) – (1,000 * £20.90)

= £50,000 - £20,900

= £29,100

Material Price Variance

= (SP – AP) x AQ

= (£20 - £20.90) x 1,000

= - £900

Material Usage Variance

= (SQ – AQ) x SP

= (2,500 – 1,000) x £20

= £30,000

Labor cost variance

= SH * SR – AH * AR

= (3,000 * £5) – (3,400 * £5.20)

= - £2,680

Labor usage/Efficiency Variance

= (SH – AH) * SR

= (3,000 – 3,400) * £5

= - £2,000

Labor rate variance

= (SR – AR) * AH

= (£5 - £5.20) * 3,400

= - £6,800

LO3. Explain the use of planning tools used in Management Accounting

P4. Explain the advantages and disadvantages of different types of planning

tools used for budgetary control

Budgetary control: A budget is a model of an arrangement that is communicated in quantitative sums. A

financial limit is a method for setting up a spending limit. Budgetary control, then again, alludes to the

standards, procedures and practices for accomplishing the objectives communicated in the fiscal reports

(Hansen, Mowen and Guan, 2007).

Cost volume profit analysis:

Cost-Volume-Profit is an analysis in which the area of interest within the management and accountant's

organization lies in observing and controlling the relationship between potential and actual manufacturing

costs — both fixed and variable — rates of production and gross profit earn maximum profits. This is

done to decide whether any thought work will be beneficial in future. Although; this analysis can be used

for anything but it is usually used only on financial questions.

Advantages:

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CVP analysis is a method of cost accounting that relates to different levels of sales and product cost

impact operating profits will have. CVP analysis is only reliable if the cost is fixed within the specified

production level. All units produced can be sold and all costs must be variable or fixed in CVP analysis.

Another assumption is that changes in activity levels lead to all changes in expenditure. Semi-variable

spending should be split between spending classifications by high-low method, scatter plot, or statistical

regression.

Disadvantages:

This method treats all expenses; whether fixed or variable as fixed overheads. The cost and uses of item is

changes overtime; so categorizing these items on the basis of their volume and benefit might not good

decision for any organization.

Pricing strategy:

It is a progression of evaluation techniques to characterize the cost of an item or administration. The cost

structure of the organization, rivalry, and customer impression of significant value must be estimated to

work. Step by step instructions to find out the sales cost is one of the most important difficulties present

in an organization. It is the most commonly used model in estimating, where all expenses are observed

and markup rates are included. In the administration segment, costs are directly identified with the

amount of hours worked and the full number of representatives engaged with administration. Depending

on the businesses, the cost will be related to raw materials, coordination and inventions (Maas,

Schaltegger and Crutzen, 2016).

Advantages:

An evaluation technique is a method for finding a critical cost for an item or administration. The system

combines 4P functionality (item, price, location and advancement) with financial models, rivalry,

advertising requests, and other performance pricing techniques that ultimately describe the item. This

technique incorporates one of the most important components of the advertising mix as it is around the

production and expansion of income for a union, which ultimately produces benefits for the organization.

Disadvantages:

This method only considered internal factors to obtain a price that covers the cost of the product or

service. This is not enough now if the company is to survive. On top of these costs must be added a sum

that will cover future investment and development costs, profits to the company owner etc. The size of

| P a g e

impact operating profits will have. CVP analysis is only reliable if the cost is fixed within the specified

production level. All units produced can be sold and all costs must be variable or fixed in CVP analysis.

Another assumption is that changes in activity levels lead to all changes in expenditure. Semi-variable

spending should be split between spending classifications by high-low method, scatter plot, or statistical

regression.

Disadvantages:

This method treats all expenses; whether fixed or variable as fixed overheads. The cost and uses of item is

changes overtime; so categorizing these items on the basis of their volume and benefit might not good

decision for any organization.

Pricing strategy:

It is a progression of evaluation techniques to characterize the cost of an item or administration. The cost

structure of the organization, rivalry, and customer impression of significant value must be estimated to

work. Step by step instructions to find out the sales cost is one of the most important difficulties present

in an organization. It is the most commonly used model in estimating, where all expenses are observed

and markup rates are included. In the administration segment, costs are directly identified with the

amount of hours worked and the full number of representatives engaged with administration. Depending

on the businesses, the cost will be related to raw materials, coordination and inventions (Maas,

Schaltegger and Crutzen, 2016).

Advantages:

An evaluation technique is a method for finding a critical cost for an item or administration. The system

combines 4P functionality (item, price, location and advancement) with financial models, rivalry,

advertising requests, and other performance pricing techniques that ultimately describe the item. This

technique incorporates one of the most important components of the advertising mix as it is around the

production and expansion of income for a union, which ultimately produces benefits for the organization.

Disadvantages:

This method only considered internal factors to obtain a price that covers the cost of the product or

service. This is not enough now if the company is to survive. On top of these costs must be added a sum

that will cover future investment and development costs, profits to the company owner etc. The size of

| P a g e

this order will of course depend on the profit requirements and the strategy chosen by the company as

well as the external factors that influence.

Value based budgeting:

Also known as value based pricing; it is a strategy for determining prices primarily based on the

consumer's perceived value of a product or service. Price valuation is customer-focused pricing, which

means that companies base their prices on how much the customer thinks a product is worth.

Advantages:

It brings out programs and achievements in a financial and real sense. This improves the budget

formulation. It provides additional tools of management control of financial activities. This makes

performance audit more objective and effective.

Disadvantages:

This budget has major disadvantages due to complexity in its method to apply. As future is uncertain and

expert supervision and estimation having experiences more than 10 years required to make estimation.

Due to this requirement; this process is expensive and rigid; as once made cannot be changed further.

Fixed budgets

A fixed budget plan is dependent on the amount of return and revenue that an organization

expects to make towards the beginning of the accounting period assigned to the coverage. Static

financial plans are usually based on information collected and analyzed before the beginning of

the spending period.

Advantages of the fixed budget

A particular favorite of the static spending plan is that it is far from difficult to implement and

follow; as static financial plans should not be updated regularly during the due accounting

periods cover them. In addition, a static financial plan can offer a solid understanding of the costs

and benefits of an organization when performing a change audit.

Disadvantages of the fixed budget

The best obstacle of the static consumption plan is its lack of flexibility. If an organization

establishes a financial plan dependent on a certain level of offers and the volume accumulates, it

| P a g e

well as the external factors that influence.

Value based budgeting:

Also known as value based pricing; it is a strategy for determining prices primarily based on the

consumer's perceived value of a product or service. Price valuation is customer-focused pricing, which

means that companies base their prices on how much the customer thinks a product is worth.

Advantages:

It brings out programs and achievements in a financial and real sense. This improves the budget

formulation. It provides additional tools of management control of financial activities. This makes

performance audit more objective and effective.

Disadvantages:

This budget has major disadvantages due to complexity in its method to apply. As future is uncertain and

expert supervision and estimation having experiences more than 10 years required to make estimation.

Due to this requirement; this process is expensive and rigid; as once made cannot be changed further.

Fixed budgets

A fixed budget plan is dependent on the amount of return and revenue that an organization

expects to make towards the beginning of the accounting period assigned to the coverage. Static

financial plans are usually based on information collected and analyzed before the beginning of

the spending period.

Advantages of the fixed budget

A particular favorite of the static spending plan is that it is far from difficult to implement and

follow; as static financial plans should not be updated regularly during the due accounting

periods cover them. In addition, a static financial plan can offer a solid understanding of the costs

and benefits of an organization when performing a change audit.

Disadvantages of the fixed budget

The best obstacle of the static consumption plan is its lack of flexibility. If an organization

establishes a financial plan dependent on a certain level of offers and the volume accumulates, it

| P a g e

cannot designate additional resources for maintenance. Therefore, if an organization is making a

difference in failure in business areas, it cannot allocate additional resources to assist.

Flexible budgeting

A flexible budget is a budget that is usually used as a static financial plan and varies substantially

with the progress that occurs in the volume or trend in the future. adapt to increase the

productivity and adaptability of the administrator as he is ready for a policy for the actual

execution of the organization.

Advantages

It can help in terms of contracts, costs and profitability at various levels of labor limits.

It helps to determine the volume / volume of the product that will be created to allow the

organization to reach the optimal level of benefit.

Disadvantages

This financial plan requires talented experts to deal with it. The reach of talented experts turns to

the test for the industry. As a result, many companies and organizations cannot use this financial

plan despite their favorable position.

M3. Analyze the use of different planning tools and their application for

preparing budgets and forecasts

Budgeting: It is very important to plan the future of the company in an economic perspective. Having an

overview of the company's finances over the next year creates both security and provides a "red thread" to

work on. A budget is the company's business expressed in numbers, a financial plan simply (Ward, 2012).

Forecasting: Forecasts are important in companies as a basis for the company's planning and budgeting. It

is estimates of developments for various measures in the future. Forecasts are usually a continuation of a

trend. They are thus usually based on the trend that will continue as before, following a linear trend going

forward (Ward, 2012).

Difference between budgeting and forecasting:

| P a g e

difference in failure in business areas, it cannot allocate additional resources to assist.

Flexible budgeting

A flexible budget is a budget that is usually used as a static financial plan and varies substantially

with the progress that occurs in the volume or trend in the future. adapt to increase the

productivity and adaptability of the administrator as he is ready for a policy for the actual

execution of the organization.

Advantages

It can help in terms of contracts, costs and profitability at various levels of labor limits.

It helps to determine the volume / volume of the product that will be created to allow the

organization to reach the optimal level of benefit.

Disadvantages

This financial plan requires talented experts to deal with it. The reach of talented experts turns to

the test for the industry. As a result, many companies and organizations cannot use this financial

plan despite their favorable position.

M3. Analyze the use of different planning tools and their application for

preparing budgets and forecasts

Budgeting: It is very important to plan the future of the company in an economic perspective. Having an

overview of the company's finances over the next year creates both security and provides a "red thread" to

work on. A budget is the company's business expressed in numbers, a financial plan simply (Ward, 2012).

Forecasting: Forecasts are important in companies as a basis for the company's planning and budgeting. It

is estimates of developments for various measures in the future. Forecasts are usually a continuation of a

trend. They are thus usually based on the trend that will continue as before, following a linear trend going

forward (Ward, 2012).

Difference between budgeting and forecasting:

| P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Once a budget has been set, the goal is to reach (or preferably exceed!) The budget set. Forecasts are used

as management tools by management to ensure that the organization is still on the right track to achieving

the established budget.

The forecast includes data for the results achieved to date and the expected changes that are expected to

apply to the assumptions made for the rest of the budget period. If the forecast shows deviations from the

budget, the management with the support of the forecasts can make the necessary changes (Ward, 2012).

Application of planning tools for budgeting and forecasting:

Cost volume profit analysis: It can be applied in Creams Ltd to forecast the future sales and any change in

costs and overheads within year. Budgeting will help company to allocate funds among the different

volumes on the basis of profit received by them in future context (Budding, Grossi and Tagesson, 2014).

Pricing strategy: This strategy can be applied by Creams Ltd; to forecast future price of the product, in

terms of internal and external factors affecting the cost of finished goods. Through budgeting process;

company could find the way to minimize other costs to get profit at competitive price. As company have

two methods to earn profit on price; through setting extra amount on cost margin; and by minimizing cost

by taking price constant.

Value based budgeting: This method can be applied by Creams Ltd to get forecasted items which can

increase the value of core products of the company. Budgeting will categories different costs according to

different department heads and allocate funds accordingly (Macintosh and Quattrone, 2010).

LO4. Compare ways in which organizations could use Management

Accounting to respond to Financial Problems

P5. Compare how organizations are adapting management accounting systems

to respond to financial problems

Today associations are facing many issues related to money, which can be identified in different ways,

which are discussed below:

Benchmarking: It is the instrument that determines the objective to be completed by the firm for the year

related to the given funds. Benchmarking can be decided on three grounds; Plan of expenses incurred by

the organization, fiscal summary of earlier years and execution of claimants; like for example Creams ltd.

has set benchmarking of achieving 25% of previous sales revenue. On the other hand, Starbucks has set

| P a g e

as management tools by management to ensure that the organization is still on the right track to achieving

the established budget.

The forecast includes data for the results achieved to date and the expected changes that are expected to

apply to the assumptions made for the rest of the budget period. If the forecast shows deviations from the

budget, the management with the support of the forecasts can make the necessary changes (Ward, 2012).

Application of planning tools for budgeting and forecasting:

Cost volume profit analysis: It can be applied in Creams Ltd to forecast the future sales and any change in

costs and overheads within year. Budgeting will help company to allocate funds among the different

volumes on the basis of profit received by them in future context (Budding, Grossi and Tagesson, 2014).

Pricing strategy: This strategy can be applied by Creams Ltd; to forecast future price of the product, in

terms of internal and external factors affecting the cost of finished goods. Through budgeting process;

company could find the way to minimize other costs to get profit at competitive price. As company have

two methods to earn profit on price; through setting extra amount on cost margin; and by minimizing cost

by taking price constant.

Value based budgeting: This method can be applied by Creams Ltd to get forecasted items which can

increase the value of core products of the company. Budgeting will categories different costs according to

different department heads and allocate funds accordingly (Macintosh and Quattrone, 2010).

LO4. Compare ways in which organizations could use Management

Accounting to respond to Financial Problems

P5. Compare how organizations are adapting management accounting systems

to respond to financial problems

Today associations are facing many issues related to money, which can be identified in different ways,

which are discussed below:

Benchmarking: It is the instrument that determines the objective to be completed by the firm for the year

related to the given funds. Benchmarking can be decided on three grounds; Plan of expenses incurred by

the organization, fiscal summary of earlier years and execution of claimants; like for example Creams ltd.

has set benchmarking of achieving 25% of previous sales revenue. On the other hand, Starbucks has set

| P a g e

benchmark on the base of cost and variable expenses. It targets to reduce wastage and decreasing variable

cost by 10% each year (Wickramasinghe and Alawattage, 2007).

KPI: Also known as key execution marker; Ratio checks are important KPIs of any association. It

increasingly thinks of the judge based on at least two years of budgetary reports and the market's standard

ratios and passes an explanation as to whether the organization performs well. For example; Creams ltd.

maintains current ratio of 2:1 as an ideal ratio; below this indicates financial problem within company.

Also company has set value 25% for profit margin. Below this standard indicates financial problem. On

the other hand; Starbucks follows return on equity, which is 9% decided by company; below this value

indicates financial problem (Granlund and Lukka, 1998).

Money Administration: This is the firm's essential structure to assess how a product chooses to garner

support for the business. There are two different ways to raise finance; Liability and Value. Both require

some cost to be paid by the business; A mixture of two costs known as the weighted normal expenditure

of capital (Corbett, 1998).

Tools to solve financial problem of both the company:

Budgeting: It is the strong tool, through which both the companies; Unilever and Tesco could make an

effort to forecast sales, variable expenses and other operating expenses; and timely check whether actual

results meet estimated result or not. Companies can also modify its strategies to match its actual

performance with budgeted one. By this way company could solve financial problem (Horngren,

Bhimani, Datar, Foster and Horngren, 2002).

Cash flow management: Through this technique both companies can improve business liquidity and

trace where the fund comes from and whether it is utilized well or not.

Comparison of both Unilever and Tesco:

For comparison; two big companies; Unilever and Tesco has been chosen. Both use some tools

to identify their financial problems. These tools have been discussed below:

Unilever:

Unilever is a big organization which sells various product lines and also has branches across the

world. It uses financial tools which are ratio analysis and growth analysis to identify any

financial problems. Also it takes previous year as a base to compare its progress and evaluate

whether company has growth or decline.

| P a g e

cost by 10% each year (Wickramasinghe and Alawattage, 2007).

KPI: Also known as key execution marker; Ratio checks are important KPIs of any association. It

increasingly thinks of the judge based on at least two years of budgetary reports and the market's standard

ratios and passes an explanation as to whether the organization performs well. For example; Creams ltd.

maintains current ratio of 2:1 as an ideal ratio; below this indicates financial problem within company.

Also company has set value 25% for profit margin. Below this standard indicates financial problem. On

the other hand; Starbucks follows return on equity, which is 9% decided by company; below this value

indicates financial problem (Granlund and Lukka, 1998).

Money Administration: This is the firm's essential structure to assess how a product chooses to garner

support for the business. There are two different ways to raise finance; Liability and Value. Both require

some cost to be paid by the business; A mixture of two costs known as the weighted normal expenditure

of capital (Corbett, 1998).

Tools to solve financial problem of both the company:

Budgeting: It is the strong tool, through which both the companies; Unilever and Tesco could make an

effort to forecast sales, variable expenses and other operating expenses; and timely check whether actual

results meet estimated result or not. Companies can also modify its strategies to match its actual

performance with budgeted one. By this way company could solve financial problem (Horngren,

Bhimani, Datar, Foster and Horngren, 2002).

Cash flow management: Through this technique both companies can improve business liquidity and

trace where the fund comes from and whether it is utilized well or not.

Comparison of both Unilever and Tesco:

For comparison; two big companies; Unilever and Tesco has been chosen. Both use some tools

to identify their financial problems. These tools have been discussed below:

Unilever:

Unilever is a big organization which sells various product lines and also has branches across the

world. It uses financial tools which are ratio analysis and growth analysis to identify any

financial problems. Also it takes previous year as a base to compare its progress and evaluate

whether company has growth or decline.

| P a g e

Turnover growth: Unilever focus on its turnover growth which is recorded to be 2% in 2019;

which has been increased by 7% compared to 2018 which was -5.1%. This shows that company

has improved its turnover compare to 2018 (Unilever annual report, 2019).

Underlying sales growth: The average sales growth of the company over 5 years is 3.3%.

Unilever use this tool to identify how much revenue it has generated over past year. The data

shows that from 2018; companies sales growth have been declined by 0.3% (2018 – 3.2%; 2019

– 2.9%).

Underlying volume growth: This shows how many units company has sold. Unilever had shown

decline in volume growth by 0.7% (2018 – 1.9%; 2019 – 1.2%).

Operating margin: It is a profit before paying any taxes and interest or income from operations

of the business. Operating margin has also decline from 2018 to 2019 by 8%.

Hence, decline in operating margin, volume growth and sales growth is financial problem for

Unilever (Unilever annual report, 2019).

Tesco:

Like Unilever; Tesco is also a big organization operating across the world and has large product

line in which it is dealing. Some of the tools used by company to know its financial problem

have been discussed below:

Net profit margin: It is net profit after paying all taxes and interests. Compare to 2018; Tesco’s

net profit margin has been declined by 1% in 2019. Which is an indication of financial problem

(Tesco annual report, 2019).

Gross profit margin: Income after paying direct expenses associated with manufacturing are

known as gross profit. Like net profit margin; gross profit also shown negative growth which is -

2% in 2019; while in 2018; it was 0% (Tesco annual report, 2019).

Return on equity: Tesco focus on return on equity to know how much profit it has earned

proportionate to equity. The result shows that, it has improved return on equity by 15% (2019 = -

16%; 2018 = -31%).

| P a g e

which has been increased by 7% compared to 2018 which was -5.1%. This shows that company

has improved its turnover compare to 2018 (Unilever annual report, 2019).

Underlying sales growth: The average sales growth of the company over 5 years is 3.3%.

Unilever use this tool to identify how much revenue it has generated over past year. The data

shows that from 2018; companies sales growth have been declined by 0.3% (2018 – 3.2%; 2019

– 2.9%).

Underlying volume growth: This shows how many units company has sold. Unilever had shown

decline in volume growth by 0.7% (2018 – 1.9%; 2019 – 1.2%).

Operating margin: It is a profit before paying any taxes and interest or income from operations

of the business. Operating margin has also decline from 2018 to 2019 by 8%.

Hence, decline in operating margin, volume growth and sales growth is financial problem for

Unilever (Unilever annual report, 2019).

Tesco:

Like Unilever; Tesco is also a big organization operating across the world and has large product

line in which it is dealing. Some of the tools used by company to know its financial problem

have been discussed below:

Net profit margin: It is net profit after paying all taxes and interests. Compare to 2018; Tesco’s

net profit margin has been declined by 1% in 2019. Which is an indication of financial problem

(Tesco annual report, 2019).

Gross profit margin: Income after paying direct expenses associated with manufacturing are

known as gross profit. Like net profit margin; gross profit also shown negative growth which is -

2% in 2019; while in 2018; it was 0% (Tesco annual report, 2019).

Return on equity: Tesco focus on return on equity to know how much profit it has earned

proportionate to equity. The result shows that, it has improved return on equity by 15% (2019 = -

16%; 2018 = -31%).

| P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore; based on above tools it can be concluded that Tesco has big financial problem as

company is facing losses over the years.

Suggested tools for analyzing financial problems for creams ltd:

Based on above comparison the suggested tools for creams ltd could be:

Ratio analysis: This is very powerful tool which can help company to identify whether it is

progressing or bearing losses compare to previous year. This tool also has an advantage of

simplicity to quick understanding and less time consuming (Drury, 2005).

Turnover growth: Creams ltd. also can use turnover growth tool to analyze the status of its

turnover over the past five years or previous year (Hoque, 2002).

M4. Analyze how, in responding to financial problems, management

accounting can lead organizations to sustainable success

1. Demand forecasting: Through forecasting demand Creams Ltd gets information about latest

trends of the market and built product accordingly to match the demand. And can lead to

sustainable success.

2. Make of buy decisions: Through estimating cost on whether to make or buy product, Creams

Ltd. has fulfilled demand on time and also increase its Net revenue through minimizing overall

costs. An appropriate decision will help company in achieving sustainable success (Sustainable

Success, 2020).

3. Activity based costing: Through this tool Creams ltd has divided all the activities or operations

on costing bases. It takes less costing activity on the top and high costing activity on bottom to

focus on each activity separately. It is done for particular period and hence can achieve

sustainable success (Budgeting and Forecasting Software, 2020).

| P a g e

company is facing losses over the years.

Suggested tools for analyzing financial problems for creams ltd:

Based on above comparison the suggested tools for creams ltd could be:

Ratio analysis: This is very powerful tool which can help company to identify whether it is

progressing or bearing losses compare to previous year. This tool also has an advantage of

simplicity to quick understanding and less time consuming (Drury, 2005).

Turnover growth: Creams ltd. also can use turnover growth tool to analyze the status of its

turnover over the past five years or previous year (Hoque, 2002).

M4. Analyze how, in responding to financial problems, management

accounting can lead organizations to sustainable success

1. Demand forecasting: Through forecasting demand Creams Ltd gets information about latest

trends of the market and built product accordingly to match the demand. And can lead to

sustainable success.

2. Make of buy decisions: Through estimating cost on whether to make or buy product, Creams

Ltd. has fulfilled demand on time and also increase its Net revenue through minimizing overall

costs. An appropriate decision will help company in achieving sustainable success (Sustainable

Success, 2020).

3. Activity based costing: Through this tool Creams ltd has divided all the activities or operations

on costing bases. It takes less costing activity on the top and high costing activity on bottom to

focus on each activity separately. It is done for particular period and hence can achieve

sustainable success (Budgeting and Forecasting Software, 2020).

| P a g e

CONCLUSION

Based on the investigation of the report it can be very well considered that; Absorption costs limit every

factor related to the cost of assembling or transaction costs; while variable costs only include those

variable costs that are related to the sale of the item. There are many situations when the booker for the

authorities has to make the necessary choices such as purchasing or choosing an option, securing related

options, choosing an enterprise from various other options and choosing the wells of the fund. These

options are not overly simple to take; it requires convenient and top-down investigation before thinking of

the end.

| P a g e

Based on the investigation of the report it can be very well considered that; Absorption costs limit every

factor related to the cost of assembling or transaction costs; while variable costs only include those

variable costs that are related to the sale of the item. There are many situations when the booker for the

authorities has to make the necessary choices such as purchasing or choosing an option, securing related

options, choosing an enterprise from various other options and choosing the wells of the fund. These

options are not overly simple to take; it requires convenient and top-down investigation before thinking of

the end.

| P a g e

REFERENCES

Books and Journals

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Budding, T., Grossi, G. and Tagesson, T. eds., 2014. Public sector accounting. Routledge.

Burns, J. and Vaivio, J., 2001. Management accounting change. Management accounting

research, 12(4).

Corbett, T., 1998. Throughput accounting: TOC's management accounting system (pp. 41-80).

Great Barrington: North river press.

Drury, C., 2005. Management accounting for business. Cengage Learning EMEA.

Granlund, M. and Lukka, K., 1998. It's a small world of management accounting

practices. Journal of management accounting research, 10, p.153.

Hansen, D., Mowen, M. and Guan, L., 2007. Cost management: accounting and control.

Cengage Learning.

Hoque, Z., 2002. Strategic management accounting. Spiro press.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T., 2002. Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Horngren, C.T., Sundem, G.L., Elliott, J.A. and Philbrick, D.R., 2002. Introduction to financial

accounting (Vol. 8). Prentice Hall.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Libby, T. and Waterhouse, J.H., 1996. Predicting change in management accounting

systems. Journal of management accounting research, 8, p.137.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2007. Management accounting change: approaches

and perspectives. Routledge.

Online

Budgeting software, 2020, Online available through: <https://www.capterra.com/budgeting-software/>

Sustainable Success, 2020, Online Available through:

<https://corporatecoachgroup.com/blog/sustainable-success>

Unilever annual report, 2019. Online available through; <https://www.unilever.com/investor-

relations/annual-report-and-accounts/>

Tesco annual report, 2019. Online available through;

<https://www.tescoplc.com/media/476423/tesco_ar_2019.pdf>

| P a g e

Books and Journals

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Budding, T., Grossi, G. and Tagesson, T. eds., 2014. Public sector accounting. Routledge.

Burns, J. and Vaivio, J., 2001. Management accounting change. Management accounting

research, 12(4).

Corbett, T., 1998. Throughput accounting: TOC's management accounting system (pp. 41-80).

Great Barrington: North river press.

Drury, C., 2005. Management accounting for business. Cengage Learning EMEA.

Granlund, M. and Lukka, K., 1998. It's a small world of management accounting

practices. Journal of management accounting research, 10, p.153.