Management Accounting Report: Financial Statements and Planning

VerifiedAdded on 2023/01/06

|15

|3855

|37

Report

AI Summary

This report provides a comprehensive analysis of management accounting, focusing on income statements, cost analysis, and planning tools within the context of Prime Furniture. It delves into microeconomic techniques, including cost volume analysis and various costing methods like absorption costing and marginal costing. The report examines the benefits and drawbacks of planning tools such as budgetary control, cash budgets, and capital budgets, along with pricing strategies and SWOT analysis. It explores the key roles of different planning tools in financial management and adapts management accounting systems to respond to financial problems, offering insights into interpreting financial statements and analyzing the use of planning tools for effective problem-solving. The report also discusses the application of these tools in responding to financial problems and offers a conclusion summarizing the key findings.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 2............................................................................................................................................3

P3. Measurement of income statements......................................................................................3

M2. Accounting techniques to produce financial statements......................................................8

D2. Interpretation of prepared financial statements....................................................................8

TASK 3........................................................................................................................................8

P4. Benefits and drawbacks of planning tool..............................................................................8

M3: Key roles of different planning tools:................................................................................11

TASK 4..........................................................................................................................................11

P5. Roles of MA systems in responding to financial-problems:...............................................11

M4. Adaption of MA systems to respond to different financial problems:...............................14

D3. Analyzing use of planning tools to respond to financial problems:...................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 2............................................................................................................................................3

P3. Measurement of income statements......................................................................................3

M2. Accounting techniques to produce financial statements......................................................8

D2. Interpretation of prepared financial statements....................................................................8

TASK 3........................................................................................................................................8

P4. Benefits and drawbacks of planning tool..............................................................................8

M3: Key roles of different planning tools:................................................................................11

TASK 4..........................................................................................................................................11

P5. Roles of MA systems in responding to financial-problems:...............................................11

M4. Adaption of MA systems to respond to different financial problems:...............................14

D3. Analyzing use of planning tools to respond to financial problems:...................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Managerial Accounting requires the adoption of specialist insights and expertise in

describing and gathering accounting details and records in a particular manner, in order to

promote management of employees in the creation of strategies, protocols and in the arranging

and tracking of organization procedures (Bedford, D.S., 2015). It provides procedures and

principles that are appropriate for efficient preparation for the selection of appropriate business

activities and for management by assessment and efficiency review. Prime Furniture, the

furniture maker firm selected for this report. The study contains detailed discussion on varied

accounting systems/frameworks, reporting methods including planning tools effective for

resolving financial problems.

MAIN BODY

TASK 2

P3. Measurement of income statements.

Micro economic techniques:

Costs – As far as accounting is concerned, the costs pertain to the monetary amount of the

expenditure / costs on raw resources, inventory, consumables, supplies, personnel, utilities, and

so forth. this is sum listed in financial statement as expenditure or costs with different titles.

Cost Volume Analysis- CV Analysis explains the dynamics of benefit dynamics in relation to

shifts in costs and quantities. In simple words, it is a forecast of the impact of prices and volumes

on profits. Formally known as CVP Study, the top management might identify the revenue level

with which company will be in a no-profit-no-loss point for this measurements. This state is

termed as break-even level.

Cost variances – These are referred to as variations if actual incurred costs are varied

from standardized costs. Whether the actual costs is narrower than the standardized costs or

if actual benefit is higher than standardized profits, the positive variability is established. Even,

Managerial Accounting requires the adoption of specialist insights and expertise in

describing and gathering accounting details and records in a particular manner, in order to

promote management of employees in the creation of strategies, protocols and in the arranging

and tracking of organization procedures (Bedford, D.S., 2015). It provides procedures and

principles that are appropriate for efficient preparation for the selection of appropriate business

activities and for management by assessment and efficiency review. Prime Furniture, the

furniture maker firm selected for this report. The study contains detailed discussion on varied

accounting systems/frameworks, reporting methods including planning tools effective for

resolving financial problems.

MAIN BODY

TASK 2

P3. Measurement of income statements.

Micro economic techniques:

Costs – As far as accounting is concerned, the costs pertain to the monetary amount of the

expenditure / costs on raw resources, inventory, consumables, supplies, personnel, utilities, and

so forth. this is sum listed in financial statement as expenditure or costs with different titles.

Cost Volume Analysis- CV Analysis explains the dynamics of benefit dynamics in relation to

shifts in costs and quantities. In simple words, it is a forecast of the impact of prices and volumes

on profits. Formally known as CVP Study, the top management might identify the revenue level

with which company will be in a no-profit-no-loss point for this measurements. This state is

termed as break-even level.

Cost variances – These are referred to as variations if actual incurred costs are varied

from standardized costs. Whether the actual costs is narrower than the standardized costs or

if actual benefit is higher than standardized profits, the positive variability is established. Even,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on the contrary, where the real expenses are greater than the normal expenses or income are

smaller, this is considered an unfavourable variation.

There is a significant variety of integral methods to drawing up financial statements such as

absorptions-method and marginal-cost method. The use of these methods enables the discovery

of various monetary and non - monetary facets. The following techniques are listed as follows:

• Cost-absorption method: Here, under this system, all production costs are clearly considered

individually in order to calculate gross profit figure.

• Marginal costing approach – The marginal costing system is primarily used for internal

reporting, with the goal of allowing managers to track and manage organisational activities. It is

a control strategy for the calculation of marginal costs as well as consequences on income of

differences in quantities or in form of a result by separating the gross costs from fixed

and variables costs (Cokins, 2013).

Product costing:

Fixed costs – These costs/expenses are those costs/expenses that typically do not change over the

longer term, even though business experiences changes to the average revenue rates or other

purchases.

Variable cost- Such costs are expenses that move up and down in certain proportion to quantity

of outputs produced.

Standard costing – This costing is a way of measuring the expense of the output process. It is just

a cost management element which the manufacturer utilizes, for example, to estimate the

spending for the next year on various costs, such as raw products, direct labours, or overheads.

Activity-based costing: This is methodology for more precise assigning of overheads costs by

assigning them to different operations. After the net expenses are assigned to the projects, the

expenses which are assigned to the things of product which are required for the tasks. The

system may be employed to reduce operating costs in a tailored way (Simons, R., 2013).

smaller, this is considered an unfavourable variation.

There is a significant variety of integral methods to drawing up financial statements such as

absorptions-method and marginal-cost method. The use of these methods enables the discovery

of various monetary and non - monetary facets. The following techniques are listed as follows:

• Cost-absorption method: Here, under this system, all production costs are clearly considered

individually in order to calculate gross profit figure.

• Marginal costing approach – The marginal costing system is primarily used for internal

reporting, with the goal of allowing managers to track and manage organisational activities. It is

a control strategy for the calculation of marginal costs as well as consequences on income of

differences in quantities or in form of a result by separating the gross costs from fixed

and variables costs (Cokins, 2013).

Product costing:

Fixed costs – These costs/expenses are those costs/expenses that typically do not change over the

longer term, even though business experiences changes to the average revenue rates or other

purchases.

Variable cost- Such costs are expenses that move up and down in certain proportion to quantity

of outputs produced.

Standard costing – This costing is a way of measuring the expense of the output process. It is just

a cost management element which the manufacturer utilizes, for example, to estimate the

spending for the next year on various costs, such as raw products, direct labours, or overheads.

Activity-based costing: This is methodology for more precise assigning of overheads costs by

assigning them to different operations. After the net expenses are assigned to the projects, the

expenses which are assigned to the things of product which are required for the tasks. The

system may be employed to reduce operating costs in a tailored way (Simons, R., 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The major role of costing process in establishing prices-it is worth taking part in establishing

prices if a firm regulates the rate in accordance with that as well. This is because, on other hand,

prices are greater than the expected expectations established by the companies.

Cost of inventory:

Inventory cost- Inventory costs are not just the amount paid for the production of the goods, as

well as the expense of keeping and storing the item for the selling of just as much as possible.

This can be divided into various categories, including purchasing expenditures, bearing

expenditures, and cost shortages.

Valuation methods:

FIFO- This approach supposes that inventory levels acquired or manufactured for the first time

are sold, while new stocks are not sold. The value of the older inventory is then assigned to the

cost of the goods delivered and the expense of the latest inventory is related to the completion of

the inventory.

LIFO- Usually, this technique is used to place accounting charges on inventory. It is based on the

assumption that the first commodity to be released / sold is the last piece of inventory purchased.

Weighted average costing method- Periodic weighted average is probably the easiest method to

stock. As the calculation is carried out at the end of the time, the net expense of the items bought

for sale is estimated and the number of total units is split. Differentiating purchases from sales is

helpful.

Calculations:

prices if a firm regulates the rate in accordance with that as well. This is because, on other hand,

prices are greater than the expected expectations established by the companies.

Cost of inventory:

Inventory cost- Inventory costs are not just the amount paid for the production of the goods, as

well as the expense of keeping and storing the item for the selling of just as much as possible.

This can be divided into various categories, including purchasing expenditures, bearing

expenditures, and cost shortages.

Valuation methods:

FIFO- This approach supposes that inventory levels acquired or manufactured for the first time

are sold, while new stocks are not sold. The value of the older inventory is then assigned to the

cost of the goods delivered and the expense of the latest inventory is related to the completion of

the inventory.

LIFO- Usually, this technique is used to place accounting charges on inventory. It is based on the

assumption that the first commodity to be released / sold is the last piece of inventory purchased.

Weighted average costing method- Periodic weighted average is probably the easiest method to

stock. As the calculation is carried out at the end of the time, the net expense of the items bought

for sale is estimated and the number of total units is split. Differentiating purchases from sales is

helpful.

Calculations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

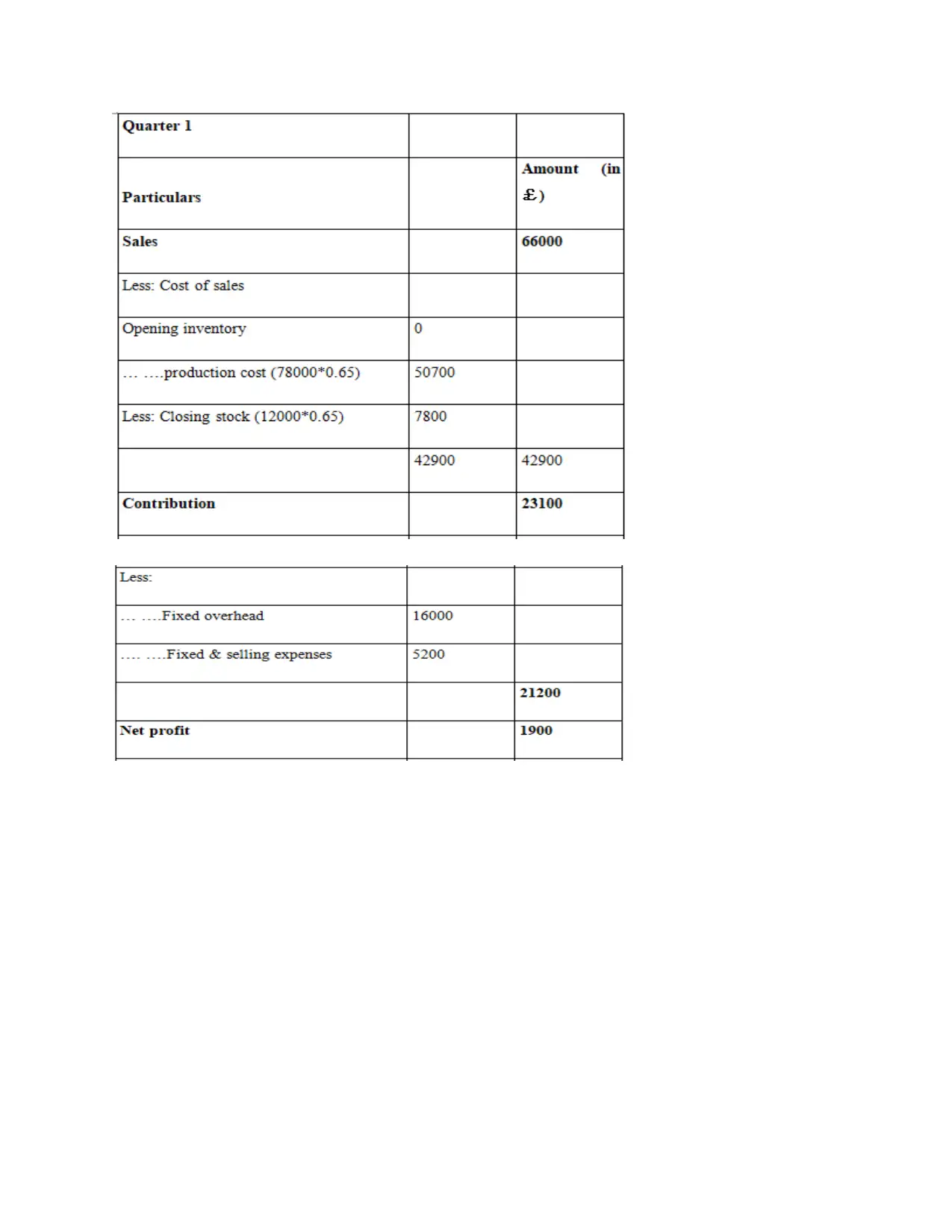

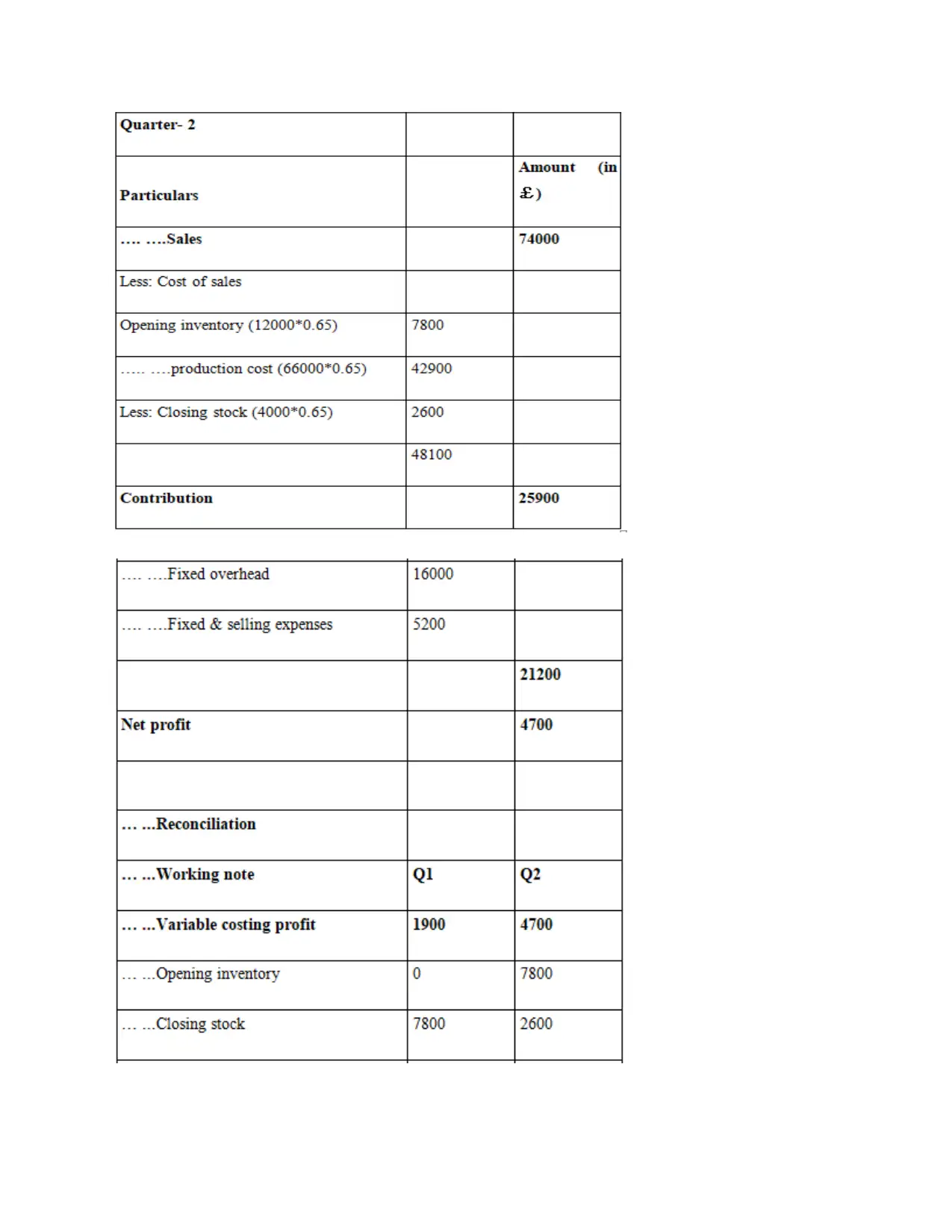

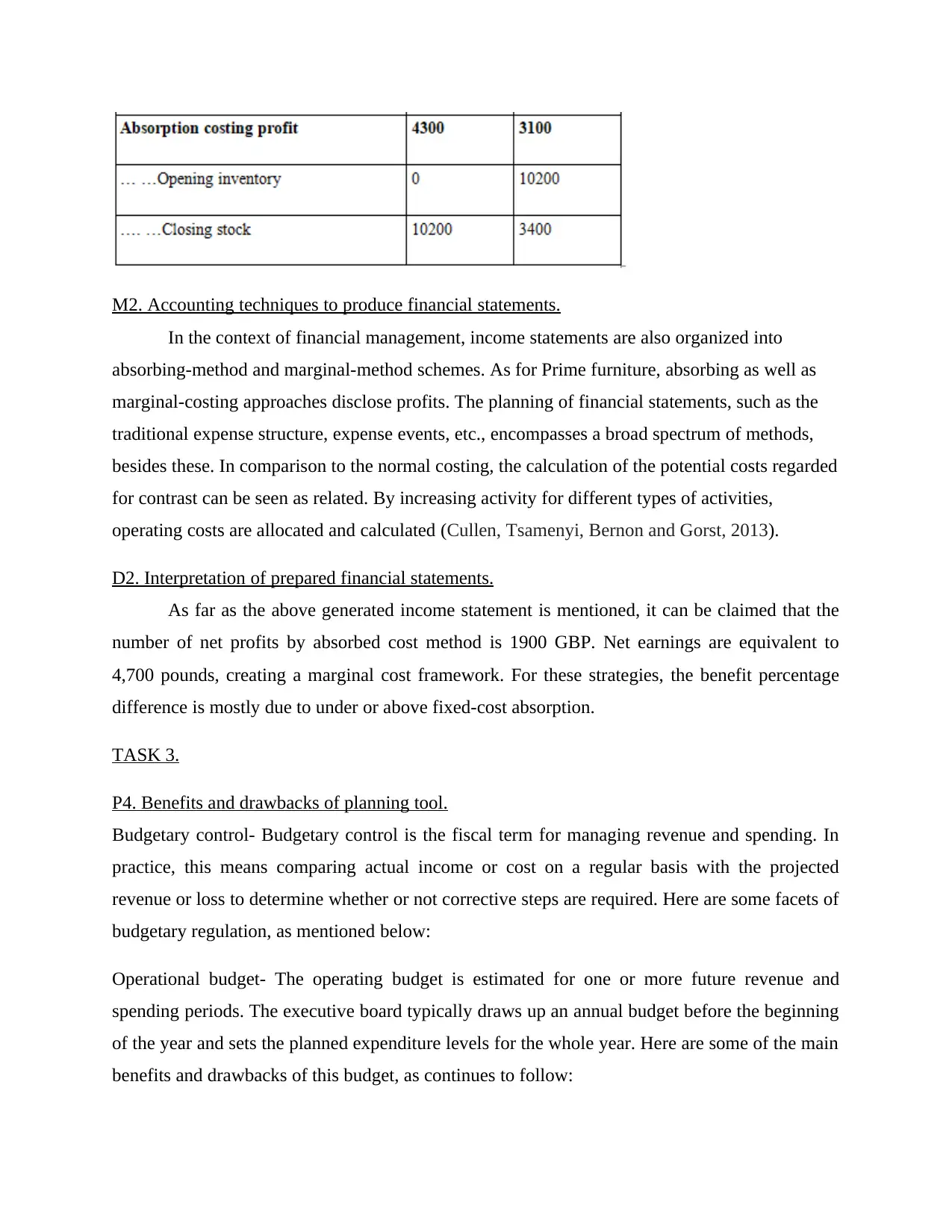

M2. Accounting techniques to produce financial statements.

In the context of financial management, income statements are also organized into

absorbing-method and marginal-method schemes. As for Prime furniture, absorbing as well as

marginal-costing approaches disclose profits. The planning of financial statements, such as the

traditional expense structure, expense events, etc., encompasses a broad spectrum of methods,

besides these. In comparison to the normal costing, the calculation of the potential costs regarded

for contrast can be seen as related. By increasing activity for different types of activities,

operating costs are allocated and calculated (Cullen, Tsamenyi, Bernon and Gorst, 2013).

D2. Interpretation of prepared financial statements.

As far as the above generated income statement is mentioned, it can be claimed that the

number of net profits by absorbed cost method is 1900 GBP. Net earnings are equivalent to

4,700 pounds, creating a marginal cost framework. For these strategies, the benefit percentage

difference is mostly due to under or above fixed-cost absorption.

TASK 3.

P4. Benefits and drawbacks of planning tool.

Budgetary control- Budgetary control is the fiscal term for managing revenue and spending. In

practice, this means comparing actual income or cost on a regular basis with the projected

revenue or loss to determine whether or not corrective steps are required. Here are some facets of

budgetary regulation, as mentioned below:

Operational budget- The operating budget is estimated for one or more future revenue and

spending periods. The executive board typically draws up an annual budget before the beginning

of the year and sets the planned expenditure levels for the whole year. Here are some of the main

benefits and drawbacks of this budget, as continues to follow:

In the context of financial management, income statements are also organized into

absorbing-method and marginal-method schemes. As for Prime furniture, absorbing as well as

marginal-costing approaches disclose profits. The planning of financial statements, such as the

traditional expense structure, expense events, etc., encompasses a broad spectrum of methods,

besides these. In comparison to the normal costing, the calculation of the potential costs regarded

for contrast can be seen as related. By increasing activity for different types of activities,

operating costs are allocated and calculated (Cullen, Tsamenyi, Bernon and Gorst, 2013).

D2. Interpretation of prepared financial statements.

As far as the above generated income statement is mentioned, it can be claimed that the

number of net profits by absorbed cost method is 1900 GBP. Net earnings are equivalent to

4,700 pounds, creating a marginal cost framework. For these strategies, the benefit percentage

difference is mostly due to under or above fixed-cost absorption.

TASK 3.

P4. Benefits and drawbacks of planning tool.

Budgetary control- Budgetary control is the fiscal term for managing revenue and spending. In

practice, this means comparing actual income or cost on a regular basis with the projected

revenue or loss to determine whether or not corrective steps are required. Here are some facets of

budgetary regulation, as mentioned below:

Operational budget- The operating budget is estimated for one or more future revenue and

spending periods. The executive board typically draws up an annual budget before the beginning

of the year and sets the planned expenditure levels for the whole year. Here are some of the main

benefits and drawbacks of this budget, as continues to follow:

Benefits- This is helpful for the organization to plan its projects successfully by determining the

real efficiency of the various projects as well as predicting them.

Drawbacks- The classification of procedures and the distribution of costs are time consuming

processes in this plan.

Cash budget- The cash estimate shall be the revenues and cash payment documentation for a

defined period of time. This is a study of monetary inflows and cash outflows for a given period

of time. The financial plan indicates the probable sales and expenses of the accounts. In other

situations, effective cash restrictions are enforced where rewards are greater than revenues.

Spending are less than income where there is excess, so the option of how to utilize excess is

made. There are some benefits and drawbacks of this proposal as follows:

Benefits- If cash is low and the gap is covered, it's useful in emergency situations. An current

bank balance makes it easier to pay on due dates, progressively dependent to reap cash-flow

bonuses.

Drawbacks- This budget mainly reflects on cash considerations and lacks other factors that limit

the importance of this budget to strategic decision-making.

Capital budget- This is a kind of plan for the purchase or repair of fixed properties, such as plant

and machinery. This is the corporate capital investment policy. Capital investment is the period

of much more than 1 year of investment accrued. It is used to buy properties or to prolong the

economic life of the assets; the funding of the project is an example of the operating expenses.

The financial planning of the plans involved would take care of the expected viability (Delafrooz

and Paim, 2011). Two calculations for calculating capital spending are used to measure the NPV

or the return on investment. The benefits and drawbacks of this proposal are set out below as

follows:

Advantage- A detailed budget analysis assesses the financial position of the respective

organization.

Drawback- Modifications are a challenge to maintain this type of budget the greatest hurdle.

Pricing:

real efficiency of the various projects as well as predicting them.

Drawbacks- The classification of procedures and the distribution of costs are time consuming

processes in this plan.

Cash budget- The cash estimate shall be the revenues and cash payment documentation for a

defined period of time. This is a study of monetary inflows and cash outflows for a given period

of time. The financial plan indicates the probable sales and expenses of the accounts. In other

situations, effective cash restrictions are enforced where rewards are greater than revenues.

Spending are less than income where there is excess, so the option of how to utilize excess is

made. There are some benefits and drawbacks of this proposal as follows:

Benefits- If cash is low and the gap is covered, it's useful in emergency situations. An current

bank balance makes it easier to pay on due dates, progressively dependent to reap cash-flow

bonuses.

Drawbacks- This budget mainly reflects on cash considerations and lacks other factors that limit

the importance of this budget to strategic decision-making.

Capital budget- This is a kind of plan for the purchase or repair of fixed properties, such as plant

and machinery. This is the corporate capital investment policy. Capital investment is the period

of much more than 1 year of investment accrued. It is used to buy properties or to prolong the

economic life of the assets; the funding of the project is an example of the operating expenses.

The financial planning of the plans involved would take care of the expected viability (Delafrooz

and Paim, 2011). Two calculations for calculating capital spending are used to measure the NPV

or the return on investment. The benefits and drawbacks of this proposal are set out below as

follows:

Advantage- A detailed budget analysis assesses the financial position of the respective

organization.

Drawback- Modifications are a challenge to maintain this type of budget the greatest hurdle.

Pricing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pricing strategies:

Penetration pricing strategy: This pricing plan instantly reduces the price of a commodity so that

a large portion of the business can be conveniently reached. The approach is successful for

customers at a lower price for the new business.

Skimming technique- Skimming pricing strategy is a pricing process in which a distribution

company initially agrees on the cost of products or services and reduces prices over time. The

corporation lowers pricing in order to recruit another value-responsive community if the rivalry

of the first consumers is exceeded.

Companies evaluate prices on the basis of industry dynamics and business activities:

organizations design prices on the basis of competitiveness. Prices are subject to the main

operations calculated and taken out.

Considerations of supply and demand- Pricing is an economic principle in the supply and

demand world. Unit or even other commercial commodities, such as labor or monetary fluid

commodities, are priced at a period where rates charged (at current rate) are all the same and

result in equal financial production and use. The prices of such goods may have been fixed.

Strategic planning

SWOT Analysis: SWOT analysis assesses internal abilities and vulnerabilities and outer chances

and risks in the company’s environmental-setting. Internal review is intended to determine the

tools, strengths, key skill sets and strategic advantages intrinsic in the enterprise. The strategic

review defines business prospects and risks by gazing at the capabilities of competition, the

business climate and the general economy (Hansen, 2011). The purpose of SWOT review in

respective company is to use the information that the organization has regarding its internally

and externally conditions and to develop its approach accordingly. This essay presents a

framework of models for performing a SWOT study and offers useful perspectives into how to

develop strategic choices.

Advantages: SWOT analysis allows the company to consider its capabilities and limitations.

Encourages strategic analysis. It allows one to concentrate on capabilities, to build or recognise

opportunities, as well as using them to its advantages. It facilitates one to anticipate potential

Penetration pricing strategy: This pricing plan instantly reduces the price of a commodity so that

a large portion of the business can be conveniently reached. The approach is successful for

customers at a lower price for the new business.

Skimming technique- Skimming pricing strategy is a pricing process in which a distribution

company initially agrees on the cost of products or services and reduces prices over time. The

corporation lowers pricing in order to recruit another value-responsive community if the rivalry

of the first consumers is exceeded.

Companies evaluate prices on the basis of industry dynamics and business activities:

organizations design prices on the basis of competitiveness. Prices are subject to the main

operations calculated and taken out.

Considerations of supply and demand- Pricing is an economic principle in the supply and

demand world. Unit or even other commercial commodities, such as labor or monetary fluid

commodities, are priced at a period where rates charged (at current rate) are all the same and

result in equal financial production and use. The prices of such goods may have been fixed.

Strategic planning

SWOT Analysis: SWOT analysis assesses internal abilities and vulnerabilities and outer chances

and risks in the company’s environmental-setting. Internal review is intended to determine the

tools, strengths, key skill sets and strategic advantages intrinsic in the enterprise. The strategic

review defines business prospects and risks by gazing at the capabilities of competition, the

business climate and the general economy (Hansen, 2011). The purpose of SWOT review in

respective company is to use the information that the organization has regarding its internally

and externally conditions and to develop its approach accordingly. This essay presents a

framework of models for performing a SWOT study and offers useful perspectives into how to

develop strategic choices.

Advantages: SWOT analysis allows the company to consider its capabilities and limitations.

Encourages strategic analysis. It allows one to concentrate on capabilities, to build or recognise

opportunities, as well as using them to its advantages. It facilitates one to anticipate potential

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

threats and also to take steps to deter or mitigate their effects. It's a basic model with no rigid

framework.

Drawbacks: Often, SWOT review may clearly lead in compiling of listings of favorable and

detrimental aspects and might not lead in the improvement and implementation of methods that

are necessary to the achieving goal. The SWOT study can be rather subjective. This can

therefore provide imbalanced or rather biased view of the scenario under review if the individual

doesn't take sufficient consideration to be impartial, analytical and have specific objectives with

respect to the intent of such review (Hopper and Bui, 2016).

M3: Key roles of different planning tools:

The planning tools are based on a straightforward but relevant logic. This helps

managers to split their plans into shorter deliverables which are simpler to accomplish. The

planning tools synthesizes raw data and then transforms it to useful information and schedule.

Planning tools depict the whole strategy and its particular components in an easy-to-receive and

evaluate performance. Different budgets help managers to analyses each level of planning

procedure and render the appropriate decisions as well as in forecasting (Kokubu and Kitada,

2015).

TASK 4

P5. Roles of MA systems in responding to financial-problems:

Financial issues/problems imply to those factors or circumstances which leads to

difficulties for business to attain their prespecified goals. Managers always concern about

handling and responding to different financial problems as to sustain business performance. In

longer period financial issues may affect business’s survival in industry thus management require

proper approach to respond to multiple financial problems. In this regard here are certain specific

financial issues which respective company is facing:

Increasing Operational Costs: Company is continually facing issue of increment in operational

costs which affects business’s overall net profitability. This is also an indication of decreasing

operational efficiency. In long run this may affect business growth and performance adversely.

framework.

Drawbacks: Often, SWOT review may clearly lead in compiling of listings of favorable and

detrimental aspects and might not lead in the improvement and implementation of methods that

are necessary to the achieving goal. The SWOT study can be rather subjective. This can

therefore provide imbalanced or rather biased view of the scenario under review if the individual

doesn't take sufficient consideration to be impartial, analytical and have specific objectives with

respect to the intent of such review (Hopper and Bui, 2016).

M3: Key roles of different planning tools:

The planning tools are based on a straightforward but relevant logic. This helps

managers to split their plans into shorter deliverables which are simpler to accomplish. The

planning tools synthesizes raw data and then transforms it to useful information and schedule.

Planning tools depict the whole strategy and its particular components in an easy-to-receive and

evaluate performance. Different budgets help managers to analyses each level of planning

procedure and render the appropriate decisions as well as in forecasting (Kokubu and Kitada,

2015).

TASK 4

P5. Roles of MA systems in responding to financial-problems:

Financial issues/problems imply to those factors or circumstances which leads to

difficulties for business to attain their prespecified goals. Managers always concern about

handling and responding to different financial problems as to sustain business performance. In

longer period financial issues may affect business’s survival in industry thus management require

proper approach to respond to multiple financial problems. In this regard here are certain specific

financial issues which respective company is facing:

Increasing Operational Costs: Company is continually facing issue of increment in operational

costs which affects business’s overall net profitability. This is also an indication of decreasing

operational efficiency. In long run this may affect business growth and performance adversely.

Mishandling of inventories: Due to mis handling of different inventories, company is facing

increase in normal and abnormal costs of inventories. This directly affects company’s gross

profit margin by increasing cost of goods sold. Inventory is material item in balance sheet which

thus mismanagement of inventories affects business’s performance (Maiyaki, 2011).

In order to deal with these financial issues management has to adopt management

accounting system as this assist managers to maintain accountability in processes and operations.

Along with systems there are specific techniques which aid in identification of main causes of

different financial problems, as listed below:

Benchmarking: Benchmarking is standard procedure and a logical technique to develop a

standard, determine best practices, find areas for change and construct a competitive atmosphere

within enterprise. Incorporating benchmarking into the company can result in useful evidence

that identify financial issues and promotes innovative concepts and activities. In respective

company, it could be used as method to help businesses identify and assess effect

of financial issues. By setting benchmarks company can easily track the root causes of financial

issues just by analyzing variations (Moser, 2012).

Key Financial Indicators: KPIs are important (key) indices of success towards the desired

outcome. KPIs concentrate on strategical and managerial change, offer an objective framework

towards decision - making, and better focus on resources on what requires most. Suppose, for

example, that sales are down for year. Company want to monitor revenues of KPIs to enable

them to increase annual revenue. Company want to add "revenue growth" to KPI dashboard.

Company's aim is to raise sales by 10% for next 6 weeks, which is a significant target as it would

make the business more financially viable. Company decide that it will calculate success against

this target by monitoring the growth in sales versus the rise in dollars expended. Company will

also understand that recruiting more sales personnel and working on customers loyalty and

engagement will help company to meet these targets. Within 6 weeks, company will know if

company has accomplished this target, but every four days, company will carry out a real-time

representation of how they're going.

Financial Governance: Financial regulation relates to sort of way in which an organization

receives, handles, tracks and regulates financial records. Financial regulation covers how

increase in normal and abnormal costs of inventories. This directly affects company’s gross

profit margin by increasing cost of goods sold. Inventory is material item in balance sheet which

thus mismanagement of inventories affects business’s performance (Maiyaki, 2011).

In order to deal with these financial issues management has to adopt management

accounting system as this assist managers to maintain accountability in processes and operations.

Along with systems there are specific techniques which aid in identification of main causes of

different financial problems, as listed below:

Benchmarking: Benchmarking is standard procedure and a logical technique to develop a

standard, determine best practices, find areas for change and construct a competitive atmosphere

within enterprise. Incorporating benchmarking into the company can result in useful evidence

that identify financial issues and promotes innovative concepts and activities. In respective

company, it could be used as method to help businesses identify and assess effect

of financial issues. By setting benchmarks company can easily track the root causes of financial

issues just by analyzing variations (Moser, 2012).

Key Financial Indicators: KPIs are important (key) indices of success towards the desired

outcome. KPIs concentrate on strategical and managerial change, offer an objective framework

towards decision - making, and better focus on resources on what requires most. Suppose, for

example, that sales are down for year. Company want to monitor revenues of KPIs to enable

them to increase annual revenue. Company want to add "revenue growth" to KPI dashboard.

Company's aim is to raise sales by 10% for next 6 weeks, which is a significant target as it would

make the business more financially viable. Company decide that it will calculate success against

this target by monitoring the growth in sales versus the rise in dollars expended. Company will

also understand that recruiting more sales personnel and working on customers loyalty and

engagement will help company to meet these targets. Within 6 weeks, company will know if

company has accomplished this target, but every four days, company will carry out a real-time

representation of how they're going.

Financial Governance: Financial regulation relates to sort of way in which an organization

receives, handles, tracks and regulates financial records. Financial regulation covers how

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

businesses monitor financial activities, monitor results and monitor information, audit, activities

and transparency. As financial control results in more comprehensive facts and figures, the

reports used by management to formulate plans and determine strategy are focused on more solid

view of financial realities of the company. This allow managers to key areas which are

responsible of different financial issues (Otley, 2016).

Here it is also relevant to discuss skills of management accountants in relation to respond

to different financial issues, as discussed below:

Communication skills: Currently, management accountant personnel not only are required to

function on report, but also are required to communicate key insights they obtain from it

to business leaders/managers. They need to be trained to do narrative and create a central

database. Communication is thus one of most important accounting management capabilities of

these times.

Predictive Skills: Management Accountants have been more focused in info, reporting and

evaluation in past years. Currently, though, the function has changed. They are

presently supposed to grasp the market thoroughly and foresee the effect of the different

variables on the activity. Currently, it creates more merit for management accountants to be

futuristic in dealings than actually evaluating the figures in hindsight (Parker, 2012).

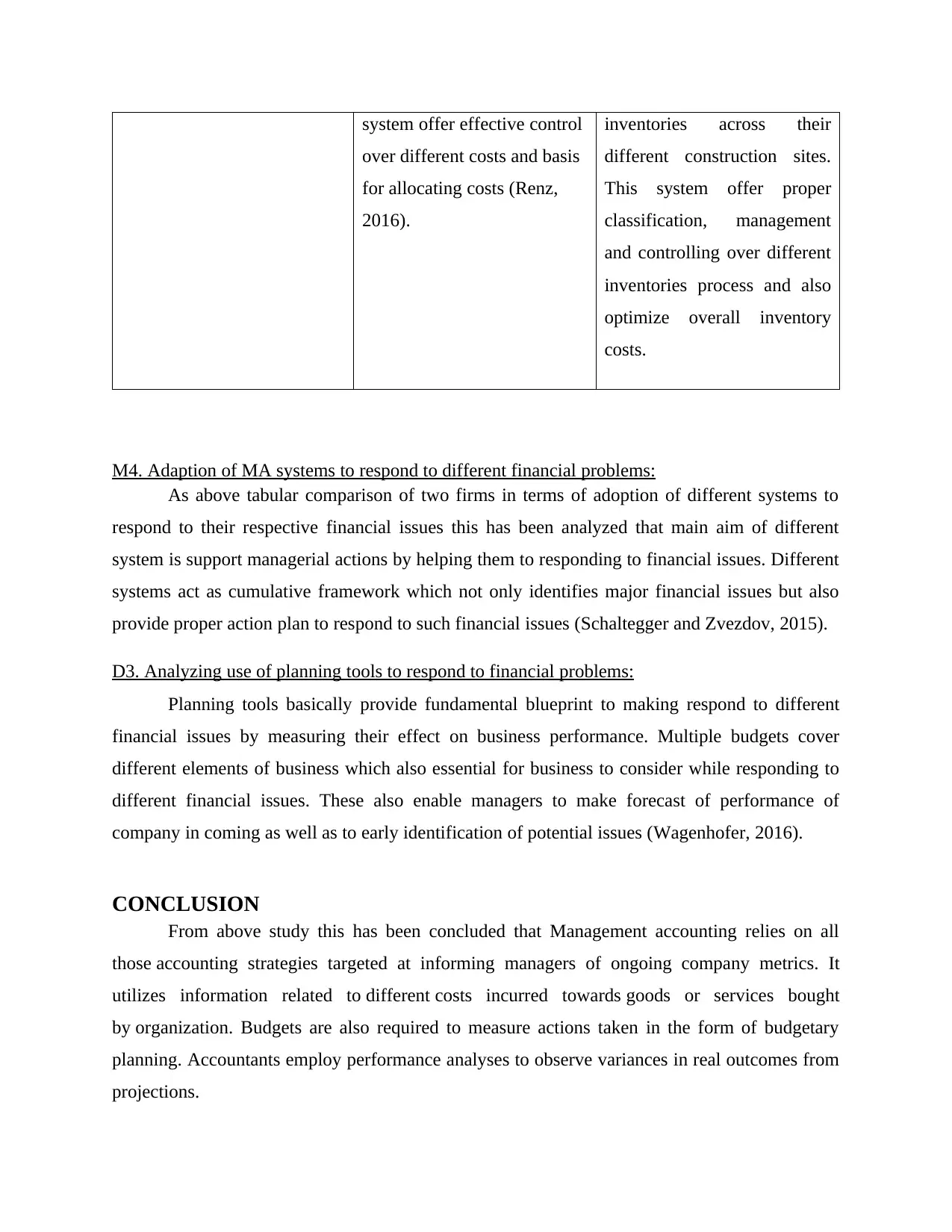

Comparison:

Basis Prime Furniture Hope Construction

Financial Issues Company is primarily facing

issue of increased operational

costs which is detrimental in

company’s profitability.

Company is struggling with

mismanagement of

inventories at their different

construction sites.

MA Systems Company must apply cost

accounting systems as to

optimize and control their

operational costs. As this

This company applies

Inventory management

system as to manager and

track their different

and transparency. As financial control results in more comprehensive facts and figures, the

reports used by management to formulate plans and determine strategy are focused on more solid

view of financial realities of the company. This allow managers to key areas which are

responsible of different financial issues (Otley, 2016).

Here it is also relevant to discuss skills of management accountants in relation to respond

to different financial issues, as discussed below:

Communication skills: Currently, management accountant personnel not only are required to

function on report, but also are required to communicate key insights they obtain from it

to business leaders/managers. They need to be trained to do narrative and create a central

database. Communication is thus one of most important accounting management capabilities of

these times.

Predictive Skills: Management Accountants have been more focused in info, reporting and

evaluation in past years. Currently, though, the function has changed. They are

presently supposed to grasp the market thoroughly and foresee the effect of the different

variables on the activity. Currently, it creates more merit for management accountants to be

futuristic in dealings than actually evaluating the figures in hindsight (Parker, 2012).

Comparison:

Basis Prime Furniture Hope Construction

Financial Issues Company is primarily facing

issue of increased operational

costs which is detrimental in

company’s profitability.

Company is struggling with

mismanagement of

inventories at their different

construction sites.

MA Systems Company must apply cost

accounting systems as to

optimize and control their

operational costs. As this

This company applies

Inventory management

system as to manager and

track their different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system offer effective control

over different costs and basis

for allocating costs (Renz,

2016).

inventories across their

different construction sites.

This system offer proper

classification, management

and controlling over different

inventories process and also

optimize overall inventory

costs.

M4. Adaption of MA systems to respond to different financial problems:

As above tabular comparison of two firms in terms of adoption of different systems to

respond to their respective financial issues this has been analyzed that main aim of different

system is support managerial actions by helping them to responding to financial issues. Different

systems act as cumulative framework which not only identifies major financial issues but also

provide proper action plan to respond to such financial issues (Schaltegger and Zvezdov, 2015).

D3. Analyzing use of planning tools to respond to financial problems:

Planning tools basically provide fundamental blueprint to making respond to different

financial issues by measuring their effect on business performance. Multiple budgets cover

different elements of business which also essential for business to consider while responding to

different financial issues. These also enable managers to make forecast of performance of

company in coming as well as to early identification of potential issues (Wagenhofer, 2016).

CONCLUSION

From above study this has been concluded that Management accounting relies on all

those accounting strategies targeted at informing managers of ongoing company metrics. It

utilizes information related to different costs incurred towards goods or services bought

by organization. Budgets are also required to measure actions taken in the form of budgetary

planning. Accountants employ performance analyses to observe variances in real outcomes from

projections.

over different costs and basis

for allocating costs (Renz,

2016).

inventories across their

different construction sites.

This system offer proper

classification, management

and controlling over different

inventories process and also

optimize overall inventory

costs.

M4. Adaption of MA systems to respond to different financial problems:

As above tabular comparison of two firms in terms of adoption of different systems to

respond to their respective financial issues this has been analyzed that main aim of different

system is support managerial actions by helping them to responding to financial issues. Different

systems act as cumulative framework which not only identifies major financial issues but also

provide proper action plan to respond to such financial issues (Schaltegger and Zvezdov, 2015).

D3. Analyzing use of planning tools to respond to financial problems:

Planning tools basically provide fundamental blueprint to making respond to different

financial issues by measuring their effect on business performance. Multiple budgets cover

different elements of business which also essential for business to consider while responding to

different financial issues. These also enable managers to make forecast of performance of

company in coming as well as to early identification of potential issues (Wagenhofer, 2016).

CONCLUSION

From above study this has been concluded that Management accounting relies on all

those accounting strategies targeted at informing managers of ongoing company metrics. It

utilizes information related to different costs incurred towards goods or services bought

by organization. Budgets are also required to measure actions taken in the form of budgetary

planning. Accountants employ performance analyses to observe variances in real outcomes from

projections.

REFERENCES

Books and Journals:

Bedford, D.S., 2015. Management control systems across different modes of innovation:

Implications for firm performance. Management Accounting Research. 28. pp.12-30.

Cokins, G., 2013. Top 7 trends in management accounting. Strategic Finance. 95(6). pp.21-30.

Cullen, J., Tsamenyi, M., Bernon, M. and Gorst, J., 2013. Reverse logistics in the UK retail

sector: A case study of the role of management accounting in driving organisational

change. Management Accounting Research. 24(3). pp.212-227.

Delafrooz, N. and Paim, L.H., 2011. Determinants of financial wellness among Malaysia

workers. African Journal of Business Management. 5(24). p.10092.

Hansen, A., 2011. Relating performative and ostensive management accounting research:

reflections on case study methodology. Qualitative Research in Accounting &

Management. 8(2). pp.108-138.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production. 108. pp.1279-1288.

Maiyaki, A.A., 2011. The Practicability of Activity Based Costing (ABC) in the Nigerian Retail

Bank. Business Intelligence Journal. 4(2). pp.351-354.

Moser, C., 2012. Gender planning and development: Theory, practice and training. Routledge.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Schaltegger, S. and Zvezdov, D., 2015. Expanding material flow cost accounting. Framework,

review and potentials. Journal of Cleaner Production. 108. pp.1333-1341.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research. 31. pp.112-117.

Books and Journals:

Bedford, D.S., 2015. Management control systems across different modes of innovation:

Implications for firm performance. Management Accounting Research. 28. pp.12-30.

Cokins, G., 2013. Top 7 trends in management accounting. Strategic Finance. 95(6). pp.21-30.

Cullen, J., Tsamenyi, M., Bernon, M. and Gorst, J., 2013. Reverse logistics in the UK retail

sector: A case study of the role of management accounting in driving organisational

change. Management Accounting Research. 24(3). pp.212-227.

Delafrooz, N. and Paim, L.H., 2011. Determinants of financial wellness among Malaysia

workers. African Journal of Business Management. 5(24). p.10092.

Hansen, A., 2011. Relating performative and ostensive management accounting research:

reflections on case study methodology. Qualitative Research in Accounting &

Management. 8(2). pp.108-138.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production. 108. pp.1279-1288.

Maiyaki, A.A., 2011. The Practicability of Activity Based Costing (ABC) in the Nigerian Retail

Bank. Business Intelligence Journal. 4(2). pp.351-354.

Moser, C., 2012. Gender planning and development: Theory, practice and training. Routledge.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Schaltegger, S. and Zvezdov, D., 2015. Expanding material flow cost accounting. Framework,

review and potentials. Journal of Cleaner Production. 108. pp.1333-1341.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research. 31. pp.112-117.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.