Management Accounting: A Comprehensive Analysis of Tech (UK) Limited

VerifiedAdded on 2024/05/30

|19

|5166

|108

AI Summary

This report delves into the intricacies of management accounting, exploring its fundamental principles, reporting techniques, and budgeting practices. Using the case study of Tech (UK) Limited, a company specializing in mobile chargers and carryout gadgets, the report analyzes the application of various management accounting tools, including absorption costing, marginal costing, and balance scorecard. It also examines the importance of budget preparation, pricing strategies, and the role of management accounting in decision-making and performance evaluation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting: Tech (UK)

Limited

1

Limited

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

In this rapid changeable business environment organisations face intense competition within the

diverse market structure due to growth and advancement in different context. Therefore, account

management is very significant part to stable overall market position by means of budgeting control,

profit as well as production measurement. The internal aspect of management is very complex, where

managers can recognize the financial situation to get a vivid report presentation of direction,

motivation, performance evaluation as well as control. This identical information is supportive for the

organisation to implement different policies as per situational demand. This report deals with the brief

discussion on management accounting and its different approaches based on the case scenario of Tech

(UK) Ltd. They produce special mobile chargers and manufacture different carryout gadgets in

various retail outlets. This report enlightens the in-depth analysis of account management and its link

with the decision-making, report presentation and budgetary control. This analysis will also display

the angle of pricing control to maintain organizational stability during emergency such as lack of

financial back up.

2

In this rapid changeable business environment organisations face intense competition within the

diverse market structure due to growth and advancement in different context. Therefore, account

management is very significant part to stable overall market position by means of budgeting control,

profit as well as production measurement. The internal aspect of management is very complex, where

managers can recognize the financial situation to get a vivid report presentation of direction,

motivation, performance evaluation as well as control. This identical information is supportive for the

organisation to implement different policies as per situational demand. This report deals with the brief

discussion on management accounting and its different approaches based on the case scenario of Tech

(UK) Ltd. They produce special mobile chargers and manufacture different carryout gadgets in

various retail outlets. This report enlightens the in-depth analysis of account management and its link

with the decision-making, report presentation and budgetary control. This analysis will also display

the angle of pricing control to maintain organizational stability during emergency such as lack of

financial back up.

2

Task 1

Tech (UK) Limited

To: Director of Finance / Line Manager

From: Management Accountant Apprentice

Subject Line: Reporting different fundamental types of management accounting

systems

a) Explanation of management accounting and the essential requirements of

management accounting system

Managerial accounting is a specialised branch, where managers can present the report in a

timely and accurate in nature. This report primarily includes both financial and non-financial

information. Through management accounting, managers can take short term and long term

decision to resolve operational consequences in a disciplinary manner. According to Boscia

and McAfee (2014), management accounting is also referred to the procedure of

measurement, recognition communication and elucidation for improving the internal

efficiency at all levels. Cost accounting, variance analysis, budget reporting and job costing

are different types of managerial accounting. From this standpoint, there are different aspect

to regulate financial accounting and management accounting.

I. Comparison of Management Accounting with Financial Accounting

In the diverse field of business operation, financial accounting and management, accounting

is operated in different contextual scenario. The major differences are as follows:-

Comparison Context Financial

accounting

Management

Accounting

Purpose It can display the Departmental

3

Tech (UK) Limited

To: Director of Finance / Line Manager

From: Management Accountant Apprentice

Subject Line: Reporting different fundamental types of management accounting

systems

a) Explanation of management accounting and the essential requirements of

management accounting system

Managerial accounting is a specialised branch, where managers can present the report in a

timely and accurate in nature. This report primarily includes both financial and non-financial

information. Through management accounting, managers can take short term and long term

decision to resolve operational consequences in a disciplinary manner. According to Boscia

and McAfee (2014), management accounting is also referred to the procedure of

measurement, recognition communication and elucidation for improving the internal

efficiency at all levels. Cost accounting, variance analysis, budget reporting and job costing

are different types of managerial accounting. From this standpoint, there are different aspect

to regulate financial accounting and management accounting.

I. Comparison of Management Accounting with Financial Accounting

In the diverse field of business operation, financial accounting and management, accounting

is operated in different contextual scenario. The major differences are as follows:-

Comparison Context Financial

accounting

Management

Accounting

Purpose It can display the Departmental

3

exact financial

position of the

company. This

report is

presented for the

support of

financial

regulators,

investors and

banks.

managers can take

effective decision on

performance

improvement through

the support of

managerial

accounting.

Outputs Output of

financial

statement is

income

statement of the

company in

annual or

monthly term.

Output of managerial

accounting is demand

report, variance report

and scheduled report.

Time horizon This report is

related financial

accounting,

which usually

prepared for one

accounting year.

This report generally

presented from an

interval of 15 to 20

years.

Behavioural

beneficiary

In this branch,

behavioural

beneficiaries are

external users

such as

investors, banks

and financial

regulators.

In this branch, internal

body such as

managers, directors

and owners are

considered as

behavioural

beneficiary.

Governing principles GAAP In this case, no such

4

position of the

company. This

report is

presented for the

support of

financial

regulators,

investors and

banks.

managers can take

effective decision on

performance

improvement through

the support of

managerial

accounting.

Outputs Output of

financial

statement is

income

statement of the

company in

annual or

monthly term.

Output of managerial

accounting is demand

report, variance report

and scheduled report.

Time horizon This report is

related financial

accounting,

which usually

prepared for one

accounting year.

This report generally

presented from an

interval of 15 to 20

years.

Behavioural

beneficiary

In this branch,

behavioural

beneficiaries are

external users

such as

investors, banks

and financial

regulators.

In this branch, internal

body such as

managers, directors

and owners are

considered as

behavioural

beneficiary.

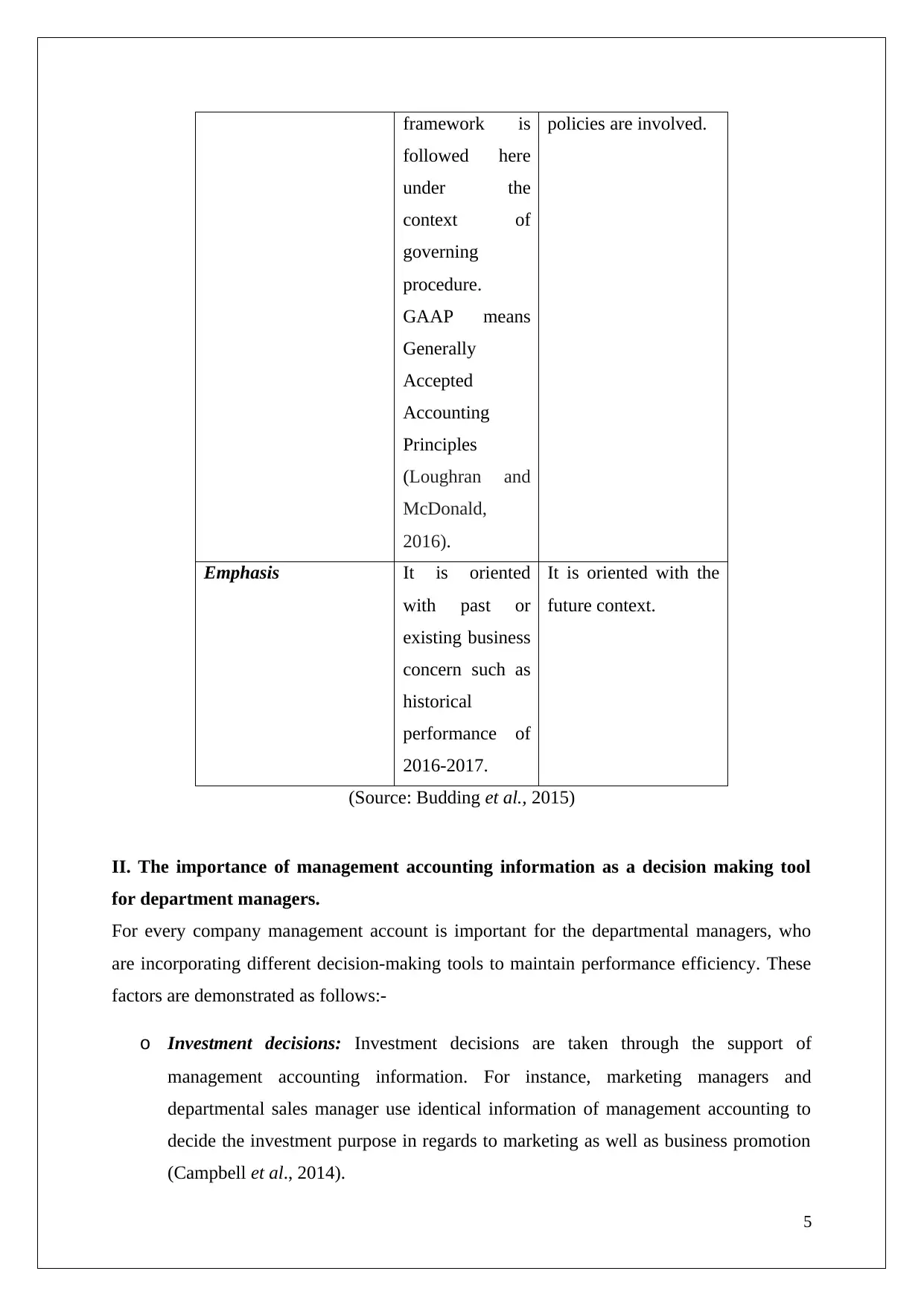

Governing principles GAAP In this case, no such

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

framework is

followed here

under the

context of

governing

procedure.

GAAP means

Generally

Accepted

Accounting

Principles

(Loughran and

McDonald,

2016).

policies are involved.

Emphasis It is oriented

with past or

existing business

concern such as

historical

performance of

2016-2017.

It is oriented with the

future context.

(Source: Budding et al., 2015)

II. The importance of management accounting information as a decision making tool

for department managers.

For every company management account is important for the departmental managers, who

are incorporating different decision-making tools to maintain performance efficiency. These

factors are demonstrated as follows:-

o Investment decisions: Investment decisions are taken through the support of

management accounting information. For instance, marketing managers and

departmental sales manager use identical information of management accounting to

decide the investment purpose in regards to marketing as well as business promotion

(Campbell et al., 2014).

5

followed here

under the

context of

governing

procedure.

GAAP means

Generally

Accepted

Accounting

Principles

(Loughran and

McDonald,

2016).

policies are involved.

Emphasis It is oriented

with past or

existing business

concern such as

historical

performance of

2016-2017.

It is oriented with the

future context.

(Source: Budding et al., 2015)

II. The importance of management accounting information as a decision making tool

for department managers.

For every company management account is important for the departmental managers, who

are incorporating different decision-making tools to maintain performance efficiency. These

factors are demonstrated as follows:-

o Investment decisions: Investment decisions are taken through the support of

management accounting information. For instance, marketing managers and

departmental sales manager use identical information of management accounting to

decide the investment purpose in regards to marketing as well as business promotion

(Campbell et al., 2014).

5

o Problem solving: Through assessing the managerial accounting details, organizational

managers can understand their gap in existing policies, which will be supportive for

introducing new policies for resolving sudden consequences.

o Operational planning: Through managerial accounting, management bodies can plan

their required daily business tactics.

o Decision-making: Decision-making has primitive role in business process, where

managerial accounting supports the managers to take priority on niche markets,

competitive markets as well as service innovation.

o Operational control

It helps the organization to take control over inventory tracking, where spending cost-

control is required to maintain profitable performance (Chouhan et al., 2017). In

addition, departmental managers can supervise their control on supply process and

purchasing with more clarified determination.

III. Cost accounting systems (actual, normal and standard costing)

Cost accounting system is associated with the cost measurement within the organisation.

According to Kandampully et al., (2015), there are three different cost accounting systems,

which are described are as follows:-

Standard costing: Departmental managers measure this cost through comparing the actual

costs of the organization as well as standard spending costs.

Actual costing: Actual measurable cost is related to cost of the service or product, which

primarily spent for procuring productivity as well as profit.

Normal costing: It measures the enterprise costs through application of both standardised

overhead cost and actual direct costs.

IV. Inventory management systems

Currently Inventory managers follow several stocking and cash controlling methods for

fostering operational performance. As per the opinion of (), there are three effective inventory

management principles for optimising inventory management within the organisation.

AVCO method (Average cost method): In the periodic inventory system, Average

cost calculates the sold goods-cost as well as cost of ending inventory. Under this

6

managers can understand their gap in existing policies, which will be supportive for

introducing new policies for resolving sudden consequences.

o Operational planning: Through managerial accounting, management bodies can plan

their required daily business tactics.

o Decision-making: Decision-making has primitive role in business process, where

managerial accounting supports the managers to take priority on niche markets,

competitive markets as well as service innovation.

o Operational control

It helps the organization to take control over inventory tracking, where spending cost-

control is required to maintain profitable performance (Chouhan et al., 2017). In

addition, departmental managers can supervise their control on supply process and

purchasing with more clarified determination.

III. Cost accounting systems (actual, normal and standard costing)

Cost accounting system is associated with the cost measurement within the organisation.

According to Kandampully et al., (2015), there are three different cost accounting systems,

which are described are as follows:-

Standard costing: Departmental managers measure this cost through comparing the actual

costs of the organization as well as standard spending costs.

Actual costing: Actual measurable cost is related to cost of the service or product, which

primarily spent for procuring productivity as well as profit.

Normal costing: It measures the enterprise costs through application of both standardised

overhead cost and actual direct costs.

IV. Inventory management systems

Currently Inventory managers follow several stocking and cash controlling methods for

fostering operational performance. As per the opinion of (), there are three effective inventory

management principles for optimising inventory management within the organisation.

AVCO method (Average cost method): In the periodic inventory system, Average

cost calculates the sold goods-cost as well as cost of ending inventory. Under this

6

method, average price is stocked for selling the entire inventory. It is a distinct but

appropriate stock management method rather than that of LIFO and FIFO

(McKercher and Tung, 2015).

LIFO method (The last in and first out): this method is incorporated while a

particular stock positioned at the last level in the storage (Kireeva, 2016). Through

this method, last level stocks are sold first as primary priority rather than selling the

first level stocks in the storage.

FIFO method (The first in & first out): this method is opposite to the LIFO method

under the term of valuation. This method is effective to maintain a structured process.

Through this method, first purchased stocks in the storage are sold out as first priority.

V. Job costing systems

These systems are used for evaluating the cost involved in different jobs in an organization. Different

types of job costing systems available are:

Contract costing: Different types of costs involved while undertaking a contract by an organization is

referred as contract costing (Kerzner and Kerzner, 2017). Few examples of contract costing are cost

involved in case of contracts related to construction of buildings, offices, hotels and so on.

Process costing: When an organization is involved in manufacturing different types of units that can

be distinguished from everyone else, then this type of job costing is adopted. In such organizations,

the job costing is calculated by determining average cost from the cost that is spend in producing each

unit.

Batch costing: In an organization, where similar kind of products is produced on a large scale, there

this type of job costing is used or adopted.

Job costing: Job costing are costs involved in accomplishing any type of action or activity in order to

fulfill customer needs. These are used in many large factories and manufacturing workshops

(Edmonds et al., 2016).

b) Presenting financial information

I. Different types of managerial accounting reports

There are many different types of management accounting reports that are often used for various

tasks. Different management accounting reports are mentioned below:

7

appropriate stock management method rather than that of LIFO and FIFO

(McKercher and Tung, 2015).

LIFO method (The last in and first out): this method is incorporated while a

particular stock positioned at the last level in the storage (Kireeva, 2016). Through

this method, last level stocks are sold first as primary priority rather than selling the

first level stocks in the storage.

FIFO method (The first in & first out): this method is opposite to the LIFO method

under the term of valuation. This method is effective to maintain a structured process.

Through this method, first purchased stocks in the storage are sold out as first priority.

V. Job costing systems

These systems are used for evaluating the cost involved in different jobs in an organization. Different

types of job costing systems available are:

Contract costing: Different types of costs involved while undertaking a contract by an organization is

referred as contract costing (Kerzner and Kerzner, 2017). Few examples of contract costing are cost

involved in case of contracts related to construction of buildings, offices, hotels and so on.

Process costing: When an organization is involved in manufacturing different types of units that can

be distinguished from everyone else, then this type of job costing is adopted. In such organizations,

the job costing is calculated by determining average cost from the cost that is spend in producing each

unit.

Batch costing: In an organization, where similar kind of products is produced on a large scale, there

this type of job costing is used or adopted.

Job costing: Job costing are costs involved in accomplishing any type of action or activity in order to

fulfill customer needs. These are used in many large factories and manufacturing workshops

(Edmonds et al., 2016).

b) Presenting financial information

I. Different types of managerial accounting reports

There are many different types of management accounting reports that are often used for various

tasks. Different management accounting reports are mentioned below:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Exception reports- This type of report provides information about unreturned or the obsolete stocks

of a firm. Another important information that can be gathered from this report is about expenses that a

company spends on maintenance.

Scheduled reports- Scheduled report includes information about the various debts that need to be

paid, thus considerably important for understanding the amount that is overdue of debtors. The report

includes information about account, balance sheet and so on (Weygandt et al., 2015).

Planning reports- The report includes information about finances and economies of the company,

usually of previous years. This report is crucial as it provides information about the financial strength

of the company, essential for determining strategies for future (Bromwich and Scapens, 2016).

Demand reports- This report provides information about several things that can be generated by a

computer. Few examples of information derived from this report is sales report, customer feedback

report and so on.

II. Why it is important for the information to be presented in manner that must be

understandable

Proper understanding of financial standing of an organization is essential for bringing any change in

the course of an organization (Fullerton et al., 2014.). Financial statement of an organization serves

many different purposes, therefore presenting them in a proper manner should be the top priority. The

following are the importance of financial information:

The future prospects of an organization are decided based on the current financial

standing of the organization

The information derived from the repot can provide insight about the performance of

the organization

It is used for finding improved plans for an organization

It is used for taking strategic and tactical decisions for an organization

Financial information is often shared with shareholders and other financial institution

to attract more funds and resources

Task 2

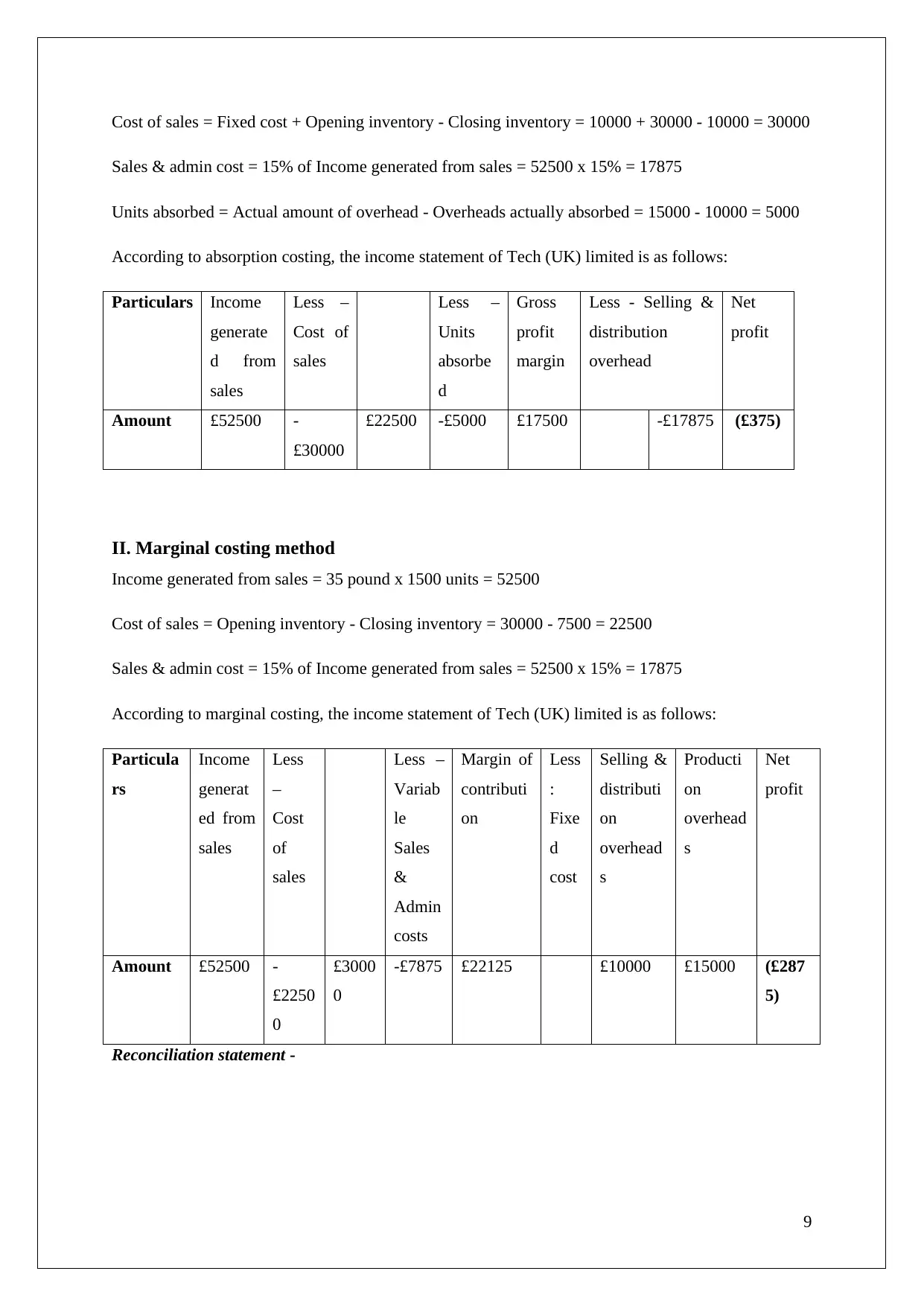

I. Absorption costing method

Income generated from sales = 35 pound x 1500 units = 52500

8

of a firm. Another important information that can be gathered from this report is about expenses that a

company spends on maintenance.

Scheduled reports- Scheduled report includes information about the various debts that need to be

paid, thus considerably important for understanding the amount that is overdue of debtors. The report

includes information about account, balance sheet and so on (Weygandt et al., 2015).

Planning reports- The report includes information about finances and economies of the company,

usually of previous years. This report is crucial as it provides information about the financial strength

of the company, essential for determining strategies for future (Bromwich and Scapens, 2016).

Demand reports- This report provides information about several things that can be generated by a

computer. Few examples of information derived from this report is sales report, customer feedback

report and so on.

II. Why it is important for the information to be presented in manner that must be

understandable

Proper understanding of financial standing of an organization is essential for bringing any change in

the course of an organization (Fullerton et al., 2014.). Financial statement of an organization serves

many different purposes, therefore presenting them in a proper manner should be the top priority. The

following are the importance of financial information:

The future prospects of an organization are decided based on the current financial

standing of the organization

The information derived from the repot can provide insight about the performance of

the organization

It is used for finding improved plans for an organization

It is used for taking strategic and tactical decisions for an organization

Financial information is often shared with shareholders and other financial institution

to attract more funds and resources

Task 2

I. Absorption costing method

Income generated from sales = 35 pound x 1500 units = 52500

8

Cost of sales = Fixed cost + Opening inventory - Closing inventory = 10000 + 30000 - 10000 = 30000

Sales & admin cost = 15% of Income generated from sales = 52500 x 15% = 17875

Units absorbed = Actual amount of overhead - Overheads actually absorbed = 15000 - 10000 = 5000

According to absorption costing, the income statement of Tech (UK) limited is as follows:

Particulars Income

generate

d from

sales

Less –

Cost of

sales

Less –

Units

absorbe

d

Gross

profit

margin

Less - Selling &

distribution

overhead

Net

profit

Amount £52500 -

£30000

£22500 -£5000 £17500 -£17875 (£375)

II. Marginal costing method

Income generated from sales = 35 pound x 1500 units = 52500

Cost of sales = Opening inventory - Closing inventory = 30000 - 7500 = 22500

Sales & admin cost = 15% of Income generated from sales = 52500 x 15% = 17875

According to marginal costing, the income statement of Tech (UK) limited is as follows:

Particula

rs

Income

generat

ed from

sales

Less

–

Cost

of

sales

Less –

Variab

le

Sales

&

Admin

costs

Margin of

contributi

on

Less

:

Fixe

d

cost

Selling &

distributi

on

overhead

s

Producti

on

overhead

s

Net

profit

Amount £52500 -

£2250

0

£3000

0

-£7875 £22125 £10000 £15000 (£287

5)

Reconciliation statement -

9

Sales & admin cost = 15% of Income generated from sales = 52500 x 15% = 17875

Units absorbed = Actual amount of overhead - Overheads actually absorbed = 15000 - 10000 = 5000

According to absorption costing, the income statement of Tech (UK) limited is as follows:

Particulars Income

generate

d from

sales

Less –

Cost of

sales

Less –

Units

absorbe

d

Gross

profit

margin

Less - Selling &

distribution

overhead

Net

profit

Amount £52500 -

£30000

£22500 -£5000 £17500 -£17875 (£375)

II. Marginal costing method

Income generated from sales = 35 pound x 1500 units = 52500

Cost of sales = Opening inventory - Closing inventory = 30000 - 7500 = 22500

Sales & admin cost = 15% of Income generated from sales = 52500 x 15% = 17875

According to marginal costing, the income statement of Tech (UK) limited is as follows:

Particula

rs

Income

generat

ed from

sales

Less

–

Cost

of

sales

Less –

Variab

le

Sales

&

Admin

costs

Margin of

contributi

on

Less

:

Fixe

d

cost

Selling &

distributi

on

overhead

s

Producti

on

overhead

s

Net

profit

Amount £52500 -

£2250

0

£3000

0

-£7875 £22125 £10000 £15000 (£287

5)

Reconciliation statement -

9

Particular

s

Profit

figure

(marginal

costing)

Add –

Fixed

expenses

Profit

figure

(absorption

costing)

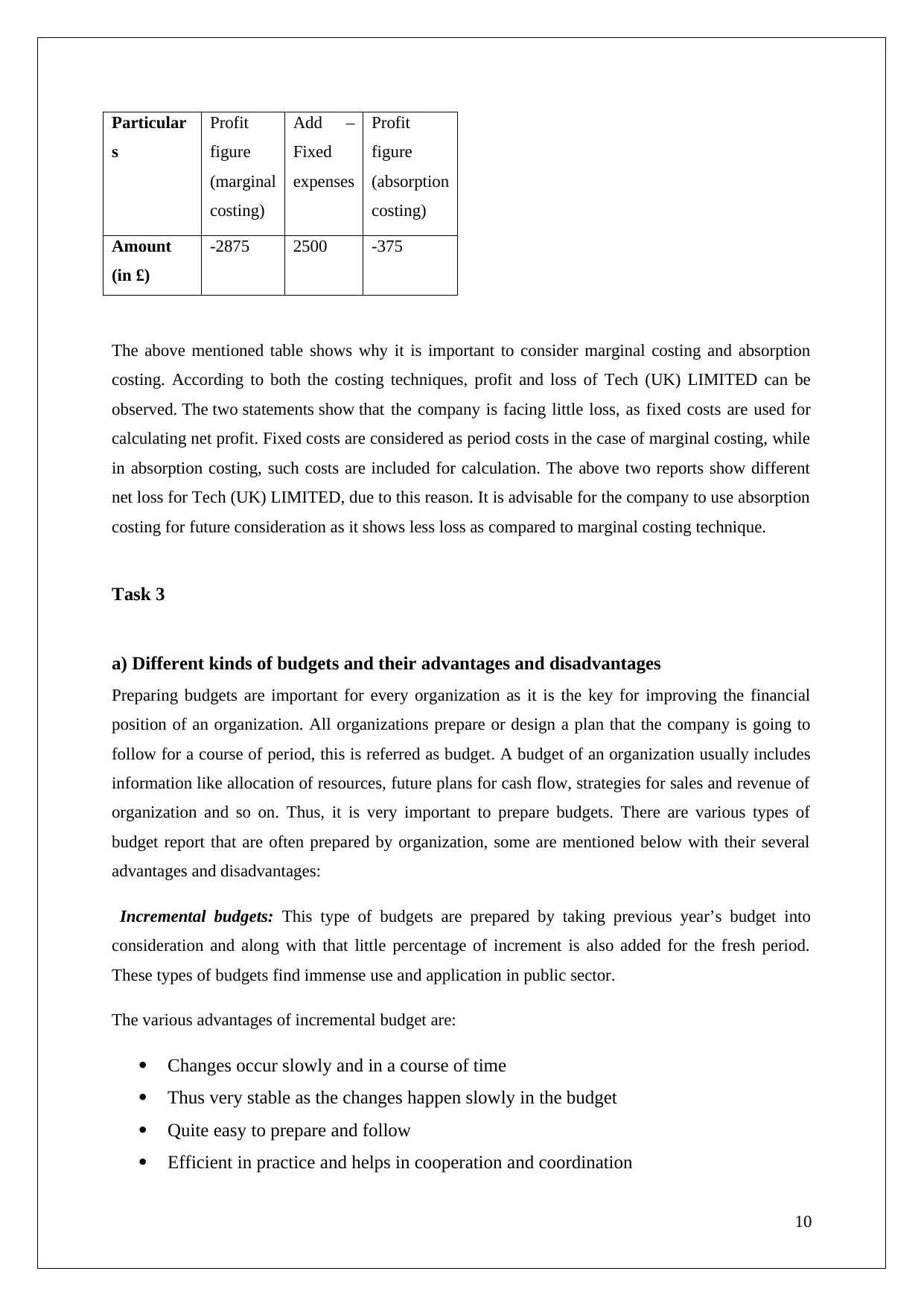

Amount

(in £)

-2875 2500 -375

The above mentioned table shows why it is important to consider marginal costing and absorption

costing. According to both the costing techniques, profit and loss of Tech (UK) LIMITED can be

observed. The two statements show that the company is facing little loss, as fixed costs are used for

calculating net profit. Fixed costs are considered as period costs in the case of marginal costing, while

in absorption costing, such costs are included for calculation. The above two reports show different

net loss for Tech (UK) LIMITED, due to this reason. It is advisable for the company to use absorption

costing for future consideration as it shows less loss as compared to marginal costing technique.

Task 3

a) Different kinds of budgets and their advantages and disadvantages

Preparing budgets are important for every organization as it is the key for improving the financial

position of an organization. All organizations prepare or design a plan that the company is going to

follow for a course of period, this is referred as budget. A budget of an organization usually includes

information like allocation of resources, future plans for cash flow, strategies for sales and revenue of

organization and so on. Thus, it is very important to prepare budgets. There are various types of

budget report that are often prepared by organization, some are mentioned below with their several

advantages and disadvantages:

Incremental budgets: This type of budgets are prepared by taking previous year’s budget into

consideration and along with that little percentage of increment is also added for the fresh period.

These types of budgets find immense use and application in public sector.

The various advantages of incremental budget are:

Changes occur slowly and in a course of time

Thus very stable as the changes happen slowly in the budget

Quite easy to prepare and follow

Efficient in practice and helps in cooperation and coordination

10

s

Profit

figure

(marginal

costing)

Add –

Fixed

expenses

Profit

figure

(absorption

costing)

Amount

(in £)

-2875 2500 -375

The above mentioned table shows why it is important to consider marginal costing and absorption

costing. According to both the costing techniques, profit and loss of Tech (UK) LIMITED can be

observed. The two statements show that the company is facing little loss, as fixed costs are used for

calculating net profit. Fixed costs are considered as period costs in the case of marginal costing, while

in absorption costing, such costs are included for calculation. The above two reports show different

net loss for Tech (UK) LIMITED, due to this reason. It is advisable for the company to use absorption

costing for future consideration as it shows less loss as compared to marginal costing technique.

Task 3

a) Different kinds of budgets and their advantages and disadvantages

Preparing budgets are important for every organization as it is the key for improving the financial

position of an organization. All organizations prepare or design a plan that the company is going to

follow for a course of period, this is referred as budget. A budget of an organization usually includes

information like allocation of resources, future plans for cash flow, strategies for sales and revenue of

organization and so on. Thus, it is very important to prepare budgets. There are various types of

budget report that are often prepared by organization, some are mentioned below with their several

advantages and disadvantages:

Incremental budgets: This type of budgets are prepared by taking previous year’s budget into

consideration and along with that little percentage of increment is also added for the fresh period.

These types of budgets find immense use and application in public sector.

The various advantages of incremental budget are:

Changes occur slowly and in a course of time

Thus very stable as the changes happen slowly in the budget

Quite easy to prepare and follow

Efficient in practice and helps in cooperation and coordination

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The various disadvantages of incremental budget are:

The budget has been observed to create obstacles and several problems for new and

unique ideas of organization

This type of budgets usually leads to far more expenditure because increments are

added while determining overall cost of the organization

Zero based budgets: This type of budgets is often made in an organization that is completely new and

fresh. In zero based budget, no reference is made to last financial year budget whatsoever and a

completely new budget from scratch is made. Thus a fresh budget gets created from base zero and all

costs and expense are included in this for the upcoming financial year.

The various advantages of zero based budgets are:

This budget helps in bringing several changes and modifications in the organization

The budget creates opportunities for improved line of communication, coordination

and cooperation

Very helpful in minimizing and removing unproductive actions and functions

The various disadvantages of zero based budgets are:

Lot skilled employees is required for executing the plan according to this budget

The budget requires lot of time and complexity

Thus very difficult to implement and creates several problems

Fixed budgets: As the name suggests, this type of budget remains fixed for the whole financial period

for which it has been designed. The budget does not involve any sort of changes or modifications in it

for its entire period of execution (Mauskopf et al., 2017). This is why it is often referred as static

budget. This type of budget often finds application in public limited companies.

The various advantages of fixed budgets are:

The method of preparing and implementing this type of budget is very easy

The costs involved in controlling the company reduce drastically

The various disadvantages of fixed budgets are:

As no changes are allowed in this type of budget, thus it loses flexibility and the

power to adjust to changes

11

The budget has been observed to create obstacles and several problems for new and

unique ideas of organization

This type of budgets usually leads to far more expenditure because increments are

added while determining overall cost of the organization

Zero based budgets: This type of budgets is often made in an organization that is completely new and

fresh. In zero based budget, no reference is made to last financial year budget whatsoever and a

completely new budget from scratch is made. Thus a fresh budget gets created from base zero and all

costs and expense are included in this for the upcoming financial year.

The various advantages of zero based budgets are:

This budget helps in bringing several changes and modifications in the organization

The budget creates opportunities for improved line of communication, coordination

and cooperation

Very helpful in minimizing and removing unproductive actions and functions

The various disadvantages of zero based budgets are:

Lot skilled employees is required for executing the plan according to this budget

The budget requires lot of time and complexity

Thus very difficult to implement and creates several problems

Fixed budgets: As the name suggests, this type of budget remains fixed for the whole financial period

for which it has been designed. The budget does not involve any sort of changes or modifications in it

for its entire period of execution (Mauskopf et al., 2017). This is why it is often referred as static

budget. This type of budget often finds application in public limited companies.

The various advantages of fixed budgets are:

The method of preparing and implementing this type of budget is very easy

The costs involved in controlling the company reduce drastically

The various disadvantages of fixed budgets are:

As no changes are allowed in this type of budget, thus it loses flexibility and the

power to adjust to changes

11

The budget is often observed to have a negative impact on the earnings of the

organization

Variable budgets: The variable budget offers lot flexibility and addictiveness in preparing and

executing this budget, because variable budgets can be changed and altered any time required (Philips

et al., 2016). A certain example of this budget would be that, if any change occurs in the production

function of the organization, the changes can be made in the budget as well. This type of budget is

often referred as variable budget.

The various advantages of variable budgets are:

Any sort of change and modification is welcomed in this type of budget

An organization facing any downturn or economic slowdown, the changes occurring

surrounding environment can be easily incorporated in the budget

The various disadvantages of variable budgets are:

The budget is difficult to understand and thus involves problems in execution

Business involves several changes and modification in its environment, thus those

updates and alterations need to be updated in the budget as well

b) The budget preparation process including determination of pricing and different

costing systems that can be used

Several steps are involved in the preparation of budget for an organization. In other words, the method

of preparing the budget often includes five different types of steps or levels. These five levels are

mentioned below:

Study of the earlier performances and the current circumstances in conjunction with

market exploration

Study and recognition of the present ability

Determination of the future prospects and necessities

Making of the budget

Accomplishment of budget and assessment of performance

The pricing strategy of an organization gives an idea about the method or way the organization

decided to price its products and services. These strategies depend on several factors like political

stability, customer preferences and needs, supply and demand issues, laws and regulations, expense of

12

organization

Variable budgets: The variable budget offers lot flexibility and addictiveness in preparing and

executing this budget, because variable budgets can be changed and altered any time required (Philips

et al., 2016). A certain example of this budget would be that, if any change occurs in the production

function of the organization, the changes can be made in the budget as well. This type of budget is

often referred as variable budget.

The various advantages of variable budgets are:

Any sort of change and modification is welcomed in this type of budget

An organization facing any downturn or economic slowdown, the changes occurring

surrounding environment can be easily incorporated in the budget

The various disadvantages of variable budgets are:

The budget is difficult to understand and thus involves problems in execution

Business involves several changes and modification in its environment, thus those

updates and alterations need to be updated in the budget as well

b) The budget preparation process including determination of pricing and different

costing systems that can be used

Several steps are involved in the preparation of budget for an organization. In other words, the method

of preparing the budget often includes five different types of steps or levels. These five levels are

mentioned below:

Study of the earlier performances and the current circumstances in conjunction with

market exploration

Study and recognition of the present ability

Determination of the future prospects and necessities

Making of the budget

Accomplishment of budget and assessment of performance

The pricing strategy of an organization gives an idea about the method or way the organization

decided to price its products and services. These strategies depend on several factors like political

stability, customer preferences and needs, supply and demand issues, laws and regulations, expense of

12

inventory and so on. Pricing strategy is highly influencing in the success or failure of a product or

service. The different pricing strategy applied is given below:

ROI pricing – This pricing strategy is effective as the price of products and services are decided on

the basis of addition or inclusion of a mark-up percentage. The mark-up percentage is actually the

quantity of profit that an organization desires to achieve and in addition the costs involved in deciding

the selling price of products and services are included. This entire pricing strategy is often called the

ROI pricing strategy (Nagle et al., 2016).

Cost plus pricing – According to this pricing strategy, an organization sets the prices of its products

and services by multiplying the cost that is spent in the production of particular product and also a

particular mark-up percentage is included to finally arrive at the selling of product or service. The

addition of the result so obtained with the expense of production gives the final selling price.

Selling price = Cost of product + (Cost of product x Markup percentage)

Variable cost pricing – This is another pricing strategy often implemented by companies in order to

set appropriate prices for their products. The prices of goods and services are set by adding the mark-

up percentage with the total variable cost that the organization has spent. However, fixed costs are not

considered while using this type of pricing strategy for setting product prices (Hull and Basu, 2016).

Absorption cost pricing – Absorption cost pricing involves deciding of product prices by considering

both indirect and direct expenses of an organization, that are spent for manufacturing the product and

service and also for comparing it with competitors.

c) The importance of budget as a tool for planning and control purposes

Budgets are nothing but future plans and designs that a company decides to follow in order to achieve

it set goals and objectives (Johnson, 2016). Thus, the importance of budget is important and essential

for deciding the course or path that needs to be followed. The importance of budget as a tool for

designing and planning is mentioned below:

Preparing a budget gives the company an idea about how to proceed and carry out

various functions

Achieving short and long term goals possible only through budget

They help in proper allocation of resources which in turn helps in proper utilization of

it

Budget allows better control over the various functions of an organization like

inventories, costs and expenses and so on

13

service. The different pricing strategy applied is given below:

ROI pricing – This pricing strategy is effective as the price of products and services are decided on

the basis of addition or inclusion of a mark-up percentage. The mark-up percentage is actually the

quantity of profit that an organization desires to achieve and in addition the costs involved in deciding

the selling price of products and services are included. This entire pricing strategy is often called the

ROI pricing strategy (Nagle et al., 2016).

Cost plus pricing – According to this pricing strategy, an organization sets the prices of its products

and services by multiplying the cost that is spent in the production of particular product and also a

particular mark-up percentage is included to finally arrive at the selling of product or service. The

addition of the result so obtained with the expense of production gives the final selling price.

Selling price = Cost of product + (Cost of product x Markup percentage)

Variable cost pricing – This is another pricing strategy often implemented by companies in order to

set appropriate prices for their products. The prices of goods and services are set by adding the mark-

up percentage with the total variable cost that the organization has spent. However, fixed costs are not

considered while using this type of pricing strategy for setting product prices (Hull and Basu, 2016).

Absorption cost pricing – Absorption cost pricing involves deciding of product prices by considering

both indirect and direct expenses of an organization, that are spent for manufacturing the product and

service and also for comparing it with competitors.

c) The importance of budget as a tool for planning and control purposes

Budgets are nothing but future plans and designs that a company decides to follow in order to achieve

it set goals and objectives (Johnson, 2016). Thus, the importance of budget is important and essential

for deciding the course or path that needs to be followed. The importance of budget as a tool for

designing and planning is mentioned below:

Preparing a budget gives the company an idea about how to proceed and carry out

various functions

Achieving short and long term goals possible only through budget

They help in proper allocation of resources which in turn helps in proper utilization of

it

Budget allows better control over the various functions of an organization like

inventories, costs and expenses and so on

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget helps in planning and organizing work and also help in meeting customer

needs and requirements

Task 4

(I)Balance scorecard and its perspectives

Balance scorecard is often viewed as technique that in management accounting that helps in

examining and determining the entire performance of an organization. They help in getting a complete

overview of financial strength of an organization (Fooladvand et al., 2015). This tool allows adding

different perspective in an organization while providing opportunities to check the finances and

economies of the organization. The four different types of perspectives that are included in balance

scorecard are given below:

Financial perspective – Balance scorecard provides a holistic view of financial strength of an

organization along with that measurement of the financial aspects of a business like determination of

total profitability, analysis of sales, checking return on investments, revenues and so on.

Customer perspective – Balance scorecard also provides customer perspective and guides in

evaluating the performance of an organization. It allows measuring the level of satisfaction of

consumers, analyzing its market share and determining brand value along with that investigating the

organizational ability of customer retention (Grijalva et al., 2016).

Internal business process perspective – This perspective is important as it support and guides in

evaluation of the internal business process of an organization or business. Inventories of an

organization, their orders, proper resource allocation in the organization and the quality control are

few processes that become easy through this perspective. Following this, allows to measure overall

efficiency of an organization.

Learning and growth perspective – This perspective, learning and growth, allows an organization to

carry out evaluation of the performance based on the learning outcome of the organization. The

various areas that are analyzed before reaching the desired outcome are evaluation of employee skills,

employee turnover, employee satisfaction, and employee education, this helps to examine the overall

performance of the organization.

14

needs and requirements

Task 4

(I)Balance scorecard and its perspectives

Balance scorecard is often viewed as technique that in management accounting that helps in

examining and determining the entire performance of an organization. They help in getting a complete

overview of financial strength of an organization (Fooladvand et al., 2015). This tool allows adding

different perspective in an organization while providing opportunities to check the finances and

economies of the organization. The four different types of perspectives that are included in balance

scorecard are given below:

Financial perspective – Balance scorecard provides a holistic view of financial strength of an

organization along with that measurement of the financial aspects of a business like determination of

total profitability, analysis of sales, checking return on investments, revenues and so on.

Customer perspective – Balance scorecard also provides customer perspective and guides in

evaluating the performance of an organization. It allows measuring the level of satisfaction of

consumers, analyzing its market share and determining brand value along with that investigating the

organizational ability of customer retention (Grijalva et al., 2016).

Internal business process perspective – This perspective is important as it support and guides in

evaluation of the internal business process of an organization or business. Inventories of an

organization, their orders, proper resource allocation in the organization and the quality control are

few processes that become easy through this perspective. Following this, allows to measure overall

efficiency of an organization.

Learning and growth perspective – This perspective, learning and growth, allows an organization to

carry out evaluation of the performance based on the learning outcome of the organization. The

various areas that are analyzed before reaching the desired outcome are evaluation of employee skills,

employee turnover, employee satisfaction, and employee education, this helps to examine the overall

performance of the organization.

14

(II) Uses of balance scorecard for identification and response to the financial problems

of Tech (UK) Limited

The Company Tech (UK) Limited has suffered a loss of 1.5 million pounds during the previous year,

according to recent findings and analysis. However, the loss suffered by the company can easily be

recovered by implementation of balance scorecard within the organization. It helps an organization to

appropriately respond to its financial problem. The financial problems of the Company Tech (UK)

Limited can be solved in following ways -

The performance of the company Tech (UK) Limited can be calculated through four

areas only because of balance scorecard approach

Balance scorecard allows the company Tech (UK) Limited to align its daily activities

to achieve maximum growth

The above mentioned approach allows to achieve long-term goals as well as short

term goals for Tech (UK) Limited

(III) Comparison of balance scorecard with another management accounting approach

and its use in another organization

The Samworth Brothers Holdings Ltd. is a manufacturing company that operates within the

boundaries of UK. The company is known as the leading manufacturers of food and pork pies in the

region. However, a complete investigation of organization shows that the company suffered a loss of

44764 million in the previous financial year 2016. This concludes that Samworth Brothers Holdings

Ltd. suffered more loss than Tech (UK) Limited. The possible reason for loss might be improper

management carried out by senior managers in the company. Further evaluation of the company,

Samworth Brothers Holdings Ltd., shows that it uses a management accounting tool known as RCA

(Resource Consumption Accounting). This technique of management accounting is an included,

active and complete approach which allows company’s managers to support and take decisions that

will help in growth and profitability optimization (Okutmus, 2015).

However, the company is facing large losses every year, only due to different loopholes in the system.

Comparison of RCA with balance scorecard provides complete evidence to understand RCA as well

as identify drawbacks of RCA.

The RCA, management accounting tool, provides lot of information in order to

optimize an enterprise. A balance scorecard provides information related to different

perspectives of an organization, which RCA cannot do or provide.

15

of Tech (UK) Limited

The Company Tech (UK) Limited has suffered a loss of 1.5 million pounds during the previous year,

according to recent findings and analysis. However, the loss suffered by the company can easily be

recovered by implementation of balance scorecard within the organization. It helps an organization to

appropriately respond to its financial problem. The financial problems of the Company Tech (UK)

Limited can be solved in following ways -

The performance of the company Tech (UK) Limited can be calculated through four

areas only because of balance scorecard approach

Balance scorecard allows the company Tech (UK) Limited to align its daily activities

to achieve maximum growth

The above mentioned approach allows to achieve long-term goals as well as short

term goals for Tech (UK) Limited

(III) Comparison of balance scorecard with another management accounting approach

and its use in another organization

The Samworth Brothers Holdings Ltd. is a manufacturing company that operates within the

boundaries of UK. The company is known as the leading manufacturers of food and pork pies in the

region. However, a complete investigation of organization shows that the company suffered a loss of

44764 million in the previous financial year 2016. This concludes that Samworth Brothers Holdings

Ltd. suffered more loss than Tech (UK) Limited. The possible reason for loss might be improper

management carried out by senior managers in the company. Further evaluation of the company,

Samworth Brothers Holdings Ltd., shows that it uses a management accounting tool known as RCA

(Resource Consumption Accounting). This technique of management accounting is an included,

active and complete approach which allows company’s managers to support and take decisions that

will help in growth and profitability optimization (Okutmus, 2015).

However, the company is facing large losses every year, only due to different loopholes in the system.

Comparison of RCA with balance scorecard provides complete evidence to understand RCA as well

as identify drawbacks of RCA.

The RCA, management accounting tool, provides lot of information in order to

optimize an enterprise. A balance scorecard provides information related to different

perspectives of an organization, which RCA cannot do or provide.

15

RCA is a quantity-based approach that helps to review and check the behavior of

expenses and resources of an organization. However, RCA fails to align the various

strategies of an organization according to day-to-day activities that is through balance

scorecard.

16

expenses and resources of an organization. However, RCA fails to align the various

strategies of an organization according to day-to-day activities that is through balance

scorecard.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conclusion

The assessment helped in understanding the management accounting and its role and importance

within an organization. Management accounting has great role and part to play in the entire

functioning and activities of an organization. There are several reporting techniques that are often

used by organizations to present their financial information. The study also helped to understand

various budgets that are developed and what are their respective advantages and disadvantages. The

report also includes information about balance scorecard and their use in context to Tech (UK) limited

and how they help in increasing management accounting. Various pricing strategies that an

organization implements in order to set prices of product or service are also briefly discussed.

17

The assessment helped in understanding the management accounting and its role and importance

within an organization. Management accounting has great role and part to play in the entire

functioning and activities of an organization. There are several reporting techniques that are often

used by organizations to present their financial information. The study also helped to understand

various budgets that are developed and what are their respective advantages and disadvantages. The

report also includes information about balance scorecard and their use in context to Tech (UK) limited

and how they help in increasing management accounting. Various pricing strategies that an

organization implements in order to set prices of product or service are also briefly discussed.

17

Reference list

Boscia, M.W. and McAfee, R.B., 2014. Using the balance scorecard approach: A group

exercise. Developments in Business Simulation and Experiential Learning, 35.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years on. Management

Accounting Research, 31, pp.1-9

Budding, T., Grossi, G. and Tagesson, T., 2015. Public sector budgeting. Public Sector Accounting,

pp.122-144.

Campbell, D., Erkens, D.H. and Loumioti, M., 2014. Exception Reports as a Source of Idiosyncratic

Information.

Chouhan, V., Soral, G. and Chandra, B., 2017. Activity based costing model for inventory

valuation. Management Science Letters, 7(3), pp.135-144.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education

Fooladvand, M., Yarmohammadian, M.H. and Shahtalebi, S., 2015. The application strategic planning

and balance scorecard modelling in enhance of higher education.Procedia-Social and Behavioral

Sciences,186, pp.950-954

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm performance:

The incremental contribution of lean management accounting practices.Journal of Operations

Management, 32(7-8), pp.414-428

Grijalva, P., Ramesh, B.K., Darrow, L. and Mirdad, W., 2016. BALANCE SCORECARD

APPROACH IN ASSESSING SOCIAL IMPACT PERFORMANCE MEASURES. InProceedings of

the International Annual Conference of the American Society for Engineering Management. (pp. 1-

11). American Society for Engineering Management (ASEM).

Hull, J.C. and Basu, S., 2016. Options, futures, and other derivatives. Pearson Education India.

Johnson, G., 2016. Exploring strategy: text and cases. Pearson Education

Kandampully, J., Zhang, T. and Bilgihan, A., 2015. Customer loyalty: a review and future directions

with a special focus on the hospitality industry. International Journal of Contemporary Hospitality

Management, 27(3), pp.379-414.

Kerzner, H. and Kerzner, H.R., 2017. Project management: a systems approach to planning,

scheduling, and controlling. John Wiley & Sons.

18

Boscia, M.W. and McAfee, R.B., 2014. Using the balance scorecard approach: A group

exercise. Developments in Business Simulation and Experiential Learning, 35.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years on. Management

Accounting Research, 31, pp.1-9

Budding, T., Grossi, G. and Tagesson, T., 2015. Public sector budgeting. Public Sector Accounting,

pp.122-144.

Campbell, D., Erkens, D.H. and Loumioti, M., 2014. Exception Reports as a Source of Idiosyncratic

Information.

Chouhan, V., Soral, G. and Chandra, B., 2017. Activity based costing model for inventory

valuation. Management Science Letters, 7(3), pp.135-144.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education

Fooladvand, M., Yarmohammadian, M.H. and Shahtalebi, S., 2015. The application strategic planning

and balance scorecard modelling in enhance of higher education.Procedia-Social and Behavioral

Sciences,186, pp.950-954

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm performance:

The incremental contribution of lean management accounting practices.Journal of Operations

Management, 32(7-8), pp.414-428

Grijalva, P., Ramesh, B.K., Darrow, L. and Mirdad, W., 2016. BALANCE SCORECARD

APPROACH IN ASSESSING SOCIAL IMPACT PERFORMANCE MEASURES. InProceedings of

the International Annual Conference of the American Society for Engineering Management. (pp. 1-

11). American Society for Engineering Management (ASEM).

Hull, J.C. and Basu, S., 2016. Options, futures, and other derivatives. Pearson Education India.

Johnson, G., 2016. Exploring strategy: text and cases. Pearson Education

Kandampully, J., Zhang, T. and Bilgihan, A., 2015. Customer loyalty: a review and future directions

with a special focus on the hospitality industry. International Journal of Contemporary Hospitality

Management, 27(3), pp.379-414.

Kerzner, H. and Kerzner, H.R., 2017. Project management: a systems approach to planning,

scheduling, and controlling. John Wiley & Sons.

18

Kireeva, E.V., 2016. Effective management of personal finance. Современные тенденции развития

науки и технологий, (5-7), pp.5-7.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A survey. Journal

of Accounting Research, 54(4), pp.1187-1230.

Mauskopf, J., Earnshaw, S. and Brogan, A., 2017. Creating Your Own Budget-Impact Analyses

Today and Tomorrow. In Budget-Impact Analysis of Health Care Interventions (pp. 217-224). Adis,

Cham.

McKercher, B. and Tung, V., 2015. Publishing in tourism and hospitality journals: Is the past a

prelude to the future?. Tourism Management, 50, pp.306-315.

Nagle, T.T., Hogan, J. and Zale, J., 2016.The Strategy and Tactics of Pricing: New International

Edition. Routledge

Okutmus, E., 2015. Resource consumption accounting with cost dimension and an application in a

glass factory. International Journal of Academic Research in Accounting, Finance and Management

Sciences, 5(1), pp.46-57.

Philips, M., Shalaby, Y. and Marden, J.R., 2016, December. The importance of budget in efficient

utility design. In Decision and Control (CDC), 2016 IEEE 55th Conference on (pp. 6117-6122). IEEE

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons

19

науки и технологий, (5-7), pp.5-7.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A survey. Journal

of Accounting Research, 54(4), pp.1187-1230.

Mauskopf, J., Earnshaw, S. and Brogan, A., 2017. Creating Your Own Budget-Impact Analyses

Today and Tomorrow. In Budget-Impact Analysis of Health Care Interventions (pp. 217-224). Adis,

Cham.

McKercher, B. and Tung, V., 2015. Publishing in tourism and hospitality journals: Is the past a

prelude to the future?. Tourism Management, 50, pp.306-315.

Nagle, T.T., Hogan, J. and Zale, J., 2016.The Strategy and Tactics of Pricing: New International

Edition. Routledge

Okutmus, E., 2015. Resource consumption accounting with cost dimension and an application in a

glass factory. International Journal of Academic Research in Accounting, Finance and Management

Sciences, 5(1), pp.46-57.

Philips, M., Shalaby, Y. and Marden, J.R., 2016, December. The importance of budget in efficient

utility design. In Decision and Control (CDC), 2016 IEEE 55th Conference on (pp. 6117-6122). IEEE

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons

19

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.