Management Accounting: A Comprehensive Guide to Cost Analysis, Budgeting, and Sustainable Success

VerifiedAdded on 2024/05/21

|25

|5248

|407

AI Summary

This report delves into the intricacies of management accounting, exploring its role in organizational decision-making, cost analysis, and strategic planning. It examines various management accounting systems, including inventory management, cost accounting, job costing, and price optimizing systems, and analyzes their benefits and applications within an organizational context. The report further investigates the integration of management accounting systems and reporting, highlighting their crucial role in achieving organizational goals. It explores different methods used for management accounting reporting, such as accounts receivable aging reports, budgeting reports, order information reports, job cost reports, and performance reports. The report also delves into the calculation of costs using marginal and absorption costing techniques, providing a comprehensive understanding of these methods and their implications for income statement preparation. Additionally, the report examines the advantages and disadvantages of different planning tools used in budgetary control, including PEST analysis, SWOT analysis, balance scorecard, and Porter's Five Forces. It analyzes how these tools can be effectively applied for preparing and forecasting budgets. The report concludes by exploring how organizations are adapting management accounting systems to respond to financial problems and how management accounting can lead organizations to sustainable success. It critically evaluates how planning tools for accounting respond appropriately to solving financial problems to lead organizations to sustainable success.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction.................................................................................................................................................3

LO 1............................................................................................................................................................4

P1) Explain management accounting and give the essential requirements of different types of

management accounting..........................................................................................................................4

P2) Explain different methods used for management accounting reporting.............................................6

M1) Evaluate benefits of management accounting systems and their application within organizational

context.....................................................................................................................................................8

D1) Critical evaluation of how management accounting systems and management accounting reporting

are integrated within organizational context............................................................................................9

LO 2..........................................................................................................................................................10

P3) Calculate cost using appropriate techniques of cost analysis to prepare income statement using

marginal and absorption costing. (M2, D2)...........................................................................................10

LO 3..........................................................................................................................................................13

P4) Explain advantages and disadvantages of different types of planning tools used in budgetary

control...................................................................................................................................................13

M3) Analyze the use of different planning tools and their application for preparing and forecasting

budget....................................................................................................................................................15

LO 4..........................................................................................................................................................17

P5) Compare how organizations are adapting management accounting systems to respond to financial

problems................................................................................................................................................17

M4) Analyze how in responding to financial problems, management accounting can lead organization

to sustainable success............................................................................................................................19

2

Introduction.................................................................................................................................................3

LO 1............................................................................................................................................................4

P1) Explain management accounting and give the essential requirements of different types of

management accounting..........................................................................................................................4

P2) Explain different methods used for management accounting reporting.............................................6

M1) Evaluate benefits of management accounting systems and their application within organizational

context.....................................................................................................................................................8

D1) Critical evaluation of how management accounting systems and management accounting reporting

are integrated within organizational context............................................................................................9

LO 2..........................................................................................................................................................10

P3) Calculate cost using appropriate techniques of cost analysis to prepare income statement using

marginal and absorption costing. (M2, D2)...........................................................................................10

LO 3..........................................................................................................................................................13

P4) Explain advantages and disadvantages of different types of planning tools used in budgetary

control...................................................................................................................................................13

M3) Analyze the use of different planning tools and their application for preparing and forecasting

budget....................................................................................................................................................15

LO 4..........................................................................................................................................................17

P5) Compare how organizations are adapting management accounting systems to respond to financial

problems................................................................................................................................................17

M4) Analyze how in responding to financial problems, management accounting can lead organization

to sustainable success............................................................................................................................19

2

D3) Critically evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organization to sustainable success.............................................................................20

Conclusion.................................................................................................................................................21

References.................................................................................................................................................22

3

problems to lead organization to sustainable success.............................................................................20

Conclusion.................................................................................................................................................21

References.................................................................................................................................................22

3

Introduction

This report discusses the management accounting and its various methods which are used by the

managers of the organizations so as to evaluate the performance. It also includes the explanation

of the management accounting systems and how they are integrated with management

accounting reporting. Through this, the understanding of the management accounting systems

will be developed. Zylla company is the multinational organization which has expanded its

business in different locations so that the new market share can be captured with the use of the

management accounting systems. Further, the income statements are also prepared using

marginal and absorption costing. The report also explains the advantages as well as the

disadvantages of the budgetary control so that the performance can be appraised. An analysis has

also been done which shows that how management accounting systems and reporting help in

solving the financial problems so that the sustainability can be achieved.

4

This report discusses the management accounting and its various methods which are used by the

managers of the organizations so as to evaluate the performance. It also includes the explanation

of the management accounting systems and how they are integrated with management

accounting reporting. Through this, the understanding of the management accounting systems

will be developed. Zylla company is the multinational organization which has expanded its

business in different locations so that the new market share can be captured with the use of the

management accounting systems. Further, the income statements are also prepared using

marginal and absorption costing. The report also explains the advantages as well as the

disadvantages of the budgetary control so that the performance can be appraised. An analysis has

also been done which shows that how management accounting systems and reporting help in

solving the financial problems so that the sustainability can be achieved.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

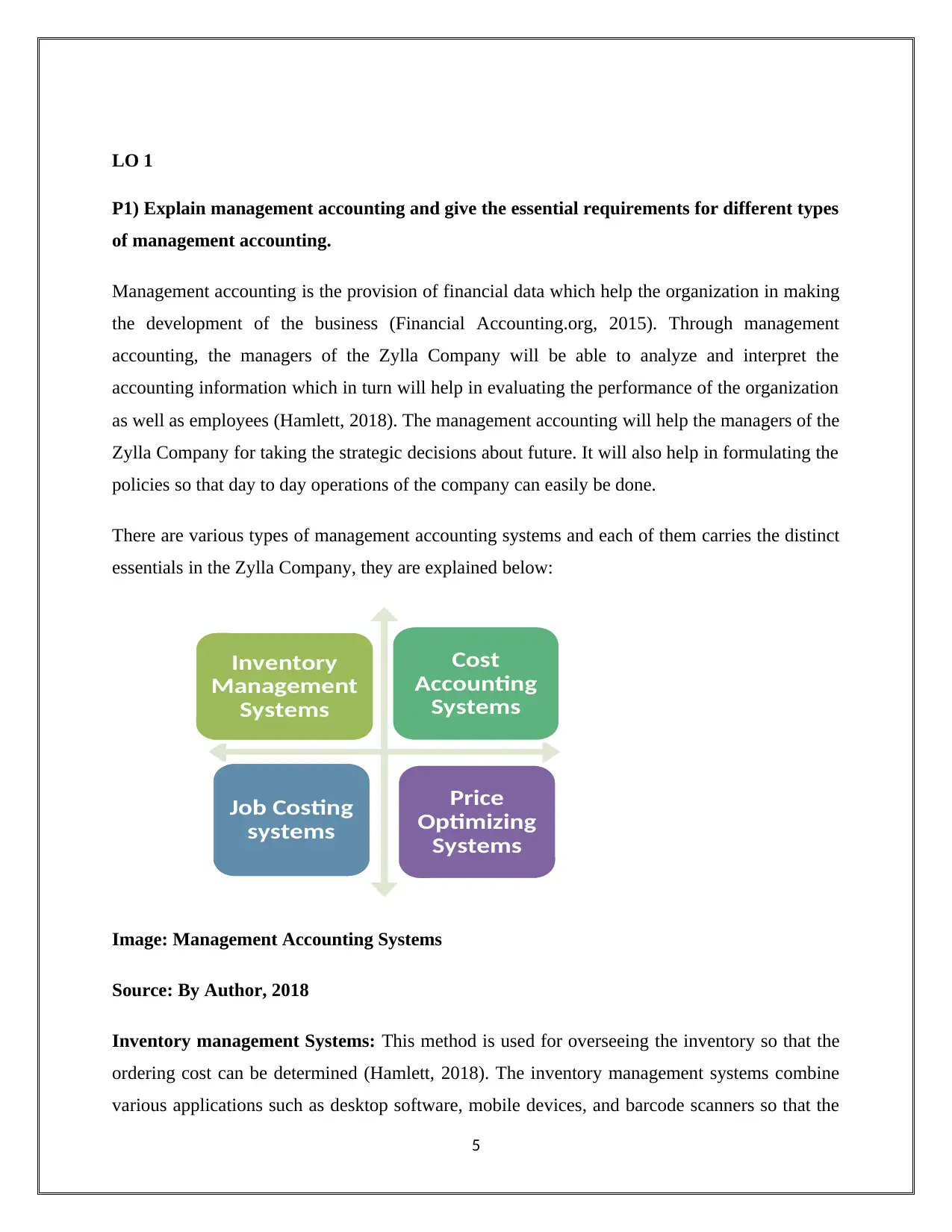

LO 1

P1) Explain management accounting and give the essential requirements for different types

of management accounting.

Management accounting is the provision of financial data which help the organization in making

the development of the business (Financial Accounting.org, 2015). Through management

accounting, the managers of the Zylla Company will be able to analyze and interpret the

accounting information which in turn will help in evaluating the performance of the organization

as well as employees (Hamlett, 2018). The management accounting will help the managers of the

Zylla Company for taking the strategic decisions about future. It will also help in formulating the

policies so that day to day operations of the company can easily be done.

There are various types of management accounting systems and each of them carries the distinct

essentials in the Zylla Company, they are explained below:

Image: Management Accounting Systems

Source: By Author, 2018

Inventory management Systems: This method is used for overseeing the inventory so that the

ordering cost can be determined (Hamlett, 2018). The inventory management systems combine

various applications such as desktop software, mobile devices, and barcode scanners so that the

5

Inventory

Management

Systems

Cost

Accounting

Systems

Job Costing

systems

Price

Optimizing

Systems

P1) Explain management accounting and give the essential requirements for different types

of management accounting.

Management accounting is the provision of financial data which help the organization in making

the development of the business (Financial Accounting.org, 2015). Through management

accounting, the managers of the Zylla Company will be able to analyze and interpret the

accounting information which in turn will help in evaluating the performance of the organization

as well as employees (Hamlett, 2018). The management accounting will help the managers of the

Zylla Company for taking the strategic decisions about future. It will also help in formulating the

policies so that day to day operations of the company can easily be done.

There are various types of management accounting systems and each of them carries the distinct

essentials in the Zylla Company, they are explained below:

Image: Management Accounting Systems

Source: By Author, 2018

Inventory management Systems: This method is used for overseeing the inventory so that the

ordering cost can be determined (Hamlett, 2018). The inventory management systems combine

various applications such as desktop software, mobile devices, and barcode scanners so that the

5

Inventory

Management

Systems

Cost

Accounting

Systems

Job Costing

systems

Price

Optimizing

Systems

inventory can be managed as suppliers, stock as well as the goods. The tracking of quantities will

enable the managers of the Zylla Company to take inventory related decisions effectively

(Hamlett, 2018).

Cost accounting Systems: These systems will determine the cost of Zylla Company’s product

so that the inventory can be evaluated, the cost can be controlled and the profitability can be

attained. This system will also help in measuring the financial performance by evaluating the

costs of input outcomes to that of the actual output (Hamlett, 2018). It is the main concept as it

offers the analytical tools such as marginal costing and absorption costing so that the

productivity can be effectively utilized.

Job Costing Systems: It is the system which allocates the cost to the individual item or the batch

of the products (Hamlett, 2018). This job costing is mainly used in the manufacturing firms

(Lister, 2018). This information is necessary as it helps in determining the accuracy of the

systems of Zylla Company which is capable of quoting prices for the reasonable income

(Hamlett, 2018).

Price Optimizing Systems: It will help Zylla Company in determining that how consumers will

react to the various prices offered for the goods as well as the services (Hamlett, 2018). It also

helps the company in determining that which price is best suited for the goods and the services

so that the gross profit can be maximized. With this, the undesired price can be minimized.

6

enable the managers of the Zylla Company to take inventory related decisions effectively

(Hamlett, 2018).

Cost accounting Systems: These systems will determine the cost of Zylla Company’s product

so that the inventory can be evaluated, the cost can be controlled and the profitability can be

attained. This system will also help in measuring the financial performance by evaluating the

costs of input outcomes to that of the actual output (Hamlett, 2018). It is the main concept as it

offers the analytical tools such as marginal costing and absorption costing so that the

productivity can be effectively utilized.

Job Costing Systems: It is the system which allocates the cost to the individual item or the batch

of the products (Hamlett, 2018). This job costing is mainly used in the manufacturing firms

(Lister, 2018). This information is necessary as it helps in determining the accuracy of the

systems of Zylla Company which is capable of quoting prices for the reasonable income

(Hamlett, 2018).

Price Optimizing Systems: It will help Zylla Company in determining that how consumers will

react to the various prices offered for the goods as well as the services (Hamlett, 2018). It also

helps the company in determining that which price is best suited for the goods and the services

so that the gross profit can be maximized. With this, the undesired price can be minimized.

6

P2) Explain different methods used for management accounting reporting.

Management accounting in the organizations is basically used for planning, controlling and

decision making. The accountants of the Zylla Company will be dependent upon the financial

statements such as balance sheet and profit & loss accounts for calculating the results

(Sarokolaei, 2012). However, the preparation of the accounting reports plays the crucial part in

the organization. Some of the reports are:

Accounts Receivable Aging Reports: These report basically focuses on managing the accounts

receivable of a particular company. These reports are prepared by the Zylla Company so that the

problem of the company’s collection period can be identified. The invoices of the customer's

balances are segregated which reveals how long the credit will be owned (Lister, 2018). It

ensures the tight credit policy of the company so that the old debs can be reduced and the

liquidity can be maintained.

Budgeting Reports: These reports help in evaluating the performance of the company. It also

provides the motivation spirit among the employees so that the organizational objectives can be

achieved (Sarokolaei, 2012). With the help of the budgets, the organization can forecast the

future costs and the expenses which will impact the company in the coming accounting period

(Lister, 2018). Through these reports, the top level managers of the Zylla Company will be able

to evaluate the financial performance of the employees.

Order Information Reports: These reports help the organization in evaluating the current

trends. This will help the Zylla Company in integrating the management and the operations to

achieve low cost while ordering the product (Lister, 2018). This will help in controlling the cost

and increasing the revenue simultaneously.

Job Cost Reports: This report provides an opportunity to the business to identify the areas of

improvement by evaluating the cost, expense as well as the profits of the particular job. By

evaluating the cost as well as the expenses the wastage of the cost can be reduced which in turn

will enhance the profitability as well as the accountability.

7

Management accounting in the organizations is basically used for planning, controlling and

decision making. The accountants of the Zylla Company will be dependent upon the financial

statements such as balance sheet and profit & loss accounts for calculating the results

(Sarokolaei, 2012). However, the preparation of the accounting reports plays the crucial part in

the organization. Some of the reports are:

Accounts Receivable Aging Reports: These report basically focuses on managing the accounts

receivable of a particular company. These reports are prepared by the Zylla Company so that the

problem of the company’s collection period can be identified. The invoices of the customer's

balances are segregated which reveals how long the credit will be owned (Lister, 2018). It

ensures the tight credit policy of the company so that the old debs can be reduced and the

liquidity can be maintained.

Budgeting Reports: These reports help in evaluating the performance of the company. It also

provides the motivation spirit among the employees so that the organizational objectives can be

achieved (Sarokolaei, 2012). With the help of the budgets, the organization can forecast the

future costs and the expenses which will impact the company in the coming accounting period

(Lister, 2018). Through these reports, the top level managers of the Zylla Company will be able

to evaluate the financial performance of the employees.

Order Information Reports: These reports help the organization in evaluating the current

trends. This will help the Zylla Company in integrating the management and the operations to

achieve low cost while ordering the product (Lister, 2018). This will help in controlling the cost

and increasing the revenue simultaneously.

Job Cost Reports: This report provides an opportunity to the business to identify the areas of

improvement by evaluating the cost, expense as well as the profits of the particular job. By

evaluating the cost as well as the expenses the wastage of the cost can be reduced which in turn

will enhance the profitability as well as the accountability.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Reports: It calculates the differences between the actual results as well as the

budgeted results so that the performance can be evaluated (Lister, 2018). The results of these

variances are then recorded in the performance reports. The performance reports are prepared on

the yearly basis as the budgets are prepared for the whole accounting period (Lister, 2018). The

results arrived from these reports also helps in determining the areas where the effectiveness can

be maximized to attain profits (Sarokolaei, 2012).

8

budgeted results so that the performance can be evaluated (Lister, 2018). The results of these

variances are then recorded in the performance reports. The performance reports are prepared on

the yearly basis as the budgets are prepared for the whole accounting period (Lister, 2018). The

results arrived from these reports also helps in determining the areas where the effectiveness can

be maximized to attain profits (Sarokolaei, 2012).

8

M1) Evaluate benefits of management accounting systems and their application within an

organizational context.

The application of the management accounting systems will provide various benefits to the Zylla

Company but for the ease of understanding the benefits of those systems are explained which

have been discussed earlier.

Inventory Management Systems:

The application of the inventory management systems in the Zylla Company will

improve the effectiveness as well as the productivity in the organization by saving the

time as well as money (Lister, 2018).

The accuracy of the ordering cost will be maintained.

Cost Accounting Systems:

The will be controlled cost control which in turn will help in reducing the prices of the

Zylla Company (Lister, 2018).

It also provides all the information which is necessary for planning.

Job Costing Systems:

It will help in eliminating the wastage of cost during the manufacturing process.

Through this Zylla, Company will be able to evaluate the quality of the goods produced

(Lister, 2018).

Price Optimizing Systems:

With the price optimizing system, the Zylla Company will be able to maximize the gross

profit of the organization by selecting the appropriate price.

The attitude of customers towards the various prices of the products can also be evaluated

(Lister, 2018).

9

organizational context.

The application of the management accounting systems will provide various benefits to the Zylla

Company but for the ease of understanding the benefits of those systems are explained which

have been discussed earlier.

Inventory Management Systems:

The application of the inventory management systems in the Zylla Company will

improve the effectiveness as well as the productivity in the organization by saving the

time as well as money (Lister, 2018).

The accuracy of the ordering cost will be maintained.

Cost Accounting Systems:

The will be controlled cost control which in turn will help in reducing the prices of the

Zylla Company (Lister, 2018).

It also provides all the information which is necessary for planning.

Job Costing Systems:

It will help in eliminating the wastage of cost during the manufacturing process.

Through this Zylla, Company will be able to evaluate the quality of the goods produced

(Lister, 2018).

Price Optimizing Systems:

With the price optimizing system, the Zylla Company will be able to maximize the gross

profit of the organization by selecting the appropriate price.

The attitude of customers towards the various prices of the products can also be evaluated

(Lister, 2018).

9

D1) Critical evaluation of how management accounting systems and management

accounting reporting are integrated within an organizational context.

Both management accounting systems as well the management accounting reporting are

integrated within the organizations as they both help in attaining the profits for the organization.

With the accounts, receivable aging reports the timely collection of the accounts

receivable can be done in the organization which will help monitoring the collection

policy from time to time so as to ensure accuracy as well as profitability (Gregory, 2018).

The budgeting reports will help in analyzing the performance with that the targets are

also set through which all the employees in the Zylla Company will work toward the

achievement of the common objectives (Gregory, 2018).

The performance of the employees can be evaluated through the performance reports

which will bring the competitive spirit among the employees.

With the integration of the inventory management reports with that of the systems will

help in reducing the wastage of the inventory as it helps in determining the accurate level

of the purchases. The integration process helps in better management of the inventory

levels.

Through the cost reports the Zylla Company will easily be able to evaluate the pricing

strategy for the product which in turn will help them to capture the market share and

hence increase profits.

All the reports critically help in analyzing the situations which will help in making the

decisions related to the financial position of the Zylla Company (Kolios and Read, 2013).

10

accounting reporting are integrated within an organizational context.

Both management accounting systems as well the management accounting reporting are

integrated within the organizations as they both help in attaining the profits for the organization.

With the accounts, receivable aging reports the timely collection of the accounts

receivable can be done in the organization which will help monitoring the collection

policy from time to time so as to ensure accuracy as well as profitability (Gregory, 2018).

The budgeting reports will help in analyzing the performance with that the targets are

also set through which all the employees in the Zylla Company will work toward the

achievement of the common objectives (Gregory, 2018).

The performance of the employees can be evaluated through the performance reports

which will bring the competitive spirit among the employees.

With the integration of the inventory management reports with that of the systems will

help in reducing the wastage of the inventory as it helps in determining the accurate level

of the purchases. The integration process helps in better management of the inventory

levels.

Through the cost reports the Zylla Company will easily be able to evaluate the pricing

strategy for the product which in turn will help them to capture the market share and

hence increase profits.

All the reports critically help in analyzing the situations which will help in making the

decisions related to the financial position of the Zylla Company (Kolios and Read, 2013).

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

LO 2

P3) Calculate cost using appropriate techniques of cost analysis to prepare income

statement using marginal and absorption costing. (M2, D2)

Scenario:

Selling Price £35

Unit Costs:

Direct Material £6

Direct Labor £5

Variable Production Overhead £2

Variable Sales Overhead £1

Fixed Costs:

Production Overhead =£1,800

Administration Cost = £800

Selling Cost = £400

Actual Sales = 500 Units

Actual production =600 Units

Solution:

Working Notes

Direct Materials £6

Direct Labor £5

Variable cost £2

Total cost £1

3

Cost: The cost is defined as the value of money in the monetary terms. These costs are incurred

in the goods as well as the services (Nawaz, 2013). The cost can be fixed as well as variable.

Fixed costs are those costs that remain constant with the change in the level of the output. The

11

P3) Calculate cost using appropriate techniques of cost analysis to prepare income

statement using marginal and absorption costing. (M2, D2)

Scenario:

Selling Price £35

Unit Costs:

Direct Material £6

Direct Labor £5

Variable Production Overhead £2

Variable Sales Overhead £1

Fixed Costs:

Production Overhead =£1,800

Administration Cost = £800

Selling Cost = £400

Actual Sales = 500 Units

Actual production =600 Units

Solution:

Working Notes

Direct Materials £6

Direct Labor £5

Variable cost £2

Total cost £1

3

Cost: The cost is defined as the value of money in the monetary terms. These costs are incurred

in the goods as well as the services (Nawaz, 2013). The cost can be fixed as well as variable.

Fixed costs are those costs that remain constant with the change in the level of the output. The

11

value of the fixed cost decreases with the increase in output. The variable cost is the cost which

changes with the change in output. It increases with the increase in output (Nawaz, 2013).

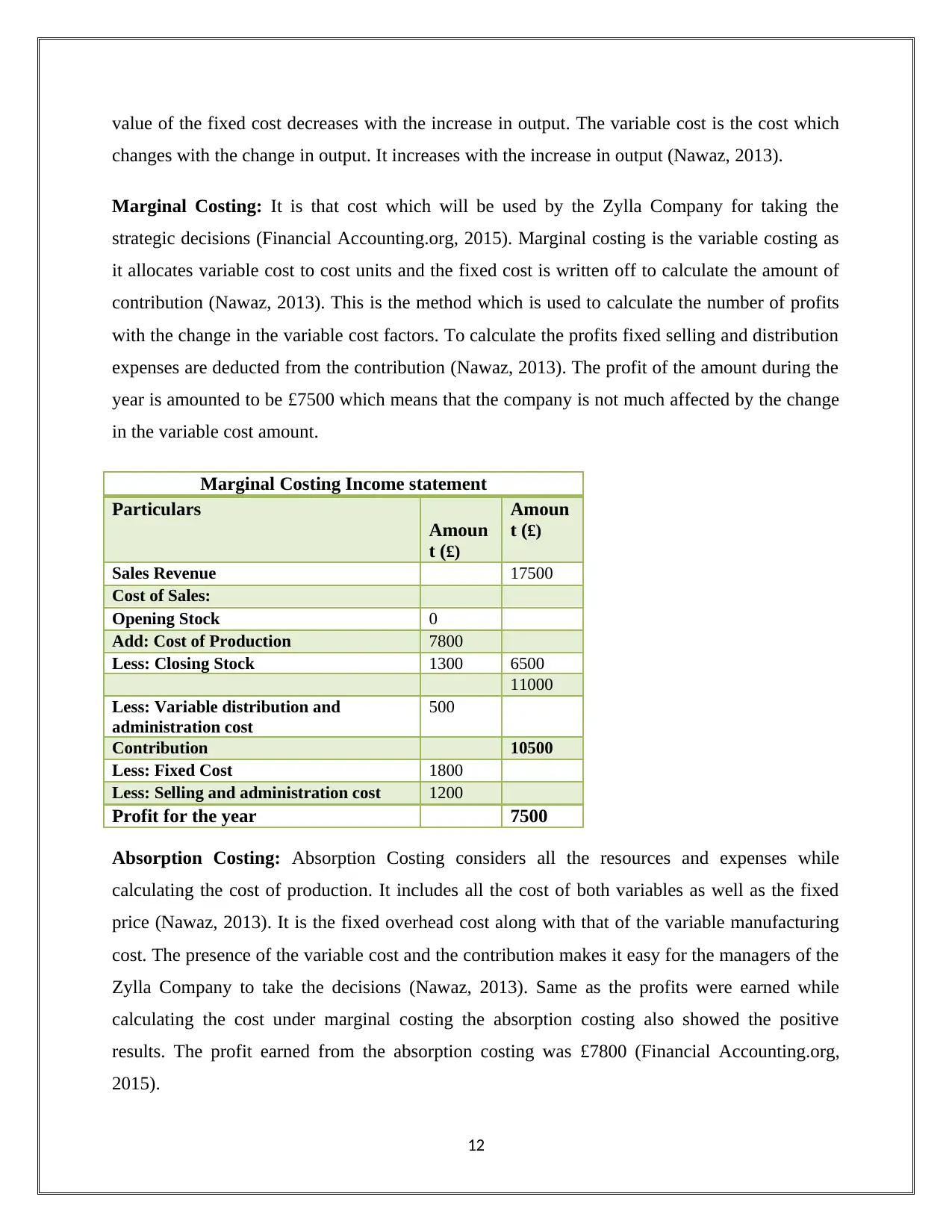

Marginal Costing: It is that cost which will be used by the Zylla Company for taking the

strategic decisions (Financial Accounting.org, 2015). Marginal costing is the variable costing as

it allocates variable cost to cost units and the fixed cost is written off to calculate the amount of

contribution (Nawaz, 2013). This is the method which is used to calculate the number of profits

with the change in the variable cost factors. To calculate the profits fixed selling and distribution

expenses are deducted from the contribution (Nawaz, 2013). The profit of the amount during the

year is amounted to be £7500 which means that the company is not much affected by the change

in the variable cost amount.

Marginal Costing Income statement

Particulars

Amoun

t (£)

Amoun

t (£)

Sales Revenue 17500

Cost of Sales:

Opening Stock 0

Add: Cost of Production 7800

Less: Closing Stock 1300 6500

11000

Less: Variable distribution and

administration cost

500

Contribution 10500

Less: Fixed Cost 1800

Less: Selling and administration cost 1200

Profit for the year 7500

Absorption Costing: Absorption Costing considers all the resources and expenses while

calculating the cost of production. It includes all the cost of both variables as well as the fixed

price (Nawaz, 2013). It is the fixed overhead cost along with that of the variable manufacturing

cost. The presence of the variable cost and the contribution makes it easy for the managers of the

Zylla Company to take the decisions (Nawaz, 2013). Same as the profits were earned while

calculating the cost under marginal costing the absorption costing also showed the positive

results. The profit earned from the absorption costing was £7800 (Financial Accounting.org,

2015).

12

changes with the change in output. It increases with the increase in output (Nawaz, 2013).

Marginal Costing: It is that cost which will be used by the Zylla Company for taking the

strategic decisions (Financial Accounting.org, 2015). Marginal costing is the variable costing as

it allocates variable cost to cost units and the fixed cost is written off to calculate the amount of

contribution (Nawaz, 2013). This is the method which is used to calculate the number of profits

with the change in the variable cost factors. To calculate the profits fixed selling and distribution

expenses are deducted from the contribution (Nawaz, 2013). The profit of the amount during the

year is amounted to be £7500 which means that the company is not much affected by the change

in the variable cost amount.

Marginal Costing Income statement

Particulars

Amoun

t (£)

Amoun

t (£)

Sales Revenue 17500

Cost of Sales:

Opening Stock 0

Add: Cost of Production 7800

Less: Closing Stock 1300 6500

11000

Less: Variable distribution and

administration cost

500

Contribution 10500

Less: Fixed Cost 1800

Less: Selling and administration cost 1200

Profit for the year 7500

Absorption Costing: Absorption Costing considers all the resources and expenses while

calculating the cost of production. It includes all the cost of both variables as well as the fixed

price (Nawaz, 2013). It is the fixed overhead cost along with that of the variable manufacturing

cost. The presence of the variable cost and the contribution makes it easy for the managers of the

Zylla Company to take the decisions (Nawaz, 2013). Same as the profits were earned while

calculating the cost under marginal costing the absorption costing also showed the positive

results. The profit earned from the absorption costing was £7800 (Financial Accounting.org,

2015).

12

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

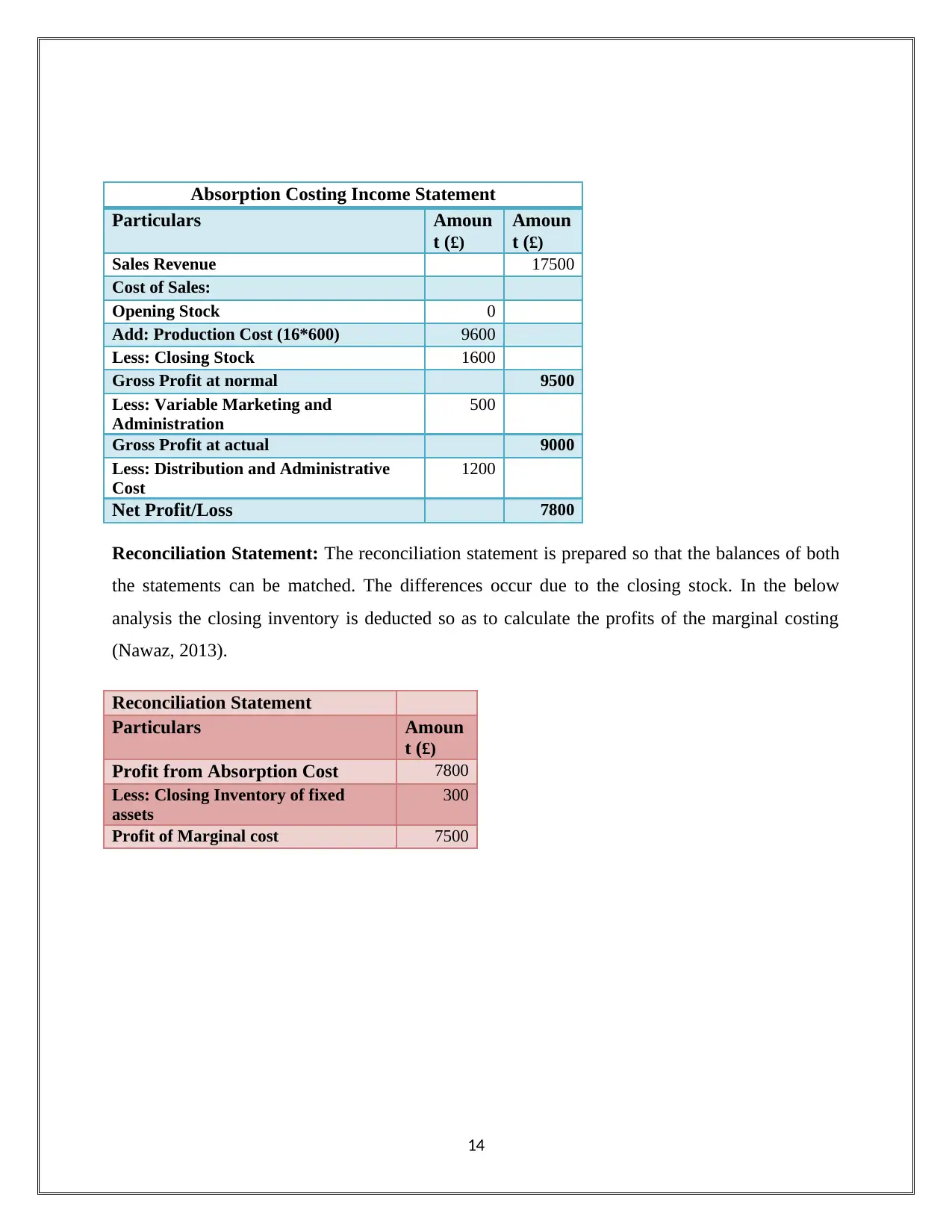

Absorption Costing Income Statement

Particulars Amoun

t (£)

Amoun

t (£)

Sales Revenue 17500

Cost of Sales:

Opening Stock 0

Add: Production Cost (16*600) 9600

Less: Closing Stock 1600

Gross Profit at normal 9500

Less: Variable Marketing and

Administration

500

Gross Profit at actual 9000

Less: Distribution and Administrative

Cost

1200

Net Profit/Loss 7800

Reconciliation Statement: The reconciliation statement is prepared so that the balances of both

the statements can be matched. The differences occur due to the closing stock. In the below

analysis the closing inventory is deducted so as to calculate the profits of the marginal costing

(Nawaz, 2013).

Reconciliation Statement

Particulars Amoun

t (£)

Profit from Absorption Cost 7800

Less: Closing Inventory of fixed

assets

300

Profit of Marginal cost 7500

14

Particulars Amoun

t (£)

Amoun

t (£)

Sales Revenue 17500

Cost of Sales:

Opening Stock 0

Add: Production Cost (16*600) 9600

Less: Closing Stock 1600

Gross Profit at normal 9500

Less: Variable Marketing and

Administration

500

Gross Profit at actual 9000

Less: Distribution and Administrative

Cost

1200

Net Profit/Loss 7800

Reconciliation Statement: The reconciliation statement is prepared so that the balances of both

the statements can be matched. The differences occur due to the closing stock. In the below

analysis the closing inventory is deducted so as to calculate the profits of the marginal costing

(Nawaz, 2013).

Reconciliation Statement

Particulars Amoun

t (£)

Profit from Absorption Cost 7800

Less: Closing Inventory of fixed

assets

300

Profit of Marginal cost 7500

14

LO 3

P4) Explain advantages and disadvantages of different types of planning tools used in the

budgetary control.

Budgets are used in organizations so that the particular target can be set and all the employees of

the organization can work towards the attainment of those goals. These goals in future will help

in earning the profits for Zylla Company (Hartman, 2017). The budgetary control helps in

coordinating the activities of various departments with this the wastage can be eliminated so as

to maximize the profits. With this, the departments can effectively and economically coordinate

the activities.

Image: Merits Limitations Chart

Source: By Author, 2018

Pros:

Adaptation: This is one of the main advantages of budgetary control that it provides an

opportunity to make changes according to the change in the business policies so that the growth

of the organization can be maintained (Hartman, 2017). This will also help the Zylla Company’s

managers to take the correct actions before the issues have arrived.

Tracking progress: The budgetary control will provide Zylla Company a clear path to track the

progress of the organization internally (Hartman, 2017). Through the budget, the managers of the

organization can track the activities of the various departments that which department is going

15

Advantages

Adaption

Tracking

Process

Disadvantages

Reliable on

Numeric

data

Cost

P4) Explain advantages and disadvantages of different types of planning tools used in the

budgetary control.

Budgets are used in organizations so that the particular target can be set and all the employees of

the organization can work towards the attainment of those goals. These goals in future will help

in earning the profits for Zylla Company (Hartman, 2017). The budgetary control helps in

coordinating the activities of various departments with this the wastage can be eliminated so as

to maximize the profits. With this, the departments can effectively and economically coordinate

the activities.

Image: Merits Limitations Chart

Source: By Author, 2018

Pros:

Adaptation: This is one of the main advantages of budgetary control that it provides an

opportunity to make changes according to the change in the business policies so that the growth

of the organization can be maintained (Hartman, 2017). This will also help the Zylla Company’s

managers to take the correct actions before the issues have arrived.

Tracking progress: The budgetary control will provide Zylla Company a clear path to track the

progress of the organization internally (Hartman, 2017). Through the budget, the managers of the

organization can track the activities of the various departments that which department is going

15

Advantages

Adaption

Tracking

Process

Disadvantages

Reliable on

Numeric

data

Cost

beyond the budgetary limits. This evaluation will help in taking the correct decisions in the

future to maintain effectiveness.

Cons:

Reliable on Numeric Data: The budgetary control is mainly dependent upon the numeric data

which is one of the main disadvantages. If the numeric data has been taken wrong then whole

analysis about the future will get impacted (Hartman, 2017). The decisions can prove positive in

short run but in the long run, decisions may prove to be wrong.

Cost: This is another disadvantage of the budgetary control as all the departments directly rely

upon the judgments done by the top level management (Hartman, 2017). The new financial

reports are prepared by managers of the Zylla Company so these cost rises as new employees are

hired for assisting the accounts departments (Money Matters, 2018).

Uncertainty about Future: The budgets are always prepared for the future but the future is

uncertain. The conditions or the business policies may change in future which in turn will impact

the budget prepared by the Zylla Company. With uncertainty, the budgetary control systems

cannot be utilized (Hartman, 2017).

16

future to maintain effectiveness.

Cons:

Reliable on Numeric Data: The budgetary control is mainly dependent upon the numeric data

which is one of the main disadvantages. If the numeric data has been taken wrong then whole

analysis about the future will get impacted (Hartman, 2017). The decisions can prove positive in

short run but in the long run, decisions may prove to be wrong.

Cost: This is another disadvantage of the budgetary control as all the departments directly rely

upon the judgments done by the top level management (Hartman, 2017). The new financial

reports are prepared by managers of the Zylla Company so these cost rises as new employees are

hired for assisting the accounts departments (Money Matters, 2018).

Uncertainty about Future: The budgets are always prepared for the future but the future is

uncertain. The conditions or the business policies may change in future which in turn will impact

the budget prepared by the Zylla Company. With uncertainty, the budgetary control systems

cannot be utilized (Hartman, 2017).

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

M3) Analyze the use of different planning tools and their application for preparing and

forecasting budget.

The planning tools will help the Zylla Company in preparing and forecasting Budget (Gupta,

2013). The organization used various types of the planning tools so that the forecasting can be

accurately done and the effectiveness can be maintained (Kolios and Read, 2013).

PEST Analysis:

Image: PEST Analysis

Source: Silva, 2016

The PEST analysis is useful for the Zylla Company as it examines the macro-environmental

factors that may impact the company in the future (Silva, 2016). This analysis is much same as

that of the SWOT analysis as it focuses on the four main factors which include the political,

economic, socio-culture as well as the technology (Silva, 2016).

SWOT Analysis:

It is the management planning tool which helps in identifying the strengths and weaknesses of

the organization with that it also identifies the opportunities as well as the threats (Richard

Lavron, 2016). As the PEST analysis considers the macro factors during the evaluation the

17

forecasting budget.

The planning tools will help the Zylla Company in preparing and forecasting Budget (Gupta,

2013). The organization used various types of the planning tools so that the forecasting can be

accurately done and the effectiveness can be maintained (Kolios and Read, 2013).

PEST Analysis:

Image: PEST Analysis

Source: Silva, 2016

The PEST analysis is useful for the Zylla Company as it examines the macro-environmental

factors that may impact the company in the future (Silva, 2016). This analysis is much same as

that of the SWOT analysis as it focuses on the four main factors which include the political,

economic, socio-culture as well as the technology (Silva, 2016).

SWOT Analysis:

It is the management planning tool which helps in identifying the strengths and weaknesses of

the organization with that it also identifies the opportunities as well as the threats (Richard

Lavron, 2016). As the PEST analysis considers the macro factors during the evaluation the

17

SWOT analysis considers the microenvironmental factors as it will identify the internal

capabilities of Zylla Company (Gregory, 2018).

Balance Score Card:

It is also one of the management tools which will help Zylla Company in measuring the

performance by continuously monitoring the business activities (Hashemi, 2017). It basically

focuses on the implementation of the operational activities (Balance Scorecard Institution, 2017).

The main characteristic of the balance scorecard is that it uses both financial as well as the

nonfinancial data while evaluation (Balance Scorecard Institution, 2017).

Porter’s Five Forces:

This model is also known as the competitive forces model. The main aim of this model is to

determine the potential of the company to earn profits in the market (Hashemi, 2017). Zylla

Company will have considered five factors during planning which when combined will help the

organization in attaining the profits (Balance Scorecard Institution, 2017).

18

capabilities of Zylla Company (Gregory, 2018).

Balance Score Card:

It is also one of the management tools which will help Zylla Company in measuring the

performance by continuously monitoring the business activities (Hashemi, 2017). It basically

focuses on the implementation of the operational activities (Balance Scorecard Institution, 2017).

The main characteristic of the balance scorecard is that it uses both financial as well as the

nonfinancial data while evaluation (Balance Scorecard Institution, 2017).

Porter’s Five Forces:

This model is also known as the competitive forces model. The main aim of this model is to

determine the potential of the company to earn profits in the market (Hashemi, 2017). Zylla

Company will have considered five factors during planning which when combined will help the

organization in attaining the profits (Balance Scorecard Institution, 2017).

18

LO 4

P5) Compare how organizations are adapting management accounting systems to respond

to financial problems

As management accounting is the process of analyzing and evaluating the financial statements of

the organizations so this evaluation will help in solving the financial problems of the Zylla

Company (Accounting Tools, 2018). Here the solution to the financial problems has been

depicted by considering the four factors those are Benchmarks, KPI’s, budgetary targets to

identify variances and financial governance.

Benchmarks: The benchmarks helps in comparing two things these are the level of performance

of produced goods and services and the best level of the performance in the market having the

same process. The setting up of the benchmarks assures that the benchmarks are set at that level

that it can easily be comparable (Richard Lavron, 2016). As the variances help in identifying the

internal performance of the organization, the benchmarks help in assessing the external

capability of Zylla Company against a competitor (Accounting Tools, 2018).

Key Performance Indicator: Key performance indicators are those indicators which check

whether the organizational activities are running according to the predetermined plan or not. The

KPI’s are of two types: Financial as well as Non-Financial KPI. The financial KPI’s measures

the cash flows as well as the value of the assets (Richard Lavron, 2016). It identifies the

profitability against the benchmarks such as budgeted sales, profits, and cost. Non-Financial

KPI’s measures flexibility and innovation ability of the business activities. It contributes to

factors such as a change in cost structures and environment. These KPI’s, in turn, will solve the

financial problems (Richard Lavron, 2016).

Budgetary target to identify variances: Once the master budget has been approved by the top

level managers of the organization then the reports are evaluated against those targets to

calculate the variances. These reports are evaluated on the monthly, quarterly or yearly basis so

as evaluate the performances (Accounting Tools, 2018). The budgets are allocated to all the

departments and now it’s the responsibility of employees of Zylla Company to meet those targets

19

P5) Compare how organizations are adapting management accounting systems to respond

to financial problems

As management accounting is the process of analyzing and evaluating the financial statements of

the organizations so this evaluation will help in solving the financial problems of the Zylla

Company (Accounting Tools, 2018). Here the solution to the financial problems has been

depicted by considering the four factors those are Benchmarks, KPI’s, budgetary targets to

identify variances and financial governance.

Benchmarks: The benchmarks helps in comparing two things these are the level of performance

of produced goods and services and the best level of the performance in the market having the

same process. The setting up of the benchmarks assures that the benchmarks are set at that level

that it can easily be comparable (Richard Lavron, 2016). As the variances help in identifying the

internal performance of the organization, the benchmarks help in assessing the external

capability of Zylla Company against a competitor (Accounting Tools, 2018).

Key Performance Indicator: Key performance indicators are those indicators which check

whether the organizational activities are running according to the predetermined plan or not. The

KPI’s are of two types: Financial as well as Non-Financial KPI. The financial KPI’s measures

the cash flows as well as the value of the assets (Richard Lavron, 2016). It identifies the

profitability against the benchmarks such as budgeted sales, profits, and cost. Non-Financial

KPI’s measures flexibility and innovation ability of the business activities. It contributes to

factors such as a change in cost structures and environment. These KPI’s, in turn, will solve the

financial problems (Richard Lavron, 2016).

Budgetary target to identify variances: Once the master budget has been approved by the top

level managers of the organization then the reports are evaluated against those targets to

calculate the variances. These reports are evaluated on the monthly, quarterly or yearly basis so

as evaluate the performances (Accounting Tools, 2018). The budgets are allocated to all the

departments and now it’s the responsibility of employees of Zylla Company to meet those targets

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effectively which will help in solving the financial problems so as to attain profits (Accounting

Tools, 2018).

Financial Governance: The financial problems of the Zylla Company can also be solved with

the use of financial governance. The ways through which the financial governance will solve

financial problem includes the internal as well as the external auditing of the financial statement

and through control over the internal systems (Accounting Tools, 2018). The reports will be

prepared by the committees so that the strategic planning can be done. Some of the reports are

variance analysis reports, budget reports as well as the investment and capital reports.

20

Tools, 2018).

Financial Governance: The financial problems of the Zylla Company can also be solved with

the use of financial governance. The ways through which the financial governance will solve

financial problem includes the internal as well as the external auditing of the financial statement

and through control over the internal systems (Accounting Tools, 2018). The reports will be

prepared by the committees so that the strategic planning can be done. Some of the reports are

variance analysis reports, budget reports as well as the investment and capital reports.

20

M4) Analyze how in responding to financial problems, management accounting can lead

the organization to sustainable success

The ways through which the management accounting can lead Zylla Company to sustainable

success by solving the financial problems are:

While doing the strategic planning and making decisions the managers of the

organization may consider the plans and policies which lead the organization to the attain

sustainability (White, 2015).

The management accounting helps in preparing the financial reports so these reports

should also show the impact of the sustainability so that the actual performance can be

evaluated.

Through the inventory management systems, the inventory of the Zylla Company can be

properly tracked as the proper database will be maintained which in turn will enhance the

productivity by solving the problem of excess inventory which in turn will help in

attaining the sustainable success (White, 2015).

The integration of the sustainability issues in the reporting strategies will allow reporting

of both financial as well as the nonfinancial information so that the profitability can be

attained (White, 2015).

With the integration of sustainable information, the decisions related to the marginal and

the absorption costing will enhance as the pricing decisions will be taken more

accurately.

21

the organization to sustainable success

The ways through which the management accounting can lead Zylla Company to sustainable

success by solving the financial problems are:

While doing the strategic planning and making decisions the managers of the

organization may consider the plans and policies which lead the organization to the attain

sustainability (White, 2015).

The management accounting helps in preparing the financial reports so these reports

should also show the impact of the sustainability so that the actual performance can be

evaluated.

Through the inventory management systems, the inventory of the Zylla Company can be

properly tracked as the proper database will be maintained which in turn will enhance the

productivity by solving the problem of excess inventory which in turn will help in

attaining the sustainable success (White, 2015).

The integration of the sustainability issues in the reporting strategies will allow reporting

of both financial as well as the nonfinancial information so that the profitability can be

attained (White, 2015).

With the integration of sustainable information, the decisions related to the marginal and

the absorption costing will enhance as the pricing decisions will be taken more

accurately.

21

D3) Critically evaluate how planning tools for accounting respond appropriately to solving

financial problems to lead the organization to sustainable success.

Through the planning tools, the financial problems can be identified and solved. This solution of

the financial problems will lead the organization to the sustainable success. The information

which has been received from these planning tools helps in taking the strategic financial

decisions which in turn will solve the financial problems of the Zylla Company (White, 2015).

The interpretation of financial data will ensure the growth of the enterprise. The solution of the

financial problem will also help in taking the decisions related to the investment opportunities.

The planning and controlling of the management accounting in Zylla Company ensure that all

the operations are executed according to the predetermined plans. The managers of the

organizations should implement the information which is related to the budgets so that the

process of the budgeting can be evaluated (White, 2015). This will ensure that the resources in

the organization are allocated according to the needs of the departments so that the wastage can

be reduced and the success can be achieved.

The well-managed strategies of the Zylla Company will help in managing the databases

accurately so that the productivity will increase which in turn will enhance the sustainability of

the organization. The use of the PEST and SWOT in the decision-making process will help the

Zylla Company to attain the financial success (White, 2015). The organizational strategies, as

well as the techniques, will focus on the competitive advantage so that the cost can be controlled

and the revenue, as well as the profit, can be increased. The budget helps in setting the target

with which the financial position can be determined and the evaluation can be done by

calculating the variances. The improvements are done according to the variances through which

the sustainable success will be achieved (White, 2015).

22

financial problems to lead the organization to sustainable success.

Through the planning tools, the financial problems can be identified and solved. This solution of

the financial problems will lead the organization to the sustainable success. The information

which has been received from these planning tools helps in taking the strategic financial

decisions which in turn will solve the financial problems of the Zylla Company (White, 2015).

The interpretation of financial data will ensure the growth of the enterprise. The solution of the

financial problem will also help in taking the decisions related to the investment opportunities.

The planning and controlling of the management accounting in Zylla Company ensure that all

the operations are executed according to the predetermined plans. The managers of the

organizations should implement the information which is related to the budgets so that the

process of the budgeting can be evaluated (White, 2015). This will ensure that the resources in

the organization are allocated according to the needs of the departments so that the wastage can

be reduced and the success can be achieved.

The well-managed strategies of the Zylla Company will help in managing the databases

accurately so that the productivity will increase which in turn will enhance the sustainability of

the organization. The use of the PEST and SWOT in the decision-making process will help the

Zylla Company to attain the financial success (White, 2015). The organizational strategies, as

well as the techniques, will focus on the competitive advantage so that the cost can be controlled

and the revenue, as well as the profit, can be increased. The budget helps in setting the target

with which the financial position can be determined and the evaluation can be done by

calculating the variances. The improvements are done according to the variances through which

the sustainable success will be achieved (White, 2015).

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conclusion

It can be concluded that the management accounting systems are important for the organizations

so that the right decisions can be taken which leads the organization to achieve the sustainable

success. Through two costing techniques, the analysis of the cost has been done so that the

proper track on the cost can do so as to reduce the wastage. The Zylla Company needs to apply

all the management accounting systems as well as the reporting so that the profitability and the

growth can be achieved. For improving the decision-making process and to produce the accurate

results the managers of the Zylla Company has to implement the sustainability issues in their

reports. The budgets are prepared by the organization so that the long-term sustainability can be

achieved and the performance can be evaluated. The financial reports prepared by the Zylla

Company should produce the accurate and reliable data as it impacts the whole process of the

organization.

23

It can be concluded that the management accounting systems are important for the organizations

so that the right decisions can be taken which leads the organization to achieve the sustainable

success. Through two costing techniques, the analysis of the cost has been done so that the

proper track on the cost can do so as to reduce the wastage. The Zylla Company needs to apply

all the management accounting systems as well as the reporting so that the profitability and the

growth can be achieved. For improving the decision-making process and to produce the accurate

results the managers of the Zylla Company has to implement the sustainability issues in their

reports. The budgets are prepared by the organization so that the long-term sustainability can be

achieved and the performance can be evaluated. The financial reports prepared by the Zylla

Company should produce the accurate and reliable data as it impacts the whole process of the

organization.

23

References

Accounting Tools, 2018. The Job Costing System. [Online]. Accounting Tools. Available

at: https://www.accountingtools.com/articles/what-is-a-job-costing-system.html.

[Accessed On 14 April 2018]

Balance Scorecard Institution, 2017. Balanced Scorecard Basics. [Online]. Balance

Scorecard Institution. Available at:

http://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard.

[Accessed On 14 April 2018] Financial Accounting.org, 2015. Absorption Costing. [Online]. Financial

Accounting.org. Available at: http://www.financialaccountancy.org/absorption-costing-

approach-or-total-costing/absorption-costing/. [Accessed On 14 April 2018]

Gregory, A., 2018. How to Conduct a SWOT Analysis for Your Small Business.

[Online]. The Balance. Available at: https://www.thebalance.com/swot-analysis-for-

small-business-2951706. [Accessed On 14 April 2018]

Gupta, A., 2013. Environmental and pest analysis: An approach to the external business

environment. Merit Research Journal of Art, Social Science, and Humanities, 1(2),

pp.13-17.

Hamlett, K., 2018. Types of Inventory Management Systems. [Online]. Chron. Available

at: http://smallbusiness.chron.com/types-inventory-management-systems-2195.html.

[Accessed On 14 April 2018]

Hartman, D., 2017. Advantages & Disadvantages of Budgetary Control. [Online].

Bizfluent. Available at: https://bizfluent.com/info-8338790-advantages-disadvantages-

budgetary-control.html. [Accessed On 14 April 2018]

Hashemi, S.M., Samani, F.S. and Shahbazi, V., 2017. Strengths, Weaknesses,

Opportunities, and Threats (SWOT) Analysis and Strategic Planning for Iranian

24

Accounting Tools, 2018. The Job Costing System. [Online]. Accounting Tools. Available

at: https://www.accountingtools.com/articles/what-is-a-job-costing-system.html.

[Accessed On 14 April 2018]

Balance Scorecard Institution, 2017. Balanced Scorecard Basics. [Online]. Balance

Scorecard Institution. Available at:

http://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard.

[Accessed On 14 April 2018] Financial Accounting.org, 2015. Absorption Costing. [Online]. Financial

Accounting.org. Available at: http://www.financialaccountancy.org/absorption-costing-

approach-or-total-costing/absorption-costing/. [Accessed On 14 April 2018]

Gregory, A., 2018. How to Conduct a SWOT Analysis for Your Small Business.

[Online]. The Balance. Available at: https://www.thebalance.com/swot-analysis-for-

small-business-2951706. [Accessed On 14 April 2018]

Gupta, A., 2013. Environmental and pest analysis: An approach to the external business

environment. Merit Research Journal of Art, Social Science, and Humanities, 1(2),

pp.13-17.

Hamlett, K., 2018. Types of Inventory Management Systems. [Online]. Chron. Available

at: http://smallbusiness.chron.com/types-inventory-management-systems-2195.html.

[Accessed On 14 April 2018]

Hartman, D., 2017. Advantages & Disadvantages of Budgetary Control. [Online].

Bizfluent. Available at: https://bizfluent.com/info-8338790-advantages-disadvantages-

budgetary-control.html. [Accessed On 14 April 2018]

Hashemi, S.M., Samani, F.S. and Shahbazi, V., 2017. Strengths, Weaknesses,

Opportunities, and Threats (SWOT) Analysis and Strategic Planning for Iranian

24

Language Institutions Development. Journal of Applied Linguistics and Language

Research, 4(2), pp.139-149.

Kolios, A. and Read, G., 2013. A political, economic, social, technology, legal and

environmental (PESTLE) approach for risk identification of the tidal industry in the

United Kingdom. Energies, 6(10), pp.5023-5045.

Lister, J., 2018. What Kind of Businesses Can Use Job Costing. [Online]. Chron.

Available at: http://smallbusiness.chron.com/kind-businesses-can-use-job-costing-

38870.html. [Accessed On 14 April 2018]

Money Matters, 2018. Disadvantages or Limitations of Budgetary Control. [Online].

Money Matters. Available at: https://accountlearning.com/disadvantages-or-limitations-

of-budgetary-control/. [Accessed On 14 April 2018]

Nawaz, M., 2013. An insight into the two costing techniques: Absorption Costing and

Marginal Costing. Board research in accounting, Negotiation, and distribution, Vol.4,

Issue 1.

Richard Lavron, 2016. 8 tools and techniques to apply to strategic analysis and planning.

[Online]. Richard Lavron. Available at: http://braveworld.ca/8-tools-techniques-to-apply-

to-strategic-analysis-planning/. [Accessed On 14 April 2018] Sarokolaei, M.A., Ebrati, M., Khanghah, V.T. and Ebrati, M., 2012. A comparative study

of activity-based costing system and the traditional system: A case study of Refah Bank.

African Journal of Business Management, 6(45), p.11221.

Silva, N., 2016. Why Every Business Needs a PESTLE Analysis. [Online]. Tweak your

Biz. Available at: http://tweakyourbiz.com/marketing/2016/01/25/every-business-needs-

pestle-analysis/. [Accessed On 14 April 2018]

White, S., 2015. How management accountants can lead their organizations towards

sustainable success. [Online]. Financial Management. Available at: https://www.fm-

magazine.com/news/2015/jan/201511533.html. [Accessed On 14 April 2018]

25

Research, 4(2), pp.139-149.

Kolios, A. and Read, G., 2013. A political, economic, social, technology, legal and

environmental (PESTLE) approach for risk identification of the tidal industry in the

United Kingdom. Energies, 6(10), pp.5023-5045.

Lister, J., 2018. What Kind of Businesses Can Use Job Costing. [Online]. Chron.

Available at: http://smallbusiness.chron.com/kind-businesses-can-use-job-costing-

38870.html. [Accessed On 14 April 2018]

Money Matters, 2018. Disadvantages or Limitations of Budgetary Control. [Online].

Money Matters. Available at: https://accountlearning.com/disadvantages-or-limitations-

of-budgetary-control/. [Accessed On 14 April 2018]

Nawaz, M., 2013. An insight into the two costing techniques: Absorption Costing and

Marginal Costing. Board research in accounting, Negotiation, and distribution, Vol.4,

Issue 1.

Richard Lavron, 2016. 8 tools and techniques to apply to strategic analysis and planning.

[Online]. Richard Lavron. Available at: http://braveworld.ca/8-tools-techniques-to-apply-

to-strategic-analysis-planning/. [Accessed On 14 April 2018] Sarokolaei, M.A., Ebrati, M., Khanghah, V.T. and Ebrati, M., 2012. A comparative study

of activity-based costing system and the traditional system: A case study of Refah Bank.

African Journal of Business Management, 6(45), p.11221.

Silva, N., 2016. Why Every Business Needs a PESTLE Analysis. [Online]. Tweak your

Biz. Available at: http://tweakyourbiz.com/marketing/2016/01/25/every-business-needs-

pestle-analysis/. [Accessed On 14 April 2018]

White, S., 2015. How management accountants can lead their organizations towards

sustainable success. [Online]. Financial Management. Available at: https://www.fm-

magazine.com/news/2015/jan/201511533.html. [Accessed On 14 April 2018]

25

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.