Management Accounting Report: Excite Entertainment (2020) Analysis

VerifiedAdded on 2023/01/13

|12

|3089

|59

Report

AI Summary

This report analyzes management accounting principles through the lens of Excite Entertainment Ltd., a company involved in concert and festival promotions. It begins by differentiating between management accounting (MA) and financial accounting, exploring various MA systems like cost accounting, stock management, and job costing, and outlining their benefits. The report then delves into different types of MA reports, including budget reports, accounts receivable aging reports, and job cost reports, emphasizing the importance of accurate information. A key section presents financial reports for January 2020, comparing income statements prepared using absorption costing and marginal costing, highlighting their respective advantages and disadvantages. Finally, the report compares and contrasts three planning tools used in management accounting: production budgets, cash budgets, and master budgets, providing insights into their benefits and drawbacks for effective financial management and decision-making within the context of the company's operations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Section (A)..................................................................................................................................3

Section (B)..................................................................................................................................4

TASK 2............................................................................................................................................6

Financial report for the month of January 2020..........................................................................6

TASK 3............................................................................................................................................7

Compare and contrast three planning tools used in management accounting.............................7

TASK 4............................................................................................................................................9

Ways in which management

accounting is applied to deal with financial problems...............................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Section (A)..................................................................................................................................3

Section (B)..................................................................................................................................4

TASK 2............................................................................................................................................6

Financial report for the month of January 2020..........................................................................6

TASK 3............................................................................................................................................7

Compare and contrast three planning tools used in management accounting.............................7

TASK 4............................................................................................................................................9

Ways in which management

accounting is applied to deal with financial problems...............................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The term management accounting (MA) is a form of accounting which is aligned to

procedure of gathering monetary and non-monetary data from different resources to produce

inner reports (Nimtrakoon and Tayles, 2015). These reports act as a crucial framework to take

important decisions. The aim of project report is to understand about importance of MA for inner

stakeholders of corporations. This report is based on a company that is Excite entertainment

limited company. The company operates its operations in promotion of concerts and festivals.

This company is a client company of “Grant Thornton” that is a leading accountancy firm in UK.

The project report covers detailed information about detailed understanding of management

accounting systems (MAS), MA reporting, planning tools etc.

TASK 1.

Section (A)

(a)Difference between MA and financial accounting:

Basis MA FA

Mandatory MA is not necessary as financial

accounting.

While financial accounting is

essential to be applied in companies

accounting process.

Format In this accounting any specific

format to produce inner reports is

not applied.

On the other hand, under its

financial statements are prepared as

per the accounting standards.

Information In MA, information about financial

and anti-financial aspects is

included.

In this accounting only financial

information is included for further

process.

Time frame In this accounting, there is no any

specific time to prepare internal

reports.

On the other hand, under this

financial statements are prepared at

the end of an accounting period.

(b) Cost accounting system- This accounting system is applied by production department of a

business entity in order to manage expenses of different functions. Its objective is to keep

an effective control over additional and unwanted cost. This is based on two types of

The term management accounting (MA) is a form of accounting which is aligned to

procedure of gathering monetary and non-monetary data from different resources to produce

inner reports (Nimtrakoon and Tayles, 2015). These reports act as a crucial framework to take

important decisions. The aim of project report is to understand about importance of MA for inner

stakeholders of corporations. This report is based on a company that is Excite entertainment

limited company. The company operates its operations in promotion of concerts and festivals.

This company is a client company of “Grant Thornton” that is a leading accountancy firm in UK.

The project report covers detailed information about detailed understanding of management

accounting systems (MAS), MA reporting, planning tools etc.

TASK 1.

Section (A)

(a)Difference between MA and financial accounting:

Basis MA FA

Mandatory MA is not necessary as financial

accounting.

While financial accounting is

essential to be applied in companies

accounting process.

Format In this accounting any specific

format to produce inner reports is

not applied.

On the other hand, under its

financial statements are prepared as

per the accounting standards.

Information In MA, information about financial

and anti-financial aspects is

included.

In this accounting only financial

information is included for further

process.

Time frame In this accounting, there is no any

specific time to prepare internal

reports.

On the other hand, under this

financial statements are prepared at

the end of an accounting period.

(b) Cost accounting system- This accounting system is applied by production department of a

business entity in order to manage expenses of different functions. Its objective is to keep

an effective control over additional and unwanted cost. This is based on two types of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing methods which are direct and indirect costing. The direct costing is defined as

charging cost of product which is variable (Papazov and Mihaylova, 2015). While

indirect costs are those which are not directly linked to a particular cost object. In the

context of above Excite entertainment limited company, this accounting system is applied

to manage overall expenses regards to organising any event.

(c) Stock management system- It is an accounting system which is based on evaluation of

quantity of stored stock by help of different techniques such as LIFO, FIFO etc. The

objective of this accounting system is to keep control over usage of raw material in

production process. In the Excite entertainment limited company, this accounting system

is applied to track usage of instruments in organising an event.

(d) Job costing system- In this accounting system cost of per unit is calculated by assigning

cost of job of each item. This is beneficial for those companies whose product portfolio is

larger. In the Excite entertainment limited company, their managers apply this accounting

system to track cost of organised event as well as cost of each function.

(e) Benefits of accounting systems:

Cost accounting system- It is associated to reducing cost of different activities and

operations. In the above company, this contributes to their finance department in

order to minimising those expenses which are unwanted.

Stock management system- This is linked with managing cost of materials that are

stored in warehouses. In the above company, their manufacturing department

implies this accounting system to better management of stored raw materials.

Job costing system- It contributes in calculating cost of per unit separately. In

Excite entertainment limited company, they apply this accounting system to

manage cost of job as well as finding value of per unit cost.

Section (B)

(a) Different kinds of MA reports.

In business environment, different MA reports have a major role in strengthening the

business operations and determining the weak areas of business and task. These areas are needed

needed to be altered and modified to make maximum profit for company. Some of these are

detailed below:

charging cost of product which is variable (Papazov and Mihaylova, 2015). While

indirect costs are those which are not directly linked to a particular cost object. In the

context of above Excite entertainment limited company, this accounting system is applied

to manage overall expenses regards to organising any event.

(c) Stock management system- It is an accounting system which is based on evaluation of

quantity of stored stock by help of different techniques such as LIFO, FIFO etc. The

objective of this accounting system is to keep control over usage of raw material in

production process. In the Excite entertainment limited company, this accounting system

is applied to track usage of instruments in organising an event.

(d) Job costing system- In this accounting system cost of per unit is calculated by assigning

cost of job of each item. This is beneficial for those companies whose product portfolio is

larger. In the Excite entertainment limited company, their managers apply this accounting

system to track cost of organised event as well as cost of each function.

(e) Benefits of accounting systems:

Cost accounting system- It is associated to reducing cost of different activities and

operations. In the above company, this contributes to their finance department in

order to minimising those expenses which are unwanted.

Stock management system- This is linked with managing cost of materials that are

stored in warehouses. In the above company, their manufacturing department

implies this accounting system to better management of stored raw materials.

Job costing system- It contributes in calculating cost of per unit separately. In

Excite entertainment limited company, they apply this accounting system to

manage cost of job as well as finding value of per unit cost.

Section (B)

(a) Different kinds of MA reports.

In business environment, different MA reports have a major role in strengthening the

business operations and determining the weak areas of business and task. These areas are needed

needed to be altered and modified to make maximum profit for company. Some of these are

detailed below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget report: This report is mainly prepared to examine the overall performance of

business in a specific year (Revellino and Mouritsen, 2015). In excite Ltd, manager can prepare

budget report to ascertain the performance of various department and even regulate cost with the

budgeted figures. The estimated budget for a year is figure out from the past expenses and

appropriate steps are made according to variance analysis.

Accounts receivable ageing report: This is consider to be a crucial report to manage

cash flows in company which offer credit facilities to customer. With the help of this report

manager in respective firm can make intimate customer according to their payment deadline and

with outstanding balance. Company can also make tighter credit policies if debt because of

delay payment.

Job cost report: This report is prepared for evaluating the total cost involved on various

job within an organisation. Manager can easily coordinate with the income prediction for

ascertaining the Job profitability. In Excite Ltd, manager by using this report can find out the

jobs which are not producing favourable report and make steps to improve these jobs to increase

profit margin.

B) Features of collected information

It is really essential that information provided in various ways should be trustworthy, up-

to-date, genuine and up to date in a timely manner as it supports various useful decisions.

Manager should ensure that document does not include any type of error and that these are

compelled in accordance with accounting principles. In Excite entertainment management Ltd

track and periodically use various reports to recognize industry patterns to find out that company

is making income.

C) Critical evaluation of management accounting systems and reports.

In Excite Entertainment Ltd, different method and accurate documents are valuable

because they are equally relevant in achieving the pre-planned performance. Like cost

management system helpful in allocating overall cost related to various business operations and

procedures. Thus, it help in preparing cost report which record each and every cost incurred in

various operation and make certain plan to regulate expenses or not in a year.

business in a specific year (Revellino and Mouritsen, 2015). In excite Ltd, manager can prepare

budget report to ascertain the performance of various department and even regulate cost with the

budgeted figures. The estimated budget for a year is figure out from the past expenses and

appropriate steps are made according to variance analysis.

Accounts receivable ageing report: This is consider to be a crucial report to manage

cash flows in company which offer credit facilities to customer. With the help of this report

manager in respective firm can make intimate customer according to their payment deadline and

with outstanding balance. Company can also make tighter credit policies if debt because of

delay payment.

Job cost report: This report is prepared for evaluating the total cost involved on various

job within an organisation. Manager can easily coordinate with the income prediction for

ascertaining the Job profitability. In Excite Ltd, manager by using this report can find out the

jobs which are not producing favourable report and make steps to improve these jobs to increase

profit margin.

B) Features of collected information

It is really essential that information provided in various ways should be trustworthy, up-

to-date, genuine and up to date in a timely manner as it supports various useful decisions.

Manager should ensure that document does not include any type of error and that these are

compelled in accordance with accounting principles. In Excite entertainment management Ltd

track and periodically use various reports to recognize industry patterns to find out that company

is making income.

C) Critical evaluation of management accounting systems and reports.

In Excite Entertainment Ltd, different method and accurate documents are valuable

because they are equally relevant in achieving the pre-planned performance. Like cost

management system helpful in allocating overall cost related to various business operations and

procedures. Thus, it help in preparing cost report which record each and every cost incurred in

various operation and make certain plan to regulate expenses or not in a year.

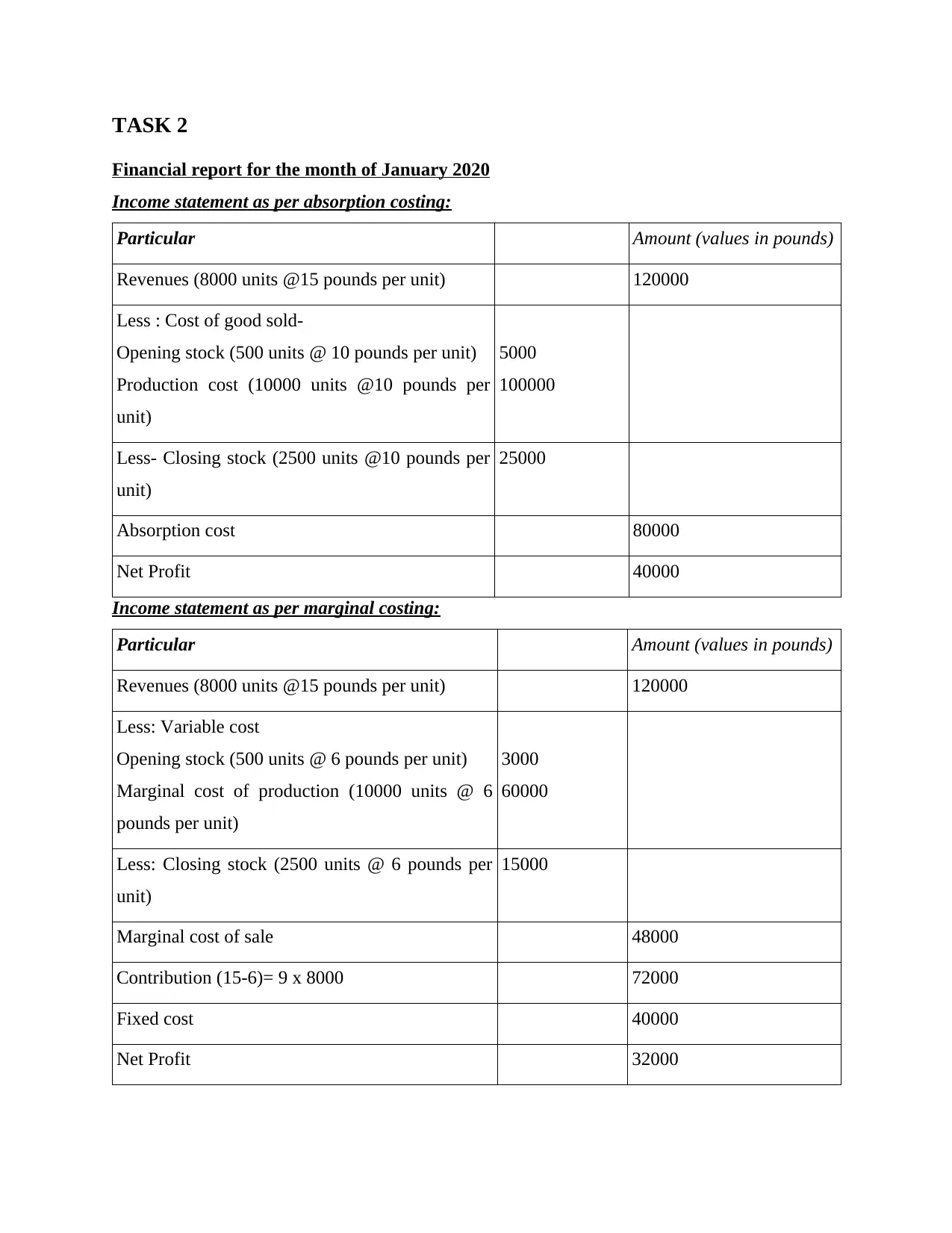

TASK 2

Financial report for the month of January 2020

Income statement as per absorption costing:

Particular Amount (values in pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less : Cost of good sold-

Opening stock (500 units @ 10 pounds per unit)

Production cost (10000 units @10 pounds per

unit)

5000

100000

Less- Closing stock (2500 units @10 pounds per

unit)

25000

Absorption cost 80000

Net Profit 40000

Income statement as per marginal costing:

Particular Amount (values in pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less: Variable cost

Opening stock (500 units @ 6 pounds per unit)

Marginal cost of production (10000 units @ 6

pounds per unit)

3000

60000

Less: Closing stock (2500 units @ 6 pounds per

unit)

15000

Marginal cost of sale 48000

Contribution (15-6)= 9 x 8000 72000

Fixed cost 40000

Net Profit 32000

Financial report for the month of January 2020

Income statement as per absorption costing:

Particular Amount (values in pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less : Cost of good sold-

Opening stock (500 units @ 10 pounds per unit)

Production cost (10000 units @10 pounds per

unit)

5000

100000

Less- Closing stock (2500 units @10 pounds per

unit)

25000

Absorption cost 80000

Net Profit 40000

Income statement as per marginal costing:

Particular Amount (values in pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less: Variable cost

Opening stock (500 units @ 6 pounds per unit)

Marginal cost of production (10000 units @ 6

pounds per unit)

3000

60000

Less: Closing stock (2500 units @ 6 pounds per

unit)

15000

Marginal cost of sale 48000

Contribution (15-6)= 9 x 8000 72000

Fixed cost 40000

Net Profit 32000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

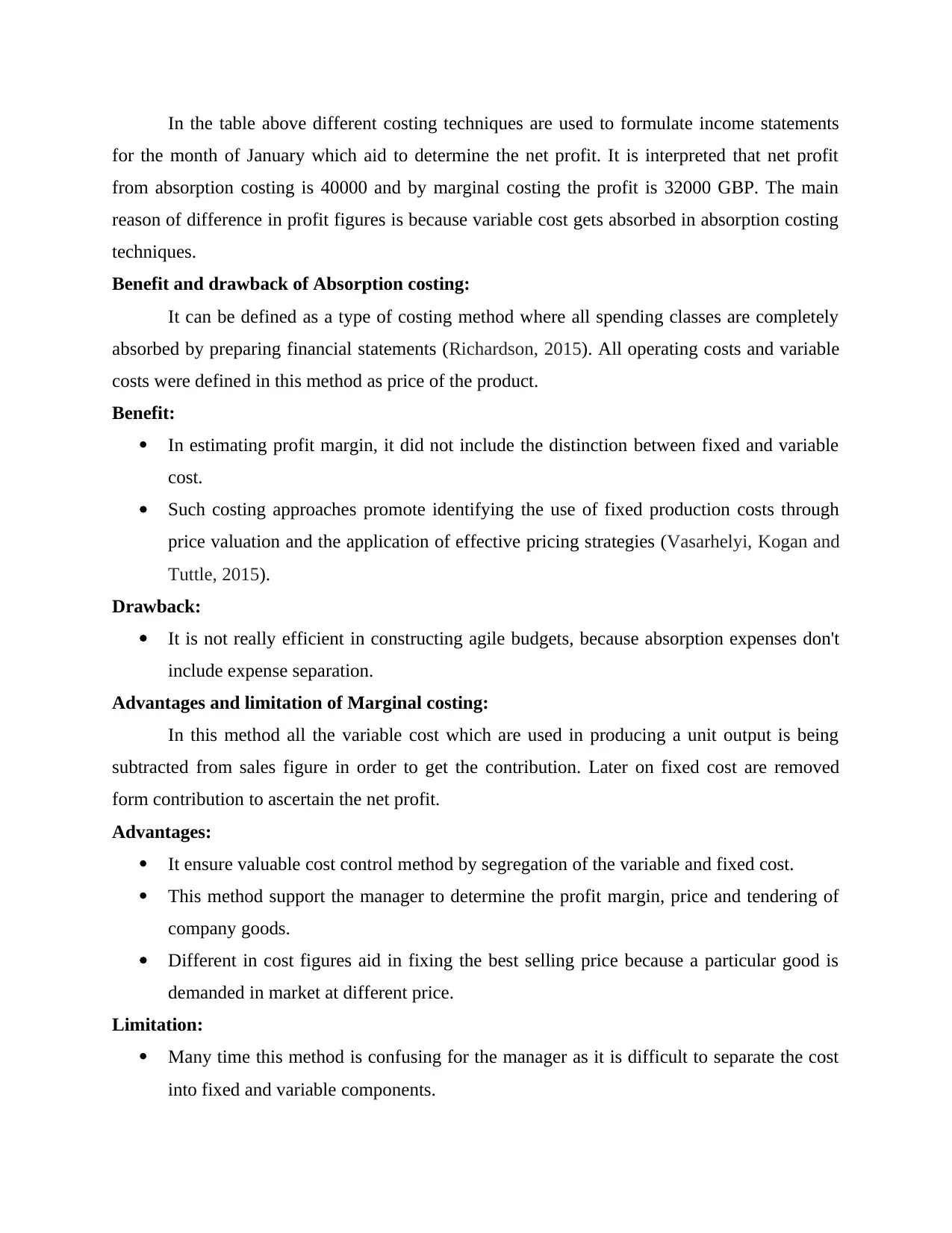

In the table above different costing techniques are used to formulate income statements

for the month of January which aid to determine the net profit. It is interpreted that net profit

from absorption costing is 40000 and by marginal costing the profit is 32000 GBP. The main

reason of difference in profit figures is because variable cost gets absorbed in absorption costing

techniques.

Benefit and drawback of Absorption costing:

It can be defined as a type of costing method where all spending classes are completely

absorbed by preparing financial statements (Richardson, 2015). All operating costs and variable

costs were defined in this method as price of the product.

Benefit:

In estimating profit margin, it did not include the distinction between fixed and variable

cost.

Such costing approaches promote identifying the use of fixed production costs through

price valuation and the application of effective pricing strategies (Vasarhelyi, Kogan and

Tuttle, 2015).

Drawback:

It is not really efficient in constructing agile budgets, because absorption expenses don't

include expense separation.

Advantages and limitation of Marginal costing:

In this method all the variable cost which are used in producing a unit output is being

subtracted from sales figure in order to get the contribution. Later on fixed cost are removed

form contribution to ascertain the net profit.

Advantages:

It ensure valuable cost control method by segregation of the variable and fixed cost.

This method support the manager to determine the profit margin, price and tendering of

company goods.

Different in cost figures aid in fixing the best selling price because a particular good is

demanded in market at different price.

Limitation:

Many time this method is confusing for the manager as it is difficult to separate the cost

into fixed and variable components.

for the month of January which aid to determine the net profit. It is interpreted that net profit

from absorption costing is 40000 and by marginal costing the profit is 32000 GBP. The main

reason of difference in profit figures is because variable cost gets absorbed in absorption costing

techniques.

Benefit and drawback of Absorption costing:

It can be defined as a type of costing method where all spending classes are completely

absorbed by preparing financial statements (Richardson, 2015). All operating costs and variable

costs were defined in this method as price of the product.

Benefit:

In estimating profit margin, it did not include the distinction between fixed and variable

cost.

Such costing approaches promote identifying the use of fixed production costs through

price valuation and the application of effective pricing strategies (Vasarhelyi, Kogan and

Tuttle, 2015).

Drawback:

It is not really efficient in constructing agile budgets, because absorption expenses don't

include expense separation.

Advantages and limitation of Marginal costing:

In this method all the variable cost which are used in producing a unit output is being

subtracted from sales figure in order to get the contribution. Later on fixed cost are removed

form contribution to ascertain the net profit.

Advantages:

It ensure valuable cost control method by segregation of the variable and fixed cost.

This method support the manager to determine the profit margin, price and tendering of

company goods.

Different in cost figures aid in fixing the best selling price because a particular good is

demanded in market at different price.

Limitation:

Many time this method is confusing for the manager as it is difficult to separate the cost

into fixed and variable components.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales price may gets modify with the changes in operation level.

TASK 3

Compare and contrast three planning tools used in management accounting

Budgetary management is said to be focused on strategies which are selected by an

agency to monitor financial performance by planning addition to executing different budgets.

There are various kind of budgets which can be used by excite entertainment limited as a

planning tool. So that they can easily ascertain the outcome with the support of budgetary control

system and these results are compared with estimated figures. Some of these are discussed

underneath:

Production budgets: By using this budget as a planning manager of excite Ltd can make

decision related with optimum manufacture level after interacting with different departments.

This help in attaining the maximum level of profit with favourable cost. Therefore, company

executives must include budgetary controlling in their work since it helps in the preparation of

particular period budgets and in monitoring or recording of costs associated to the operations

carried out in that span. So it is necessary for the manage to prepare these budgets with utmost

care as it have a direct influence on sales and cash budgets.

Benefits: This budget presume an inbuilt place among sales and stock budget and thus

support in make strong polices related with inventory and sales. Most importantly this budget

help in ensuring the physical controlling of stack at different level which tends to increase the

productivity level.

Drawbacks: The main disadvantage of this budget is that it do not clear the macro

economic trends due to which production level gets impacted. It consumer more time and require

skills which might hamper overall performance of company.

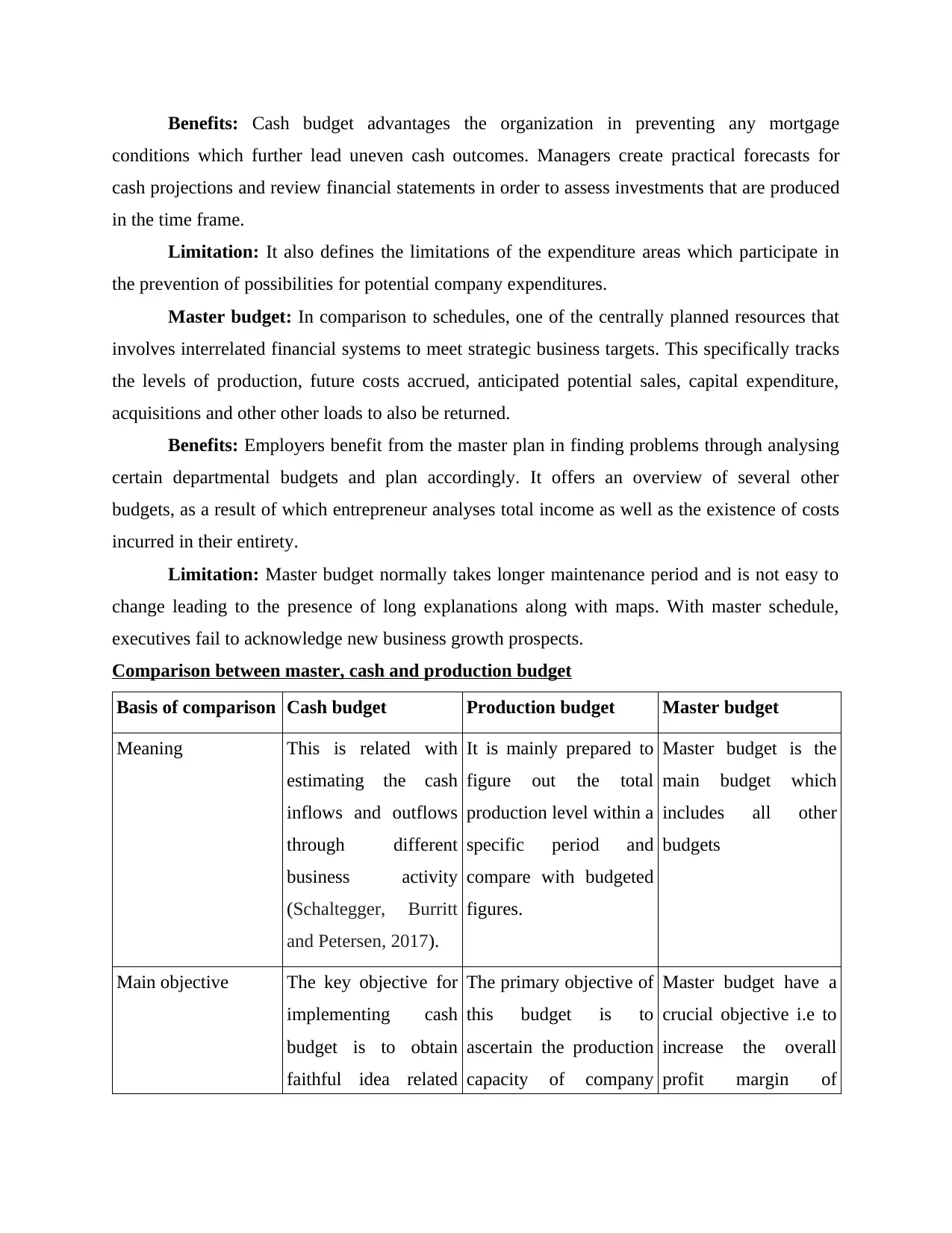

Cash Budget:

These expenditures plan have a crucial part in overall company budget anticipation and

estimating (Benefits of Cash budget, 2020). Changes within cash level due to business operation

are recorded in order to determine the productive activities. With this program, administrators of

Excite Entertainment Ltd receive full cash balance details so further important decisions are

formulated prudently in the sense of generating savings and utilizes.

TASK 3

Compare and contrast three planning tools used in management accounting

Budgetary management is said to be focused on strategies which are selected by an

agency to monitor financial performance by planning addition to executing different budgets.

There are various kind of budgets which can be used by excite entertainment limited as a

planning tool. So that they can easily ascertain the outcome with the support of budgetary control

system and these results are compared with estimated figures. Some of these are discussed

underneath:

Production budgets: By using this budget as a planning manager of excite Ltd can make

decision related with optimum manufacture level after interacting with different departments.

This help in attaining the maximum level of profit with favourable cost. Therefore, company

executives must include budgetary controlling in their work since it helps in the preparation of

particular period budgets and in monitoring or recording of costs associated to the operations

carried out in that span. So it is necessary for the manage to prepare these budgets with utmost

care as it have a direct influence on sales and cash budgets.

Benefits: This budget presume an inbuilt place among sales and stock budget and thus

support in make strong polices related with inventory and sales. Most importantly this budget

help in ensuring the physical controlling of stack at different level which tends to increase the

productivity level.

Drawbacks: The main disadvantage of this budget is that it do not clear the macro

economic trends due to which production level gets impacted. It consumer more time and require

skills which might hamper overall performance of company.

Cash Budget:

These expenditures plan have a crucial part in overall company budget anticipation and

estimating (Benefits of Cash budget, 2020). Changes within cash level due to business operation

are recorded in order to determine the productive activities. With this program, administrators of

Excite Entertainment Ltd receive full cash balance details so further important decisions are

formulated prudently in the sense of generating savings and utilizes.

Benefits: Cash budget advantages the organization in preventing any mortgage

conditions which further lead uneven cash outcomes. Managers create practical forecasts for

cash projections and review financial statements in order to assess investments that are produced

in the time frame.

Limitation: It also defines the limitations of the expenditure areas which participate in

the prevention of possibilities for potential company expenditures.

Master budget: In comparison to schedules, one of the centrally planned resources that

involves interrelated financial systems to meet strategic business targets. This specifically tracks

the levels of production, future costs accrued, anticipated potential sales, capital expenditure,

acquisitions and other other loads to also be returned.

Benefits: Employers benefit from the master plan in finding problems through analysing

certain departmental budgets and plan accordingly. It offers an overview of several other

budgets, as a result of which entrepreneur analyses total income as well as the existence of costs

incurred in their entirety.

Limitation: Master budget normally takes longer maintenance period and is not easy to

change leading to the presence of long explanations along with maps. With master schedule,

executives fail to acknowledge new business growth prospects.

Comparison between master, cash and production budget

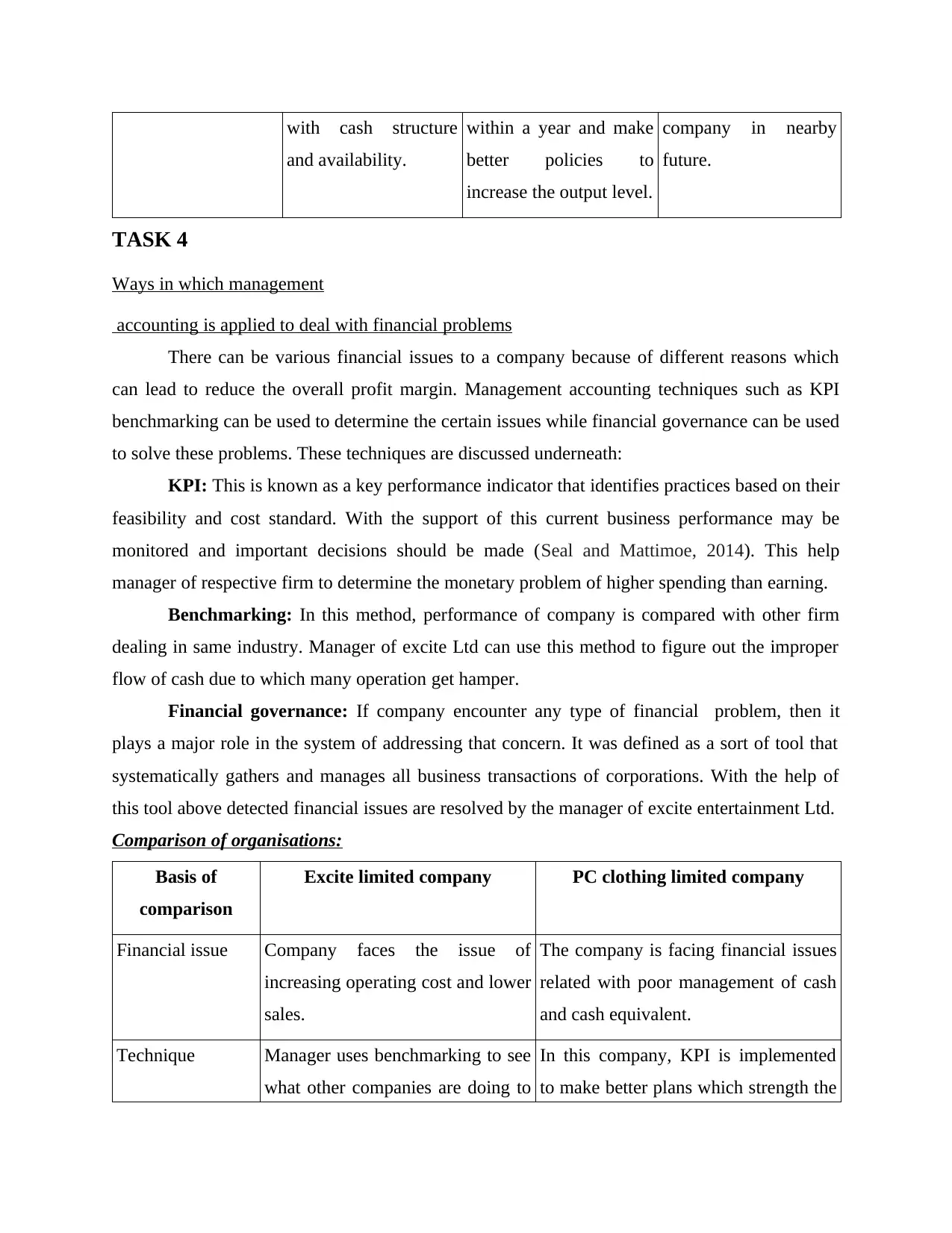

Basis of comparison Cash budget Production budget Master budget

Meaning This is related with

estimating the cash

inflows and outflows

through different

business activity

(Schaltegger, Burritt

and Petersen, 2017).

It is mainly prepared to

figure out the total

production level within a

specific period and

compare with budgeted

figures.

Master budget is the

main budget which

includes all other

budgets

Main objective The key objective for

implementing cash

budget is to obtain

faithful idea related

The primary objective of

this budget is to

ascertain the production

capacity of company

Master budget have a

crucial objective i.e to

increase the overall

profit margin of

conditions which further lead uneven cash outcomes. Managers create practical forecasts for

cash projections and review financial statements in order to assess investments that are produced

in the time frame.

Limitation: It also defines the limitations of the expenditure areas which participate in

the prevention of possibilities for potential company expenditures.

Master budget: In comparison to schedules, one of the centrally planned resources that

involves interrelated financial systems to meet strategic business targets. This specifically tracks

the levels of production, future costs accrued, anticipated potential sales, capital expenditure,

acquisitions and other other loads to also be returned.

Benefits: Employers benefit from the master plan in finding problems through analysing

certain departmental budgets and plan accordingly. It offers an overview of several other

budgets, as a result of which entrepreneur analyses total income as well as the existence of costs

incurred in their entirety.

Limitation: Master budget normally takes longer maintenance period and is not easy to

change leading to the presence of long explanations along with maps. With master schedule,

executives fail to acknowledge new business growth prospects.

Comparison between master, cash and production budget

Basis of comparison Cash budget Production budget Master budget

Meaning This is related with

estimating the cash

inflows and outflows

through different

business activity

(Schaltegger, Burritt

and Petersen, 2017).

It is mainly prepared to

figure out the total

production level within a

specific period and

compare with budgeted

figures.

Master budget is the

main budget which

includes all other

budgets

Main objective The key objective for

implementing cash

budget is to obtain

faithful idea related

The primary objective of

this budget is to

ascertain the production

capacity of company

Master budget have a

crucial objective i.e to

increase the overall

profit margin of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with cash structure

and availability.

within a year and make

better policies to

increase the output level.

company in nearby

future.

TASK 4

Ways in which management

accounting is applied to deal with financial problems

There can be various financial issues to a company because of different reasons which

can lead to reduce the overall profit margin. Management accounting techniques such as KPI

benchmarking can be used to determine the certain issues while financial governance can be used

to solve these problems. These techniques are discussed underneath:

KPI: This is known as a key performance indicator that identifies practices based on their

feasibility and cost standard. With the support of this current business performance may be

monitored and important decisions should be made (Seal and Mattimoe, 2014). This help

manager of respective firm to determine the monetary problem of higher spending than earning.

Benchmarking: In this method, performance of company is compared with other firm

dealing in same industry. Manager of excite Ltd can use this method to figure out the improper

flow of cash due to which many operation get hamper.

Financial governance: If company encounter any type of financial problem, then it

plays a major role in the system of addressing that concern. It was defined as a sort of tool that

systematically gathers and manages all business transactions of corporations. With the help of

this tool above detected financial issues are resolved by the manager of excite entertainment Ltd.

Comparison of organisations:

Basis of

comparison

Excite limited company PC clothing limited company

Financial issue Company faces the issue of

increasing operating cost and lower

sales.

The company is facing financial issues

related with poor management of cash

and cash equivalent.

Technique Manager uses benchmarking to see

what other companies are doing to

In this company, KPI is implemented

to make better plans which strength the

and availability.

within a year and make

better policies to

increase the output level.

company in nearby

future.

TASK 4

Ways in which management

accounting is applied to deal with financial problems

There can be various financial issues to a company because of different reasons which

can lead to reduce the overall profit margin. Management accounting techniques such as KPI

benchmarking can be used to determine the certain issues while financial governance can be used

to solve these problems. These techniques are discussed underneath:

KPI: This is known as a key performance indicator that identifies practices based on their

feasibility and cost standard. With the support of this current business performance may be

monitored and important decisions should be made (Seal and Mattimoe, 2014). This help

manager of respective firm to determine the monetary problem of higher spending than earning.

Benchmarking: In this method, performance of company is compared with other firm

dealing in same industry. Manager of excite Ltd can use this method to figure out the improper

flow of cash due to which many operation get hamper.

Financial governance: If company encounter any type of financial problem, then it

plays a major role in the system of addressing that concern. It was defined as a sort of tool that

systematically gathers and manages all business transactions of corporations. With the help of

this tool above detected financial issues are resolved by the manager of excite entertainment Ltd.

Comparison of organisations:

Basis of

comparison

Excite limited company PC clothing limited company

Financial issue Company faces the issue of

increasing operating cost and lower

sales.

The company is facing financial issues

related with poor management of cash

and cash equivalent.

Technique Manager uses benchmarking to see

what other companies are doing to

In this company, KPI is implemented

to make better plans which strength the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

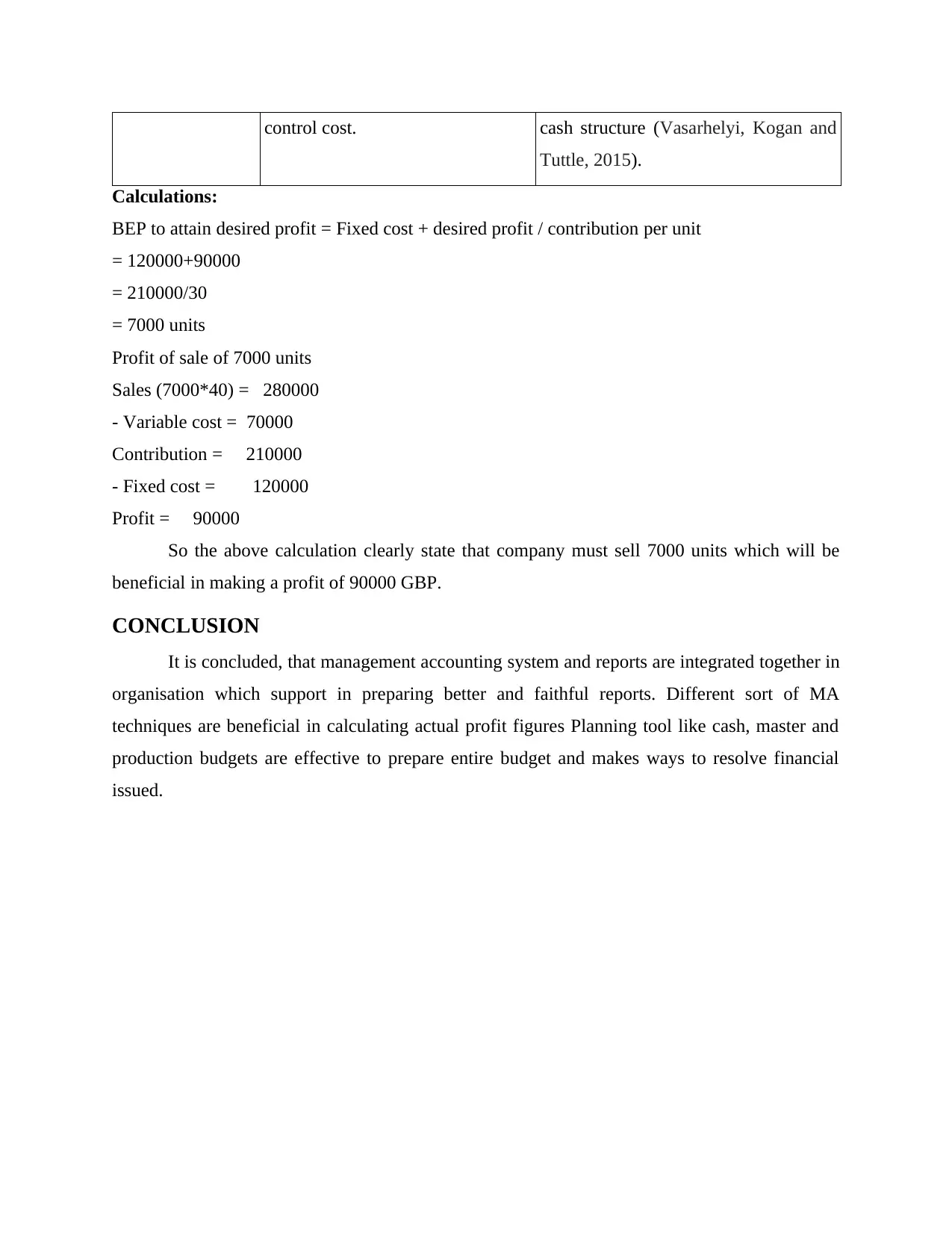

control cost. cash structure (Vasarhelyi, Kogan and

Tuttle, 2015).

Calculations:

BEP to attain desired profit = Fixed cost + desired profit / contribution per unit

= 120000+90000

= 210000/30

= 7000 units

Profit of sale of 7000 units

Sales (7000*40) = 280000

- Variable cost = 70000

Contribution = 210000

- Fixed cost = 120000

Profit = 90000

So the above calculation clearly state that company must sell 7000 units which will be

beneficial in making a profit of 90000 GBP.

CONCLUSION

It is concluded, that management accounting system and reports are integrated together in

organisation which support in preparing better and faithful reports. Different sort of MA

techniques are beneficial in calculating actual profit figures Planning tool like cash, master and

production budgets are effective to prepare entire budget and makes ways to resolve financial

issued.

Tuttle, 2015).

Calculations:

BEP to attain desired profit = Fixed cost + desired profit / contribution per unit

= 120000+90000

= 210000/30

= 7000 units

Profit of sale of 7000 units

Sales (7000*40) = 280000

- Variable cost = 70000

Contribution = 210000

- Fixed cost = 120000

Profit = 90000

So the above calculation clearly state that company must sell 7000 units which will be

beneficial in making a profit of 90000 GBP.

CONCLUSION

It is concluded, that management accounting system and reports are integrated together in

organisation which support in preparing better and faithful reports. Different sort of MA

techniques are beneficial in calculating actual profit figures Planning tool like cash, master and

production budgets are effective to prepare entire budget and makes ways to resolve financial

issued.

REFERENCES

Books and Journals:

Nimtrakoon, S. and Tayles, M., 2015. Explaining management accounting practices and strategy

in Thailand: A selection approach using cluster analysis. Journal of Accounting in

Emerging Economies. 5(3). pp.269-298.

Papazov, E. and Mihaylova, L., 2015. Organization of Management Accounting Information in

the Context of Corporate Strategy. Procedia-Social and Behavioral Sciences. 213.

pp.309-313.

Revellino, S. and Mouritsen, J., 2015. Accounting as an engine: The performativity of

calculative practices and the dynamics of innovation. Management Accounting

Research. 28. pp.31-49.

Richardson, A. J., 2015. Quantitative research and the critical accounting project. Critical

Perspectives on Accounting. 32. pp.67-77.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Seal, W. and Mattimoe, R., 2014. Controlling strategy through dialectical

management. Management Accounting Research. 25(3). pp.230-243.

Vasarhelyi, M. A., Kogan, A. and Tuttle, B. M., 2015. Big Data in accounting: An

overview. Accounting Horizons. 29(2). pp.381-396.

Online

Benefits of Cash budget. 2020. [Online]. Available through:

<https://www.sapling.com/7757509/benefits-cash-budget>

Books and Journals:

Nimtrakoon, S. and Tayles, M., 2015. Explaining management accounting practices and strategy

in Thailand: A selection approach using cluster analysis. Journal of Accounting in

Emerging Economies. 5(3). pp.269-298.

Papazov, E. and Mihaylova, L., 2015. Organization of Management Accounting Information in

the Context of Corporate Strategy. Procedia-Social and Behavioral Sciences. 213.

pp.309-313.

Revellino, S. and Mouritsen, J., 2015. Accounting as an engine: The performativity of

calculative practices and the dynamics of innovation. Management Accounting

Research. 28. pp.31-49.

Richardson, A. J., 2015. Quantitative research and the critical accounting project. Critical

Perspectives on Accounting. 32. pp.67-77.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Seal, W. and Mattimoe, R., 2014. Controlling strategy through dialectical

management. Management Accounting Research. 25(3). pp.230-243.

Vasarhelyi, M. A., Kogan, A. and Tuttle, B. M., 2015. Big Data in accounting: An

overview. Accounting Horizons. 29(2). pp.381-396.

Online

Benefits of Cash budget. 2020. [Online]. Available through:

<https://www.sapling.com/7757509/benefits-cash-budget>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.