Analyzing Management Accounting Practices at Snooker England Ltd

VerifiedAdded on 2023/06/15

|13

|3603

|186

Report

AI Summary

This report provides an analysis of management accounting (MA) activities within Snooker England Limited. It evaluates the integration of MA systems, such as cost accounting, inventory management, and job costing, and their essential requirements. Various MA reporting methods, including budget reports, accounts receivable aging, job cost reports, and inventory & manufacturing reports, are discussed. The report includes the preparation of income statements using marginal and absorption costing, along with a reconciliation statement and cash flow statement. It also evaluates different planning tools for budgetary control, such as budgets, marginal costing, and pricing strategies, highlighting their advantages and disadvantages. The report further compares management accounting systems used by different organizations to respond to financial problems, such as just-in-time inventory management. The document emphasizes the importance of MA systems in ensuring sustainable success for organizations.

MANAGEMENT

ACCOUNTING

ACTIVITIES

ACCOUNTING

ACTIVITIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management Accounting and essential requirements of different Management accounting

systems.........................................................................................................................................3

P2 Methods used for Management Accounting reporting...........................................................4

M1 Benefits of MA system and their application in business context........................................5

D1 Integration of Management accounting system and reporting within organizational

processes......................................................................................................................................5

LO 2.................................................................................................................................................6

P3, M2, D2 Preparation of income statement through marginal and absorption costing............6

LO 3.................................................................................................................................................8

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................8

M3................................................................................................................................................9

LO 4...............................................................................................................................................10

P5 Comparison between different organization's management accounting systems they used to

respond to financial problems....................................................................................................10

M4..............................................................................................................................................11

D3...............................................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management Accounting and essential requirements of different Management accounting

systems.........................................................................................................................................3

P2 Methods used for Management Accounting reporting...........................................................4

M1 Benefits of MA system and their application in business context........................................5

D1 Integration of Management accounting system and reporting within organizational

processes......................................................................................................................................5

LO 2.................................................................................................................................................6

P3, M2, D2 Preparation of income statement through marginal and absorption costing............6

LO 3.................................................................................................................................................8

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................8

M3................................................................................................................................................9

LO 4...............................................................................................................................................10

P5 Comparison between different organization's management accounting systems they used to

respond to financial problems....................................................................................................10

M4..............................................................................................................................................11

D3...............................................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a modern tool for management which involves presentation of

accounting information in a manner which results in assisting managerial decision-making, so

that policies and strategies can be created for the day to day business operations (Ameen, Ahmed

and Abd Hafez, 2018). With reference to Snooker England Limited, different types of MA

systems will be discussed in this report. Also, various MA reporting methods, pros and cons of

planning tools for budgetary control and MA to respond to business's financial problems will be

discussed in this report. At last, it would be highlighted that how with the help of introducing

MA, organisations can ensure their sustainable success.

MAIN BODY

1. Evaluation of integration of Management Accounting systems and management accounting

reporting within organisational processes

MA is a profession which includes assisting management while making decisions,

devising plans and policies, applying performance management systems, preparing financial

reports and establishing control over the internal processes of the organization by formulating

and implementing strategies. Various financial reports such as inventory reports, budget reports,

etc. are used for facilitating decision-making to effectively and efficiently undertake operational

activities (Saukkonen, Laine and Suomala, 2018).

There are various MA systems applied within Snooker England having different essential

requirements, such as the following:

Cost accounting system: It is framework used by Snooker England to undertake estimation of its

product's costs to facilitate cost control, profitability analysis and inventory valuation (Ostaev

and et.al., 2020). In this way, records can generated pertaining to cost of manufacturing concern

by grouping costs into different categories such as direct, indirect, fixed and variable costs. This

system is essential for the company to determine per unit cost of its product and setting its final

price.

Inventory management system: With this system, Snooker England can value its inventory by

applying different techniques such as LIFO, AVCO and FIFO. Also, tracking of inventory of

materials and final products can be possible throughout the supply chain. It is essential for setting

selling price, determining further requirement of products and materials and any loss associated

with it (Endenich and Trapp, 2020).

Management accounting is a modern tool for management which involves presentation of

accounting information in a manner which results in assisting managerial decision-making, so

that policies and strategies can be created for the day to day business operations (Ameen, Ahmed

and Abd Hafez, 2018). With reference to Snooker England Limited, different types of MA

systems will be discussed in this report. Also, various MA reporting methods, pros and cons of

planning tools for budgetary control and MA to respond to business's financial problems will be

discussed in this report. At last, it would be highlighted that how with the help of introducing

MA, organisations can ensure their sustainable success.

MAIN BODY

1. Evaluation of integration of Management Accounting systems and management accounting

reporting within organisational processes

MA is a profession which includes assisting management while making decisions,

devising plans and policies, applying performance management systems, preparing financial

reports and establishing control over the internal processes of the organization by formulating

and implementing strategies. Various financial reports such as inventory reports, budget reports,

etc. are used for facilitating decision-making to effectively and efficiently undertake operational

activities (Saukkonen, Laine and Suomala, 2018).

There are various MA systems applied within Snooker England having different essential

requirements, such as the following:

Cost accounting system: It is framework used by Snooker England to undertake estimation of its

product's costs to facilitate cost control, profitability analysis and inventory valuation (Ostaev

and et.al., 2020). In this way, records can generated pertaining to cost of manufacturing concern

by grouping costs into different categories such as direct, indirect, fixed and variable costs. This

system is essential for the company to determine per unit cost of its product and setting its final

price.

Inventory management system: With this system, Snooker England can value its inventory by

applying different techniques such as LIFO, AVCO and FIFO. Also, tracking of inventory of

materials and final products can be possible throughout the supply chain. It is essential for setting

selling price, determining further requirement of products and materials and any loss associated

with it (Endenich and Trapp, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system: With the help of this system, Snooker England can accumulate data about

costs associated with particular job (Azudin and Mansor, 2018). It is helpful in determining

whether a particular job is profitable or not. Accordingly, resources can be easily diverted among

low profitable and high profitable jobs.

Management Accounting reporting

MA has become very crucial while managing organizational performance and it is

recommended to Snooker England to utilize different methods of MA, so that managerial tasks

can be accomplished in efficient manner. The various MA reporting methods are as follows:

Budget report: This report helps in establishing budgetary control through which future aspects

of Snooker England can be determined (Pasch, 2019). It depicts spending plan of the company

and accordingly, arrangement for the amount of money can be done in advance to avoid

shortages. Also, steps could be taken while comparing actual performance against what has been

budgeted to ensure that the organization is moving towards its end goals.

Account receivables ageing: This report shows record of unpaid invoices along with indicating

the duration of their being outstanding (Kostyukova and et.al., 2018). This procedure within MA

allows Snooker England to determine those invoices that are open and also keeping those clients

on the top who are considered to be slow paying one. Accounting, effective collection and credit

management can be ensured and policies associated with it can be modified as per the

requirements.

Job cost reports: It is a comprehensive documentation of all the costs associated with specific

jobs concerning the organization through which expenditure plan can be created to ensure its

accomplishment on time without any shortages (Maheshwari, Maheshwari and Maheshwari,

2021). Also, with this report cost can be tracked for all jobs that is ongoing in the real time.

Inventory & manufacturing report: This method of reporting allows for identifying material in

stock, shortages or loss of materials and sales rate of the final product. Snooker England can

make decisions on whether it should manufacture more or not and in how much quantity.

Integration within organizational context

MA systems benefit organization in many aspects, like cost accounting system is helpful in

ascertaining the cost of the business operations accurately, which in turn allows for creating

effective budgets to ensure cost controlling and higher efficiency. Similarly, inventory

costs associated with particular job (Azudin and Mansor, 2018). It is helpful in determining

whether a particular job is profitable or not. Accordingly, resources can be easily diverted among

low profitable and high profitable jobs.

Management Accounting reporting

MA has become very crucial while managing organizational performance and it is

recommended to Snooker England to utilize different methods of MA, so that managerial tasks

can be accomplished in efficient manner. The various MA reporting methods are as follows:

Budget report: This report helps in establishing budgetary control through which future aspects

of Snooker England can be determined (Pasch, 2019). It depicts spending plan of the company

and accordingly, arrangement for the amount of money can be done in advance to avoid

shortages. Also, steps could be taken while comparing actual performance against what has been

budgeted to ensure that the organization is moving towards its end goals.

Account receivables ageing: This report shows record of unpaid invoices along with indicating

the duration of their being outstanding (Kostyukova and et.al., 2018). This procedure within MA

allows Snooker England to determine those invoices that are open and also keeping those clients

on the top who are considered to be slow paying one. Accounting, effective collection and credit

management can be ensured and policies associated with it can be modified as per the

requirements.

Job cost reports: It is a comprehensive documentation of all the costs associated with specific

jobs concerning the organization through which expenditure plan can be created to ensure its

accomplishment on time without any shortages (Maheshwari, Maheshwari and Maheshwari,

2021). Also, with this report cost can be tracked for all jobs that is ongoing in the real time.

Inventory & manufacturing report: This method of reporting allows for identifying material in

stock, shortages or loss of materials and sales rate of the final product. Snooker England can

make decisions on whether it should manufacture more or not and in how much quantity.

Integration within organizational context

MA systems benefit organization in many aspects, like cost accounting system is helpful in

ascertaining the cost of the business operations accurately, which in turn allows for creating

effective budgets to ensure cost controlling and higher efficiency. Similarly, inventory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

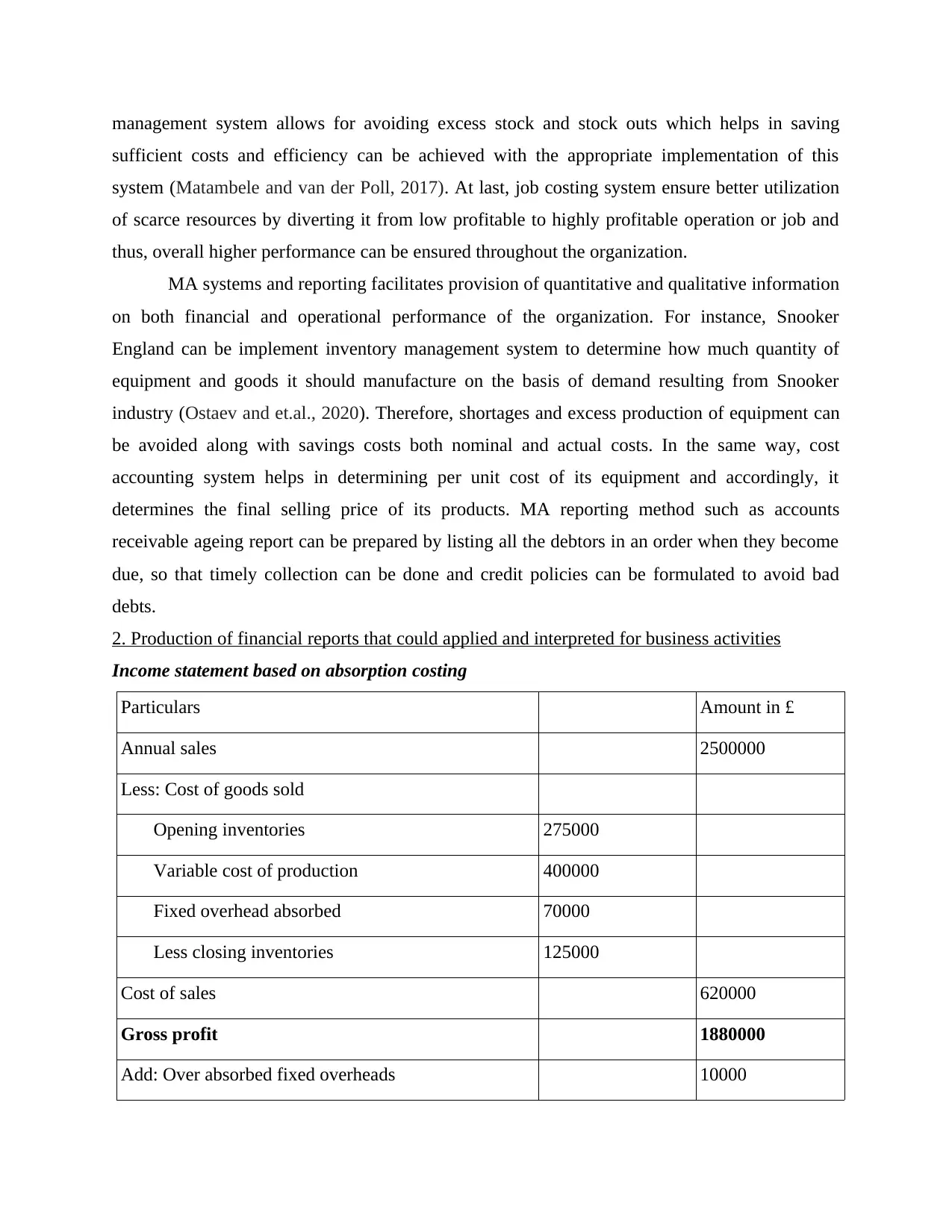

management system allows for avoiding excess stock and stock outs which helps in saving

sufficient costs and efficiency can be achieved with the appropriate implementation of this

system (Matambele and van der Poll, 2017). At last, job costing system ensure better utilization

of scarce resources by diverting it from low profitable to highly profitable operation or job and

thus, overall higher performance can be ensured throughout the organization.

MA systems and reporting facilitates provision of quantitative and qualitative information

on both financial and operational performance of the organization. For instance, Snooker

England can be implement inventory management system to determine how much quantity of

equipment and goods it should manufacture on the basis of demand resulting from Snooker

industry (Ostaev and et.al., 2020). Therefore, shortages and excess production of equipment can

be avoided along with savings costs both nominal and actual costs. In the same way, cost

accounting system helps in determining per unit cost of its equipment and accordingly, it

determines the final selling price of its products. MA reporting method such as accounts

receivable ageing report can be prepared by listing all the debtors in an order when they become

due, so that timely collection can be done and credit policies can be formulated to avoid bad

debts.

2. Production of financial reports that could applied and interpreted for business activities

Income statement based on absorption costing

Particulars Amount in £

Annual sales 2500000

Less: Cost of goods sold

Opening inventories 275000

Variable cost of production 400000

Fixed overhead absorbed 70000

Less closing inventories 125000

Cost of sales 620000

Gross profit 1880000

Add: Over absorbed fixed overheads 10000

sufficient costs and efficiency can be achieved with the appropriate implementation of this

system (Matambele and van der Poll, 2017). At last, job costing system ensure better utilization

of scarce resources by diverting it from low profitable to highly profitable operation or job and

thus, overall higher performance can be ensured throughout the organization.

MA systems and reporting facilitates provision of quantitative and qualitative information

on both financial and operational performance of the organization. For instance, Snooker

England can be implement inventory management system to determine how much quantity of

equipment and goods it should manufacture on the basis of demand resulting from Snooker

industry (Ostaev and et.al., 2020). Therefore, shortages and excess production of equipment can

be avoided along with savings costs both nominal and actual costs. In the same way, cost

accounting system helps in determining per unit cost of its equipment and accordingly, it

determines the final selling price of its products. MA reporting method such as accounts

receivable ageing report can be prepared by listing all the debtors in an order when they become

due, so that timely collection can be done and credit policies can be formulated to avoid bad

debts.

2. Production of financial reports that could applied and interpreted for business activities

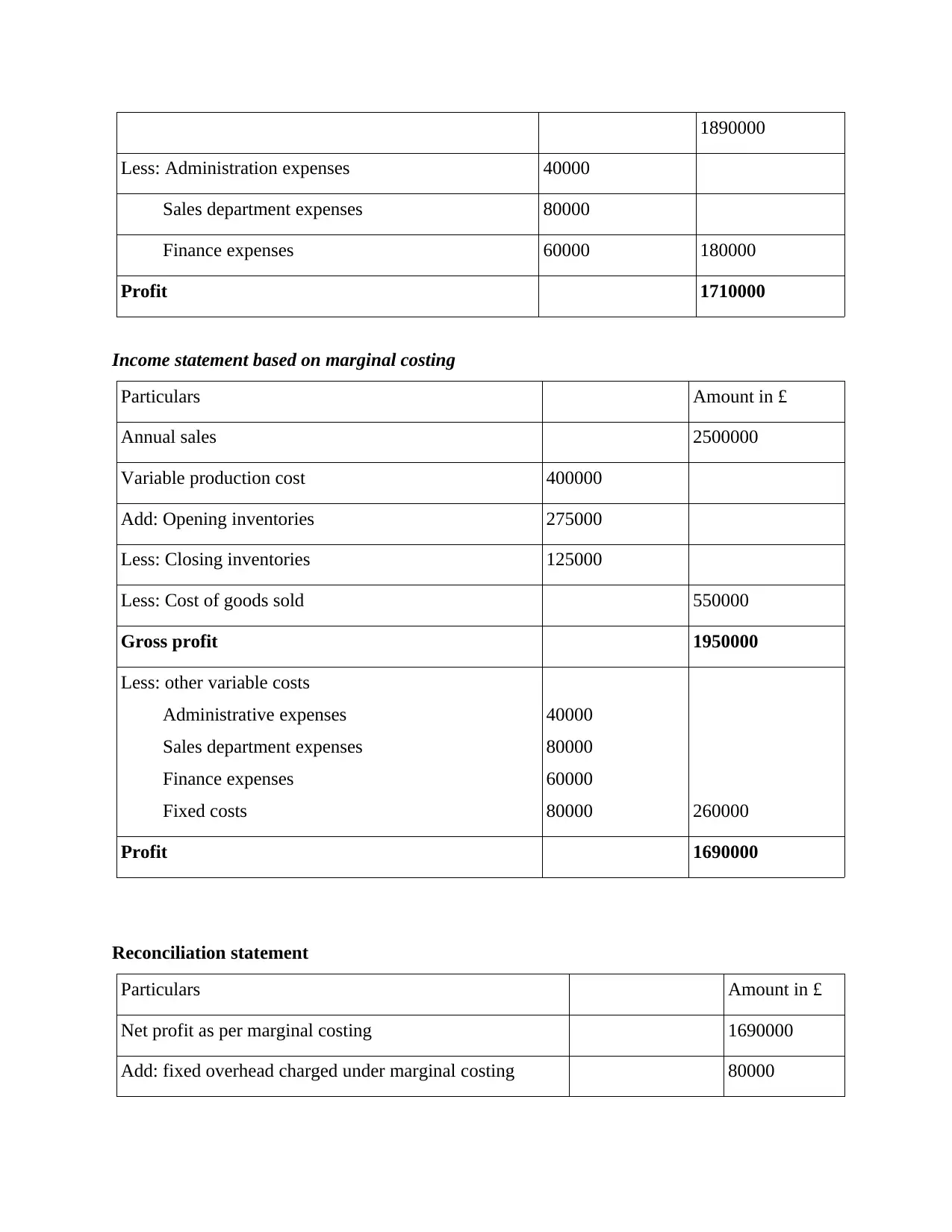

Income statement based on absorption costing

Particulars Amount in £

Annual sales 2500000

Less: Cost of goods sold

Opening inventories 275000

Variable cost of production 400000

Fixed overhead absorbed 70000

Less closing inventories 125000

Cost of sales 620000

Gross profit 1880000

Add: Over absorbed fixed overheads 10000

1890000

Less: Administration expenses 40000

Sales department expenses 80000

Finance expenses 60000 180000

Profit 1710000

Income statement based on marginal costing

Particulars Amount in £

Annual sales 2500000

Variable production cost 400000

Add: Opening inventories 275000

Less: Closing inventories 125000

Less: Cost of goods sold 550000

Gross profit 1950000

Less: other variable costs

Administrative expenses

Sales department expenses

Finance expenses

Fixed costs

40000

80000

60000

80000 260000

Profit 1690000

Reconciliation statement

Particulars Amount in £

Net profit as per marginal costing 1690000

Add: fixed overhead charged under marginal costing 80000

Less: Administration expenses 40000

Sales department expenses 80000

Finance expenses 60000 180000

Profit 1710000

Income statement based on marginal costing

Particulars Amount in £

Annual sales 2500000

Variable production cost 400000

Add: Opening inventories 275000

Less: Closing inventories 125000

Less: Cost of goods sold 550000

Gross profit 1950000

Less: other variable costs

Administrative expenses

Sales department expenses

Finance expenses

Fixed costs

40000

80000

60000

80000 260000

Profit 1690000

Reconciliation statement

Particulars Amount in £

Net profit as per marginal costing 1690000

Add: fixed overhead charged under marginal costing 80000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

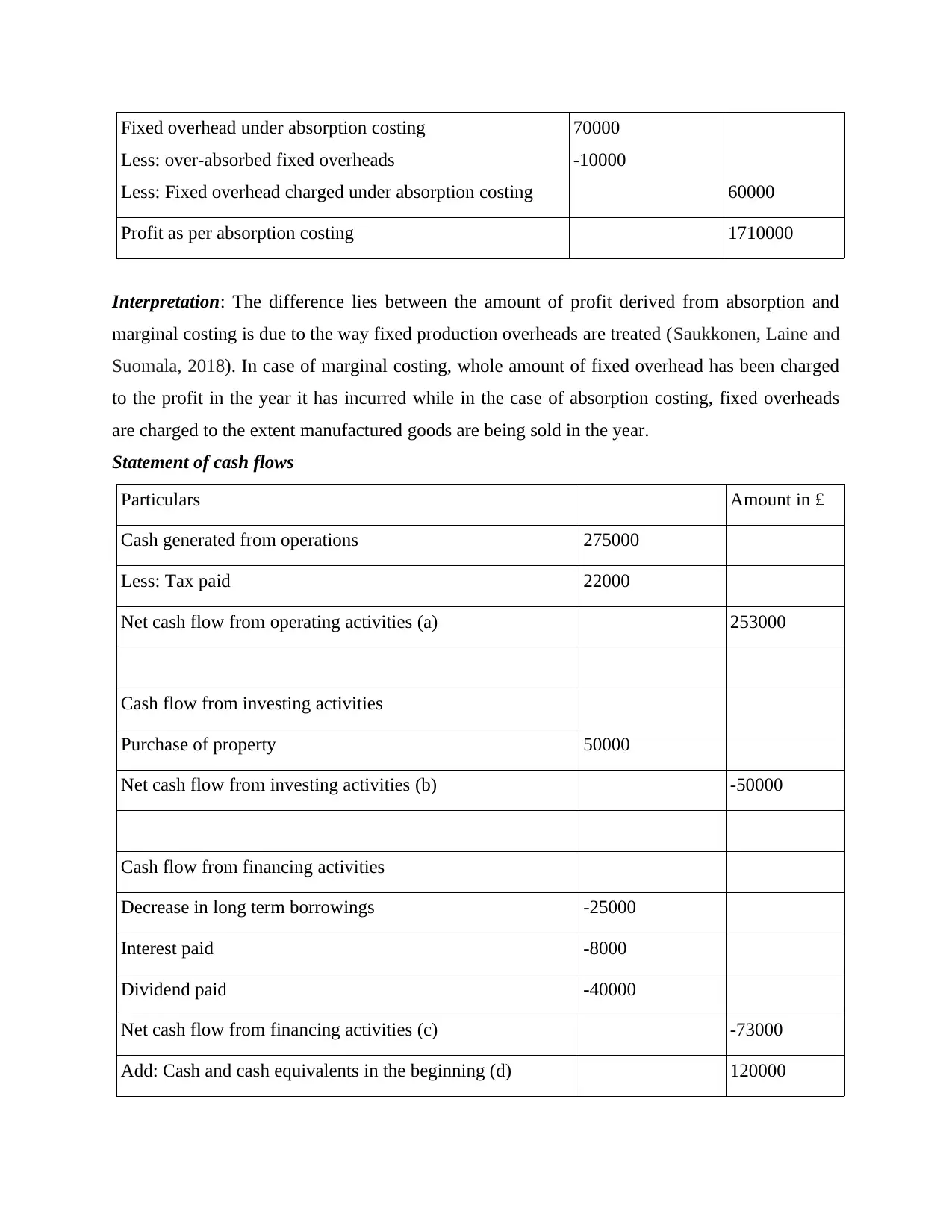

Fixed overhead under absorption costing

Less: over-absorbed fixed overheads

Less: Fixed overhead charged under absorption costing

70000

-10000

60000

Profit as per absorption costing 1710000

Interpretation: The difference lies between the amount of profit derived from absorption and

marginal costing is due to the way fixed production overheads are treated (Saukkonen, Laine and

Suomala, 2018). In case of marginal costing, whole amount of fixed overhead has been charged

to the profit in the year it has incurred while in the case of absorption costing, fixed overheads

are charged to the extent manufactured goods are being sold in the year.

Statement of cash flows

Particulars Amount in £

Cash generated from operations 275000

Less: Tax paid 22000

Net cash flow from operating activities (a) 253000

Cash flow from investing activities

Purchase of property 50000

Net cash flow from investing activities (b) -50000

Cash flow from financing activities

Decrease in long term borrowings -25000

Interest paid -8000

Dividend paid -40000

Net cash flow from financing activities (c) -73000

Add: Cash and cash equivalents in the beginning (d) 120000

Less: over-absorbed fixed overheads

Less: Fixed overhead charged under absorption costing

70000

-10000

60000

Profit as per absorption costing 1710000

Interpretation: The difference lies between the amount of profit derived from absorption and

marginal costing is due to the way fixed production overheads are treated (Saukkonen, Laine and

Suomala, 2018). In case of marginal costing, whole amount of fixed overhead has been charged

to the profit in the year it has incurred while in the case of absorption costing, fixed overheads

are charged to the extent manufactured goods are being sold in the year.

Statement of cash flows

Particulars Amount in £

Cash generated from operations 275000

Less: Tax paid 22000

Net cash flow from operating activities (a) 253000

Cash flow from investing activities

Purchase of property 50000

Net cash flow from investing activities (b) -50000

Cash flow from financing activities

Decrease in long term borrowings -25000

Interest paid -8000

Dividend paid -40000

Net cash flow from financing activities (c) -73000

Add: Cash and cash equivalents in the beginning (d) 120000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash and cash equivalents at the end a+b+c+d 250000

3. Evaluation of planning tools in MA to respond to financial problems for leading organizations

to sustainable success

The different types of planning tools that is available to the Snooker England Ltd for their

budgetary control along with its advantages and disadvantage are as follows:

Budgets: This is a planning tool of management accounting with the help of which

Snooker England company estimates the revenue and expenses of future period (Abdusalomova,

2019). The various budgets prepared by Snooker company is production budget, sales budget,

cash budget, material purchase budget etc.

Advantages:

It helps in controlling the unnecessary expenses and wastage of resources as it assists in

planning which must be achievable.

The coordination and communication between the different departments of Snooker

company get improves because of budgets preparation.

Disadvantages:

Preparation of monthly cash and other activities budgets are quite time-consuming which

sometime distracts the managers from their main goals.

As budgets are based on estimations, which does not provide accurate information the

impact of which any wrong estimation may leads to heavy financial loss to company

(Maheshwari, Maheshwari and Maheshwari, 2021).

Marginal Costing: This is another planning tool which helps in budgetary control with

the help of the break-even analysis. The break-even analysis defines the sales level at which

Snooker company will neither earn any profit nor it will incur loss.

Advantages:

It helps in identifying the margin of safety which means the sales level above break-even

where Snooker company starts earning profit.

It is also one of the best and effective tool to control the cost of sales of the products and

services (Nørreklit, 2017).

Disadvantages:

3. Evaluation of planning tools in MA to respond to financial problems for leading organizations

to sustainable success

The different types of planning tools that is available to the Snooker England Ltd for their

budgetary control along with its advantages and disadvantage are as follows:

Budgets: This is a planning tool of management accounting with the help of which

Snooker England company estimates the revenue and expenses of future period (Abdusalomova,

2019). The various budgets prepared by Snooker company is production budget, sales budget,

cash budget, material purchase budget etc.

Advantages:

It helps in controlling the unnecessary expenses and wastage of resources as it assists in

planning which must be achievable.

The coordination and communication between the different departments of Snooker

company get improves because of budgets preparation.

Disadvantages:

Preparation of monthly cash and other activities budgets are quite time-consuming which

sometime distracts the managers from their main goals.

As budgets are based on estimations, which does not provide accurate information the

impact of which any wrong estimation may leads to heavy financial loss to company

(Maheshwari, Maheshwari and Maheshwari, 2021).

Marginal Costing: This is another planning tool which helps in budgetary control with

the help of the break-even analysis. The break-even analysis defines the sales level at which

Snooker company will neither earn any profit nor it will incur loss.

Advantages:

It helps in identifying the margin of safety which means the sales level above break-even

where Snooker company starts earning profit.

It is also one of the best and effective tool to control the cost of sales of the products and

services (Nørreklit, 2017).

Disadvantages:

It does not consider the semi-variable and fixed cost which is difficult for the Snooker

company to analyse overheads.

It does not provide the best result of sales and profit as time elements are ignored while

classifying total cost into fixed and variable (Rikhardsson and Yigitbasioglu, 2018).

Pricing strategies: This is a tool which the help of which Snooker England Ltd able to

expand its profit margin, market share etc. Basically, Snooker company adopted cost-plus

pricing strategy to set the selling price of its products by adding mark-up to the cost.

Advantages:

It is one of the simplest method to determine cost and also takes few resources such as

research and development.

It also provides a consistent rate of return because it calculates cost per items and

products.

Disadvantage:

As this strategy does take consumers into account which further result into the creation of

profit losing isolationism (Weetman, 2019).

The above discussed planning tools have to be adopted and applied by the Snooker

England Ltd within their business in order to prepare and forecast the budgets. This will help the

company in increasing the productivity and efficiency. For example, Snooker company can also

able to meet their target and achieve goals in specified time-frame if they adopt the planning

tools such as standard costing, variance analysis and budgets (Caglio, A. and Ditillo, 2021).

However, it also causes heavy loss if there is no proper communication between the departments

of company. This might leads to wrong assumptions on various budgets. Thus, the company

further have to adopt two-way communication.

MA systems to respond to financial problems

The various management accounting systems adopted by different organizations in order to deal

with the financial problems are as follows:

Just-in-time inventory management: This is a method of inventory management system

which is used by Tesco Plc within their organization at the time when the demand of their

products are high. The financial problem face by Tesco within their business is that

during the high demand or peak time, the company unable to produce goods and supply it

company to analyse overheads.

It does not provide the best result of sales and profit as time elements are ignored while

classifying total cost into fixed and variable (Rikhardsson and Yigitbasioglu, 2018).

Pricing strategies: This is a tool which the help of which Snooker England Ltd able to

expand its profit margin, market share etc. Basically, Snooker company adopted cost-plus

pricing strategy to set the selling price of its products by adding mark-up to the cost.

Advantages:

It is one of the simplest method to determine cost and also takes few resources such as

research and development.

It also provides a consistent rate of return because it calculates cost per items and

products.

Disadvantage:

As this strategy does take consumers into account which further result into the creation of

profit losing isolationism (Weetman, 2019).

The above discussed planning tools have to be adopted and applied by the Snooker

England Ltd within their business in order to prepare and forecast the budgets. This will help the

company in increasing the productivity and efficiency. For example, Snooker company can also

able to meet their target and achieve goals in specified time-frame if they adopt the planning

tools such as standard costing, variance analysis and budgets (Caglio, A. and Ditillo, 2021).

However, it also causes heavy loss if there is no proper communication between the departments

of company. This might leads to wrong assumptions on various budgets. Thus, the company

further have to adopt two-way communication.

MA systems to respond to financial problems

The various management accounting systems adopted by different organizations in order to deal

with the financial problems are as follows:

Just-in-time inventory management: This is a method of inventory management system

which is used by Tesco Plc within their organization at the time when the demand of their

products are high. The financial problem face by Tesco within their business is that

during the high demand or peak time, the company unable to produce goods and supply it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to the supermarkets & stores. This has also affected its sales to the large extent. So, in

order to deal with this financial problem, company has adopted Just-in-time method of

inventory management system (Caglio and Ditillo, 2021). It also helpful in reducing

waste, inventory holding cost and improve cash flows within business.

Activity Based costing: This is one of the method of cost accounting system with the

help of which the company can allocate its overheads and indirect cost to products and

services. This system of management accounting is uses by Verdant Leisure company in

order to solve the financial problem (Ameen, Ahmed and Abd Hafez, 2018). The

problem faces by Verdant is low profit margin because of the unprofitable services. With

the help of activity based costing, the company identifies the profit and loss of its

different products and services and further stop the unprofitable services. The impact of

which the wastage of its money over unnecessary activities get decreased and its profit

margin get increased.

Price-optimization system: This is a method which is helpful for the company to

analyse how the demand of their products varies at the different level of prices of

products. The financial problem faces by Snooker is low profit which might be because

of the high price of its products and services. In order to solve this problem, the company

have to adopt the price-optimization system of management accounting (Lebedev, 2019).

Here, the company need to analyse the demand of consumer of its products on different

level of prices before setting final price. This is one of the best method which help the

company in increasing its profit.

Along with the price-optimization system, it is also recommendable to Snooker England

Ltd is that they have to adopt the investment appraisal techniques in order to identify the best

and high return option for investment (falih Chichan and Alabdullah, 2021). This helps the

company in improving their cash flows within the business.

An effective management accounting system will definitely help Snooker England

organization in their sustainable success. It is because these systems manages and utilizes all

available resources such as tangible and intangible to create value of sustainability. For example,

if Snooker company will adopt the management accounting system then their ability to analyse

the internal and external factors of business environment get increased. The impact of which they

order to deal with this financial problem, company has adopted Just-in-time method of

inventory management system (Caglio and Ditillo, 2021). It also helpful in reducing

waste, inventory holding cost and improve cash flows within business.

Activity Based costing: This is one of the method of cost accounting system with the

help of which the company can allocate its overheads and indirect cost to products and

services. This system of management accounting is uses by Verdant Leisure company in

order to solve the financial problem (Ameen, Ahmed and Abd Hafez, 2018). The

problem faces by Verdant is low profit margin because of the unprofitable services. With

the help of activity based costing, the company identifies the profit and loss of its

different products and services and further stop the unprofitable services. The impact of

which the wastage of its money over unnecessary activities get decreased and its profit

margin get increased.

Price-optimization system: This is a method which is helpful for the company to

analyse how the demand of their products varies at the different level of prices of

products. The financial problem faces by Snooker is low profit which might be because

of the high price of its products and services. In order to solve this problem, the company

have to adopt the price-optimization system of management accounting (Lebedev, 2019).

Here, the company need to analyse the demand of consumer of its products on different

level of prices before setting final price. This is one of the best method which help the

company in increasing its profit.

Along with the price-optimization system, it is also recommendable to Snooker England

Ltd is that they have to adopt the investment appraisal techniques in order to identify the best

and high return option for investment (falih Chichan and Alabdullah, 2021). This helps the

company in improving their cash flows within the business.

An effective management accounting system will definitely help Snooker England

organization in their sustainable success. It is because these systems manages and utilizes all

available resources such as tangible and intangible to create value of sustainability. For example,

if Snooker company will adopt the management accounting system then their ability to analyse

the internal and external factors of business environment get increased. The impact of which they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can further identify opportunities and threats to their business including strength and weaknesses

(Zhang and Niu, 2019). This will help the company in gaining opportunities and competitive

advantage which leads to sustainable success.

The planning tools of management accounting such as pricing, budgets, marginal,

standard costing etc. will help the company to solve various financial problems. For example,

with the application of standard costing tool of MA, Snooker England Ltd can compare the

actual data with its budgets. This will provide the result of variance and gap between the both

which further work as a base for the company which help them in estimations of upcoming

periods (Maheshwari, Maheshwari and Maheshwari, 2021).

CONCLUSION

The report has concluded the concepts, various tools, techniques and systems of

management accounting which help them in solving their financial problems and managing

sustainable success. Further, the report has also prepared the income statement and cash flow

statement. The income statement under both marginal and absorption costing are calculated

under this report. Lastly, the report has also compared the different management accounting

system used by organization to solve their financial problems.

(Zhang and Niu, 2019). This will help the company in gaining opportunities and competitive

advantage which leads to sustainable success.

The planning tools of management accounting such as pricing, budgets, marginal,

standard costing etc. will help the company to solve various financial problems. For example,

with the application of standard costing tool of MA, Snooker England Ltd can compare the

actual data with its budgets. This will provide the result of variance and gap between the both

which further work as a base for the company which help them in estimations of upcoming

periods (Maheshwari, Maheshwari and Maheshwari, 2021).

CONCLUSION

The report has concluded the concepts, various tools, techniques and systems of

management accounting which help them in solving their financial problems and managing

sustainable success. Further, the report has also prepared the income statement and cash flow

statement. The income statement under both marginal and absorption costing are calculated

under this report. Lastly, the report has also compared the different management accounting

system used by organization to solve their financial problems.

REFERENCES

Ameen, A. M., Ahmed, M. F. and Abd Hafez, M. A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management, 2(1), p.02.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making: Limitations stemming from the process structure and the actors

involved. Qualitative Research in Accounting & Management.

Ostaev, G. Y., and et.al., 2020. Accounting agricultural business from scratch: management

accounting, decision making, analysis and monitoring of business processes. Amazonia

Investiga, 9(27), pp.319-332.

Endenich, C. and Trapp, R., 2020. Ethical implications of management accounting and control:

A systematic review of the contributions from the Journal of Business Ethics. Journal

of business ethics, 163(2), pp.309-328.

Pasch, T., 2019. Strategy and innovation: the mediating role of management accountants and

management accounting systems’ use. Journal of Management Control, 30(2), pp.213-

246.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Matambele, K. and van der Poll, H. M., 2017. Management Accounting Tools for Sustainability

Information Decision-making and Financial Performance. Alternation Journal, (20),

pp.189-213.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Nørreklit, H. ed., 2017. A philosophy of management accounting: A pragmatic constructivist

approach. Taylor & Francis.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Caglio, A. and Ditillo, A., 2021. Reviewing interorganizational management accounting and

control literature: a new look. Journal of Management Accounting Research. 33(1).

pp.149-169.

Ameen, A. M., Ahmed, M. F. and Abd Hafez, M. A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management, 2(1), p.02.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making: Limitations stemming from the process structure and the actors

involved. Qualitative Research in Accounting & Management.

Ostaev, G. Y., and et.al., 2020. Accounting agricultural business from scratch: management

accounting, decision making, analysis and monitoring of business processes. Amazonia

Investiga, 9(27), pp.319-332.

Endenich, C. and Trapp, R., 2020. Ethical implications of management accounting and control:

A systematic review of the contributions from the Journal of Business Ethics. Journal

of business ethics, 163(2), pp.309-328.

Pasch, T., 2019. Strategy and innovation: the mediating role of management accountants and

management accounting systems’ use. Journal of Management Control, 30(2), pp.213-

246.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Matambele, K. and van der Poll, H. M., 2017. Management Accounting Tools for Sustainability

Information Decision-making and Financial Performance. Alternation Journal, (20),

pp.189-213.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

Nørreklit, H. ed., 2017. A philosophy of management accounting: A pragmatic constructivist

approach. Taylor & Francis.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Caglio, A. and Ditillo, A., 2021. Reviewing interorganizational management accounting and

control literature: a new look. Journal of Management Accounting Research. 33(1).

pp.149-169.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.