Management Accounting Report: UCK Furniture Analysis

VerifiedAdded on 2020/10/22

|12

|3324

|68

Report

AI Summary

This report provides an in-depth analysis of management accounting principles, focusing on costing methods, budgeting techniques, and financial issue resolution within the context of UCK Furniture. It begins by exploring various costing methods, including absorption and marginal costing, and calculates net profit using each method. The report then delves into the advantages and disadvantages of planning tools such as forecasting, contingency, and scenario tools, illustrating their application in budgetary processes. Furthermore, the analysis extends to examining financial data from income statements and comparing expenses, particularly for July and August, employing tools like variable and fixed cost calculations. Finally, it addresses the use of accounting systems in identifying financial issues and evaluating financial challenges faced by UCK furniture. The report concludes by summarizing the key findings and the significance of management accounting in business operations.

Management Accounting

Part 2

Part 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Calculation of cost by using various methods.......................................................................1

1.2 Range of management accounting techniques.......................................................................3

1.3: Analysis of data collected from income statement...............................................................3

TASK 2............................................................................................................................................4

2.1 Advantage and disadvantage of using planning tools............................................................4

2.2 Analysis of expenses of July and August.............................................................................5

2.3: Objective and cash budget....................................................................................................6

TASK 3............................................................................................................................................8

3.1: Use of accounting system to determine financial issues.......................................................8

3.2: Evaluating financial issues faced by UCK furniture............................................................9

3.3: Analysis of planning tools that is used in management accounting.....................................9

CONCUSION .................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Calculation of cost by using various methods.......................................................................1

1.2 Range of management accounting techniques.......................................................................3

1.3: Analysis of data collected from income statement...............................................................3

TASK 2............................................................................................................................................4

2.1 Advantage and disadvantage of using planning tools............................................................4

2.2 Analysis of expenses of July and August.............................................................................5

2.3: Objective and cash budget....................................................................................................6

TASK 3............................................................................................................................................8

3.1: Use of accounting system to determine financial issues.......................................................8

3.2: Evaluating financial issues faced by UCK furniture............................................................9

3.3: Analysis of planning tools that is used in management accounting.....................................9

CONCUSION .................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

In present era, every company wants their operation and system to be manage in

appropriate manner. So management accounting is defined as one of the valuable aspect of

company that help internal manager to analyse the financial performance and improve them in

required (Amoako, 2013).

In this report, costing method are discussed to calculate the net profit for company. There

are number of tools that help to overcome different issues. Report shows their advantage and

disadvantage and how they support in budgetary process. Management accounting system also

helpful in resolving different financial problem and comparison of two com0pnaies are discussed

in this report.

TASK 1

1.1 Calculation of cost by using various methods.

In recent management tools and techniques has been updated that help to calculate the net

profit by analysing the cost for a given period of time. In general cost is defined as the amount

paid by buyer of to seller in order to purchase a particular product. Thus cost are involved by

companies in their production and other process to make their operation work effectively. So

costing is consider to be a systematic procedure of calculating actual and complete expenses or

cost incurred by UCK furniture in producing furniture with the present cost of capital. It is

observed that cost is either directly and indirectly related to the production process that support

in completing a task (Brewer, Sorensen and Stout, 2014). So there are different types of costing

method that are linked with UCK furniture business activities. Some of these are discussed

below:

Absorption costing: This type of cost are applicable on manufacturing a product for

company over a period of time. Absorption costing includes fixed and variable cost as it is

knows as full costing method of calculation profit. This method is consider to be one of the most

effective method as it help in making crucial decision. But at the same time there are certain

limitation to absorption costing method as it affect the net profitability of company and decrease

its market position (Absorption costing, 2018.).

Marginal costing: This is related to calculation of cost incurred by companies on

producing an additional unit of output. It consider only variable factor while calculating

In present era, every company wants their operation and system to be manage in

appropriate manner. So management accounting is defined as one of the valuable aspect of

company that help internal manager to analyse the financial performance and improve them in

required (Amoako, 2013).

In this report, costing method are discussed to calculate the net profit for company. There

are number of tools that help to overcome different issues. Report shows their advantage and

disadvantage and how they support in budgetary process. Management accounting system also

helpful in resolving different financial problem and comparison of two com0pnaies are discussed

in this report.

TASK 1

1.1 Calculation of cost by using various methods.

In recent management tools and techniques has been updated that help to calculate the net

profit by analysing the cost for a given period of time. In general cost is defined as the amount

paid by buyer of to seller in order to purchase a particular product. Thus cost are involved by

companies in their production and other process to make their operation work effectively. So

costing is consider to be a systematic procedure of calculating actual and complete expenses or

cost incurred by UCK furniture in producing furniture with the present cost of capital. It is

observed that cost is either directly and indirectly related to the production process that support

in completing a task (Brewer, Sorensen and Stout, 2014). So there are different types of costing

method that are linked with UCK furniture business activities. Some of these are discussed

below:

Absorption costing: This type of cost are applicable on manufacturing a product for

company over a period of time. Absorption costing includes fixed and variable cost as it is

knows as full costing method of calculation profit. This method is consider to be one of the most

effective method as it help in making crucial decision. But at the same time there are certain

limitation to absorption costing method as it affect the net profitability of company and decrease

its market position (Absorption costing, 2018.).

Marginal costing: This is related to calculation of cost incurred by companies on

producing an additional unit of output. It consider only variable factor while calculating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

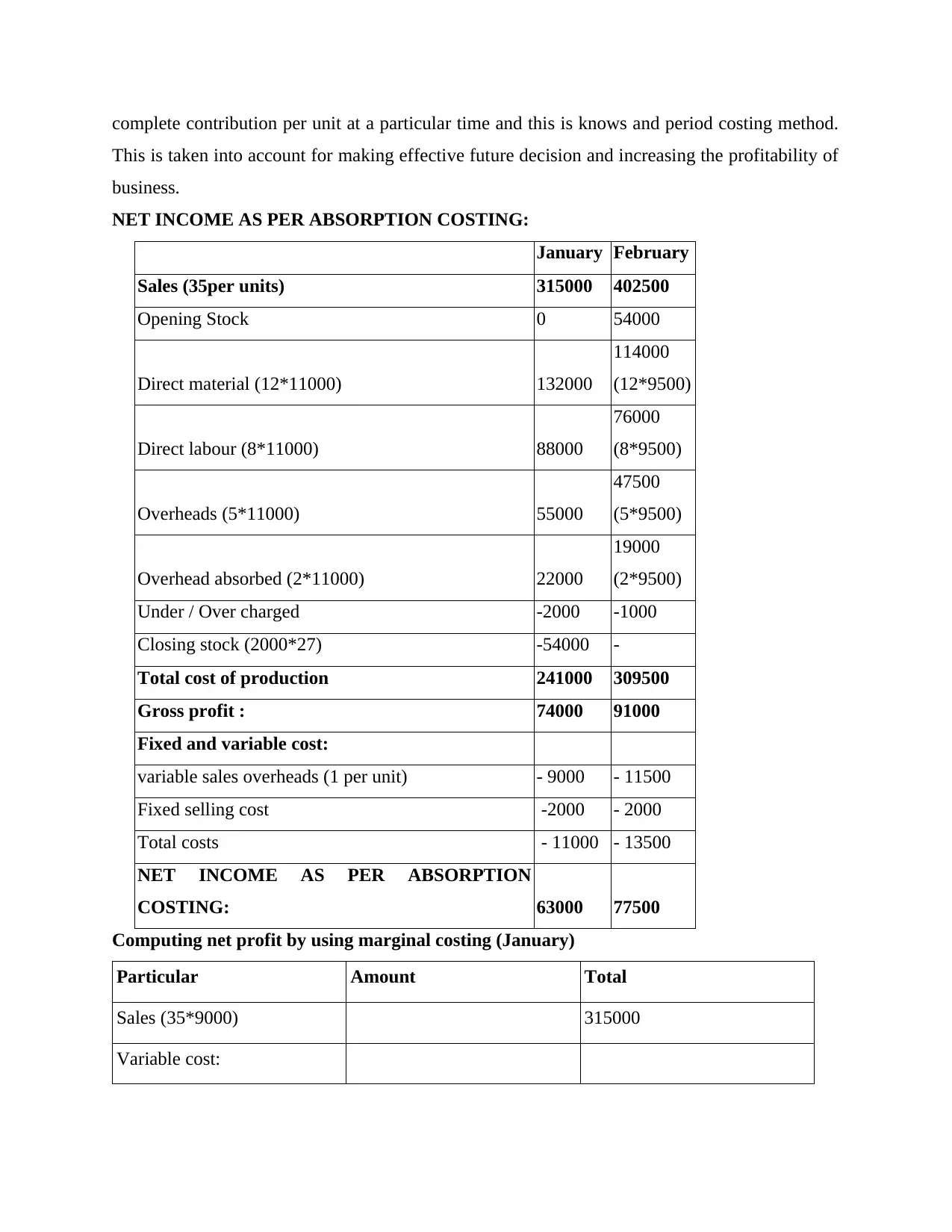

complete contribution per unit at a particular time and this is knows and period costing method.

This is taken into account for making effective future decision and increasing the profitability of

business.

NET INCOME AS PER ABSORPTION COSTING:

January February

Sales (35per units) 315000 402500

Opening Stock 0 54000

Direct material (12*11000) 132000

114000

(12*9500)

Direct labour (8*11000) 88000

76000

(8*9500)

Overheads (5*11000) 55000

47500

(5*9500)

Overhead absorbed (2*11000) 22000

19000

(2*9500)

Under / Over charged -2000 -1000

Closing stock (2000*27) -54000 -

Total cost of production 241000 309500

Gross profit : 74000 91000

Fixed and variable cost:

variable sales overheads (1 per unit) - 9000 - 11500

Fixed selling cost -2000 - 2000

Total costs - 11000 - 13500

NET INCOME AS PER ABSORPTION

COSTING: 63000 77500

Computing net profit by using marginal costing (January)

Particular Amount Total

Sales (35*9000) 315000

Variable cost:

This is taken into account for making effective future decision and increasing the profitability of

business.

NET INCOME AS PER ABSORPTION COSTING:

January February

Sales (35per units) 315000 402500

Opening Stock 0 54000

Direct material (12*11000) 132000

114000

(12*9500)

Direct labour (8*11000) 88000

76000

(8*9500)

Overheads (5*11000) 55000

47500

(5*9500)

Overhead absorbed (2*11000) 22000

19000

(2*9500)

Under / Over charged -2000 -1000

Closing stock (2000*27) -54000 -

Total cost of production 241000 309500

Gross profit : 74000 91000

Fixed and variable cost:

variable sales overheads (1 per unit) - 9000 - 11500

Fixed selling cost -2000 - 2000

Total costs - 11000 - 13500

NET INCOME AS PER ABSORPTION

COSTING: 63000 77500

Computing net profit by using marginal costing (January)

Particular Amount Total

Sales (35*9000) 315000

Variable cost:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

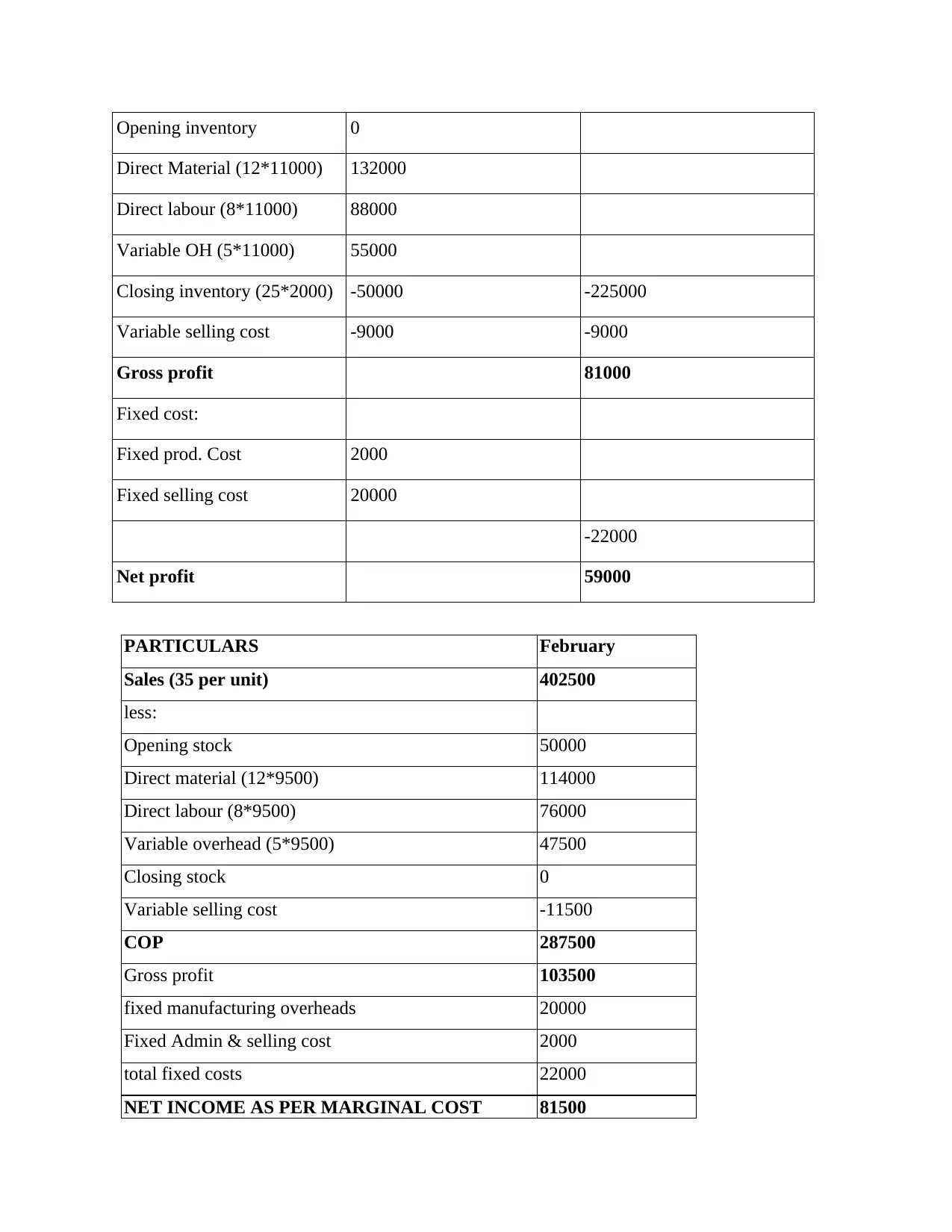

Opening inventory 0

Direct Material (12*11000) 132000

Direct labour (8*11000) 88000

Variable OH (5*11000) 55000

Closing inventory (25*2000) -50000 -225000

Variable selling cost -9000 -9000

Gross profit 81000

Fixed cost:

Fixed prod. Cost 2000

Fixed selling cost 20000

-22000

Net profit 59000

PARTICULARS February

Sales (35 per unit) 402500

less:

Opening stock 50000

Direct material (12*9500) 114000

Direct labour (8*9500) 76000

Variable overhead (5*9500) 47500

Closing stock 0

Variable selling cost -11500

COP 287500

Gross profit 103500

fixed manufacturing overheads 20000

Fixed Admin & selling cost 2000

total fixed costs 22000

NET INCOME AS PER MARGINAL COST 81500

Direct Material (12*11000) 132000

Direct labour (8*11000) 88000

Variable OH (5*11000) 55000

Closing inventory (25*2000) -50000 -225000

Variable selling cost -9000 -9000

Gross profit 81000

Fixed cost:

Fixed prod. Cost 2000

Fixed selling cost 20000

-22000

Net profit 59000

PARTICULARS February

Sales (35 per unit) 402500

less:

Opening stock 50000

Direct material (12*9500) 114000

Direct labour (8*9500) 76000

Variable overhead (5*9500) 47500

Closing stock 0

Variable selling cost -11500

COP 287500

Gross profit 103500

fixed manufacturing overheads 20000

Fixed Admin & selling cost 2000

total fixed costs 22000

NET INCOME AS PER MARGINAL COST 81500

1.2 Range of management accounting techniques.

In accordance to develop, grow and sustain financial stability manager of UCK furniture

has to make effective use of management techniques and tools that support in giving more strong

result for company. Some of these are defined underneath;

Marginal cost: It is defined as the cost added by manufacturing one extra unit of product

or services. This is consider to be the change in total cost that arises when quantity produced in

increase by one unit.

Historical cost: In accounting, historical cost is the original nominal monetary value of a

particular product. This involves reporting of assets and liabilities at their historical cost that are

not updated for changes in the actual values ((JOSHI and et. al., 2011).

1.3: Analysis of data collected from income statement

From the above calculation it has been ascertained that with the help of absorption

costing gross profit for January is 74000 and for February it is 91000. The net profit for both

months January and February is 63000 and 77500 respectively. It has been also observed that

through marginal costing the gross profit for January is 81000 and net profit is 59000. And the

Gross profit for February is 103500 and net profit is 81500.

TASK 2

2.1 Advantage and disadvantage of using planning tools.

In present time, budgets is an effective system that help to estimate overall expenses and

control cost for company at a particular period of time. It help in increasing profit of company

and improving the production process. In order to maintain sustainable in business activity

manager prepare number of budgets such as flexible, sales, production and marketing by which

effective policies are made. So in respect to control the affect of budgets certain planning tool are

used that are discussed below:

Forecasting Costing: With the help of this planning tool manager of UCK furniture are

able to predict about the future expenses so that they are able to ascertain the upcoming profit

and loss. It help in use of present resource in effective manner so that profitability of company

can be maintained. Forecasting tool give best result as it predict the future depending on the past

data so that future losses can be avoided (Klemstine and Maher, 2014).

In accordance to develop, grow and sustain financial stability manager of UCK furniture

has to make effective use of management techniques and tools that support in giving more strong

result for company. Some of these are defined underneath;

Marginal cost: It is defined as the cost added by manufacturing one extra unit of product

or services. This is consider to be the change in total cost that arises when quantity produced in

increase by one unit.

Historical cost: In accounting, historical cost is the original nominal monetary value of a

particular product. This involves reporting of assets and liabilities at their historical cost that are

not updated for changes in the actual values ((JOSHI and et. al., 2011).

1.3: Analysis of data collected from income statement

From the above calculation it has been ascertained that with the help of absorption

costing gross profit for January is 74000 and for February it is 91000. The net profit for both

months January and February is 63000 and 77500 respectively. It has been also observed that

through marginal costing the gross profit for January is 81000 and net profit is 59000. And the

Gross profit for February is 103500 and net profit is 81500.

TASK 2

2.1 Advantage and disadvantage of using planning tools.

In present time, budgets is an effective system that help to estimate overall expenses and

control cost for company at a particular period of time. It help in increasing profit of company

and improving the production process. In order to maintain sustainable in business activity

manager prepare number of budgets such as flexible, sales, production and marketing by which

effective policies are made. So in respect to control the affect of budgets certain planning tool are

used that are discussed below:

Forecasting Costing: With the help of this planning tool manager of UCK furniture are

able to predict about the future expenses so that they are able to ascertain the upcoming profit

and loss. It help in use of present resource in effective manner so that profitability of company

can be maintained. Forecasting tool give best result as it predict the future depending on the past

data so that future losses can be avoided (Klemstine and Maher, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantage:

The primary purpose of using this forecasting tool is it provide effective estimation for

total cost and expenses in more suitable way.

Thus better forecast help to make valuable decision for the main objective of earning

more revenue at a particular period of time.

Disadvantage:

It is observed that prediction about future risk cannot be accurate as business operation

are qualitative in nature.

Contingency tool: This is consider to be an effective planning tool that help internal manager of

company to analyse and evaluate all type of contingency and risk those are non-identical for

business operation. So, in UCK manager use to analyse each factor closely so that any

contingency that may effect the future business can be removed. Some advantage and

disadvantage are discussed below:

Advantage:

With the aid of this tool manager are able to examine the actual expenses and losses that

company is going to get after the formulation of budgets.

Contingency tool support to control all related risk and problems those may effect the

productivity of company in nearby future (Lim, 2011).

Disadvantage:

The main demerit of this tool is that, many time there may arise urgent issues or risk that

cannot be resolved at a particular time.

This is a lengthy process and require more time and prior permission from the top

authority of company.

Scenario tool: This tool help in short term forecasting that further support to create budgets and

control unexpected expenses. So manager of company look upon scenarios that might effect their

production process and reduce their profitability level.

Advantage:

Early determination help UCK furniture to overcome scenarios that assist them to make

better decision.

It really unfolds and the origin of conflict that happen to realize better by the managers.

Disadvantage:

The primary purpose of using this forecasting tool is it provide effective estimation for

total cost and expenses in more suitable way.

Thus better forecast help to make valuable decision for the main objective of earning

more revenue at a particular period of time.

Disadvantage:

It is observed that prediction about future risk cannot be accurate as business operation

are qualitative in nature.

Contingency tool: This is consider to be an effective planning tool that help internal manager of

company to analyse and evaluate all type of contingency and risk those are non-identical for

business operation. So, in UCK manager use to analyse each factor closely so that any

contingency that may effect the future business can be removed. Some advantage and

disadvantage are discussed below:

Advantage:

With the aid of this tool manager are able to examine the actual expenses and losses that

company is going to get after the formulation of budgets.

Contingency tool support to control all related risk and problems those may effect the

productivity of company in nearby future (Lim, 2011).

Disadvantage:

The main demerit of this tool is that, many time there may arise urgent issues or risk that

cannot be resolved at a particular time.

This is a lengthy process and require more time and prior permission from the top

authority of company.

Scenario tool: This tool help in short term forecasting that further support to create budgets and

control unexpected expenses. So manager of company look upon scenarios that might effect their

production process and reduce their profitability level.

Advantage:

Early determination help UCK furniture to overcome scenarios that assist them to make

better decision.

It really unfolds and the origin of conflict that happen to realize better by the managers.

Disadvantage:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The main disadvantage of this tool is that in tough situation it is unable to give best result.

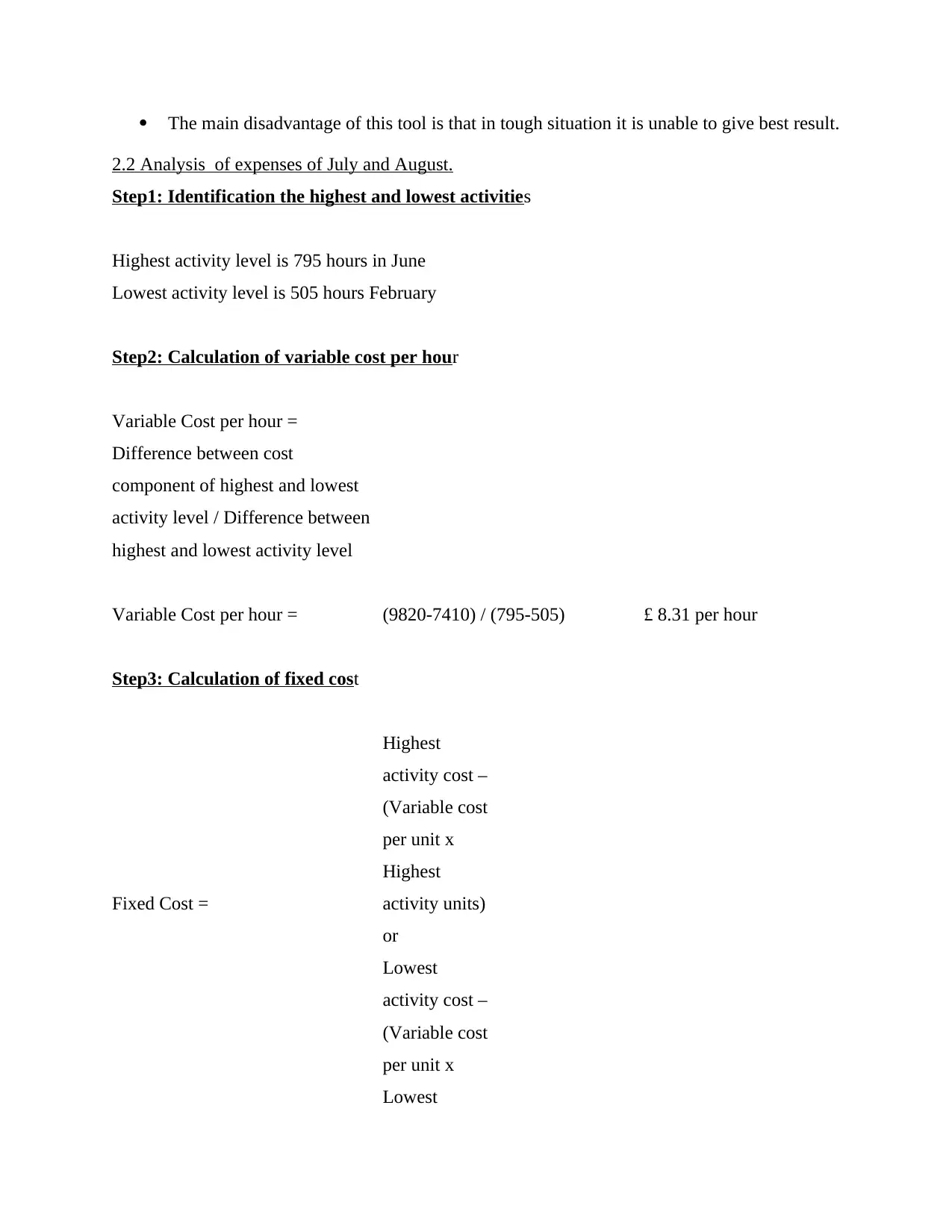

2.2 Analysis of expenses of July and August.

Step1: Identification the highest and lowest activities

Highest activity level is 795 hours in June

Lowest activity level is 505 hours February

Step2: Calculation of variable cost per hour

Variable Cost per hour =

Difference between cost

component of highest and lowest

activity level / Difference between

highest and lowest activity level

Variable Cost per hour = (9820-7410) / (795-505) £ 8.31 per hour

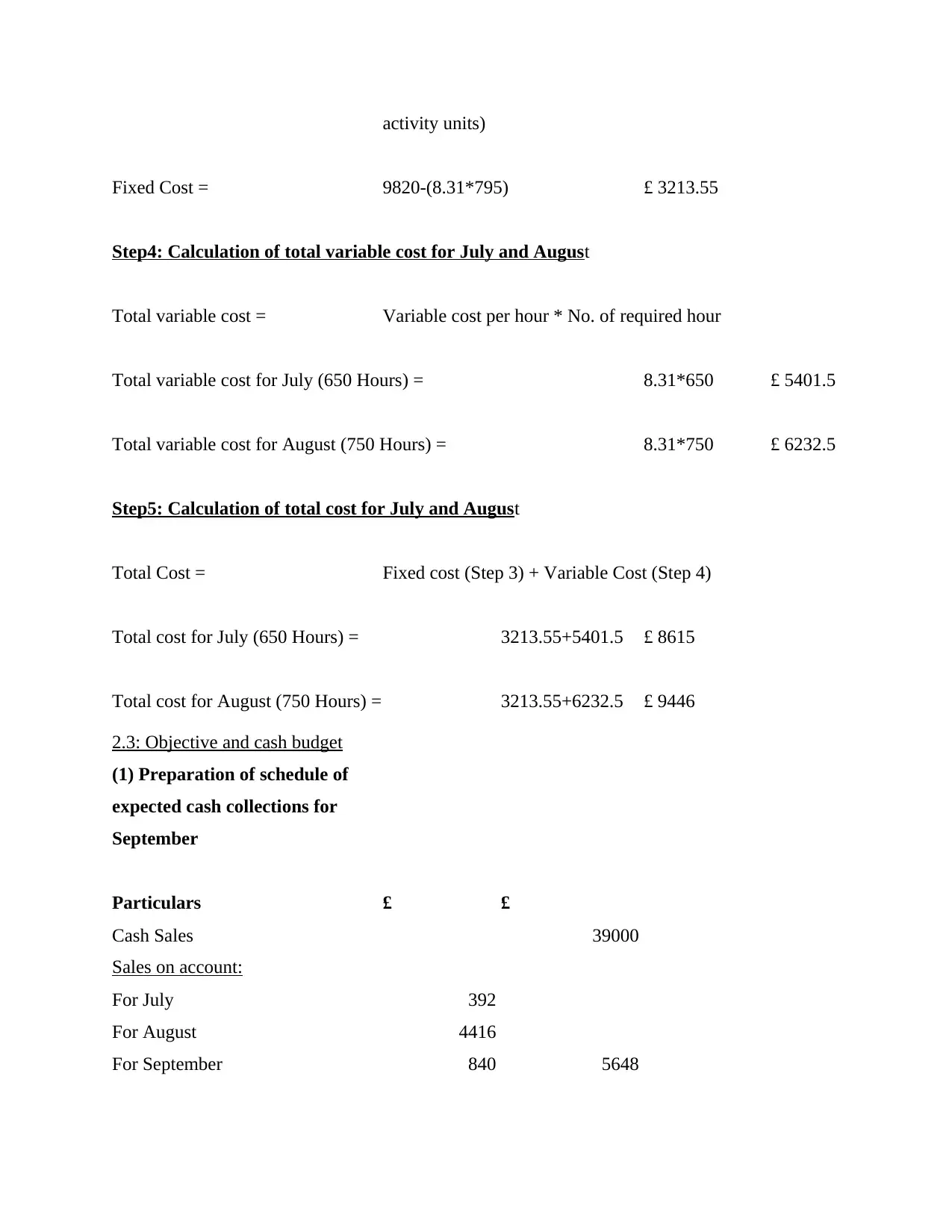

Step3: Calculation of fixed cost

Fixed Cost =

Highest

activity cost –

(Variable cost

per unit x

Highest

activity units)

or

Lowest

activity cost –

(Variable cost

per unit x

Lowest

2.2 Analysis of expenses of July and August.

Step1: Identification the highest and lowest activities

Highest activity level is 795 hours in June

Lowest activity level is 505 hours February

Step2: Calculation of variable cost per hour

Variable Cost per hour =

Difference between cost

component of highest and lowest

activity level / Difference between

highest and lowest activity level

Variable Cost per hour = (9820-7410) / (795-505) £ 8.31 per hour

Step3: Calculation of fixed cost

Fixed Cost =

Highest

activity cost –

(Variable cost

per unit x

Highest

activity units)

or

Lowest

activity cost –

(Variable cost

per unit x

Lowest

activity units)

Fixed Cost = 9820-(8.31*795) £ 3213.55

Step4: Calculation of total variable cost for July and August

Total variable cost = Variable cost per hour * No. of required hour

Total variable cost for July (650 Hours) = 8.31*650 £ 5401.5

Total variable cost for August (750 Hours) = 8.31*750 £ 6232.5

Step5: Calculation of total cost for July and August

Total Cost = Fixed cost (Step 3) + Variable Cost (Step 4)

Total cost for July (650 Hours) = 3213.55+5401.5 £ 8615

Total cost for August (750 Hours) = 3213.55+6232.5 £ 9446

2.3: Objective and cash budget

(1) Preparation of schedule of

expected cash collections for

September

Particulars £ £

Cash Sales 39000

Sales on account:

For July 392

For August 4416

For September 840 5648

Fixed Cost = 9820-(8.31*795) £ 3213.55

Step4: Calculation of total variable cost for July and August

Total variable cost = Variable cost per hour * No. of required hour

Total variable cost for July (650 Hours) = 8.31*650 £ 5401.5

Total variable cost for August (750 Hours) = 8.31*750 £ 6232.5

Step5: Calculation of total cost for July and August

Total Cost = Fixed cost (Step 3) + Variable Cost (Step 4)

Total cost for July (650 Hours) = 3213.55+5401.5 £ 8615

Total cost for August (750 Hours) = 3213.55+6232.5 £ 9446

2.3: Objective and cash budget

(1) Preparation of schedule of

expected cash collections for

September

Particulars £ £

Cash Sales 39000

Sales on account:

For July 392

For August 4416

For September 840 5648

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

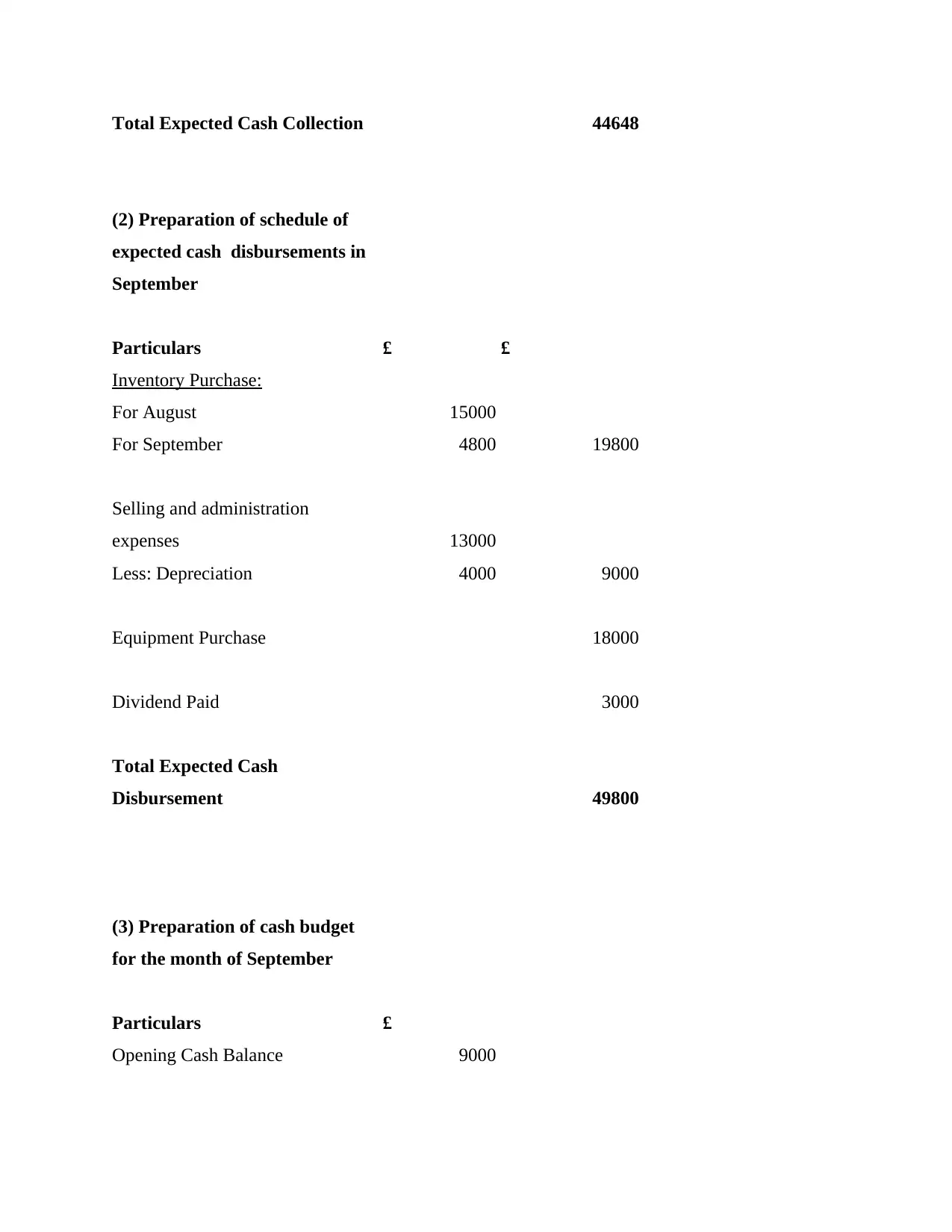

Total Expected Cash Collection 44648

(2) Preparation of schedule of

expected cash disbursements in

September

Particulars £ £

Inventory Purchase:

For August 15000

For September 4800 19800

Selling and administration

expenses 13000

Less: Depreciation 4000 9000

Equipment Purchase 18000

Dividend Paid 3000

Total Expected Cash

Disbursement 49800

(3) Preparation of cash budget

for the month of September

Particulars £

Opening Cash Balance 9000

(2) Preparation of schedule of

expected cash disbursements in

September

Particulars £ £

Inventory Purchase:

For August 15000

For September 4800 19800

Selling and administration

expenses 13000

Less: Depreciation 4000 9000

Equipment Purchase 18000

Dividend Paid 3000

Total Expected Cash

Disbursement 49800

(3) Preparation of cash budget

for the month of September

Particulars £

Opening Cash Balance 9000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Add: Total Expected Cash

Collection 44648

Less: Total Expected Cash

Disbursement 49800

Expected Closing Cash Balance 3848

Add: Bank Credit 1152

Expected Closing Cash Balance

with bank credit 5000

TASK 3

3.1: Use of accounting system to determine financial issues

Ratios Formula UCK furniture’s UCK woodworks

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+

31930

=0.68 times

8150/81230

=0.100 times

Comparison

UCK Furniture’s UCK WOODWORKDS

Collection 44648

Less: Total Expected Cash

Disbursement 49800

Expected Closing Cash Balance 3848

Add: Bank Credit 1152

Expected Closing Cash Balance

with bank credit 5000

TASK 3

3.1: Use of accounting system to determine financial issues

Ratios Formula UCK furniture’s UCK woodworks

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+

31930

=0.68 times

8150/81230

=0.100 times

Comparison

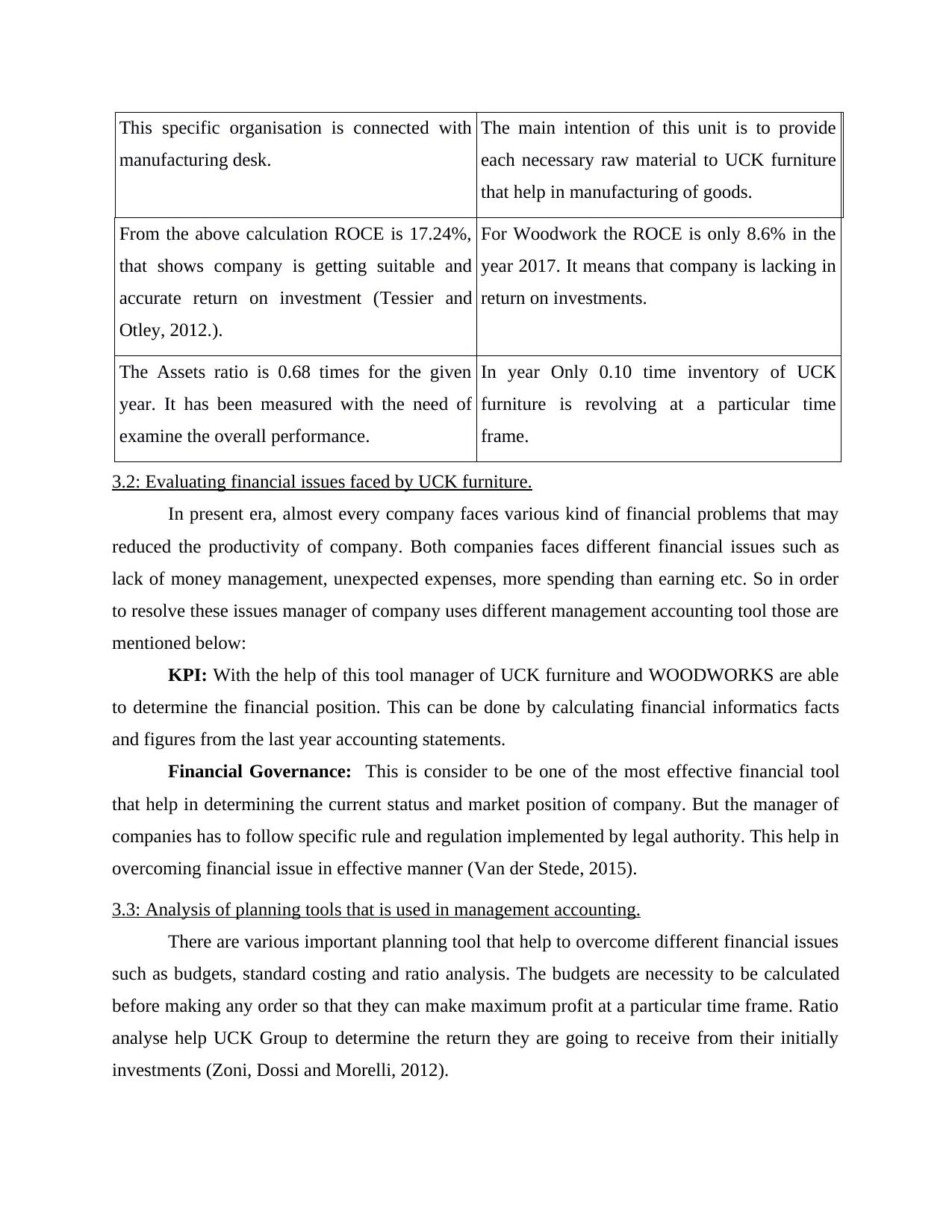

UCK Furniture’s UCK WOODWORKDS

This specific organisation is connected with

manufacturing desk.

The main intention of this unit is to provide

each necessary raw material to UCK furniture

that help in manufacturing of goods.

From the above calculation ROCE is 17.24%,

that shows company is getting suitable and

accurate return on investment (Tessier and

Otley, 2012.).

For Woodwork the ROCE is only 8.6% in the

year 2017. It means that company is lacking in

return on investments.

The Assets ratio is 0.68 times for the given

year. It has been measured with the need of

examine the overall performance.

In year Only 0.10 time inventory of UCK

furniture is revolving at a particular time

frame.

3.2: Evaluating financial issues faced by UCK furniture.

In present era, almost every company faces various kind of financial problems that may

reduced the productivity of company. Both companies faces different financial issues such as

lack of money management, unexpected expenses, more spending than earning etc. So in order

to resolve these issues manager of company uses different management accounting tool those are

mentioned below:

KPI: With the help of this tool manager of UCK furniture and WOODWORKS are able

to determine the financial position. This can be done by calculating financial informatics facts

and figures from the last year accounting statements.

Financial Governance: This is consider to be one of the most effective financial tool

that help in determining the current status and market position of company. But the manager of

companies has to follow specific rule and regulation implemented by legal authority. This help in

overcoming financial issue in effective manner (Van der Stede, 2015).

3.3: Analysis of planning tools that is used in management accounting.

There are various important planning tool that help to overcome different financial issues

such as budgets, standard costing and ratio analysis. The budgets are necessity to be calculated

before making any order so that they can make maximum profit at a particular time frame. Ratio

analyse help UCK Group to determine the return they are going to receive from their initially

investments (Zoni, Dossi and Morelli, 2012).

manufacturing desk.

The main intention of this unit is to provide

each necessary raw material to UCK furniture

that help in manufacturing of goods.

From the above calculation ROCE is 17.24%,

that shows company is getting suitable and

accurate return on investment (Tessier and

Otley, 2012.).

For Woodwork the ROCE is only 8.6% in the

year 2017. It means that company is lacking in

return on investments.

The Assets ratio is 0.68 times for the given

year. It has been measured with the need of

examine the overall performance.

In year Only 0.10 time inventory of UCK

furniture is revolving at a particular time

frame.

3.2: Evaluating financial issues faced by UCK furniture.

In present era, almost every company faces various kind of financial problems that may

reduced the productivity of company. Both companies faces different financial issues such as

lack of money management, unexpected expenses, more spending than earning etc. So in order

to resolve these issues manager of company uses different management accounting tool those are

mentioned below:

KPI: With the help of this tool manager of UCK furniture and WOODWORKS are able

to determine the financial position. This can be done by calculating financial informatics facts

and figures from the last year accounting statements.

Financial Governance: This is consider to be one of the most effective financial tool

that help in determining the current status and market position of company. But the manager of

companies has to follow specific rule and regulation implemented by legal authority. This help in

overcoming financial issue in effective manner (Van der Stede, 2015).

3.3: Analysis of planning tools that is used in management accounting.

There are various important planning tool that help to overcome different financial issues

such as budgets, standard costing and ratio analysis. The budgets are necessity to be calculated

before making any order so that they can make maximum profit at a particular time frame. Ratio

analyse help UCK Group to determine the return they are going to receive from their initially

investments (Zoni, Dossi and Morelli, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.