Management Accounting Report: Airdri - Cost Analysis and Planning

VerifiedAdded on 2021/01/02

|16

|5530

|200

Report

AI Summary

This report provides a detailed analysis of management accounting principles, focusing on a case study of Airdri, a manufacturing company and importer. The report covers key aspects of management accounting, including the importance of management accounting systems, such as cost accounting, inventory management, price optimization, and job costing. It explores different types of management accounting reports, including performance reports, inventory management reports, accounts receivable reports, and job costing reports. The report also examines the integration of accounting systems and reporting methods. Furthermore, it delves into cost analysis techniques, budgetary control tools, and the application of these tools in addressing financial issues. The report aims to provide insights into how Airdri utilizes management accounting to enhance its financial performance and decision-making processes.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirement of its system...................................................1

P2. Different type of management accounting reports...........................................................3

M1. Importance of different management accounting system...............................................4

D1: Various reporting method and accounting system integration........................................5

TASK 2............................................................................................................................................6

P3. Techniques used to analyse cost with marginal and absorption costs..............................6

M2. Various type of Accounting tool and techniques............................................................8

D2. Financial report for the data of business activities..........................................................8

TASK3.............................................................................................................................................9

P4. Different planning tool used for budgetary control..........................................................9

M3 Analysis of various planning tool and its application for forecasting...........................10

P5: Financial issue and resolution........................................................................................11

M4 Analysis of planning tool to deal with financial issue...................................................12

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirement of its system...................................................1

P2. Different type of management accounting reports...........................................................3

M1. Importance of different management accounting system...............................................4

D1: Various reporting method and accounting system integration........................................5

TASK 2............................................................................................................................................6

P3. Techniques used to analyse cost with marginal and absorption costs..............................6

M2. Various type of Accounting tool and techniques............................................................8

D2. Financial report for the data of business activities..........................................................8

TASK3.............................................................................................................................................9

P4. Different planning tool used for budgetary control..........................................................9

M3 Analysis of various planning tool and its application for forecasting...........................10

P5: Financial issue and resolution........................................................................................11

M4 Analysis of planning tool to deal with financial issue...................................................12

CONCLUSION .............................................................................................................................12

REFERENCES .............................................................................................................................13

INTRODUCTION

Management accounting is a process of collecting business information and than record

that information in management reports. It is a system which is followed by the management of a

company to generate reports that may provide actual information of company's performance and

its position in market (Amidu, Effah and Abor, 2011). It helps the internal stakeholder of an

organisation to gather information of operational and executional activities of the business and

form crucial decision in context of the business. Managers monitor, control and analyse the

information and than make policies and strategies to attain organisational goals. It help the

managers in strategic decision making which is used to resolve possible issues that may occur.

The company chosen for this project report is Airdri, it is a manufacturing company of hand

Dryer. It is also a leading importer in UK.

This project reports consist detailed information of management accounting, its systems,

reports, their types, benefits of management accounting system, different costing techniques,

various planning tools that are used in budgetary control and how organisation is using

management accounting to respond financial problems that they are facing.

TASK 1

P1 Management accounting and requirement of its system

Management accounting refers to the examination of accounting data by the managers to

find the accuracy of the information which has been recorded in the books. It help the internal

stakeholders to analyse the performance of running business and its position in the market.

Management accounting system is used by various organisations to evaluate the transparency of

the data which has been recorded by the managers in the books of management (Bennett and

James, 2017). In Airdri it is used by the management to analyse various information such as cost,

inventory and performance. There are four different types of management accounting like cost

accounting, price optimisation, inventory management and job costing system. These systems are

explained below:

Cost accounting system: A cost accounting system is used by a company to analyse its

actual profitability by estimating actual cost of its products. It helps the managers and internal

stakeholder to assess the cost which is involved in the manufacturing process of the company. In

Airdri it is used to record all the production related activities that are performed by the company.

1

Management accounting is a process of collecting business information and than record

that information in management reports. It is a system which is followed by the management of a

company to generate reports that may provide actual information of company's performance and

its position in market (Amidu, Effah and Abor, 2011). It helps the internal stakeholder of an

organisation to gather information of operational and executional activities of the business and

form crucial decision in context of the business. Managers monitor, control and analyse the

information and than make policies and strategies to attain organisational goals. It help the

managers in strategic decision making which is used to resolve possible issues that may occur.

The company chosen for this project report is Airdri, it is a manufacturing company of hand

Dryer. It is also a leading importer in UK.

This project reports consist detailed information of management accounting, its systems,

reports, their types, benefits of management accounting system, different costing techniques,

various planning tools that are used in budgetary control and how organisation is using

management accounting to respond financial problems that they are facing.

TASK 1

P1 Management accounting and requirement of its system

Management accounting refers to the examination of accounting data by the managers to

find the accuracy of the information which has been recorded in the books. It help the internal

stakeholders to analyse the performance of running business and its position in the market.

Management accounting system is used by various organisations to evaluate the transparency of

the data which has been recorded by the managers in the books of management (Bennett and

James, 2017). In Airdri it is used by the management to analyse various information such as cost,

inventory and performance. There are four different types of management accounting like cost

accounting, price optimisation, inventory management and job costing system. These systems are

explained below:

Cost accounting system: A cost accounting system is used by a company to analyse its

actual profitability by estimating actual cost of its products. It helps the managers and internal

stakeholder to assess the cost which is involved in the manufacturing process of the company. In

Airdri it is used to record all the production related activities that are performed by the company.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It help to examine the flow of inventory. It is very beneficial for the organisation because it helps

the managers to get the exact information of cost which is involved in manufacturing process.

There are three different type of cost accounting systems. Standard costing which is used to

analyse the difference between actual cost and budgeted cost, Marginal costing, it help to

identify the cost of additional units of production that are produced by the organisation and at

last absorption costing in which the manufacturing cost of units are absorbed from the sale of

same units.

Inventory management system: It is mainly used by manufacturing companies as it

may provide exact information of inventory. It helps the managers to track the inventory while it

is in transit, warehouse or in production (Bryer, 2013). The managers of Airdri use inventory

management system to record the activities that are related to inventory. It help the management

to keep an eye to their goods that are taken in and out of the organisation. There are three types

of this system. LIFO, FIFO, AVCO, In LIFO the recently received inventory will be used first by

the company for production. In FIFO the earlier received stock will be used first for

manufacturing process. In AVCO the inventory will be used on average basis for the production

process of products. It is very important for the company because it may facilitate managers

while analysing the inventory information.

Price optimisation system: This system is used by organisations to find the best prices

of their products that may lead the organisation toward its organisational goals that are profit

maximisation and customer satisfaction. In Airdri price optimisation system is used to examine

customer's reactions toward their price changing strategies. It help the managers while deciding

the right prices for their products by studying the behaviour of the customers and determining

their needs and wants. It also help to make effective pricing decisions which will lead the

organisation toward success. It is very advantageous for the company because it help to set

appropriate prices for the products by recording the reaction of customers toward price changing

strategies of the company.

Job costing system: It is concerned with the process of analysing the cost which is

involved in different activities of the company. Managers of company are responsible to record

cost of various production segments in management reports. In Airdri it is used to determine cost

of different jobs that are totally different form each other and performed according to the

specifications of customers (Carlsson-Wall, Kraus and Lind, 2015). It also separates the direct

2

the managers to get the exact information of cost which is involved in manufacturing process.

There are three different type of cost accounting systems. Standard costing which is used to

analyse the difference between actual cost and budgeted cost, Marginal costing, it help to

identify the cost of additional units of production that are produced by the organisation and at

last absorption costing in which the manufacturing cost of units are absorbed from the sale of

same units.

Inventory management system: It is mainly used by manufacturing companies as it

may provide exact information of inventory. It helps the managers to track the inventory while it

is in transit, warehouse or in production (Bryer, 2013). The managers of Airdri use inventory

management system to record the activities that are related to inventory. It help the management

to keep an eye to their goods that are taken in and out of the organisation. There are three types

of this system. LIFO, FIFO, AVCO, In LIFO the recently received inventory will be used first by

the company for production. In FIFO the earlier received stock will be used first for

manufacturing process. In AVCO the inventory will be used on average basis for the production

process of products. It is very important for the company because it may facilitate managers

while analysing the inventory information.

Price optimisation system: This system is used by organisations to find the best prices

of their products that may lead the organisation toward its organisational goals that are profit

maximisation and customer satisfaction. In Airdri price optimisation system is used to examine

customer's reactions toward their price changing strategies. It help the managers while deciding

the right prices for their products by studying the behaviour of the customers and determining

their needs and wants. It also help to make effective pricing decisions which will lead the

organisation toward success. It is very advantageous for the company because it help to set

appropriate prices for the products by recording the reaction of customers toward price changing

strategies of the company.

Job costing system: It is concerned with the process of analysing the cost which is

involved in different activities of the company. Managers of company are responsible to record

cost of various production segments in management reports. In Airdri it is used to determine cost

of different jobs that are totally different form each other and performed according to the

specifications of customers (Carlsson-Wall, Kraus and Lind, 2015). It also separates the direct

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and indirect costs which include the cost of material, labour and overheads of activities. It is very

beneficial for the organisation because it can provide the exact information of different costs that

are included in process of manufacturing.

P2. Different type of management accounting reports.

In every business there is a need to prepare accurate and appropriate management

accounting report so that can be helpful for internal manager to measure and improve

performance of employee as well as of company. These accounting report provides valuable

information to manager like trim cost of production, high-performing employee employee, invest

in those product and good that provide best return to the company. These report are especially

important for small firm like Airdri that help their management to derive important strategies for

achieving their goal. Manager record all applicable information in organised manner so that they

can have actual picture about the operation performed by company (Chang, 2013). Accounting

report are also prepared in the faith of shareholder and other creditors so that the might have the

exact information about the Airdri. This help them to make precious decision about the

investments within the company.

Management of Airdri prepare accounting report to make important decision in respect to

measure and improve performance of employee working with them. By these report they gather

all the specified information like cost involved in production, sales analyse, financial

performance etc. As Airdri is a manufacturer of hand dryer so it requires lot of money and

workforce to run its business. So, management of this company generate these report quarterly,

monthly to track, calculate and measure all expenses incurred in production of and also record

income generated within a period. There are various type of management accounting report that

are prepared by manager of Airdri to record all happing and figure out the current position that is

benefited for shareholder. Different type of report are performance report, inventory

management report, account receivable report and job cost report that are useful of Airdri and are

explained below:

Performance Report: These are very important for company as management use this

performance report to analyse and compare the execution of worker working in company with

actual and budgets performance. The estimated budgets of performance for a specific period are

usually the actual performance from prior year or period. Some basic example are, annual

performance report of employee, report related to various project and production of product

3

beneficial for the organisation because it can provide the exact information of different costs that

are included in process of manufacturing.

P2. Different type of management accounting reports.

In every business there is a need to prepare accurate and appropriate management

accounting report so that can be helpful for internal manager to measure and improve

performance of employee as well as of company. These accounting report provides valuable

information to manager like trim cost of production, high-performing employee employee, invest

in those product and good that provide best return to the company. These report are especially

important for small firm like Airdri that help their management to derive important strategies for

achieving their goal. Manager record all applicable information in organised manner so that they

can have actual picture about the operation performed by company (Chang, 2013). Accounting

report are also prepared in the faith of shareholder and other creditors so that the might have the

exact information about the Airdri. This help them to make precious decision about the

investments within the company.

Management of Airdri prepare accounting report to make important decision in respect to

measure and improve performance of employee working with them. By these report they gather

all the specified information like cost involved in production, sales analyse, financial

performance etc. As Airdri is a manufacturer of hand dryer so it requires lot of money and

workforce to run its business. So, management of this company generate these report quarterly,

monthly to track, calculate and measure all expenses incurred in production of and also record

income generated within a period. There are various type of management accounting report that

are prepared by manager of Airdri to record all happing and figure out the current position that is

benefited for shareholder. Different type of report are performance report, inventory

management report, account receivable report and job cost report that are useful of Airdri and are

explained below:

Performance Report: These are very important for company as management use this

performance report to analyse and compare the execution of worker working in company with

actual and budgets performance. The estimated budgets of performance for a specific period are

usually the actual performance from prior year or period. Some basic example are, annual

performance report of employee, report related to various project and production of product

3

report etc. Airdri is small business firm so their manager prepare these yearly report to measure

and compare the performance of employee involved in production of . So they are able to figure

out the efficiency of worker and in case if required they can improve the efficiency which result

in achievement of company goal (Dražić Lutilsky and Dragija, 2012).

Inventory management reports: Every company makes these report especially those

organisation that produce physical with down break disposition find these inventory report very

valuable. They gather centralize data on cost of stock, labour and all other production overhead

involved in producing a product. Management a with these report manage stock movement

within company like time of arrival, exploit of inventory, stock stored in warehouses etc.

Manager of Airdri prepare accurate and effective stock report as they will be able to figure out

the profitability, turnover and demand for their stock. There are different techniques adopted by

manager of Airdri to maintain their stock such as, ABC analysis, Just-in-time, EOQ analysis.

Account Receivable Report: These report plays an important role for every company

that offer credit services to their buyer. This report provide full information about all the unpaid

invoices and idle credit note depending upon the days of outstanding. Account receivable report

are useful in improving the credit collection system and increase the inflows within the company.

Collection department through this report determine those bill which are due. In Airdri manager

prepare these report to find out all outstanding bills of buyer according to their credit date.

Through this process they will be able to generate inflows from unpaid invoices and can easily

detect the financial position of Airdri (Fisher and Krumwiede, 2012).

Job costing report: these report are prepared by management to view the total cost

incurred in a single project compared to the expected income output by that particular project.

Manager prepare these report to calculate the profitability of the specific type job involved. By

using these report manager of Airdri record the total cost incur on production of hand dryer and

try to control these cost if required. This report involve the calculation and measurement of

labour cost, material cost and production overhead etc. that will increase the profitability of

company.

M1. Importance of different management accounting system

Accounting system are very important for manager that help them to forecasted future

attainment of company goal. There are various management accounting system that aid the

management to increase the profitability of company. Manager of Airdri follow all management

4

and compare the performance of employee involved in production of . So they are able to figure

out the efficiency of worker and in case if required they can improve the efficiency which result

in achievement of company goal (Dražić Lutilsky and Dragija, 2012).

Inventory management reports: Every company makes these report especially those

organisation that produce physical with down break disposition find these inventory report very

valuable. They gather centralize data on cost of stock, labour and all other production overhead

involved in producing a product. Management a with these report manage stock movement

within company like time of arrival, exploit of inventory, stock stored in warehouses etc.

Manager of Airdri prepare accurate and effective stock report as they will be able to figure out

the profitability, turnover and demand for their stock. There are different techniques adopted by

manager of Airdri to maintain their stock such as, ABC analysis, Just-in-time, EOQ analysis.

Account Receivable Report: These report plays an important role for every company

that offer credit services to their buyer. This report provide full information about all the unpaid

invoices and idle credit note depending upon the days of outstanding. Account receivable report

are useful in improving the credit collection system and increase the inflows within the company.

Collection department through this report determine those bill which are due. In Airdri manager

prepare these report to find out all outstanding bills of buyer according to their credit date.

Through this process they will be able to generate inflows from unpaid invoices and can easily

detect the financial position of Airdri (Fisher and Krumwiede, 2012).

Job costing report: these report are prepared by management to view the total cost

incurred in a single project compared to the expected income output by that particular project.

Manager prepare these report to calculate the profitability of the specific type job involved. By

using these report manager of Airdri record the total cost incur on production of hand dryer and

try to control these cost if required. This report involve the calculation and measurement of

labour cost, material cost and production overhead etc. that will increase the profitability of

company.

M1. Importance of different management accounting system

Accounting system are very important for manager that help them to forecasted future

attainment of company goal. There are various management accounting system that aid the

management to increase the profitability of company. Manager of Airdri follow all management

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system that help them to increase the effectiveness of their business operation. These accounting

system have different advantages to the company that are described underneath:

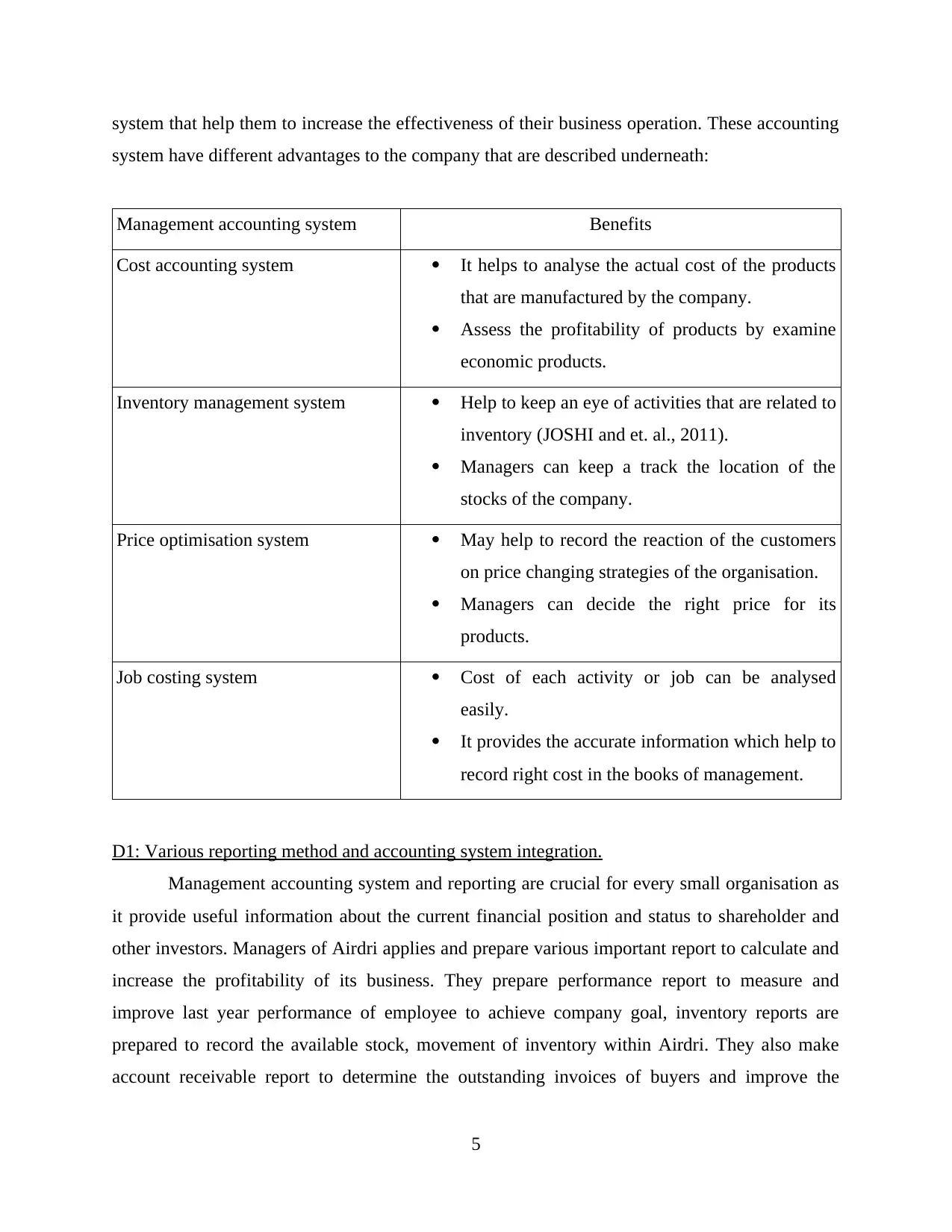

Management accounting system Benefits

Cost accounting system It helps to analyse the actual cost of the products

that are manufactured by the company.

Assess the profitability of products by examine

economic products.

Inventory management system Help to keep an eye of activities that are related to

inventory (JOSHI and et. al., 2011).

Managers can keep a track the location of the

stocks of the company.

Price optimisation system May help to record the reaction of the customers

on price changing strategies of the organisation.

Managers can decide the right price for its

products.

Job costing system Cost of each activity or job can be analysed

easily.

It provides the accurate information which help to

record right cost in the books of management.

D1: Various reporting method and accounting system integration.

Management accounting system and reporting are crucial for every small organisation as

it provide useful information about the current financial position and status to shareholder and

other investors. Managers of Airdri applies and prepare various important report to calculate and

increase the profitability of its business. They prepare performance report to measure and

improve last year performance of employee to achieve company goal, inventory reports are

prepared to record the available stock, movement of inventory within Airdri. They also make

account receivable report to determine the outstanding invoices of buyers and improve the

5

system have different advantages to the company that are described underneath:

Management accounting system Benefits

Cost accounting system It helps to analyse the actual cost of the products

that are manufactured by the company.

Assess the profitability of products by examine

economic products.

Inventory management system Help to keep an eye of activities that are related to

inventory (JOSHI and et. al., 2011).

Managers can keep a track the location of the

stocks of the company.

Price optimisation system May help to record the reaction of the customers

on price changing strategies of the organisation.

Managers can decide the right price for its

products.

Job costing system Cost of each activity or job can be analysed

easily.

It provides the accurate information which help to

record right cost in the books of management.

D1: Various reporting method and accounting system integration.

Management accounting system and reporting are crucial for every small organisation as

it provide useful information about the current financial position and status to shareholder and

other investors. Managers of Airdri applies and prepare various important report to calculate and

increase the profitability of its business. They prepare performance report to measure and

improve last year performance of employee to achieve company goal, inventory reports are

prepared to record the available stock, movement of inventory within Airdri. They also make

account receivable report to determine the outstanding invoices of buyers and improve the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

collection process of company (Klychova, Faskhutdinova and Sadrieva, 2014). Job report help

them to figure out the total cost incurred on individual job for completing project in Airdri.

TASK 2

P3. Techniques used to analyse cost with marginal and absorption costs.

Cost is the amount paid by an individual to buy a particular product or services. It is

considered as the flow of money from buyer to seller. In contrast, these are the monetary value of

material, resources, opportunity incurred in production and delivery of good and services. It is

said that all expense involved in business are cost but all cost are not consider as expenses as

some of them can be an income for the organisation. Management of Airdri requires huge

amount of cost to expand their business and improve its operation in order to achieve more

outcome. They also require cost in the production and making of expensive hand dryer. There

are various type of cost such as variable cost that includes raw material cost, labour cost and

fixed cost that are related to the hour involved in production process. In Airdri management uses

various different costing method to calculate net profit such as marginal costing and absorption

costing. These costing system are described below:

Marginal costing: This is defines as the cost that is involved in production of one

additional unit of output. It is used to ascertain the optimal manufacture amount for an company,

where it costs the least amount to produce additional outcome. These costing system only

includes variable cost in the total revenue sales revenue so net profit margin is calculated for an

organisation (Kuula, Putkiranta and Toivanen, 2012). It includes cost related to labour, material,

production overheads and selling cost. This is considers more effective way for evaluating net

profit and thus gives better information for future decision.

Absorption costing: This method includes all fixed and variable cost that is involved in

the production process. It is commonly also known as full costing method that involved cost of

direct labour, fixed an variable manufacture overheads, material etc. to calculate net profit. As

compared to marginal costing this concepts is more effective as it is use to absorb fixed and

variable cost incur during cost of production.

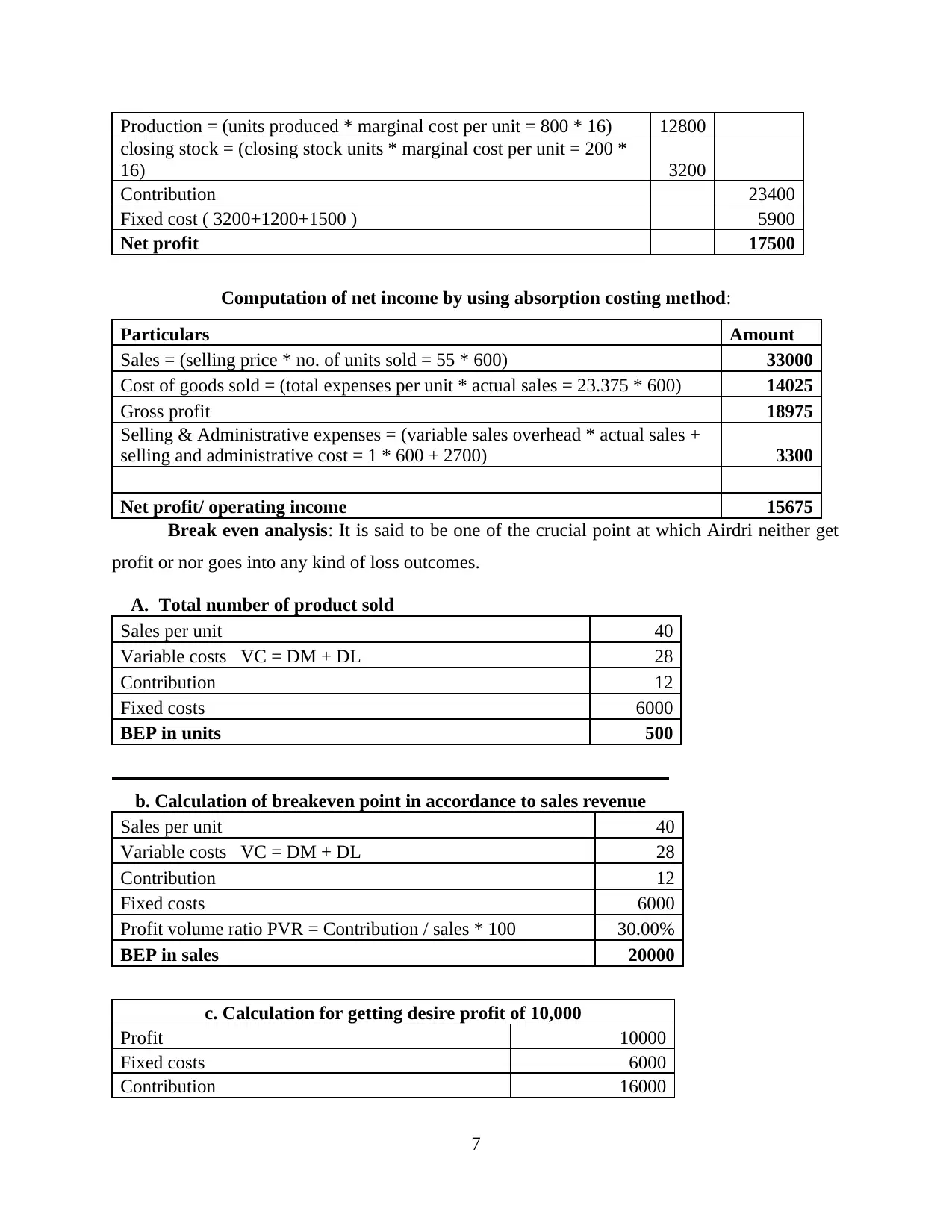

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

6

them to figure out the total cost incurred on individual job for completing project in Airdri.

TASK 2

P3. Techniques used to analyse cost with marginal and absorption costs.

Cost is the amount paid by an individual to buy a particular product or services. It is

considered as the flow of money from buyer to seller. In contrast, these are the monetary value of

material, resources, opportunity incurred in production and delivery of good and services. It is

said that all expense involved in business are cost but all cost are not consider as expenses as

some of them can be an income for the organisation. Management of Airdri requires huge

amount of cost to expand their business and improve its operation in order to achieve more

outcome. They also require cost in the production and making of expensive hand dryer. There

are various type of cost such as variable cost that includes raw material cost, labour cost and

fixed cost that are related to the hour involved in production process. In Airdri management uses

various different costing method to calculate net profit such as marginal costing and absorption

costing. These costing system are described below:

Marginal costing: This is defines as the cost that is involved in production of one

additional unit of output. It is used to ascertain the optimal manufacture amount for an company,

where it costs the least amount to produce additional outcome. These costing system only

includes variable cost in the total revenue sales revenue so net profit margin is calculated for an

organisation (Kuula, Putkiranta and Toivanen, 2012). It includes cost related to labour, material,

production overheads and selling cost. This is considers more effective way for evaluating net

profit and thus gives better information for future decision.

Absorption costing: This method includes all fixed and variable cost that is involved in

the production process. It is commonly also known as full costing method that involved cost of

direct labour, fixed an variable manufacture overheads, material etc. to calculate net profit. As

compared to marginal costing this concepts is more effective as it is use to absorb fixed and

variable cost incur during cost of production.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

6

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is said to be one of the crucial point at which Airdri neither get

profit or nor goes into any kind of loss outcomes.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

7

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is said to be one of the crucial point at which Airdri neither get

profit or nor goes into any kind of loss outcomes.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

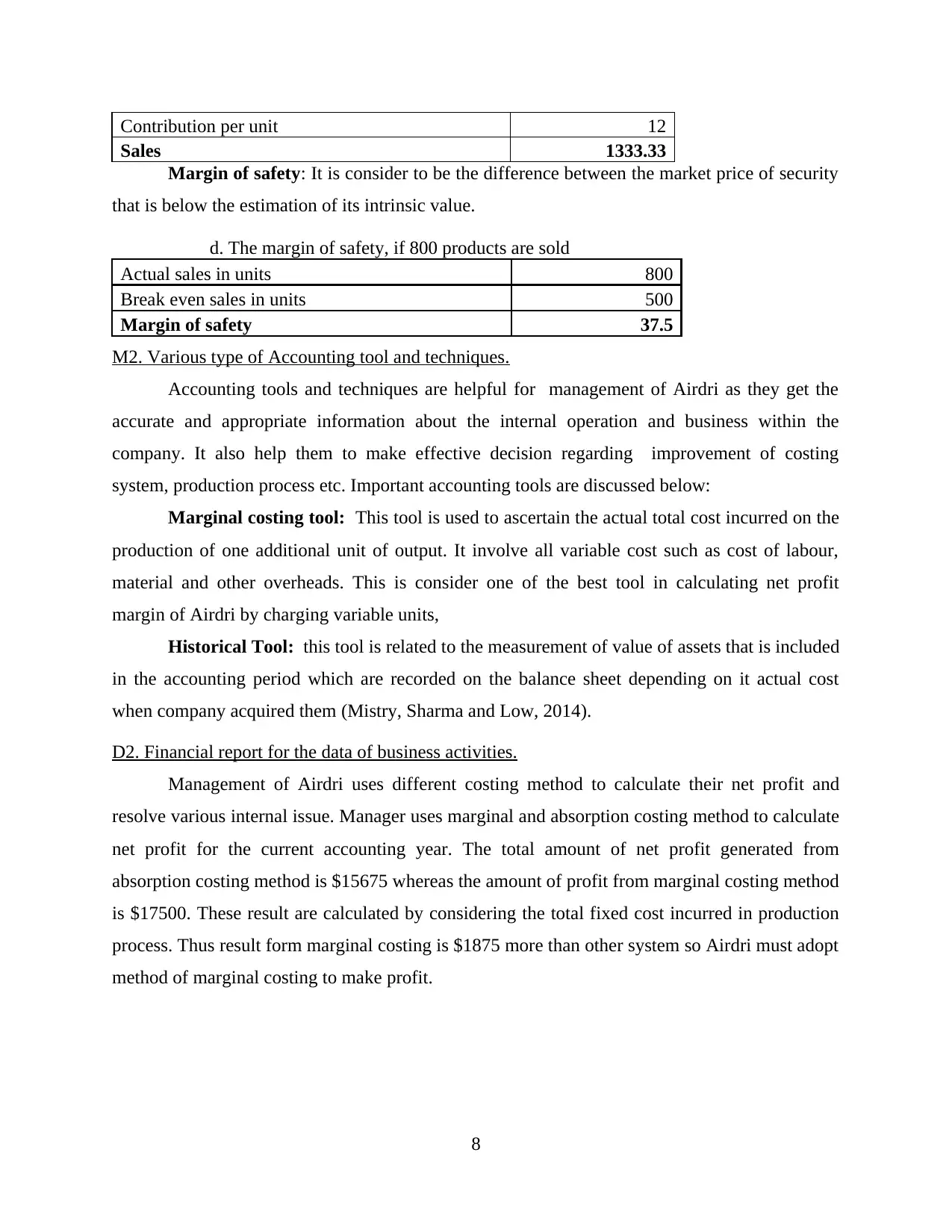

Contribution per unit 12

Sales 1333.33

Margin of safety: It is consider to be the difference between the market price of security

that is below the estimation of its intrinsic value.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2. Various type of Accounting tool and techniques.

Accounting tools and techniques are helpful for management of Airdri as they get the

accurate and appropriate information about the internal operation and business within the

company. It also help them to make effective decision regarding improvement of costing

system, production process etc. Important accounting tools are discussed below:

Marginal costing tool: This tool is used to ascertain the actual total cost incurred on the

production of one additional unit of output. It involve all variable cost such as cost of labour,

material and other overheads. This is consider one of the best tool in calculating net profit

margin of Airdri by charging variable units,

Historical Tool: this tool is related to the measurement of value of assets that is included

in the accounting period which are recorded on the balance sheet depending on it actual cost

when company acquired them (Mistry, Sharma and Low, 2014).

D2. Financial report for the data of business activities.

Management of Airdri uses different costing method to calculate their net profit and

resolve various internal issue. Manager uses marginal and absorption costing method to calculate

net profit for the current accounting year. The total amount of net profit generated from

absorption costing method is $15675 whereas the amount of profit from marginal costing method

is $17500. These result are calculated by considering the total fixed cost incurred in production

process. Thus result form marginal costing is $1875 more than other system so Airdri must adopt

method of marginal costing to make profit.

8

Sales 1333.33

Margin of safety: It is consider to be the difference between the market price of security

that is below the estimation of its intrinsic value.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2. Various type of Accounting tool and techniques.

Accounting tools and techniques are helpful for management of Airdri as they get the

accurate and appropriate information about the internal operation and business within the

company. It also help them to make effective decision regarding improvement of costing

system, production process etc. Important accounting tools are discussed below:

Marginal costing tool: This tool is used to ascertain the actual total cost incurred on the

production of one additional unit of output. It involve all variable cost such as cost of labour,

material and other overheads. This is consider one of the best tool in calculating net profit

margin of Airdri by charging variable units,

Historical Tool: this tool is related to the measurement of value of assets that is included

in the accounting period which are recorded on the balance sheet depending on it actual cost

when company acquired them (Mistry, Sharma and Low, 2014).

D2. Financial report for the data of business activities.

Management of Airdri uses different costing method to calculate their net profit and

resolve various internal issue. Manager uses marginal and absorption costing method to calculate

net profit for the current accounting year. The total amount of net profit generated from

absorption costing method is $15675 whereas the amount of profit from marginal costing method

is $17500. These result are calculated by considering the total fixed cost incurred in production

process. Thus result form marginal costing is $1875 more than other system so Airdri must adopt

method of marginal costing to make profit.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK3

P4. Different planning tool used for budgetary control.

Budgets are prepared to predict the financial result and position of a company for future

Small firms like Airdri uses preplanned budgets to plan and measure performance of employee

and business operation, control spending on production activity of hand dryer. It also help them

to control operation and develop new product etc. with the available resources. It is the future

identification of total income and profit company is going to earn in the forthcoming period

(What is budgeting, 2018).

Budgetary control process:

It is consider to be one of the most effective process that is helpful for an organisation to

evaluate total profit and expenses for future period. Under this process, budgeted and actual

prospect those are used to evaluate and remove all kind of difference that must arises in an

organisation. There are various useful centres that consists of effective process to cop-up with

various budget needs (Öker and Özyapici, 2013). Planning is one of the essential tools that can

be taken into account for controlling various issues those are arises in an organisation. Manager

of Airdri uses various budgetary planning tool such as forecasting, contingency and scenario

tools that are explained below:

Forecasting tool: This process is simply making a prediction about the future depending

upon the data collected from past and present research of tendency. Anyone can make a forecast,

the condition is to be right or close enough so that important planning decisions can be based on

the forecast. Manager of Airdri uses this tool to estimate upcoming events for their business and

future projects. Businesses employ a different vesture of forecasting methods to evaluate

potential results stemming from their decisions.

Advantages: The most illustrious advantage of forecasting methods to Airdri is that the

projections rely on the strength of past data. The chief advantage of this tool is that the main

source of data comes from the experiences of well-qualified executives and employees. The vast

majority of business owners mix the hard data with personal strike to develop useful prediction.

Disadvantages: The disadvantages of forecasting is the same as that of any other method

of predicting the future, no one can absolutely sure how the future of business will be. Any

unforeseen factors can render a forecast useless, regardless the quality of data. In some cases,

9

P4. Different planning tool used for budgetary control.

Budgets are prepared to predict the financial result and position of a company for future

Small firms like Airdri uses preplanned budgets to plan and measure performance of employee

and business operation, control spending on production activity of hand dryer. It also help them

to control operation and develop new product etc. with the available resources. It is the future

identification of total income and profit company is going to earn in the forthcoming period

(What is budgeting, 2018).

Budgetary control process:

It is consider to be one of the most effective process that is helpful for an organisation to

evaluate total profit and expenses for future period. Under this process, budgeted and actual

prospect those are used to evaluate and remove all kind of difference that must arises in an

organisation. There are various useful centres that consists of effective process to cop-up with

various budget needs (Öker and Özyapici, 2013). Planning is one of the essential tools that can

be taken into account for controlling various issues those are arises in an organisation. Manager

of Airdri uses various budgetary planning tool such as forecasting, contingency and scenario

tools that are explained below:

Forecasting tool: This process is simply making a prediction about the future depending

upon the data collected from past and present research of tendency. Anyone can make a forecast,

the condition is to be right or close enough so that important planning decisions can be based on

the forecast. Manager of Airdri uses this tool to estimate upcoming events for their business and

future projects. Businesses employ a different vesture of forecasting methods to evaluate

potential results stemming from their decisions.

Advantages: The most illustrious advantage of forecasting methods to Airdri is that the

projections rely on the strength of past data. The chief advantage of this tool is that the main

source of data comes from the experiences of well-qualified executives and employees. The vast

majority of business owners mix the hard data with personal strike to develop useful prediction.

Disadvantages: The disadvantages of forecasting is the same as that of any other method

of predicting the future, no one can absolutely sure how the future of business will be. Any

unforeseen factors can render a forecast useless, regardless the quality of data. In some cases,

9

one forecasting method shows the interest rate will rise, and another will illustrate the rate will

steady or decline

Scenario tool: It is making assumptions on what the future is going to be and how your

business environment will change overtime in-light of that future. It's a planning tool which

identify a specific set of uncertainties, different realities of what might happen in future of your

business. Its sounds simple, and possibly not worth the trouble or specific effort, however,

building this set of assumptions are crucial for long term organisation's guidance. Management

of Airdri depends upon various scenario that can be resulted in future and have a diverse effect

on their business operation (Tsai and et. al., 2013).

Advantages: Scenario planning is an emerging method designed to energise thinking.

May allow real insights and unlock creativity and allows for business outside the box.

Disadvantage: Planning of scenario required expert forecast, sometime there may be

lack those scenario that result let improper decision making and may effect the future growth of

the Airdri.

Contingency tool:A contingency plan commonly known as “Plan B” describes what will

happen in a possible, but not expected, situation. Usually, contingency plans are designed to

handle emergency situations. This provide course of action that is designed to help Airdri to

respond to different type of business risk that might have diverse affect of the company.

Advantages: Plan B or contingency planning help to overcome all kind of contingency

or emergency those might effect the performance and profitability of the company. These plans

are developed by providing proper training to the employee. The advantage of using this tool is

to that it eliminates major disruption in the operations of the business.

Disadvantage: In case emergency some time it is not possible to make plan on the spot.

This system require expert opinion in order to plan about any future contingency and if not it

may led to mismanagement within company. It is more involved in some kind of situation

because of its analysis nature.

M3 Analysis of various planning tool and its application for forecasting

Management of Airdri uses different planning tool for budgetary control such as

forecasting tool to predict and develop plans for future uncertainties like total cost incurred etc.

Contingency tool are referred as Plan B that are useful in controlling risk that might effect

10

steady or decline

Scenario tool: It is making assumptions on what the future is going to be and how your

business environment will change overtime in-light of that future. It's a planning tool which

identify a specific set of uncertainties, different realities of what might happen in future of your

business. Its sounds simple, and possibly not worth the trouble or specific effort, however,

building this set of assumptions are crucial for long term organisation's guidance. Management

of Airdri depends upon various scenario that can be resulted in future and have a diverse effect

on their business operation (Tsai and et. al., 2013).

Advantages: Scenario planning is an emerging method designed to energise thinking.

May allow real insights and unlock creativity and allows for business outside the box.

Disadvantage: Planning of scenario required expert forecast, sometime there may be

lack those scenario that result let improper decision making and may effect the future growth of

the Airdri.

Contingency tool:A contingency plan commonly known as “Plan B” describes what will

happen in a possible, but not expected, situation. Usually, contingency plans are designed to

handle emergency situations. This provide course of action that is designed to help Airdri to

respond to different type of business risk that might have diverse affect of the company.

Advantages: Plan B or contingency planning help to overcome all kind of contingency

or emergency those might effect the performance and profitability of the company. These plans

are developed by providing proper training to the employee. The advantage of using this tool is

to that it eliminates major disruption in the operations of the business.

Disadvantage: In case emergency some time it is not possible to make plan on the spot.

This system require expert opinion in order to plan about any future contingency and if not it

may led to mismanagement within company. It is more involved in some kind of situation

because of its analysis nature.

M3 Analysis of various planning tool and its application for forecasting

Management of Airdri uses different planning tool for budgetary control such as

forecasting tool to predict and develop plans for future uncertainties like total cost incurred etc.

Contingency tool are referred as Plan B that are useful in controlling risk that might effect

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.