Management Accounting: Monthly Control Report and Recommendations for Amana Ltd

VerifiedAdded on 2023/06/07

|13

|3283

|282

AI Summary

This report provides a monthly control report for Amana Ltd, including original and flexed budgets and variances. It also offers recommendations for areas of development and advice on whether to set up their own online shop or sell on Amazon.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(i) Preparation of monthly control report showing original budget, flexed budget and variances

.....................................................................................................................................................3

(ii) Presenting report on performance of Amana’s company during the year 2020 using the

control report prepared above......................................................................................................5

(iii) Recommendations to Amana’s CEO on area of development.............................................7

PART B...........................................................................................................................................7

1. Advise to Mr Amana’s on decision either set up their own online shop or sell on Amazon. .7

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(i) Preparation of monthly control report showing original budget, flexed budget and variances

.....................................................................................................................................................3

(ii) Presenting report on performance of Amana’s company during the year 2020 using the

control report prepared above......................................................................................................5

(iii) Recommendations to Amana’s CEO on area of development.............................................7

PART B...........................................................................................................................................7

1. Advise to Mr Amana’s on decision either set up their own online shop or sell on Amazon. .7

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting refer to process of analysing as well as communicating the

financial information to business managers for making informative decisions (Pavlatos and

Kostakis, 2018). It differs from financial accounting as it intends to managerial purposes for

guiding users to make better business decisions. It concerns with cost and sales information of

commodities that are created by firm. Following report present the information related to Amana

ltd a family owned business in England, they usually sell souvenirs to travellers, currently due to

covid pandemic it has imposed challenges for businesses. Where uncertainty in economy has

impacted the growth of firm. This report will cover the monthly control report that will highlight

original, flexed budget. Furthermore, it will also cover the range of recommendation to

improvise services, it will also illustrate the information about whether company should go

online or not.

PART A

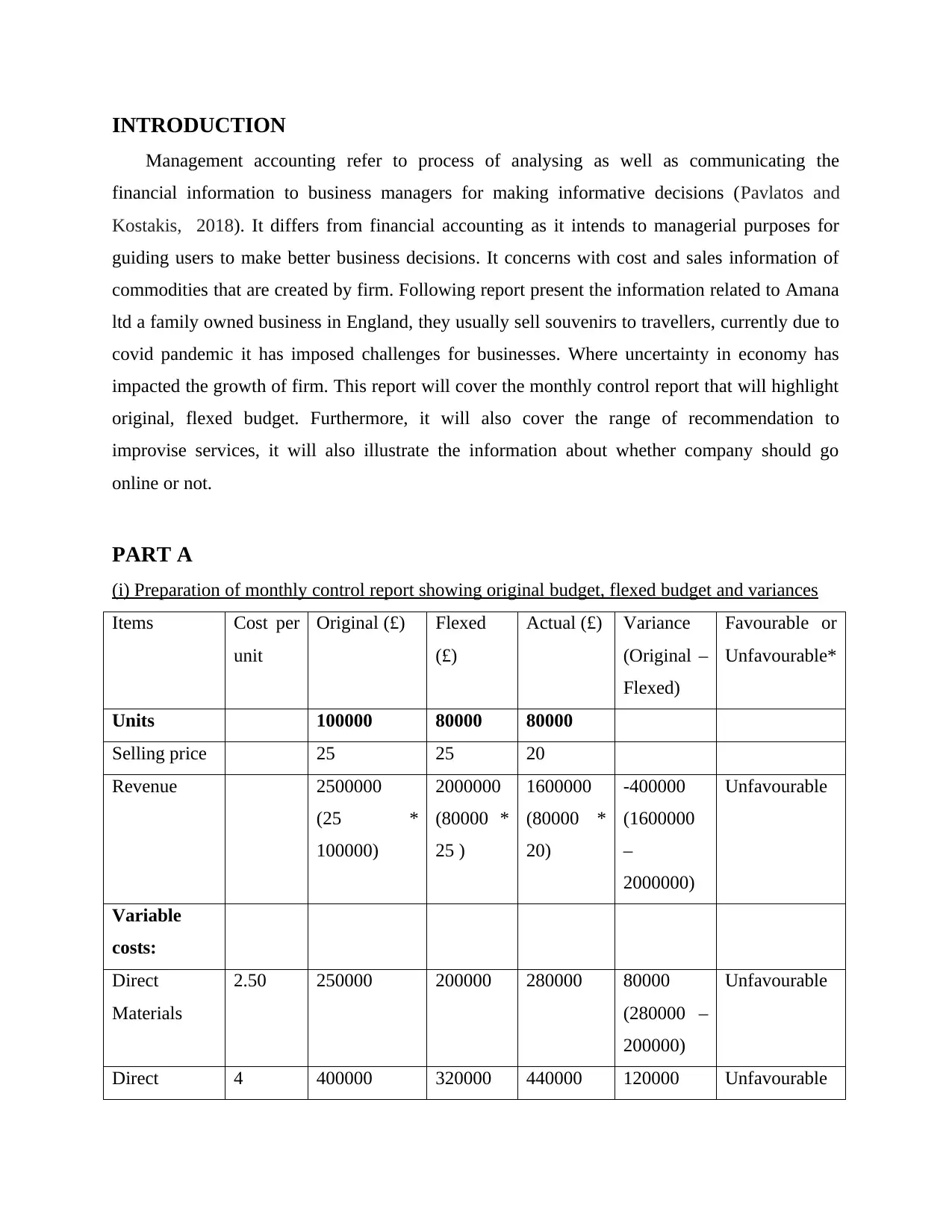

(i) Preparation of monthly control report showing original budget, flexed budget and variances

Items Cost per

unit

Original (£) Flexed

(£)

Actual (£) Variance

(Original –

Flexed)

Favourable or

Unfavourable*

Units 100000 80000 80000

Selling price 25 25 20

Revenue 2500000

(25 *

100000)

2000000

(80000 *

25 )

1600000

(80000 *

20)

-400000

(1600000

–

2000000)

Unfavourable

Variable

costs:

Direct

Materials

2.50 250000 200000 280000 80000

(280000 –

200000)

Unfavourable

Direct 4 400000 320000 440000 120000 Unfavourable

Management accounting refer to process of analysing as well as communicating the

financial information to business managers for making informative decisions (Pavlatos and

Kostakis, 2018). It differs from financial accounting as it intends to managerial purposes for

guiding users to make better business decisions. It concerns with cost and sales information of

commodities that are created by firm. Following report present the information related to Amana

ltd a family owned business in England, they usually sell souvenirs to travellers, currently due to

covid pandemic it has imposed challenges for businesses. Where uncertainty in economy has

impacted the growth of firm. This report will cover the monthly control report that will highlight

original, flexed budget. Furthermore, it will also cover the range of recommendation to

improvise services, it will also illustrate the information about whether company should go

online or not.

PART A

(i) Preparation of monthly control report showing original budget, flexed budget and variances

Items Cost per

unit

Original (£) Flexed

(£)

Actual (£) Variance

(Original –

Flexed)

Favourable or

Unfavourable*

Units 100000 80000 80000

Selling price 25 25 20

Revenue 2500000

(25 *

100000)

2000000

(80000 *

25 )

1600000

(80000 *

20)

-400000

(1600000

–

2000000)

Unfavourable

Variable

costs:

Direct

Materials

2.50 250000 200000 280000 80000

(280000 –

200000)

Unfavourable

Direct 4 400000 320000 440000 120000 Unfavourable

Labour (440000 –

320000)

Direct

Overhead

1.50 150000 120000 120000 0

(120000 –

120000)

-

Contributio

n

17 1700000 1360000 760000 600000

(760000 –

1360000)

Unfavourable

Fixed

Overheads:

Warehouse

rental

200000 200000 200000 170000 30000

(170000 –

200000)

Favourable

Insurance 100000 100000 100000 100000 0

(100000 –

100000)

-

Full time

warehouse

Supervisor

Salary

50000 50000 50000 35000 -15000

(35000 –

50000)

Favourable

Profit 1350000 1010000 455000 - 555000

(455000 –

1010000)

Unfavourable

Note* In case, if the actual revenue or income is higher than the expected income or revenue

than this leads to favourable variance. While on the other hand, if actual revenue is lower than

the expected revenue, than this indicate unfavourable variance.

On the other hand, if actual expenses are higher than flexed expenses than this indicate

unfavourable variance and if actual expenses are lower than the flexed expenses than this

indicate favourable variance.

320000)

Direct

Overhead

1.50 150000 120000 120000 0

(120000 –

120000)

-

Contributio

n

17 1700000 1360000 760000 600000

(760000 –

1360000)

Unfavourable

Fixed

Overheads:

Warehouse

rental

200000 200000 200000 170000 30000

(170000 –

200000)

Favourable

Insurance 100000 100000 100000 100000 0

(100000 –

100000)

-

Full time

warehouse

Supervisor

Salary

50000 50000 50000 35000 -15000

(35000 –

50000)

Favourable

Profit 1350000 1010000 455000 - 555000

(455000 –

1010000)

Unfavourable

Note* In case, if the actual revenue or income is higher than the expected income or revenue

than this leads to favourable variance. While on the other hand, if actual revenue is lower than

the expected revenue, than this indicate unfavourable variance.

On the other hand, if actual expenses are higher than flexed expenses than this indicate

unfavourable variance and if actual expenses are lower than the flexed expenses than this

indicate favourable variance.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(ii) Presenting report on performance of Amana’s company during the year 2020 using the

control report prepared above

On the basis of monthly control report it is found that revenue statement for the company is

unfavourable as they didn’t get the expected result with their implemented strategies. It is found

that before covid company was making good revenues but after uncertainty in economy due to

pandemic it has imposed potential challenges for growth of business. As their original budget for

the products was £2500000, and flexed budget was £2000000, actual budget £1600000, overall

variance value is seen as negative which specifies that company’s performance is not up to mark.

All conditions are unfavourable for them, therefore for that Amanda ltd firm need to reconsider

their project revenue by making modification in prices, volumes and process. Another way

which firm can proceed to undertake as to enhance their consumer demand by changing product

and increasing marketing budget for it.

Regarding direct materials which calculates the materials that is being purchased in some

duration to fulfil the requirements for production budget (Agustia, Sawarjuwono and Dianawati,

2019). For Amanda ltd this information is also unfavourable as due to improper market research

and other factors has imposed challenge for firm where they are not able to accomplish their

desired goal. Their original budget for direct materials was £250000 and flexed was £200000,

but they didn’t get the result which they have expected before implementation of their project.

Therefore, firm need to look into their strategies and to set it appropriately in order to sustain in

market.

Further, analysing the monthly control report of Amana Ltd. it has been identified that the

direct labour cost is unfavourable. It means the actual direct labour cost is higher than the flexed

cost. This indicate that the performance of company in the year 2020 is poor in term of labour

cost management and controlling. The company fails to manage and reduce the cost of labour in

the year 2020. It further requires the company to do some market research and adopt appropriate

strategy to enhance the performance of company (Rikhardsson and Yigitbasioglu, 2018).

However, on the other hand, it has been also identified from the above control report that there is

no gap or variance between the actual and flexed direct overhead cost. This is indicating the

good performance of Amana Ltd because the company management able to control the

overspending of overheads on the products and services. But the contribution of the company is

control report prepared above

On the basis of monthly control report it is found that revenue statement for the company is

unfavourable as they didn’t get the expected result with their implemented strategies. It is found

that before covid company was making good revenues but after uncertainty in economy due to

pandemic it has imposed potential challenges for growth of business. As their original budget for

the products was £2500000, and flexed budget was £2000000, actual budget £1600000, overall

variance value is seen as negative which specifies that company’s performance is not up to mark.

All conditions are unfavourable for them, therefore for that Amanda ltd firm need to reconsider

their project revenue by making modification in prices, volumes and process. Another way

which firm can proceed to undertake as to enhance their consumer demand by changing product

and increasing marketing budget for it.

Regarding direct materials which calculates the materials that is being purchased in some

duration to fulfil the requirements for production budget (Agustia, Sawarjuwono and Dianawati,

2019). For Amanda ltd this information is also unfavourable as due to improper market research

and other factors has imposed challenge for firm where they are not able to accomplish their

desired goal. Their original budget for direct materials was £250000 and flexed was £200000,

but they didn’t get the result which they have expected before implementation of their project.

Therefore, firm need to look into their strategies and to set it appropriately in order to sustain in

market.

Further, analysing the monthly control report of Amana Ltd. it has been identified that the

direct labour cost is unfavourable. It means the actual direct labour cost is higher than the flexed

cost. This indicate that the performance of company in the year 2020 is poor in term of labour

cost management and controlling. The company fails to manage and reduce the cost of labour in

the year 2020. It further requires the company to do some market research and adopt appropriate

strategy to enhance the performance of company (Rikhardsson and Yigitbasioglu, 2018).

However, on the other hand, it has been also identified from the above control report that there is

no gap or variance between the actual and flexed direct overhead cost. This is indicating the

good performance of Amana Ltd because the company management able to control the

overspending of overheads on the products and services. But the contribution of the company is

unfavourable. The company required to focus on their internal control system to meet the

expected standard of the budget.

Further, it has been also analysed from the monthly control report that in the year 2020

warehouse rental overheads are favourable. It means the actual expenses regarding the

warehouse rental of company is lower than the flexed expenses. This indicate the good

performance of company during the year 2020. It might be because the warehouse rental is a

fixed expense which remain constant over the period of year. So, the company get the chance to

adopt appropriate strategy to reduce the warehouse rental expenses of the company. This also

helps the company to manage the overall profitability of business. The insurance is also one of

the fixed expenses that company need to pay each year to protect the company profit or stock

from any natural disaster. After preparing and analysing the control report, it has been identified

that there is no gap or difference between the actual and flexed budget. This state that the

performance of company in term of managing overhead cost is good of Amana Ltd. However,

the company have earned profit during the year but the actual profit is lower than what they

expected or identified as per flexed budget (Johnstone, 2020).

Hence, on this basis, it is recommended to the company that they should adopt suitable

strategies to reduce the expenses and increase the sales revenue. To eliminate the gap or

variance, it is first important that company its impact on the performance of company properly.

For example, on the basis of the control report, it is identified that the actual supervisor salary of

company is lower during the year 2020 is lower as compared to flexed or budgeted amount. It

might be arising because of the increase in the wages and salary of warehouse supervisor. The

demand of supervisor has increased because of the other job opportunity (Alabdullah, 2022).

Hence, it is significant for the company to analyse each and every element of the budget which

are creating variance. After than the company able to adopt the appropriate strategies or ways to

reduce or eliminate the same.

The major reason of variance between the actual and budgeted is Covid-19 situation.

Uncertainties are the part of global pandemic which have created major difficulties of the

company to analyse and predict what is going to happen in future. Hence, this leads to variance

between actual and budgeted.

expected standard of the budget.

Further, it has been also analysed from the monthly control report that in the year 2020

warehouse rental overheads are favourable. It means the actual expenses regarding the

warehouse rental of company is lower than the flexed expenses. This indicate the good

performance of company during the year 2020. It might be because the warehouse rental is a

fixed expense which remain constant over the period of year. So, the company get the chance to

adopt appropriate strategy to reduce the warehouse rental expenses of the company. This also

helps the company to manage the overall profitability of business. The insurance is also one of

the fixed expenses that company need to pay each year to protect the company profit or stock

from any natural disaster. After preparing and analysing the control report, it has been identified

that there is no gap or difference between the actual and flexed budget. This state that the

performance of company in term of managing overhead cost is good of Amana Ltd. However,

the company have earned profit during the year but the actual profit is lower than what they

expected or identified as per flexed budget (Johnstone, 2020).

Hence, on this basis, it is recommended to the company that they should adopt suitable

strategies to reduce the expenses and increase the sales revenue. To eliminate the gap or

variance, it is first important that company its impact on the performance of company properly.

For example, on the basis of the control report, it is identified that the actual supervisor salary of

company is lower during the year 2020 is lower as compared to flexed or budgeted amount. It

might be arising because of the increase in the wages and salary of warehouse supervisor. The

demand of supervisor has increased because of the other job opportunity (Alabdullah, 2022).

Hence, it is significant for the company to analyse each and every element of the budget which

are creating variance. After than the company able to adopt the appropriate strategies or ways to

reduce or eliminate the same.

The major reason of variance between the actual and budgeted is Covid-19 situation.

Uncertainties are the part of global pandemic which have created major difficulties of the

company to analyse and predict what is going to happen in future. Hence, this leads to variance

between actual and budgeted.

(iii) Recommendations to Amana’s CEO on area of development

The major areas that require development in particular are mainly the budget

development as well as budget management in particular. For the reason of development as well

as enhancement in the future of the company in particular. Firstly, the company is required to

conduct training programs for the employees of the company in particular. Training programs or

training sessions mainly will help or support the new as well as the existing employees of the

company to learn and develop skills that will enhance their calibre to prepare the most suitable

and most appropriate budgets for the operations that are to be conducted by the company. And

also, these budgets or the financial resources that are specified by the company for certain tasks

or activities need to be used in a optimum way and not be wasted at all.

The company should also start preparing flexible budget rather than preparing static

budget in particular (Oyadomari. And et.al., 2018). The flexible budget will enable the company

to pursue better and new opportunities present in the external environment which will positively

impact the growth of the company. This will also allow in the procedure of mitigation of risks in

particular. The flexible budgeting technique will also reflect the situation or the state of the

finances and financial transactions of the business more accurately. Further it will also support in

profit, costs and sales calculation at various levels of the operating capacity in particular.

Whereas, static budgeting will not support such things.

The company should also, come in forward contracts to make the amount of direct

materials favourable. This means, the company should decide an amount which is to be given to

the supplier in return to the supplies and continue to give the same amount to the supplier, even

if there is change in the market price of the goods supplied.

PART B

1. Advise to Mr Amana’s on decision either set up their own online shop or sell on Amazon

Before making any decision for Amana, firstly it is important to look at the cost the company

will incur in both the option.

First option: Setting up own online shop

Particulars Amount in £

No of units will be sold by company

(Guaranteed)

£2000000

(100000 * £20)

The major areas that require development in particular are mainly the budget

development as well as budget management in particular. For the reason of development as well

as enhancement in the future of the company in particular. Firstly, the company is required to

conduct training programs for the employees of the company in particular. Training programs or

training sessions mainly will help or support the new as well as the existing employees of the

company to learn and develop skills that will enhance their calibre to prepare the most suitable

and most appropriate budgets for the operations that are to be conducted by the company. And

also, these budgets or the financial resources that are specified by the company for certain tasks

or activities need to be used in a optimum way and not be wasted at all.

The company should also start preparing flexible budget rather than preparing static

budget in particular (Oyadomari. And et.al., 2018). The flexible budget will enable the company

to pursue better and new opportunities present in the external environment which will positively

impact the growth of the company. This will also allow in the procedure of mitigation of risks in

particular. The flexible budgeting technique will also reflect the situation or the state of the

finances and financial transactions of the business more accurately. Further it will also support in

profit, costs and sales calculation at various levels of the operating capacity in particular.

Whereas, static budgeting will not support such things.

The company should also, come in forward contracts to make the amount of direct

materials favourable. This means, the company should decide an amount which is to be given to

the supplier in return to the supplies and continue to give the same amount to the supplier, even

if there is change in the market price of the goods supplied.

PART B

1. Advise to Mr Amana’s on decision either set up their own online shop or sell on Amazon

Before making any decision for Amana, firstly it is important to look at the cost the company

will incur in both the option.

First option: Setting up own online shop

Particulars Amount in £

No of units will be sold by company

(Guaranteed)

£2000000

(100000 * £20)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

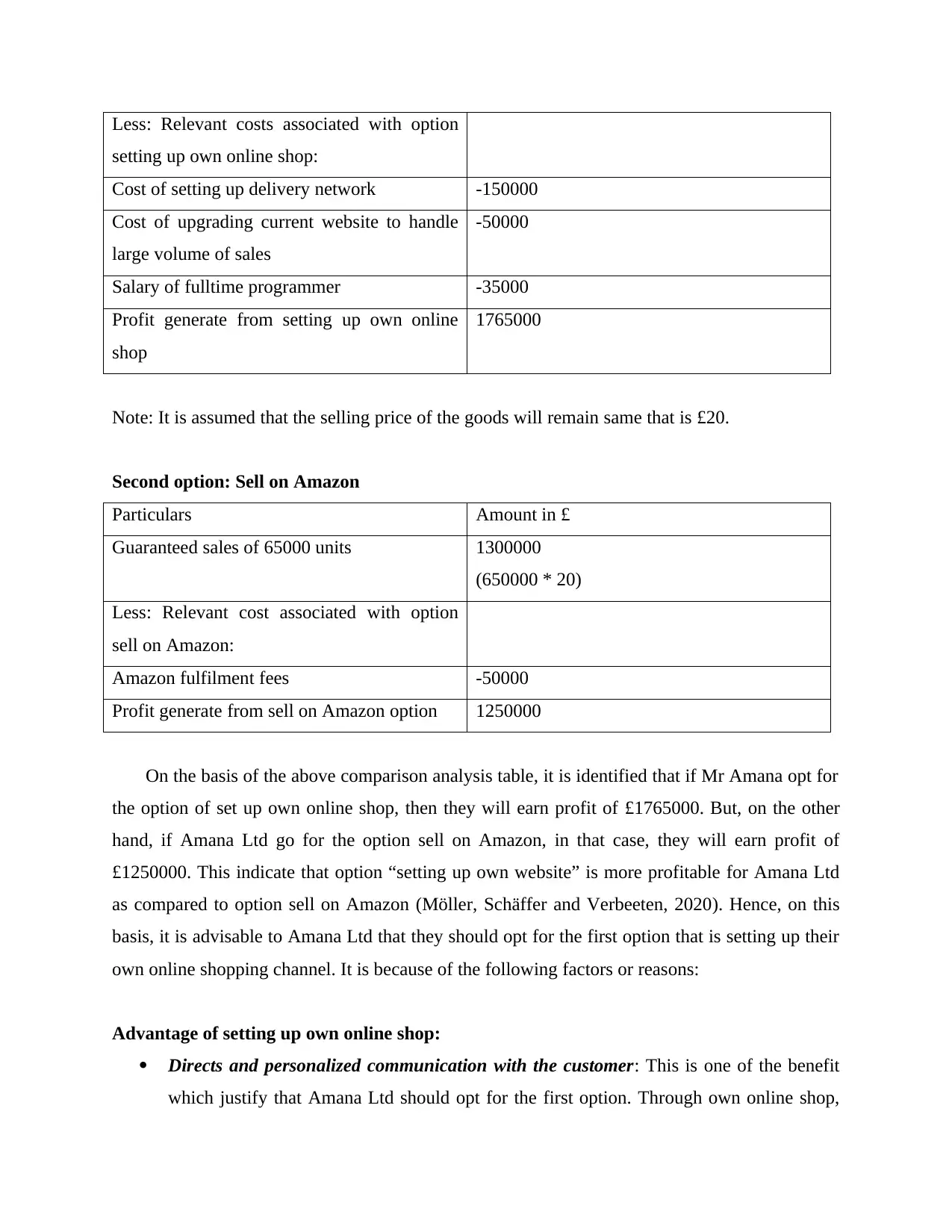

Less: Relevant costs associated with option

setting up own online shop:

Cost of setting up delivery network -150000

Cost of upgrading current website to handle

large volume of sales

-50000

Salary of fulltime programmer -35000

Profit generate from setting up own online

shop

1765000

Note: It is assumed that the selling price of the goods will remain same that is £20.

Second option: Sell on Amazon

Particulars Amount in £

Guaranteed sales of 65000 units 1300000

(650000 * 20)

Less: Relevant cost associated with option

sell on Amazon:

Amazon fulfilment fees -50000

Profit generate from sell on Amazon option 1250000

On the basis of the above comparison analysis table, it is identified that if Mr Amana opt for

the option of set up own online shop, then they will earn profit of £1765000. But, on the other

hand, if Amana Ltd go for the option sell on Amazon, in that case, they will earn profit of

£1250000. This indicate that option “setting up own website” is more profitable for Amana Ltd

as compared to option sell on Amazon (Möller, Schäffer and Verbeeten, 2020). Hence, on this

basis, it is advisable to Amana Ltd that they should opt for the first option that is setting up their

own online shopping channel. It is because of the following factors or reasons:

Advantage of setting up own online shop:

Directs and personalized communication with the customer: This is one of the benefit

which justify that Amana Ltd should opt for the first option. Through own online shop,

setting up own online shop:

Cost of setting up delivery network -150000

Cost of upgrading current website to handle

large volume of sales

-50000

Salary of fulltime programmer -35000

Profit generate from setting up own online

shop

1765000

Note: It is assumed that the selling price of the goods will remain same that is £20.

Second option: Sell on Amazon

Particulars Amount in £

Guaranteed sales of 65000 units 1300000

(650000 * 20)

Less: Relevant cost associated with option

sell on Amazon:

Amazon fulfilment fees -50000

Profit generate from sell on Amazon option 1250000

On the basis of the above comparison analysis table, it is identified that if Mr Amana opt for

the option of set up own online shop, then they will earn profit of £1765000. But, on the other

hand, if Amana Ltd go for the option sell on Amazon, in that case, they will earn profit of

£1250000. This indicate that option “setting up own website” is more profitable for Amana Ltd

as compared to option sell on Amazon (Möller, Schäffer and Verbeeten, 2020). Hence, on this

basis, it is advisable to Amana Ltd that they should opt for the first option that is setting up their

own online shopping channel. It is because of the following factors or reasons:

Advantage of setting up own online shop:

Directs and personalized communication with the customer: This is one of the benefit

which justify that Amana Ltd should opt for the first option. Through own online shop,

the company able to communicate with the customer directly and identify the issues they

are facing. After identification of customer concerns, the management of Amana Ltd able

to adopt appropriate strategies to solve customer issues. This is not possible in case of sell

through Amazon platform.

Improved customer loyalty and retention: If the company wants to improve their

customer loyalty and customer retention rate, in that case company should start selling

goods and service through own online shopping channel or application. The company

able to provide appropriate discounts and benefits to its customer which they unable to

provide through other online channels (Endenich and Trapp, 2020).

Full access to customer information: This is also one of the benefit of setting up own

online channel which indicate that through own online shop, Amana Ltd able to get

access to its customer information. This information is further used by the company to

personalized the products and service of its company as per the needs and expectation of

customers.

Faster dispute solutions: As compared to sell on Amazon option, the management team

of Amana Ltd able to solve the disputes of customer through own online shop quickly

and easily (Korhonen and et.al., 2020). The customers want immediate response

regarding their issue from its supplier which is only possible in case of first option.

Hence, it is recommended to Amana Ltd that they should opt for the first option such as

setting up own online shop.

However, on the other hand, it is also significant for Amana Ltd to understand that setting up

own online shop is quite time consuming and costly process. In case if appropriate benefits is not

returned from this option than it may leads to heavy loss to company. Hence, before adopting

this decision proper customer survey should be conducted to assess the market demand and

expectations of customer (Gunarathne, Lee and Hitigala Kaluarachchilage, 2021).

Cons of using other methods:

Online selling is one of the most challenging task in the business, company need to have

budget, online knowledge and certain other type of factors to ensure success. Amana Ltd is

planning to introduce their own online platform which can be used as means of online shop.

are facing. After identification of customer concerns, the management of Amana Ltd able

to adopt appropriate strategies to solve customer issues. This is not possible in case of sell

through Amazon platform.

Improved customer loyalty and retention: If the company wants to improve their

customer loyalty and customer retention rate, in that case company should start selling

goods and service through own online shopping channel or application. The company

able to provide appropriate discounts and benefits to its customer which they unable to

provide through other online channels (Endenich and Trapp, 2020).

Full access to customer information: This is also one of the benefit of setting up own

online channel which indicate that through own online shop, Amana Ltd able to get

access to its customer information. This information is further used by the company to

personalized the products and service of its company as per the needs and expectation of

customers.

Faster dispute solutions: As compared to sell on Amazon option, the management team

of Amana Ltd able to solve the disputes of customer through own online shop quickly

and easily (Korhonen and et.al., 2020). The customers want immediate response

regarding their issue from its supplier which is only possible in case of first option.

Hence, it is recommended to Amana Ltd that they should opt for the first option such as

setting up own online shop.

However, on the other hand, it is also significant for Amana Ltd to understand that setting up

own online shop is quite time consuming and costly process. In case if appropriate benefits is not

returned from this option than it may leads to heavy loss to company. Hence, before adopting

this decision proper customer survey should be conducted to assess the market demand and

expectations of customer (Gunarathne, Lee and Hitigala Kaluarachchilage, 2021).

Cons of using other methods:

Online selling is one of the most challenging task in the business, company need to have

budget, online knowledge and certain other type of factors to ensure success. Amana Ltd is

planning to introduce their own online platform which can be used as means of online shop.

However, if they are planning to consider other methods these may include certain type of

disadvantages, these are:

Costly: Affiliating with E-commerce and other platform is costly, company need to provide

commission and other charges to sell products on these platform. Amana Ltd need to

prefer their own online shop or platform which can be reached by every audience, they

need to avoid E-commerce platform to save their marginal cost. Affiliation may include

certain type of charges, if Amana Ltd is planning to discount their products then they will

unable to over extra cost, it is better to start an online shop which is far better for future

growth as well.

Competition: This is one of the most common but important factor in which company face

competition from similar range products, E-commerce platform like Amazon welcome

every business organization to list and sell their product, which means competitors will

be active on these platform and will impact firms online performance. However, it

completely depends on type of marketing adopted by the business organization while

considering E-commerce platform. Competition arrive when this E-commerce platform

provide opportunity to competitors. For example; if competitor increase the rate of

commission then E-commerce platform will increase their visibility on the platform.

disadvantages, these are:

Costly: Affiliating with E-commerce and other platform is costly, company need to provide

commission and other charges to sell products on these platform. Amana Ltd need to

prefer their own online shop or platform which can be reached by every audience, they

need to avoid E-commerce platform to save their marginal cost. Affiliation may include

certain type of charges, if Amana Ltd is planning to discount their products then they will

unable to over extra cost, it is better to start an online shop which is far better for future

growth as well.

Competition: This is one of the most common but important factor in which company face

competition from similar range products, E-commerce platform like Amazon welcome

every business organization to list and sell their product, which means competitors will

be active on these platform and will impact firms online performance. However, it

completely depends on type of marketing adopted by the business organization while

considering E-commerce platform. Competition arrive when this E-commerce platform

provide opportunity to competitors. For example; if competitor increase the rate of

commission then E-commerce platform will increase their visibility on the platform.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

From the above report it has been concluded that having proper management accounting

helps the businesses to make growth decisions and with this firms could easily view their actual

performance versus their future goals and objectives. Above report has illustrated the discussion

about requirement of management accounting, it also discussed the case study where firm is

looking for to get back their position in market again which is affected by covid pandemic. It has

illustrated the Information regarding monthly control report for firm that highlighted flexed

budget and variances, furthermore have discussed recommendations for business. Report lastly

concluded with the description about analysis of decision to go online, it also illustrated the

suggestions whether to establish own shop or to sell product through Amazon.

From the above report it has been concluded that having proper management accounting

helps the businesses to make growth decisions and with this firms could easily view their actual

performance versus their future goals and objectives. Above report has illustrated the discussion

about requirement of management accounting, it also discussed the case study where firm is

looking for to get back their position in market again which is affected by covid pandemic. It has

illustrated the Information regarding monthly control report for firm that highlighted flexed

budget and variances, furthermore have discussed recommendations for business. Report lastly

concluded with the description about analysis of decision to go online, it also illustrated the

suggestions whether to establish own shop or to sell product through Amazon.

REFERENCES

Books and journals

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Johnstone, L., 2020. A systematic analysis of environmental management systems in SMEs:

Possible research directions from a management accounting and control stance. Journal

of Cleaner Production. 244. p.118802.

Alabdullah, T. T. Y., 2022. Management accounting insight via a new perspective on risk

management-companies' profitability relationship. International Journal of Intelligent

Enterprise. 9(2). pp.244-257.

Möller, K., Schäffer, U. and Verbeeten, F., 2020. Digitalization in management accounting and

control: an editorial. Journal of Management Control. 31(1). pp.1-8.

Endenich, C. and Trapp, R., 2020. Ethical implications of management accounting and control:

A systematic review of the contributions from the Journal of Business Ethics. Journal of

Business Ethics. 163(2). pp.309-328.

Korhonen, T. and et.al., 2020. Exploring the programmability of management accounting work

for increasing automation: an interventionist case study. Accounting, Auditing &

Accountability Journal.

Gunarathne, A. N., Lee, K. H. and Hitigala Kaluarachchilage, P. K., 2021. Institutional

pressures, environmental management strategy, and organizational performance: The role

of environmental management accounting. Business Strategy and the Environment. 30(2).

pp.825-839.

Oyadomari, J.C.T. And et.al., 2018. Flexible budgeting influence on organizational inertia and

flexibility. International Journal of Productivity and Performance Management.

Agustia, D., Sawarjuwono, T. and Dianawati, W., 2019. The mediating effect of environmental

management accounting on green innovation-Firm value relationship. International

Journal of Energy Economics and Policy. 9(2). pp.299-306.

Pavlatos, O. and Kostakis, X., 2018. The impact of top management team characteristics and

historical financial performance on strategic management accounting. Journal of

Accounting & organizational change.

1

Books and journals

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Johnstone, L., 2020. A systematic analysis of environmental management systems in SMEs:

Possible research directions from a management accounting and control stance. Journal

of Cleaner Production. 244. p.118802.

Alabdullah, T. T. Y., 2022. Management accounting insight via a new perspective on risk

management-companies' profitability relationship. International Journal of Intelligent

Enterprise. 9(2). pp.244-257.

Möller, K., Schäffer, U. and Verbeeten, F., 2020. Digitalization in management accounting and

control: an editorial. Journal of Management Control. 31(1). pp.1-8.

Endenich, C. and Trapp, R., 2020. Ethical implications of management accounting and control:

A systematic review of the contributions from the Journal of Business Ethics. Journal of

Business Ethics. 163(2). pp.309-328.

Korhonen, T. and et.al., 2020. Exploring the programmability of management accounting work

for increasing automation: an interventionist case study. Accounting, Auditing &

Accountability Journal.

Gunarathne, A. N., Lee, K. H. and Hitigala Kaluarachchilage, P. K., 2021. Institutional

pressures, environmental management strategy, and organizational performance: The role

of environmental management accounting. Business Strategy and the Environment. 30(2).

pp.825-839.

Oyadomari, J.C.T. And et.al., 2018. Flexible budgeting influence on organizational inertia and

flexibility. International Journal of Productivity and Performance Management.

Agustia, D., Sawarjuwono, T. and Dianawati, W., 2019. The mediating effect of environmental

management accounting on green innovation-Firm value relationship. International

Journal of Energy Economics and Policy. 9(2). pp.299-306.

Pavlatos, O. and Kostakis, X., 2018. The impact of top management team characteristics and

historical financial performance on strategic management accounting. Journal of

Accounting & organizational change.

1

2

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.