Management Accounting: Budgetary Control Report and Recommendations for Improvement

VerifiedAdded on 2023/06/07

|11

|3105

|166

AI Summary

This report discusses budgetary control and variance analysis for Amana's company, along with recommendations for improvement. It also analyzes the performance of the organization during the year 2020. Additionally, it suggests moving towards online sales through own online shops.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART-A...........................................................................................................................................3

1) Preparation of monthly control report showing flexed budget, original budget, variances-...3

2) Report showing performance of the organization during the year 2020-................................4

3) Recommendation to the CEO of Amana's CEO for making improvement-...........................6

PART B............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

PART-A...........................................................................................................................................3

1) Preparation of monthly control report showing flexed budget, original budget, variances-...3

2) Report showing performance of the organization during the year 2020-................................4

3) Recommendation to the CEO of Amana's CEO for making improvement-...........................6

PART B............................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting can be defined as an accounting practise which is used by

organizations in order to drive better understaffing to management so can make more drastic and

rational decisions. The report is aimed to discuss different notions such as budgetary control and

variance analysis, at the same time, some sets of recommendations are supposed to be extended

in attempt to hike the organizational performance. At the end of the report, a severe comparison

would be made between the available strategies for the organization and making an intensive

comparison so can guide the decision of Mr. Amana (Shefren, et. al. 2021)

Management accounting is having its great role in the installation of efficient

management at any organization. As it could be deciphered in the case of Amana's company

where it was intended to abide with pre intended outcomes but could not succeed and ultimately

ended up with sort of loss generation. The report will be discussing these all elements to the

fullest extend substantiating with the undertaken case.

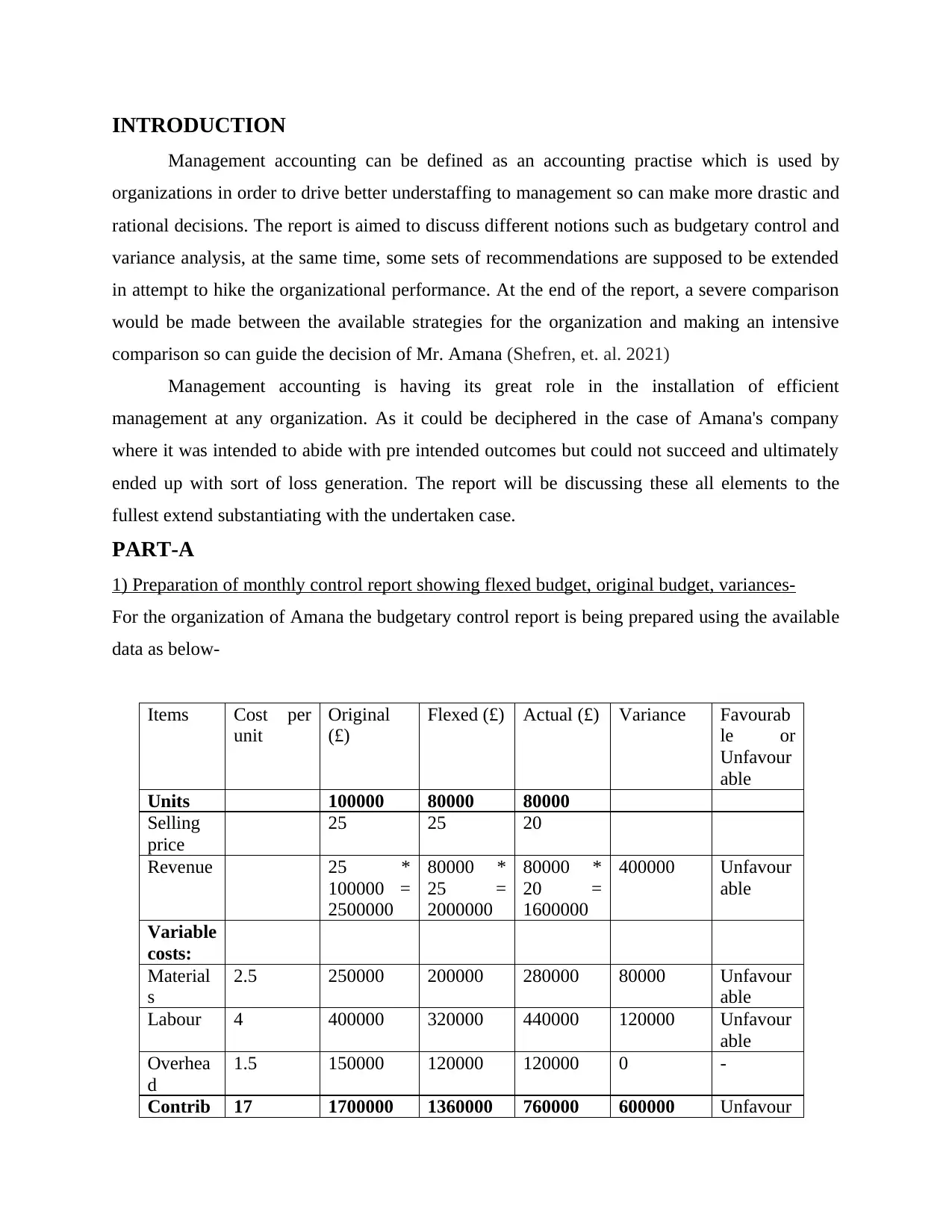

PART-A

1) Preparation of monthly control report showing flexed budget, original budget, variances-

For the organization of Amana the budgetary control report is being prepared using the available

data as below-

Items Cost per

unit

Original

(£)

Flexed (£) Actual (£) Variance Favourab

le or

Unfavour

able

Units 100000 80000 80000

Selling

price

25 25 20

Revenue 25 *

100000 =

2500000

80000 *

25 =

2000000

80000 *

20 =

1600000

400000 Unfavour

able

Variable

costs:

Material

s

2.5 250000 200000 280000 80000 Unfavour

able

Labour 4 400000 320000 440000 120000 Unfavour

able

Overhea

d

1.5 150000 120000 120000 0 -

Contrib 17 1700000 1360000 760000 600000 Unfavour

Management accounting can be defined as an accounting practise which is used by

organizations in order to drive better understaffing to management so can make more drastic and

rational decisions. The report is aimed to discuss different notions such as budgetary control and

variance analysis, at the same time, some sets of recommendations are supposed to be extended

in attempt to hike the organizational performance. At the end of the report, a severe comparison

would be made between the available strategies for the organization and making an intensive

comparison so can guide the decision of Mr. Amana (Shefren, et. al. 2021)

Management accounting is having its great role in the installation of efficient

management at any organization. As it could be deciphered in the case of Amana's company

where it was intended to abide with pre intended outcomes but could not succeed and ultimately

ended up with sort of loss generation. The report will be discussing these all elements to the

fullest extend substantiating with the undertaken case.

PART-A

1) Preparation of monthly control report showing flexed budget, original budget, variances-

For the organization of Amana the budgetary control report is being prepared using the available

data as below-

Items Cost per

unit

Original

(£)

Flexed (£) Actual (£) Variance Favourab

le or

Unfavour

able

Units 100000 80000 80000

Selling

price

25 25 20

Revenue 25 *

100000 =

2500000

80000 *

25 =

2000000

80000 *

20 =

1600000

400000 Unfavour

able

Variable

costs:

Material

s

2.5 250000 200000 280000 80000 Unfavour

able

Labour 4 400000 320000 440000 120000 Unfavour

able

Overhea

d

1.5 150000 120000 120000 0 -

Contrib 17 1700000 1360000 760000 600000 Unfavour

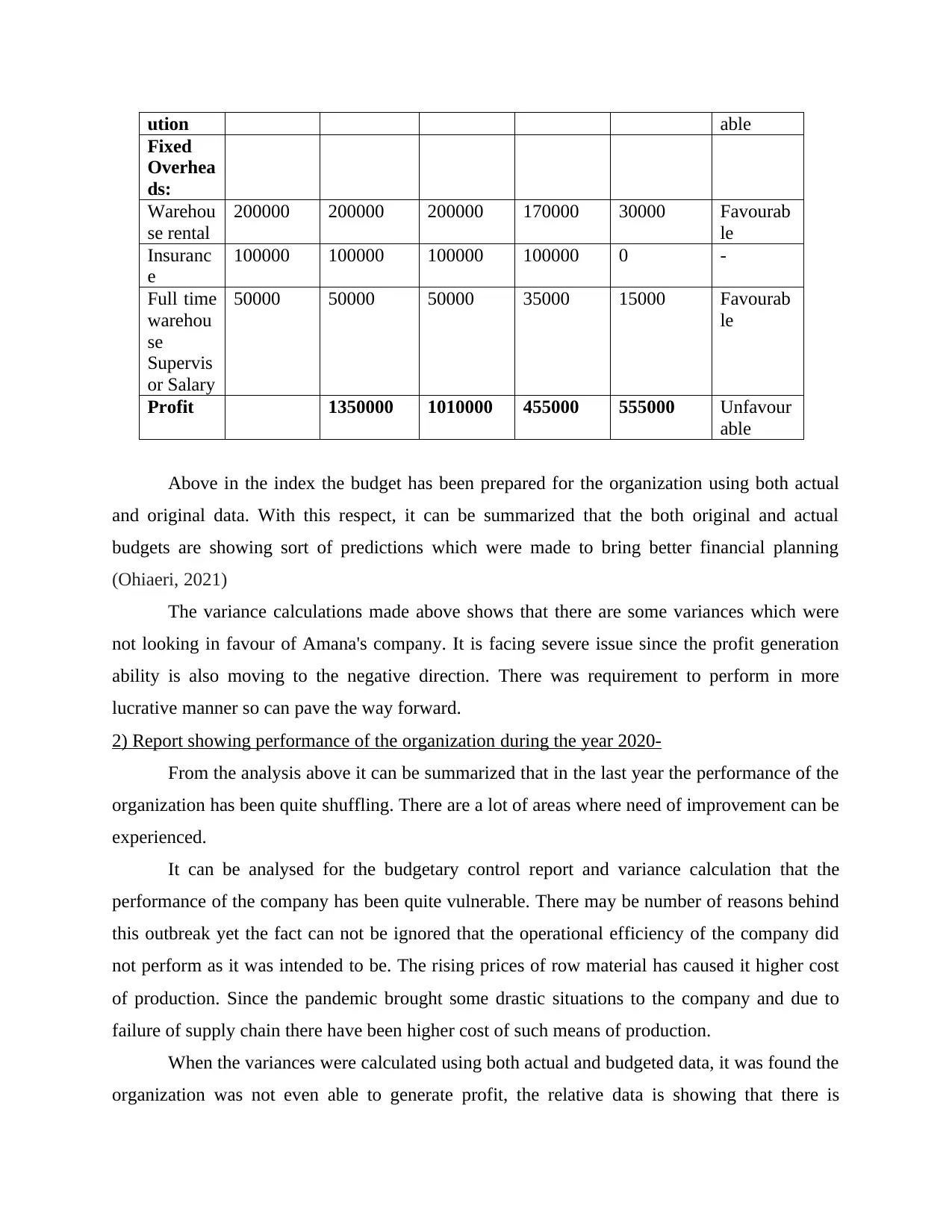

ution able

Fixed

Overhea

ds:

Warehou

se rental

200000 200000 200000 170000 30000 Favourab

le

Insuranc

e

100000 100000 100000 100000 0 -

Full time

warehou

se

Supervis

or Salary

50000 50000 50000 35000 15000 Favourab

le

Profit 1350000 1010000 455000 555000 Unfavour

able

Above in the index the budget has been prepared for the organization using both actual

and original data. With this respect, it can be summarized that the both original and actual

budgets are showing sort of predictions which were made to bring better financial planning

(Ohiaeri, 2021)

The variance calculations made above shows that there are some variances which were

not looking in favour of Amana's company. It is facing severe issue since the profit generation

ability is also moving to the negative direction. There was requirement to perform in more

lucrative manner so can pave the way forward.

2) Report showing performance of the organization during the year 2020-

From the analysis above it can be summarized that in the last year the performance of the

organization has been quite shuffling. There are a lot of areas where need of improvement can be

experienced.

It can be analysed for the budgetary control report and variance calculation that the

performance of the company has been quite vulnerable. There may be number of reasons behind

this outbreak yet the fact can not be ignored that the operational efficiency of the company did

not perform as it was intended to be. The rising prices of row material has caused it higher cost

of production. Since the pandemic brought some drastic situations to the company and due to

failure of supply chain there have been higher cost of such means of production.

When the variances were calculated using both actual and budgeted data, it was found the

organization was not even able to generate profit, the relative data is showing that there is

Fixed

Overhea

ds:

Warehou

se rental

200000 200000 200000 170000 30000 Favourab

le

Insuranc

e

100000 100000 100000 100000 0 -

Full time

warehou

se

Supervis

or Salary

50000 50000 50000 35000 15000 Favourab

le

Profit 1350000 1010000 455000 555000 Unfavour

able

Above in the index the budget has been prepared for the organization using both actual

and original data. With this respect, it can be summarized that the both original and actual

budgets are showing sort of predictions which were made to bring better financial planning

(Ohiaeri, 2021)

The variance calculations made above shows that there are some variances which were

not looking in favour of Amana's company. It is facing severe issue since the profit generation

ability is also moving to the negative direction. There was requirement to perform in more

lucrative manner so can pave the way forward.

2) Report showing performance of the organization during the year 2020-

From the analysis above it can be summarized that in the last year the performance of the

organization has been quite shuffling. There are a lot of areas where need of improvement can be

experienced.

It can be analysed for the budgetary control report and variance calculation that the

performance of the company has been quite vulnerable. There may be number of reasons behind

this outbreak yet the fact can not be ignored that the operational efficiency of the company did

not perform as it was intended to be. The rising prices of row material has caused it higher cost

of production. Since the pandemic brought some drastic situations to the company and due to

failure of supply chain there have been higher cost of such means of production.

When the variances were calculated using both actual and budgeted data, it was found the

organization was not even able to generate profit, the relative data is showing that there is

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

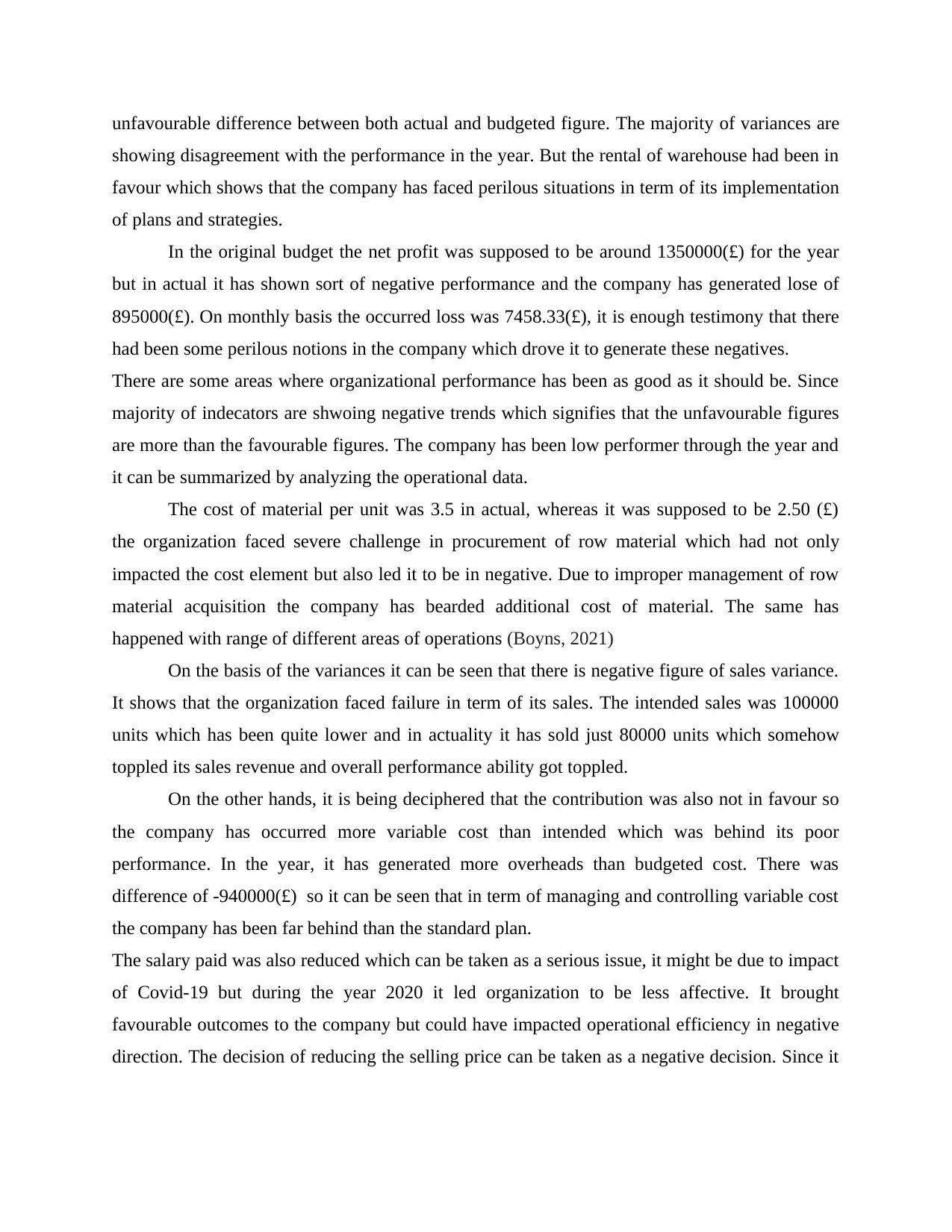

unfavourable difference between both actual and budgeted figure. The majority of variances are

showing disagreement with the performance in the year. But the rental of warehouse had been in

favour which shows that the company has faced perilous situations in term of its implementation

of plans and strategies.

In the original budget the net profit was supposed to be around 1350000(£) for the year

but in actual it has shown sort of negative performance and the company has generated lose of

895000(£). On monthly basis the occurred loss was 7458.33(£), it is enough testimony that there

had been some perilous notions in the company which drove it to generate these negatives.

There are some areas where organizational performance has been as good as it should be. Since

majority of indecators are shwoing negative trends which signifies that the unfavourable figures

are more than the favourable figures. The company has been low performer through the year and

it can be summarized by analyzing the operational data.

The cost of material per unit was 3.5 in actual, whereas it was supposed to be 2.50 (£)

the organization faced severe challenge in procurement of row material which had not only

impacted the cost element but also led it to be in negative. Due to improper management of row

material acquisition the company has bearded additional cost of material. The same has

happened with range of different areas of operations (Boyns, 2021)

On the basis of the variances it can be seen that there is negative figure of sales variance.

It shows that the organization faced failure in term of its sales. The intended sales was 100000

units which has been quite lower and in actuality it has sold just 80000 units which somehow

toppled its sales revenue and overall performance ability got toppled.

On the other hands, it is being deciphered that the contribution was also not in favour so

the company has occurred more variable cost than intended which was behind its poor

performance. In the year, it has generated more overheads than budgeted cost. There was

difference of -940000(£) so it can be seen that in term of managing and controlling variable cost

the company has been far behind than the standard plan.

The salary paid was also reduced which can be taken as a serious issue, it might be due to impact

of Covid-19 but during the year 2020 it led organization to be less affective. It brought

favourable outcomes to the company but could have impacted operational efficiency in negative

direction. The decision of reducing the selling price can be taken as a negative decision. Since it

showing disagreement with the performance in the year. But the rental of warehouse had been in

favour which shows that the company has faced perilous situations in term of its implementation

of plans and strategies.

In the original budget the net profit was supposed to be around 1350000(£) for the year

but in actual it has shown sort of negative performance and the company has generated lose of

895000(£). On monthly basis the occurred loss was 7458.33(£), it is enough testimony that there

had been some perilous notions in the company which drove it to generate these negatives.

There are some areas where organizational performance has been as good as it should be. Since

majority of indecators are shwoing negative trends which signifies that the unfavourable figures

are more than the favourable figures. The company has been low performer through the year and

it can be summarized by analyzing the operational data.

The cost of material per unit was 3.5 in actual, whereas it was supposed to be 2.50 (£)

the organization faced severe challenge in procurement of row material which had not only

impacted the cost element but also led it to be in negative. Due to improper management of row

material acquisition the company has bearded additional cost of material. The same has

happened with range of different areas of operations (Boyns, 2021)

On the basis of the variances it can be seen that there is negative figure of sales variance.

It shows that the organization faced failure in term of its sales. The intended sales was 100000

units which has been quite lower and in actuality it has sold just 80000 units which somehow

toppled its sales revenue and overall performance ability got toppled.

On the other hands, it is being deciphered that the contribution was also not in favour so

the company has occurred more variable cost than intended which was behind its poor

performance. In the year, it has generated more overheads than budgeted cost. There was

difference of -940000(£) so it can be seen that in term of managing and controlling variable cost

the company has been far behind than the standard plan.

The salary paid was also reduced which can be taken as a serious issue, it might be due to impact

of Covid-19 but during the year 2020 it led organization to be less affective. It brought

favourable outcomes to the company but could have impacted operational efficiency in negative

direction. The decision of reducing the selling price can be taken as a negative decision. Since it

was supposed to keep it aligning with the planned or budgeted plan. But due to impact of Covid-

19 the decision might be made to topple the prices in order to hike sales (Ayorekire, 2018)

This decision of the company did not favour it and ultimately caused it lower sales and

lower revenues. It fetched negatives in bot ways. On the basis of the decision it would be fair

enough to articulate that the organizational efficiency has been lower and quite disappointing in

the year which had pointed out its poor areas.

3) Recommendation to the CEO of Amana's CEO for making improvement-

On the basis of the analysis made above it can be concluded that the performance was not

as good as it was intended to be so keeping the loose performance of the organization there are

some suggestions for the management so can go for betterment and enhancement in its overall

operations.

There is strong need to work on the management and control of overheads. Since with the

progress of time, the organizations are more likely to generate more overheads. The share of

overhead in the total cost is being growing with the progress of time. Here, the management of

the firm are recommended to install sort of new technique to manage and control the overheads.

It would somehow give it edge and would enable the organization in enhancement of revenues.

As it was found, in the year 2020 the overheads were running over the intended amount. It can

not be bearded by the company (Mohamed, 2022)

At the same time, the variance shoring contribution was also negative. There is need to

work on escalation of sales. As it was intended that around one lac units would be sold but in

reality it has just sold 80000 units. Which might have caused it negative repercussions and it has

generated sort of negative contribution. With this respect, the organization is recommended to

work on its operational efficiency. There are rigours requirements to manage the sales along with

its selling price. The management may go for better promotional strategies so can fulfil its

requirements in term of profit generation.

The warehouse costs had been quite higher which was totally unintended and which did

not only impacted the profitability but also brought sort of negative impacts on operational

performance. There was need to predict it as appropriate as much possible but it could have gone

wrong. It is recommended that there must be a fully fledged plan to manage the warehouse cost

or any such cost which can not be controlled intensively (Dauda, 2019)

19 the decision might be made to topple the prices in order to hike sales (Ayorekire, 2018)

This decision of the company did not favour it and ultimately caused it lower sales and

lower revenues. It fetched negatives in bot ways. On the basis of the decision it would be fair

enough to articulate that the organizational efficiency has been lower and quite disappointing in

the year which had pointed out its poor areas.

3) Recommendation to the CEO of Amana's CEO for making improvement-

On the basis of the analysis made above it can be concluded that the performance was not

as good as it was intended to be so keeping the loose performance of the organization there are

some suggestions for the management so can go for betterment and enhancement in its overall

operations.

There is strong need to work on the management and control of overheads. Since with the

progress of time, the organizations are more likely to generate more overheads. The share of

overhead in the total cost is being growing with the progress of time. Here, the management of

the firm are recommended to install sort of new technique to manage and control the overheads.

It would somehow give it edge and would enable the organization in enhancement of revenues.

As it was found, in the year 2020 the overheads were running over the intended amount. It can

not be bearded by the company (Mohamed, 2022)

At the same time, the variance shoring contribution was also negative. There is need to

work on escalation of sales. As it was intended that around one lac units would be sold but in

reality it has just sold 80000 units. Which might have caused it negative repercussions and it has

generated sort of negative contribution. With this respect, the organization is recommended to

work on its operational efficiency. There are rigours requirements to manage the sales along with

its selling price. The management may go for better promotional strategies so can fulfil its

requirements in term of profit generation.

The warehouse costs had been quite higher which was totally unintended and which did

not only impacted the profitability but also brought sort of negative impacts on operational

performance. There was need to predict it as appropriate as much possible but it could have gone

wrong. It is recommended that there must be a fully fledged plan to manage the warehouse cost

or any such cost which can not be controlled intensively (Dauda, 2019)

It was experienced that in term of management of row material, labour etc. the

organization accomplished a great control. So it would not be unfair to articulate that these costs

could have been controlled to more intense manner. Keeping this notion into focus, the entity is

recommended to have more inclination to these costs and may go for in-depth scrutiny in order

to bring hyper control and can minimize it to the fullest extent.

PART B

Mr. Amana a businessman who is engaged in offline sales of products is planning to

move towards online sales by selling 50% of production online. Online business is fast growing

and profitable platform of modern business. Online business enables company to gather

information about customers and their behaviour which would help organization to make

necessary changes in products to improve customer experience. This platform also reduces

marketing cost of company and exempts company from geographical limitations and attract

international clients (Taher, 2021). Along with benefits there are some drawbacks of online sales.

This reduces physical interaction with customers and initial cost of implementing online business

is costly. The online business would enable Amana to increase its sales volume and to increase

profit margin. In initial period this method may be costly but cost can be recovered over time by

reaching more customers and building strong and effective customer relationship by providing

online after sale service. The increase in competitive demands for both online and offline

business to increase market shares and profitability. Online business will enable company to

expand its business globally and enhance customer base. There are two alternatives of moving

into online platform.

Alt. 1 Cost through their own online shops

Particulars Amount (in £)

Cost of setting delivery network 150000

Cost of up gradation of current website 50000

Salary to IT programmer 35000

Total cost 235000

Guaranteed sales 100000 (units)

Cost per unit (235000/100000) £2.35

organization accomplished a great control. So it would not be unfair to articulate that these costs

could have been controlled to more intense manner. Keeping this notion into focus, the entity is

recommended to have more inclination to these costs and may go for in-depth scrutiny in order

to bring hyper control and can minimize it to the fullest extent.

PART B

Mr. Amana a businessman who is engaged in offline sales of products is planning to

move towards online sales by selling 50% of production online. Online business is fast growing

and profitable platform of modern business. Online business enables company to gather

information about customers and their behaviour which would help organization to make

necessary changes in products to improve customer experience. This platform also reduces

marketing cost of company and exempts company from geographical limitations and attract

international clients (Taher, 2021). Along with benefits there are some drawbacks of online sales.

This reduces physical interaction with customers and initial cost of implementing online business

is costly. The online business would enable Amana to increase its sales volume and to increase

profit margin. In initial period this method may be costly but cost can be recovered over time by

reaching more customers and building strong and effective customer relationship by providing

online after sale service. The increase in competitive demands for both online and offline

business to increase market shares and profitability. Online business will enable company to

expand its business globally and enhance customer base. There are two alternatives of moving

into online platform.

Alt. 1 Cost through their own online shops

Particulars Amount (in £)

Cost of setting delivery network 150000

Cost of up gradation of current website 50000

Salary to IT programmer 35000

Total cost 235000

Guaranteed sales 100000 (units)

Cost per unit (235000/100000) £2.35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alt. 2 Cost of selling through Amazon

Particulars Amount (in £)

Amazon fulfilment fees 50000

Guaranteed sales 65000 (units)

Cost per unit (50000/65000) £0.77

There are two methods of selecting project: financial considerations and non financial

considerations. Financial considerations includes mathematical or quantitative aspects which

affects the selection of appropriate project. Non financial considerations are qualitative factors

that are to be considered before selection of project. Financial consideration consists of various

techniques such as benefit/cost ratio, net present value, interest rate of return, opportunity cost,

payback period and discounted cash flow (Project selection methods, 2022). Non financial

considerations includes customer relationship, organizational strategy, etc. which doesn't include

any quantitative aspects. Both the aspects of selection will be considered before coming at any

conclusion regarding selection of appropriate alternative for Amana to move into online mode of

sales.

Financial consideration: Through financial consideration it can be analysed that per unit cost of

selling products through amazon is less than cost incurred by own online shops. The selling units

of own online shops are more than that by selling through amazon. But there is potential of

increase in selling of units through amazon depending on demand. This means that if there is

increase in demand for products of Amana on amazon then volume of sales through amazon will

also increase that is cost per unit will decrease according to increase in sales volume (Zwikael

and Meredith, 2019). As per the quantitative scenario it will be beneficial for company to move

towards online sales through amazon. The difference in per unit cost of both alternatives is £1.58

(2.35-0.77) which is favourable if sold through amazon. On the other hand the volume of sales is

more in own online shops by 35000 (100000-65000) this encourages to sale through own online

shops. But it is mentioned that company has potential of increase in sales volume through

amazon if there is increase in demand. It can be assumed that there may be increase in sales

Particulars Amount (in £)

Amazon fulfilment fees 50000

Guaranteed sales 65000 (units)

Cost per unit (50000/65000) £0.77

There are two methods of selecting project: financial considerations and non financial

considerations. Financial considerations includes mathematical or quantitative aspects which

affects the selection of appropriate project. Non financial considerations are qualitative factors

that are to be considered before selection of project. Financial consideration consists of various

techniques such as benefit/cost ratio, net present value, interest rate of return, opportunity cost,

payback period and discounted cash flow (Project selection methods, 2022). Non financial

considerations includes customer relationship, organizational strategy, etc. which doesn't include

any quantitative aspects. Both the aspects of selection will be considered before coming at any

conclusion regarding selection of appropriate alternative for Amana to move into online mode of

sales.

Financial consideration: Through financial consideration it can be analysed that per unit cost of

selling products through amazon is less than cost incurred by own online shops. The selling units

of own online shops are more than that by selling through amazon. But there is potential of

increase in selling of units through amazon depending on demand. This means that if there is

increase in demand for products of Amana on amazon then volume of sales through amazon will

also increase that is cost per unit will decrease according to increase in sales volume (Zwikael

and Meredith, 2019). As per the quantitative scenario it will be beneficial for company to move

towards online sales through amazon. The difference in per unit cost of both alternatives is £1.58

(2.35-0.77) which is favourable if sold through amazon. On the other hand the volume of sales is

more in own online shops by 35000 (100000-65000) this encourages to sale through own online

shops. But it is mentioned that company has potential of increase in sales volume through

amazon if there is increase in demand. It can be assumed that there may be increase in sales

volume which ultimately suggest to choice 2nd alternative as increase in sales will decrease per

unit cost.

Non financial consideration: Before taking any decision it is essential to look into all the aspects

that may impact the decision. In accordance to non financial aspect it is better to move into

online mode of sales through amazon but every coin has two sides (Alvarenga and et.al., 2018).

The another aspect of reaching a decision is qualitative aspect. Sales through amazon will

adversely affect the control over pricing and return policy of company. There will be lack of

control over price of product as price may be set by amazon and company has to agree with the

same as it will enter into contract. The return policy of company will also be affected through

this alternative. The company will not be able to build direct relationship with its customers if it

sells its products through amazon and this may impact its future operations as building and

maintaining strong customer relationship is very essential for an organization.

From above, it can be recommended that company is required to ascertain which

consideration is more beneficial for sustainable growth and development of business. For the

long term profit and development of business it will be better for company to select first

alternative i.e. set up its own online shop (Xue and et.al., 2020). In the initial period it may be

cost effective but when the demand for product will raise it would ultimately reduce per unit cost

to company and it will also ensure control over price and return policy. Company will also be

able to build direct relationship with its customers and would be able to understand needs and

preferences of customers.

CONCLUSION

The project is related to management accounting which includes control report showing

original budget, flexed budget and variances. Through preparation of these budgets Amana's

performance can be evaluated that is what are the areas where company is required to improve.

The report included recommendations on areas where company is required to improve itself. The

second part of project was about the advantages and disadvantages of online business and

whether it is beneficial for Amana to move towards online business. It also highlighted two

alternatives for company to move online and analysis on both alternatives. At last there was

advice regarding selection of appropriate online alternative for company.

unit cost.

Non financial consideration: Before taking any decision it is essential to look into all the aspects

that may impact the decision. In accordance to non financial aspect it is better to move into

online mode of sales through amazon but every coin has two sides (Alvarenga and et.al., 2018).

The another aspect of reaching a decision is qualitative aspect. Sales through amazon will

adversely affect the control over pricing and return policy of company. There will be lack of

control over price of product as price may be set by amazon and company has to agree with the

same as it will enter into contract. The return policy of company will also be affected through

this alternative. The company will not be able to build direct relationship with its customers if it

sells its products through amazon and this may impact its future operations as building and

maintaining strong customer relationship is very essential for an organization.

From above, it can be recommended that company is required to ascertain which

consideration is more beneficial for sustainable growth and development of business. For the

long term profit and development of business it will be better for company to select first

alternative i.e. set up its own online shop (Xue and et.al., 2020). In the initial period it may be

cost effective but when the demand for product will raise it would ultimately reduce per unit cost

to company and it will also ensure control over price and return policy. Company will also be

able to build direct relationship with its customers and would be able to understand needs and

preferences of customers.

CONCLUSION

The project is related to management accounting which includes control report showing

original budget, flexed budget and variances. Through preparation of these budgets Amana's

performance can be evaluated that is what are the areas where company is required to improve.

The report included recommendations on areas where company is required to improve itself. The

second part of project was about the advantages and disadvantages of online business and

whether it is beneficial for Amana to move towards online business. It also highlighted two

alternatives for company to move online and analysis on both alternatives. At last there was

advice regarding selection of appropriate online alternative for company.

REFERENCES

Alvarenga, J. C. and et.al., 2018. A revaluation of the criticality of the project manager to the

project's success. Business management dynamics. 8(2). pp.1-18.

Ayorekire, M., 2018. Budgeting and budgetary control in non-governmental organisations: a

case of Infectious Diseases Research Collaboration (IDRC).

Boyns, T., 2021. Organizational change, budgetary control and success and failure in Formula 1:

Rubery Owen and British Racing Motors, 1947–1977. Management & Organizational

History. 16(3-4), pp.204-227.

Dauda, H., 2019. Examining the Role of Budgeting and Budgetary Control in Achieving

Objectives of Business Organisations.

Mohamed, A. I., 2022. The impact of budgetary control on manufacturing firms' financial

performance Mogadishu-Somalia. NeuroQuantology, 20(6), pp.4741-4755.

Ohiaeri, N. V., 2021. Mainstreaming Public Expenditure Budgetary Control Connectivity With

Economic Growth of Nigeria.

Shefren, A. S. A., et. al. 2021. FACTORS INFLUENCING BUDGETARY CONTROL

AMONG SMES IN THE KLANG VALLEY, MALAYSIA. Electronic Journal of

Business and Management. 6(2), pp.1-17.

Taher, G., 2021. E-commerce: advantages and limitations. International Journal of Academic

Research in Accounting Finance and Management Sciences. 11(1). pp.153-165.

Xue, J. and et.al., 2020. The impact of project manager soft competences on project

sustainability. Sustainability. 12(16). p.6537.

Zwikael, O. and Meredith, J., 2019. Evaluating the success of a project and the performance of

its leaders. IEEE transactions on engineering management. 68(6). pp.1745-1757.

Online

Project selection methods, 2022. [Online]. Available through:

<https://www.simplilearn.com/project-selection-methods-article>

Alvarenga, J. C. and et.al., 2018. A revaluation of the criticality of the project manager to the

project's success. Business management dynamics. 8(2). pp.1-18.

Ayorekire, M., 2018. Budgeting and budgetary control in non-governmental organisations: a

case of Infectious Diseases Research Collaboration (IDRC).

Boyns, T., 2021. Organizational change, budgetary control and success and failure in Formula 1:

Rubery Owen and British Racing Motors, 1947–1977. Management & Organizational

History. 16(3-4), pp.204-227.

Dauda, H., 2019. Examining the Role of Budgeting and Budgetary Control in Achieving

Objectives of Business Organisations.

Mohamed, A. I., 2022. The impact of budgetary control on manufacturing firms' financial

performance Mogadishu-Somalia. NeuroQuantology, 20(6), pp.4741-4755.

Ohiaeri, N. V., 2021. Mainstreaming Public Expenditure Budgetary Control Connectivity With

Economic Growth of Nigeria.

Shefren, A. S. A., et. al. 2021. FACTORS INFLUENCING BUDGETARY CONTROL

AMONG SMES IN THE KLANG VALLEY, MALAYSIA. Electronic Journal of

Business and Management. 6(2), pp.1-17.

Taher, G., 2021. E-commerce: advantages and limitations. International Journal of Academic

Research in Accounting Finance and Management Sciences. 11(1). pp.153-165.

Xue, J. and et.al., 2020. The impact of project manager soft competences on project

sustainability. Sustainability. 12(16). p.6537.

Zwikael, O. and Meredith, J., 2019. Evaluating the success of a project and the performance of

its leaders. IEEE transactions on engineering management. 68(6). pp.1745-1757.

Online

Project selection methods, 2022. [Online]. Available through:

<https://www.simplilearn.com/project-selection-methods-article>

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.