Management Accounting Techniques and Reporting for Tech UK

VerifiedAdded on 2020/10/05

|18

|4697

|455

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the case of Tech UK Limited. It begins with an introduction to management accounting, defining its role and importance in comparison to financial accounting, and then explores key aspects like cost accounting systems, inventory management techniques (FIFO, LIFO, AVCO), and job costing systems. The report further examines various accounting reporting methods, including performance reports, inventory management reports, account receivable reports, and job cost reports, highlighting their significance in financial decision-making. It then delves into different types of costing methods, analyzing accounting techniques and interpreting data from income statements. The report also covers budgeting, analyzing planning tools, and critically analyzing financial issues, along with an overview of the balance scorecard approach and its role in analyzing financial issues. The conclusion summarizes the findings and emphasizes the importance of effective management accounting for enhancing profitability and making informed business decisions within Tech UK.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTENTS

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a): Definition of management and their essential requirement.............................................1

(i): Comparison.......................................................................................................................2

(ii) Importance of management accounting information........................................................2

(iii): Cost accounting system..................................................................................................2

(iv): Inventory management system.......................................................................................3

(V): Job costing system..........................................................................................................3

(b): (i); Various method of accounting reporting...................................................................4

(ii): Importance of using reporting methods...........................................................................5

M1: Benefits of using management accounting system.........................................................5

D1: Critical analysis of various reporting system..................................................................5

TASK 2............................................................................................................................................6

(A): Different types of costing methods.................................................................................6

M2: Analysing accounting techniques.................................................................................11

D2: Data interpretation of calculated outcomes from income statements............................11

TASK 3..........................................................................................................................................11

(i): Types of budget..............................................................................................................11

M3: Analysis of planning tools............................................................................................13

D3: Critical analysis of financial issues...............................................................................13

TASK 4..........................................................................................................................................14

(i): Balance scorecard approach...........................................................................................14

M4: Analysing financial issues............................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a): Definition of management and their essential requirement.............................................1

(i): Comparison.......................................................................................................................2

(ii) Importance of management accounting information........................................................2

(iii): Cost accounting system..................................................................................................2

(iv): Inventory management system.......................................................................................3

(V): Job costing system..........................................................................................................3

(b): (i); Various method of accounting reporting...................................................................4

(ii): Importance of using reporting methods...........................................................................5

M1: Benefits of using management accounting system.........................................................5

D1: Critical analysis of various reporting system..................................................................5

TASK 2............................................................................................................................................6

(A): Different types of costing methods.................................................................................6

M2: Analysing accounting techniques.................................................................................11

D2: Data interpretation of calculated outcomes from income statements............................11

TASK 3..........................................................................................................................................11

(i): Types of budget..............................................................................................................11

M3: Analysis of planning tools............................................................................................13

D3: Critical analysis of financial issues...............................................................................13

TASK 4..........................................................................................................................................14

(i): Balance scorecard approach...........................................................................................14

M4: Analysing financial issues............................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

In present scenario management is always planning to make use of appropriate

accounting techniques which will lead to increase better outcomes in coming period of time. It

seems to be one of the crucial role of managers to make use of reliable resources that are

sufficient enough to attain maximum profit for the company (Hilton and Platt, 2013) .According

to the mentioned case of Tech UK it has been analyse the company is planning to analyse their

financial statements because they are not able to earn valuable amount of revenues in last few

years. For this purpose they have appointed a new accountant for auditing of their financial

statements. This project an aim is to evaluated accounting and reporting methods in effective

manner so that every transaction can be recorded effectively. Apart from this, different types of

costing methods are being used to calculate net profit for the company. However, use of various

types of budgets can lead to manage their future costs and expense. Evaluation of various

management accounting techniques those are use for the purpose of resolving financial issues

those are arises in an organisation.

TASK 1

(a): Definition of management and their essential requirement

In accordance with increase overall goodwill of Tech (UK) Limited in front of other

companies they need to grab new opportunities by using appropriate accounting systems. This

will be consider more effective in recording all financial and non-financial transactions those are

done within an accounting period of time. The manager always looks to make use of reliable

systems which will be essential enough to increase overall productivity and growth for the

company (Parker, 2012). Management accounting is known as one of the essential process of

collecting, recording, summarising and evaluating all data in more vital manner in the set period.

Managers are uses the provision of all information in respect to make better inform themselves

before they decide all essential matters within their organisation. These effective provisions

assist financial data and make advice to every company for using in the organisation and

evaluation data that are made by company in last year. The process of formulating management

accounting report and account that used to provide reliable and accurate financial and statistical

results for the company. One more effective point is taken into account that financial and

management accounting is having some kind of differences those are mentioned below:

1

In present scenario management is always planning to make use of appropriate

accounting techniques which will lead to increase better outcomes in coming period of time. It

seems to be one of the crucial role of managers to make use of reliable resources that are

sufficient enough to attain maximum profit for the company (Hilton and Platt, 2013) .According

to the mentioned case of Tech UK it has been analyse the company is planning to analyse their

financial statements because they are not able to earn valuable amount of revenues in last few

years. For this purpose they have appointed a new accountant for auditing of their financial

statements. This project an aim is to evaluated accounting and reporting methods in effective

manner so that every transaction can be recorded effectively. Apart from this, different types of

costing methods are being used to calculate net profit for the company. However, use of various

types of budgets can lead to manage their future costs and expense. Evaluation of various

management accounting techniques those are use for the purpose of resolving financial issues

those are arises in an organisation.

TASK 1

(a): Definition of management and their essential requirement

In accordance with increase overall goodwill of Tech (UK) Limited in front of other

companies they need to grab new opportunities by using appropriate accounting systems. This

will be consider more effective in recording all financial and non-financial transactions those are

done within an accounting period of time. The manager always looks to make use of reliable

systems which will be essential enough to increase overall productivity and growth for the

company (Parker, 2012). Management accounting is known as one of the essential process of

collecting, recording, summarising and evaluating all data in more vital manner in the set period.

Managers are uses the provision of all information in respect to make better inform themselves

before they decide all essential matters within their organisation. These effective provisions

assist financial data and make advice to every company for using in the organisation and

evaluation data that are made by company in last year. The process of formulating management

accounting report and account that used to provide reliable and accurate financial and statistical

results for the company. One more effective point is taken into account that financial and

management accounting is having some kind of differences those are mentioned below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

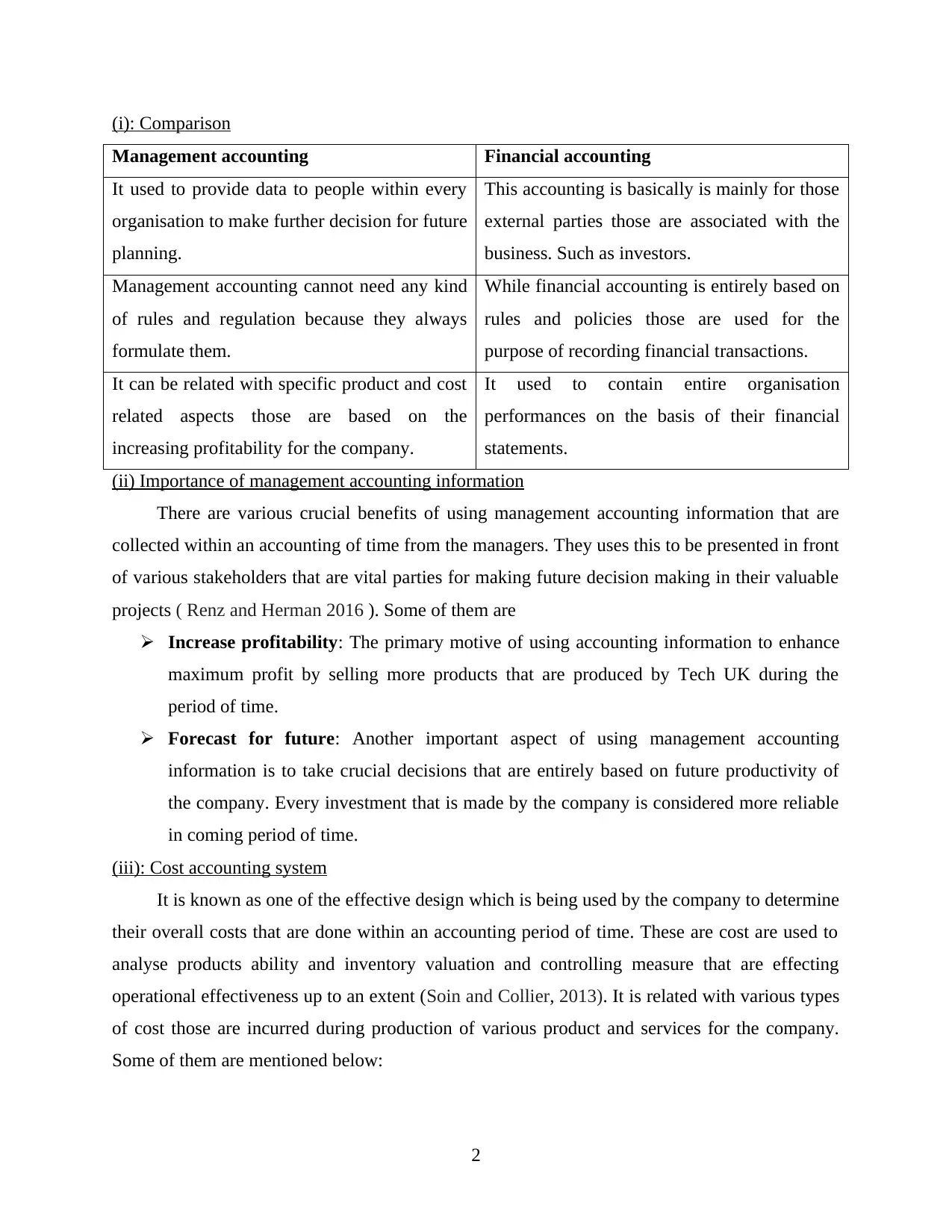

(i): Comparison

Management accounting Financial accounting

It used to provide data to people within every

organisation to make further decision for future

planning.

This accounting is basically is mainly for those

external parties those are associated with the

business. Such as investors.

Management accounting cannot need any kind

of rules and regulation because they always

formulate them.

While financial accounting is entirely based on

rules and policies those are used for the

purpose of recording financial transactions.

It can be related with specific product and cost

related aspects those are based on the

increasing profitability for the company.

It used to contain entire organisation

performances on the basis of their financial

statements.

(ii) Importance of management accounting information

There are various crucial benefits of using management accounting information that are

collected within an accounting of time from the managers. They uses this to be presented in front

of various stakeholders that are vital parties for making future decision making in their valuable

projects ( Renz and Herman 2016 ). Some of them are

Increase profitability: The primary motive of using accounting information to enhance

maximum profit by selling more products that are produced by Tech UK during the

period of time.

Forecast for future: Another important aspect of using management accounting

information is to take crucial decisions that are entirely based on future productivity of

the company. Every investment that is made by the company is considered more reliable

in coming period of time.

(iii): Cost accounting system

It is known as one of the effective design which is being used by the company to determine

their overall costs that are done within an accounting period of time. These are cost are used to

analyse products ability and inventory valuation and controlling measure that are effecting

operational effectiveness up to an extent (Soin and Collier, 2013). It is related with various types

of cost those are incurred during production of various product and services for the company.

Some of them are mentioned below:

2

Management accounting Financial accounting

It used to provide data to people within every

organisation to make further decision for future

planning.

This accounting is basically is mainly for those

external parties those are associated with the

business. Such as investors.

Management accounting cannot need any kind

of rules and regulation because they always

formulate them.

While financial accounting is entirely based on

rules and policies those are used for the

purpose of recording financial transactions.

It can be related with specific product and cost

related aspects those are based on the

increasing profitability for the company.

It used to contain entire organisation

performances on the basis of their financial

statements.

(ii) Importance of management accounting information

There are various crucial benefits of using management accounting information that are

collected within an accounting of time from the managers. They uses this to be presented in front

of various stakeholders that are vital parties for making future decision making in their valuable

projects ( Renz and Herman 2016 ). Some of them are

Increase profitability: The primary motive of using accounting information to enhance

maximum profit by selling more products that are produced by Tech UK during the

period of time.

Forecast for future: Another important aspect of using management accounting

information is to take crucial decisions that are entirely based on future productivity of

the company. Every investment that is made by the company is considered more reliable

in coming period of time.

(iii): Cost accounting system

It is known as one of the effective design which is being used by the company to determine

their overall costs that are done within an accounting period of time. These are cost are used to

analyse products ability and inventory valuation and controlling measure that are effecting

operational effectiveness up to an extent (Soin and Collier, 2013). It is related with various types

of cost those are incurred during production of various product and services for the company.

Some of them are mentioned below:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Actual costing: These are said to be that cost which are actually incurred by Tech UK

while production process. It is mostly related with direct material and direct overhead.

Standard costing: It is mostly used by an organisation to make analysis of actual cost

that is paid by the company are relatively different from one another.

Normal costing: It is basically that cost which is being incurred normally on direct cost

of production such as direct material, labour and overhead costs.

(iv): Inventory management system

This seems to be ongoing procedure for moving parts and products into and out of a

company premises. Tech UK used to manage their entire stock on regular basis as they are

placed for new one or before shipping orders to various customers. This seems to be more

relatively associated with tracking stock levels, orders and sales and deliveries during the period

of time. There are various techniques that are related with controlling various stock of the

company. Some of them are discussed underneath:

FIFO: It is known as first in, first out which means that the long time stock items are

recorded as sell firstly but do not important to detect exact oldest objects that has been

tracked and sold by the company ( Christ and Burritt, 2013).

LIFO: According to this, cost flow valuation that can be determine by various companies

in moving their production cost from stock to the cost of product sold during the time.

AVCO: This seems to be utmost valuable costing methods that are based on average cost

of stock during an accounting period of time. It is used to calculate the cost of closing

stocks and cost of goods sold for given period on the basis of weighted average cost per

unit of products produced.

(V): Job costing system

Job order costing is basically reliable for assigning production costs to a single products or

group of products that are produced within an accounting time. Basically, the job costing is

consider only those situation the product manufactured are relatively separate from one another.

There are various types of job costing which are incurred within an organisation during

generating sufficient amount of goods to the company. Some of them are:

Batch costing: According to this cost an organisation is liable to make analysis of

products that are produces in batches in a given period. Each batch has been allotted a

number that is relatively different from another.

3

while production process. It is mostly related with direct material and direct overhead.

Standard costing: It is mostly used by an organisation to make analysis of actual cost

that is paid by the company are relatively different from one another.

Normal costing: It is basically that cost which is being incurred normally on direct cost

of production such as direct material, labour and overhead costs.

(iv): Inventory management system

This seems to be ongoing procedure for moving parts and products into and out of a

company premises. Tech UK used to manage their entire stock on regular basis as they are

placed for new one or before shipping orders to various customers. This seems to be more

relatively associated with tracking stock levels, orders and sales and deliveries during the period

of time. There are various techniques that are related with controlling various stock of the

company. Some of them are discussed underneath:

FIFO: It is known as first in, first out which means that the long time stock items are

recorded as sell firstly but do not important to detect exact oldest objects that has been

tracked and sold by the company ( Christ and Burritt, 2013).

LIFO: According to this, cost flow valuation that can be determine by various companies

in moving their production cost from stock to the cost of product sold during the time.

AVCO: This seems to be utmost valuable costing methods that are based on average cost

of stock during an accounting period of time. It is used to calculate the cost of closing

stocks and cost of goods sold for given period on the basis of weighted average cost per

unit of products produced.

(V): Job costing system

Job order costing is basically reliable for assigning production costs to a single products or

group of products that are produced within an accounting time. Basically, the job costing is

consider only those situation the product manufactured are relatively separate from one another.

There are various types of job costing which are incurred within an organisation during

generating sufficient amount of goods to the company. Some of them are:

Batch costing: According to this cost an organisation is liable to make analysis of

products that are produces in batches in a given period. Each batch has been allotted a

number that is relatively different from another.

3

Process costing: As per this method company used to assign cost to units of

manufacturing in Tech UK producing large amount of products for an organisation. Such

kind of cost is mostly used to ascertain costs of a product at every phase of production

(Figge and Hahn, 2013).

(b): (i); Various method of accounting reporting

In current era, management is trying to make use of various effective reporting methods

that are effectively responsible for increasing profitability of the company. Every reports are

having certain benefits those are vital for the owner to plan their future projects in more effective

manner. Reporting used to provide enterprises certain information about financial position of the

company on the basis of their financial statements that are prepared by managers in last year’s.

These reports are considered more reliable for making future decision in more reliable manner.

There are various sources from which financial information can be gathered by accountant and to

be presented to various investors and stakeholder for the purpose of making business strategies in

near future time. There are various types of reporting methods which will be valuable for

planning, organising and coordinating resources of the company. Some of them are mentioned

underneath:

Performance report: This happens to be more crucial activities which are used in project

planning process. It consists of collecting necessary information from project progress,

utilisation of resources and estimation of future growth of the company (Wickramasinghe and

Alawattage, 2012 ). This can be more valuable in case all the data collected by the accountant are

accurately provided to the company. It can be related with past performance and profit they are

incurred from the selling of products. Such kind of report is more helpful for the administration

to success of a project and budget related matters.

Inventory management reports: According to this particular report which will be prepared by

the accountant for the purpose of analysing current stock position of the company. All the

opening and closing information of inventory are recorded in this report. This will assist an

organisation to increase their internal capacity by use resources at the time of production of

products and services with the accounting time frame. These are various inventory valuation

techniques which are effective useful for the company such as economic order quantity level,

inventory turnover ratio of an organisation.

4

manufacturing in Tech UK producing large amount of products for an organisation. Such

kind of cost is mostly used to ascertain costs of a product at every phase of production

(Figge and Hahn, 2013).

(b): (i); Various method of accounting reporting

In current era, management is trying to make use of various effective reporting methods

that are effectively responsible for increasing profitability of the company. Every reports are

having certain benefits those are vital for the owner to plan their future projects in more effective

manner. Reporting used to provide enterprises certain information about financial position of the

company on the basis of their financial statements that are prepared by managers in last year’s.

These reports are considered more reliable for making future decision in more reliable manner.

There are various sources from which financial information can be gathered by accountant and to

be presented to various investors and stakeholder for the purpose of making business strategies in

near future time. There are various types of reporting methods which will be valuable for

planning, organising and coordinating resources of the company. Some of them are mentioned

underneath:

Performance report: This happens to be more crucial activities which are used in project

planning process. It consists of collecting necessary information from project progress,

utilisation of resources and estimation of future growth of the company (Wickramasinghe and

Alawattage, 2012 ). This can be more valuable in case all the data collected by the accountant are

accurately provided to the company. It can be related with past performance and profit they are

incurred from the selling of products. Such kind of report is more helpful for the administration

to success of a project and budget related matters.

Inventory management reports: According to this particular report which will be prepared by

the accountant for the purpose of analysing current stock position of the company. All the

opening and closing information of inventory are recorded in this report. This will assist an

organisation to increase their internal capacity by use resources at the time of production of

products and services with the accounting time frame. These are various inventory valuation

techniques which are effective useful for the company such as economic order quantity level,

inventory turnover ratio of an organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account receivable report: As per this report, manager can easily be able to analyse their total

list of customer invoices that are remain unpaid from very longer period. The major aims of an

organisation to make use of specific data and time to get recover that outstanding amount from

debtors. All the detail information can be attain in effective manner by using most valuable

aspects for the company.

Job cost report: As per this particular costing report a company can be able to analyse their

overall cost they are paying to produce an individual job. This seems to be more suitable report

for the investors in order to make valuable decision in coming period of time. This can be

implemented by using necessary information from various departments that are operating at

internal and external level of the company (Schäffer, 2013).

(ii): Importance of using reporting methods

There are various crucial reporting approaches that are use by the company in order to

make reporting of all information those are collected within an organisation. They are

considering for using data in accordance with attaining more reliable outcomes in coming period

of time. Every reporting is vital for the investors as they are showing overall financial position of

Tech UK and by analysing those statements they use to make decision to invest capital into their

business.

M1: Benefits of using management accounting system

It has been seen that every accounting systems is consider valuable aspects for Tech UK

company. These accounting leads to make effective decision for increase profitability position in

respect to other organisation. All the above discussed systems are taken as beneficial for the

company such as cost accounting is used to analyse total cost invested in a product production.

While inventory management system is more vital for analyse total stock kept by the company

with them.

D1: Critical analysis of various reporting system

According to the all above mentioned reporting systems, managers can easily be able to

present all necessary aspects of their business in overall planning of business operations. Such as

performance report are consider more crucial report that provide information about last and

current year position of the company (Hansen, 2011). While account receivable report is taken in

account for analyse total time period for retaining their outstanding amounts from the debtors.

5

list of customer invoices that are remain unpaid from very longer period. The major aims of an

organisation to make use of specific data and time to get recover that outstanding amount from

debtors. All the detail information can be attain in effective manner by using most valuable

aspects for the company.

Job cost report: As per this particular costing report a company can be able to analyse their

overall cost they are paying to produce an individual job. This seems to be more suitable report

for the investors in order to make valuable decision in coming period of time. This can be

implemented by using necessary information from various departments that are operating at

internal and external level of the company (Schäffer, 2013).

(ii): Importance of using reporting methods

There are various crucial reporting approaches that are use by the company in order to

make reporting of all information those are collected within an organisation. They are

considering for using data in accordance with attaining more reliable outcomes in coming period

of time. Every reporting is vital for the investors as they are showing overall financial position of

Tech UK and by analysing those statements they use to make decision to invest capital into their

business.

M1: Benefits of using management accounting system

It has been seen that every accounting systems is consider valuable aspects for Tech UK

company. These accounting leads to make effective decision for increase profitability position in

respect to other organisation. All the above discussed systems are taken as beneficial for the

company such as cost accounting is used to analyse total cost invested in a product production.

While inventory management system is more vital for analyse total stock kept by the company

with them.

D1: Critical analysis of various reporting system

According to the all above mentioned reporting systems, managers can easily be able to

present all necessary aspects of their business in overall planning of business operations. Such as

performance report are consider more crucial report that provide information about last and

current year position of the company (Hansen, 2011). While account receivable report is taken in

account for analyse total time period for retaining their outstanding amounts from the debtors.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are some other reporting methods those are equally effective for an organisation to make

valuable decision in coming period of future.

TASK 2

(A): Different types of costing methods

Cost is one of the essential components of the company. It is directly or indirectly related

with the production of products and services. All direct material, labour and overhead costs are

taken into account while calculating cost for TECH (UK) Limited. In case of small and wide

organisation, cost is more concern factors for them to plan their production ability in coming

time. Cost is necessary aspect of every manufacturing making companies that are associated with

development of effective goods and services for the company in the allotted period. It is said to

value of money that is being paid for getting something in return. This seems to be considering in

financial valuation of efforts, quality and risks that are associated with production process.

Costing process is predication of total cost which is associated with a product of building up of

new venture. It consists of all those variable costs those are known to be variables as compare to

their costs (Chan, Wang and Raffoni, 2014). There are various types of costs which are related

with production planning. Some of them are discussed underneath:

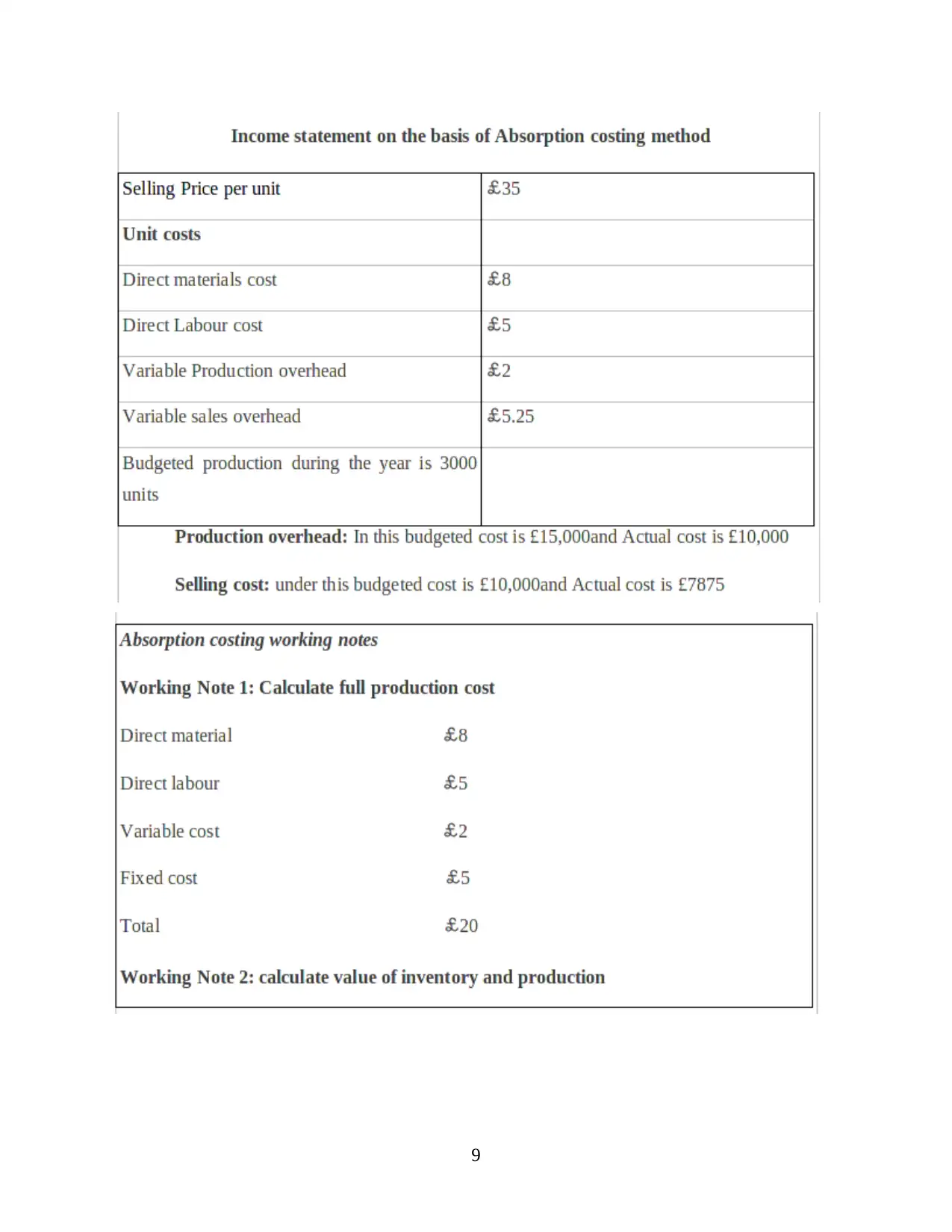

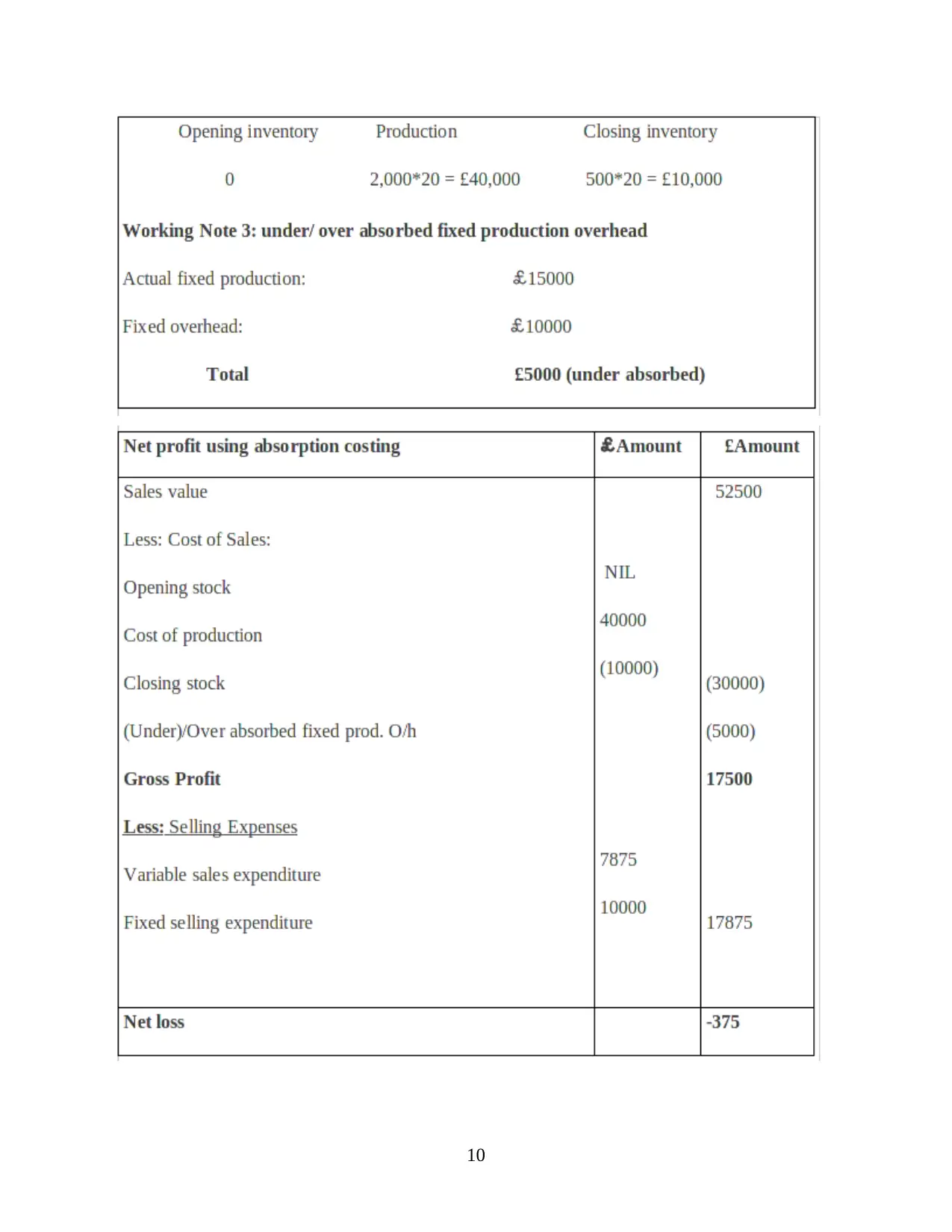

Absorption costing: It is known as one of the reliable costing method which is associated

with production of products and services. It included both variable and fixed costs that are

incurred in producing one unit or more than one. Because of this effective nature, it is said to be

full costing method. Instead of all this crucial aspects, it is not so effective costing for making

future decision making for the company. It is a valuable technique which is used for analysing

total cost of goods through taking necessary steps of indirect cost as well as other cost.

Marginal costing: This refers to be more reliable costing method that is use by the

company for producing one additional unit during the manufacturing process. It consists of only

variable cost and fixed costs get absorbed while calculating contribution per unit. Instead of all

matters this is consider more reliable for future decision making. Such kinds of cost are charges

as per their higher unit cost generated from the margin.

6

valuable decision in coming period of future.

TASK 2

(A): Different types of costing methods

Cost is one of the essential components of the company. It is directly or indirectly related

with the production of products and services. All direct material, labour and overhead costs are

taken into account while calculating cost for TECH (UK) Limited. In case of small and wide

organisation, cost is more concern factors for them to plan their production ability in coming

time. Cost is necessary aspect of every manufacturing making companies that are associated with

development of effective goods and services for the company in the allotted period. It is said to

value of money that is being paid for getting something in return. This seems to be considering in

financial valuation of efforts, quality and risks that are associated with production process.

Costing process is predication of total cost which is associated with a product of building up of

new venture. It consists of all those variable costs those are known to be variables as compare to

their costs (Chan, Wang and Raffoni, 2014). There are various types of costs which are related

with production planning. Some of them are discussed underneath:

Absorption costing: It is known as one of the reliable costing method which is associated

with production of products and services. It included both variable and fixed costs that are

incurred in producing one unit or more than one. Because of this effective nature, it is said to be

full costing method. Instead of all this crucial aspects, it is not so effective costing for making

future decision making for the company. It is a valuable technique which is used for analysing

total cost of goods through taking necessary steps of indirect cost as well as other cost.

Marginal costing: This refers to be more reliable costing method that is use by the

company for producing one additional unit during the manufacturing process. It consists of only

variable cost and fixed costs get absorbed while calculating contribution per unit. Instead of all

matters this is consider more reliable for future decision making. Such kinds of cost are charges

as per their higher unit cost generated from the margin.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.