Analysis of Management Accounting Systems and Financial Problems

VerifiedAdded on 2023/01/12

|24

|2779

|62

Report

AI Summary

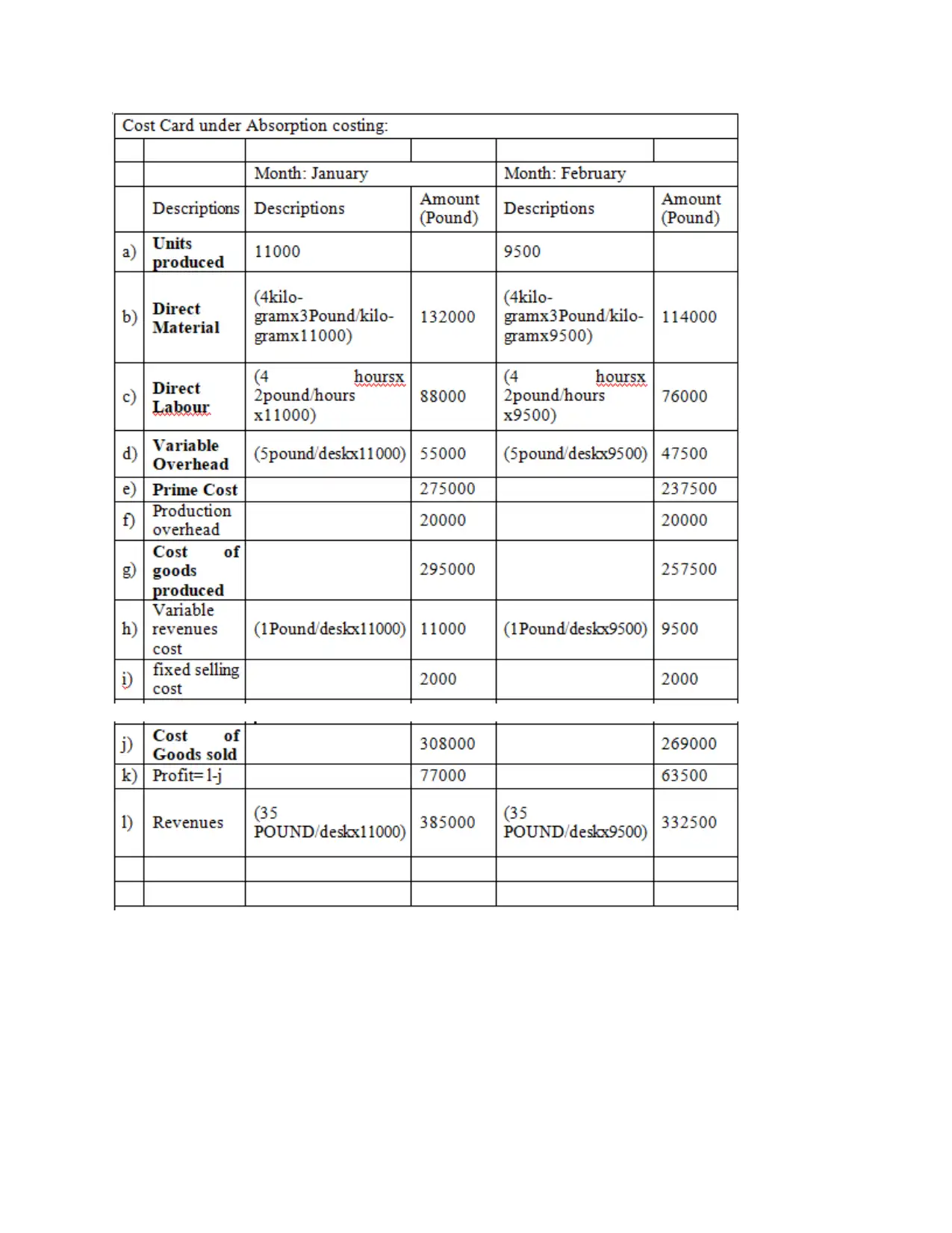

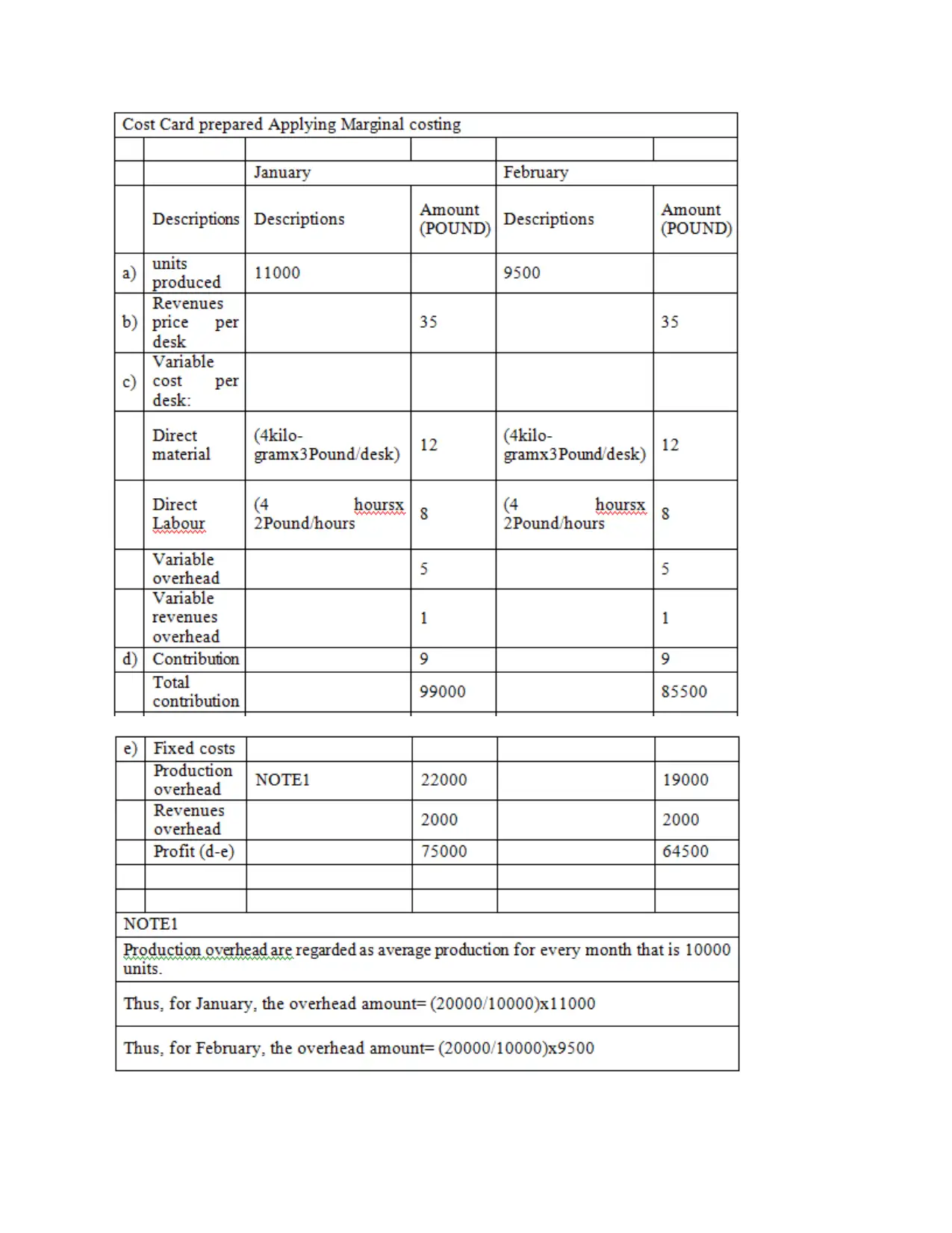

This report provides a comprehensive overview of management accounting (MA) and its various systems, focusing on their role in organizational decision-making and financial management. It begins by defining MA and outlining the basic requirements for different MA systems, such as inventory management, price optimization, and job costing. The report also discusses the importance of management accounting reporting, highlighting key reports like job costing, inventory, and performance reports, and evaluates the benefits of these systems. Furthermore, it examines how MA systems are integrated within an organization's processes, using UCK furniture as a case study. The report also explains and compares marginal and absorption costing methods, analyzing their merits and demerits and includes an interpretation of income statements under both methods. The purpose of budgeting is defined, and the document discusses how entities adjust MA systems to handle financial problems and improve overall financial performance, using ratio analysis to compare UCK furniture and UCK woodwork. Concluding with the importance of MA for sustained success and to find similar solved assignments and past papers, students can refer to Desklib.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.