Lets Grow Ltd: Management Accounting, Cash Budget, and Planning

VerifiedAdded on 2023/01/11

|15

|4207

|95

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and their benefits, focusing on their application within Lets Grow Ltd. It covers various systems, including cost accounting, inventory management, job costing, and price optimization, detailing their advantages and practical applications. The report also examines different types of management accounting reports, such as accounts receivable aging, performance, and cost managerial accounting reports. A cash budget for Lets Grow Ltd is presented for the six months ending August 2020, followed by an evaluation of planning tools like cash budgets and flexible budgets for managing financial challenges. The report concludes by suggesting a suitable management accounting system to address financial problems and critically evaluates Lets Grow Ltd's financial position based on the forecasted cash budget. Desklib offers a wide array of study tools and resources for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...............................................................................................................3

Scenario.............................................................................................................................3

a) Management accounting (MA) systems and its benefits..........................................3

b) Management accounting reports...............................................................................5

c) Cash budget for the next 6 months ending August 2020..........................................6

d) Planning tools for managing the financial problems of the organization..................7

e) MA system that can be adopted to respond to the financial problems...................10

f) Critically evaluating the financial position of Lets Grow Ltd as per the forecasted

cash budget.................................................................................................................12

CONCLUSION.................................................................................................................12

REFERENCES............................................................................................................................13

INTRODUCTION...............................................................................................................3

Scenario.............................................................................................................................3

a) Management accounting (MA) systems and its benefits..........................................3

b) Management accounting reports...............................................................................5

c) Cash budget for the next 6 months ending August 2020..........................................6

d) Planning tools for managing the financial problems of the organization..................7

e) MA system that can be adopted to respond to the financial problems...................10

f) Critically evaluating the financial position of Lets Grow Ltd as per the forecasted

cash budget.................................................................................................................12

CONCLUSION.................................................................................................................12

REFERENCES............................................................................................................................13

INTRODUCTION

Management accounting is the process through which the financial information

pertaining to the business collected by the management which helps it in better and

improved decision making with respect to the future success of the business. It is

different from the financial management as it takes into consideration both quantitative

and qualitative information. This report covers about the essential requirements,

systems and approaches of management accounting in an organization.

Scenario

a) Management accounting (MA) systems and its benefits

The management accounting system helps the business organization in dealing

with different types of business problems and makes the process much easier to

manage. The different types of management accounting system are stated below.

Cost accounting system

This system is used by the organization with the purpose to effectively manage

the cost in relation to the products in terms of profitability and cost control. It helps in

analysing the cost of each and every product that is being produced by the organization

(Khan, Parvin and Sayeeda, 2019). It analyses the cost of production in respect to

variable and the fixed cost at every step of the production. The essential requirement of

it is to conduct cost and profitability analysis for each of the product and effective way.

Benefits

Cost accounting system helps in reviewing the raw material under each stage of

production.

It provides assistance in lowering the cost of production which leads to lowering

the operational cost by identifying the exercising control over the activities or

task. Thus, leads to profit maximization. It's real time aspect of it helps the management in taking informed and quick

decisions without waiting for the reports.

Application

The cost accounting system will help Lets Grow Ltd in effectively managing its

material usage as and when it undergoes various production process and the cost

incurring at each level.

Management accounting is the process through which the financial information

pertaining to the business collected by the management which helps it in better and

improved decision making with respect to the future success of the business. It is

different from the financial management as it takes into consideration both quantitative

and qualitative information. This report covers about the essential requirements,

systems and approaches of management accounting in an organization.

Scenario

a) Management accounting (MA) systems and its benefits

The management accounting system helps the business organization in dealing

with different types of business problems and makes the process much easier to

manage. The different types of management accounting system are stated below.

Cost accounting system

This system is used by the organization with the purpose to effectively manage

the cost in relation to the products in terms of profitability and cost control. It helps in

analysing the cost of each and every product that is being produced by the organization

(Khan, Parvin and Sayeeda, 2019). It analyses the cost of production in respect to

variable and the fixed cost at every step of the production. The essential requirement of

it is to conduct cost and profitability analysis for each of the product and effective way.

Benefits

Cost accounting system helps in reviewing the raw material under each stage of

production.

It provides assistance in lowering the cost of production which leads to lowering

the operational cost by identifying the exercising control over the activities or

task. Thus, leads to profit maximization. It's real time aspect of it helps the management in taking informed and quick

decisions without waiting for the reports.

Application

The cost accounting system will help Lets Grow Ltd in effectively managing its

material usage as and when it undergoes various production process and the cost

incurring at each level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system

The inventory management system is the system which is being used by the

organization for the purpose of effectively monitoring and managing the stock of the

materials and finished goods (Swafford Jr and et.al, 2017). It assists in tracking the

movement of the goods from one process to another and also timely delivering the

same to the clients. It optimizes the entire supply chain process. It involves raw

material, work in process and the finished goods. It is essential for effectively managing

the inventory of the organization.

Benefits

This system helps in reducing the amount of inaccuracy when the entries were

made manually and also helps in avoiding the duplicity of the data.

It is an automated process which helps in effectively recording and tracking the

processes which leads to no errors. It also helps in enhancing the productivity as the instant report can be prepared

as per the requirement so that changes can be made in a timely manner.

Application

The implementation of inventory management system in Lets Grow Ltd will

provide assistance in managing its inventory which will lead to reduction in the inventory

management cost.

Job costing system

Under this, a complete set of information is collected in respect to the cost with

different jobs undertaken. It is useful in providing cost report to the customer based on

the specification given by them. It determines the cost pertaining to the customers order

(Bottomley and Bosman, 2018). The product is manufactured as per the needs and the

requirements of the customer and a separate cost sheet is prepared. It is essential for

determining the cost associated with the different expenses charged in concern to the

job.

Benefits

It provides assistance in determining the profits for each job separately.

It provides complete information with respect to the material, labour and the

overhead expenses incurred for each job.

The inventory management system is the system which is being used by the

organization for the purpose of effectively monitoring and managing the stock of the

materials and finished goods (Swafford Jr and et.al, 2017). It assists in tracking the

movement of the goods from one process to another and also timely delivering the

same to the clients. It optimizes the entire supply chain process. It involves raw

material, work in process and the finished goods. It is essential for effectively managing

the inventory of the organization.

Benefits

This system helps in reducing the amount of inaccuracy when the entries were

made manually and also helps in avoiding the duplicity of the data.

It is an automated process which helps in effectively recording and tracking the

processes which leads to no errors. It also helps in enhancing the productivity as the instant report can be prepared

as per the requirement so that changes can be made in a timely manner.

Application

The implementation of inventory management system in Lets Grow Ltd will

provide assistance in managing its inventory which will lead to reduction in the inventory

management cost.

Job costing system

Under this, a complete set of information is collected in respect to the cost with

different jobs undertaken. It is useful in providing cost report to the customer based on

the specification given by them. It determines the cost pertaining to the customers order

(Bottomley and Bosman, 2018). The product is manufactured as per the needs and the

requirements of the customer and a separate cost sheet is prepared. It is essential for

determining the cost associated with the different expenses charged in concern to the

job.

Benefits

It provides assistance in determining the profits for each job separately.

It provides complete information with respect to the material, labour and the

overhead expenses incurred for each job.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This system helps the organization in identifying any defect or spoilage in the

specific job so that responsibility can be fixed on the individuals.

Application

This system will assist Lets Grow Ltd in determining the any defect in the

production system in accordance with the job carried out.

Price optimization system

This management accounting system is a strategy which is being used by the

organization for the purpose of determining the price of the product (Alaeddin and

Thabet, 2018). It is based on the demand and supply of the product in the market along

with the factors such as taste and preferences of the customers. It helps in knowing

how much the customer is willing to pay for the particular product. This system is

essential in determining the price of the product.

Benefits

This system assists the organization in focussing on the key areas which

includes sales margin, conversion rate etc. the revenue generated through it

adds to business growth and expansion.

It reduces the manual work which leads to minimizing the probability of human

errors. The decisions made through this system is more precise and has a huge impact

on the business.

Application

The application of this system in Lets Grow Ltd will help in determining the right

price for its products.

b) Management accounting reports

There are various types of reports which is being used by the organization for the

purpose of decision making. A detailed description is given below.

Account receivable aging report

This report is very important for the business organization which is provides

goods to its customers on credit basis on a large basis (H Roy Austin, 2019). It provides

a complete detail about each and every customer along with the total amount due from

them and the credit period provided. It also helps the business organization in

specific job so that responsibility can be fixed on the individuals.

Application

This system will assist Lets Grow Ltd in determining the any defect in the

production system in accordance with the job carried out.

Price optimization system

This management accounting system is a strategy which is being used by the

organization for the purpose of determining the price of the product (Alaeddin and

Thabet, 2018). It is based on the demand and supply of the product in the market along

with the factors such as taste and preferences of the customers. It helps in knowing

how much the customer is willing to pay for the particular product. This system is

essential in determining the price of the product.

Benefits

This system assists the organization in focussing on the key areas which

includes sales margin, conversion rate etc. the revenue generated through it

adds to business growth and expansion.

It reduces the manual work which leads to minimizing the probability of human

errors. The decisions made through this system is more precise and has a huge impact

on the business.

Application

The application of this system in Lets Grow Ltd will help in determining the right

price for its products.

b) Management accounting reports

There are various types of reports which is being used by the organization for the

purpose of decision making. A detailed description is given below.

Account receivable aging report

This report is very important for the business organization which is provides

goods to its customers on credit basis on a large basis (H Roy Austin, 2019). It provides

a complete detail about each and every customer along with the total amount due from

them and the credit period provided. It also helps the business organization in

identifying any bad debts so that provision can be created for the same for avoiding the

future problems.

Performance report

This report is prepared in respect to each department and each employee of the

organization which is based on the performance. These reports are useful in making

crucial business decisions (Maas and Verdoorn, 2017). The employees who are under

performing are mostly let go and the employees who perform well and achieve targets

or the set goals are rewarded. It is also useful in identifying any flaw in the workflow

system. This report provides assistance to the organization in order to remain on track.

Cost managerial accounting reports

This reports provide information about the cost incurred in manufacturing a

particular product. It takes into account all the costs such as overhead, labour and so

forth, which is then divided into the number of produced manufactured. It provides

bifurcation between the cost of products and selling price of the managers (What is

Managerial Accounting? 2020). It helps in exercising cost control activities after

analysing the expenses. Thus, this report provides exact details about the cost that the

organization is incurring so that a complete cost analysis process can be carried out.

Therefore, this report is very important from the business point of view mainly for the

manufacturing organization.

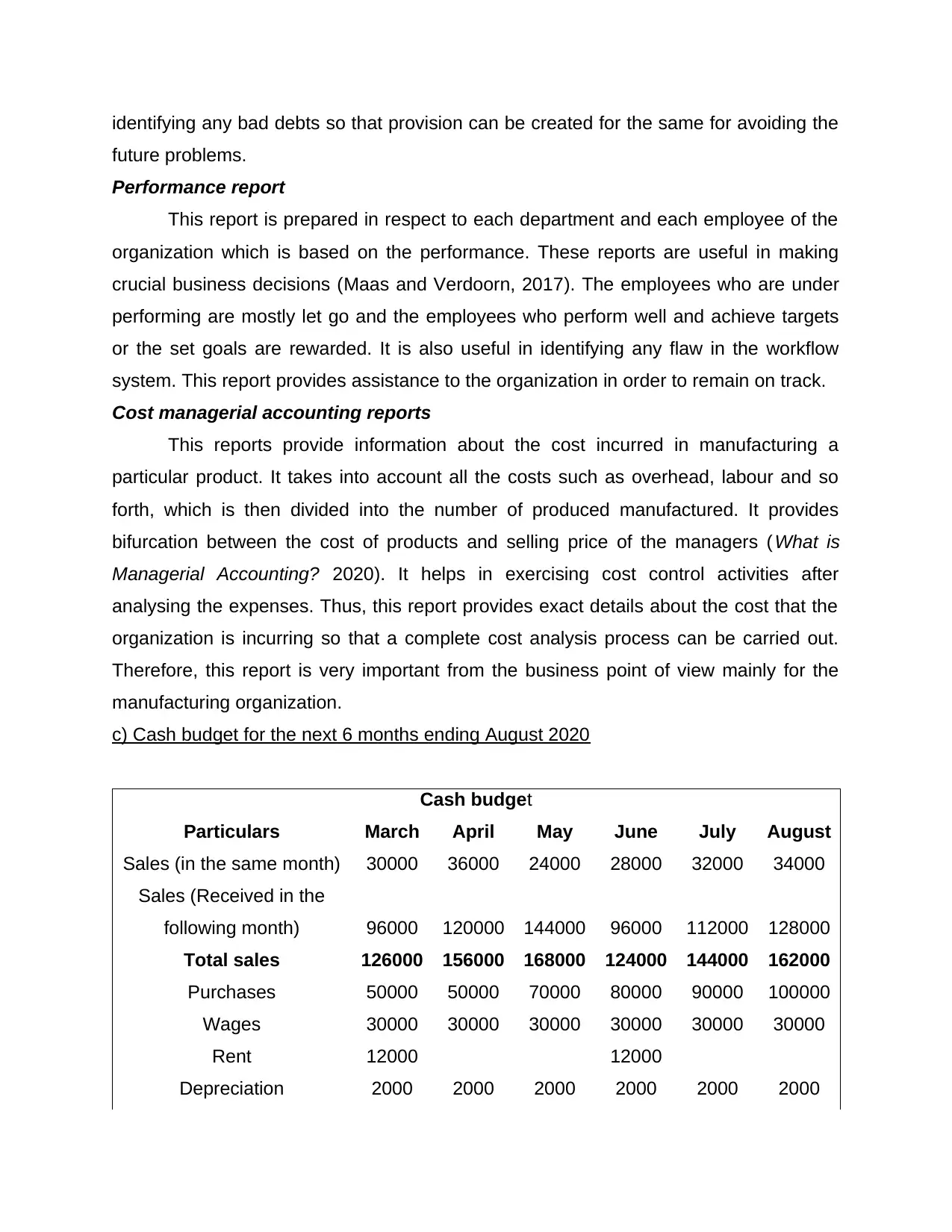

c) Cash budget for the next 6 months ending August 2020

Cash budget

Particulars March April May June July August

Sales (in the same month) 30000 36000 24000 28000 32000 34000

Sales (Received in the

following month) 96000 120000 144000 96000 112000 128000

Total sales 126000 156000 168000 124000 144000 162000

Purchases 50000 50000 70000 80000 90000 100000

Wages 30000 30000 30000 30000 30000 30000

Rent 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

future problems.

Performance report

This report is prepared in respect to each department and each employee of the

organization which is based on the performance. These reports are useful in making

crucial business decisions (Maas and Verdoorn, 2017). The employees who are under

performing are mostly let go and the employees who perform well and achieve targets

or the set goals are rewarded. It is also useful in identifying any flaw in the workflow

system. This report provides assistance to the organization in order to remain on track.

Cost managerial accounting reports

This reports provide information about the cost incurred in manufacturing a

particular product. It takes into account all the costs such as overhead, labour and so

forth, which is then divided into the number of produced manufactured. It provides

bifurcation between the cost of products and selling price of the managers (What is

Managerial Accounting? 2020). It helps in exercising cost control activities after

analysing the expenses. Thus, this report provides exact details about the cost that the

organization is incurring so that a complete cost analysis process can be carried out.

Therefore, this report is very important from the business point of view mainly for the

manufacturing organization.

c) Cash budget for the next 6 months ending August 2020

Cash budget

Particulars March April May June July August

Sales (in the same month) 30000 36000 24000 28000 32000 34000

Sales (Received in the

following month) 96000 120000 144000 96000 112000 128000

Total sales 126000 156000 168000 124000 144000 162000

Purchases 50000 50000 70000 80000 90000 100000

Wages 30000 30000 30000 30000 30000 30000

Rent 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overheads 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus/Deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

Closing cash balance 12000 41000 59000 17000 -5000 -21000

d) Planning tools for managing the financial problems of the organization

There are different types of planning tools which can be utilized by the

organization for the purpose of facing and the financial problems that may come across.

The various forms of planning tools are stated below.

Cash budget

The cash budget is useful in determining the cash input and output of the

organization in a specific period. It is mainly used for determining whether the company

is having sufficient amount of cash in order to carry out its day to day business activities

(Mariana, 2018). It is also used in determining whether the huge and unnecessary

amount is being spent on the unproductive manner which is not beneficial for the

business organization. By preparing cash budget, the company provides a complete

summary of the anticipated revenue and expenditure.

Advantages Disadvantages

This budget assists the organization

in avoiding the situation of taking

additional debt. It means that in

case the company is having less

cash which indicates that the

company should set aside the

remaining cash in order to meet the

emergency situations.

This budget helps in finding the

other sources of which can help in

meeting the financial deficiency. It

Cash is considered as the easiest

asset to steal and in case where

most of the transactions re done on

cash basis then it becomes very

essential to maintain the proper

documentation of it because it is not

easy to trace the cost pertaining to

the items involved.

While using this budget, the non-

financial aspects are completely

ignored. For instance, one bank

Fixed overheads 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus/Deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

Closing cash balance 12000 41000 59000 17000 -5000 -21000

d) Planning tools for managing the financial problems of the organization

There are different types of planning tools which can be utilized by the

organization for the purpose of facing and the financial problems that may come across.

The various forms of planning tools are stated below.

Cash budget

The cash budget is useful in determining the cash input and output of the

organization in a specific period. It is mainly used for determining whether the company

is having sufficient amount of cash in order to carry out its day to day business activities

(Mariana, 2018). It is also used in determining whether the huge and unnecessary

amount is being spent on the unproductive manner which is not beneficial for the

business organization. By preparing cash budget, the company provides a complete

summary of the anticipated revenue and expenditure.

Advantages Disadvantages

This budget assists the organization

in avoiding the situation of taking

additional debt. It means that in

case the company is having less

cash which indicates that the

company should set aside the

remaining cash in order to meet the

emergency situations.

This budget helps in finding the

other sources of which can help in

meeting the financial deficiency. It

Cash is considered as the easiest

asset to steal and in case where

most of the transactions re done on

cash basis then it becomes very

essential to maintain the proper

documentation of it because it is not

easy to trace the cost pertaining to

the items involved.

While using this budget, the non-

financial aspects are completely

ignored. For instance, one bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

also helps in exercising control over

overspending of the cash and helps

in finding new and better ways to

grow (Reichard and Van Helden,

2016).

It assists in identifying if there is any

deficit in the cash requirement or

might arise in future so that

potential and significant steps can

be taken in order to avoid any such

problems.

It helps in depicting the current

state and financial health of the

organization as anyone with the

basis knowledge can understand

the cash inflows and outflows and

identify the current and the future

issues that might arise.

offers loan at the lower rate of

interest which can be recorded in

the cash budget while the another

bank offers excellent customer

services cannot be recorded.

The cash budget can be easily

manipulated by the managers to

depict good with the objective to

gain benefit from it.

Once the budget is prepared and

reported to the management, the

numbers cannot be changed later

on. This makes this budget rigid as

it lacks the flexibility to make

changes.

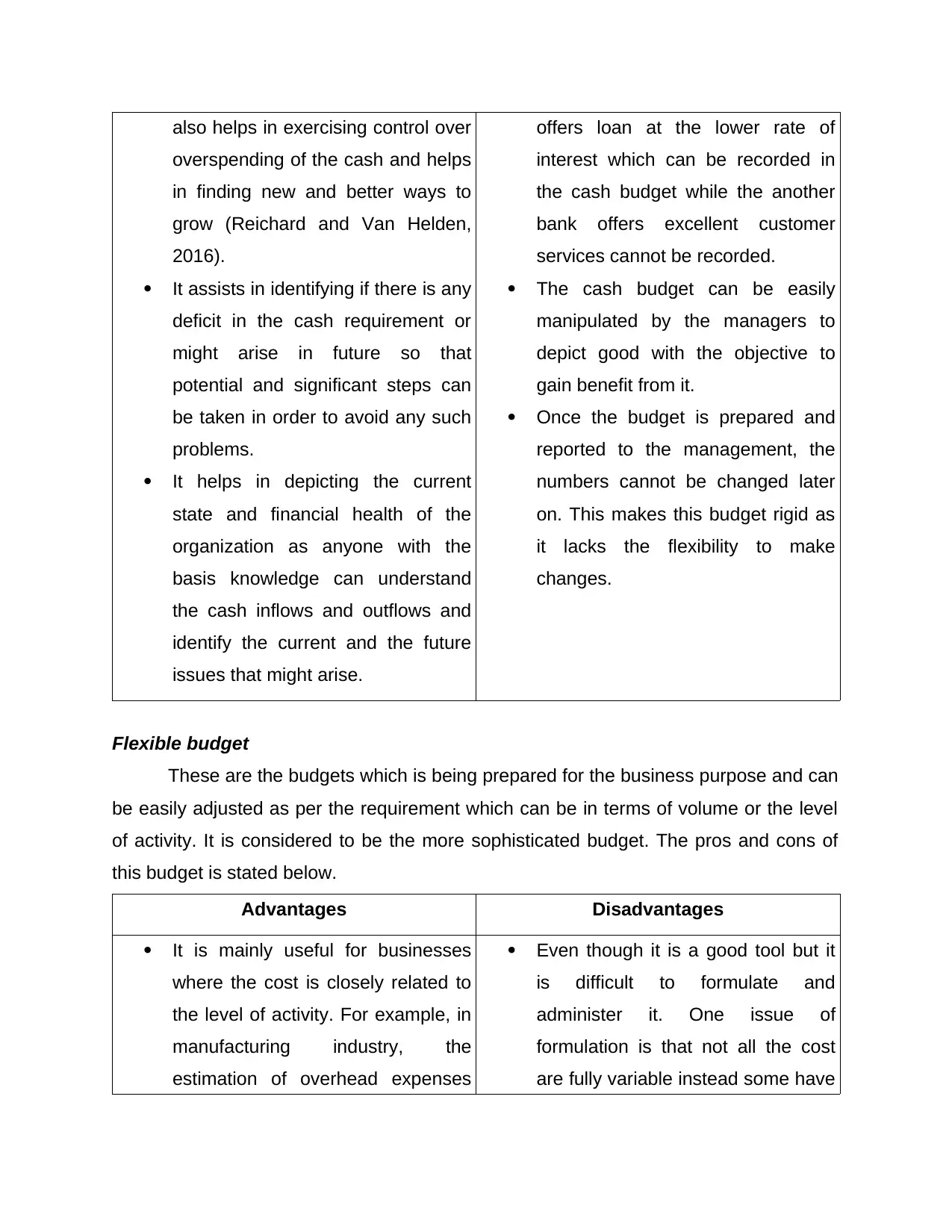

Flexible budget

These are the budgets which is being prepared for the business purpose and can

be easily adjusted as per the requirement which can be in terms of volume or the level

of activity. It is considered to be the more sophisticated budget. The pros and cons of

this budget is stated below.

Advantages Disadvantages

It is mainly useful for businesses

where the cost is closely related to

the level of activity. For example, in

manufacturing industry, the

estimation of overhead expenses

Even though it is a good tool but it

is difficult to formulate and

administer it. One issue of

formulation is that not all the cost

are fully variable instead some have

overspending of the cash and helps

in finding new and better ways to

grow (Reichard and Van Helden,

2016).

It assists in identifying if there is any

deficit in the cash requirement or

might arise in future so that

potential and significant steps can

be taken in order to avoid any such

problems.

It helps in depicting the current

state and financial health of the

organization as anyone with the

basis knowledge can understand

the cash inflows and outflows and

identify the current and the future

issues that might arise.

offers loan at the lower rate of

interest which can be recorded in

the cash budget while the another

bank offers excellent customer

services cannot be recorded.

The cash budget can be easily

manipulated by the managers to

depict good with the objective to

gain benefit from it.

Once the budget is prepared and

reported to the management, the

numbers cannot be changed later

on. This makes this budget rigid as

it lacks the flexibility to make

changes.

Flexible budget

These are the budgets which is being prepared for the business purpose and can

be easily adjusted as per the requirement which can be in terms of volume or the level

of activity. It is considered to be the more sophisticated budget. The pros and cons of

this budget is stated below.

Advantages Disadvantages

It is mainly useful for businesses

where the cost is closely related to

the level of activity. For example, in

manufacturing industry, the

estimation of overhead expenses

Even though it is a good tool but it

is difficult to formulate and

administer it. One issue of

formulation is that not all the cost

are fully variable instead some have

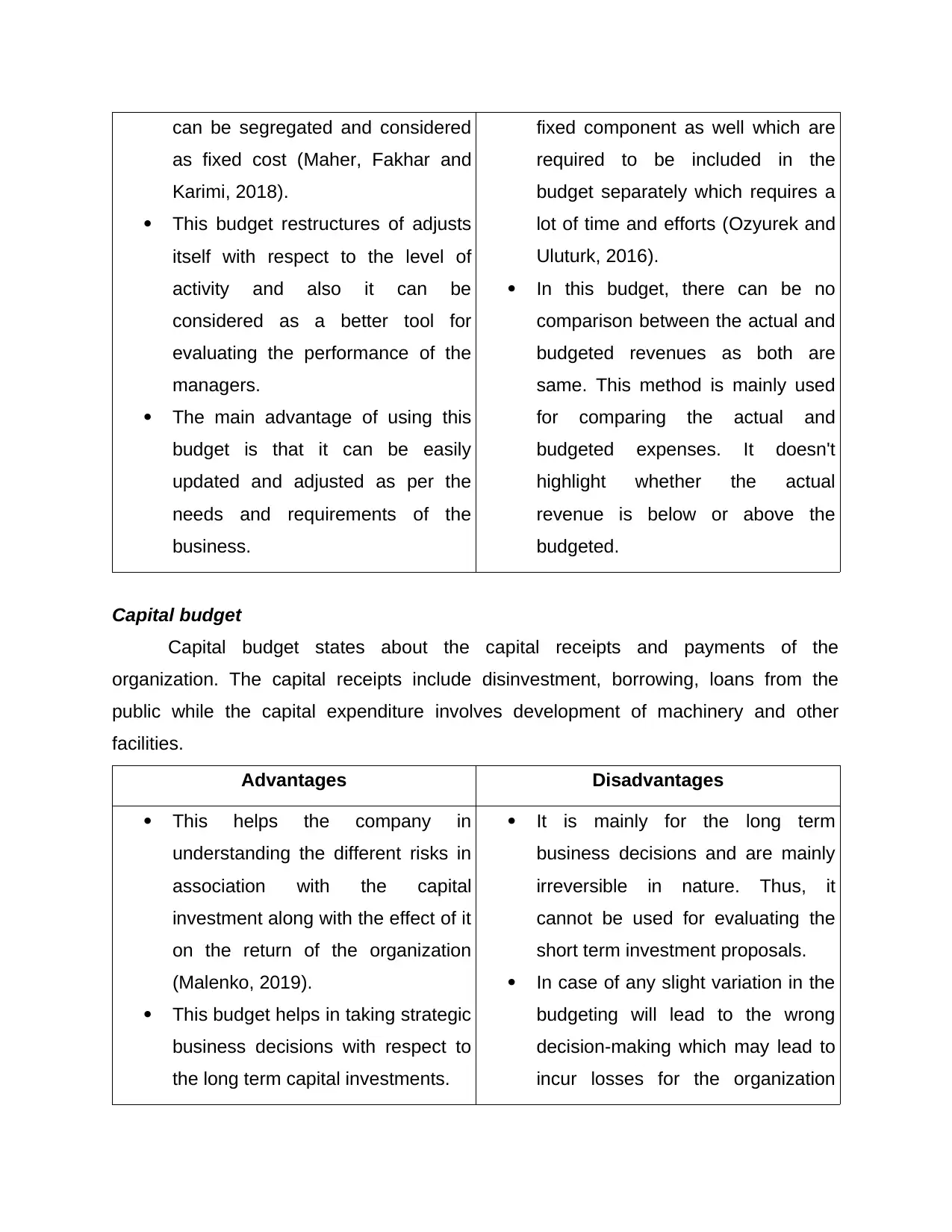

can be segregated and considered

as fixed cost (Maher, Fakhar and

Karimi, 2018).

This budget restructures of adjusts

itself with respect to the level of

activity and also it can be

considered as a better tool for

evaluating the performance of the

managers.

The main advantage of using this

budget is that it can be easily

updated and adjusted as per the

needs and requirements of the

business.

fixed component as well which are

required to be included in the

budget separately which requires a

lot of time and efforts (Ozyurek and

Uluturk, 2016).

In this budget, there can be no

comparison between the actual and

budgeted revenues as both are

same. This method is mainly used

for comparing the actual and

budgeted expenses. It doesn't

highlight whether the actual

revenue is below or above the

budgeted.

Capital budget

Capital budget states about the capital receipts and payments of the

organization. The capital receipts include disinvestment, borrowing, loans from the

public while the capital expenditure involves development of machinery and other

facilities.

Advantages Disadvantages

This helps the company in

understanding the different risks in

association with the capital

investment along with the effect of it

on the return of the organization

(Malenko, 2019).

This budget helps in taking strategic

business decisions with respect to

the long term capital investments.

It is mainly for the long term

business decisions and are mainly

irreversible in nature. Thus, it

cannot be used for evaluating the

short term investment proposals.

In case of any slight variation in the

budgeting will lead to the wrong

decision-making which may lead to

incur losses for the organization

as fixed cost (Maher, Fakhar and

Karimi, 2018).

This budget restructures of adjusts

itself with respect to the level of

activity and also it can be

considered as a better tool for

evaluating the performance of the

managers.

The main advantage of using this

budget is that it can be easily

updated and adjusted as per the

needs and requirements of the

business.

fixed component as well which are

required to be included in the

budget separately which requires a

lot of time and efforts (Ozyurek and

Uluturk, 2016).

In this budget, there can be no

comparison between the actual and

budgeted revenues as both are

same. This method is mainly used

for comparing the actual and

budgeted expenses. It doesn't

highlight whether the actual

revenue is below or above the

budgeted.

Capital budget

Capital budget states about the capital receipts and payments of the

organization. The capital receipts include disinvestment, borrowing, loans from the

public while the capital expenditure involves development of machinery and other

facilities.

Advantages Disadvantages

This helps the company in

understanding the different risks in

association with the capital

investment along with the effect of it

on the return of the organization

(Malenko, 2019).

This budget helps in taking strategic

business decisions with respect to

the long term capital investments.

It is mainly for the long term

business decisions and are mainly

irreversible in nature. Thus, it

cannot be used for evaluating the

short term investment proposals.

In case of any slight variation in the

budgeting will lead to the wrong

decision-making which may lead to

incur losses for the organization

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

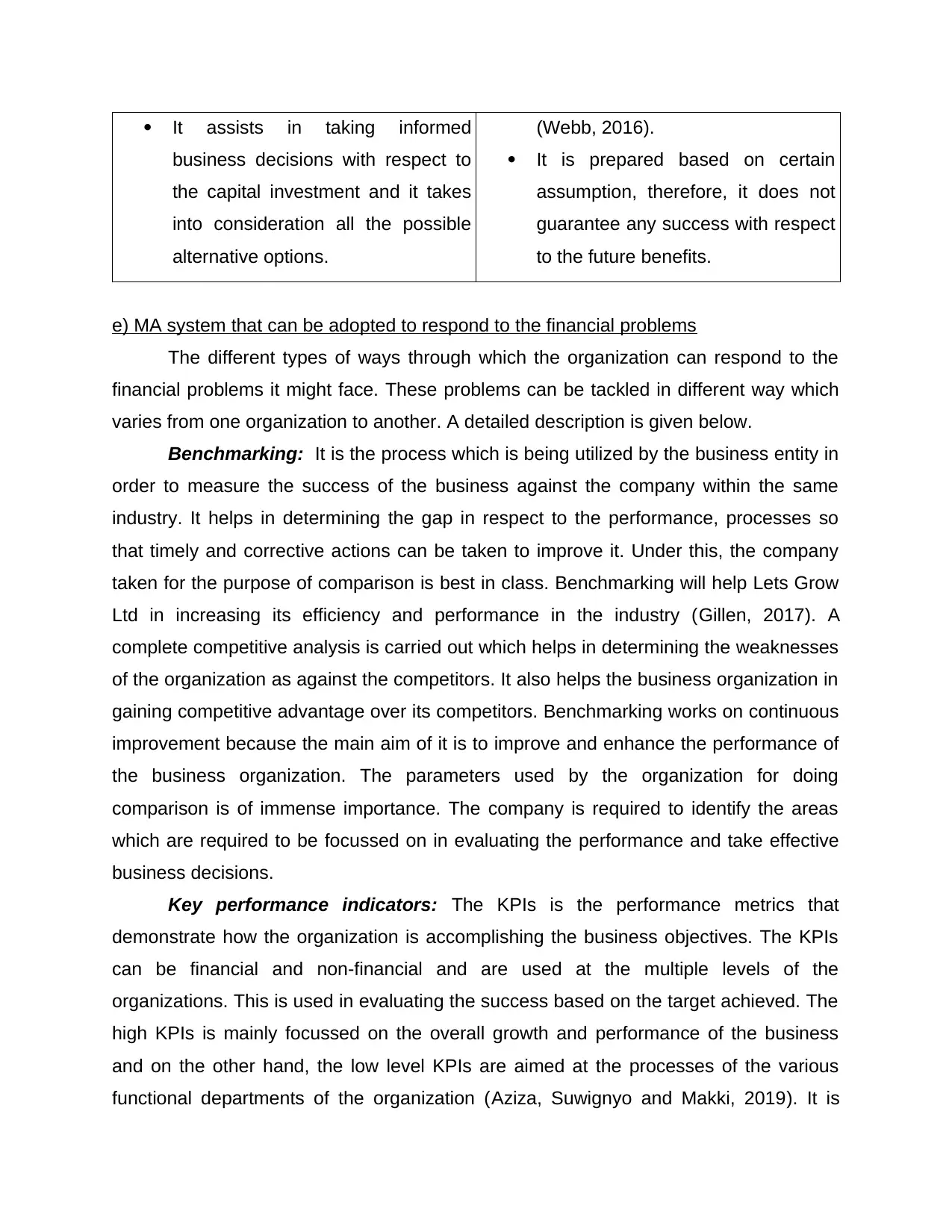

It assists in taking informed

business decisions with respect to

the capital investment and it takes

into consideration all the possible

alternative options.

(Webb, 2016).

It is prepared based on certain

assumption, therefore, it does not

guarantee any success with respect

to the future benefits.

e) MA system that can be adopted to respond to the financial problems

The different types of ways through which the organization can respond to the

financial problems it might face. These problems can be tackled in different way which

varies from one organization to another. A detailed description is given below.

Benchmarking: It is the process which is being utilized by the business entity in

order to measure the success of the business against the company within the same

industry. It helps in determining the gap in respect to the performance, processes so

that timely and corrective actions can be taken to improve it. Under this, the company

taken for the purpose of comparison is best in class. Benchmarking will help Lets Grow

Ltd in increasing its efficiency and performance in the industry (Gillen, 2017). A

complete competitive analysis is carried out which helps in determining the weaknesses

of the organization as against the competitors. It also helps the business organization in

gaining competitive advantage over its competitors. Benchmarking works on continuous

improvement because the main aim of it is to improve and enhance the performance of

the business organization. The parameters used by the organization for doing

comparison is of immense importance. The company is required to identify the areas

which are required to be focussed on in evaluating the performance and take effective

business decisions.

Key performance indicators: The KPIs is the performance metrics that

demonstrate how the organization is accomplishing the business objectives. The KPIs

can be financial and non-financial and are used at the multiple levels of the

organizations. This is used in evaluating the success based on the target achieved. The

high KPIs is mainly focussed on the overall growth and performance of the business

and on the other hand, the low level KPIs are aimed at the processes of the various

functional departments of the organization (Aziza, Suwignyo and Makki, 2019). It is

business decisions with respect to

the capital investment and it takes

into consideration all the possible

alternative options.

(Webb, 2016).

It is prepared based on certain

assumption, therefore, it does not

guarantee any success with respect

to the future benefits.

e) MA system that can be adopted to respond to the financial problems

The different types of ways through which the organization can respond to the

financial problems it might face. These problems can be tackled in different way which

varies from one organization to another. A detailed description is given below.

Benchmarking: It is the process which is being utilized by the business entity in

order to measure the success of the business against the company within the same

industry. It helps in determining the gap in respect to the performance, processes so

that timely and corrective actions can be taken to improve it. Under this, the company

taken for the purpose of comparison is best in class. Benchmarking will help Lets Grow

Ltd in increasing its efficiency and performance in the industry (Gillen, 2017). A

complete competitive analysis is carried out which helps in determining the weaknesses

of the organization as against the competitors. It also helps the business organization in

gaining competitive advantage over its competitors. Benchmarking works on continuous

improvement because the main aim of it is to improve and enhance the performance of

the business organization. The parameters used by the organization for doing

comparison is of immense importance. The company is required to identify the areas

which are required to be focussed on in evaluating the performance and take effective

business decisions.

Key performance indicators: The KPIs is the performance metrics that

demonstrate how the organization is accomplishing the business objectives. The KPIs

can be financial and non-financial and are used at the multiple levels of the

organizations. This is used in evaluating the success based on the target achieved. The

high KPIs is mainly focussed on the overall growth and performance of the business

and on the other hand, the low level KPIs are aimed at the processes of the various

functional departments of the organization (Aziza, Suwignyo and Makki, 2019). It is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

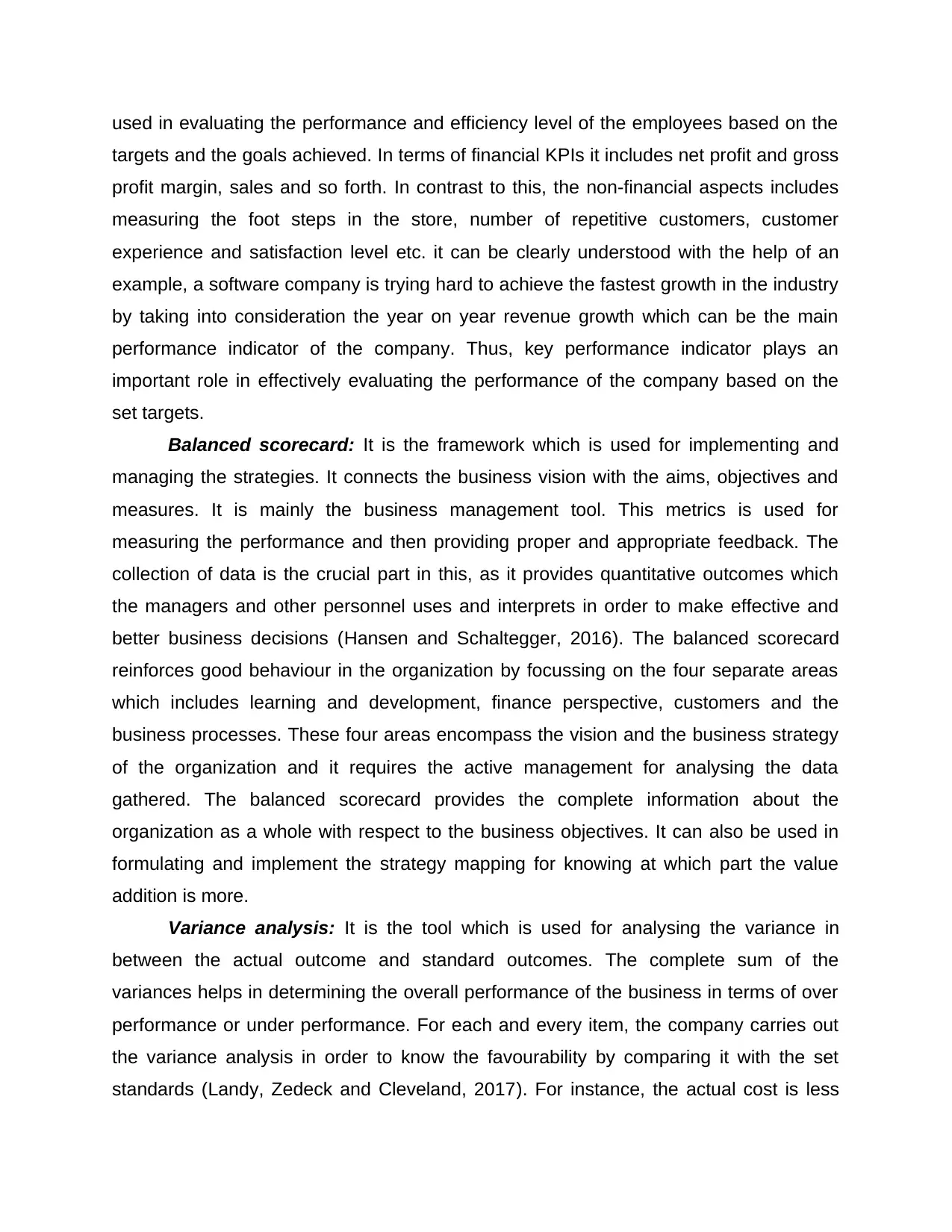

used in evaluating the performance and efficiency level of the employees based on the

targets and the goals achieved. In terms of financial KPIs it includes net profit and gross

profit margin, sales and so forth. In contrast to this, the non-financial aspects includes

measuring the foot steps in the store, number of repetitive customers, customer

experience and satisfaction level etc. it can be clearly understood with the help of an

example, a software company is trying hard to achieve the fastest growth in the industry

by taking into consideration the year on year revenue growth which can be the main

performance indicator of the company. Thus, key performance indicator plays an

important role in effectively evaluating the performance of the company based on the

set targets.

Balanced scorecard: It is the framework which is used for implementing and

managing the strategies. It connects the business vision with the aims, objectives and

measures. It is mainly the business management tool. This metrics is used for

measuring the performance and then providing proper and appropriate feedback. The

collection of data is the crucial part in this, as it provides quantitative outcomes which

the managers and other personnel uses and interprets in order to make effective and

better business decisions (Hansen and Schaltegger, 2016). The balanced scorecard

reinforces good behaviour in the organization by focussing on the four separate areas

which includes learning and development, finance perspective, customers and the

business processes. These four areas encompass the vision and the business strategy

of the organization and it requires the active management for analysing the data

gathered. The balanced scorecard provides the complete information about the

organization as a whole with respect to the business objectives. It can also be used in

formulating and implement the strategy mapping for knowing at which part the value

addition is more.

Variance analysis: It is the tool which is used for analysing the variance in

between the actual outcome and standard outcomes. The complete sum of the

variances helps in determining the overall performance of the business in terms of over

performance or under performance. For each and every item, the company carries out

the variance analysis in order to know the favourability by comparing it with the set

standards (Landy, Zedeck and Cleveland, 2017). For instance, the actual cost is less

targets and the goals achieved. In terms of financial KPIs it includes net profit and gross

profit margin, sales and so forth. In contrast to this, the non-financial aspects includes

measuring the foot steps in the store, number of repetitive customers, customer

experience and satisfaction level etc. it can be clearly understood with the help of an

example, a software company is trying hard to achieve the fastest growth in the industry

by taking into consideration the year on year revenue growth which can be the main

performance indicator of the company. Thus, key performance indicator plays an

important role in effectively evaluating the performance of the company based on the

set targets.

Balanced scorecard: It is the framework which is used for implementing and

managing the strategies. It connects the business vision with the aims, objectives and

measures. It is mainly the business management tool. This metrics is used for

measuring the performance and then providing proper and appropriate feedback. The

collection of data is the crucial part in this, as it provides quantitative outcomes which

the managers and other personnel uses and interprets in order to make effective and

better business decisions (Hansen and Schaltegger, 2016). The balanced scorecard

reinforces good behaviour in the organization by focussing on the four separate areas

which includes learning and development, finance perspective, customers and the

business processes. These four areas encompass the vision and the business strategy

of the organization and it requires the active management for analysing the data

gathered. The balanced scorecard provides the complete information about the

organization as a whole with respect to the business objectives. It can also be used in

formulating and implement the strategy mapping for knowing at which part the value

addition is more.

Variance analysis: It is the tool which is used for analysing the variance in

between the actual outcome and standard outcomes. The complete sum of the

variances helps in determining the overall performance of the business in terms of over

performance or under performance. For each and every item, the company carries out

the variance analysis in order to know the favourability by comparing it with the set

standards (Landy, Zedeck and Cleveland, 2017). For instance, the actual cost is less

than the standard cost in terms of material used will result into favourable price

variance, in other words, it is cost saving for the organization. In another situation like, if

the standard quantity was 10000 pieces of raw input and 15000 pieces of input was

required in the production process, this would mean an unfavourable quantity variance

since more input was being used as compared to the anticipated one. On determining

the variance, the corrective actions are being taken by the management in identifying

the causes for the deviation and remedial steps that can be taken in order to reduce it.

f) Critically evaluating the financial position of Lets Grow Ltd as per the forecasted cash

budget

Based on the foretasted cash budget of Lets Grow Ltd, it can be interpreted that

the there has been a drastic change in these 6 months. In March, April and May, the

company was having cash surplus and in the last three months it was negative, that

means the company was having deficit cash. It can be seen that there is an increase in

the payment for purchases made by the company. In last two months, that is, July and

August, the closing cash balance becomes negative which is -5000 and -21000

respectively. Thus, it can be said that Lets Grow Ltd is not effective enough in managing

its cash requirements and this cause the problem of cash crunch in the organization as

the company might not be able to carry out its business activities in effective way. Also,

there are chances that the company might be required to procure additional funds for

smoothing running its daily business activities. Thus, currently the position of the

company is not good.

CONCLUSION

It can be summed up from the above that management accounting (MA) is very

useful for the business organization in order to meet the business requirements. There

are various management accounting system that can be implemented by the

organization which meet its operation requirements. The MA systems that can be used

are cost accounting, inventory management, job costing and so forth. Each of these

systems has their own benefits. The different reports that are being prepared under

management accounting will provide valuable information to the business which assist

in taking better and improved business decisions. The cash budget is very useful for the

business organization in terms of analysing the liquidity position of the business and is

variance, in other words, it is cost saving for the organization. In another situation like, if

the standard quantity was 10000 pieces of raw input and 15000 pieces of input was

required in the production process, this would mean an unfavourable quantity variance

since more input was being used as compared to the anticipated one. On determining

the variance, the corrective actions are being taken by the management in identifying

the causes for the deviation and remedial steps that can be taken in order to reduce it.

f) Critically evaluating the financial position of Lets Grow Ltd as per the forecasted cash

budget

Based on the foretasted cash budget of Lets Grow Ltd, it can be interpreted that

the there has been a drastic change in these 6 months. In March, April and May, the

company was having cash surplus and in the last three months it was negative, that

means the company was having deficit cash. It can be seen that there is an increase in

the payment for purchases made by the company. In last two months, that is, July and

August, the closing cash balance becomes negative which is -5000 and -21000

respectively. Thus, it can be said that Lets Grow Ltd is not effective enough in managing

its cash requirements and this cause the problem of cash crunch in the organization as

the company might not be able to carry out its business activities in effective way. Also,

there are chances that the company might be required to procure additional funds for

smoothing running its daily business activities. Thus, currently the position of the

company is not good.

CONCLUSION

It can be summed up from the above that management accounting (MA) is very

useful for the business organization in order to meet the business requirements. There

are various management accounting system that can be implemented by the

organization which meet its operation requirements. The MA systems that can be used

are cost accounting, inventory management, job costing and so forth. Each of these

systems has their own benefits. The different reports that are being prepared under

management accounting will provide valuable information to the business which assist

in taking better and improved business decisions. The cash budget is very useful for the

business organization in terms of analysing the liquidity position of the business and is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.