Management Accounting | Assessment 1

VerifiedAdded on 2022/10/06

|12

|2387

|14

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Authors Note:

Management Accounting

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING

1

Table of Contents

Question 1: Stating one of the ethical standards, as provided by the Institute of Management

Accountants................................................................................................................................3

Question 2:.................................................................................................................................3

a) Classifying the 8 activities among the four types of quality costs:........................................3

b) Explaining the relationship between the four types of quality costs and changes throughout

the years:....................................................................................................................................4

Question 3:.................................................................................................................................4

a) Explaining John and Paul’s differing points of view of quality costs:..................................4

b) Explaining the measures that are considered in Year 4:........................................................5

Question 4:.................................................................................................................................5

a) Estimating the variable and the fixed portions of the delivery expense for Fridges-R-Fun:. 5

b) Reviewing Ringo's estimated delivery expenses using the high-low method:......................5

Question 5:.................................................................................................................................6

a) Calculating the predetermined overhead rates used for welding and assembly:...................6

b) Calculating the total overhead cost applied to this specific job:............................................6

c) Calculating the total manufacturing cost recorded for this specific job:...............................6

d) Considering the specific job containing 100 units, while calculating the unit product cost: 7

e) Explaining the cause a difference between the specific job and the industry benchmark for

the assembly overhead cost:.......................................................................................................7

Question 6:.................................................................................................................................8

a) Listing and explaining three limitations of using cost-plus pricing, as discussed by

Dholakia:....................................................................................................................................8

b) Explaining how value-based pricing would benefit from the costs of quality changes

implemented by Ringo:..............................................................................................................8

1

Table of Contents

Question 1: Stating one of the ethical standards, as provided by the Institute of Management

Accountants................................................................................................................................3

Question 2:.................................................................................................................................3

a) Classifying the 8 activities among the four types of quality costs:........................................3

b) Explaining the relationship between the four types of quality costs and changes throughout

the years:....................................................................................................................................4

Question 3:.................................................................................................................................4

a) Explaining John and Paul’s differing points of view of quality costs:..................................4

b) Explaining the measures that are considered in Year 4:........................................................5

Question 4:.................................................................................................................................5

a) Estimating the variable and the fixed portions of the delivery expense for Fridges-R-Fun:. 5

b) Reviewing Ringo's estimated delivery expenses using the high-low method:......................5

Question 5:.................................................................................................................................6

a) Calculating the predetermined overhead rates used for welding and assembly:...................6

b) Calculating the total overhead cost applied to this specific job:............................................6

c) Calculating the total manufacturing cost recorded for this specific job:...............................6

d) Considering the specific job containing 100 units, while calculating the unit product cost: 7

e) Explaining the cause a difference between the specific job and the industry benchmark for

the assembly overhead cost:.......................................................................................................7

Question 6:.................................................................................................................................8

a) Listing and explaining three limitations of using cost-plus pricing, as discussed by

Dholakia:....................................................................................................................................8

b) Explaining how value-based pricing would benefit from the costs of quality changes

implemented by Ringo:..............................................................................................................8

MANAGEMENT ACCOUNTING

2

Question 7:.................................................................................................................................9

a) Determining the amount of under applied or over applied manufacturing overhead for Year

1:.................................................................................................................................................9

b) Implication of having large over applied or under applied overhead to the management

planning and product costing:..................................................................................................10

References:...............................................................................................................................11

2

Question 7:.................................................................................................................................9

a) Determining the amount of under applied or over applied manufacturing overhead for Year

1:.................................................................................................................................................9

b) Implication of having large over applied or under applied overhead to the management

planning and product costing:..................................................................................................10

References:...............................................................................................................................11

MANAGEMENT ACCOUNTING

3

Question 1: Stating one of the ethical standards, as provided by the Institute of

Management Accountants

According to the ethical standards, the employment of a plumber who is licensed to

only provide plumbing jobs and not identify the relevant unnecessary cost that is in curing in

the organization is relatively unethical. Hiring George would directly initiate and jeopardize

the standard that was needed to comply with the detection of relevant and necessary cost as

he excels in plumbing jobs and not identifying any kind of unnecessary cost associated with

production and other expenses. Therefore, it is unethical under both ethical standards for

professional codes of conduct in accounting do not use an accounting professional to identify

the relevant cost and unnecessary expenses that is being conducted by the organization. The

use of George would directly initiate frauds and scandals within the organization, as he will

not be able to cope up with the relevant accounting needs that are required for identifying any

kind of manipulations conducted within the organization. Additionally, he would be

supportive to Paul and allow him to embezzle the funds of the organization (Lachman 2014).

Question 2:

a) Classifying the 8 activities among the four types of quality costs:

Types of quality

costs

Activities

System Systems development

Technical support Technical support to suppliers of compressors

Technical support to suppliers of pipes

Customers support Field testing at customers’ sites

3

Question 1: Stating one of the ethical standards, as provided by the Institute of

Management Accountants

According to the ethical standards, the employment of a plumber who is licensed to

only provide plumbing jobs and not identify the relevant unnecessary cost that is in curing in

the organization is relatively unethical. Hiring George would directly initiate and jeopardize

the standard that was needed to comply with the detection of relevant and necessary cost as

he excels in plumbing jobs and not identifying any kind of unnecessary cost associated with

production and other expenses. Therefore, it is unethical under both ethical standards for

professional codes of conduct in accounting do not use an accounting professional to identify

the relevant cost and unnecessary expenses that is being conducted by the organization. The

use of George would directly initiate frauds and scandals within the organization, as he will

not be able to cope up with the relevant accounting needs that are required for identifying any

kind of manipulations conducted within the organization. Additionally, he would be

supportive to Paul and allow him to embezzle the funds of the organization (Lachman 2014).

Question 2:

a) Classifying the 8 activities among the four types of quality costs:

Types of quality

costs

Activities

System Systems development

Technical support Technical support to suppliers of compressors

Technical support to suppliers of pipes

Customers support Field testing at customers’ sites

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING

4

Inspection on assembling line

Rework on assembling line

Warranty Warranty repairs of fridges

Warranty replacements of fridges

b) Explaining the relationship between the four types of quality costs and changes

throughout the years:

The relationship between the identified four types of quality cost is relative Lee

changing due to the implementation process. Currently the aim of the organization is to

improve system development, technical support, field support, and warranties for adequately

reducing the level of expenses that was previously conducted on warranties and rework

assembly line. The reduction and the relevant levels of warranty expenses is due to the

improvements that was conducted in the production line in the support provided to the

suppliers and customers (Ross 2017).

Question 3:

a) Explaining John and Paul’s differing points of view of quality costs:

There is a relevant difference no point of John and Paul regarding the quality cost,

John is more focused on reworking and Paul is more focused open driving the relevant cost

that is increasing due to the increment in reworks. Therefore, John is only trying to increase

the quality cost that is incurred in yearly basis. However, Paul is more focused on reducing

the level of cost that is incurred due to the excessive he works that is conducted by the

customers.

4

Inspection on assembling line

Rework on assembling line

Warranty Warranty repairs of fridges

Warranty replacements of fridges

b) Explaining the relationship between the four types of quality costs and changes

throughout the years:

The relationship between the identified four types of quality cost is relative Lee

changing due to the implementation process. Currently the aim of the organization is to

improve system development, technical support, field support, and warranties for adequately

reducing the level of expenses that was previously conducted on warranties and rework

assembly line. The reduction and the relevant levels of warranty expenses is due to the

improvements that was conducted in the production line in the support provided to the

suppliers and customers (Ross 2017).

Question 3:

a) Explaining John and Paul’s differing points of view of quality costs:

There is a relevant difference no point of John and Paul regarding the quality cost,

John is more focused on reworking and Paul is more focused open driving the relevant cost

that is increasing due to the increment in reworks. Therefore, John is only trying to increase

the quality cost that is incurred in yearly basis. However, Paul is more focused on reducing

the level of cost that is incurred due to the excessive he works that is conducted by the

customers.

MANAGEMENT ACCOUNTING

5

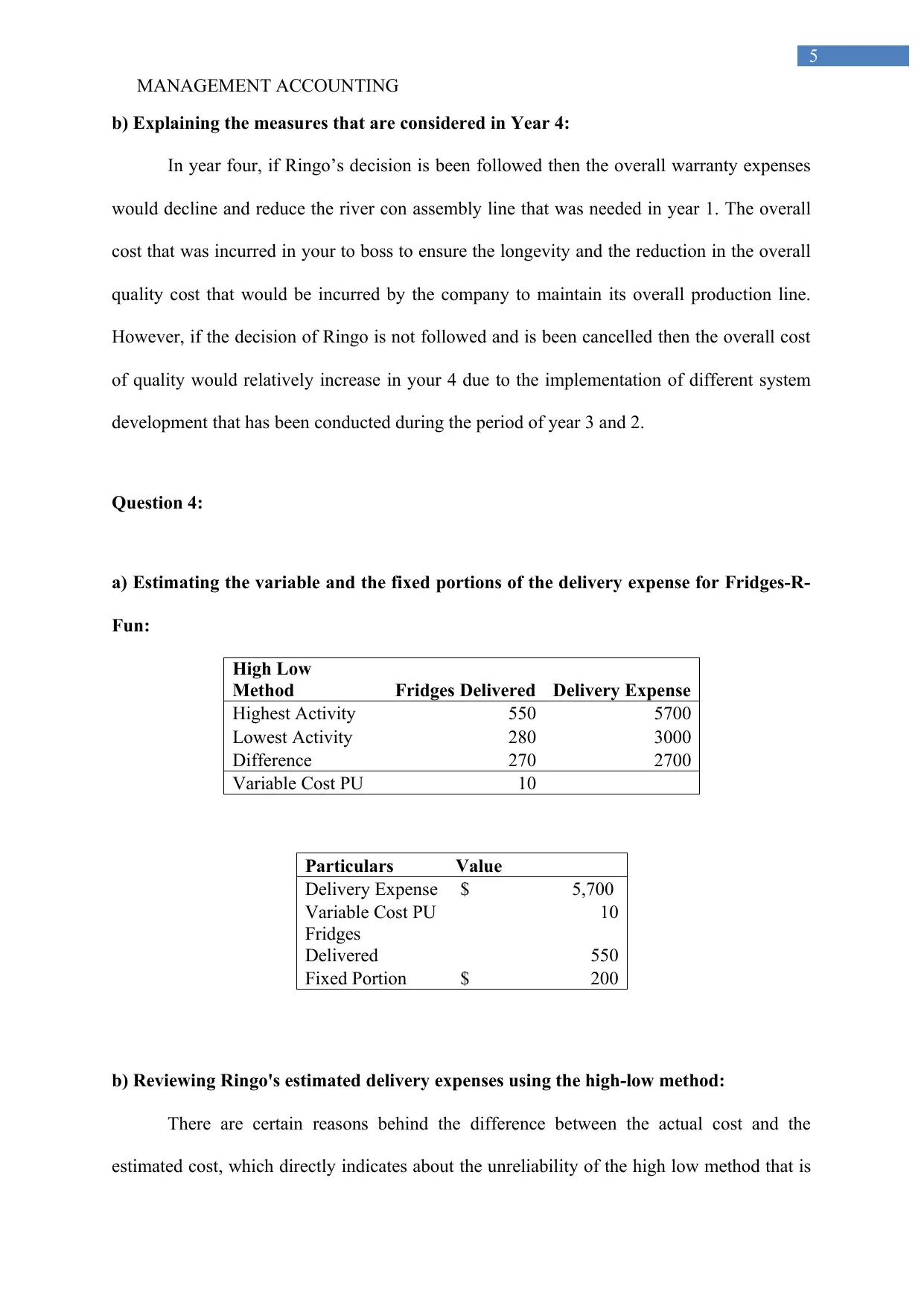

b) Explaining the measures that are considered in Year 4:

In year four, if Ringo’s decision is been followed then the overall warranty expenses

would decline and reduce the river con assembly line that was needed in year 1. The overall

cost that was incurred in your to boss to ensure the longevity and the reduction in the overall

quality cost that would be incurred by the company to maintain its overall production line.

However, if the decision of Ringo is not followed and is been cancelled then the overall cost

of quality would relatively increase in your 4 due to the implementation of different system

development that has been conducted during the period of year 3 and 2.

Question 4:

a) Estimating the variable and the fixed portions of the delivery expense for Fridges-R-

Fun:

High Low

Method Fridges Delivered Delivery Expense

Highest Activity 550 5700

Lowest Activity 280 3000

Difference 270 2700

Variable Cost PU 10

Particulars Value

Delivery Expense $ 5,700

Variable Cost PU 10

Fridges

Delivered 550

Fixed Portion $ 200

b) Reviewing Ringo's estimated delivery expenses using the high-low method:

There are certain reasons behind the difference between the actual cost and the

estimated cost, which directly indicates about the unreliability of the high low method that is

5

b) Explaining the measures that are considered in Year 4:

In year four, if Ringo’s decision is been followed then the overall warranty expenses

would decline and reduce the river con assembly line that was needed in year 1. The overall

cost that was incurred in your to boss to ensure the longevity and the reduction in the overall

quality cost that would be incurred by the company to maintain its overall production line.

However, if the decision of Ringo is not followed and is been cancelled then the overall cost

of quality would relatively increase in your 4 due to the implementation of different system

development that has been conducted during the period of year 3 and 2.

Question 4:

a) Estimating the variable and the fixed portions of the delivery expense for Fridges-R-

Fun:

High Low

Method Fridges Delivered Delivery Expense

Highest Activity 550 5700

Lowest Activity 280 3000

Difference 270 2700

Variable Cost PU 10

Particulars Value

Delivery Expense $ 5,700

Variable Cost PU 10

Fridges

Delivered 550

Fixed Portion $ 200

b) Reviewing Ringo's estimated delivery expenses using the high-low method:

There are certain reasons behind the difference between the actual cost and the

estimated cost, which directly indicates about the unreliability of the high low method that is

MANAGEMENT ACCOUNTING

6

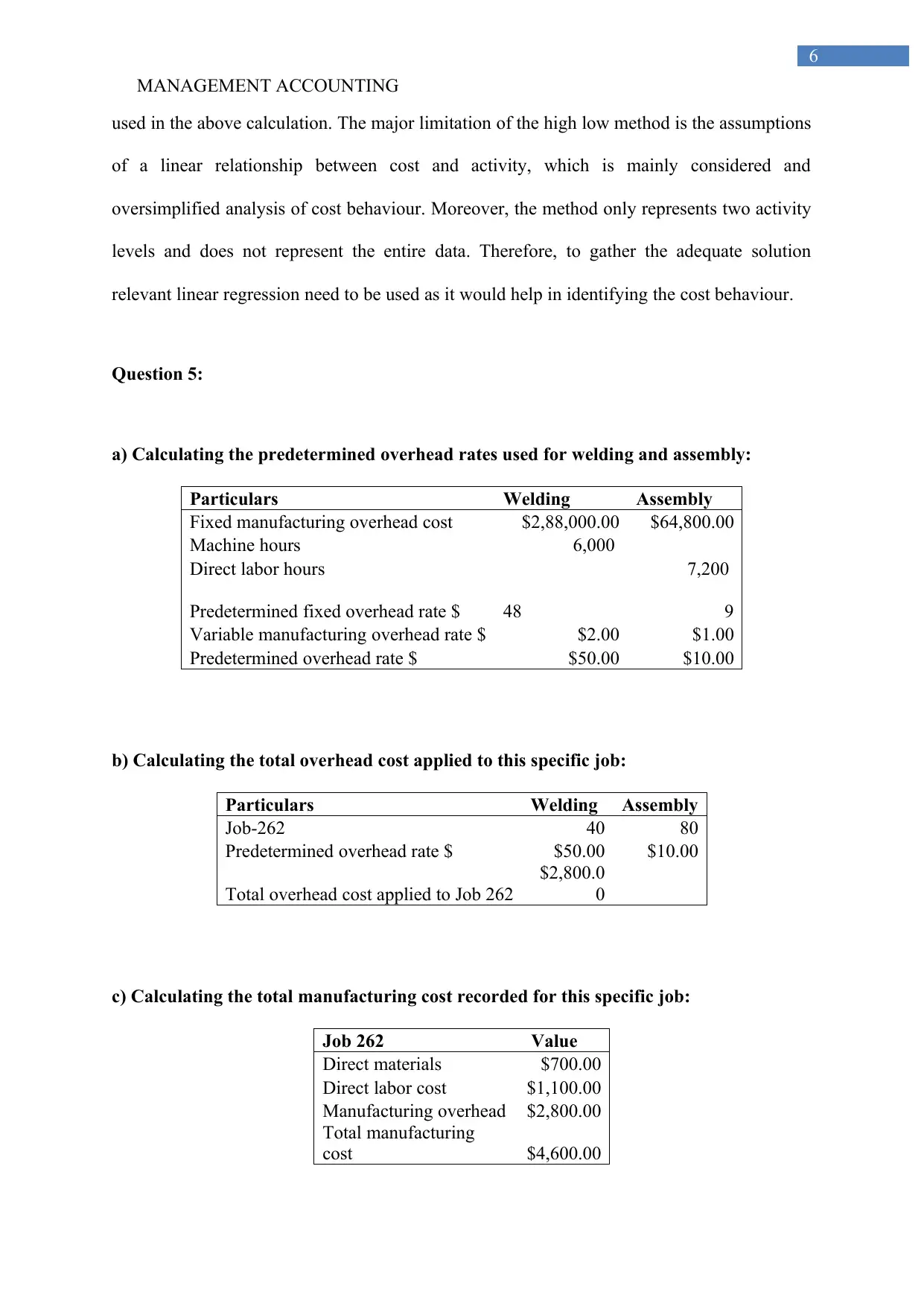

used in the above calculation. The major limitation of the high low method is the assumptions

of a linear relationship between cost and activity, which is mainly considered and

oversimplified analysis of cost behaviour. Moreover, the method only represents two activity

levels and does not represent the entire data. Therefore, to gather the adequate solution

relevant linear regression need to be used as it would help in identifying the cost behaviour.

Question 5:

a) Calculating the predetermined overhead rates used for welding and assembly:

Particulars Welding Assembly

Fixed manufacturing overhead cost $2,88,000.00 $64,800.00

Machine hours 6,000

Direct labor hours 7,200

Predetermined fixed overhead rate $ 48 9

Variable manufacturing overhead rate $ $2.00 $1.00

Predetermined overhead rate $ $50.00 $10.00

b) Calculating the total overhead cost applied to this specific job:

Particulars Welding Assembly

Job-262 40 80

Predetermined overhead rate $ $50.00 $10.00

Total overhead cost applied to Job 262

$2,800.0

0

c) Calculating the total manufacturing cost recorded for this specific job:

Job 262 Value

Direct materials $700.00

Direct labor cost $1,100.00

Manufacturing overhead $2,800.00

Total manufacturing

cost $4,600.00

6

used in the above calculation. The major limitation of the high low method is the assumptions

of a linear relationship between cost and activity, which is mainly considered and

oversimplified analysis of cost behaviour. Moreover, the method only represents two activity

levels and does not represent the entire data. Therefore, to gather the adequate solution

relevant linear regression need to be used as it would help in identifying the cost behaviour.

Question 5:

a) Calculating the predetermined overhead rates used for welding and assembly:

Particulars Welding Assembly

Fixed manufacturing overhead cost $2,88,000.00 $64,800.00

Machine hours 6,000

Direct labor hours 7,200

Predetermined fixed overhead rate $ 48 9

Variable manufacturing overhead rate $ $2.00 $1.00

Predetermined overhead rate $ $50.00 $10.00

b) Calculating the total overhead cost applied to this specific job:

Particulars Welding Assembly

Job-262 40 80

Predetermined overhead rate $ $50.00 $10.00

Total overhead cost applied to Job 262

$2,800.0

0

c) Calculating the total manufacturing cost recorded for this specific job:

Job 262 Value

Direct materials $700.00

Direct labor cost $1,100.00

Manufacturing overhead $2,800.00

Total manufacturing

cost $4,600.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

7

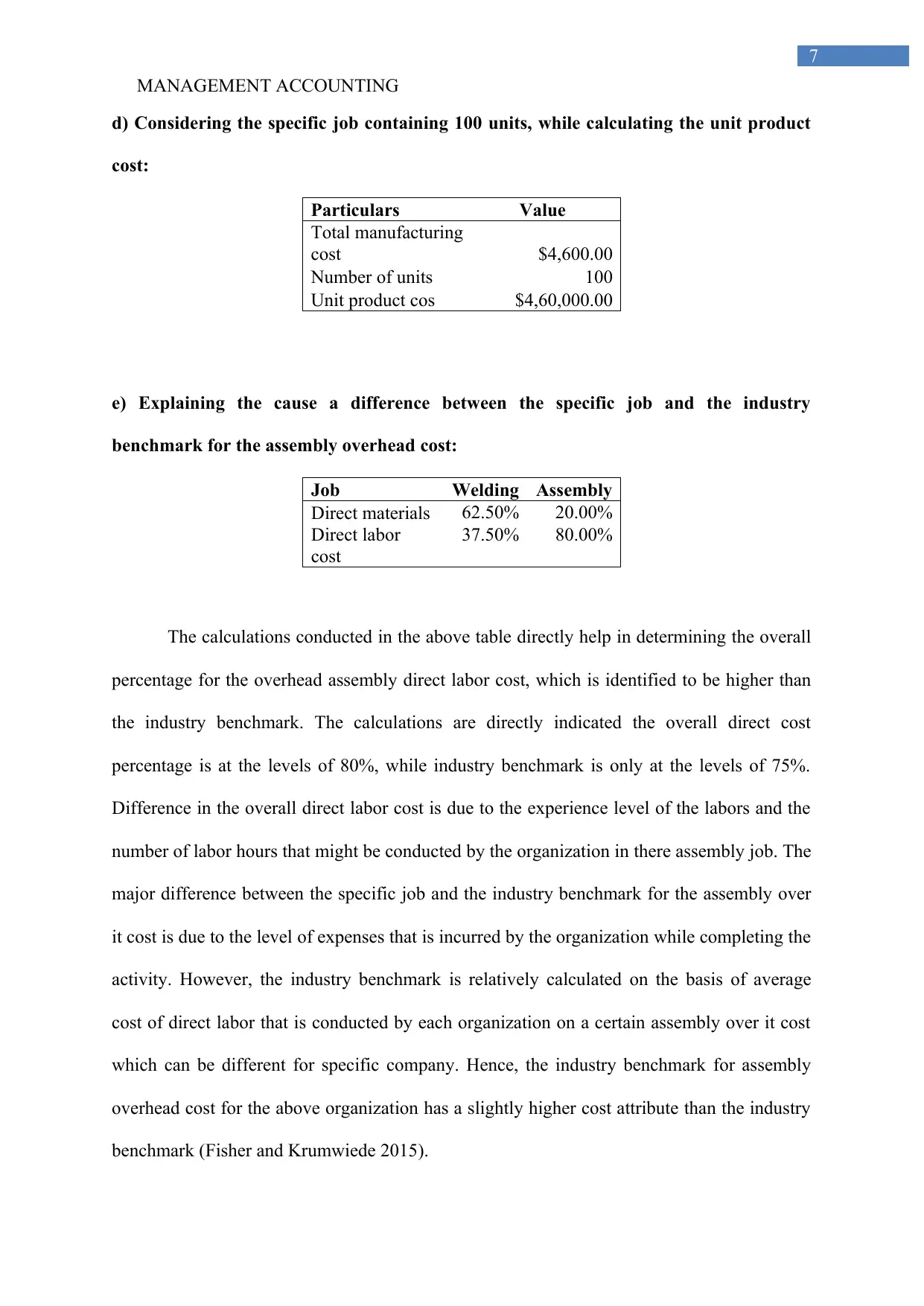

d) Considering the specific job containing 100 units, while calculating the unit product

cost:

Particulars Value

Total manufacturing

cost $4,600.00

Number of units 100

Unit product cos $4,60,000.00

e) Explaining the cause a difference between the specific job and the industry

benchmark for the assembly overhead cost:

Job Welding Assembly

Direct materials 62.50% 20.00%

Direct labor

cost

37.50% 80.00%

The calculations conducted in the above table directly help in determining the overall

percentage for the overhead assembly direct labor cost, which is identified to be higher than

the industry benchmark. The calculations are directly indicated the overall direct cost

percentage is at the levels of 80%, while industry benchmark is only at the levels of 75%.

Difference in the overall direct labor cost is due to the experience level of the labors and the

number of labor hours that might be conducted by the organization in there assembly job. The

major difference between the specific job and the industry benchmark for the assembly over

it cost is due to the level of expenses that is incurred by the organization while completing the

activity. However, the industry benchmark is relatively calculated on the basis of average

cost of direct labor that is conducted by each organization on a certain assembly over it cost

which can be different for specific company. Hence, the industry benchmark for assembly

overhead cost for the above organization has a slightly higher cost attribute than the industry

benchmark (Fisher and Krumwiede 2015).

7

d) Considering the specific job containing 100 units, while calculating the unit product

cost:

Particulars Value

Total manufacturing

cost $4,600.00

Number of units 100

Unit product cos $4,60,000.00

e) Explaining the cause a difference between the specific job and the industry

benchmark for the assembly overhead cost:

Job Welding Assembly

Direct materials 62.50% 20.00%

Direct labor

cost

37.50% 80.00%

The calculations conducted in the above table directly help in determining the overall

percentage for the overhead assembly direct labor cost, which is identified to be higher than

the industry benchmark. The calculations are directly indicated the overall direct cost

percentage is at the levels of 80%, while industry benchmark is only at the levels of 75%.

Difference in the overall direct labor cost is due to the experience level of the labors and the

number of labor hours that might be conducted by the organization in there assembly job. The

major difference between the specific job and the industry benchmark for the assembly over

it cost is due to the level of expenses that is incurred by the organization while completing the

activity. However, the industry benchmark is relatively calculated on the basis of average

cost of direct labor that is conducted by each organization on a certain assembly over it cost

which can be different for specific company. Hence, the industry benchmark for assembly

overhead cost for the above organization has a slightly higher cost attribute than the industry

benchmark (Fisher and Krumwiede 2015).

MANAGEMENT ACCOUNTING

8

Question 6:

a) Listing and explaining three limitations of using cost-plus pricing, as discussed by

Dholakia:

The three justified drawbacks that were appointed by Dholakiya regarding cost plus

pricing are depicted as follows.

Cost plus pricing is revised for some electrometric reason as it directly discourages

efficiency, as cost containment would lower cost, which directly reduces the level of

profits and revenues that could be generated by the organization.

The second drawback that was identified was the guarantee that was provided by the cost

plus measure, which directly indicates about the sales volume beforehand, and the overall

cost that should be incurred in the process. However, cost plus prices does not provide

adequate guarantee of the cost covering of the earnings of a profit, which reduces its

functionality and efficiency in the organization (Hbr.org 2018).

The third drawback that was highlighted regarding the cost plus pricing calculation is the

ignorance of both customer's willingness to pay and the competitor’s prices. Therefore,

instead of cost plus pricing methods managers directly utilize the value based pricing

condition, which helps in accounting for all the relevant factors that influences the

decision making conditions of a manager.

b) Explaining how value-based pricing would benefit from the costs of quality changes

implemented by Ringo:

Ringo directly provided adequate information about the overall quality coarse

activities that can be conducted by the organization to reduce the level of spending that was

conducted on warranties. Ringo directly introduced and provided information regarding the

relevant changes that needs to be implemented within the organization for adequately

8

Question 6:

a) Listing and explaining three limitations of using cost-plus pricing, as discussed by

Dholakia:

The three justified drawbacks that were appointed by Dholakiya regarding cost plus

pricing are depicted as follows.

Cost plus pricing is revised for some electrometric reason as it directly discourages

efficiency, as cost containment would lower cost, which directly reduces the level of

profits and revenues that could be generated by the organization.

The second drawback that was identified was the guarantee that was provided by the cost

plus measure, which directly indicates about the sales volume beforehand, and the overall

cost that should be incurred in the process. However, cost plus prices does not provide

adequate guarantee of the cost covering of the earnings of a profit, which reduces its

functionality and efficiency in the organization (Hbr.org 2018).

The third drawback that was highlighted regarding the cost plus pricing calculation is the

ignorance of both customer's willingness to pay and the competitor’s prices. Therefore,

instead of cost plus pricing methods managers directly utilize the value based pricing

condition, which helps in accounting for all the relevant factors that influences the

decision making conditions of a manager.

b) Explaining how value-based pricing would benefit from the costs of quality changes

implemented by Ringo:

Ringo directly provided adequate information about the overall quality coarse

activities that can be conducted by the organization to reduce the level of spending that was

conducted on warranties. Ringo directly introduced and provided information regarding the

relevant changes that needs to be implemented within the organization for adequately

MANAGEMENT ACCOUNTING

9

reducing the overall extra expenses and minimize the level of quality costs. The measures

such as development of new system for streamlining the assembly line, providing technical

support for minimizing the receiving of faulty materials, field testing the fridges on customer

sites and inspecting the fridges on the assembly line. These measures directly allowed Ringo

to minimize the level of quality cost in year 3, as the overall expenses in warranties declined.

Therefore, value-based pricing method would directly allow the organizations to improve

their current pricing conditions and generate higher level of income in the long run.

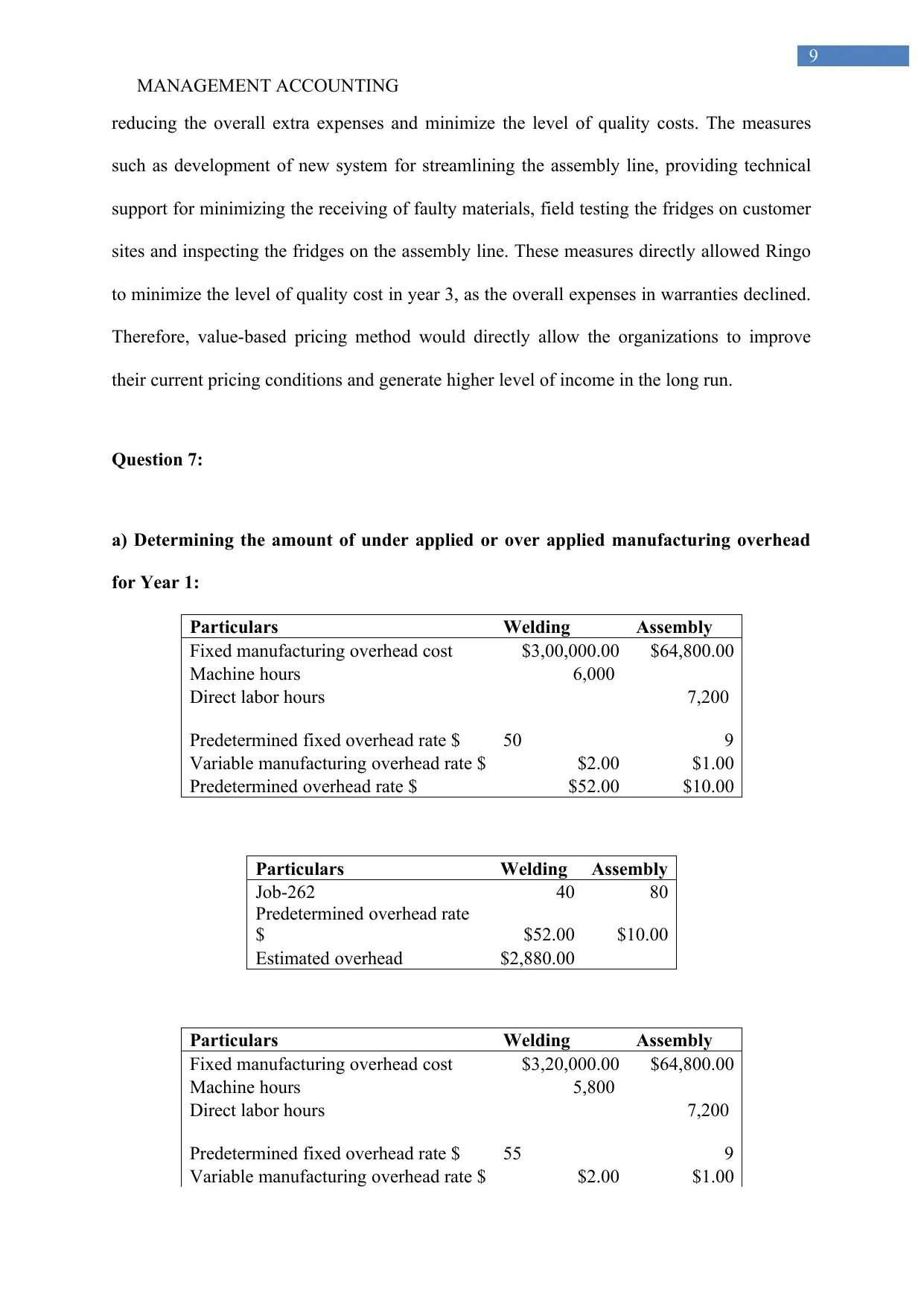

Question 7:

a) Determining the amount of under applied or over applied manufacturing overhead

for Year 1:

Particulars Welding Assembly

Fixed manufacturing overhead cost $3,00,000.00 $64,800.00

Machine hours 6,000

Direct labor hours 7,200

Predetermined fixed overhead rate $ 50 9

Variable manufacturing overhead rate $ $2.00 $1.00

Predetermined overhead rate $ $52.00 $10.00

Particulars Welding Assembly

Job-262 40 80

Predetermined overhead rate

$ $52.00 $10.00

Estimated overhead $2,880.00

Particulars Welding Assembly

Fixed manufacturing overhead cost $3,20,000.00 $64,800.00

Machine hours 5,800

Direct labor hours 7,200

Predetermined fixed overhead rate $ 55 9

Variable manufacturing overhead rate $ $2.00 $1.00

9

reducing the overall extra expenses and minimize the level of quality costs. The measures

such as development of new system for streamlining the assembly line, providing technical

support for minimizing the receiving of faulty materials, field testing the fridges on customer

sites and inspecting the fridges on the assembly line. These measures directly allowed Ringo

to minimize the level of quality cost in year 3, as the overall expenses in warranties declined.

Therefore, value-based pricing method would directly allow the organizations to improve

their current pricing conditions and generate higher level of income in the long run.

Question 7:

a) Determining the amount of under applied or over applied manufacturing overhead

for Year 1:

Particulars Welding Assembly

Fixed manufacturing overhead cost $3,00,000.00 $64,800.00

Machine hours 6,000

Direct labor hours 7,200

Predetermined fixed overhead rate $ 50 9

Variable manufacturing overhead rate $ $2.00 $1.00

Predetermined overhead rate $ $52.00 $10.00

Particulars Welding Assembly

Job-262 40 80

Predetermined overhead rate

$ $52.00 $10.00

Estimated overhead $2,880.00

Particulars Welding Assembly

Fixed manufacturing overhead cost $3,20,000.00 $64,800.00

Machine hours 5,800

Direct labor hours 7,200

Predetermined fixed overhead rate $ 55 9

Variable manufacturing overhead rate $ $2.00 $1.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

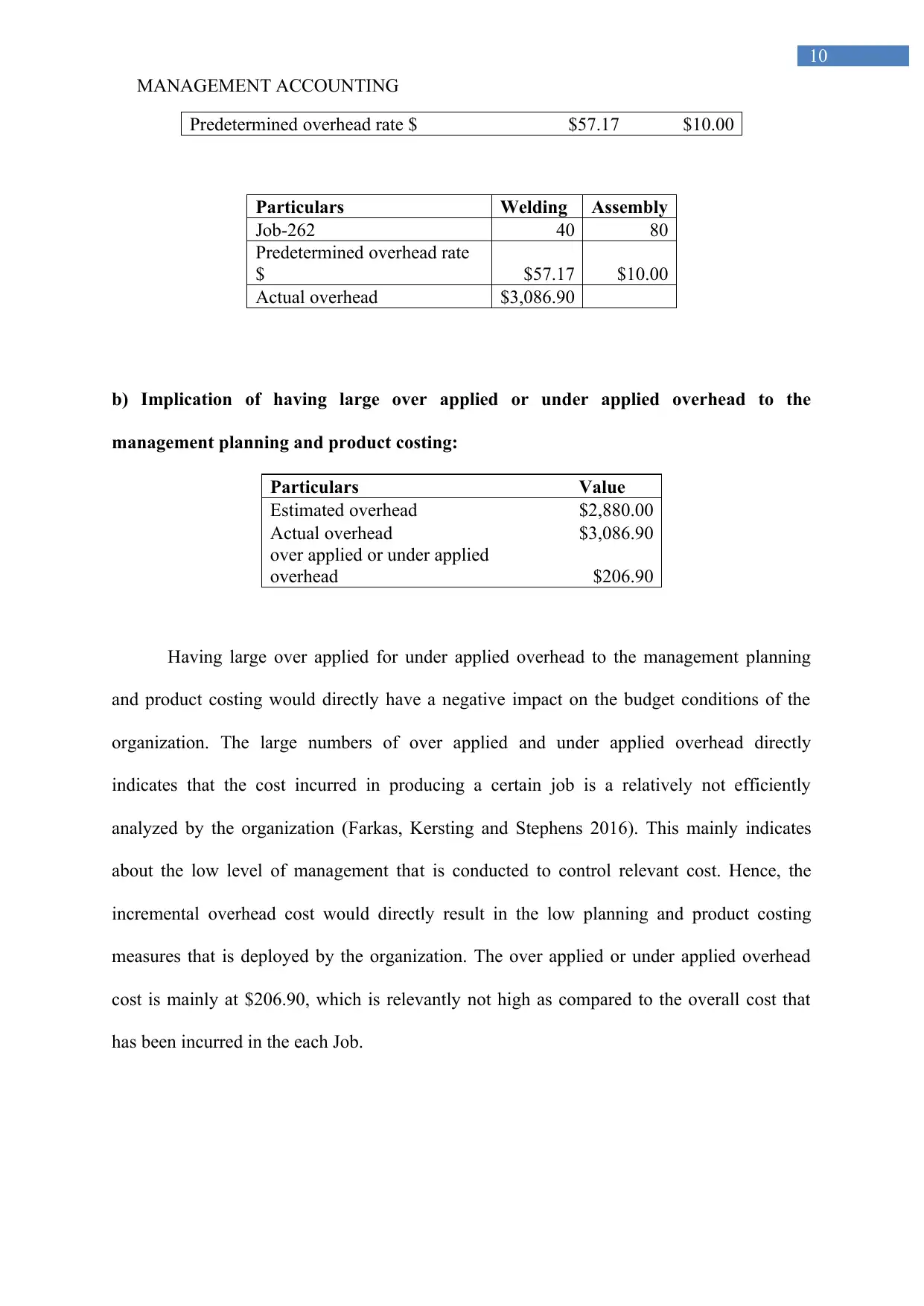

MANAGEMENT ACCOUNTING

10

Predetermined overhead rate $ $57.17 $10.00

Particulars Welding Assembly

Job-262 40 80

Predetermined overhead rate

$ $57.17 $10.00

Actual overhead $3,086.90

b) Implication of having large over applied or under applied overhead to the

management planning and product costing:

Particulars Value

Estimated overhead $2,880.00

Actual overhead $3,086.90

over applied or under applied

overhead $206.90

Having large over applied for under applied overhead to the management planning

and product costing would directly have a negative impact on the budget conditions of the

organization. The large numbers of over applied and under applied overhead directly

indicates that the cost incurred in producing a certain job is a relatively not efficiently

analyzed by the organization (Farkas, Kersting and Stephens 2016). This mainly indicates

about the low level of management that is conducted to control relevant cost. Hence, the

incremental overhead cost would directly result in the low planning and product costing

measures that is deployed by the organization. The over applied or under applied overhead

cost is mainly at $206.90, which is relevantly not high as compared to the overall cost that

has been incurred in the each Job.

10

Predetermined overhead rate $ $57.17 $10.00

Particulars Welding Assembly

Job-262 40 80

Predetermined overhead rate

$ $57.17 $10.00

Actual overhead $3,086.90

b) Implication of having large over applied or under applied overhead to the

management planning and product costing:

Particulars Value

Estimated overhead $2,880.00

Actual overhead $3,086.90

over applied or under applied

overhead $206.90

Having large over applied for under applied overhead to the management planning

and product costing would directly have a negative impact on the budget conditions of the

organization. The large numbers of over applied and under applied overhead directly

indicates that the cost incurred in producing a certain job is a relatively not efficiently

analyzed by the organization (Farkas, Kersting and Stephens 2016). This mainly indicates

about the low level of management that is conducted to control relevant cost. Hence, the

incremental overhead cost would directly result in the low planning and product costing

measures that is deployed by the organization. The over applied or under applied overhead

cost is mainly at $206.90, which is relevantly not high as compared to the overall cost that

has been incurred in the each Job.

MANAGEMENT ACCOUNTING

11

References:

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education, 35, pp.56-

68.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Hbr.org. 2018. When Cost-Plus Pricing Is a Good Idea. [online] Available at:

https://hbr.org/2018/07/when-cost-plus-pricing-is-a-good-idea [Accessed 8 Aug. 2019].

Lachman, V.D., 2014. Ethical issues in the disruptive behaviors of incivility, bullying, and

horizontal/lateral violence. Medsurg Nurs, 23(1), pp.56-60.

Ross, J.E., 2017. Total quality management: Text, cases, and readings. Routledge.

11

References:

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education, 35, pp.56-

68.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Hbr.org. 2018. When Cost-Plus Pricing Is a Good Idea. [online] Available at:

https://hbr.org/2018/07/when-cost-plus-pricing-is-a-good-idea [Accessed 8 Aug. 2019].

Lachman, V.D., 2014. Ethical issues in the disruptive behaviors of incivility, bullying, and

horizontal/lateral violence. Medsurg Nurs, 23(1), pp.56-60.

Ross, J.E., 2017. Total quality management: Text, cases, and readings. Routledge.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.