Management Accounting: XLG Case Study on Variance Analysis and Risks

VerifiedAdded on 2023/01/09

|12

|3232

|27

Homework Assignment

AI Summary

This management accounting assignment delves into variance analysis, utilizing a case study of XLG, a cleaning-products manufacturer. Part A of the assignment focuses on calculating sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance based on the provided data. It also includes a critical analysis of the merits and demerits of using variances to determine managerial performance. Part B evaluates the risks associated with importing a patent product (fama Q) and assesses the impact of these risks on XLG during the lockdown, considering increased sales prices and demand for chemicals X and Y. The assignment explores the implications of different import strategies, including the potential for increased costs and the importance of timely fulfillment of customer demand. The analysis highlights the importance of considering both quantitative and qualitative factors in management accounting decisions.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(i) Sales price variance and sales volume contribution variance:................................................3

(ii). Material price planning variance and material price operational variance:..........................4

(iii). Critical and effective analysis of all the merits and demerits linked with variances use in

determining managers performance:...........................................................................................5

PART B...........................................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(i) Sales price variance and sales volume contribution variance:................................................3

(ii). Material price planning variance and material price operational variance:..........................4

(iii). Critical and effective analysis of all the merits and demerits linked with variances use in

determining managers performance:...........................................................................................5

PART B...........................................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

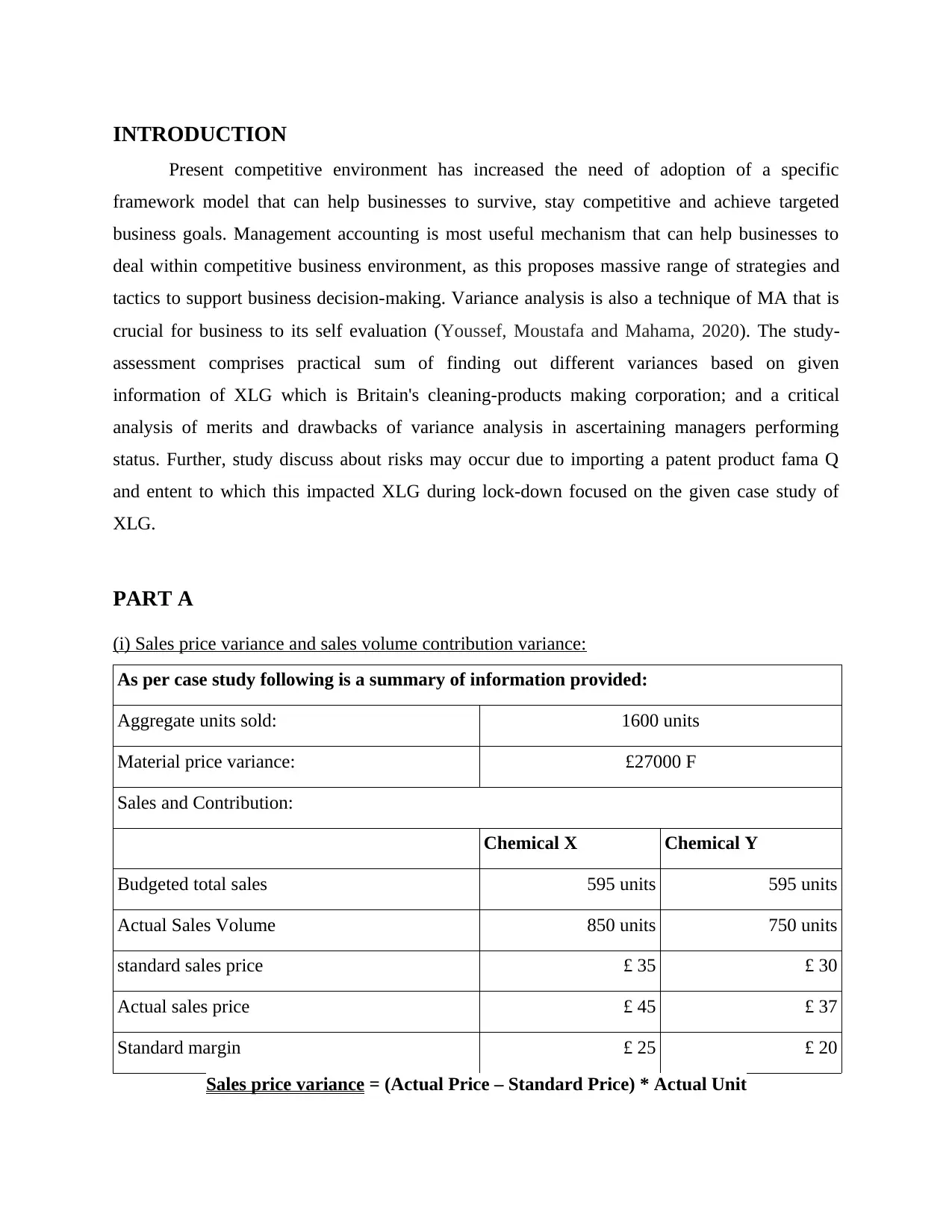

INTRODUCTION

Present competitive environment has increased the need of adoption of a specific

framework model that can help businesses to survive, stay competitive and achieve targeted

business goals. Management accounting is most useful mechanism that can help businesses to

deal within competitive business environment, as this proposes massive range of strategies and

tactics to support business decision-making. Variance analysis is also a technique of MA that is

crucial for business to its self evaluation (Youssef, Moustafa and Mahama, 2020). The study-

assessment comprises practical sum of finding out different variances based on given

information of XLG which is Britain's cleaning-products making corporation; and a critical

analysis of merits and drawbacks of variance analysis in ascertaining managers performing

status. Further, study discuss about risks may occur due to importing a patent product fama Q

and entent to which this impacted XLG during lock-down focused on the given case study of

XLG.

PART A

(i) Sales price variance and sales volume contribution variance:

As per case study following is a summary of information provided:

Aggregate units sold: 1600 units

Material price variance: £27000 F

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance = (Actual Price – Standard Price) * Actual Unit

Present competitive environment has increased the need of adoption of a specific

framework model that can help businesses to survive, stay competitive and achieve targeted

business goals. Management accounting is most useful mechanism that can help businesses to

deal within competitive business environment, as this proposes massive range of strategies and

tactics to support business decision-making. Variance analysis is also a technique of MA that is

crucial for business to its self evaluation (Youssef, Moustafa and Mahama, 2020). The study-

assessment comprises practical sum of finding out different variances based on given

information of XLG which is Britain's cleaning-products making corporation; and a critical

analysis of merits and drawbacks of variance analysis in ascertaining managers performing

status. Further, study discuss about risks may occur due to importing a patent product fama Q

and entent to which this impacted XLG during lock-down focused on the given case study of

XLG.

PART A

(i) Sales price variance and sales volume contribution variance:

As per case study following is a summary of information provided:

Aggregate units sold: 1600 units

Material price variance: £27000 F

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance = (Actual Price – Standard Price) * Actual Unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

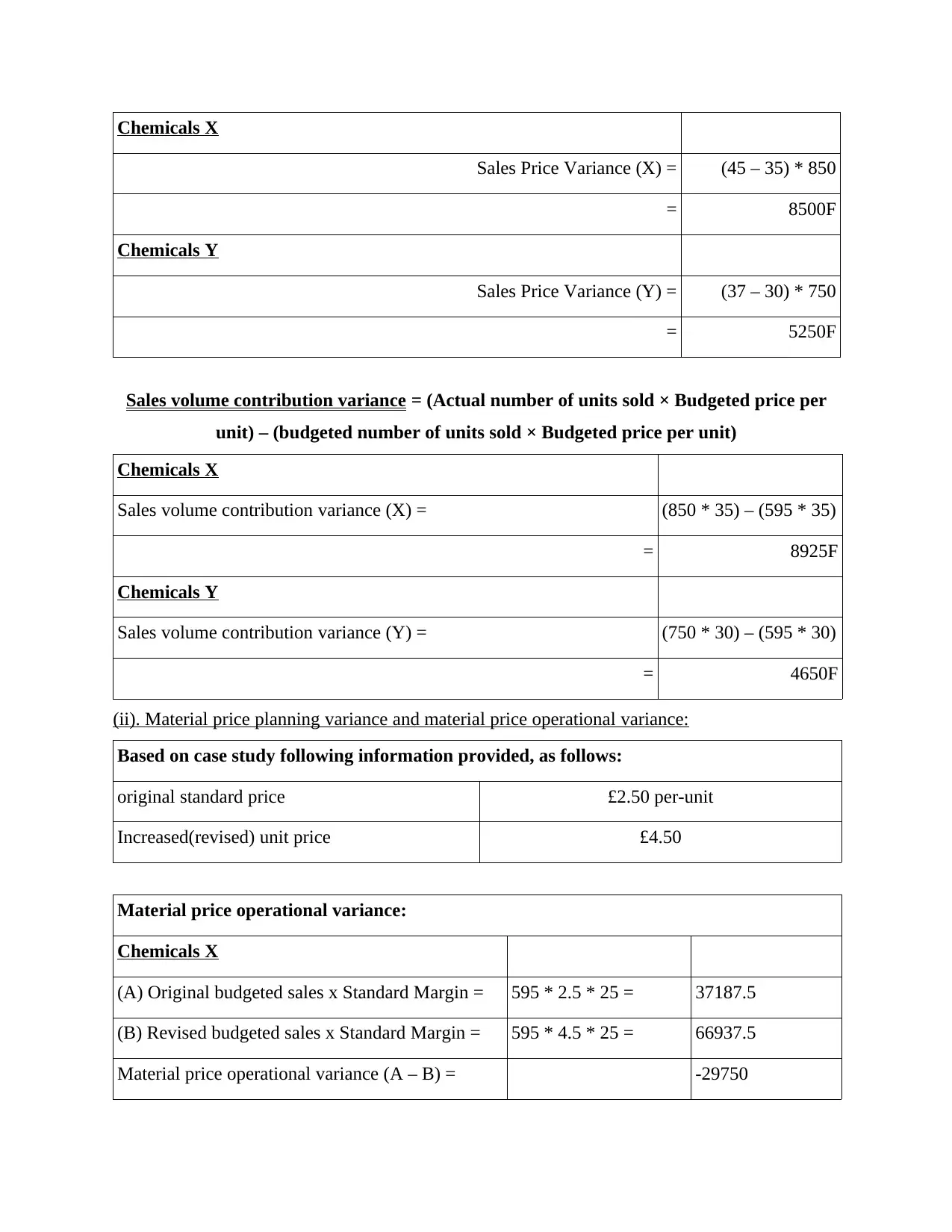

Chemicals X

Sales Price Variance (X) = (45 – 35) * 850

= 8500F

Chemicals Y

Sales Price Variance (Y) = (37 – 30) * 750

= 5250F

Sales volume contribution variance = (Actual number of units sold × Budgeted price per

unit) – (budgeted number of units sold × Budgeted price per unit)

Chemicals X

Sales volume contribution variance (X) = (850 * 35) – (595 * 35)

= 8925F

Chemicals Y

Sales volume contribution variance (Y) = (750 * 30) – (595 * 30)

= 4650F

(ii). Material price planning variance and material price operational variance:

Based on case study following information provided, as follows:

original standard price £2.50 per-unit

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 = 37187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 = 66937.5

Material price operational variance (A – B) = -29750

Sales Price Variance (X) = (45 – 35) * 850

= 8500F

Chemicals Y

Sales Price Variance (Y) = (37 – 30) * 750

= 5250F

Sales volume contribution variance = (Actual number of units sold × Budgeted price per

unit) – (budgeted number of units sold × Budgeted price per unit)

Chemicals X

Sales volume contribution variance (X) = (850 * 35) – (595 * 35)

= 8925F

Chemicals Y

Sales volume contribution variance (Y) = (750 * 30) – (595 * 30)

= 4650F

(ii). Material price planning variance and material price operational variance:

Based on case study following information provided, as follows:

original standard price £2.50 per-unit

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 = 37187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 = 66937.5

Material price operational variance (A – B) = -29750

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

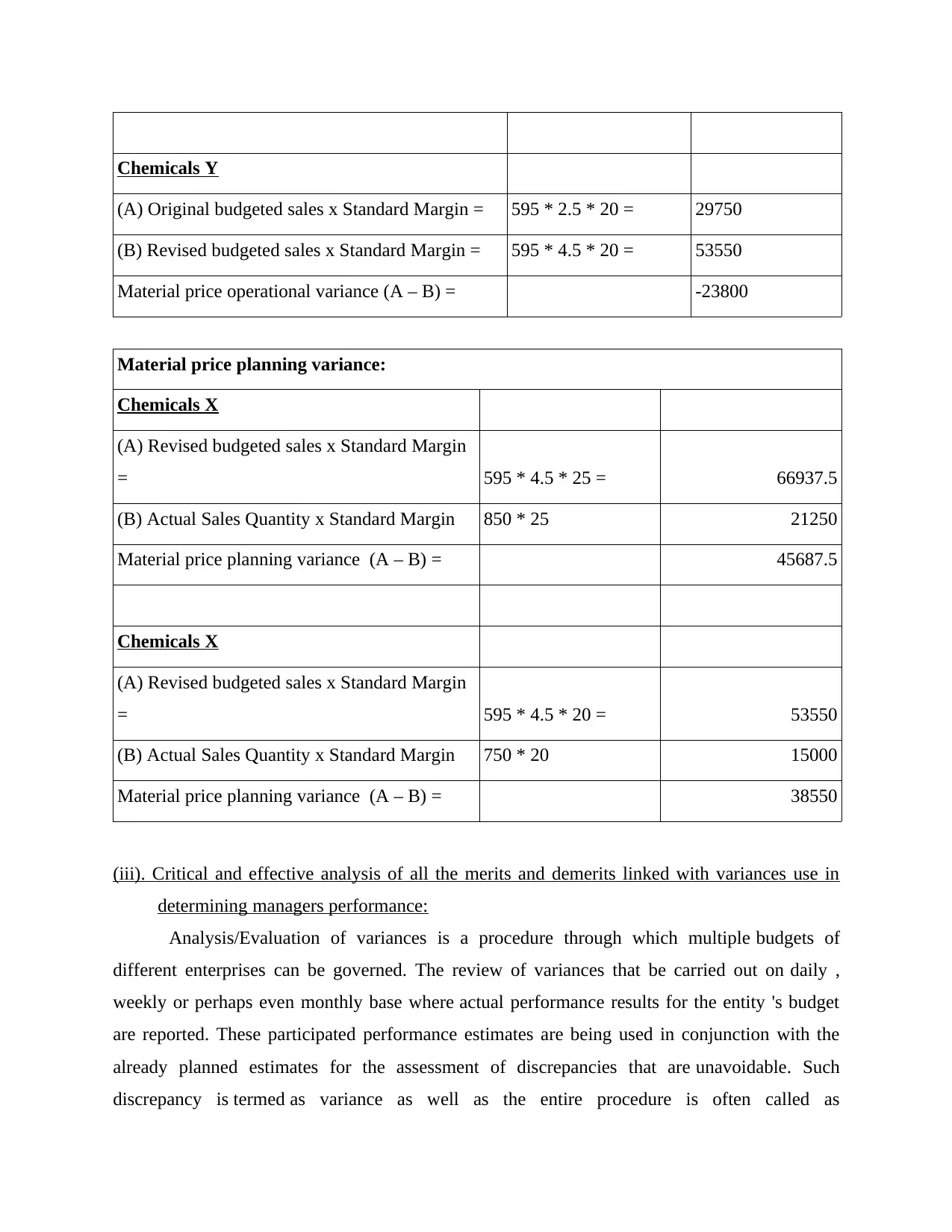

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 = 29750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 = 53550

Material price operational variance (A – B) = -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 25 = 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price planning variance (A – B) = 45687.5

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 20 = 53550

(B) Actual Sales Quantity x Standard Margin 750 * 20 15000

Material price planning variance (A – B) = 38550

(iii). Critical and effective analysis of all the merits and demerits linked with variances use in

determining managers performance:

Analysis/Evaluation of variances is a procedure through which multiple budgets of

different enterprises can be governed. The review of variances that be carried out on daily ,

weekly or perhaps even monthly base where actual performance results for the entity 's budget

are reported. These participated performance estimates are being used in conjunction with the

already planned estimates for the assessment of discrepancies that are unavoidable. Such

discrepancy is termed as variance as well as the entire procedure is often called as

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 = 29750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 = 53550

Material price operational variance (A – B) = -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 25 = 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price planning variance (A – B) = 45687.5

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 20 = 53550

(B) Actual Sales Quantity x Standard Margin 750 * 20 15000

Material price planning variance (A – B) = 38550

(iii). Critical and effective analysis of all the merits and demerits linked with variances use in

determining managers performance:

Analysis/Evaluation of variances is a procedure through which multiple budgets of

different enterprises can be governed. The review of variances that be carried out on daily ,

weekly or perhaps even monthly base where actual performance results for the entity 's budget

are reported. These participated performance estimates are being used in conjunction with the

already planned estimates for the assessment of discrepancies that are unavoidable. Such

discrepancy is termed as variance as well as the entire procedure is often called as

variances analysis (variance Equal to standard budget-actual budget). In a case that sum

budgeted exceeded the actual sum, the difference found is positive, meaning that amount spent

was lower than budgeted amount (Fleischman and McLean, 2020). An Unfavourable variations

arise whenever actual output sum exceeds the budgeted sum. This should be remembered that

different budgets are developed for primary purpose that they provide a benchmark by

which performance of every company is assessed. at other hand , review of variances determines

the efficiency of the business organization in relation to budgets. There are several variables that

the management team should acknowledge when conducting variance analysis. There's several

situations wherein variances exist and each situation needs to be handled uniquely in attempt to

prevent errors. Planning variance analyses and the process of reviewing results are very critical

activities for the company. Variance analysis assists a good deal in decision-making process

in enterprise. This analysis allows management to formulate various operating strategies in order

to enhance efficiency and also to delegate specific activities to various employees (Frick, Birt

and Waters, 2020). This analysis is also important as it allows management to determine the

reasons of variances and therefore to undertake effective corrective steps to cope with variations.

The decisions made by management after reviewing variance reports can include the following.

Cost variances provide hints to a probable issue and can trigger it. Analysis of variance can be

used for timely detection as well as prevention. Management can find manner to determine if

such variances are actually due to circumstance or to real problem which requires to be

addressed. Favourable variance is defined as predicted cost is greater than actual cost or expected

revenue is less than actual revenue. If estimated cost outweighs the estimated benefits, that's an

unacceptable variance. The choice to examine is taken by balancing the anticipated benefits

with anticipated costs (Asuquo, 2020). Managers are directly concerned with variance results as

an adverse variance in specific area like material , labour etc. indicates that manager who handle

such area is not performing as per the expectation or he is not capable to handle such specific

area's operations. Here in this regard following are certain key merits and demerits of variance

analysis in relation to assessing managers' performance, as follows:

Merits:

The causes for total variances could be conveniently identified for taking corrective

action. The subsection of the evaluation of variances reveals the key relationship that

budgeted exceeded the actual sum, the difference found is positive, meaning that amount spent

was lower than budgeted amount (Fleischman and McLean, 2020). An Unfavourable variations

arise whenever actual output sum exceeds the budgeted sum. This should be remembered that

different budgets are developed for primary purpose that they provide a benchmark by

which performance of every company is assessed. at other hand , review of variances determines

the efficiency of the business organization in relation to budgets. There are several variables that

the management team should acknowledge when conducting variance analysis. There's several

situations wherein variances exist and each situation needs to be handled uniquely in attempt to

prevent errors. Planning variance analyses and the process of reviewing results are very critical

activities for the company. Variance analysis assists a good deal in decision-making process

in enterprise. This analysis allows management to formulate various operating strategies in order

to enhance efficiency and also to delegate specific activities to various employees (Frick, Birt

and Waters, 2020). This analysis is also important as it allows management to determine the

reasons of variances and therefore to undertake effective corrective steps to cope with variations.

The decisions made by management after reviewing variance reports can include the following.

Cost variances provide hints to a probable issue and can trigger it. Analysis of variance can be

used for timely detection as well as prevention. Management can find manner to determine if

such variances are actually due to circumstance or to real problem which requires to be

addressed. Favourable variance is defined as predicted cost is greater than actual cost or expected

revenue is less than actual revenue. If estimated cost outweighs the estimated benefits, that's an

unacceptable variance. The choice to examine is taken by balancing the anticipated benefits

with anticipated costs (Asuquo, 2020). Managers are directly concerned with variance results as

an adverse variance in specific area like material , labour etc. indicates that manager who handle

such area is not performing as per the expectation or he is not capable to handle such specific

area's operations. Here in this regard following are certain key merits and demerits of variance

analysis in relation to assessing managers' performance, as follows:

Merits:

The causes for total variances could be conveniently identified for taking corrective

action. The subsection of the evaluation of variances reveals the key relationship that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prevails between the multiple variations. It is very useful to decide the obligation of the

person or unit separately towards each identified variance.

It points out or underlines all ineffective performance as well as the level of

ineffectiveness thus also employed for cost controlling purposes. Upper management

may, by exception, adopt the principles of management and only undesirable variances

are reported to top mangers (Sohl, Vroom and Fitza, 2020).

Often variances may be categorized as controllable or uncontrollable variations.

Controllable variations are put into account in this scenario for further review. The

preparation of profits should be carried out efficiently by top management. The outcomes

of the management action could be a decrease in costs. It induces cost-consciousness

in minds of every staff within a business organisation.

Effective analysis of all the variance allow managers to efficient allocation of all the

business resources and thereby increase overall productivity of business. Further

managers can also assess the over or any under utilisation of different resources.

Variance analysis also form a base for preparation of annual financial budget as this

present actual efficiency and operational level of organisation by showing variance in

performance.

Further this allow managing personnel to focus on weak areas of business organisation

and also act as alarming framework by exhibiting variances in particular areas which

ultimately supports decision-making within entity (Chang, van Witteloostuijn and Eden,

2020).

Demerits:

Accounting personnel compile all variances at month end before presenting the reports to

the managers. In fast-paced environment, managers require input much quicker than once

in a month, therefore tends to dependent on other measures or indicator markers which

are obtained on-site (particularly in production area).

Some of the factors for variances generally not appear in accounting reports, and

accounting personnel will dig through details like inventory costs, labour, and payroll

data to identify the sources of the issues. additional analysis is only cost-effective if

managers can systematically fix issues on the basis of such information.

person or unit separately towards each identified variance.

It points out or underlines all ineffective performance as well as the level of

ineffectiveness thus also employed for cost controlling purposes. Upper management

may, by exception, adopt the principles of management and only undesirable variances

are reported to top mangers (Sohl, Vroom and Fitza, 2020).

Often variances may be categorized as controllable or uncontrollable variations.

Controllable variations are put into account in this scenario for further review. The

preparation of profits should be carried out efficiently by top management. The outcomes

of the management action could be a decrease in costs. It induces cost-consciousness

in minds of every staff within a business organisation.

Effective analysis of all the variance allow managers to efficient allocation of all the

business resources and thereby increase overall productivity of business. Further

managers can also assess the over or any under utilisation of different resources.

Variance analysis also form a base for preparation of annual financial budget as this

present actual efficiency and operational level of organisation by showing variance in

performance.

Further this allow managing personnel to focus on weak areas of business organisation

and also act as alarming framework by exhibiting variances in particular areas which

ultimately supports decision-making within entity (Chang, van Witteloostuijn and Eden,

2020).

Demerits:

Accounting personnel compile all variances at month end before presenting the reports to

the managers. In fast-paced environment, managers require input much quicker than once

in a month, therefore tends to dependent on other measures or indicator markers which

are obtained on-site (particularly in production area).

Some of the factors for variances generally not appear in accounting reports, and

accounting personnel will dig through details like inventory costs, labour, and payroll

data to identify the sources of the issues. additional analysis is only cost-effective if

managers can systematically fix issues on the basis of such information.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The analysing variance is necessary in comparison of actual findings with arbitrary

standards which may have been extracted from political agreements. Consequentially, the

eventual variance could not provide any effective information (Wen and Siqin, 2020).

Variance analysis can promote short-termism owing to its inherent orientation towards

shorter-term, quantitative targets and outcomes. Negative views of the

corporation's variance analysis method that also promote other suboptimal actions among

personnel, like attempts to implement budgeting slacks.

Accountability is a central feature of variance analysis. Variations may occur for a range

of reasons varying from unrealistic objectives/targets (e.g. failure to consider the

anticipated rise in wages rates) to operational factors ( e.g. change in the direct-material

usage attributable to the hiring of less skilled labour). Planning shortfalls that might have

generated significant variances owing to setting of incorrect standards/budgets could be

resolved retrospectively through measuring planning and operating variations. However,

this may be more complicated to determine the precise reasons and delegate the duties

of organizational variances to a particular individual, division or task within an entity

(Lanzolla and Markides, 2019).

PART B

Evaluation of risks before making a major decisions is crucial for business as this allow

to recognise any potential risks and their effects on business associated with such decision

(Salles, Rocha and Gonçalves, 2020). As presented in XLG's particular scenario, because of the

lock-down, there's a substantial rise in sales prices because as standard sale price every

single unit of the chemical X is being enhanced from £ 35 to £45, as well as in that case chemical

Y's the sale price has also been enhanced from £ 30 to £37. The main consequence of such a rise

in the sales prices is the significant rise in the price of the fama-Q, the superior effective cleaning

item of the corporation that is combined in company's products. Consequence of the lock-down,

and also the restraints and limitations on overseas travels, it is essential for the corporation to

import the fama-Q from the air transit system. It has considerably enhanced the costs of imports,

as air transit is too costly especially in comparison to sea transit. As a consequence of one such

rise in transportation costs, the sales prices of chemicals X and Y have been risen. Fama Q's

standard rate is £2.50 each unit, which was raised to £4.50 but £3.70 is actually charged by XLG.

Here, the significant effect is that the total profitability of the corporation would be influenced.

standards which may have been extracted from political agreements. Consequentially, the

eventual variance could not provide any effective information (Wen and Siqin, 2020).

Variance analysis can promote short-termism owing to its inherent orientation towards

shorter-term, quantitative targets and outcomes. Negative views of the

corporation's variance analysis method that also promote other suboptimal actions among

personnel, like attempts to implement budgeting slacks.

Accountability is a central feature of variance analysis. Variations may occur for a range

of reasons varying from unrealistic objectives/targets (e.g. failure to consider the

anticipated rise in wages rates) to operational factors ( e.g. change in the direct-material

usage attributable to the hiring of less skilled labour). Planning shortfalls that might have

generated significant variances owing to setting of incorrect standards/budgets could be

resolved retrospectively through measuring planning and operating variations. However,

this may be more complicated to determine the precise reasons and delegate the duties

of organizational variances to a particular individual, division or task within an entity

(Lanzolla and Markides, 2019).

PART B

Evaluation of risks before making a major decisions is crucial for business as this allow

to recognise any potential risks and their effects on business associated with such decision

(Salles, Rocha and Gonçalves, 2020). As presented in XLG's particular scenario, because of the

lock-down, there's a substantial rise in sales prices because as standard sale price every

single unit of the chemical X is being enhanced from £ 35 to £45, as well as in that case chemical

Y's the sale price has also been enhanced from £ 30 to £37. The main consequence of such a rise

in the sales prices is the significant rise in the price of the fama-Q, the superior effective cleaning

item of the corporation that is combined in company's products. Consequence of the lock-down,

and also the restraints and limitations on overseas travels, it is essential for the corporation to

import the fama-Q from the air transit system. It has considerably enhanced the costs of imports,

as air transit is too costly especially in comparison to sea transit. As a consequence of one such

rise in transportation costs, the sales prices of chemicals X and Y have been risen. Fama Q's

standard rate is £2.50 each unit, which was raised to £4.50 but £3.70 is actually charged by XLG.

Here, the significant effect is that the total profitability of the corporation would be influenced.

In addition to sales rates, a drastic rise in demands and use of chemicals X and Y has also been

recorded. The rise is beneficial for the organization because this boost in the net revenue of its

main products. That's one major impacts of lock-down. The reason for this large rise in demand

for household cleaners is that people are now becoming more conscientious of sanitation and

hygiene. Therefore here major risk for company is to drop down in sales due to non fulfilment of

customer's demand on time.

Further, additional information given in the scenario that if the corporation tends to

make single unit of a fama-Q, this will cost the organization £ 3 for every unit, including a

decrease in shipping period of 15 days. This is also given that the demand for chemicals X and Y

expanded about 45 % and is projected to continue. Therefore, focused on additional details and

case scenario, there are major two options available to the XLG, as set out below:

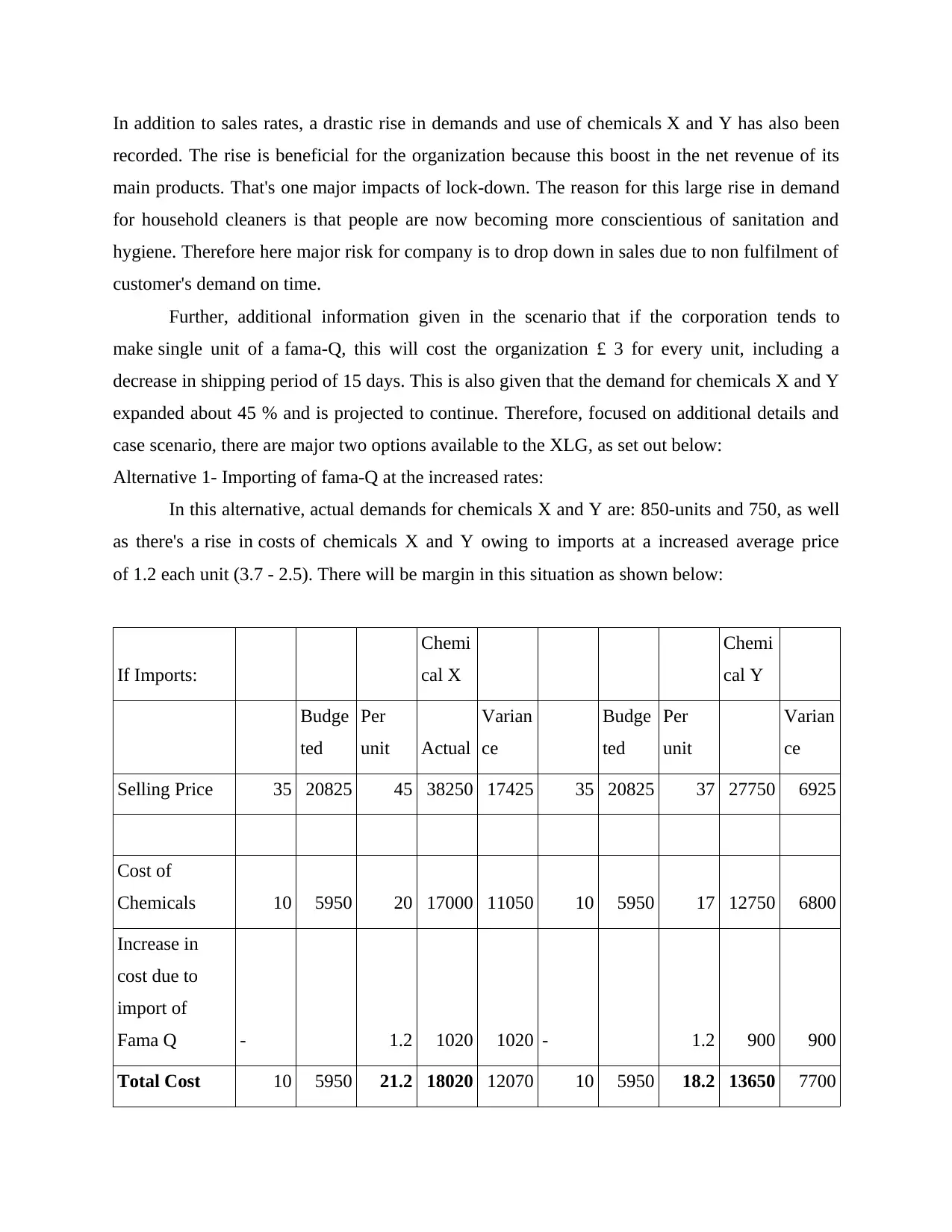

Alternative 1- Importing of fama-Q at the increased rates:

In this alternative, actual demands for chemicals X and Y are: 850-units and 750, as well

as there's a rise in costs of chemicals X and Y owing to imports at a increased average price

of 1.2 each unit (3.7 - 2.5). There will be margin in this situation as shown below:

If Imports:

Chemi

cal X

Chemi

cal Y

Budge

ted

Per

unit Actual

Varian

ce

Budge

ted

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in

cost due to

import of

Fama Q - 1.2 1020 1020 - 1.2 900 900

Total Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

recorded. The rise is beneficial for the organization because this boost in the net revenue of its

main products. That's one major impacts of lock-down. The reason for this large rise in demand

for household cleaners is that people are now becoming more conscientious of sanitation and

hygiene. Therefore here major risk for company is to drop down in sales due to non fulfilment of

customer's demand on time.

Further, additional information given in the scenario that if the corporation tends to

make single unit of a fama-Q, this will cost the organization £ 3 for every unit, including a

decrease in shipping period of 15 days. This is also given that the demand for chemicals X and Y

expanded about 45 % and is projected to continue. Therefore, focused on additional details and

case scenario, there are major two options available to the XLG, as set out below:

Alternative 1- Importing of fama-Q at the increased rates:

In this alternative, actual demands for chemicals X and Y are: 850-units and 750, as well

as there's a rise in costs of chemicals X and Y owing to imports at a increased average price

of 1.2 each unit (3.7 - 2.5). There will be margin in this situation as shown below:

If Imports:

Chemi

cal X

Chemi

cal Y

Budge

ted

Per

unit Actual

Varian

ce

Budge

ted

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in

cost due to

import of

Fama Q - 1.2 1020 1020 - 1.2 900 900

Total Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Alternative 2- Making fama-Q in house:

In this alternative, demands has risen by 45 per cent and delivery/shipment time has

decreased by 15 days, whereas the cost of developing fama-Q is £3. Premised on this

information, following is evaluation of the product margin, as stated below:

If making

fama Q

Chemi

cal X

Chemi

cal Y

Per

unit

Budge

ted

Per

unit

Varian

ce

Budge

ted

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in

cost due to

import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Alternative 2- Making fama-Q in house:

In this alternative, demands has risen by 45 per cent and delivery/shipment time has

decreased by 15 days, whereas the cost of developing fama-Q is £3. Premised on this

information, following is evaluation of the product margin, as stated below:

If making

fama Q

Chemi

cal X

Chemi

cal Y

Per

unit

Budge

ted

Per

unit

Varian

ce

Budge

ted

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in

cost due to

import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

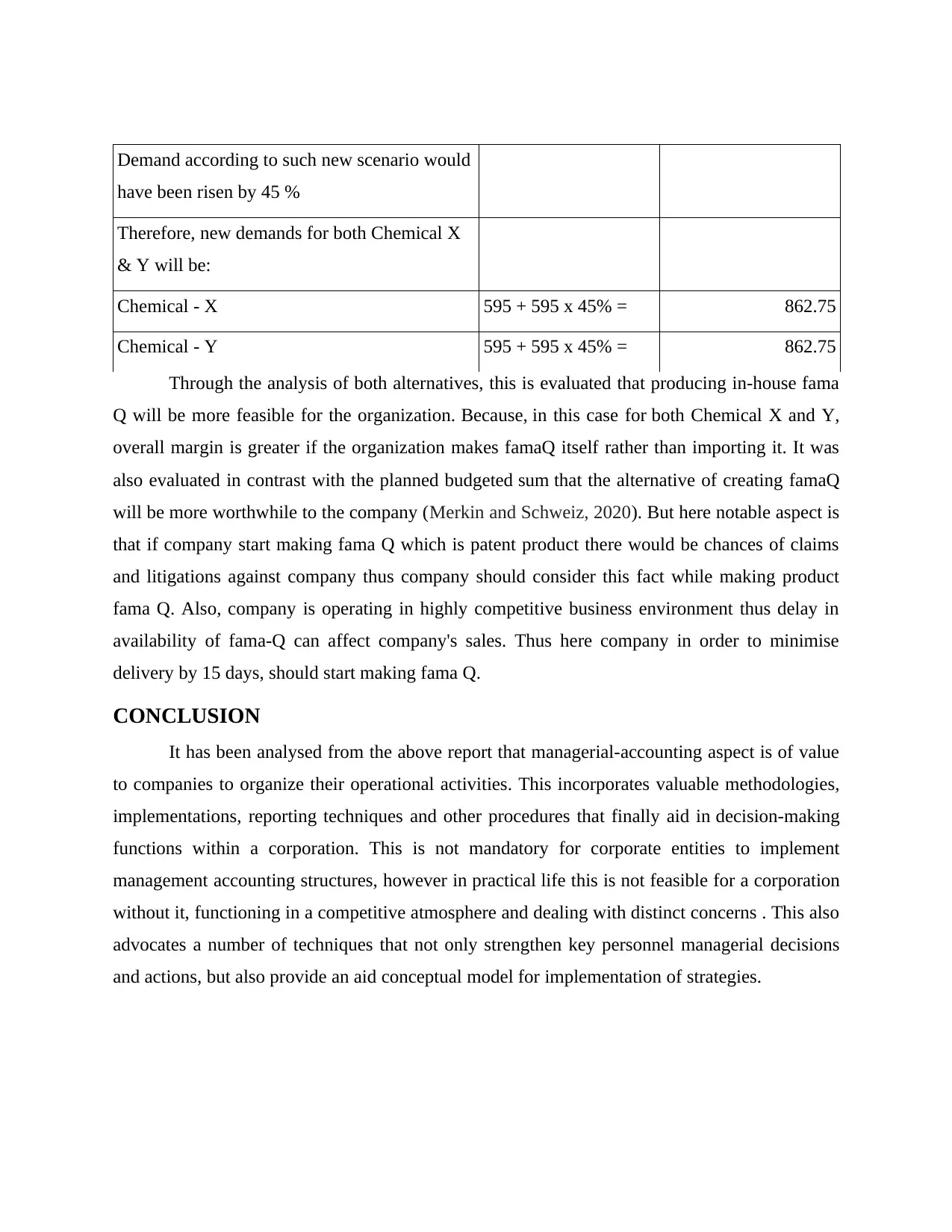

Demand according to such new scenario would

have been risen by 45 %

Therefore, new demands for both Chemical X

& Y will be:

Chemical - X 595 + 595 x 45% = 862.75

Chemical - Y 595 + 595 x 45% = 862.75

Through the analysis of both alternatives, this is evaluated that producing in-house fama

Q will be more feasible for the organization. Because, in this case for both Chemical X and Y,

overall margin is greater if the organization makes famaQ itself rather than importing it. It was

also evaluated in contrast with the planned budgeted sum that the alternative of creating famaQ

will be more worthwhile to the company (Merkin and Schweiz, 2020). But here notable aspect is

that if company start making fama Q which is patent product there would be chances of claims

and litigations against company thus company should consider this fact while making product

fama Q. Also, company is operating in highly competitive business environment thus delay in

availability of fama-Q can affect company's sales. Thus here company in order to minimise

delivery by 15 days, should start making fama Q.

CONCLUSION

It has been analysed from the above report that managerial-accounting aspect is of value

to companies to organize their operational activities. This incorporates valuable methodologies,

implementations, reporting techniques and other procedures that finally aid in decision-making

functions within a corporation. This is not mandatory for corporate entities to implement

management accounting structures, however in practical life this is not feasible for a corporation

without it, functioning in a competitive atmosphere and dealing with distinct concerns . This also

advocates a number of techniques that not only strengthen key personnel managerial decisions

and actions, but also provide an aid conceptual model for implementation of strategies.

have been risen by 45 %

Therefore, new demands for both Chemical X

& Y will be:

Chemical - X 595 + 595 x 45% = 862.75

Chemical - Y 595 + 595 x 45% = 862.75

Through the analysis of both alternatives, this is evaluated that producing in-house fama

Q will be more feasible for the organization. Because, in this case for both Chemical X and Y,

overall margin is greater if the organization makes famaQ itself rather than importing it. It was

also evaluated in contrast with the planned budgeted sum that the alternative of creating famaQ

will be more worthwhile to the company (Merkin and Schweiz, 2020). But here notable aspect is

that if company start making fama Q which is patent product there would be chances of claims

and litigations against company thus company should consider this fact while making product

fama Q. Also, company is operating in highly competitive business environment thus delay in

availability of fama-Q can affect company's sales. Thus here company in order to minimise

delivery by 15 days, should start making fama Q.

CONCLUSION

It has been analysed from the above report that managerial-accounting aspect is of value

to companies to organize their operational activities. This incorporates valuable methodologies,

implementations, reporting techniques and other procedures that finally aid in decision-making

functions within a corporation. This is not mandatory for corporate entities to implement

management accounting structures, however in practical life this is not feasible for a corporation

without it, functioning in a competitive atmosphere and dealing with distinct concerns . This also

advocates a number of techniques that not only strengthen key personnel managerial decisions

and actions, but also provide an aid conceptual model for implementation of strategies.

REFERENCES

Books and Journals:

Youssef, M.A.E.A., Moustafa, E.E. and Mahama, H., 2020. The mediating role of management

control system characteristics in the adoption of management accounting

techniques. Pacific Accounting Review.

Fleischman, R. and McLean, T., 2020. Management accounting: theory and practice. Routledge.

Frick, H., Birt, J. and Waters, J., 2020. Enhancing student engagement in large management

accounting lectures. Accounting & Finance, 60(1), pp.271-298.

Asuquo, A.I., 2020. Applicability of Standard Magnitude variance in the determination financial

progress of business organizations. International Journal of Scientific and technology

research, 9(3), pp.6351-6358.

Sohl, T., Vroom, G. and Fitza, M.A., 2020. How much does business model matter for firm

performance? A variance decomposition analysis. Academy of Management

Discoveries, 6(1), pp.61-80.

Chang, S.J., van Witteloostuijn, A. and Eden, L., 2020. Common method variance in

international business research. In Research Methods in International Business (pp.

385-398). Palgrave Macmillan, Cham.

Wen, X. and Siqin, T., 2020. How do product quality uncertainties affect the sharing economy

platforms with risk considerations? A mean-variance analysis. International Journal of

Production Economics, 224, p.107544.

Lanzolla, G. and Markides, C., 2019. A business model view of strategy. Journal of

Management Studies.

Salles, T., Rocha, L. and Gonçalves, M., 2020. A bias-variance analysis of state-of-the-art

random forest text classifiers. Advances in Data Analysis and Classification, pp.1-27.

Merkin, A., ABB Schweiz AG, 2020. System and method for self-optimizing a user interface to

support the execution of a business process. U.S. Patent 10,540,072.

Books and Journals:

Youssef, M.A.E.A., Moustafa, E.E. and Mahama, H., 2020. The mediating role of management

control system characteristics in the adoption of management accounting

techniques. Pacific Accounting Review.

Fleischman, R. and McLean, T., 2020. Management accounting: theory and practice. Routledge.

Frick, H., Birt, J. and Waters, J., 2020. Enhancing student engagement in large management

accounting lectures. Accounting & Finance, 60(1), pp.271-298.

Asuquo, A.I., 2020. Applicability of Standard Magnitude variance in the determination financial

progress of business organizations. International Journal of Scientific and technology

research, 9(3), pp.6351-6358.

Sohl, T., Vroom, G. and Fitza, M.A., 2020. How much does business model matter for firm

performance? A variance decomposition analysis. Academy of Management

Discoveries, 6(1), pp.61-80.

Chang, S.J., van Witteloostuijn, A. and Eden, L., 2020. Common method variance in

international business research. In Research Methods in International Business (pp.

385-398). Palgrave Macmillan, Cham.

Wen, X. and Siqin, T., 2020. How do product quality uncertainties affect the sharing economy

platforms with risk considerations? A mean-variance analysis. International Journal of

Production Economics, 224, p.107544.

Lanzolla, G. and Markides, C., 2019. A business model view of strategy. Journal of

Management Studies.

Salles, T., Rocha, L. and Gonçalves, M., 2020. A bias-variance analysis of state-of-the-art

random forest text classifiers. Advances in Data Analysis and Classification, pp.1-27.

Merkin, A., ABB Schweiz AG, 2020. System and method for self-optimizing a user interface to

support the execution of a business process. U.S. Patent 10,540,072.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12