Evaluating Costing Systems for Manufacturing Efficiency

VerifiedAdded on 2020/05/08

|11

|1909

|30

AI Summary

The assignment discusses the need for an appropriate costing system to allocate manufacturing overheads effectively among products. Activity-Based Costing (ABC) is highlighted as beneficial in identifying activities directly related to organizational performance, thereby enhancing cost data reliability. The analysis reveals that while ABC improves indirect cost allocation accuracy, it may not be worthwhile if costs are generalized across activities. Furthermore, departmental based overhead rates offer a refined approach for organizations like PW, which manufactures car parts. This system allocates variable manufacturing overheads among departments and products accurately, aiding in better product pricing strategies. The assignment also suggests productivity enhancements in the engineering department by reducing idle hours and ensuring proper machine maintenance. Ultimately, adopting suitable costing systems is crucial for precise expenditure allocation and competitive product pricing.

Running Head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Authors Note:

Management Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Executive summary:

Costing system is a method used by a manufacturing organization to record its costs and

expenditures to allocate these properly to the manufacturing products. In this document, a detail

discussion shall be made with a practical solution to see the importance of using a proper costing

system for appropriate allocation of overheads and other expenditures associated with process of

manufacturing and production of different goods.

Executive summary:

Costing system is a method used by a manufacturing organization to record its costs and

expenditures to allocate these properly to the manufacturing products. In this document, a detail

discussion shall be made with a practical solution to see the importance of using a proper costing

system for appropriate allocation of overheads and other expenditures associated with process of

manufacturing and production of different goods.

2MANAGEMENT ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

Answer to part (1):...........................................................................................................................3

Answer to part (2):...........................................................................................................................4

Answer to part (3):...........................................................................................................................5

Answer to part (4):...........................................................................................................................7

Answer to part (5):...........................................................................................................................8

Answer to part (6):...........................................................................................................................8

Conclusion:......................................................................................................................................9

References:....................................................................................................................................10

Table of Contents

Introduction:....................................................................................................................................3

Answer to part (1):...........................................................................................................................3

Answer to part (2):...........................................................................................................................4

Answer to part (3):...........................................................................................................................5

Answer to part (4):...........................................................................................................................7

Answer to part (5):...........................................................................................................................8

Answer to part (6):...........................................................................................................................8

Conclusion:......................................................................................................................................9

References:....................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

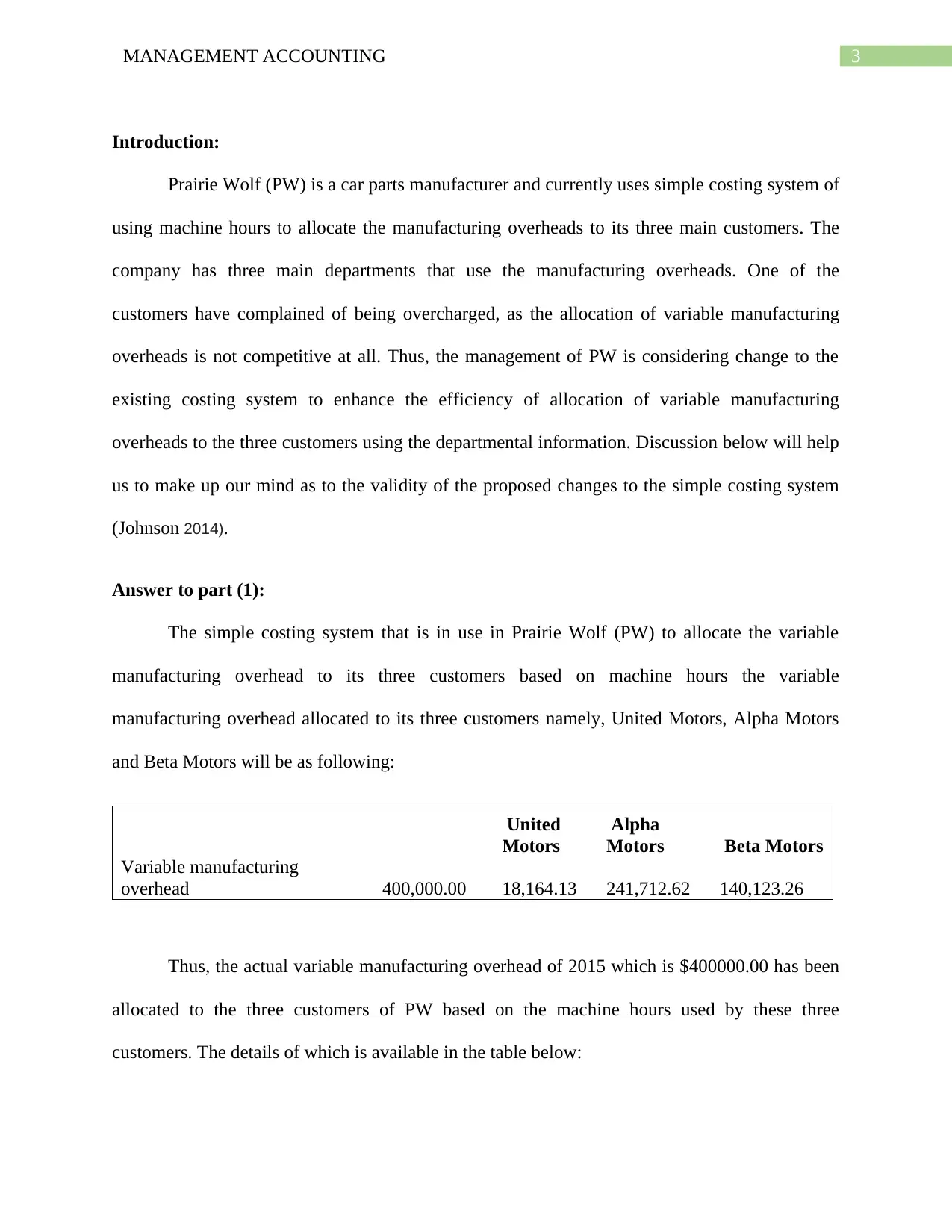

Introduction:

Prairie Wolf (PW) is a car parts manufacturer and currently uses simple costing system of

using machine hours to allocate the manufacturing overheads to its three main customers. The

company has three main departments that use the manufacturing overheads. One of the

customers have complained of being overcharged, as the allocation of variable manufacturing

overheads is not competitive at all. Thus, the management of PW is considering change to the

existing costing system to enhance the efficiency of allocation of variable manufacturing

overheads to the three customers using the departmental information. Discussion below will help

us to make up our mind as to the validity of the proposed changes to the simple costing system

(Johnson 2014).

Answer to part (1):

The simple costing system that is in use in Prairie Wolf (PW) to allocate the variable

manufacturing overhead to its three customers based on machine hours the variable

manufacturing overhead allocated to its three customers namely, United Motors, Alpha Motors

and Beta Motors will be as following:

United

Motors

Alpha

Motors Beta Motors

Variable manufacturing

overhead 400,000.00 18,164.13 241,712.62 140,123.26

Thus, the actual variable manufacturing overhead of 2015 which is $400000.00 has been

allocated to the three customers of PW based on the machine hours used by these three

customers. The details of which is available in the table below:

Introduction:

Prairie Wolf (PW) is a car parts manufacturer and currently uses simple costing system of

using machine hours to allocate the manufacturing overheads to its three main customers. The

company has three main departments that use the manufacturing overheads. One of the

customers have complained of being overcharged, as the allocation of variable manufacturing

overheads is not competitive at all. Thus, the management of PW is considering change to the

existing costing system to enhance the efficiency of allocation of variable manufacturing

overheads to the three customers using the departmental information. Discussion below will help

us to make up our mind as to the validity of the proposed changes to the simple costing system

(Johnson 2014).

Answer to part (1):

The simple costing system that is in use in Prairie Wolf (PW) to allocate the variable

manufacturing overhead to its three customers based on machine hours the variable

manufacturing overhead allocated to its three customers namely, United Motors, Alpha Motors

and Beta Motors will be as following:

United

Motors

Alpha

Motors Beta Motors

Variable manufacturing

overhead 400,000.00 18,164.13 241,712.62 140,123.26

Thus, the actual variable manufacturing overhead of 2015 which is $400000.00 has been

allocated to the three customers of PW based on the machine hours used by these three

customers. The details of which is available in the table below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

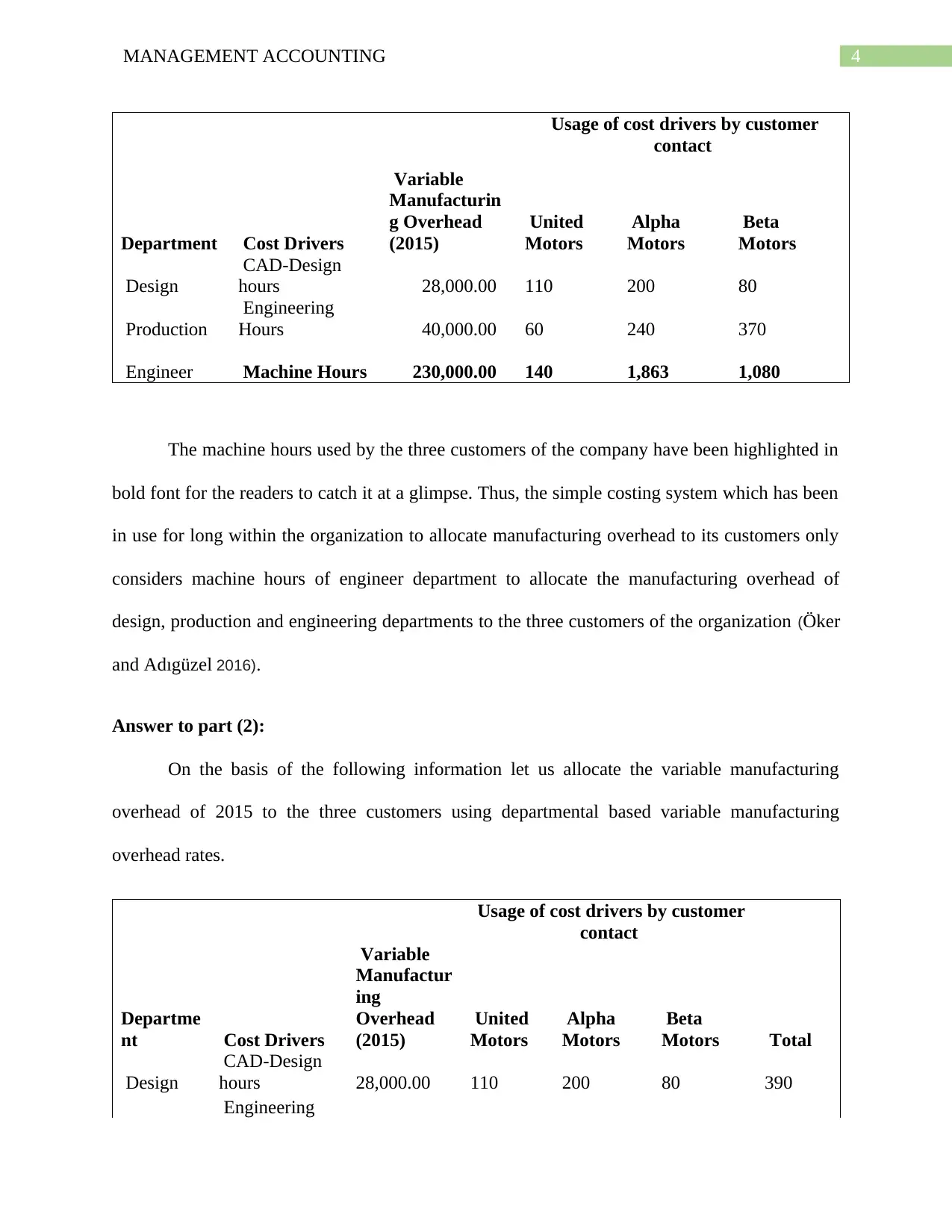

Usage of cost drivers by customer

contact

Department Cost Drivers

Variable

Manufacturin

g Overhead

(2015)

United

Motors

Alpha

Motors

Beta

Motors

Design

CAD-Design

hours 28,000.00 110 200 80

Production

Engineering

Hours 40,000.00 60 240 370

Engineer Machine Hours 230,000.00 140 1,863 1,080

The machine hours used by the three customers of the company have been highlighted in

bold font for the readers to catch it at a glimpse. Thus, the simple costing system which has been

in use for long within the organization to allocate manufacturing overhead to its customers only

considers machine hours of engineer department to allocate the manufacturing overhead of

design, production and engineering departments to the three customers of the organization (Öker

and Adıgüzel 2016).

Answer to part (2):

On the basis of the following information let us allocate the variable manufacturing

overhead of 2015 to the three customers using departmental based variable manufacturing

overhead rates.

Usage of cost drivers by customer

contact

Departme

nt Cost Drivers

Variable

Manufactur

ing

Overhead

(2015)

United

Motors

Alpha

Motors

Beta

Motors Total

Design

CAD-Design

hours 28,000.00 110 200 80 390

Engineering

Usage of cost drivers by customer

contact

Department Cost Drivers

Variable

Manufacturin

g Overhead

(2015)

United

Motors

Alpha

Motors

Beta

Motors

Design

CAD-Design

hours 28,000.00 110 200 80

Production

Engineering

Hours 40,000.00 60 240 370

Engineer Machine Hours 230,000.00 140 1,863 1,080

The machine hours used by the three customers of the company have been highlighted in

bold font for the readers to catch it at a glimpse. Thus, the simple costing system which has been

in use for long within the organization to allocate manufacturing overhead to its customers only

considers machine hours of engineer department to allocate the manufacturing overhead of

design, production and engineering departments to the three customers of the organization (Öker

and Adıgüzel 2016).

Answer to part (2):

On the basis of the following information let us allocate the variable manufacturing

overhead of 2015 to the three customers using departmental based variable manufacturing

overhead rates.

Usage of cost drivers by customer

contact

Departme

nt Cost Drivers

Variable

Manufactur

ing

Overhead

(2015)

United

Motors

Alpha

Motors

Beta

Motors Total

Design

CAD-Design

hours 28,000.00 110 200 80 390

Engineering

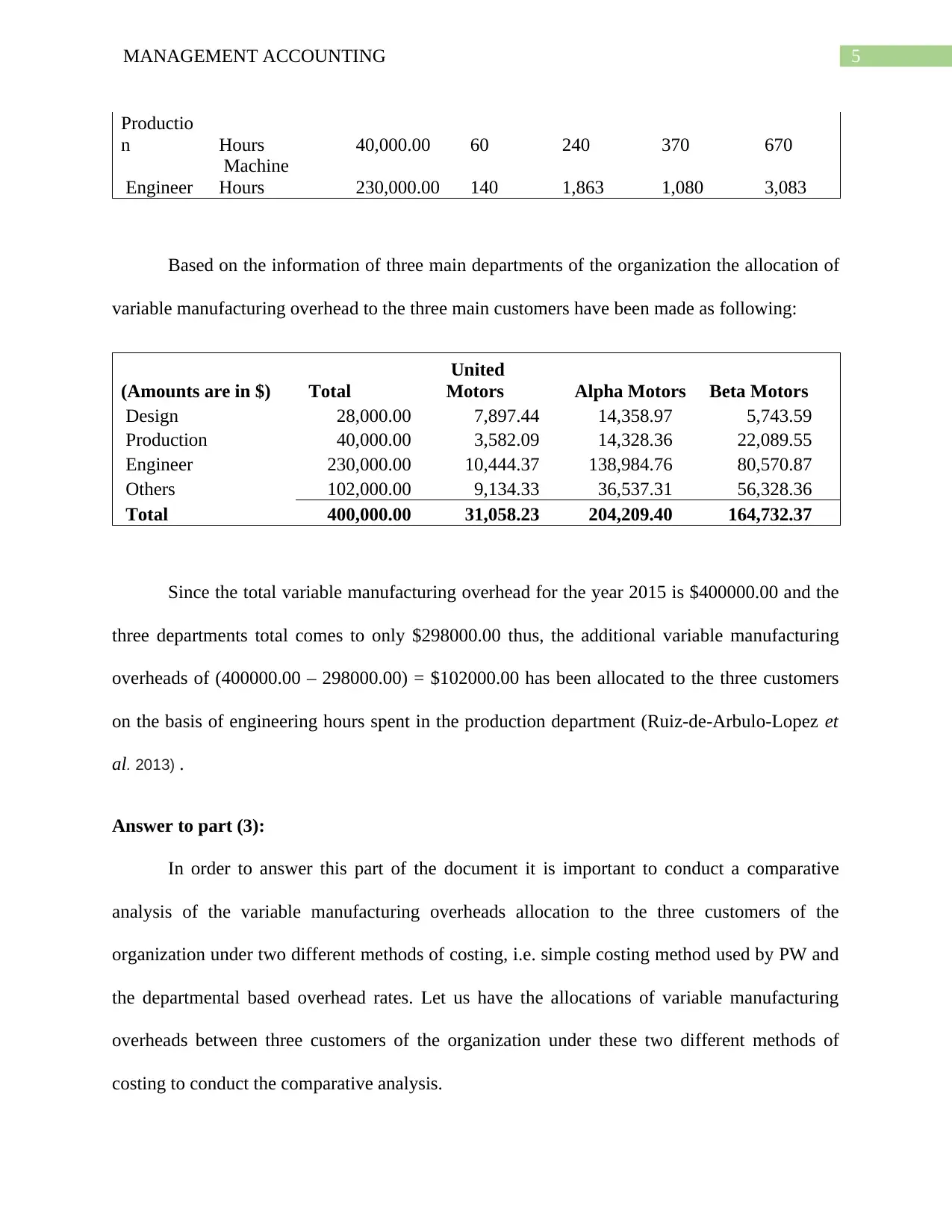

5MANAGEMENT ACCOUNTING

Productio

n Hours 40,000.00 60 240 370 670

Engineer

Machine

Hours 230,000.00 140 1,863 1,080 3,083

Based on the information of three main departments of the organization the allocation of

variable manufacturing overhead to the three main customers have been made as following:

(Amounts are in $) Total

United

Motors Alpha Motors Beta Motors

Design 28,000.00 7,897.44 14,358.97 5,743.59

Production 40,000.00 3,582.09 14,328.36 22,089.55

Engineer 230,000.00 10,444.37 138,984.76 80,570.87

Others 102,000.00 9,134.33 36,537.31 56,328.36

Total 400,000.00 31,058.23 204,209.40 164,732.37

Since the total variable manufacturing overhead for the year 2015 is $400000.00 and the

three departments total comes to only $298000.00 thus, the additional variable manufacturing

overheads of (400000.00 – 298000.00) = $102000.00 has been allocated to the three customers

on the basis of engineering hours spent in the production department (Ruiz-de-Arbulo-Lopez et

al. 2013) .

Answer to part (3):

In order to answer this part of the document it is important to conduct a comparative

analysis of the variable manufacturing overheads allocation to the three customers of the

organization under two different methods of costing, i.e. simple costing method used by PW and

the departmental based overhead rates. Let us have the allocations of variable manufacturing

overheads between three customers of the organization under these two different methods of

costing to conduct the comparative analysis.

Productio

n Hours 40,000.00 60 240 370 670

Engineer

Machine

Hours 230,000.00 140 1,863 1,080 3,083

Based on the information of three main departments of the organization the allocation of

variable manufacturing overhead to the three main customers have been made as following:

(Amounts are in $) Total

United

Motors Alpha Motors Beta Motors

Design 28,000.00 7,897.44 14,358.97 5,743.59

Production 40,000.00 3,582.09 14,328.36 22,089.55

Engineer 230,000.00 10,444.37 138,984.76 80,570.87

Others 102,000.00 9,134.33 36,537.31 56,328.36

Total 400,000.00 31,058.23 204,209.40 164,732.37

Since the total variable manufacturing overhead for the year 2015 is $400000.00 and the

three departments total comes to only $298000.00 thus, the additional variable manufacturing

overheads of (400000.00 – 298000.00) = $102000.00 has been allocated to the three customers

on the basis of engineering hours spent in the production department (Ruiz-de-Arbulo-Lopez et

al. 2013) .

Answer to part (3):

In order to answer this part of the document it is important to conduct a comparative

analysis of the variable manufacturing overheads allocation to the three customers of the

organization under two different methods of costing, i.e. simple costing method used by PW and

the departmental based overhead rates. Let us have the allocations of variable manufacturing

overheads between three customers of the organization under these two different methods of

costing to conduct the comparative analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

On the basis of Simple costing system of machine hours

Total

United

Motors

Alpha

Motors Beta Motors

Variable manufacturing

overhead 400,000.00 18,164.13 241,712.62 140,123.26

Under departmental absorbed overhead rates

(Amounts are in $) Total

United

Motors Alpha Motors Beta Motors

Design 28,000.00 7,897.44 14,358.97 5,743.59

Production 40,000.00 3,582.09 14,328.36 22,089.55

Engineer 230,000.00 10,444.37 138,984.76 80,570.87

Others 102,000.00 9,134.33 36,537.31 56,328.36

Total 400,000.00 31,058.23 204,209.40 164,732.37

Comparison Total

United

Motors

Alpha

Motors

Beta

Motors

On the basis of Simple costing system

of machine hours 400,000.00 18,164.13 241,712.62 140,123.26

Under departmental absorbed overhead

rates 400,000.00 31,058.23 204,209.40 164,732.37

Changes in variable manufacturing

cost - 12,894.10

(37,503.22

) 24,609.12

From the above comparison, it is clear that if the costing system of PW is changed from

the simple costing to departmental based overhead rates. The new system is applied for efficient

allocation of variable manufacturing overheads between three customers of the organization

Alpha Motors will be befitted as allocation of variable manufacturing overheads in simple

costing system is unnecessary burdening the organization, i.e. Alpha Motors. Thus, it is clear

On the basis of Simple costing system of machine hours

Total

United

Motors

Alpha

Motors Beta Motors

Variable manufacturing

overhead 400,000.00 18,164.13 241,712.62 140,123.26

Under departmental absorbed overhead rates

(Amounts are in $) Total

United

Motors Alpha Motors Beta Motors

Design 28,000.00 7,897.44 14,358.97 5,743.59

Production 40,000.00 3,582.09 14,328.36 22,089.55

Engineer 230,000.00 10,444.37 138,984.76 80,570.87

Others 102,000.00 9,134.33 36,537.31 56,328.36

Total 400,000.00 31,058.23 204,209.40 164,732.37

Comparison Total

United

Motors

Alpha

Motors

Beta

Motors

On the basis of Simple costing system

of machine hours 400,000.00 18,164.13 241,712.62 140,123.26

Under departmental absorbed overhead

rates 400,000.00 31,058.23 204,209.40 164,732.37

Changes in variable manufacturing

cost - 12,894.10

(37,503.22

) 24,609.12

From the above comparison, it is clear that if the costing system of PW is changed from

the simple costing to departmental based overhead rates. The new system is applied for efficient

allocation of variable manufacturing overheads between three customers of the organization

Alpha Motors will be befitted as allocation of variable manufacturing overheads in simple

costing system is unnecessary burdening the organization, i.e. Alpha Motors. Thus, it is clear

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

Alpha Motors is the one that should be complaining for being overcharged (Laudon and Laudon

2016).

Except Alpha Motors, other two customers United Motors and Beta motors both will be

unhappy with the departmental based rates for allocation of variable manufacturing overheads, as

both these customers will be charged more under the departmental based overhead rates. The

variable manufacturing overheads will be $37503.22 less for Alpha Motors and $12894.10 and

$24609.12 more respectively for United Motors and Beta Motors. Thus, Both United Motors and

Beta Motors will not be happy with the use of departmental based overhead rates for allocation

of variable manufacturing overheads.

Irrespective of one’s happiness or otherwise an organization always looks to improve its

accounting and costing system to price its products and allocate its overheads better. Use of

departmental based rates to allocate the variable manufacturing overheads will certainly help PW

to allocate its overheads better amongst the three customers of the organization than by using

simple costing system. Hence, the customers of the organization shall be convinced that use of

departmental based rates is appropriate to allocate the variable manufacturing overheads (Heizer

2016).

Answer to part (4):

Apart from allocation of variable manufacturing overheads between the three customers

of the organization, PW can also use the available departmental information to allocate other

expenditures that have been spent on the production and completion of different car parts for the

three customers of the organization. The expenditures that are not directly related to the

manufacturing of car parts but associated costs such as carriages, fare, rent of spaces used by the

Alpha Motors is the one that should be complaining for being overcharged (Laudon and Laudon

2016).

Except Alpha Motors, other two customers United Motors and Beta motors both will be

unhappy with the departmental based rates for allocation of variable manufacturing overheads, as

both these customers will be charged more under the departmental based overhead rates. The

variable manufacturing overheads will be $37503.22 less for Alpha Motors and $12894.10 and

$24609.12 more respectively for United Motors and Beta Motors. Thus, Both United Motors and

Beta Motors will not be happy with the use of departmental based overhead rates for allocation

of variable manufacturing overheads.

Irrespective of one’s happiness or otherwise an organization always looks to improve its

accounting and costing system to price its products and allocate its overheads better. Use of

departmental based rates to allocate the variable manufacturing overheads will certainly help PW

to allocate its overheads better amongst the three customers of the organization than by using

simple costing system. Hence, the customers of the organization shall be convinced that use of

departmental based rates is appropriate to allocate the variable manufacturing overheads (Heizer

2016).

Answer to part (4):

Apart from allocation of variable manufacturing overheads between the three customers

of the organization, PW can also use the available departmental information to allocate other

expenditures that have been spent on the production and completion of different car parts for the

three customers of the organization. The expenditures that are not directly related to the

manufacturing of car parts but associated costs such as carriages, fare, rent of spaces used by the

8MANAGEMENT ACCOUNTING

organization, office expenses etc. can also be allocated properly to the three customers based on

the departmental information (Popesko 2013).

Answer to part (5):

Activity Based Costing system (ABC system) is an efficient costing systems that identify

activities that directly related to the performance of an organization and uses these activities to

assign indirect costs to different products of an organization. Recognition of the relationship

between costs, activities and products to understand the relationship and assign the indirect costs

to the products of the company. Manufacturing industries use ABC system to enhance the

reliability of cost data. In case of PW since it is in the business of manufacturing car parts, use of

ABC system would be beneficial to the organization, as it will enhance the reliability of cost

data.

However, in case there are number of costs and expenditures that are general in nature

and not specific to different activities then the use of ABC system would not be worthwhile to

further refine the departmental based overhead rates costing system (Mitra 2016).

Answer to part (6):

In order to improve the productivity of the machine hours in engineering department the

first step that the management must take is to reduce the idle hours of engineering department.

The manager of the engineering department should be asked to take extra care in order to reduce

the unnecessary idle hours in the department. Workers and employees of engineering department

should be asked to maintain the time line of entering and exiting the premises. The machines in

the engineering department should be maintained properly to ensure that there is no breakdown

of machines (Elhamma and Zhang 2013). This will substantially reduce unproductive hours of

organization, office expenses etc. can also be allocated properly to the three customers based on

the departmental information (Popesko 2013).

Answer to part (5):

Activity Based Costing system (ABC system) is an efficient costing systems that identify

activities that directly related to the performance of an organization and uses these activities to

assign indirect costs to different products of an organization. Recognition of the relationship

between costs, activities and products to understand the relationship and assign the indirect costs

to the products of the company. Manufacturing industries use ABC system to enhance the

reliability of cost data. In case of PW since it is in the business of manufacturing car parts, use of

ABC system would be beneficial to the organization, as it will enhance the reliability of cost

data.

However, in case there are number of costs and expenditures that are general in nature

and not specific to different activities then the use of ABC system would not be worthwhile to

further refine the departmental based overhead rates costing system (Mitra 2016).

Answer to part (6):

In order to improve the productivity of the machine hours in engineering department the

first step that the management must take is to reduce the idle hours of engineering department.

The manager of the engineering department should be asked to take extra care in order to reduce

the unnecessary idle hours in the department. Workers and employees of engineering department

should be asked to maintain the time line of entering and exiting the premises. The machines in

the engineering department should be maintained properly to ensure that there is no breakdown

of machines (Elhamma and Zhang 2013). This will substantially reduce unproductive hours of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

engineering department. Proper employee should be recruited for different jobs in the

engineering department to further enhance the productivity of the department and the company

as a whole.

Conclusion:

Taking into consideration the above discussion it is clear that a manufacturing

organization should use a proper costing system to allocate its overheads and expenditures

properly to its different manufacturing products. This will help an organization to not only

allocate the expenditures and overheads properly to different products but also to price it

products better.

engineering department. Proper employee should be recruited for different jobs in the

engineering department to further enhance the productivity of the department and the company

as a whole.

Conclusion:

Taking into consideration the above discussion it is clear that a manufacturing

organization should use a proper costing system to allocate its overheads and expenditures

properly to its different manufacturing products. This will help an organization to not only

allocate the expenditures and overheads properly to different products but also to price it

products better.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

References:

Elhamma, A. and Zhang, Y.I., 2013. The relationship between activity based costing, business

strategy and performance in Moroccan enterprises. Accounting and Management Information

Systems, 12(1), p.22.

Heizer, J., 2016. Operations Management, 11/e. Pearson Education India.

Johnson, P.F., 2014. Purchasing and supply management. McGraw-Hill Higher Education.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Mitra, A., 2016. Fundamentals of quality control and improvement. John Wiley & Sons.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Popesko, B., 2013. Specifics of the activity-based costing applications in hospital

management. International Journal of Collaborative Research on Internal Medicine & Public

Health.

Ruiz-de-Arbulo-Lopez, P., Fortuny-Santos, J. and Cuatrecasas-Arbós, L., 2013. Lean

manufacturing: costing the value stream. Industrial Management & Data Systems, 113(5),

pp.647-668.

References:

Elhamma, A. and Zhang, Y.I., 2013. The relationship between activity based costing, business

strategy and performance in Moroccan enterprises. Accounting and Management Information

Systems, 12(1), p.22.

Heizer, J., 2016. Operations Management, 11/e. Pearson Education India.

Johnson, P.F., 2014. Purchasing and supply management. McGraw-Hill Higher Education.

Laudon, K.C. and Laudon, J.P., 2016. Management information system. Pearson Education

India.

Mitra, A., 2016. Fundamentals of quality control and improvement. John Wiley & Sons.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Popesko, B., 2013. Specifics of the activity-based costing applications in hospital

management. International Journal of Collaborative Research on Internal Medicine & Public

Health.

Ruiz-de-Arbulo-Lopez, P., Fortuny-Santos, J. and Cuatrecasas-Arbós, L., 2013. Lean

manufacturing: costing the value stream. Industrial Management & Data Systems, 113(5),

pp.647-668.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.