Seymour Civil Engineering: Management Accounting Report and Analysis

VerifiedAdded on 2020/12/09

|17

|3742

|280

Report

AI Summary

This report provides a detailed examination of management accounting principles and their practical application within the Seymour Civil Engineering company. It explores various management accounting systems, including price optimization, inventory management, and cost accounting, and how these systems are integrated into organizational processes. The report analyzes different management accounting reporting methods, such as budget reports, performance reports, and cost managerial accounting reports, illustrating their significance in evaluating business performance. Furthermore, it discusses the benefits of these systems and how organizations adapt them to address financial problems, emphasizing the role of planning tools in budgetary control and the pursuit of sustainable success. The report includes financial data, such as overhead costs and payback period calculations, to support the analysis. This report is an example of a solved assignment available on Desklib, a platform offering AI-based study tools for students.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different type of management accounting systems............1

P2 Different methods of management accounting reporting......................................................3

M1 Benefits of different management accounting systems. ......................................................4

D1 Management accounting system and reporting are integrated with the organisational

process.........................................................................................................................................5

TASK 3............................................................................................................................................5

P4. The various kinds of planning tools utilised for budgetary control......................................5

M3. Analyse the utilisation of different planning tools and their application preparing and

forecasting budgets......................................................................................................................7

TASK 4............................................................................................................................................7

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.......................................................................................................................7

M4. Analysis of responding to financial problems, management accounting can lead

organisation to sustainable success.............................................................................................9

D3. Evaluation of planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success................................................................9

CONCLUSION:.............................................................................................................................10

REFRENCES.................................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its different type of management accounting systems............1

P2 Different methods of management accounting reporting......................................................3

M1 Benefits of different management accounting systems. ......................................................4

D1 Management accounting system and reporting are integrated with the organisational

process.........................................................................................................................................5

TASK 3............................................................................................................................................5

P4. The various kinds of planning tools utilised for budgetary control......................................5

M3. Analyse the utilisation of different planning tools and their application preparing and

forecasting budgets......................................................................................................................7

TASK 4............................................................................................................................................7

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.......................................................................................................................7

M4. Analysis of responding to financial problems, management accounting can lead

organisation to sustainable success.............................................................................................9

D3. Evaluation of planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success................................................................9

CONCLUSION:.............................................................................................................................10

REFRENCES.................................................................................................................................11

INTRODUCTION

Management accounting is an accounting system which helps in the internal management

of the companies. This includes various kind of financial and non financial information that

becomes framework for the future planning and strategies. It analyse the business activities in a

conclusion way (Sánchez-Matamoros, Araujo Pinzon and Alvarez-Dardet Espejo, 2014). Herein,

it is important to know that management accounting is not a compulsory part of the companies. It

depends on the companies that whether they need it or not. To understand about management

accounting concept, its tools and techniques in the context of organisation, The Seymour civil

engineering company is selected. This company has its head office at Hartlepool, UK. It works

for different civil projects of customers.

This project report includes detailed knowledge about management accounting, its

various techniques and system. In addition it consists the way in which management accounting

system helps in solving the financial issues of the organisations.

TASK 1.

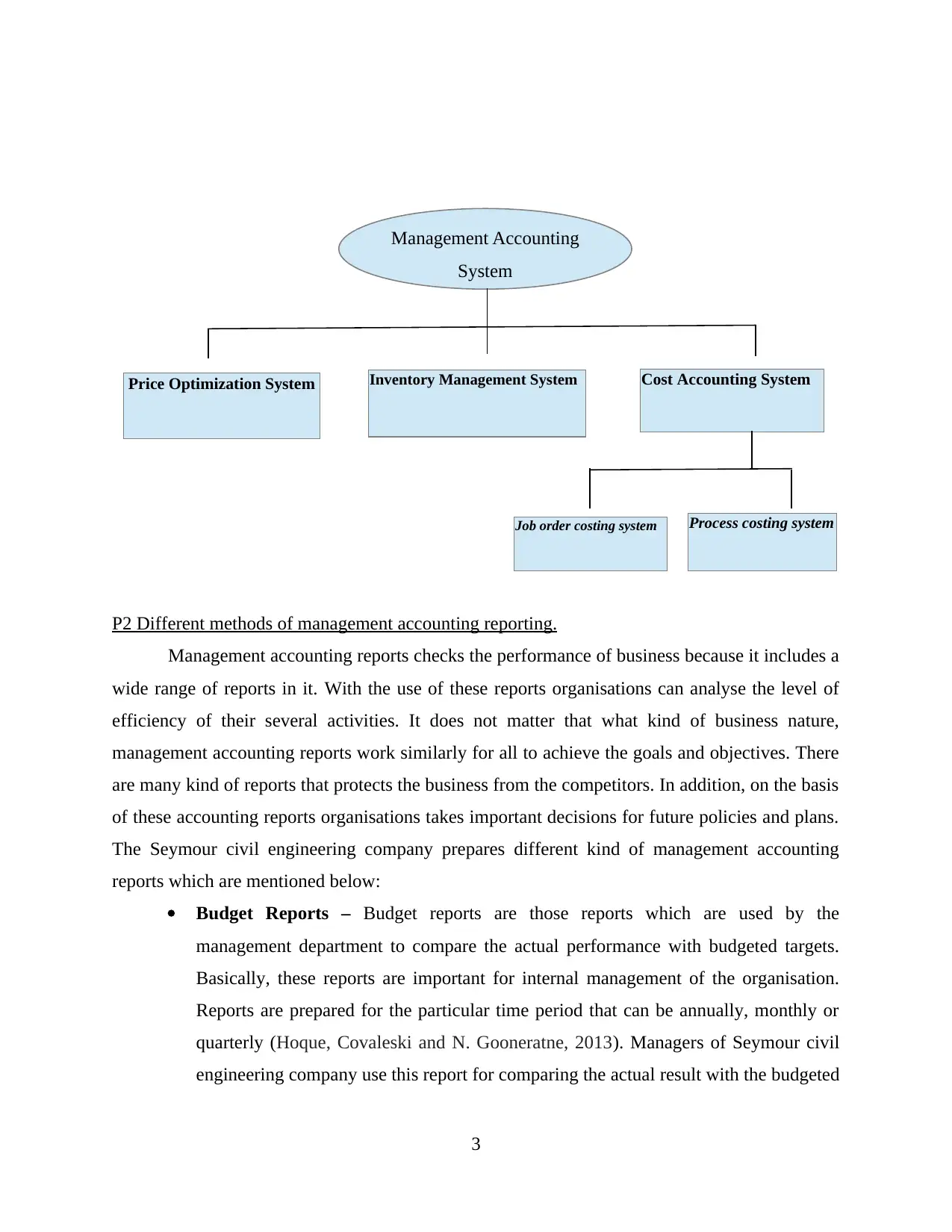

P1 Management accounting and its different type of management accounting systems.

Management accounting system is very important accounting tool for the companies. It

includes both kind of information monetary and non monetary that is required in the effective

management of the business. Apart from this, it consists various kind of tools and techniques that

enhance the decision making of the organisations for future. This accounting system does not

require to implement according to the accounting period and rules. The selected company

Seymour civil engineering company use this accounting system in their functions to improve the

services and various projects. It includes various kind of other management accounting systems

which are followings:

Price Optimization System- Price optimization system is a method of fixing the price of

different services and products. It provides a basis of analysing the level of price that can be

suitable for both to the customers and company. In addition, this also offers the way to identify

the customers’ behaviour at different pricing level (Ji, 2017). With the use of this system,

organisations can set the prices at the beneficial level. The Seymour civil engineering company

use this tool for determining the price of different construction projects and services which helps

1

Management accounting is an accounting system which helps in the internal management

of the companies. This includes various kind of financial and non financial information that

becomes framework for the future planning and strategies. It analyse the business activities in a

conclusion way (Sánchez-Matamoros, Araujo Pinzon and Alvarez-Dardet Espejo, 2014). Herein,

it is important to know that management accounting is not a compulsory part of the companies. It

depends on the companies that whether they need it or not. To understand about management

accounting concept, its tools and techniques in the context of organisation, The Seymour civil

engineering company is selected. This company has its head office at Hartlepool, UK. It works

for different civil projects of customers.

This project report includes detailed knowledge about management accounting, its

various techniques and system. In addition it consists the way in which management accounting

system helps in solving the financial issues of the organisations.

TASK 1.

P1 Management accounting and its different type of management accounting systems.

Management accounting system is very important accounting tool for the companies. It

includes both kind of information monetary and non monetary that is required in the effective

management of the business. Apart from this, it consists various kind of tools and techniques that

enhance the decision making of the organisations for future. This accounting system does not

require to implement according to the accounting period and rules. The selected company

Seymour civil engineering company use this accounting system in their functions to improve the

services and various projects. It includes various kind of other management accounting systems

which are followings:

Price Optimization System- Price optimization system is a method of fixing the price of

different services and products. It provides a basis of analysing the level of price that can be

suitable for both to the customers and company. In addition, this also offers the way to identify

the customers’ behaviour at different pricing level (Ji, 2017). With the use of this system,

organisations can set the prices at the beneficial level. The Seymour civil engineering company

use this tool for determining the price of different construction projects and services which helps

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them in the attracting more clients. As well as it is required by the company to analyse the

behaviour of their clients at different price levels.

Inventory Management System- Inventory management system is a kind of system that

tracks the movement of different goods and services in entire process. It also helps in checking

about the quantity of raw material and finished goods that helps the companies to do production

accordingly. As well as the main key function of the inventory management system is the

keeping record of all the goods that transfer within the warehouse. The Seymour civil

engineering company implements the inventory management system in the various services and

construction projects. They use it in checking the availability of different type of raw material

like cement, steel etc. in the warehouses. This system is required to track the quantity of raw

material of different projects of company. In addition this system works according to the LIFO

and FIFO system that aligns with this for better result.

Cost Accounting System- Cost accounting system is a systematic way of estimating the

total cost of products and services so that companies can analyse the profitability and loss on

different product and service (Proctor, 2012). This accounting system is categorised into two

parts: job order costing system and process costing system. It is required in the organisations to

calculate all the costs so that company can control over the cost. The Seymour civil engineering

company use both of the system of cost accounting which are described below:

Job order costing system- It is a costing system that is applicable in both service and

products providing industries. This costing system use the job cost sheet, material and labour

cash flows to analyse the cost of various products and services. As well as it works when the

customers give order for any particular service and products. The Seymour civil engineering

company applies this costing system for evaluating the cost of different kind of services which

they offer in the market. They use it calculating the cost of various kind of civil projects and this

helps them in proper analysing in the terms of profit or loss.

Process costing system- Process costing system is a method for assigning the total cost to

different units of output. Herein, this method the entire cost of different processes is calculated

then it is considered as the sum of total cost of various product and services (Zhang, Uchida and

Bu, 2013). The Seymour civil engineering company use this costing system for estimating the

total cost of projects by analysing costs at various stages or processes of civil projects.

2

behaviour of their clients at different price levels.

Inventory Management System- Inventory management system is a kind of system that

tracks the movement of different goods and services in entire process. It also helps in checking

about the quantity of raw material and finished goods that helps the companies to do production

accordingly. As well as the main key function of the inventory management system is the

keeping record of all the goods that transfer within the warehouse. The Seymour civil

engineering company implements the inventory management system in the various services and

construction projects. They use it in checking the availability of different type of raw material

like cement, steel etc. in the warehouses. This system is required to track the quantity of raw

material of different projects of company. In addition this system works according to the LIFO

and FIFO system that aligns with this for better result.

Cost Accounting System- Cost accounting system is a systematic way of estimating the

total cost of products and services so that companies can analyse the profitability and loss on

different product and service (Proctor, 2012). This accounting system is categorised into two

parts: job order costing system and process costing system. It is required in the organisations to

calculate all the costs so that company can control over the cost. The Seymour civil engineering

company use both of the system of cost accounting which are described below:

Job order costing system- It is a costing system that is applicable in both service and

products providing industries. This costing system use the job cost sheet, material and labour

cash flows to analyse the cost of various products and services. As well as it works when the

customers give order for any particular service and products. The Seymour civil engineering

company applies this costing system for evaluating the cost of different kind of services which

they offer in the market. They use it calculating the cost of various kind of civil projects and this

helps them in proper analysing in the terms of profit or loss.

Process costing system- Process costing system is a method for assigning the total cost to

different units of output. Herein, this method the entire cost of different processes is calculated

then it is considered as the sum of total cost of various product and services (Zhang, Uchida and

Bu, 2013). The Seymour civil engineering company use this costing system for estimating the

total cost of projects by analysing costs at various stages or processes of civil projects.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Different methods of management accounting reporting.

Management accounting reports checks the performance of business because it includes a

wide range of reports in it. With the use of these reports organisations can analyse the level of

efficiency of their several activities. It does not matter that what kind of business nature,

management accounting reports work similarly for all to achieve the goals and objectives. There

are many kind of reports that protects the business from the competitors. In addition, on the basis

of these accounting reports organisations takes important decisions for future policies and plans.

The Seymour civil engineering company prepares different kind of management accounting

reports which are mentioned below:

Budget Reports – Budget reports are those reports which are used by the

management department to compare the actual performance with budgeted targets.

Basically, these reports are important for internal management of the organisation.

Reports are prepared for the particular time period that can be annually, monthly or

quarterly (Hoque, Covaleski and N. Gooneratne, 2013). Managers of Seymour civil

engineering company use this report for comparing the actual result with the budgeted

3

Management Accounting

System

Price Optimization System Inventory Management System Cost Accounting System

Job order costing system Process costing system

Management accounting reports checks the performance of business because it includes a

wide range of reports in it. With the use of these reports organisations can analyse the level of

efficiency of their several activities. It does not matter that what kind of business nature,

management accounting reports work similarly for all to achieve the goals and objectives. There

are many kind of reports that protects the business from the competitors. In addition, on the basis

of these accounting reports organisations takes important decisions for future policies and plans.

The Seymour civil engineering company prepares different kind of management accounting

reports which are mentioned below:

Budget Reports – Budget reports are those reports which are used by the

management department to compare the actual performance with budgeted targets.

Basically, these reports are important for internal management of the organisation.

Reports are prepared for the particular time period that can be annually, monthly or

quarterly (Hoque, Covaleski and N. Gooneratne, 2013). Managers of Seymour civil

engineering company use this report for comparing the actual result with the budgeted

3

Management Accounting

System

Price Optimization System Inventory Management System Cost Accounting System

Job order costing system Process costing system

standards. As well as it helps them in analysing which engineering projects are

profitable and which ones are not.

Performance Reports- Performance reports are the reports that are prepared to

evaluate the performance of different activities. These reports are very important in

the context of the organisations because it helps them in checking about which

activities are giving the expected results and which ones are not. Basically, project

reports work on the basis of comparing the actual result of a particular activity with

the standard. In this context, it is important to determine the standard of performance

measurement because in the absence of accurate level of standard it can be difficult to

measure the performance. The Seymour civil engineering company use this report to

evaluate their performance and to take futuristic decisions regarding to the multi-pal

projects. The company use this report to check the performance of the various kind of

projects profit and loss.

Cost managerial accounting reports- Cost managerial accounting reports are kind

of reports that are related to the computing the overall cost which occurs in offering

products and services (Kalkhouran and et.al, 2015). It provides a framework to make

comprehensive analysis of total cost that incurred and total money earned by selling

of all units. Herein, if costs are more than selling amount then it would be loss and if

cost is less then sold money that would the profit. So with the help of this companies

can make decision about which products and services are needed to be produced more

and which ones should stop. In the Seymour civil engineering company their

managers use this report for calculate the total cost of projects and then analyse about

the revenue and loss.

Account receivable ageing report- Account receivable ageing report is helpful in

making list of those customers who have credit transaction with the company. Due to

this report organisation can check about how much amount they are needed to receive

from the customer. As well as it contains the date on which transaction took place,

this helps the company in listing about how many customers crossed the date of

payment (Zirkler, 2013). The finance department of Seymour civil engineering

company prepares this reports to see the total collection in the market so that they can

make future policies and plans accordingly. In addition, it also minimises the

4

profitable and which ones are not.

Performance Reports- Performance reports are the reports that are prepared to

evaluate the performance of different activities. These reports are very important in

the context of the organisations because it helps them in checking about which

activities are giving the expected results and which ones are not. Basically, project

reports work on the basis of comparing the actual result of a particular activity with

the standard. In this context, it is important to determine the standard of performance

measurement because in the absence of accurate level of standard it can be difficult to

measure the performance. The Seymour civil engineering company use this report to

evaluate their performance and to take futuristic decisions regarding to the multi-pal

projects. The company use this report to check the performance of the various kind of

projects profit and loss.

Cost managerial accounting reports- Cost managerial accounting reports are kind

of reports that are related to the computing the overall cost which occurs in offering

products and services (Kalkhouran and et.al, 2015). It provides a framework to make

comprehensive analysis of total cost that incurred and total money earned by selling

of all units. Herein, if costs are more than selling amount then it would be loss and if

cost is less then sold money that would the profit. So with the help of this companies

can make decision about which products and services are needed to be produced more

and which ones should stop. In the Seymour civil engineering company their

managers use this report for calculate the total cost of projects and then analyse about

the revenue and loss.

Account receivable ageing report- Account receivable ageing report is helpful in

making list of those customers who have credit transaction with the company. Due to

this report organisation can check about how much amount they are needed to receive

from the customer. As well as it contains the date on which transaction took place,

this helps the company in listing about how many customers crossed the date of

payment (Zirkler, 2013). The finance department of Seymour civil engineering

company prepares this reports to see the total collection in the market so that they can

make future policies and plans accordingly. In addition, it also minimises the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

headache of keeping remember about credit transactions because they are involved in

the business of construction projects in which lot of credit transactions occurs.

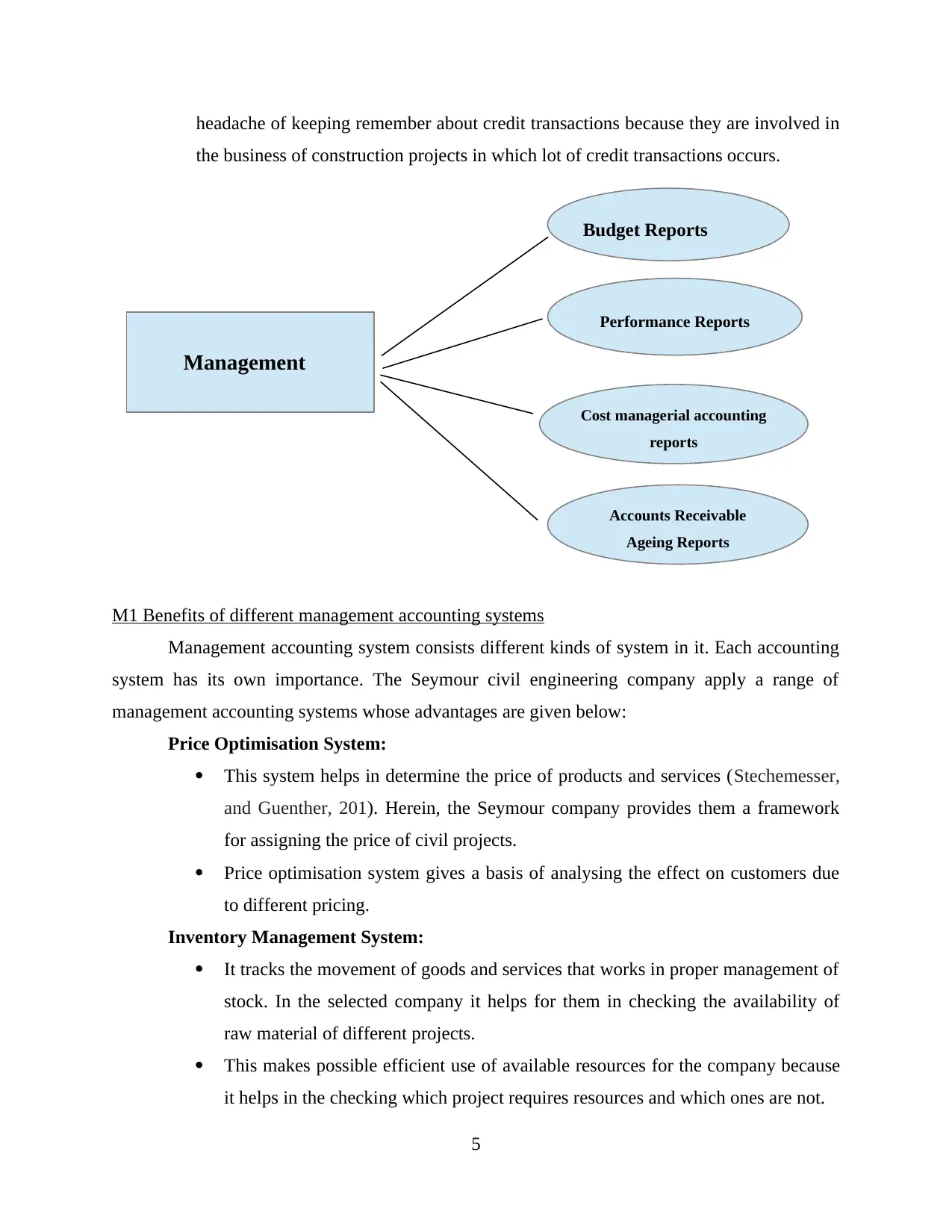

M1 Benefits of different management accounting systems

Management accounting system consists different kinds of system in it. Each accounting

system has its own importance. The Seymour civil engineering company apply a range of

management accounting systems whose advantages are given below:

Price Optimisation System:

This system helps in determine the price of products and services (Stechemesser,

and Guenther, 201). Herein, the Seymour company provides them a framework

for assigning the price of civil projects.

Price optimisation system gives a basis of analysing the effect on customers due

to different pricing.

Inventory Management System:

It tracks the movement of goods and services that works in proper management of

stock. In the selected company it helps for them in checking the availability of

raw material of different projects.

This makes possible efficient use of available resources for the company because

it helps in the checking which project requires resources and which ones are not.

5

Management

Accounting Reports

Budget Reports

Performance Reports

Cost managerial accounting

reports

Accounts Receivable

Ageing Reports

the business of construction projects in which lot of credit transactions occurs.

M1 Benefits of different management accounting systems

Management accounting system consists different kinds of system in it. Each accounting

system has its own importance. The Seymour civil engineering company apply a range of

management accounting systems whose advantages are given below:

Price Optimisation System:

This system helps in determine the price of products and services (Stechemesser,

and Guenther, 201). Herein, the Seymour company provides them a framework

for assigning the price of civil projects.

Price optimisation system gives a basis of analysing the effect on customers due

to different pricing.

Inventory Management System:

It tracks the movement of goods and services that works in proper management of

stock. In the selected company it helps for them in checking the availability of

raw material of different projects.

This makes possible efficient use of available resources for the company because

it helps in the checking which project requires resources and which ones are not.

5

Management

Accounting Reports

Budget Reports

Performance Reports

Cost managerial accounting

reports

Accounts Receivable

Ageing Reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system:

Cost accounting system is important for computing the overall cost of the

projects.

This accounting system evaluate about the actual profitability of company

by comparing the total earned amount with incurred cost.

D1 Management accounting system and reporting are integrated with the organisational process.

Management accounting system includes many accounting systems like cost accounting

system, inventory management system etc. Each accounting system is important for preparation

of accounting reports because the required information receives from the various accounting

system (Boyns, Edwards and Nikitin, 2013). In addition, this link between management

accounting system and reporting is integrated with the process of organisation. The Seymour

civil engineering company is using several accounting systems that helps for them in making

different accounting reports and it impact to the organisational process significantly.

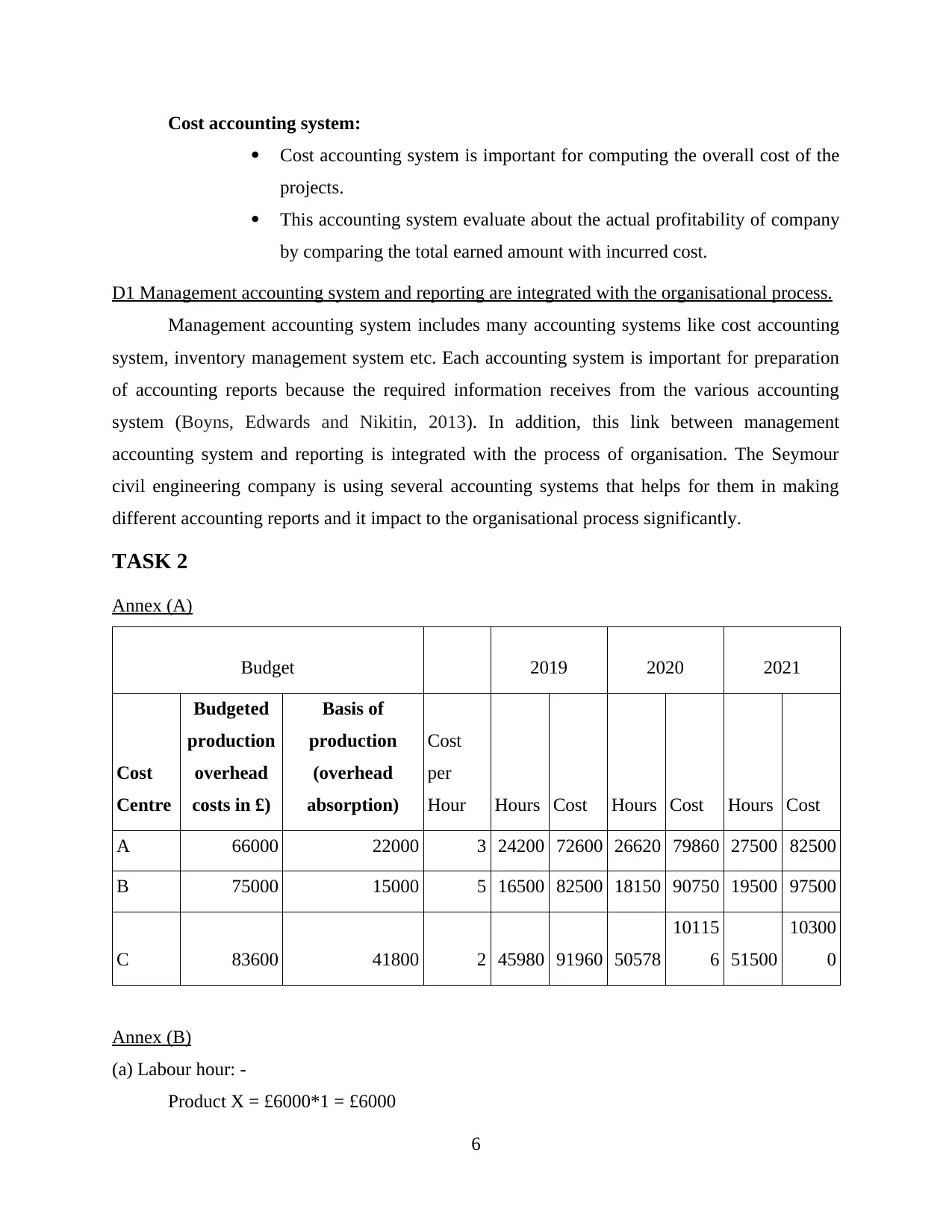

TASK 2

Annex (A)

Budget 2019 2020 2021

Cost

Centre

Budgeted

production

overhead

costs in £)

Basis of

production

(overhead

absorption)

Cost

per

Hour Hours Cost Hours Cost Hours Cost

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

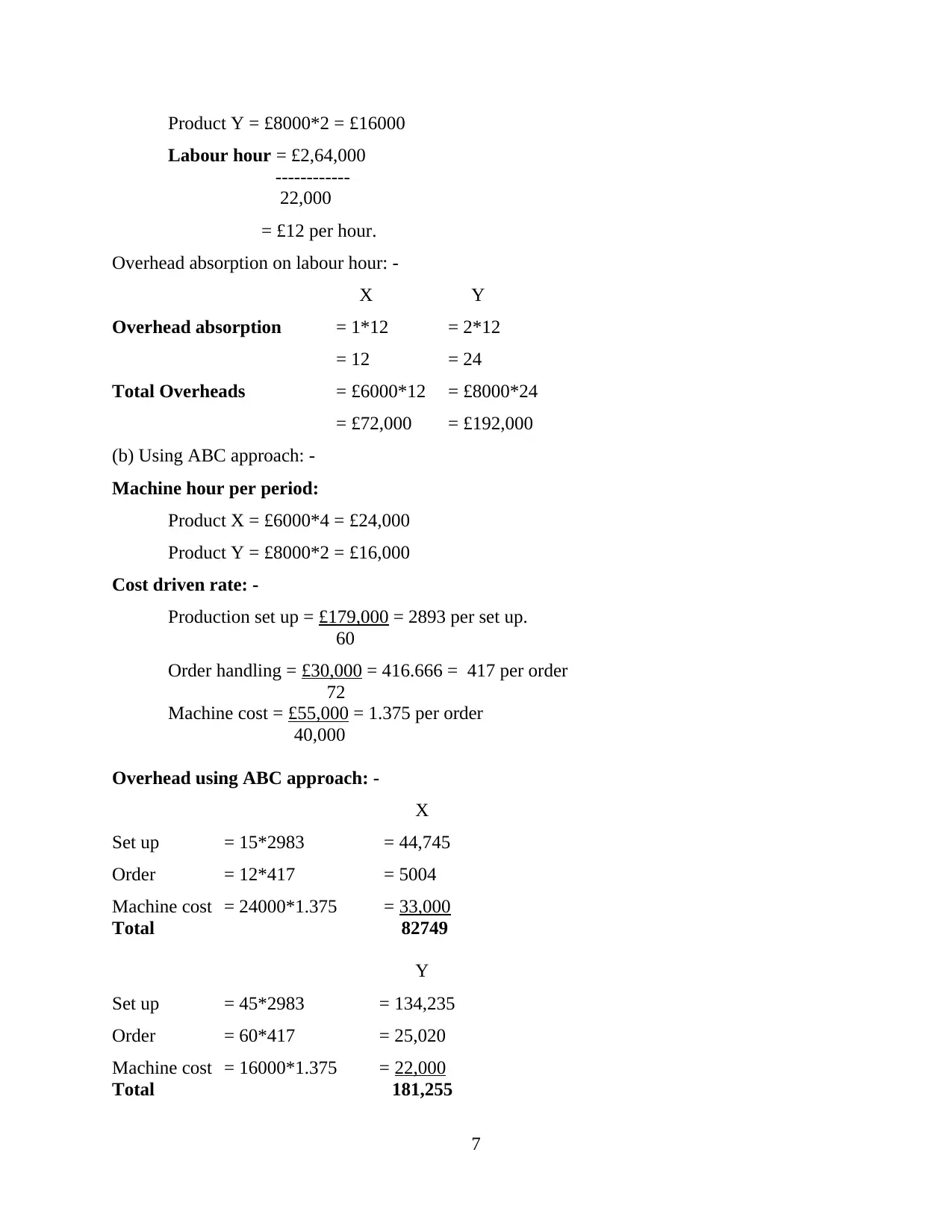

(a) Labour hour: -

Product X = £6000*1 = £6000

6

Cost accounting system is important for computing the overall cost of the

projects.

This accounting system evaluate about the actual profitability of company

by comparing the total earned amount with incurred cost.

D1 Management accounting system and reporting are integrated with the organisational process.

Management accounting system includes many accounting systems like cost accounting

system, inventory management system etc. Each accounting system is important for preparation

of accounting reports because the required information receives from the various accounting

system (Boyns, Edwards and Nikitin, 2013). In addition, this link between management

accounting system and reporting is integrated with the process of organisation. The Seymour

civil engineering company is using several accounting systems that helps for them in making

different accounting reports and it impact to the organisational process significantly.

TASK 2

Annex (A)

Budget 2019 2020 2021

Cost

Centre

Budgeted

production

overhead

costs in £)

Basis of

production

(overhead

absorption)

Cost

per

Hour Hours Cost Hours Cost Hours Cost

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

6

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

7

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4. The various kinds of planning tools utilised for budgetary control.

Budget is mainly a financial plan or a formal statement of approximated revenue as well

as expenditure based on upcoming plans and goals. Also, it forecast the financial positions and

outcomes of a firm. This is usually prepared by Seymour civil engineering company for

allocating finances for many kinds of methods and functions after examining the incomes,

expenditure as well as previous years’ profits.

Budgetary control is considered as a process for managers for setting financial as well as

performance objectives with budgets, compare exact outcomes and set performance according to

the requirements (D. Parker and Guthrie, 2014). This method is helpful for tracking and

managing budget which is ascertained for activities and procedures. Also, this is done through

seeing the variation between expected and actual outcomes for making decision how successfully

the budget is formulated in the firm. Within Seymour civil engineering company, this is used by

manager for valuing variances into budget and related that variances with performance to

prepared effectual strategies as well as policies in order to decrease those variances.

Seymour civil engineering company has to manage and control the figure of budget as

well as many process and functions for attaining sustainability in the growth and maximised

profitability. Organisation have to develop an effective plan for controlling budget that are

required to assure that functions are performed effectually. So, few crucial planning tools which

is applied through the Seymour civil engineering company for setting up the budgetary control

are explained below: Forecasting planning tools: It is the kinds of planning tools that is utilise by business

organization for developing a framework for future occurrences and events this is done

with the aids of last as well as present trends adjustments (Kastberg and Siverbo, 2016).

For profitable outcomes of this tools, it is necessary to apply appropriate and reliable data

through the external as well as internal sources of the organisations. Forecasting tools is

utilised by the Seymour civil engineering company for collecting future trends which can

influence the firm in future in negative manner.

Advantage:

8

P4. The various kinds of planning tools utilised for budgetary control.

Budget is mainly a financial plan or a formal statement of approximated revenue as well

as expenditure based on upcoming plans and goals. Also, it forecast the financial positions and

outcomes of a firm. This is usually prepared by Seymour civil engineering company for

allocating finances for many kinds of methods and functions after examining the incomes,

expenditure as well as previous years’ profits.

Budgetary control is considered as a process for managers for setting financial as well as

performance objectives with budgets, compare exact outcomes and set performance according to

the requirements (D. Parker and Guthrie, 2014). This method is helpful for tracking and

managing budget which is ascertained for activities and procedures. Also, this is done through

seeing the variation between expected and actual outcomes for making decision how successfully

the budget is formulated in the firm. Within Seymour civil engineering company, this is used by

manager for valuing variances into budget and related that variances with performance to

prepared effectual strategies as well as policies in order to decrease those variances.

Seymour civil engineering company has to manage and control the figure of budget as

well as many process and functions for attaining sustainability in the growth and maximised

profitability. Organisation have to develop an effective plan for controlling budget that are

required to assure that functions are performed effectually. So, few crucial planning tools which

is applied through the Seymour civil engineering company for setting up the budgetary control

are explained below: Forecasting planning tools: It is the kinds of planning tools that is utilise by business

organization for developing a framework for future occurrences and events this is done

with the aids of last as well as present trends adjustments (Kastberg and Siverbo, 2016).

For profitable outcomes of this tools, it is necessary to apply appropriate and reliable data

through the external as well as internal sources of the organisations. Forecasting tools is

utilised by the Seymour civil engineering company for collecting future trends which can

influence the firm in future in negative manner.

Advantage:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This aids manager of respective firm in identifying upcoming happenings and

opportunities which can impact the decisions of the business organization.

Disadvantage:

As it is hard to assume upcoming happenings so with the assistance of this tool Seymour

civil engineering company are not able to made effective approximation.

Contingency planning tools: It is the tools that are useful in valuing and apportioning

risky factor that can affects the organisational operations, growth, activities, performance and so

on in upcoming years (Kraus and Strömsten, 2012). Seymour civil engineering company apply

this tools for examining as well as measuring financial positions related to net and gross

profitability performance and conditions of many activities of firm. Also, selected organisation

have to analyse these factors also formulate strategic strategies for resolving them as early as

possible.

Advantage:

It aids Seymour civil engineering company to find out effective resources in case some

trouble created at the time of operations related to already recognise or recent resources.

Disadvantage:

This tools are too time consuming as well as costly.

Scenario Planning tools: It is the tools that developed a structured and managed manner

for improving structures for strategical planning of organisation. This is helpful for creating a

base to assume potential impacts of enterprise environment within firm (Jones, 2014). Seymour

civil engineering company can utilise scenario planning tools for finding and analysing possible

happenings which can effects the segments of enterprise in upcoming years.

Advantage:

This planning tools is also known as a flexible tool as it can perform as per the stimulated

scenarios.

Disadvantage:

Seymour civil engineering company can not use this tools practically as it is time taking.

M3. Analyse the utilisation of different planning tools and their application preparing and

forecasting budgets

After examining different types of planning tools that are utilise for budgetary control

such scenario, forecasting and contingency tools. This is clear that it assists the Seymour civil

9

opportunities which can impact the decisions of the business organization.

Disadvantage:

As it is hard to assume upcoming happenings so with the assistance of this tool Seymour

civil engineering company are not able to made effective approximation.

Contingency planning tools: It is the tools that are useful in valuing and apportioning

risky factor that can affects the organisational operations, growth, activities, performance and so

on in upcoming years (Kraus and Strömsten, 2012). Seymour civil engineering company apply

this tools for examining as well as measuring financial positions related to net and gross

profitability performance and conditions of many activities of firm. Also, selected organisation

have to analyse these factors also formulate strategic strategies for resolving them as early as

possible.

Advantage:

It aids Seymour civil engineering company to find out effective resources in case some

trouble created at the time of operations related to already recognise or recent resources.

Disadvantage:

This tools are too time consuming as well as costly.

Scenario Planning tools: It is the tools that developed a structured and managed manner

for improving structures for strategical planning of organisation. This is helpful for creating a

base to assume potential impacts of enterprise environment within firm (Jones, 2014). Seymour

civil engineering company can utilise scenario planning tools for finding and analysing possible

happenings which can effects the segments of enterprise in upcoming years.

Advantage:

This planning tools is also known as a flexible tool as it can perform as per the stimulated

scenarios.

Disadvantage:

Seymour civil engineering company can not use this tools practically as it is time taking.

M3. Analyse the utilisation of different planning tools and their application preparing and

forecasting budgets

After examining different types of planning tools that are utilise for budgetary control

such scenario, forecasting and contingency tools. This is clear that it assists the Seymour civil

9

engineering company management for maintaining the process that is linked to budgeted

planning and formulation. These planning tools provides Seymour civil engineering company a

framework so that they can formulate blue print for managing whole functions that are useful to

ascertain organisational performance as well as growth. Management of respective firm can also

apply these tools for identifying possible threats and opportunities. For the effectualness of

planning process budgetary control plays a significant role.

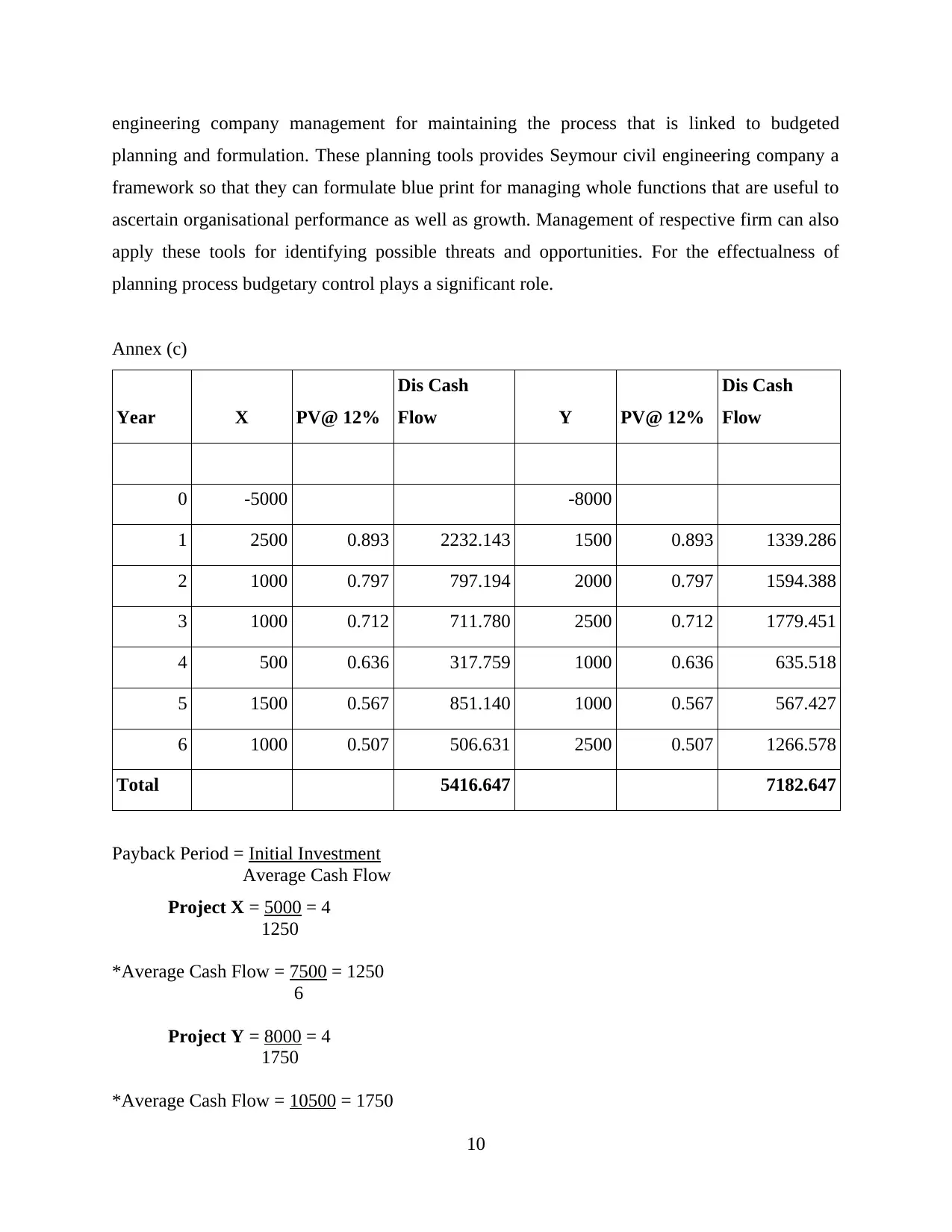

Annex (c)

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.780 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.140 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 5416.647 7182.647

Payback Period = Initial Investment

Average Cash Flow

Project X = 5000 = 4

1250

*Average Cash Flow = 7500 = 1250

6

Project Y = 8000 = 4

1750

*Average Cash Flow = 10500 = 1750

10

planning and formulation. These planning tools provides Seymour civil engineering company a

framework so that they can formulate blue print for managing whole functions that are useful to

ascertain organisational performance as well as growth. Management of respective firm can also

apply these tools for identifying possible threats and opportunities. For the effectualness of

planning process budgetary control plays a significant role.

Annex (c)

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.780 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.140 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 5416.647 7182.647

Payback Period = Initial Investment

Average Cash Flow

Project X = 5000 = 4

1250

*Average Cash Flow = 7500 = 1250

6

Project Y = 8000 = 4

1750

*Average Cash Flow = 10500 = 1750

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.