Network Critical Solution Ltd: Management Accounting Report Analysis

VerifiedAdded on 2020/12/10

|17

|5711

|218

Report

AI Summary

This report provides a detailed analysis of management accounting principles and practices, focusing on their application within an organizational context. The report begins by defining management accounting and its importance, followed by an examination of diverse management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. It then explores various management accounting reporting methods, such as budget reports, accounts receivable reports, and job cost reports, highlighting their significance in decision-making and cost minimization. The report delves into specific cost techniques, such as marginal and absorption costing, demonstrating their use in preparing income statements. Furthermore, it discusses planning tools used in budgetary control, evaluating their advantages and disadvantages, and explores how organizations use management accounting to address financial issues. The report uses Network Critical Solution Ltd. as a case study and concludes by summarizing the key findings and implications of management accounting in achieving sustainable success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Managerial accounting and management accounting system................................................1

P2 Diverse methods to management accounting reporting.........................................................3

M1 Benefits of management accounting systems and their application with in organisation....5

D1 Integration between management accounting system and management accounting

reporting......................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Preparation of income statements by using cost techniques..................................................5

M2 Application of management accounting techniques to produce financial reporting

documents...................................................................................................................................8

D2 Financial resorts and interpretation of data of business activities.........................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of type of planning tools used in budgetary control............8

M3 The use of different planning tools and their application for preparing and forecasting

budgets......................................................................................................................................10

D3 Evaluating planning tools for accounting to solve the financial problems to lead

organisation...............................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Compare ways in which organisation use management accounting to respond financial

issues.........................................................................................................................................10

M4 Responding financial problems management accounting to lead towards sustainable

success.......................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Managerial accounting and management accounting system................................................1

P2 Diverse methods to management accounting reporting.........................................................3

M1 Benefits of management accounting systems and their application with in organisation....5

D1 Integration between management accounting system and management accounting

reporting......................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Preparation of income statements by using cost techniques..................................................5

M2 Application of management accounting techniques to produce financial reporting

documents...................................................................................................................................8

D2 Financial resorts and interpretation of data of business activities.........................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of type of planning tools used in budgetary control............8

M3 The use of different planning tools and their application for preparing and forecasting

budgets......................................................................................................................................10

D3 Evaluating planning tools for accounting to solve the financial problems to lead

organisation...............................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Compare ways in which organisation use management accounting to respond financial

issues.........................................................................................................................................10

M4 Responding financial problems management accounting to lead towards sustainable

success.......................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a systematic framework that provides structure of sustaining

financial or non-financial information in well organised manner. Scope and importance of

management accounting is increasing dramatically in small, medium and large business

enterprises. Meaning of management accounting and diverse management accounting system

explained in organisational context. Role of management accounting reports to assist decision

making and interrelation between management accounting system and management accounting

reporting is defined in this context. Profit and loss evaluation by implementing costing

techniques as marginal and absorption done with practical evaluation.

Network Critical Solution Ltd is chosen organisational to assist the project. Various type

of planning tools used in budgetary control process with advantages and disadvantages are

defined in this report. Adaptation and implementation of management accounting system in

organisation to absorb financial challenges and the crisis and comparison subject to organisations

are also defined in this assignment.

TASK 1

P1 Managerial accounting and management accounting system

In every business organisation, it has been analysing that management accounting is one

of the essential part of the company. Organisations need to make use of each techniques

effectively in order to record every accounting transaction more accurately within the set time

period. It is the primary aim of financial manager or accountant to all search for best method or

opportunity that can help to the control their work in proper manner. It is said to be regulated and

established through entrepreneur as they are not standardized process. The manager uses future

data and information not only historical cost for estimating future planning. The total frequency

of preparing financial statements is defined by the company only (Albelda, 2011).

Definition: Management accounting is one of the effective process of formulating

administrative reports and account that is liable to deliver accurate and timely statistical data as

required by the manager. This will assist them to make future decision, whether related with the

short and long term period. This particular report indicates typical amount of available cash,

sales earning and amount of order present in hand within internal level of the department analyse

accordingly (Schaltegger, Zvezdov, 2011).

1

Management accounting is a systematic framework that provides structure of sustaining

financial or non-financial information in well organised manner. Scope and importance of

management accounting is increasing dramatically in small, medium and large business

enterprises. Meaning of management accounting and diverse management accounting system

explained in organisational context. Role of management accounting reports to assist decision

making and interrelation between management accounting system and management accounting

reporting is defined in this context. Profit and loss evaluation by implementing costing

techniques as marginal and absorption done with practical evaluation.

Network Critical Solution Ltd is chosen organisational to assist the project. Various type

of planning tools used in budgetary control process with advantages and disadvantages are

defined in this report. Adaptation and implementation of management accounting system in

organisation to absorb financial challenges and the crisis and comparison subject to organisations

are also defined in this assignment.

TASK 1

P1 Managerial accounting and management accounting system

In every business organisation, it has been analysing that management accounting is one

of the essential part of the company. Organisations need to make use of each techniques

effectively in order to record every accounting transaction more accurately within the set time

period. It is the primary aim of financial manager or accountant to all search for best method or

opportunity that can help to the control their work in proper manner. It is said to be regulated and

established through entrepreneur as they are not standardized process. The manager uses future

data and information not only historical cost for estimating future planning. The total frequency

of preparing financial statements is defined by the company only (Albelda, 2011).

Definition: Management accounting is one of the effective process of formulating

administrative reports and account that is liable to deliver accurate and timely statistical data as

required by the manager. This will assist them to make future decision, whether related with the

short and long term period. This particular report indicates typical amount of available cash,

sales earning and amount of order present in hand within internal level of the department analyse

accordingly (Schaltegger, Zvezdov, 2011).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Important of management accounting

Preparation of plan: It has been seen that the current age is said to be planning phase.

For every company, it is essential to make use of every accounting information

effectively so that growth chances can be enhanced. Before taking any plan the manager

used to study and analyse the present and upcoming impacts on the business.

Easy to make decision: It is essential for the manager to make effective decision on the

basis of all the financial information that is being collected within an organisation. The

management can have decided which plan or rules is positive from the given alternative

to them (Christ, Burritt, 2013).

Types of management accounting system

Cost accounting system

It is said to be the branch of accounting data system which would record, measure and

report data regarding all the cost that Tech (UK) is being investing the production process. The

main purpose of using this system is to ascertain cost and their use in decision making for the

purpose of evaluating performance of the company. There are various types of cost that Tech

(UK) would incurred during production process. Such as: Actual costing: It is the recording of information about the product costs that are based

on various factors such as actual cost of labour and material. It is used to compile the

actual cost incurred to produce one units of products. Standard costing: It is the practise of deducting an expected cost associated with actual

cost in the accounting records and variances. It is basically comparison among the

expected and actual costing.

Normal costing: It is used to evaluate production of products with the actual labour and

material costs. This method applies actual direct cost to any products as well as standard

overhead rates (Contrafatto, Burns, 2013).

Inventory management system

This accounting system mainly helps in managing the departments and deriving the

inventory management. Large manufacturing and production organisations needs to manage the

flow of inventories and operating the production process smoothly and effectively. There is

specific procedure is followed subject to organise goods and raw material. Various categories

and sections subject to stocks and inventories are considered in this accounting system. It helps

2

Preparation of plan: It has been seen that the current age is said to be planning phase.

For every company, it is essential to make use of every accounting information

effectively so that growth chances can be enhanced. Before taking any plan the manager

used to study and analyse the present and upcoming impacts on the business.

Easy to make decision: It is essential for the manager to make effective decision on the

basis of all the financial information that is being collected within an organisation. The

management can have decided which plan or rules is positive from the given alternative

to them (Christ, Burritt, 2013).

Types of management accounting system

Cost accounting system

It is said to be the branch of accounting data system which would record, measure and

report data regarding all the cost that Tech (UK) is being investing the production process. The

main purpose of using this system is to ascertain cost and their use in decision making for the

purpose of evaluating performance of the company. There are various types of cost that Tech

(UK) would incurred during production process. Such as: Actual costing: It is the recording of information about the product costs that are based

on various factors such as actual cost of labour and material. It is used to compile the

actual cost incurred to produce one units of products. Standard costing: It is the practise of deducting an expected cost associated with actual

cost in the accounting records and variances. It is basically comparison among the

expected and actual costing.

Normal costing: It is used to evaluate production of products with the actual labour and

material costs. This method applies actual direct cost to any products as well as standard

overhead rates (Contrafatto, Burns, 2013).

Inventory management system

This accounting system mainly helps in managing the departments and deriving the

inventory management. Large manufacturing and production organisations needs to manage the

flow of inventories and operating the production process smoothly and effectively. There is

specific procedure is followed subject to organise goods and raw material. Various categories

and sections subject to stocks and inventories are considered in this accounting system. It helps

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to catalysis the small units of inventories as per nature, size and use in production system. EOQ,

ABC system are some common evaluation system which helps in managing the order quantity of

stock with in the organisation.

Job costing system

Job costing is a process of accumulating and gathering the information about the cost

related to specific production process, service and job. This accounting system mainly helps in

managing the cost of different of organisation form different cost centres and section. The

organisations which operates multiple job centres and sections use job costing system. This is

one of the important tool not only bifurcate the cost of each department and section but also

evaluate the profitability at each section. Allocation of cost as direct material, direct expenses

and direct expenses one properly in this accounting system. It is beneficial in terms of

determining the cost of construction and time base contact accounts and cost. The price mainly

derive and cumulate the information more systematic and effective manner (Figge, Hahn, 2013).

Price optimising system

This is the process of determining the prices of products and services by analysing the

customer and client perspective. Maximising the profitability and decreasing the cost of products

and services considered in this accounting system. Fluctuation of price mainly depends upon

demand and requirement of products and services of business. Price of products and services are

raised by seller in proportionate the demand and vice or versa.

P2 Diverse methods to management accounting reporting

In every business organisation, it has been seen that manager always used to record every

data related to finance or non-financial into their respective formats. It is the primary role of

accountant is to be make proper analysis of each and every statement that can lead to analyse

total earning they are getting from overall investments made by various investors or

stakeholders. Reporting is said to be the systematic recording of all data into summaries manner

so that overall cost can easily be determine. There are various sources from which data can be

collected. Some of them are taken from internal as well as external sources. They need to make

use of each information effectively in order to earn healthy return in near future time. in order to

analyse various issues, manager need to make planning for future. As, they need to keep

continuous analysis about the availability of funds to an organisation (Granlund, 2011). There

3

ABC system are some common evaluation system which helps in managing the order quantity of

stock with in the organisation.

Job costing system

Job costing is a process of accumulating and gathering the information about the cost

related to specific production process, service and job. This accounting system mainly helps in

managing the cost of different of organisation form different cost centres and section. The

organisations which operates multiple job centres and sections use job costing system. This is

one of the important tool not only bifurcate the cost of each department and section but also

evaluate the profitability at each section. Allocation of cost as direct material, direct expenses

and direct expenses one properly in this accounting system. It is beneficial in terms of

determining the cost of construction and time base contact accounts and cost. The price mainly

derive and cumulate the information more systematic and effective manner (Figge, Hahn, 2013).

Price optimising system

This is the process of determining the prices of products and services by analysing the

customer and client perspective. Maximising the profitability and decreasing the cost of products

and services considered in this accounting system. Fluctuation of price mainly depends upon

demand and requirement of products and services of business. Price of products and services are

raised by seller in proportionate the demand and vice or versa.

P2 Diverse methods to management accounting reporting

In every business organisation, it has been seen that manager always used to record every

data related to finance or non-financial into their respective formats. It is the primary role of

accountant is to be make proper analysis of each and every statement that can lead to analyse

total earning they are getting from overall investments made by various investors or

stakeholders. Reporting is said to be the systematic recording of all data into summaries manner

so that overall cost can easily be determine. There are various sources from which data can be

collected. Some of them are taken from internal as well as external sources. They need to make

use of each information effectively in order to earn healthy return in near future time. in order to

analyse various issues, manager need to make planning for future. As, they need to keep

continuous analysis about the availability of funds to an organisation (Granlund, 2011). There

3

are various types of reports which is need to be prepared by the account manager. Some of them

are mentioned underneath:

Budget report: This is the report which is prepared to analyse the performance of various

departments and minimises the cost that will be incurred in future project activities. It is prepared

after estimating the future expenses while considering previous year project cost. This will help

in executing future business activities in more desired way with an optimum utilisation of

resources and minimises cost. It will also more helpful in allocation of duties and cost to

different departments after estimating their future needs and requirements (Henri, Boiral and

Roy, 2016).

Accounts receivable report: Such type of reporting is prepared with an objective of

recovering amount of the debtors whose payments are still pending. This will help management

in formulation of an effective plans to collect unpaid amount with an agreed interest rate. It also

directs the management to re-think about their credit policies so as to prevent company from any

bad-debts. Preparation of such report makes alert to the company not to allow credit to person

who is facing financial crisis so that the company's funds are protected.

Job cost report: This is the report which contains the information regarding the expenses

that will be incurred in producing individual products or group of products so that the production

process will be not disturbed. The management need to first identify which products will bring

profitable result to company and on the basis of which allocate funds to the production process.

Inventory management report: Such reports contains the information about the

availability of inventory that the company have at present in their warehouses. The management

should required to make decisions regarding placing an inventory from their suppliers if any

shortage are found that cannot be meet the market needs. Preparing of such report help company

in reducing storage cost due to ordering inventory whenever they feel shortage while producing

demanded products.

Importance of managerial accounting reports:

Decision making: Having sufficient information about availability of funds and

inventory at present enable management to make an effective budget and suitable plans in order

to execute business activities in desired manner without any interruptions (Herzig, 2012).

Minimises cost: Estimating cost that will be incurred in future project activities help

management in making an effective plans in advance so that all the hurdles are properly

4

are mentioned underneath:

Budget report: This is the report which is prepared to analyse the performance of various

departments and minimises the cost that will be incurred in future project activities. It is prepared

after estimating the future expenses while considering previous year project cost. This will help

in executing future business activities in more desired way with an optimum utilisation of

resources and minimises cost. It will also more helpful in allocation of duties and cost to

different departments after estimating their future needs and requirements (Henri, Boiral and

Roy, 2016).

Accounts receivable report: Such type of reporting is prepared with an objective of

recovering amount of the debtors whose payments are still pending. This will help management

in formulation of an effective plans to collect unpaid amount with an agreed interest rate. It also

directs the management to re-think about their credit policies so as to prevent company from any

bad-debts. Preparation of such report makes alert to the company not to allow credit to person

who is facing financial crisis so that the company's funds are protected.

Job cost report: This is the report which contains the information regarding the expenses

that will be incurred in producing individual products or group of products so that the production

process will be not disturbed. The management need to first identify which products will bring

profitable result to company and on the basis of which allocate funds to the production process.

Inventory management report: Such reports contains the information about the

availability of inventory that the company have at present in their warehouses. The management

should required to make decisions regarding placing an inventory from their suppliers if any

shortage are found that cannot be meet the market needs. Preparing of such report help company

in reducing storage cost due to ordering inventory whenever they feel shortage while producing

demanded products.

Importance of managerial accounting reports:

Decision making: Having sufficient information about availability of funds and

inventory at present enable management to make an effective budget and suitable plans in order

to execute business activities in desired manner without any interruptions (Herzig, 2012).

Minimises cost: Estimating cost that will be incurred in future project activities help

management in making an effective plans in advance so that all the hurdles are properly

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

eliminated which can increased cost. It can be done through having sufficient information which

can be obtained through management accounting reports.

Increase financial returns: Allocating funds to different departments after analysing

their needs and requirements help company in receiving profitable outcomes in near future. For

example, funds provided to provide training to their employees help in getting maximum support

from by them in achieving desired goals and objectives.

M1 Benefits of management accounting systems and their application with in organisation

There are type of management accounting systems are used subject to effective execution

and smooth formation of functions. Benefits of different accounting systems are as follows;

Price optimisation system: This accounting system helps in deciding the price of

products and services by analysing the customer's perspective (Hilton, Platt, 2013).

Inventory management system: Main advantage of this management accounting system

is to provide information about the inventories stock.

Management information system: This accounting system mainly helps to consolidate

and summarise the complex transaction equations in a single format

Job costing system: By implementing this accounting system managers be able to

determine accurate profitability form individual operations, employees performance and

benchmarks are setted by individual reports.

D1 Integration between management accounting system and management accounting reporting

There is a cross relation found in management accounting system and management

accounting reporting to assist the management reporting and analysing the performance of

business. The information and data which are gathered from management accounting system are

gathered subject to make a summarised report to evaluate and assist the functions of business. A

perfect and well organised managements accounting report assist in effective decision making

and strategic planning process (Jacobs, Cuganesan, 2014).

TASK 2

P3 Preparation of income statements by using cost techniques

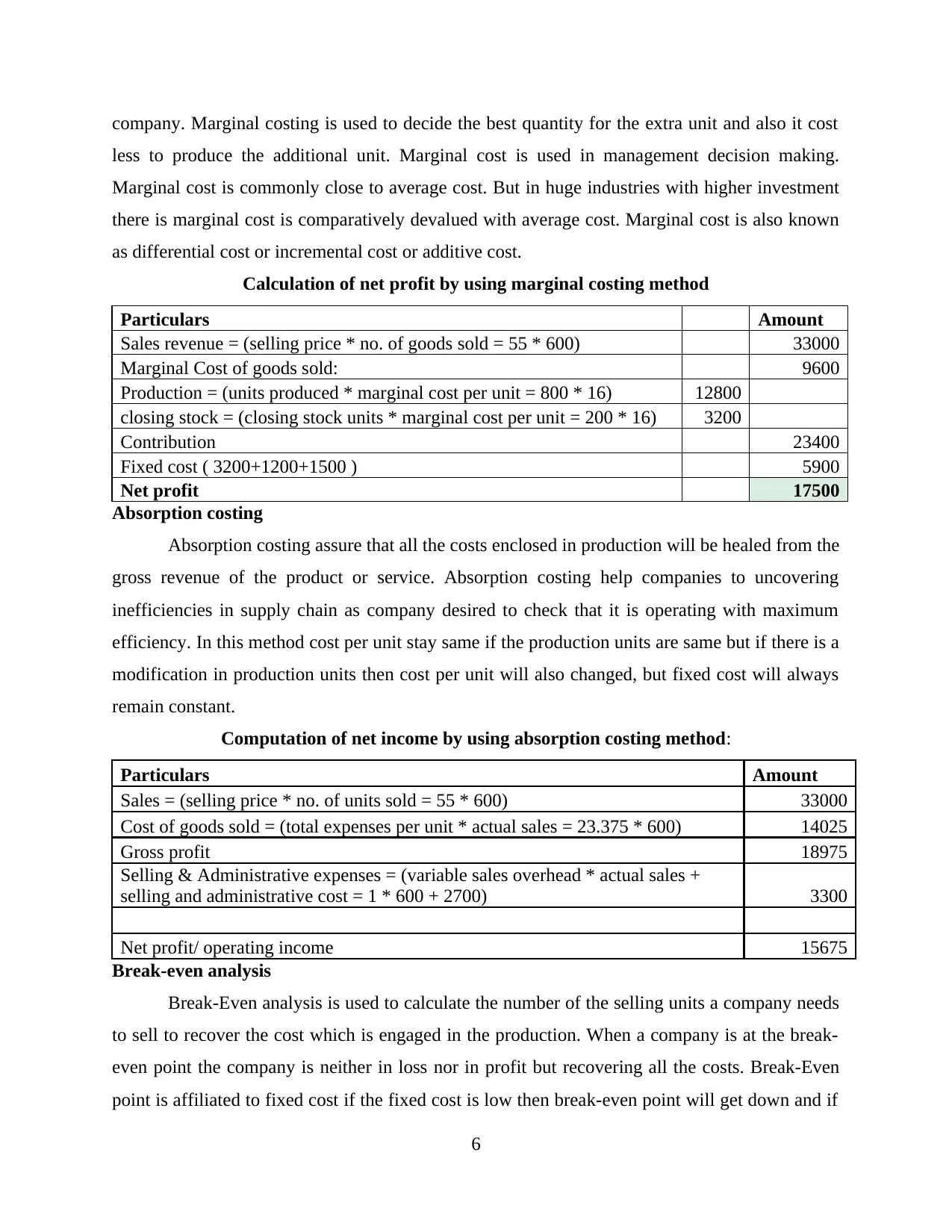

Marginal costing

In marginal costing costs are separated into two parts variable cost and fixed cost.

Marginal cost is the additive cost of the extra unit which is going to be produced by the

5

can be obtained through management accounting reports.

Increase financial returns: Allocating funds to different departments after analysing

their needs and requirements help company in receiving profitable outcomes in near future. For

example, funds provided to provide training to their employees help in getting maximum support

from by them in achieving desired goals and objectives.

M1 Benefits of management accounting systems and their application with in organisation

There are type of management accounting systems are used subject to effective execution

and smooth formation of functions. Benefits of different accounting systems are as follows;

Price optimisation system: This accounting system helps in deciding the price of

products and services by analysing the customer's perspective (Hilton, Platt, 2013).

Inventory management system: Main advantage of this management accounting system

is to provide information about the inventories stock.

Management information system: This accounting system mainly helps to consolidate

and summarise the complex transaction equations in a single format

Job costing system: By implementing this accounting system managers be able to

determine accurate profitability form individual operations, employees performance and

benchmarks are setted by individual reports.

D1 Integration between management accounting system and management accounting reporting

There is a cross relation found in management accounting system and management

accounting reporting to assist the management reporting and analysing the performance of

business. The information and data which are gathered from management accounting system are

gathered subject to make a summarised report to evaluate and assist the functions of business. A

perfect and well organised managements accounting report assist in effective decision making

and strategic planning process (Jacobs, Cuganesan, 2014).

TASK 2

P3 Preparation of income statements by using cost techniques

Marginal costing

In marginal costing costs are separated into two parts variable cost and fixed cost.

Marginal cost is the additive cost of the extra unit which is going to be produced by the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company. Marginal costing is used to decide the best quantity for the extra unit and also it cost

less to produce the additional unit. Marginal cost is used in management decision making.

Marginal cost is commonly close to average cost. But in huge industries with higher investment

there is marginal cost is comparatively devalued with average cost. Marginal cost is also known

as differential cost or incremental cost or additive cost.

Calculation of net profit by using marginal costing method

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 * 16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing

Absorption costing assure that all the costs enclosed in production will be healed from the

gross revenue of the product or service. Absorption costing help companies to uncovering

inefficiencies in supply chain as company desired to check that it is operating with maximum

efficiency. In this method cost per unit stay same if the production units are same but if there is a

modification in production units then cost per unit will also changed, but fixed cost will always

remain constant.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-even analysis

Break-Even analysis is used to calculate the number of the selling units a company needs

to sell to recover the cost which is engaged in the production. When a company is at the break-

even point the company is neither in loss nor in profit but recovering all the costs. Break-Even

point is affiliated to fixed cost if the fixed cost is low then break-even point will get down and if

6

less to produce the additional unit. Marginal cost is used in management decision making.

Marginal cost is commonly close to average cost. But in huge industries with higher investment

there is marginal cost is comparatively devalued with average cost. Marginal cost is also known

as differential cost or incremental cost or additive cost.

Calculation of net profit by using marginal costing method

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 * 16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing

Absorption costing assure that all the costs enclosed in production will be healed from the

gross revenue of the product or service. Absorption costing help companies to uncovering

inefficiencies in supply chain as company desired to check that it is operating with maximum

efficiency. In this method cost per unit stay same if the production units are same but if there is a

modification in production units then cost per unit will also changed, but fixed cost will always

remain constant.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-even analysis

Break-Even analysis is used to calculate the number of the selling units a company needs

to sell to recover the cost which is engaged in the production. When a company is at the break-

even point the company is neither in loss nor in profit but recovering all the costs. Break-Even

point is affiliated to fixed cost if the fixed cost is low then break-even point will get down and if

6

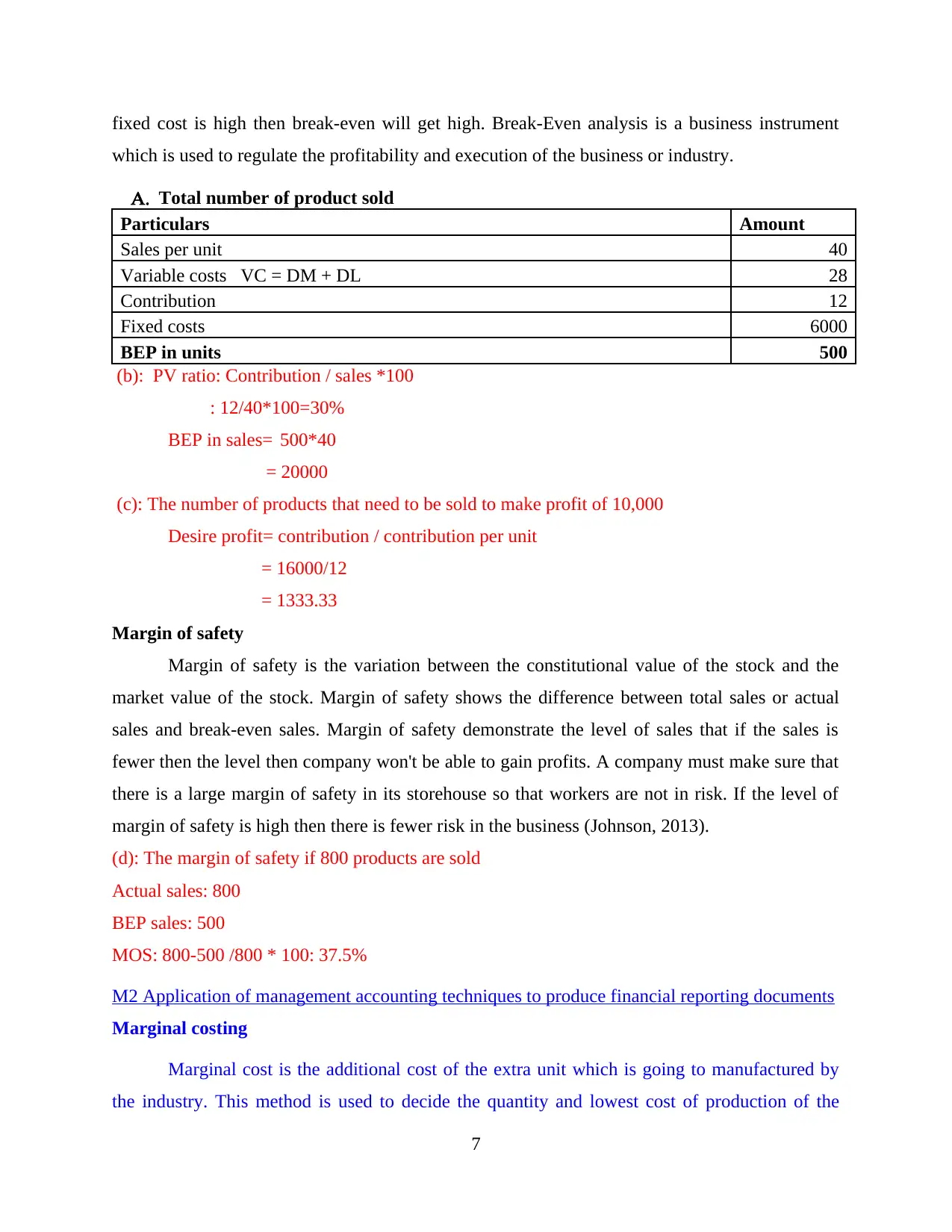

fixed cost is high then break-even will get high. Break-Even analysis is a business instrument

which is used to regulate the profitability and execution of the business or industry.

A. Total number of product sold

Particulars Amount

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

(b): PV ratio: Contribution / sales *100

: 12/40*100=30%

BEP in sales= 500*40

= 20000

(c): The number of products that need to be sold to make profit of 10,000

Desire profit= contribution / contribution per unit

= 16000/12

= 1333.33

Margin of safety

Margin of safety is the variation between the constitutional value of the stock and the

market value of the stock. Margin of safety shows the difference between total sales or actual

sales and break-even sales. Margin of safety demonstrate the level of sales that if the sales is

fewer then the level then company won't be able to gain profits. A company must make sure that

there is a large margin of safety in its storehouse so that workers are not in risk. If the level of

margin of safety is high then there is fewer risk in the business (Johnson, 2013).

(d): The margin of safety if 800 products are sold

Actual sales: 800

BEP sales: 500

MOS: 800-500 /800 * 100: 37.5%

M2 Application of management accounting techniques to produce financial reporting documents

Marginal costing

Marginal cost is the additional cost of the extra unit which is going to manufactured by

the industry. This method is used to decide the quantity and lowest cost of production of the

7

which is used to regulate the profitability and execution of the business or industry.

A. Total number of product sold

Particulars Amount

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

(b): PV ratio: Contribution / sales *100

: 12/40*100=30%

BEP in sales= 500*40

= 20000

(c): The number of products that need to be sold to make profit of 10,000

Desire profit= contribution / contribution per unit

= 16000/12

= 1333.33

Margin of safety

Margin of safety is the variation between the constitutional value of the stock and the

market value of the stock. Margin of safety shows the difference between total sales or actual

sales and break-even sales. Margin of safety demonstrate the level of sales that if the sales is

fewer then the level then company won't be able to gain profits. A company must make sure that

there is a large margin of safety in its storehouse so that workers are not in risk. If the level of

margin of safety is high then there is fewer risk in the business (Johnson, 2013).

(d): The margin of safety if 800 products are sold

Actual sales: 800

BEP sales: 500

MOS: 800-500 /800 * 100: 37.5%

M2 Application of management accounting techniques to produce financial reporting documents

Marginal costing

Marginal cost is the additional cost of the extra unit which is going to manufactured by

the industry. This method is used to decide the quantity and lowest cost of production of the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

additional unit for future production. It always help managers to pass precise judgement for

upcoming period of time. This type of management technique is used to prepare costing sheets

which includes documents such as variable cash flow.

Standard costing

Standard cost is the expenses which are allocated by management of the organisation to

their manufactured products and services. This type of costing helps to predict future demand

and supply for their products. Management reports which can be prepared by using this

technique of management is budgets such as cash budget, production budget etc.

Preparing an income statements reporting documents: It is started by recording gross

sales revenue for the accounting period. All the necessary deductions for sale return and

discounts allowances are then subtracted from the overall gross sales to get total net sales. After

that deduction related with the expenses are done to get overall net profit.

Balance sheet report: This particular statements of financial position report documents

are corporation assets, liabilities and stockholders’ equity as the final instant of the data provided

in their respective headings.

D2 Financial resorts and interpretation of data of business activities

Marginal profit for the company is 15675 and absorption profit for the company is 17500.

Company has to sale 500 units to reach at the level of BEP and the sales revenue to recover the

cost are 20000 the company has to earn 20000 to heal the cost. If company is willing to earn a

profit of 10000 then company have to sale 1333.33 units.

TASK 3

P4 Advantages and disadvantages of type of planning tools used in budgetary control

Budgetary control is a management control system which assist to compare actual income

and expenditure with budgeted income and expenditure. It is used to control the cost, prepare the

budget, coordination among departments and performing upon the outcome to maximize profits.

It is the planning to control whole business. It is defined as how well managers can utilize the

allotted budget for all the tasks (RKlychova, Faskhutdinova, Sadrieva, 2014).

Cash budget: It is known as one of the effective cash receipts and disbursements done by

the company during the period of time. By the help of this, proper flow of cash inflows and

8

upcoming period of time. This type of management technique is used to prepare costing sheets

which includes documents such as variable cash flow.

Standard costing

Standard cost is the expenses which are allocated by management of the organisation to

their manufactured products and services. This type of costing helps to predict future demand

and supply for their products. Management reports which can be prepared by using this

technique of management is budgets such as cash budget, production budget etc.

Preparing an income statements reporting documents: It is started by recording gross

sales revenue for the accounting period. All the necessary deductions for sale return and

discounts allowances are then subtracted from the overall gross sales to get total net sales. After

that deduction related with the expenses are done to get overall net profit.

Balance sheet report: This particular statements of financial position report documents

are corporation assets, liabilities and stockholders’ equity as the final instant of the data provided

in their respective headings.

D2 Financial resorts and interpretation of data of business activities

Marginal profit for the company is 15675 and absorption profit for the company is 17500.

Company has to sale 500 units to reach at the level of BEP and the sales revenue to recover the

cost are 20000 the company has to earn 20000 to heal the cost. If company is willing to earn a

profit of 10000 then company have to sale 1333.33 units.

TASK 3

P4 Advantages and disadvantages of type of planning tools used in budgetary control

Budgetary control is a management control system which assist to compare actual income

and expenditure with budgeted income and expenditure. It is used to control the cost, prepare the

budget, coordination among departments and performing upon the outcome to maximize profits.

It is the planning to control whole business. It is defined as how well managers can utilize the

allotted budget for all the tasks (RKlychova, Faskhutdinova, Sadrieva, 2014).

Cash budget: It is known as one of the effective cash receipts and disbursements done by

the company during the period of time. By the help of this, proper flow of cash inflows and

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

outflows for a business over a particular period of time. This budget is basically used to assess,

whether the entity is having sufficient cash to operate.

Advantages: This particular tools assist, whether cash balances could remain sufficient to

fulfil regular obligation and minimise liquidity as well as cash balances needs.

Disadvantages: Cash inflows cannot equate to profit. It would be resulting from overall

security deposits, fines and sale sof capital assets that are necessarily represent reliable ongoing

sources of earning. Once, the recovery period gets completed the chances of cash balances can

also be not calculated for the period.

Uses: This tools can assist in avoiding a shortage of cash at the time which a company

encounters a high number of expenses.

Forecasting tool

Forecasting tools analyses financial condition of a company, current position of the

company and how a company is going to result in future. It is based on assumptions not on real

data. This tool form early predictions accordant to the current and foregone data.

Advantages: Forecasting tools provide relevant information that can help to take

upcoming decisions and predict the future condition of organisation. This tool is useful in

determining the future conditions of the business.

Disadvantages: Not possible to forecast the actual or accurate information it is totally

based on anticipated data.

A decision which is taken on mistaken forecasted report can harm the company.

Contingency tool

Contingency tool integrates definite risk factors into the budgeting process to help a

business to be ready for possible contingencies. This tool is used to achieve executive goals of

the industry.

Advantages: Contingency tools help to bring down risk of uncertainties, used to form

cohesiveness in the work of company. These tools also help to increase credit accessibility for

the business for an extended period (Katas, 2014).

Disadvantages: Contingency tools are unstable not retroactive. If there is no risk

happened in future, then the money and time invested in this whole process will be wasted.

Scenario tool

9

whether the entity is having sufficient cash to operate.

Advantages: This particular tools assist, whether cash balances could remain sufficient to

fulfil regular obligation and minimise liquidity as well as cash balances needs.

Disadvantages: Cash inflows cannot equate to profit. It would be resulting from overall

security deposits, fines and sale sof capital assets that are necessarily represent reliable ongoing

sources of earning. Once, the recovery period gets completed the chances of cash balances can

also be not calculated for the period.

Uses: This tools can assist in avoiding a shortage of cash at the time which a company

encounters a high number of expenses.

Forecasting tool

Forecasting tools analyses financial condition of a company, current position of the

company and how a company is going to result in future. It is based on assumptions not on real

data. This tool form early predictions accordant to the current and foregone data.

Advantages: Forecasting tools provide relevant information that can help to take

upcoming decisions and predict the future condition of organisation. This tool is useful in

determining the future conditions of the business.

Disadvantages: Not possible to forecast the actual or accurate information it is totally

based on anticipated data.

A decision which is taken on mistaken forecasted report can harm the company.

Contingency tool

Contingency tool integrates definite risk factors into the budgeting process to help a

business to be ready for possible contingencies. This tool is used to achieve executive goals of

the industry.

Advantages: Contingency tools help to bring down risk of uncertainties, used to form

cohesiveness in the work of company. These tools also help to increase credit accessibility for

the business for an extended period (Katas, 2014).

Disadvantages: Contingency tools are unstable not retroactive. If there is no risk

happened in future, then the money and time invested in this whole process will be wasted.

Scenario tool

9

Scenario tools are used to assist management to take appropriate decisions. This tool is

very helpful for the managers to pass judgement of alternative views of what may occur in

business in future day. Scenario tools are used to analyse that what can occur in future, what will

be the outcome of schemes and ideas on business. It helps the company to deal with the

unpredicted risks. This tool is useful in formulation of future plans so that it would be facilitative

for the company to accomplish predetermined goals.

Advantages: Scenario tools are very important for planning of extended period of time

and helpful in taking decisions for future perspective. Facilitative in identifying the risk factor

that can occur in future. This tool is really crucial for manager to pass precise conclusion.

Disadvantage: This budgetary control tool required high level of skills and execution of

this tool is time consuming. The cost which is involved in use of this tool is very advanced, every

company is not able to bear that advanced cost for any type of analysis (Lambert, Sponem,

2012).

M3 The use of different planning tools and their application for preparing and forecasting

budgets

Planning tools are the techniques which helps in ascertaining variances in order to plan

for future events. Cash budget is a planning tool which applied in the organisations to predict

future cash inflow and outflow for the organisation. Another planning tool which is scenario tool

helps a company such as Network Critical Solution to develop variety of future possible

possibilities (Lee, 2011).

D3 Evaluating planning tools for accounting to solve the financial problems to lead organisation

It has been discovered that Network Critical Solution is confronting different budgetary

issues, for example, quality, compensation and stock cost. To accomplish long terms targets of

affiliation it is required to manage these issues. Association need to utilize few instruments

possibilities devices, situation devices and anticipating tools. Forecasting apparatuses are utilized

by association to fuse unimportant effort and Conflicts of enthusiasm of Network Critical

Solution organization by estimation of future costs and expenses. KPI will help this relationship

by picking all the key regions which can understand advantage which will at last help them in

managing their money related issues.

10

very helpful for the managers to pass judgement of alternative views of what may occur in

business in future day. Scenario tools are used to analyse that what can occur in future, what will

be the outcome of schemes and ideas on business. It helps the company to deal with the

unpredicted risks. This tool is useful in formulation of future plans so that it would be facilitative

for the company to accomplish predetermined goals.

Advantages: Scenario tools are very important for planning of extended period of time

and helpful in taking decisions for future perspective. Facilitative in identifying the risk factor

that can occur in future. This tool is really crucial for manager to pass precise conclusion.

Disadvantage: This budgetary control tool required high level of skills and execution of

this tool is time consuming. The cost which is involved in use of this tool is very advanced, every

company is not able to bear that advanced cost for any type of analysis (Lambert, Sponem,

2012).

M3 The use of different planning tools and their application for preparing and forecasting

budgets

Planning tools are the techniques which helps in ascertaining variances in order to plan

for future events. Cash budget is a planning tool which applied in the organisations to predict

future cash inflow and outflow for the organisation. Another planning tool which is scenario tool

helps a company such as Network Critical Solution to develop variety of future possible

possibilities (Lee, 2011).

D3 Evaluating planning tools for accounting to solve the financial problems to lead organisation

It has been discovered that Network Critical Solution is confronting different budgetary

issues, for example, quality, compensation and stock cost. To accomplish long terms targets of

affiliation it is required to manage these issues. Association need to utilize few instruments

possibilities devices, situation devices and anticipating tools. Forecasting apparatuses are utilized

by association to fuse unimportant effort and Conflicts of enthusiasm of Network Critical

Solution organization by estimation of future costs and expenses. KPI will help this relationship

by picking all the key regions which can understand advantage which will at last help them in

managing their money related issues.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.