Teamwork and Group Project Experience

VerifiedAdded on 2020/05/28

|12

|2880

|99

AI Summary

This assignment delves into the author's experience working within a team to complete a project. It explores instances of conflict resolution, leadership roles within the group, successes achieved, and areas for potential improvement. The reflection emphasizes the importance of patience, trust, and effective communication in fostering successful teamwork.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author Note

Management Accounting

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

MANAGEMENT ACCOUNTING

Table of Contents

Part 1................................................................................................................................................3

Answer to Question 1..................................................................................................................3

Answer to Question 2..................................................................................................................4

Answer to Question 3..................................................................................................................5

Answer to Question 4..................................................................................................................6

Part 2................................................................................................................................................7

Introduction..................................................................................................................................7

Group Description.......................................................................................................................8

My role.........................................................................................................................................8

Others’ roles.................................................................................................................................8

Group Stages................................................................................................................................8

Conflict within the group.............................................................................................................9

Leadership and decision making in the group.............................................................................9

Achievements by the team and scope of improvement...............................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

MANAGEMENT ACCOUNTING

Table of Contents

Part 1................................................................................................................................................3

Answer to Question 1..................................................................................................................3

Answer to Question 2..................................................................................................................4

Answer to Question 3..................................................................................................................5

Answer to Question 4..................................................................................................................6

Part 2................................................................................................................................................7

Introduction..................................................................................................................................7

Group Description.......................................................................................................................8

My role.........................................................................................................................................8

Others’ roles.................................................................................................................................8

Group Stages................................................................................................................................8

Conflict within the group.............................................................................................................9

Leadership and decision making in the group.............................................................................9

Achievements by the team and scope of improvement...............................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

MANAGEMENT ACCOUNTING

Part 1

Answer to Question 1

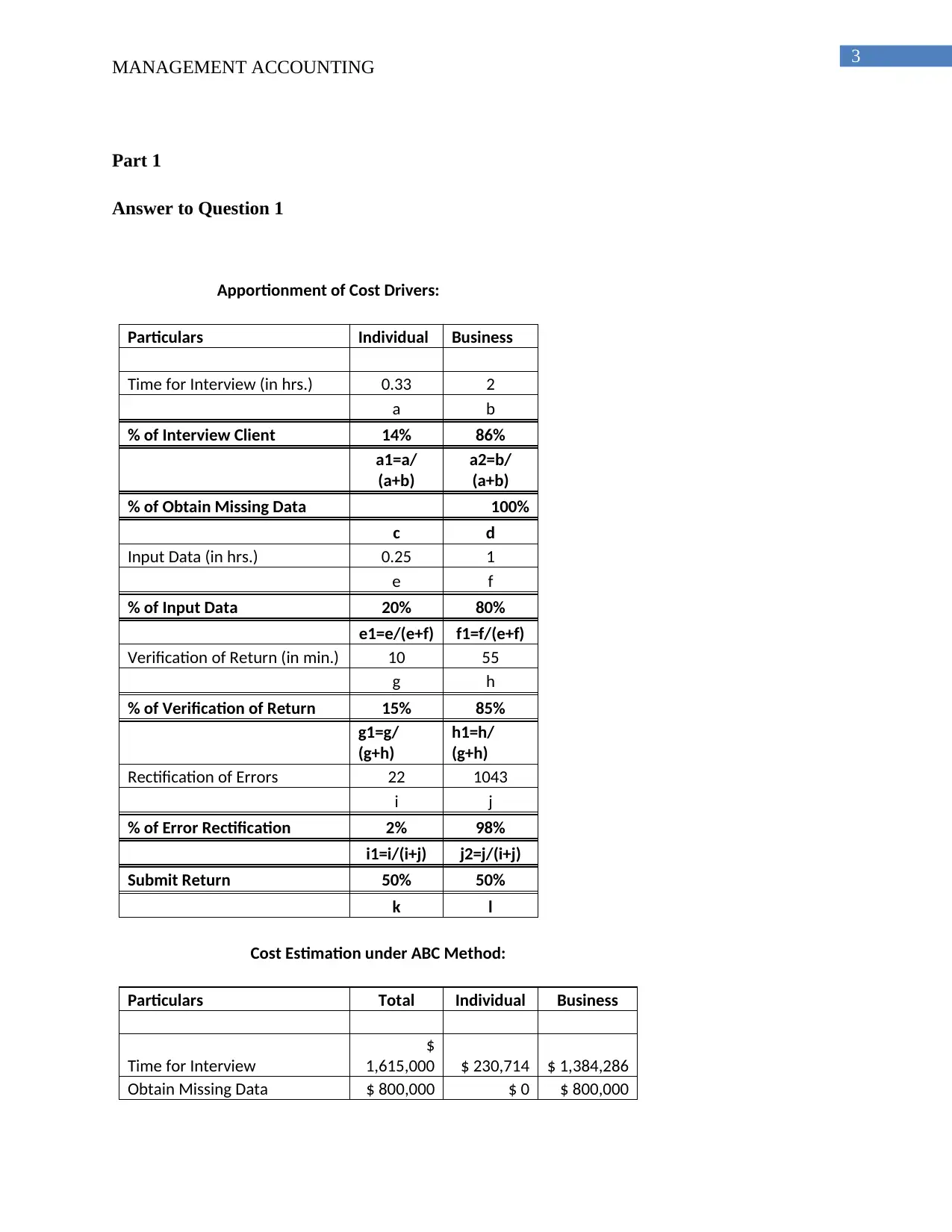

Apportionment of Cost Drivers:

Particulars Individual Business

Time for Interview (in hrs.) 0.33 2

a b

% of Interview Client 14% 86%

a1=a/

(a+b)

a2=b/

(a+b)

% of Obtain Missing Data 100%

c d

Input Data (in hrs.) 0.25 1

e f

% of Input Data 20% 80%

e1=e/(e+f) f1=f/(e+f)

Verification of Return (in min.) 10 55

g h

% of Verification of Return 15% 85%

g1=g/

(g+h)

h1=h/

(g+h)

Rectification of Errors 22 1043

i j

% of Error Rectification 2% 98%

i1=i/(i+j) j2=j/(i+j)

Submit Return 50% 50%

k l

Cost Estimation under ABC Method:

Particulars Total Individual Business

Time for Interview

$

1,615,000 $ 230,714 $ 1,384,286

Obtain Missing Data $ 800,000 $ 0 $ 800,000

MANAGEMENT ACCOUNTING

Part 1

Answer to Question 1

Apportionment of Cost Drivers:

Particulars Individual Business

Time for Interview (in hrs.) 0.33 2

a b

% of Interview Client 14% 86%

a1=a/

(a+b)

a2=b/

(a+b)

% of Obtain Missing Data 100%

c d

Input Data (in hrs.) 0.25 1

e f

% of Input Data 20% 80%

e1=e/(e+f) f1=f/(e+f)

Verification of Return (in min.) 10 55

g h

% of Verification of Return 15% 85%

g1=g/

(g+h)

h1=h/

(g+h)

Rectification of Errors 22 1043

i j

% of Error Rectification 2% 98%

i1=i/(i+j) j2=j/(i+j)

Submit Return 50% 50%

k l

Cost Estimation under ABC Method:

Particulars Total Individual Business

Time for Interview

$

1,615,000 $ 230,714 $ 1,384,286

Obtain Missing Data $ 800,000 $ 0 $ 800,000

4

MANAGEMENT ACCOUNTING

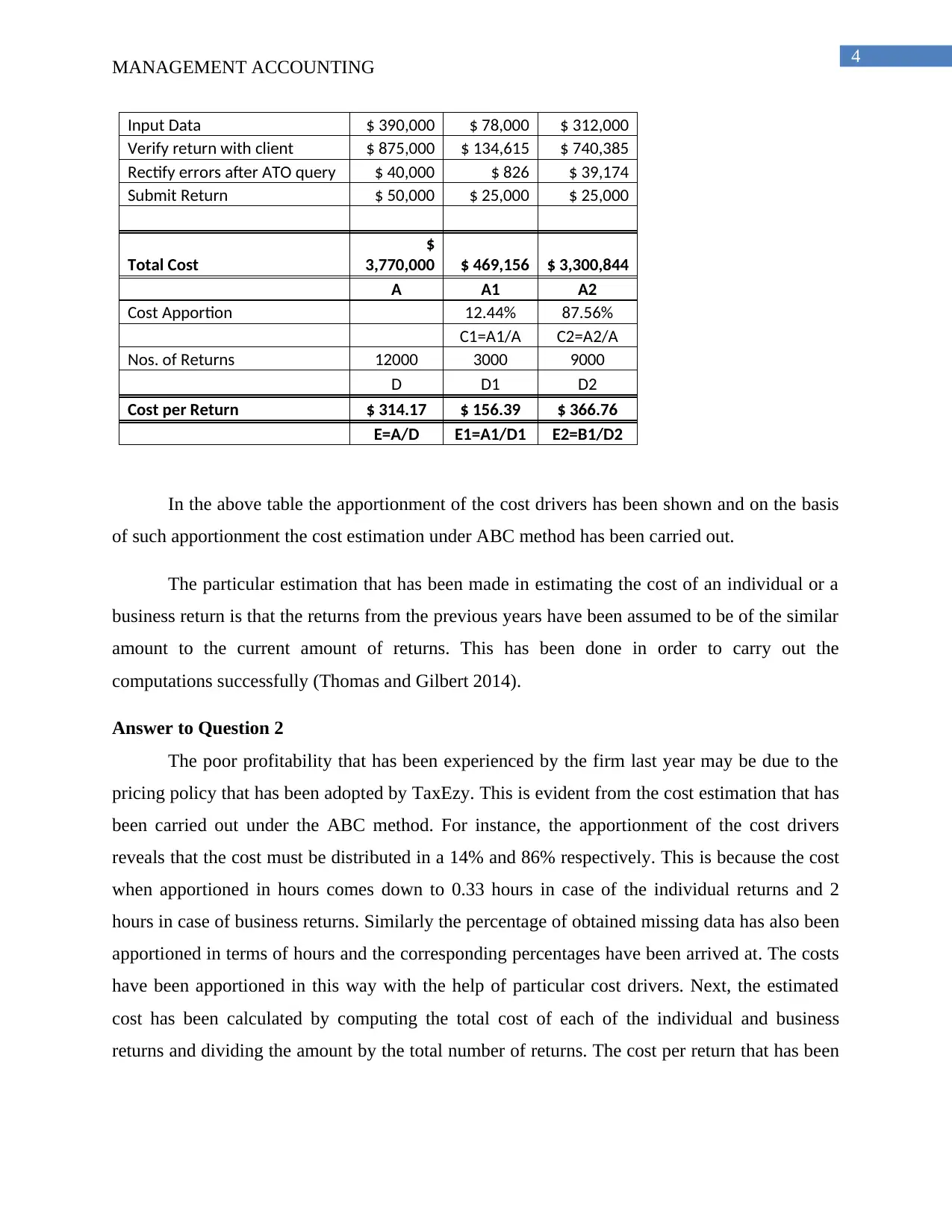

Input Data $ 390,000 $ 78,000 $ 312,000

Verify return with client $ 875,000 $ 134,615 $ 740,385

Rectify errors after ATO query $ 40,000 $ 826 $ 39,174

Submit Return $ 50,000 $ 25,000 $ 25,000

Total Cost

$

3,770,000 $ 469,156 $ 3,300,844

A A1 A2

Cost Apportion 12.44% 87.56%

C1=A1/A C2=A2/A

Nos. of Returns 12000 3000 9000

D D1 D2

Cost per Return $ 314.17 $ 156.39 $ 366.76

E=A/D E1=A1/D1 E2=B1/D2

In the above table the apportionment of the cost drivers has been shown and on the basis

of such apportionment the cost estimation under ABC method has been carried out.

The particular estimation that has been made in estimating the cost of an individual or a

business return is that the returns from the previous years have been assumed to be of the similar

amount to the current amount of returns. This has been done in order to carry out the

computations successfully (Thomas and Gilbert 2014).

Answer to Question 2

The poor profitability that has been experienced by the firm last year may be due to the

pricing policy that has been adopted by TaxEzy. This is evident from the cost estimation that has

been carried out under the ABC method. For instance, the apportionment of the cost drivers

reveals that the cost must be distributed in a 14% and 86% respectively. This is because the cost

when apportioned in hours comes down to 0.33 hours in case of the individual returns and 2

hours in case of business returns. Similarly the percentage of obtained missing data has also been

apportioned in terms of hours and the corresponding percentages have been arrived at. The costs

have been apportioned in this way with the help of particular cost drivers. Next, the estimated

cost has been calculated by computing the total cost of each of the individual and business

returns and dividing the amount by the total number of returns. The cost per return that has been

MANAGEMENT ACCOUNTING

Input Data $ 390,000 $ 78,000 $ 312,000

Verify return with client $ 875,000 $ 134,615 $ 740,385

Rectify errors after ATO query $ 40,000 $ 826 $ 39,174

Submit Return $ 50,000 $ 25,000 $ 25,000

Total Cost

$

3,770,000 $ 469,156 $ 3,300,844

A A1 A2

Cost Apportion 12.44% 87.56%

C1=A1/A C2=A2/A

Nos. of Returns 12000 3000 9000

D D1 D2

Cost per Return $ 314.17 $ 156.39 $ 366.76

E=A/D E1=A1/D1 E2=B1/D2

In the above table the apportionment of the cost drivers has been shown and on the basis

of such apportionment the cost estimation under ABC method has been carried out.

The particular estimation that has been made in estimating the cost of an individual or a

business return is that the returns from the previous years have been assumed to be of the similar

amount to the current amount of returns. This has been done in order to carry out the

computations successfully (Thomas and Gilbert 2014).

Answer to Question 2

The poor profitability that has been experienced by the firm last year may be due to the

pricing policy that has been adopted by TaxEzy. This is evident from the cost estimation that has

been carried out under the ABC method. For instance, the apportionment of the cost drivers

reveals that the cost must be distributed in a 14% and 86% respectively. This is because the cost

when apportioned in hours comes down to 0.33 hours in case of the individual returns and 2

hours in case of business returns. Similarly the percentage of obtained missing data has also been

apportioned in terms of hours and the corresponding percentages have been arrived at. The costs

have been apportioned in this way with the help of particular cost drivers. Next, the estimated

cost has been calculated by computing the total cost of each of the individual and business

returns and dividing the amount by the total number of returns. The cost per return that has been

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

MANAGEMENT ACCOUNTING

arrived at is estimated to be $156.39 per individual return and $366.76 per business return

(Selviaridis and Norrman 2014).

Now, it has been mentioned in the case study that TaxEzy offers an income tax

preparation service for small businesses and individuals at a charge of $399 and $149

respectively. However, the cost estimates that have been carried out show that the mere cost of

an individual return sums up to be $156.39 and that of a business return is $366.76. Thus, this is

the exact point where the business is suffering. This is why a very small profit had been incurred

by business last year in spite of the work volume being higher than ever. Furthermore, such a

finding also concludes that the pricing policy that has been utilized by the firm till now is flawed.

Answer to Question 3

The potential advantages and disadvantages of ABC in relation to TaxEzy can be

deduced as follows (Öker and Adıgüzel 2016):

Advantages:

Attribution of the incurred costs more correctly – the utilization of an ABC based costing

system leads to the attribution of the incurred costs more correctly. In case of TaxEzy it

can be observed how the application of activity based costing breaks down the different

components in terms of the accurate cost drivers which makes the process of

apportioning the costs easier

Budgeting – The utilization of the activity based costing will help the management of the

firm to create clear budgets. This is because the clear segregation of costs on the basis of

transparent cost drivers help the firm to understand and cut back on different costs which

may be included in the future budgets that are prepared by the management of the firm

Easy to understand – As it is mentioned in the case study that the owner manager of the

firm does not want to buy expensive solutions and that the implementation of any new

system must be understandable to the staff and in some instances to the clients even as

the price of the services should be justified to them too, activity based costing is the

potential solution for such requirements. This is because an activity based costing system

is easy to understand both by the staff and the customers.

MANAGEMENT ACCOUNTING

arrived at is estimated to be $156.39 per individual return and $366.76 per business return

(Selviaridis and Norrman 2014).

Now, it has been mentioned in the case study that TaxEzy offers an income tax

preparation service for small businesses and individuals at a charge of $399 and $149

respectively. However, the cost estimates that have been carried out show that the mere cost of

an individual return sums up to be $156.39 and that of a business return is $366.76. Thus, this is

the exact point where the business is suffering. This is why a very small profit had been incurred

by business last year in spite of the work volume being higher than ever. Furthermore, such a

finding also concludes that the pricing policy that has been utilized by the firm till now is flawed.

Answer to Question 3

The potential advantages and disadvantages of ABC in relation to TaxEzy can be

deduced as follows (Öker and Adıgüzel 2016):

Advantages:

Attribution of the incurred costs more correctly – the utilization of an ABC based costing

system leads to the attribution of the incurred costs more correctly. In case of TaxEzy it

can be observed how the application of activity based costing breaks down the different

components in terms of the accurate cost drivers which makes the process of

apportioning the costs easier

Budgeting – The utilization of the activity based costing will help the management of the

firm to create clear budgets. This is because the clear segregation of costs on the basis of

transparent cost drivers help the firm to understand and cut back on different costs which

may be included in the future budgets that are prepared by the management of the firm

Easy to understand – As it is mentioned in the case study that the owner manager of the

firm does not want to buy expensive solutions and that the implementation of any new

system must be understandable to the staff and in some instances to the clients even as

the price of the services should be justified to them too, activity based costing is the

potential solution for such requirements. This is because an activity based costing system

is easy to understand both by the staff and the customers.

6

MANAGEMENT ACCOUNTING

Disadvantages:

Expensive to implement – Implementation of the activity based costing is an expensive

affair. An activity based costing is much more expensive than traditional costing.

Furthermore, along with the implementation process, the costs to maintain the system are

high as well. Moreover, TaxEzy needs to train its employees in the utilization and

handling of the activity based costing system.

Conforming to GAAP – A major issue with the activity based costing is that it does not

conform to GAAP. GAAP or generally accepted accounting principles provide the global

standards for the accounting treatment that is utilized by the accountants worldwide.

However, the fact that the activity based costing system, not conforming to GAAP make

it difficult for the accountants to align the particular costing structure with the financial

proceedings of the firm. In case of TaxEzy, this particular difficulty must be faced by the

accountants of the firm.

Time consuming process – The preparation of an activity based costing system is also a

time consuming process as the cost accountant has to identify the potential cost drivers

and then allocate the costs accordingly

Answer to Question 4

As it can be observed from the activity based costing system, the cost that is incurred in

providing the income tax services to the small business and the individual owner amounts to up

to $156.39 per individual and $366.76 per business. However, the charge that is applied by

TaxEzy from its customers amounts to $149 per individual return and $399 per business return.

This indicates that the firm incurs no profit from the individual returns. In fact the firm incurs a

particular loss of ($156.39 - $149) $7.39. This is the reason that the firm in spite of huge

workload in the previous year has failed to incur the estimated profits. The particular amount that

has been charged against the tax preparation for businesses is $399. Thus, the particular profit

that the firm incurs in terms of the business returns is ($399 - $366.76) $32.24. However, when

the total profit is that is incurred by the firm is computed, the profit of $32.24 is offset by a loss

of $7.39, thus reducing the incurred profit to $24.85. Thus, there might be certain alterations,

MANAGEMENT ACCOUNTING

Disadvantages:

Expensive to implement – Implementation of the activity based costing is an expensive

affair. An activity based costing is much more expensive than traditional costing.

Furthermore, along with the implementation process, the costs to maintain the system are

high as well. Moreover, TaxEzy needs to train its employees in the utilization and

handling of the activity based costing system.

Conforming to GAAP – A major issue with the activity based costing is that it does not

conform to GAAP. GAAP or generally accepted accounting principles provide the global

standards for the accounting treatment that is utilized by the accountants worldwide.

However, the fact that the activity based costing system, not conforming to GAAP make

it difficult for the accountants to align the particular costing structure with the financial

proceedings of the firm. In case of TaxEzy, this particular difficulty must be faced by the

accountants of the firm.

Time consuming process – The preparation of an activity based costing system is also a

time consuming process as the cost accountant has to identify the potential cost drivers

and then allocate the costs accordingly

Answer to Question 4

As it can be observed from the activity based costing system, the cost that is incurred in

providing the income tax services to the small business and the individual owner amounts to up

to $156.39 per individual and $366.76 per business. However, the charge that is applied by

TaxEzy from its customers amounts to $149 per individual return and $399 per business return.

This indicates that the firm incurs no profit from the individual returns. In fact the firm incurs a

particular loss of ($156.39 - $149) $7.39. This is the reason that the firm in spite of huge

workload in the previous year has failed to incur the estimated profits. The particular amount that

has been charged against the tax preparation for businesses is $399. Thus, the particular profit

that the firm incurs in terms of the business returns is ($399 - $366.76) $32.24. However, when

the total profit is that is incurred by the firm is computed, the profit of $32.24 is offset by a loss

of $7.39, thus reducing the incurred profit to $24.85. Thus, there might be certain alterations,

7

MANAGEMENT ACCOUNTING

execution of which, will improve the financial performance of TaxEzy. These alterations may be

as following:

As mentioned in the case study, the accountant Bishop finds out that other tax agents

charge individuals as little as $100 for a basic return. However, the cost incurred in

providing the individual services to the clients, as computed by activity based costing, is

$156.39. Thus, in order to compete with the fellow firms TaxEzy may reduce the amount

that is charged from the individual customers and increase the amount that is charged

from the small business owners ($399) in order to compensate for the incurred loss.

However, that would lead to an unprecedented rise in the amount charged against tax

preparation for the small business owners which may in turn lead to loss of potential

customers. Therefore, the business owner may consider reducing the cost of providing the

services especially to the individual clients so that the profit obtained from sales,

increases. The owner may also consider increasing the profit obtained from the business

returns so that the profit can be rightly adjusted (Tsai 2014).

The owner of the firm may also consider reducing the costs of providing the business

services so that the profit earned by the sales of such services certainly increases and the

profits are rightfully adjusted. Thus, to be precise the management is left with two major

alternatives in regards to the pricing policy. These alternatives are, either the costs

incurred in providing the tax preparation services should be reduced or the prices should

be increased by a reasonable amount.

Part 2

Introduction

Team work is a crucial component in any field of work especially the work culture that

has developed in the current times. The capabilities of a team in terms of the dynamics and

variance that it can offer will never be possible for a single individual to provide. In case of a

team work the different perspectives of the different team members effectively broaden the scope

of the range of techniques that can be adopted in order to arrive at the desired solution. I have

been fortunate to be a part of such a team and experience the benefits of the team work (Perez-

Prado 2017).

MANAGEMENT ACCOUNTING

execution of which, will improve the financial performance of TaxEzy. These alterations may be

as following:

As mentioned in the case study, the accountant Bishop finds out that other tax agents

charge individuals as little as $100 for a basic return. However, the cost incurred in

providing the individual services to the clients, as computed by activity based costing, is

$156.39. Thus, in order to compete with the fellow firms TaxEzy may reduce the amount

that is charged from the individual customers and increase the amount that is charged

from the small business owners ($399) in order to compensate for the incurred loss.

However, that would lead to an unprecedented rise in the amount charged against tax

preparation for the small business owners which may in turn lead to loss of potential

customers. Therefore, the business owner may consider reducing the cost of providing the

services especially to the individual clients so that the profit obtained from sales,

increases. The owner may also consider increasing the profit obtained from the business

returns so that the profit can be rightly adjusted (Tsai 2014).

The owner of the firm may also consider reducing the costs of providing the business

services so that the profit earned by the sales of such services certainly increases and the

profits are rightfully adjusted. Thus, to be precise the management is left with two major

alternatives in regards to the pricing policy. These alternatives are, either the costs

incurred in providing the tax preparation services should be reduced or the prices should

be increased by a reasonable amount.

Part 2

Introduction

Team work is a crucial component in any field of work especially the work culture that

has developed in the current times. The capabilities of a team in terms of the dynamics and

variance that it can offer will never be possible for a single individual to provide. In case of a

team work the different perspectives of the different team members effectively broaden the scope

of the range of techniques that can be adopted in order to arrive at the desired solution. I have

been fortunate to be a part of such a team and experience the benefits of the team work (Perez-

Prado 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

MANAGEMENT ACCOUNTING

Group Description

The group consisted of four members including myself. The other three members were

John, Lucinda and Raphael. The number of team meetings that were held is eleven meetings.

Each of the meetings that were held lasted for a period of four to five hours. The location where

the meetings were held was the houses of the respective team members.

My role

The particular role that I had been assigned with was the creation of the analysis

framework according to which the assigned project has to be completed. Furthermore, I had to

identify the potential sources from which references for the completion of the task, could be

derived.

Others’ roles

There had been other three members in the team. John was delegated the responsibility of

computing the costs of the services provided utilizing the activity based costing system. Lucinda

had to refer to the identified sources in order to list the potential advantages and disadvantages of

activity based costing. Raphael lastly had the essential duty of compiling the obtained results by

John and Lucinda and designing them according to the framework set by me.

Group Stages

The different group stages that are used for forming the team effectively are forming,

storming, norming and performing. The forming stage essentially refers to the initial stage of

integration, when all the team members come together. This stage is generally featured by

anxiety and uncertainty (Perez-Prado 2015).

The next stage is known as storming. The conflict in opinion that is a common feature in

every tem generally occurs at this stage.

The next stage is known as norming. This is the most crucial stage in terms of formation

of the team. This is because norming is the particular stage when the entire team becomes an

integrated unit. The individual as well as the team objective is clear to every team member and as

a result the team morale is high.

MANAGEMENT ACCOUNTING

Group Description

The group consisted of four members including myself. The other three members were

John, Lucinda and Raphael. The number of team meetings that were held is eleven meetings.

Each of the meetings that were held lasted for a period of four to five hours. The location where

the meetings were held was the houses of the respective team members.

My role

The particular role that I had been assigned with was the creation of the analysis

framework according to which the assigned project has to be completed. Furthermore, I had to

identify the potential sources from which references for the completion of the task, could be

derived.

Others’ roles

There had been other three members in the team. John was delegated the responsibility of

computing the costs of the services provided utilizing the activity based costing system. Lucinda

had to refer to the identified sources in order to list the potential advantages and disadvantages of

activity based costing. Raphael lastly had the essential duty of compiling the obtained results by

John and Lucinda and designing them according to the framework set by me.

Group Stages

The different group stages that are used for forming the team effectively are forming,

storming, norming and performing. The forming stage essentially refers to the initial stage of

integration, when all the team members come together. This stage is generally featured by

anxiety and uncertainty (Perez-Prado 2015).

The next stage is known as storming. The conflict in opinion that is a common feature in

every tem generally occurs at this stage.

The next stage is known as norming. This is the most crucial stage in terms of formation

of the team. This is because norming is the particular stage when the entire team becomes an

integrated unit. The individual as well as the team objective is clear to every team member and as

a result the team morale is high.

9

MANAGEMENT ACCOUNTING

The last stage is featured by the performance of the common objective for which the team

had been constructed. This stage is featured by the successful delivery of the assigned tasks by

each team member.

My team had also gone through each of the above listed stages and had emerged as a

single integrated unit of individuals sharing a common purpose or objective (Woodcock 2017).

Conflict within the group

There had been a particular instance of conflict within the group. Lucinda and Raphael

fought over the same job role of compiling the obtained results in accordance to the established

framework. I had to step in and resolve the conflict by clearing the facts in hand. Raphael had

been a part of a team previously, who had been assigned a similar task. Thus, the particular

compilation process in which the obtained results should be designed will be better understood

and executed by Raphael. Lucinda on the other hand having a thorough knowledge of costing

would better utilize her skills by carrying out the assigned task that is listing the potential

advantages and disadvantages of activity based costing. The learning that I acquired through

such an experience is the leadership skills that are required in effectively managing a team.

Leadership and decision making in the group

The leadership and decision making in the team had been executed by me. The

providence of such a position had been unanimously decided by the team without any

disagreements. My team members did place enough trust in me and this made me feel motivated

and enhanced my self confidence.

Achievements by the team and scope of improvement

The task that had been assigned to the team had been successfully carried out within the

stipulated time frame. Such an achievement according to me is the most important criteria, which

matters. The delivered assignment also met the required quality standards signifying that the

capabilities or the vast range of expertise that a team could possess, would never match with the

capabilities of an individual.

However, potential improvements could also be achieved in terms of team discipline.

This is evident from the fact that each of the team members had been absent from one or two

MANAGEMENT ACCOUNTING

The last stage is featured by the performance of the common objective for which the team

had been constructed. This stage is featured by the successful delivery of the assigned tasks by

each team member.

My team had also gone through each of the above listed stages and had emerged as a

single integrated unit of individuals sharing a common purpose or objective (Woodcock 2017).

Conflict within the group

There had been a particular instance of conflict within the group. Lucinda and Raphael

fought over the same job role of compiling the obtained results in accordance to the established

framework. I had to step in and resolve the conflict by clearing the facts in hand. Raphael had

been a part of a team previously, who had been assigned a similar task. Thus, the particular

compilation process in which the obtained results should be designed will be better understood

and executed by Raphael. Lucinda on the other hand having a thorough knowledge of costing

would better utilize her skills by carrying out the assigned task that is listing the potential

advantages and disadvantages of activity based costing. The learning that I acquired through

such an experience is the leadership skills that are required in effectively managing a team.

Leadership and decision making in the group

The leadership and decision making in the team had been executed by me. The

providence of such a position had been unanimously decided by the team without any

disagreements. My team members did place enough trust in me and this made me feel motivated

and enhanced my self confidence.

Achievements by the team and scope of improvement

The task that had been assigned to the team had been successfully carried out within the

stipulated time frame. Such an achievement according to me is the most important criteria, which

matters. The delivered assignment also met the required quality standards signifying that the

capabilities or the vast range of expertise that a team could possess, would never match with the

capabilities of an individual.

However, potential improvements could also be achieved in terms of team discipline.

This is evident from the fact that each of the team members had been absent from one or two

10

MANAGEMENT ACCOUNTING

team meetings for which an extra meeting had to be conducted. This did reduce the speed of

performance of the team.

Conclusion

Thus, as it can be concluded from the above discussion team work has effectively taught

me to be patient and has made me a believer in the capabilities of team work.

MANAGEMENT ACCOUNTING

team meetings for which an extra meeting had to be conducted. This did reduce the speed of

performance of the team.

Conclusion

Thus, as it can be concluded from the above discussion team work has effectively taught

me to be patient and has made me a believer in the capabilities of team work.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

MANAGEMENT ACCOUNTING

References

Hanrahan, S.J. and Pedro, R.A., 2015. Team building activities in dance and discoveries from

reflective essays.

Hanrahan, S.J. and Pedro, R.A., 2017. Team-building activities in dance classes and discoveries

from reflective essays. Asia-Pacific Journal of Health, Sport and Physical Education, 8(1),

pp.53-66.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Selviaridis, K. and Norrman, A., 2014. Performance-based contracting in service supply chains:

a service provider risk perspective. Supply Chain Management: An International Journal, 19(2),

pp.153-172.

Team Writing for Team Building: A Collaborative Writing Approach for Use in Traditional and

Online Classrooms of English Language Learners. HOW Journal, 10(1), pp.53-66.

Thomas, D.S. and Gilbert, S.W., 2014. Costs and cost effectiveness of additive manufacturing.

NIST Special Publication, 1176, p.12.

Tsai, W.H., Yang, C.H., Chang, J.C. and Lee, H.L., 2014. An Activity-Based Costing decision

model for life cycle assessment in green building projects. European Journal of Operational

Research, 238(2), pp.607-619.

Woodcock, M., 2017. Team development manual. Routledge.

MANAGEMENT ACCOUNTING

References

Hanrahan, S.J. and Pedro, R.A., 2015. Team building activities in dance and discoveries from

reflective essays.

Hanrahan, S.J. and Pedro, R.A., 2017. Team-building activities in dance classes and discoveries

from reflective essays. Asia-Pacific Journal of Health, Sport and Physical Education, 8(1),

pp.53-66.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Selviaridis, K. and Norrman, A., 2014. Performance-based contracting in service supply chains:

a service provider risk perspective. Supply Chain Management: An International Journal, 19(2),

pp.153-172.

Team Writing for Team Building: A Collaborative Writing Approach for Use in Traditional and

Online Classrooms of English Language Learners. HOW Journal, 10(1), pp.53-66.

Thomas, D.S. and Gilbert, S.W., 2014. Costs and cost effectiveness of additive manufacturing.

NIST Special Publication, 1176, p.12.

Tsai, W.H., Yang, C.H., Chang, J.C. and Lee, H.L., 2014. An Activity-Based Costing decision

model for life cycle assessment in green building projects. European Journal of Operational

Research, 238(2), pp.607-619.

Woodcock, M., 2017. Team development manual. Routledge.

12

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.