Management Accounting Practices and Trends

VerifiedAdded on 2020/06/06

|14

|4966

|424

AI Summary

This assignment analyzes recent research in the field of management accounting. It examines current themes and trends, drawing upon various academic sources to understand the evolving nature of this discipline. The review includes perspectives on the societal relevance of management accounting innovations, approaches to validation and evaluation in qualitative studies, and the use of partial least squares structural equation modeling (PLS-SEM) in management accounting research.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Different management accounting system and their essential requirements..........................1

P2 Methods used for management accounting reporting............................................................3

TASK 2............................................................................................................................................5

P3 Marginal and absorption costing method...............................................................................5

TASK 3............................................................................................................................................7

P4 Advantage and disadvantage of using different planning tools that can be used for

budgetary control at workplace...................................................................................................7

P5 Way in which firms are adopting mangement accounting system in order to respond to

financial problems.....................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Table 1Profit by absorption costing method....................................................................................4

Table 2Profit by marginal costing method......................................................................................5

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Different management accounting system and their essential requirements..........................1

P2 Methods used for management accounting reporting............................................................3

TASK 2............................................................................................................................................5

P3 Marginal and absorption costing method...............................................................................5

TASK 3............................................................................................................................................7

P4 Advantage and disadvantage of using different planning tools that can be used for

budgetary control at workplace...................................................................................................7

P5 Way in which firms are adopting mangement accounting system in order to respond to

financial problems.....................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Table 1Profit by absorption costing method....................................................................................4

Table 2Profit by marginal costing method......................................................................................5

INTRODUCTION

Management accounting is the one of the field that is gaining wide popularity among

business firms. This is because cost control is the one of the main objective of the firms and

management accounting is the dicipline that assist firms in sorting out these problems. In the

present research study varied management accounting system are discussed in details. Apart

from this, varied reporting systems that are quite popular among varied entities are also analyzed.

In midle part of the report, profit calculation is done by using varied approaches. At end of the

report, varied planning tools in respect to budgetary control are discussed and MA system that

can be adopted to tackle financial problem are also explained.

TASK 1

P1 Different management accounting system and their essential requirements

To

The Small White Elephant Date: 14-2-2018

Subject: Management accounting systems and reporting systems

Management accounting is the one of the field which underpin cost control strategy of the firm

by providing relevant inputs that are considered for preparing mentioned tactics. It is tool that

assist company to foray in respect to cost control. Varied management accounting systems are

evolved in past few years according to requirement of different companies. Selection of

maangement accounting system largely depeneds on firm product portfolio and type of

decisions or elements on which company intends to keep control. Varied management

accounting systems that can be taken in to account by the business firm are as follows. Cost accounting system: It is the accounting system widely adopt by the corporate at

workplace to obtain an overview of the summed value of fixed and variable expenses

in the business (Harris and Durden, 2012). In this regard, Small White Elephant at

initial stage categorize expenses in category of fixed, variable and semi variable

expenses and at end of the specific duration whenever required all elements values that

are in fixed, variable and semi variable category are added together. By doing so

overall cost that is incurred in the products are identified. Thus, it can be said that by

using cost accounting system it can be identified that which are the products where

variable expenses made are high or fixed expenses incurred are high. Cost accounting

system is used by most of business firms because fixed expenses are certain in the

1 | P a g e

Management accounting is the one of the field that is gaining wide popularity among

business firms. This is because cost control is the one of the main objective of the firms and

management accounting is the dicipline that assist firms in sorting out these problems. In the

present research study varied management accounting system are discussed in details. Apart

from this, varied reporting systems that are quite popular among varied entities are also analyzed.

In midle part of the report, profit calculation is done by using varied approaches. At end of the

report, varied planning tools in respect to budgetary control are discussed and MA system that

can be adopted to tackle financial problem are also explained.

TASK 1

P1 Different management accounting system and their essential requirements

To

The Small White Elephant Date: 14-2-2018

Subject: Management accounting systems and reporting systems

Management accounting is the one of the field which underpin cost control strategy of the firm

by providing relevant inputs that are considered for preparing mentioned tactics. It is tool that

assist company to foray in respect to cost control. Varied management accounting systems are

evolved in past few years according to requirement of different companies. Selection of

maangement accounting system largely depeneds on firm product portfolio and type of

decisions or elements on which company intends to keep control. Varied management

accounting systems that can be taken in to account by the business firm are as follows. Cost accounting system: It is the accounting system widely adopt by the corporate at

workplace to obtain an overview of the summed value of fixed and variable expenses

in the business (Harris and Durden, 2012). In this regard, Small White Elephant at

initial stage categorize expenses in category of fixed, variable and semi variable

expenses and at end of the specific duration whenever required all elements values that

are in fixed, variable and semi variable category are added together. By doing so

overall cost that is incurred in the products are identified. Thus, it can be said that by

using cost accounting system it can be identified that which are the products where

variable expenses made are high or fixed expenses incurred are high. Cost accounting

system is used by most of business firms because fixed expenses are certain in the

1 | P a g e

business but variable expenses are dynamic in nature and with passage of time same

get change regularly. Thus, it can be said that cost accounting system matter a lot for

the company because in it cost classification is done in the proper manner and assist

them in making decisions at workplace in terms of cost control. Process costing system: Process costing system is one under which each and every

stage that is related to process is taken in to account for costing purpose. Means that

while producing products varied stages are performed. In process costing for each of

these stages costing is done at Small White Elephant. Hence, it can be said that process

costing system have high importance for the manufacturing firms. By adopting this

costing system they identify that in which stage of production cost is high. Thereafter,

analysis can be done and it can be identified that which are the components due to

which cost of production is high duirng specific stage (Chiwamit, Modell and Yang,

2014). If possible unproductive steps are removed from the production process and by

doing so cost control is done. Hence, it can be said that process costing system have

due importance for the firms as it assist firm in cost control and curtailment. Job costing system: Job costing system is one under which for each job costing is done

separately. This accounting system is adopted by the firms who manufacture products

based on customer order received. Different orders have vaired specifications and due

to this reason same costing is not possible in case of all products. Hence, under job

costing system separately for each job expenses are recorded and by applying specific

technique cost is computed. Hence, it can be said that job costing system is the one of

the most important costing system that is mostly used by the automobile makers in

their busuiness. By using job costing system products where cost is high can be

identified and on preliminary stage efforts can be made to control cost. By doing so

profitability is enhanced in the business. It can be said that job costing system is

adopted by large number of firms in their business practice. Throughput costing system: It is another accounting system under which costing is

done in different manner. Mentioned system is also known as modern costing system

and it was developed by Israeli businessman (Nitzl, 2016). Under this accounting

system all tasks are analyzed deeply and on that basis activities where cost is high are

identified and controlled. Hence, it can be said that there is significence of througput

2 | P a g e

get change regularly. Thus, it can be said that cost accounting system matter a lot for

the company because in it cost classification is done in the proper manner and assist

them in making decisions at workplace in terms of cost control. Process costing system: Process costing system is one under which each and every

stage that is related to process is taken in to account for costing purpose. Means that

while producing products varied stages are performed. In process costing for each of

these stages costing is done at Small White Elephant. Hence, it can be said that process

costing system have high importance for the manufacturing firms. By adopting this

costing system they identify that in which stage of production cost is high. Thereafter,

analysis can be done and it can be identified that which are the components due to

which cost of production is high duirng specific stage (Chiwamit, Modell and Yang,

2014). If possible unproductive steps are removed from the production process and by

doing so cost control is done. Hence, it can be said that process costing system have

due importance for the firms as it assist firm in cost control and curtailment. Job costing system: Job costing system is one under which for each job costing is done

separately. This accounting system is adopted by the firms who manufacture products

based on customer order received. Different orders have vaired specifications and due

to this reason same costing is not possible in case of all products. Hence, under job

costing system separately for each job expenses are recorded and by applying specific

technique cost is computed. Hence, it can be said that job costing system is the one of

the most important costing system that is mostly used by the automobile makers in

their busuiness. By using job costing system products where cost is high can be

identified and on preliminary stage efforts can be made to control cost. By doing so

profitability is enhanced in the business. It can be said that job costing system is

adopted by large number of firms in their business practice. Throughput costing system: It is another accounting system under which costing is

done in different manner. Mentioned system is also known as modern costing system

and it was developed by Israeli businessman (Nitzl, 2016). Under this accounting

system all tasks are analyzed deeply and on that basis activities where cost is high are

identified and controlled. Hence, it can be said that there is significence of througput

2 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

accounting system for the business firms because also like other system facilitate cost

control.

P2 Methods used for management accounting reporting

To

The Small White Elephant Date: 14-2-2018

Subject: Management accounting systems and reporting systems

Reporting is the one of the most important task in the business that play vital role in its

growth. This is because through reporting managers comes to know about things that are going

on in the business. Reporting can be done through charts and tables. Many advanced softwares

like Tableau are used by the firms for visualization purpose. Different facts are revealed from

these tables and images about business performance. In current time period business are

increasing at rapid pace and due to this reason it become difficult for firms to keep check on

expenses and manag company operations. There are different softwares that can be used by the

firms for making business decisions because in them reports are generated and for same there

is need to just put an input in the software. It can be said that there is huge importance of the

maangement accounting reporitng for the firms (Hopper and Bui, 2016). Automatically

software by taking in to account all inputs prepare management accounting report which

encompas varied facts that can be used to make bsuiness decisions. Management accounting

reporting refers to the situation where diffeent sort of reports are prepared and used for making

business decisiosn. All these report reflects firm performance on different fronts. On basis of

these reports it is identified that which are those areas where condition is good or bad.

Corrective actions are taken on basis of relevant inputs. Budget report: In budget report varied budgets are given like incremental budget, fixed

budget or flexible budget in respect to varied departments like production, marketing

and finance etc. In these reports actual expenses are also listed and on basis of

comparison that will be made it will be identified that whether expenses are in control

of the firm or there is need to take action on time to handle condition. It can be said

that budget report help firms in identifying multiple facts and figures and show them

area where there is need to actually do the work in order to control expenses in the

3 | P a g e

control.

P2 Methods used for management accounting reporting

To

The Small White Elephant Date: 14-2-2018

Subject: Management accounting systems and reporting systems

Reporting is the one of the most important task in the business that play vital role in its

growth. This is because through reporting managers comes to know about things that are going

on in the business. Reporting can be done through charts and tables. Many advanced softwares

like Tableau are used by the firms for visualization purpose. Different facts are revealed from

these tables and images about business performance. In current time period business are

increasing at rapid pace and due to this reason it become difficult for firms to keep check on

expenses and manag company operations. There are different softwares that can be used by the

firms for making business decisions because in them reports are generated and for same there

is need to just put an input in the software. It can be said that there is huge importance of the

maangement accounting reporitng for the firms (Hopper and Bui, 2016). Automatically

software by taking in to account all inputs prepare management accounting report which

encompas varied facts that can be used to make bsuiness decisions. Management accounting

reporting refers to the situation where diffeent sort of reports are prepared and used for making

business decisiosn. All these report reflects firm performance on different fronts. On basis of

these reports it is identified that which are those areas where condition is good or bad.

Corrective actions are taken on basis of relevant inputs. Budget report: In budget report varied budgets are given like incremental budget, fixed

budget or flexible budget in respect to varied departments like production, marketing

and finance etc. In these reports actual expenses are also listed and on basis of

comparison that will be made it will be identified that whether expenses are in control

of the firm or there is need to take action on time to handle condition. It can be said

that budget report help firms in identifying multiple facts and figures and show them

area where there is need to actually do the work in order to control expenses in the

3 | P a g e

business. Budget report are prepared monthly, quarterly, half year and annual basis and

by making comparison with actual performance is accessed. Thus, it can be assumed

that budget report have due importance for the firms. Job cost report: Job cost report is also prepared by many firms like Small White

Elephant specially those that are working in automobile sector. In this report, in

respect to varied jobs cost are given (Van der Meer-Kooistra and Vosselman, 2012).

These costs can be further classfied in to fixed and variable as well as semi variable

expenses. It can be said that deeply cost can be analyzed by using job cost report. It is

one of the most important reporting method that is used on large scale by the firms.

Companies that produce products on basis of specfic specifications usually use job cost

report in order to make business decisions. Income statement: Income statement is another statement which is prepared by all

firms whether their size is large, small and big. Under income statement revenue and

expenses are listed and from revenue amount expenes are subtracted. On yearly basis

income statement values can be compared with other and on that basis it can be

identified whether expenses increase or decrease in the business. Apart from this, by

doing analysis it can also be identified that what proportion of sales is covered by

specific sort of expenses in the business (Kihn and Ihantola, 2015). On yearly basis by

considering this factor comparison can be done and it can be identified that which sort

of expenses are increasing at fast rate. By preparing cost control tactics situation that

was out of control is bringing in control by the managers. Account receivable reporting: It is the another mode of reporting under which entire

calculation and detail of account receivable are given in the reporting. It is the one of

the important reporting method because in business time to time goods are sold on

credit basis to the business firms. In the report, one can easily identify customers from

whom higher amount of sales is made through receivables. Thus, focus can be made on

such customers in respect to making credit sales and management on time can make

effort to control bad debt in the business. All these things lead to strong control on

bloackage of cash in the business and also assist firm in taking steps on right time to

control bad debt. Overall, it can be said that account receivable reporting assist in

improving maangement at workplace.

4 | P a g e

by making comparison with actual performance is accessed. Thus, it can be assumed

that budget report have due importance for the firms. Job cost report: Job cost report is also prepared by many firms like Small White

Elephant specially those that are working in automobile sector. In this report, in

respect to varied jobs cost are given (Van der Meer-Kooistra and Vosselman, 2012).

These costs can be further classfied in to fixed and variable as well as semi variable

expenses. It can be said that deeply cost can be analyzed by using job cost report. It is

one of the most important reporting method that is used on large scale by the firms.

Companies that produce products on basis of specfic specifications usually use job cost

report in order to make business decisions. Income statement: Income statement is another statement which is prepared by all

firms whether their size is large, small and big. Under income statement revenue and

expenses are listed and from revenue amount expenes are subtracted. On yearly basis

income statement values can be compared with other and on that basis it can be

identified whether expenses increase or decrease in the business. Apart from this, by

doing analysis it can also be identified that what proportion of sales is covered by

specific sort of expenses in the business (Kihn and Ihantola, 2015). On yearly basis by

considering this factor comparison can be done and it can be identified that which sort

of expenses are increasing at fast rate. By preparing cost control tactics situation that

was out of control is bringing in control by the managers. Account receivable reporting: It is the another mode of reporting under which entire

calculation and detail of account receivable are given in the reporting. It is the one of

the important reporting method because in business time to time goods are sold on

credit basis to the business firms. In the report, one can easily identify customers from

whom higher amount of sales is made through receivables. Thus, focus can be made on

such customers in respect to making credit sales and management on time can make

effort to control bad debt in the business. All these things lead to strong control on

bloackage of cash in the business and also assist firm in taking steps on right time to

control bad debt. Overall, it can be said that account receivable reporting assist in

improving maangement at workplace.

4 | P a g e

TASK 2

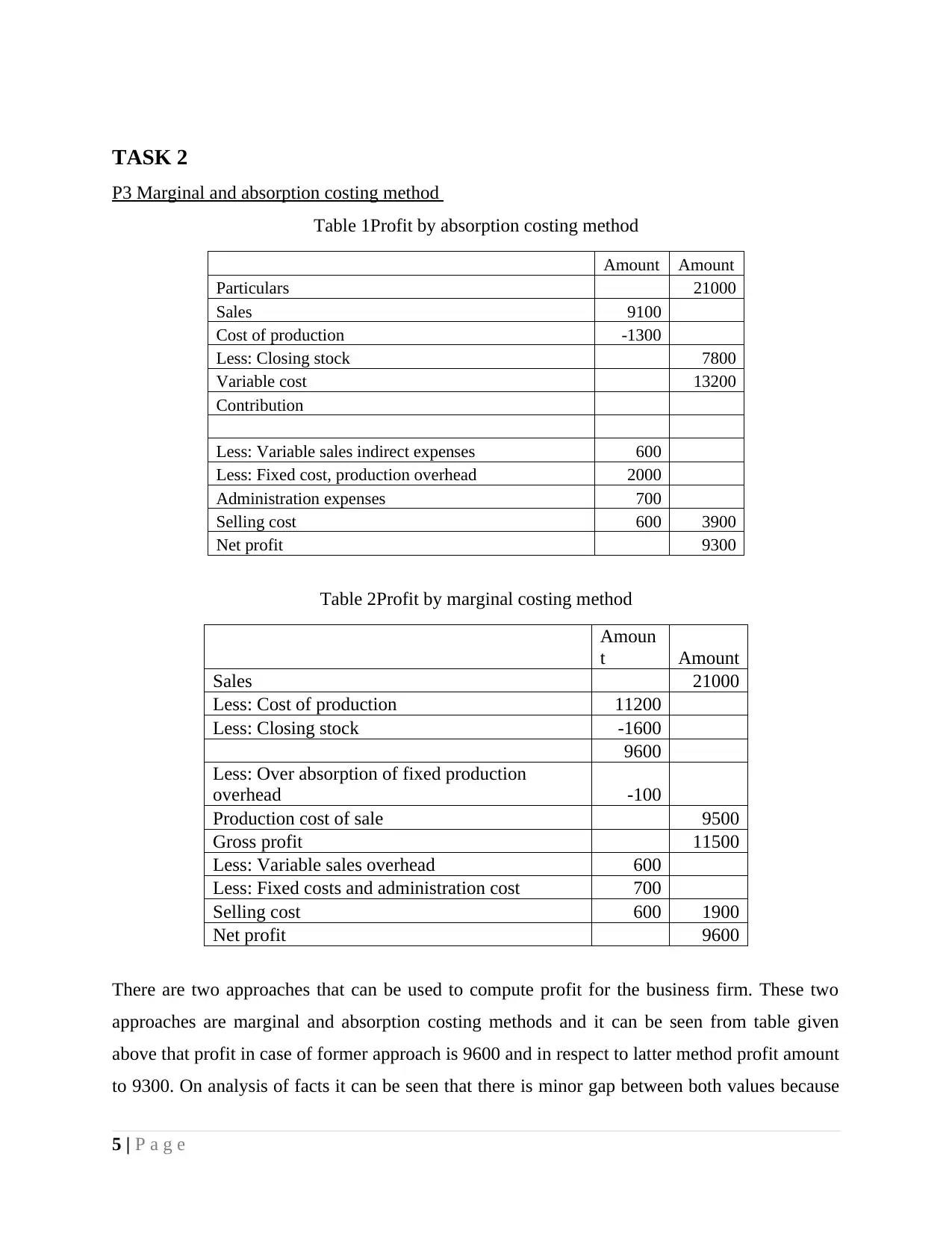

P3 Marginal and absorption costing method

Table 1Profit by absorption costing method

Amount Amount

Particulars 21000

Sales 9100

Cost of production -1300

Less: Closing stock 7800

Variable cost 13200

Contribution

Less: Variable sales indirect expenses 600

Less: Fixed cost, production overhead 2000

Administration expenses 700

Selling cost 600 3900

Net profit 9300

Table 2Profit by marginal costing method

Amoun

t Amount

Sales 21000

Less: Cost of production 11200

Less: Closing stock -1600

9600

Less: Over absorption of fixed production

overhead -100

Production cost of sale 9500

Gross profit 11500

Less: Variable sales overhead 600

Less: Fixed costs and administration cost 700

Selling cost 600 1900

Net profit 9600

There are two approaches that can be used to compute profit for the business firm. These two

approaches are marginal and absorption costing methods and it can be seen from table given

above that profit in case of former approach is 9600 and in respect to latter method profit amount

to 9300. On analysis of facts it can be seen that there is minor gap between both values because

5 | P a g e

P3 Marginal and absorption costing method

Table 1Profit by absorption costing method

Amount Amount

Particulars 21000

Sales 9100

Cost of production -1300

Less: Closing stock 7800

Variable cost 13200

Contribution

Less: Variable sales indirect expenses 600

Less: Fixed cost, production overhead 2000

Administration expenses 700

Selling cost 600 3900

Net profit 9300

Table 2Profit by marginal costing method

Amoun

t Amount

Sales 21000

Less: Cost of production 11200

Less: Closing stock -1600

9600

Less: Over absorption of fixed production

overhead -100

Production cost of sale 9500

Gross profit 11500

Less: Variable sales overhead 600

Less: Fixed costs and administration cost 700

Selling cost 600 1900

Net profit 9600

There are two approaches that can be used to compute profit for the business firm. These two

approaches are marginal and absorption costing methods and it can be seen from table given

above that profit in case of former approach is 9600 and in respect to latter method profit amount

to 9300. On analysis of facts it can be seen that there is minor gap between both values because

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

calculation approach vary from each other. It is the slight difference in the approach that make

both approaches different from each other. However, both methods are usually used by the

companies to make decisions and it depend on their requirement that which of approach they

find more appropriate for profit calculation. There are some fundamental difference between

marginal and absorption costing method. One of them is that in case of marginal costing method

only variable expenses are taken in to account. There is another method which is also known as

absorption costing method and under this both fixed and variable expenses are taken in to

account (Ahmad, 2013). It can be said that there is difference between both marginal and

absorption costing method and firms according to their requirement can select any method to

compute profitability in the business. In terms of profit marginal costing method give better

results than absorption costing. It is inevitable to understand the fixed expenses and other sort of

expenditures that are made in the business. Fixed expenditures are those that remain static or

unchanged irrespective of level of production. This is because fixed expenses are made on assets.

Whatever, expenses made in terms of fixed cost are deducted in same year from sales value. In

this way, both variable and fixed expenses are included in overall cost of product and deducted

from sales value. Opposite to this, in marginal costing method variable expenses only are

considered. This is the reason due to which high amount of profit is revealed by marginal then

absorption costing method. It can be said that it depend on managers that which of approach they

find more suitable for profit calculation. This is because some managers may want to view effect

of both fixed and variable expenses on profit. Such kind of managers will prefer to use

absorption costing method (Sunarni, 2013). On other hand, if manager intend to know effect of

marginal cost on profit then in that case it will be better to use marginal costing method. Thus,

there is importance of both marginal and absorption costing method for the business firms. It can

be said that use of marginal costing method will be appropriate for the firm because for

producing goods only variable expenses are incurred not fixed expenses. Hence, inclusion of

fixed expenses in profit calculation does not seem appropriate. However, fixed expenses are

incurred in the business and same is capital expenditure for the firm and due to this reason its

deduction from sales cannot be avoided. Hence, it is very important to ensure that both

approaches are used at workplace because they reflect different scenarios to managers. Both

approaches are appropriate and managers according to need must use these methods to perform

calculation. In usual practice it is observed that most of firms use absorption costing method

6 | P a g e

both approaches different from each other. However, both methods are usually used by the

companies to make decisions and it depend on their requirement that which of approach they

find more appropriate for profit calculation. There are some fundamental difference between

marginal and absorption costing method. One of them is that in case of marginal costing method

only variable expenses are taken in to account. There is another method which is also known as

absorption costing method and under this both fixed and variable expenses are taken in to

account (Ahmad, 2013). It can be said that there is difference between both marginal and

absorption costing method and firms according to their requirement can select any method to

compute profitability in the business. In terms of profit marginal costing method give better

results than absorption costing. It is inevitable to understand the fixed expenses and other sort of

expenditures that are made in the business. Fixed expenditures are those that remain static or

unchanged irrespective of level of production. This is because fixed expenses are made on assets.

Whatever, expenses made in terms of fixed cost are deducted in same year from sales value. In

this way, both variable and fixed expenses are included in overall cost of product and deducted

from sales value. Opposite to this, in marginal costing method variable expenses only are

considered. This is the reason due to which high amount of profit is revealed by marginal then

absorption costing method. It can be said that it depend on managers that which of approach they

find more suitable for profit calculation. This is because some managers may want to view effect

of both fixed and variable expenses on profit. Such kind of managers will prefer to use

absorption costing method (Sunarni, 2013). On other hand, if manager intend to know effect of

marginal cost on profit then in that case it will be better to use marginal costing method. Thus,

there is importance of both marginal and absorption costing method for the business firms. It can

be said that use of marginal costing method will be appropriate for the firm because for

producing goods only variable expenses are incurred not fixed expenses. Hence, inclusion of

fixed expenses in profit calculation does not seem appropriate. However, fixed expenses are

incurred in the business and same is capital expenditure for the firm and due to this reason its

deduction from sales cannot be avoided. Hence, it is very important to ensure that both

approaches are used at workplace because they reflect different scenarios to managers. Both

approaches are appropriate and managers according to need must use these methods to perform

calculation. In usual practice it is observed that most of firms use absorption costing method

6 | P a g e

because it give clear overview of costing that is observed in the company. Absorption costing

method is the extension of the marginal costing method. Importance is given to both these

approaches by the business firms but high priority is given absorption costing over marginal

costing approach (Christ, 2014). In researches that are conducted earlier it is observed that firms

whether they are small, medium or large in size are using absorption costing method. Hence,

there is wide popularity of mentioned method among business firms.

TASK 3

P4 Advantage and disadvantage of using different planning tools that can be used for budgetary

control at workplace

There are number of planning tools that are used by the firms in their business and all of

them have some advantages and disadvantages. Different sort of planning tools that are available

to the business firms are budget and capital budgeting appraoches. In class of budget

classifications can be done. Cash budget: It is the one of the most important budget that is usually prepared by the

firm which is Small White Elephant. Under cash budget varied items of cash inflow and

outflow are included. Opening cash balance is recorded and on same revenue amount is

added. In this way overall cash inflow amount is computed. From cash inflow amount

expenses are subtracted and in this way net balance is calculated and same is transferred

to the next month. Again same process is carried out and in this way cash budget is

prepared by the business firms (Zaleha Abdul and et.al., 2011). There are some of

advantage and disadvantage of the cash budget for the firms and same are explained

below.

Advantage

Main advantage of using cash budget is that by using same high level of control is

maintained on expenditures in the business. This is because firm makes an attempt to

make actual expenses beneath determined standard. In some cases actual expenses are

greater then standard then in that situation corrective actions are taken to improve

condition.

Other main advantage of using cash budget is that it help firm in controlling expenses in

systematic way. Means that first of all estimation is made about likely growth of sales

reevnue in the business. Expenses are accordingly computed in the budget and by doing

7 | P a g e

method is the extension of the marginal costing method. Importance is given to both these

approaches by the business firms but high priority is given absorption costing over marginal

costing approach (Christ, 2014). In researches that are conducted earlier it is observed that firms

whether they are small, medium or large in size are using absorption costing method. Hence,

there is wide popularity of mentioned method among business firms.

TASK 3

P4 Advantage and disadvantage of using different planning tools that can be used for budgetary

control at workplace

There are number of planning tools that are used by the firms in their business and all of

them have some advantages and disadvantages. Different sort of planning tools that are available

to the business firms are budget and capital budgeting appraoches. In class of budget

classifications can be done. Cash budget: It is the one of the most important budget that is usually prepared by the

firm which is Small White Elephant. Under cash budget varied items of cash inflow and

outflow are included. Opening cash balance is recorded and on same revenue amount is

added. In this way overall cash inflow amount is computed. From cash inflow amount

expenses are subtracted and in this way net balance is calculated and same is transferred

to the next month. Again same process is carried out and in this way cash budget is

prepared by the business firms (Zaleha Abdul and et.al., 2011). There are some of

advantage and disadvantage of the cash budget for the firms and same are explained

below.

Advantage

Main advantage of using cash budget is that by using same high level of control is

maintained on expenditures in the business. This is because firm makes an attempt to

make actual expenses beneath determined standard. In some cases actual expenses are

greater then standard then in that situation corrective actions are taken to improve

condition.

Other main advantage of using cash budget is that it help firm in controlling expenses in

systematic way. Means that first of all estimation is made about likely growth of sales

reevnue in the business. Expenses are accordingly computed in the budget and by doing

7 | P a g e

so in systematic in right direction and to great extent effort is made to control expenses in

the business.

Disadvantage

Major disadvantage of cash budget is that projection is made by estimating growth rate. It

is possible that managers estimate this growth rate in wrong manner. If same happened

then in that case budget will be prepared in wrong direction. Thus, this will lead to

making wrong decisions in the business. Fixed budget: Fixed budget is one under which same values are taken in to account for

every month and year and no change happened in values (Abrahamsson, Englund and

Gerdin, 2011). It can be said that fixed budget is quite different from cash budget and it is

not flexible like cash budget that is formed in the business.

Advantage

One of main advantage of using fixed budget is that one does not need to consume lots of

time in preparing budget. This is because budget is already prepared and there is no need

to do modification in same. Hence, lots of time is saved.

Managers does not need to face problem of determining growth rate of sales as it is very

difficult task to determine growth rate of the business, number of factors need to be

considered. In case wrong estimations are made projection goes in wrong direction.

Hence, it can be said that use of fixed budget prevent managers from doing

brainstorming.

Disadvantage

Major disadvantage of fixed budget is that values can not be altered and situation keeps

on changing consistently. Hence, fixed budget can proved suitable to the company in

single year but every it can be right to follow same budget because with change in

situation profitability of product also change. Zero based budgeting: This is different approach of budgeting and under this last year

budget is not considered and department heads at their own level determine value of the

elements of the budget (Shields, 2015). In this approch top manager demand budget from

department managers. After understanding condition and determining assumptions all

department heads prepare budget for their departments. These budgets are send to the top

manager for approval. After slight discussion top manager either approve budget or make

8 | P a g e

the business.

Disadvantage

Major disadvantage of cash budget is that projection is made by estimating growth rate. It

is possible that managers estimate this growth rate in wrong manner. If same happened

then in that case budget will be prepared in wrong direction. Thus, this will lead to

making wrong decisions in the business. Fixed budget: Fixed budget is one under which same values are taken in to account for

every month and year and no change happened in values (Abrahamsson, Englund and

Gerdin, 2011). It can be said that fixed budget is quite different from cash budget and it is

not flexible like cash budget that is formed in the business.

Advantage

One of main advantage of using fixed budget is that one does not need to consume lots of

time in preparing budget. This is because budget is already prepared and there is no need

to do modification in same. Hence, lots of time is saved.

Managers does not need to face problem of determining growth rate of sales as it is very

difficult task to determine growth rate of the business, number of factors need to be

considered. In case wrong estimations are made projection goes in wrong direction.

Hence, it can be said that use of fixed budget prevent managers from doing

brainstorming.

Disadvantage

Major disadvantage of fixed budget is that values can not be altered and situation keeps

on changing consistently. Hence, fixed budget can proved suitable to the company in

single year but every it can be right to follow same budget because with change in

situation profitability of product also change. Zero based budgeting: This is different approach of budgeting and under this last year

budget is not considered and department heads at their own level determine value of the

elements of the budget (Shields, 2015). In this approch top manager demand budget from

department managers. After understanding condition and determining assumptions all

department heads prepare budget for their departments. These budgets are send to the top

manager for approval. After slight discussion top manager either approve budget or make

8 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

some modifications in it and then give final approval to the managers. After approval

fund are given to the department heads. In this way, entire mechanism in respect to zero

based budget work.

Advantage

Major advantage of zero based budgeting is that it is the systemaic approch that is used to

prepare budget as first of all mangers determine budget at their own level and then same

is discussed with top managers (Viere, von Enden and Schaltegger, 2011). Such kind of

procedure ensure that budget will be prepared in proper manner.

Disadvantage

Major disadvantage of the zero based budget is that budget of all departments are

interrelated to each other. If one department prepare budget in wrong manner then other

department budget automatically become wrong. Hence, all these things will lead to

making wrong business decisions. Capital budgeting method: Capital budgeting method refers to the project evaluation

methods like payback period, IRR, NPV and ARR that are used to measure viability of

the project. In order to select any project these techniques are applied on cash flows

which are estimated by managers and from different angels profitability of project is

measured.

Advantage

One of major advantage of using capital budgeting method is that by using same best

alternative is selected by the firm. In determining final cash flows expenses are also taken

in to account and every attempt is made to control those expenses. Hence, in this way

budgetary control method assist in cost control.

Disadvantage

Major disadvantage of capital budgeting is that in same growth rate is taken in to account

and if same is estimated wrongly then cash flows will be computed wrongly which will

ultimately lead to selection of wrong project in the business.

Other major disadvantage of capital budgeting method is that while preparing cash flows

for the project number of assumptions are made. Means that there are number of elements

that are coverd in these cash flows. It is possible that analyst make wrong assumption in

respect to multiple elements of cash flows (Becker, Ulrich and Staffel, 2011). On basis of

9 | P a g e

fund are given to the department heads. In this way, entire mechanism in respect to zero

based budget work.

Advantage

Major advantage of zero based budgeting is that it is the systemaic approch that is used to

prepare budget as first of all mangers determine budget at their own level and then same

is discussed with top managers (Viere, von Enden and Schaltegger, 2011). Such kind of

procedure ensure that budget will be prepared in proper manner.

Disadvantage

Major disadvantage of the zero based budget is that budget of all departments are

interrelated to each other. If one department prepare budget in wrong manner then other

department budget automatically become wrong. Hence, all these things will lead to

making wrong business decisions. Capital budgeting method: Capital budgeting method refers to the project evaluation

methods like payback period, IRR, NPV and ARR that are used to measure viability of

the project. In order to select any project these techniques are applied on cash flows

which are estimated by managers and from different angels profitability of project is

measured.

Advantage

One of major advantage of using capital budgeting method is that by using same best

alternative is selected by the firm. In determining final cash flows expenses are also taken

in to account and every attempt is made to control those expenses. Hence, in this way

budgetary control method assist in cost control.

Disadvantage

Major disadvantage of capital budgeting is that in same growth rate is taken in to account

and if same is estimated wrongly then cash flows will be computed wrongly which will

ultimately lead to selection of wrong project in the business.

Other major disadvantage of capital budgeting method is that while preparing cash flows

for the project number of assumptions are made. Means that there are number of elements

that are coverd in these cash flows. It is possible that analyst make wrong assumption in

respect to multiple elements of cash flows (Becker, Ulrich and Staffel, 2011). On basis of

9 | P a g e

these elements multiple calculations are performed in model. If actual expenses are

greater then determined values then in that case it is difficult task to identify that what are

the reasons or what sort of variables are wrongly estimated due to which actual and

estimated values become different from each other.

P5 Way in which firms are adopting mangement accounting system in order to respond to

financial problems

Financial problems are usually observed by the firms in their business and it may be

related to inability control cost or credit crunch etc. In order to sort out these financial problems

there is need to adopt management accounting systems so that in proper manner company can

respond to financial problems. Some of the management accounting systems that can be adopt to

solve relevant issue are explained below. Key performance indicators: It is the one of the important tool which is used to evaluate

company performance. In this method some parameters are fixed and comparison of

obtained results are made with these parameters. By doing so direction in which there is

need to work can be determined. In respect to KPI firms normally use softwares like

Tableau in which KPI are developed and actual data is plotted against KPI. By doing so

gap that exist between both is identified in proper manner. It can be said that KPI is the

one of the important approach that can be used to solve problem. For example company

take loan at flexible interest rate and it want to track its performance so that decisions can

be taken on time and control can be made on finance cost (Management accounting, what

is management accounting?., 2017). On KPI on one side current market interest rate can

be plotted and on other side fixed interest rate can be plotted and by doing so it can be

identified whether good performance is achieved or there is need to made to make

improvement in same by adopting any strategy in business which cover loss that is

observed in the business due to gap that exist between both interest rate. Balanced scorecard: Balanced scorecard is the one of the technique that is used to

evauate firm performance. For balance scorecard there four areas that are analyzed like

financial, customer, learning and growth as well as internal business process. In respect to

these areas four things are determined like objectives, measures, target and initiatives.

Means that in respect to each component objectives are determined and measures are

determined. Apart from this, targets are ascertained that need to achieved in respect to

10 | P a g e

greater then determined values then in that case it is difficult task to identify that what are

the reasons or what sort of variables are wrongly estimated due to which actual and

estimated values become different from each other.

P5 Way in which firms are adopting mangement accounting system in order to respond to

financial problems

Financial problems are usually observed by the firms in their business and it may be

related to inability control cost or credit crunch etc. In order to sort out these financial problems

there is need to adopt management accounting systems so that in proper manner company can

respond to financial problems. Some of the management accounting systems that can be adopt to

solve relevant issue are explained below. Key performance indicators: It is the one of the important tool which is used to evaluate

company performance. In this method some parameters are fixed and comparison of

obtained results are made with these parameters. By doing so direction in which there is

need to work can be determined. In respect to KPI firms normally use softwares like

Tableau in which KPI are developed and actual data is plotted against KPI. By doing so

gap that exist between both is identified in proper manner. It can be said that KPI is the

one of the important approach that can be used to solve problem. For example company

take loan at flexible interest rate and it want to track its performance so that decisions can

be taken on time and control can be made on finance cost (Management accounting, what

is management accounting?., 2017). On KPI on one side current market interest rate can

be plotted and on other side fixed interest rate can be plotted and by doing so it can be

identified whether good performance is achieved or there is need to made to make

improvement in same by adopting any strategy in business which cover loss that is

observed in the business due to gap that exist between both interest rate. Balanced scorecard: Balanced scorecard is the one of the technique that is used to

evauate firm performance. For balance scorecard there four areas that are analyzed like

financial, customer, learning and growth as well as internal business process. In respect to

these areas four things are determined like objectives, measures, target and initiatives.

Means that in respect to each component objectives are determined and measures are

determined. Apart from this, targets are ascertained that need to achieved in respect to

10 | P a g e

elements of balance scorecard. Initaitves are also mentioned in scorecard that will be

taken to ensure that determined target will be achieved in every condition. Hence, it can

be said that there is huge importance of balance scorecard approach for the busines firms. Financial governance: Under financial governance approach for each and every

employee that is handling financial affairs roles and responsibilities are clearly

determined and it is ensured that these roles and responsibilitie does not overlap each

other. Thus, it can be said that financial governance in case of any crisis or situation help

management in making someone responsible for negative consequences. Such kind of

practice make employee liable and motivate them to give their best for benefit of an

organzation.

CONCLUSION

On basis of above discussion it is concluded that variety of management accounting

systems are available to firms as option. Management must select one of best option that best suit

its requirements. It is also concluded that marginal and absorption costing both approaches are

best and firm either can use both of them or specific one according to business needs. There are

number methods that can be used to solve financial problems. Managers can adopt all aproaches

at workplace like financial governance, KPI and benchmark altogether to ascertain that financial

problem will be handeled on time.

11 | P a g e

taken to ensure that determined target will be achieved in every condition. Hence, it can

be said that there is huge importance of balance scorecard approach for the busines firms. Financial governance: Under financial governance approach for each and every

employee that is handling financial affairs roles and responsibilities are clearly

determined and it is ensured that these roles and responsibilitie does not overlap each

other. Thus, it can be said that financial governance in case of any crisis or situation help

management in making someone responsible for negative consequences. Such kind of

practice make employee liable and motivate them to give their best for benefit of an

organzation.

CONCLUSION

On basis of above discussion it is concluded that variety of management accounting

systems are available to firms as option. Management must select one of best option that best suit

its requirements. It is also concluded that marginal and absorption costing both approaches are

best and firm either can use both of them or specific one according to business needs. There are

number methods that can be used to solve financial problems. Managers can adopt all aproaches

at workplace like financial governance, KPI and benchmark altogether to ascertain that financial

problem will be handeled on time.

11 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Abrahamsson, G., Englund, H. and Gerdin, J., 2011. Organizational identity and management

accounting change. Accounting, Auditing & Accountability Journal. 24(3). pp.345-376.

Ahmad, K., 2013. The adoption of management accounting practices in Malaysian Small and

Medium-sized Enterprises. Asian Social Science. 10(2). p.236.

Becker, W., Ulrich, P. and Staffel, M., 2011. Management accounting and controlling in German

SMEs–do company size and family influence matter?. International Journal of

Entrepreneurial Venturing. 3(3). pp.281-300.

Chiwamit, P., Modell, S. and Yang, C.L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Christ, K.L., 2014. Water management accounting and the wine supply chain: Empirical

evidence from Australia. The British Accounting Review. 46(4). pp.379-396.

Harris, J. and Durden, C., 2012. Management accounting research: An analysis of recent themes

and directions for the future. Journal of Applied Management Accounting Research. 10(2).

p.21.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Kihn, L.A. and Ihantola, E.M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management. 12(3). pp.230-255.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Shields, M.D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research. 27(1). pp.123-132.

Sunarni, C.W., 2013. Management accounting practices and the role of management accountant:

Evidence from manufacturing companies throughout Yogyakarta, Indonesia. Review of

Integrative Business and Economics Research. 2(2). p.616.

12 | P a g e

Books and journals

Abrahamsson, G., Englund, H. and Gerdin, J., 2011. Organizational identity and management

accounting change. Accounting, Auditing & Accountability Journal. 24(3). pp.345-376.

Ahmad, K., 2013. The adoption of management accounting practices in Malaysian Small and

Medium-sized Enterprises. Asian Social Science. 10(2). p.236.

Becker, W., Ulrich, P. and Staffel, M., 2011. Management accounting and controlling in German

SMEs–do company size and family influence matter?. International Journal of

Entrepreneurial Venturing. 3(3). pp.281-300.

Chiwamit, P., Modell, S. and Yang, C.L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Christ, K.L., 2014. Water management accounting and the wine supply chain: Empirical

evidence from Australia. The British Accounting Review. 46(4). pp.379-396.

Harris, J. and Durden, C., 2012. Management accounting research: An analysis of recent themes

and directions for the future. Journal of Applied Management Accounting Research. 10(2).

p.21.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Kihn, L.A. and Ihantola, E.M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management. 12(3). pp.230-255.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Shields, M.D., 2015. Established management accounting knowledge. Journal of Management

Accounting Research. 27(1). pp.123-132.

Sunarni, C.W., 2013. Management accounting practices and the role of management accountant:

Evidence from manufacturing companies throughout Yogyakarta, Indonesia. Review of

Integrative Business and Economics Research. 2(2). p.616.

12 | P a g e

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.