Management Accounting Report: Financial Performance of RL Maynard

VerifiedAdded on 2020/06/06

|18

|4602

|34

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to RL Maynard, a manufacturing company. It begins with an evaluation of management accounting systems, including traditional cost accounting, transfer pricing, and inventory management, emphasizing their significance in financial decision-making. The report then explores various reporting methods, such as production reports, budget reports, and sales reports, highlighting their role in providing stakeholders with crucial financial information. The core of the report focuses on preparing income statements using both absorption and marginal costing methods, comparing their differences, and analyzing their impact on profitability. It also delves into the pros and cons of budgetary control tools and discusses the application of management accounting systems to resolve financial problems, concluding with a discussion on the benefits of effective management accounting. The report includes detailed illustrations of income statements and working notes to support its findings.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Evaluation of management accounting and significant needs of different kinds of this

system..........................................................................................................................................1

P2 Analysis of methods that are for reporting of management accounting ...............................3

TASK 2............................................................................................................................................4

P3 Preparation of statement of income of absorption and marginal costing and analyse the

difference.....................................................................................................................................4

Difference between both the management accounting methods.................................................8

TASK 3............................................................................................................................................9

P4 Analysis of pros and cons of various tools used in budgetary control...................................9

TASK 4..........................................................................................................................................10

P5 Use of management accounting system for the resolution of financial problems...............10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Illustration Index

Illustration 1: Income statement on the basis of absorption costing................................................5

Illustration 2: Income statement on the basis of marginal costing...................................................6

Illustration 3: Working notes...........................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Evaluation of management accounting and significant needs of different kinds of this

system..........................................................................................................................................1

P2 Analysis of methods that are for reporting of management accounting ...............................3

TASK 2............................................................................................................................................4

P3 Preparation of statement of income of absorption and marginal costing and analyse the

difference.....................................................................................................................................4

Difference between both the management accounting methods.................................................8

TASK 3............................................................................................................................................9

P4 Analysis of pros and cons of various tools used in budgetary control...................................9

TASK 4..........................................................................................................................................10

P5 Use of management accounting system for the resolution of financial problems...............10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Illustration Index

Illustration 1: Income statement on the basis of absorption costing................................................5

Illustration 2: Income statement on the basis of marginal costing...................................................6

Illustration 3: Working notes...........................................................................................................7

INTRODUCTION

Accounting is the process which help organization company to make the reports and

different type of statement of financial transaction by using various standards. We can easily

measure its performance and find out the problems in the relation to the profit and expenses. In

this report we are analysing the management accounting of RL Maynard which is one of the

leading organization operating in the manufacturing industry. In this report we have taken

different approaches to identify the managing the financial problem. Income statement is most

significant and effective statement that is created to determine the firms' financial profitability

situation at end of particular year or specific period that is being mentioned in the report.

TASK 1

P1 Evaluation of management accounting and significant needs of different kinds of this system.

It is considered as an system of accounting that involves a continuous process of

analysing the costs and business data for the preparation of various financial reports, journals and

accounts in order to provide assistance to managers in decisions making (Cinquini and Tenucci,

2010). It is also recognised as evaluation of financial data of business for converting in to useful

information by preparing multiple reports that helps the management to analyse the actual

financial position of enterprise. In the context, analysis of RL Maynard limited is done as

accounting officer to analyse the financial position of firms in the construction industry. Various

types of systems and approaches of management accounting are considered that must be utilized

by the cited firm to manage the business operations and achieve a continuous growth in industry.

Following are the essential needs of management accounting system which are followed by the

cited firm such as:

Traditional cost accounting: Most essential system that used is by the management for

the allocation of manufacturing cost of products that are to be developed. It is also

considered as conventional method designed to analyse the direct and indirect expenses

on the work which has to be accomplished by the firm (Nandan, 2010). In this system,

allocation of production overhead cost of the products that has to be developed by firm in

their premises. In this context, it has been recognised that the most of the firms operating

in manufacturing sector used this system of analysing the cost, like RL Maynard. Mainly

it includes the distribution of indirect cost in production unit over the manufactured

units. It involves two other system of accounting that such as job costing and process

1

Accounting is the process which help organization company to make the reports and

different type of statement of financial transaction by using various standards. We can easily

measure its performance and find out the problems in the relation to the profit and expenses. In

this report we are analysing the management accounting of RL Maynard which is one of the

leading organization operating in the manufacturing industry. In this report we have taken

different approaches to identify the managing the financial problem. Income statement is most

significant and effective statement that is created to determine the firms' financial profitability

situation at end of particular year or specific period that is being mentioned in the report.

TASK 1

P1 Evaluation of management accounting and significant needs of different kinds of this system.

It is considered as an system of accounting that involves a continuous process of

analysing the costs and business data for the preparation of various financial reports, journals and

accounts in order to provide assistance to managers in decisions making (Cinquini and Tenucci,

2010). It is also recognised as evaluation of financial data of business for converting in to useful

information by preparing multiple reports that helps the management to analyse the actual

financial position of enterprise. In the context, analysis of RL Maynard limited is done as

accounting officer to analyse the financial position of firms in the construction industry. Various

types of systems and approaches of management accounting are considered that must be utilized

by the cited firm to manage the business operations and achieve a continuous growth in industry.

Following are the essential needs of management accounting system which are followed by the

cited firm such as:

Traditional cost accounting: Most essential system that used is by the management for

the allocation of manufacturing cost of products that are to be developed. It is also

considered as conventional method designed to analyse the direct and indirect expenses

on the work which has to be accomplished by the firm (Nandan, 2010). In this system,

allocation of production overhead cost of the products that has to be developed by firm in

their premises. In this context, it has been recognised that the most of the firms operating

in manufacturing sector used this system of analysing the cost, like RL Maynard. Mainly

it includes the distribution of indirect cost in production unit over the manufactured

units. It involves two other system of accounting that such as job costing and process

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing that helps the firm to analyse the expenses that are to be done made on

development of particular unit.

Transfer pricing: It is also significant process that is used to allocate the cost of

transferring the goods from the holding firm to the subsidiary enterprise. It also

recognised as the expenses that are incurred by the parent company on the transfer of

goods to other host company (Angelakis, Theriou, and Floropoulos, 2010). In present

context, cost of variables and opportunity cost mainly incurred by cited firm on transfer

of particular product or services. Firms use this method of pricing to reduce the cost of

raw material is to be utilized in process of manufacturing the units. Cost of variable is

depended on the unit of production and the opportunity is that amount which the firm has

to bear at the time of outsourcing of goods to the subsidiary company.

Accounting of cost: It is also considered as a suitable frame work that is utilized by the

firms to analyse the overall cots of manufacturing a unit. It is most suitable method of

accounting that should be considered to analyse the data of cost to be incurred by the

cited business entity at level of operations. Along with this, it can also consider as

suitable for them to reduce the high expenses on the manufacturing of units.

System of price optimization: Another system that is considered as essential for cited to

analyse the response of potential buyers towards different possible cost of units

manufactured ( Bebbington and Thomson, 2013). In this context, this system of

accounting is mainly used by RL Maynard for the optimization of cost that must be

suitable for customer.

Accounting for inventory: Essential system of accounting utilised by the managers to

analyse the raw material that is available at the factory premises in order to meet the

requirement in the future. Further, it can be said that it is beneficial for authorities to

manage the inventory and provide the information about the future needs.

P2 Analysis of methods that are for reporting of management accounting

In the competitive business environment, is essential for the firms manage theeir funds

appropriately in order to meet the future requirements (DRURY, 2013). For the generation of

funds, they have determined the actual position of business to its stakeholders and they will

provide information by using various accounting reports. Following are the essential reports that

are to be formulated and combined with the financial statements by R.L Maynard such as:

2

development of particular unit.

Transfer pricing: It is also significant process that is used to allocate the cost of

transferring the goods from the holding firm to the subsidiary enterprise. It also

recognised as the expenses that are incurred by the parent company on the transfer of

goods to other host company (Angelakis, Theriou, and Floropoulos, 2010). In present

context, cost of variables and opportunity cost mainly incurred by cited firm on transfer

of particular product or services. Firms use this method of pricing to reduce the cost of

raw material is to be utilized in process of manufacturing the units. Cost of variable is

depended on the unit of production and the opportunity is that amount which the firm has

to bear at the time of outsourcing of goods to the subsidiary company.

Accounting of cost: It is also considered as a suitable frame work that is utilized by the

firms to analyse the overall cots of manufacturing a unit. It is most suitable method of

accounting that should be considered to analyse the data of cost to be incurred by the

cited business entity at level of operations. Along with this, it can also consider as

suitable for them to reduce the high expenses on the manufacturing of units.

System of price optimization: Another system that is considered as essential for cited to

analyse the response of potential buyers towards different possible cost of units

manufactured ( Bebbington and Thomson, 2013). In this context, this system of

accounting is mainly used by RL Maynard for the optimization of cost that must be

suitable for customer.

Accounting for inventory: Essential system of accounting utilised by the managers to

analyse the raw material that is available at the factory premises in order to meet the

requirement in the future. Further, it can be said that it is beneficial for authorities to

manage the inventory and provide the information about the future needs.

P2 Analysis of methods that are for reporting of management accounting

In the competitive business environment, is essential for the firms manage theeir funds

appropriately in order to meet the future requirements (DRURY, 2013). For the generation of

funds, they have determined the actual position of business to its stakeholders and they will

provide information by using various accounting reports. Following are the essential reports that

are to be formulated and combined with the financial statements by R.L Maynard such as:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reports of production: In this particular report, the firms has to keep the records and

data which is related to the development of goods and services. In this context, the cited

firm also use this method to determine the cost of manufacturing the units to its

stakeholders.

Reports of budget: It helps the owners of small business enterprise to analyse their

performance of their company and managers will also measure the performance of its

departments and control the cost (Abdel-Kader, 2011). Firms expected budget for a

particular time is always supported on the actual expenses from the preceding year.

Payroll report: In the organization, this reports mainly consists of the cost that is

incurred by the firms on its workforce. This accounting report allocates the information

of employee's compensation that clearly describes the current financial position to the RL

Maynard. Further, with this managers will able to recognise the firm's ability to pay the

compensation to its employees in the future. Information this report mainly utilized by

the firms to reduce the expenditure of company on its employees and evaluate the

employee performance at workplace.

Job costing report: In the manufacturing sector, there are different stages that is used by

firms to develop the products and services ( Cuganesan, Dunford and Palmer, 2012). In

this context, there are various types of cost that are associated with the manufacturing of

units that are considered as expenditure. With this report, managers of the cited SME

will analyse the expenses that are incurred to develop a single unit and paid to different

personnel for development. It helps the firm to identify the profitability so that they can

focus on the development of that unit.

Report of sales: Another significant reports which is formulated to analyse the variations

in the sales of enterprise and analyse the profitability that is to be earned by business. In

this context, this report will help the managers of the enterprise to analyse the revenue

that generated after the construction of various units.

Account receivable report: It is considered as critical tool that is utilised to manage the

cash flow for the firms that provides credit to their customers. In this context, this report

is developed to keep the data and record of amount on invoices that are received from the

customers. It will provide information to authorities about the amount which they have to

take from the client's.

3

data which is related to the development of goods and services. In this context, the cited

firm also use this method to determine the cost of manufacturing the units to its

stakeholders.

Reports of budget: It helps the owners of small business enterprise to analyse their

performance of their company and managers will also measure the performance of its

departments and control the cost (Abdel-Kader, 2011). Firms expected budget for a

particular time is always supported on the actual expenses from the preceding year.

Payroll report: In the organization, this reports mainly consists of the cost that is

incurred by the firms on its workforce. This accounting report allocates the information

of employee's compensation that clearly describes the current financial position to the RL

Maynard. Further, with this managers will able to recognise the firm's ability to pay the

compensation to its employees in the future. Information this report mainly utilized by

the firms to reduce the expenditure of company on its employees and evaluate the

employee performance at workplace.

Job costing report: In the manufacturing sector, there are different stages that is used by

firms to develop the products and services ( Cuganesan, Dunford and Palmer, 2012). In

this context, there are various types of cost that are associated with the manufacturing of

units that are considered as expenditure. With this report, managers of the cited SME

will analyse the expenses that are incurred to develop a single unit and paid to different

personnel for development. It helps the firm to identify the profitability so that they can

focus on the development of that unit.

Report of sales: Another significant reports which is formulated to analyse the variations

in the sales of enterprise and analyse the profitability that is to be earned by business. In

this context, this report will help the managers of the enterprise to analyse the revenue

that generated after the construction of various units.

Account receivable report: It is considered as critical tool that is utilised to manage the

cash flow for the firms that provides credit to their customers. In this context, this report

is developed to keep the data and record of amount on invoices that are received from the

customers. It will provide information to authorities about the amount which they have to

take from the client's.

3

M1

Below given are the benefits of management accounting system:

Reduce cost: It enables to reduce operational expenses for companies like R.L. Maynard.

Managers make use of accounting information to review cost of economic resources and other

operations related to business. Management accounting reduces various direct and indirect

expanses of the organisation in effective and efficient way. These expenses include sales

expenses, production expenses, raw materials expanses, etc.

Improves flow of funds: Budget is used by business owners of R.L. Maynard Ltd. to have

financial road map for the business expenditure in the future. Management accounting helps to

improve the flow of cash in organisation. By implementing effective accounting technique and

cost budgeting, cash flow improves in the organisation.

TASK 2

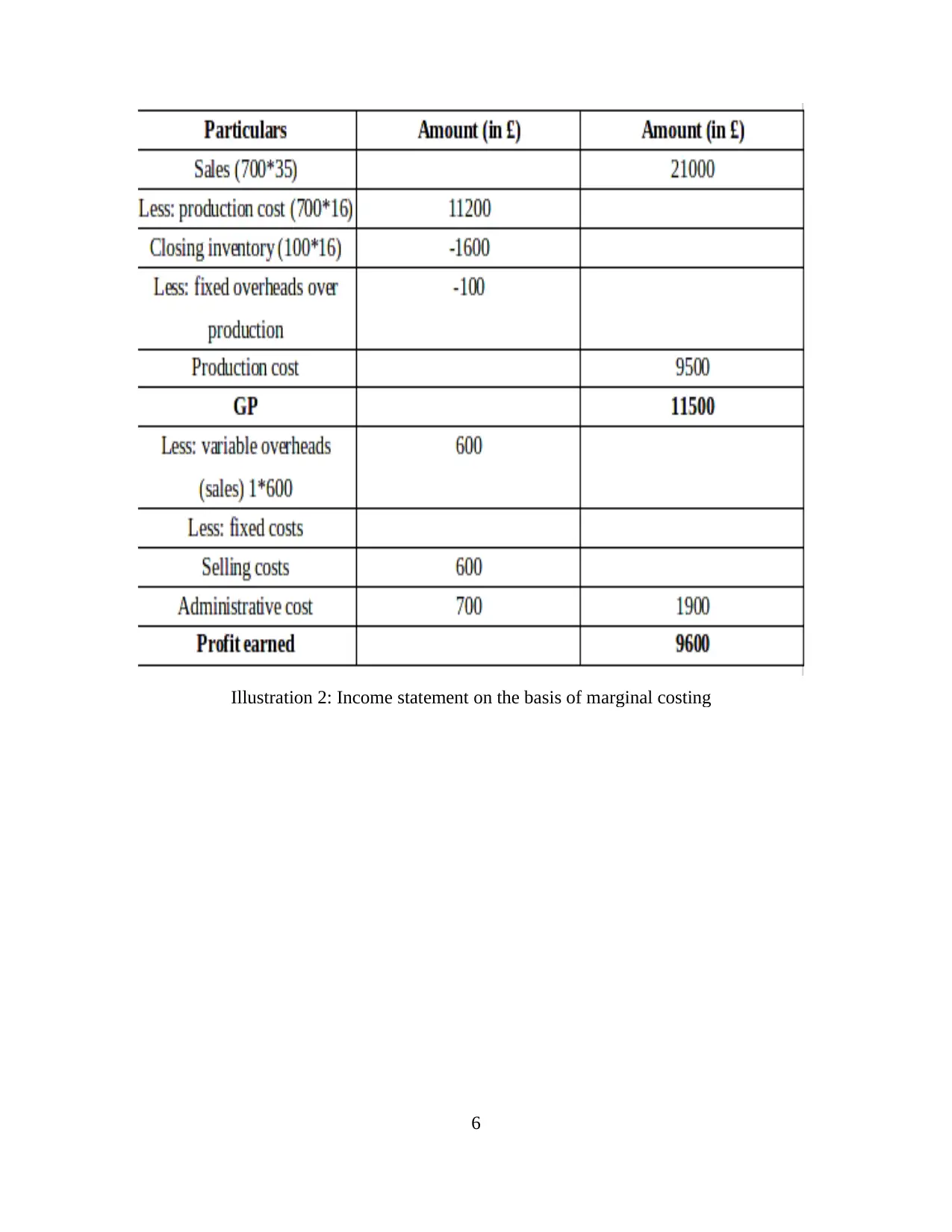

P3 Preparation of statement of income of absorption and marginal costing and analyse the

difference.

Income statement is most significant and effective statement that is created to determine

the firms' financial profitability situation at end of particular year or specific period that is being

mentioned in the report (Burritt and Schaltegger, 2010). In this context, this statement has been

created to analyse the situations of profitability of RL Maynard to understand the competency of

the firm to manage its expenses.

There are various methods that must be utilized by firm to manage its revenues and expenses.

This statement has been prepared on the basis of two methods i.e. marginal and absorption

costing which is determined below:

4

Below given are the benefits of management accounting system:

Reduce cost: It enables to reduce operational expenses for companies like R.L. Maynard.

Managers make use of accounting information to review cost of economic resources and other

operations related to business. Management accounting reduces various direct and indirect

expanses of the organisation in effective and efficient way. These expenses include sales

expenses, production expenses, raw materials expanses, etc.

Improves flow of funds: Budget is used by business owners of R.L. Maynard Ltd. to have

financial road map for the business expenditure in the future. Management accounting helps to

improve the flow of cash in organisation. By implementing effective accounting technique and

cost budgeting, cash flow improves in the organisation.

TASK 2

P3 Preparation of statement of income of absorption and marginal costing and analyse the

difference.

Income statement is most significant and effective statement that is created to determine

the firms' financial profitability situation at end of particular year or specific period that is being

mentioned in the report (Burritt and Schaltegger, 2010). In this context, this statement has been

created to analyse the situations of profitability of RL Maynard to understand the competency of

the firm to manage its expenses.

There are various methods that must be utilized by firm to manage its revenues and expenses.

This statement has been prepared on the basis of two methods i.e. marginal and absorption

costing which is determined below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5

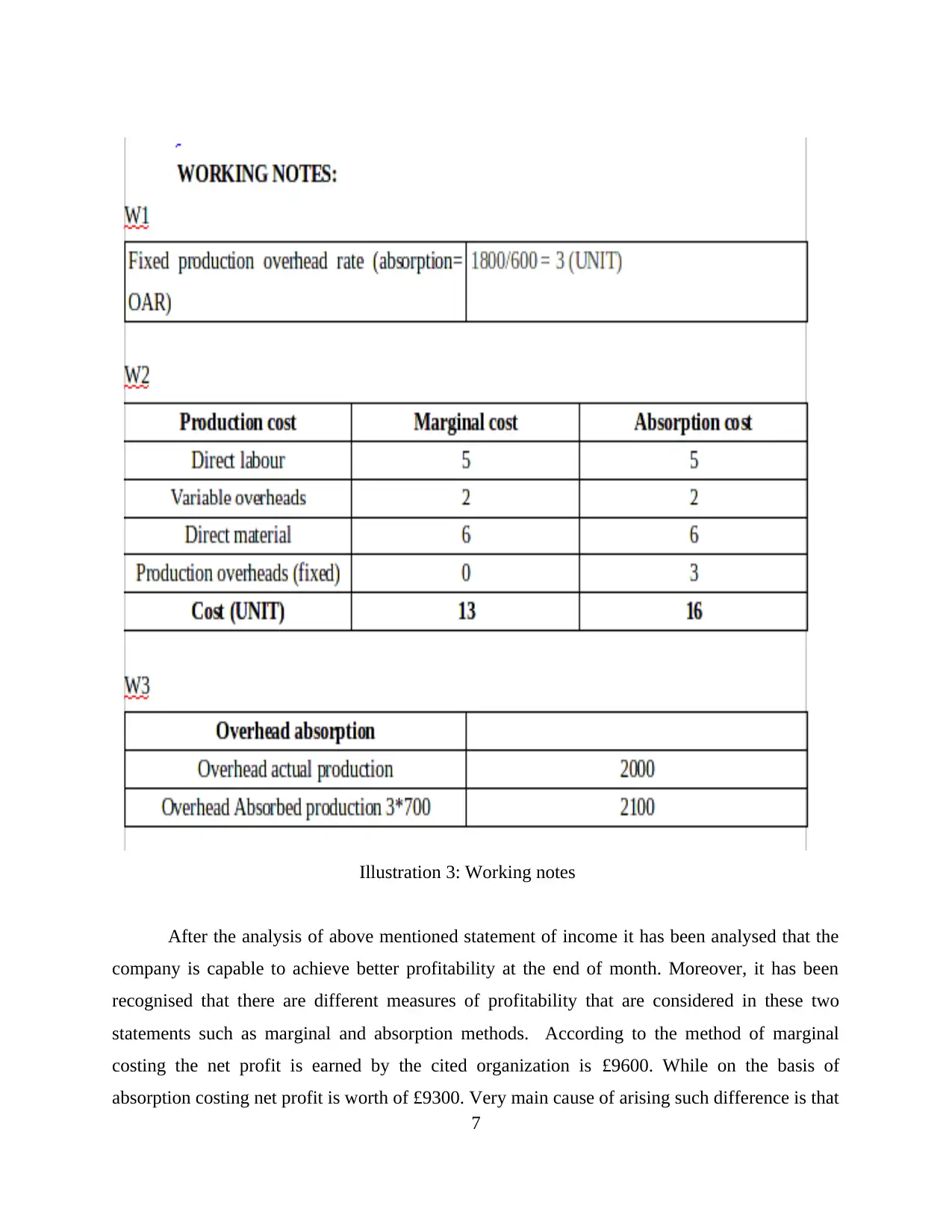

Illustration 1: Income statement on the basis of absorption costing

Illustration 1: Income statement on the basis of absorption costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

Illustration 2: Income statement on the basis of marginal costing

Illustration 2: Income statement on the basis of marginal costing

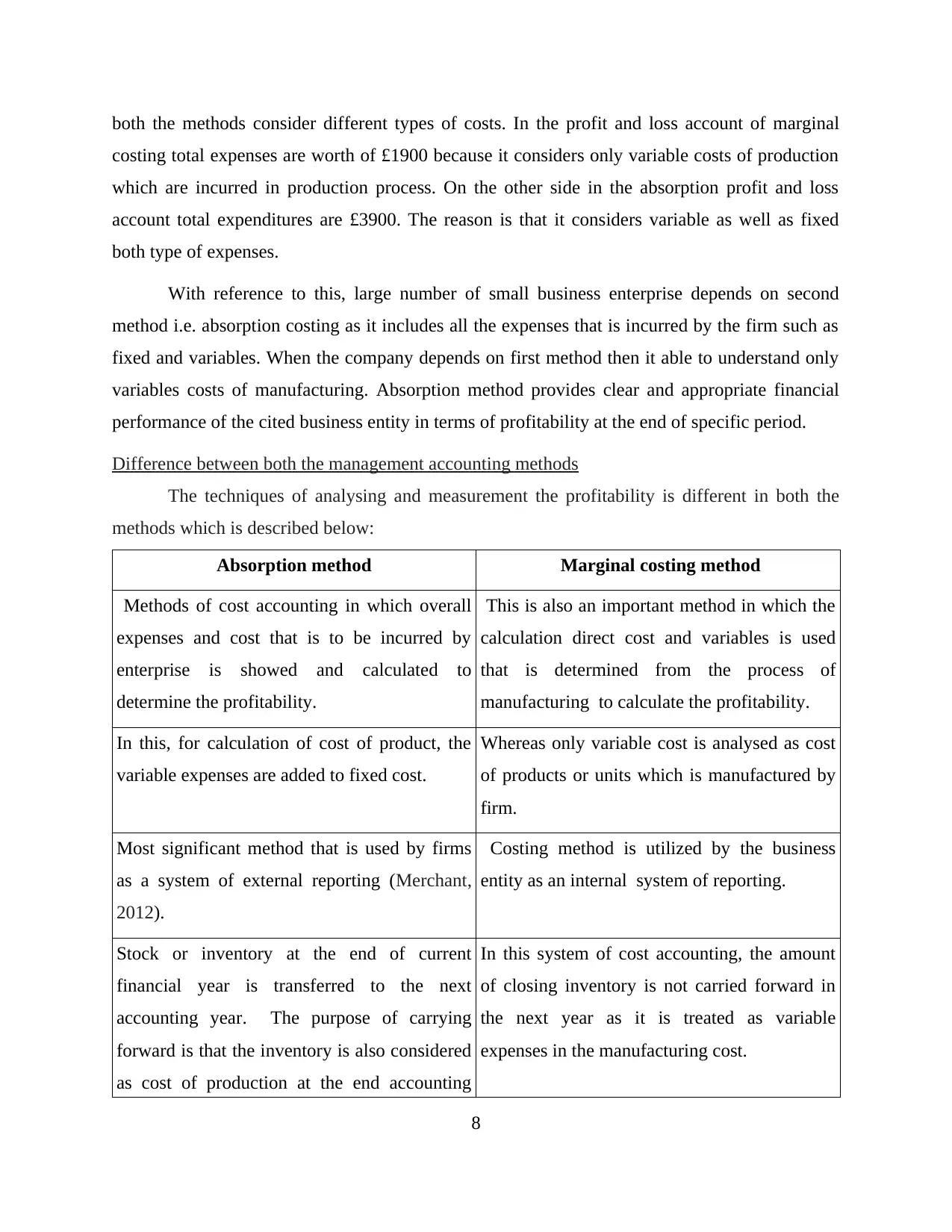

After the analysis of above mentioned statement of income it has been analysed that the

company is capable to achieve better profitability at the end of month. Moreover, it has been

recognised that there are different measures of profitability that are considered in these two

statements such as marginal and absorption methods. According to the method of marginal

costing the net profit is earned by the cited organization is £9600. While on the basis of

absorption costing net profit is worth of £9300. Very main cause of arising such difference is that

7

Illustration 3: Working notes

company is capable to achieve better profitability at the end of month. Moreover, it has been

recognised that there are different measures of profitability that are considered in these two

statements such as marginal and absorption methods. According to the method of marginal

costing the net profit is earned by the cited organization is £9600. While on the basis of

absorption costing net profit is worth of £9300. Very main cause of arising such difference is that

7

Illustration 3: Working notes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

both the methods consider different types of costs. In the profit and loss account of marginal

costing total expenses are worth of £1900 because it considers only variable costs of production

which are incurred in production process. On the other side in the absorption profit and loss

account total expenditures are £3900. The reason is that it considers variable as well as fixed

both type of expenses.

With reference to this, large number of small business enterprise depends on second

method i.e. absorption costing as it includes all the expenses that is incurred by the firm such as

fixed and variables. When the company depends on first method then it able to understand only

variables costs of manufacturing. Absorption method provides clear and appropriate financial

performance of the cited business entity in terms of profitability at the end of specific period.

Difference between both the management accounting methods

The techniques of analysing and measurement the profitability is different in both the

methods which is described below:

Absorption method Marginal costing method

Methods of cost accounting in which overall

expenses and cost that is to be incurred by

enterprise is showed and calculated to

determine the profitability.

This is also an important method in which the

calculation direct cost and variables is used

that is determined from the process of

manufacturing to calculate the profitability.

In this, for calculation of cost of product, the

variable expenses are added to fixed cost.

Whereas only variable cost is analysed as cost

of products or units which is manufactured by

firm.

Most significant method that is used by firms

as a system of external reporting (Merchant,

2012).

Costing method is utilized by the business

entity as an internal system of reporting.

Stock or inventory at the end of current

financial year is transferred to the next

accounting year. The purpose of carrying

forward is that the inventory is also considered

as cost of production at the end accounting

In this system of cost accounting, the amount

of closing inventory is not carried forward in

the next year as it is treated as variable

expenses in the manufacturing cost.

8

costing total expenses are worth of £1900 because it considers only variable costs of production

which are incurred in production process. On the other side in the absorption profit and loss

account total expenditures are £3900. The reason is that it considers variable as well as fixed

both type of expenses.

With reference to this, large number of small business enterprise depends on second

method i.e. absorption costing as it includes all the expenses that is incurred by the firm such as

fixed and variables. When the company depends on first method then it able to understand only

variables costs of manufacturing. Absorption method provides clear and appropriate financial

performance of the cited business entity in terms of profitability at the end of specific period.

Difference between both the management accounting methods

The techniques of analysing and measurement the profitability is different in both the

methods which is described below:

Absorption method Marginal costing method

Methods of cost accounting in which overall

expenses and cost that is to be incurred by

enterprise is showed and calculated to

determine the profitability.

This is also an important method in which the

calculation direct cost and variables is used

that is determined from the process of

manufacturing to calculate the profitability.

In this, for calculation of cost of product, the

variable expenses are added to fixed cost.

Whereas only variable cost is analysed as cost

of products or units which is manufactured by

firm.

Most significant method that is used by firms

as a system of external reporting (Merchant,

2012).

Costing method is utilized by the business

entity as an internal system of reporting.

Stock or inventory at the end of current

financial year is transferred to the next

accounting year. The purpose of carrying

forward is that the inventory is also considered

as cost of production at the end accounting

In this system of cost accounting, the amount

of closing inventory is not carried forward in

the next year as it is treated as variable

expenses in the manufacturing cost.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

year.

Net probability is usually low in comparison to

the other as all the cost of fixed and variable

expenses are considered in this system.

As compared to other, the amount of profit is

high as all the expenses are not considered for

the calculation.

M2

There are different type of management accounting system some of them are as follows:

Capital fund: This can be determined to be the techniques or the process through which

business plans for their long term investment. Business entity is able to plan their future so that

they will be able to make investment for their business. Capital budgets are maintained and

documented by the finance and account manager of the organization efficiently.

Ratio analysis: It is beneficial for Cited firm to make evaluation of various aspects of

financial performance and operations. In this context, it includes liquidity, solvency, etc.

There are financial reporting documents that are helpful for the firm to determine the

business position. In this context it consists of profit and loss account, balance sheet in which

assets and liability are determined.

TASK 3

P4 Analysis of pros and cons of various tools used in budgetary control.

In the present competitive scenario, there are various ways that are used by the firms to

reduce their different expenses of manufacturing through raising the sales revenue and

probability by controlling the budget (Jansen, 2011). It is also analysed as one of the most

significant aspects that will helps the firm to develop control the cost that is to be incurred on

production of various units. In this context, there are various techniques and tools have been

analysed that is utilized by the RL Maynard such as:

Ratio analysis: Most significant tool that is utilized by various SMEs for the calculation

and interpretation of their financial statements (Tools and techniques of Management

Accounting, 2017). In this technique, different types of ratios have been calculated and

used to analysed the sales and revenue generated by firm. Various information and data

has been gathered from the accounting statements such as cash flow, balance sheet and

9

Net probability is usually low in comparison to

the other as all the cost of fixed and variable

expenses are considered in this system.

As compared to other, the amount of profit is

high as all the expenses are not considered for

the calculation.

M2

There are different type of management accounting system some of them are as follows:

Capital fund: This can be determined to be the techniques or the process through which

business plans for their long term investment. Business entity is able to plan their future so that

they will be able to make investment for their business. Capital budgets are maintained and

documented by the finance and account manager of the organization efficiently.

Ratio analysis: It is beneficial for Cited firm to make evaluation of various aspects of

financial performance and operations. In this context, it includes liquidity, solvency, etc.

There are financial reporting documents that are helpful for the firm to determine the

business position. In this context it consists of profit and loss account, balance sheet in which

assets and liability are determined.

TASK 3

P4 Analysis of pros and cons of various tools used in budgetary control.

In the present competitive scenario, there are various ways that are used by the firms to

reduce their different expenses of manufacturing through raising the sales revenue and

probability by controlling the budget (Jansen, 2011). It is also analysed as one of the most

significant aspects that will helps the firm to develop control the cost that is to be incurred on

production of various units. In this context, there are various techniques and tools have been

analysed that is utilized by the RL Maynard such as:

Ratio analysis: Most significant tool that is utilized by various SMEs for the calculation

and interpretation of their financial statements (Tools and techniques of Management

Accounting, 2017). In this technique, different types of ratios have been calculated and

used to analysed the sales and revenue generated by firm. Various information and data

has been gathered from the accounting statements such as cash flow, balance sheet and

9

profit and loss statement etc. These ratios will help the managers to determine the amount

of the debtors and equity for the analysis in order to calculate the profitability.

Merits of ratio analysis:

Helps the firm to analyse the variations in the performance and profitability of present

year in the manufacturing industry of UK.

Beneficial toward the formulation of budget in the organisation as it is based on the

previous analysis of performance.

Provides an assistance to the firm in taking various financial and business decisions in

order to achieve growth in profitability and market position.

Also, considered as beneficial towards the reduction of expenses in production.

Allows the cited firm to compare the financial position from its competitors regulating in

the same industry (Sánchez-Rodríguez and Spraakman, 2012).

Demerits of ratio analysis:

Lack of financial data and information is the main drawback of ratio analysis.

Various tools and techniques are not considered in this method to analyse the market

performance of enterprise.

The standards that are analysed by the management in this are different in each ratio

therefore actual performance is not calculated every time.

Budget: It is also a financial similar as other that is commonly used by various firms to manage

their revenues and cost. It is also determined as one of the most important toll that is taken in

consideration to calculate the performance of previous years and the budget for the maximization

of profits (Parker, 2012). In this context, various different methods have utilized by the RL

Maynard to formulate the statement of budget. There are various types of budgets have been

calculated and made with the help of financial statement.

Merits of budget:

Helps in achievement of financial goal as the organization will formulate various long

term and short term objectives and analyse accurate financial statement.

It also helps the RL Maynard in to allocate the funds and resources for every functional

activity in effective manner (DRURY, 2013).

Helps the firm to develop effective strategies and take decisions to raise their customers.

10

of the debtors and equity for the analysis in order to calculate the profitability.

Merits of ratio analysis:

Helps the firm to analyse the variations in the performance and profitability of present

year in the manufacturing industry of UK.

Beneficial toward the formulation of budget in the organisation as it is based on the

previous analysis of performance.

Provides an assistance to the firm in taking various financial and business decisions in

order to achieve growth in profitability and market position.

Also, considered as beneficial towards the reduction of expenses in production.

Allows the cited firm to compare the financial position from its competitors regulating in

the same industry (Sánchez-Rodríguez and Spraakman, 2012).

Demerits of ratio analysis:

Lack of financial data and information is the main drawback of ratio analysis.

Various tools and techniques are not considered in this method to analyse the market

performance of enterprise.

The standards that are analysed by the management in this are different in each ratio

therefore actual performance is not calculated every time.

Budget: It is also a financial similar as other that is commonly used by various firms to manage

their revenues and cost. It is also determined as one of the most important toll that is taken in

consideration to calculate the performance of previous years and the budget for the maximization

of profits (Parker, 2012). In this context, various different methods have utilized by the RL

Maynard to formulate the statement of budget. There are various types of budgets have been

calculated and made with the help of financial statement.

Merits of budget:

Helps in achievement of financial goal as the organization will formulate various long

term and short term objectives and analyse accurate financial statement.

It also helps the RL Maynard in to allocate the funds and resources for every functional

activity in effective manner (DRURY, 2013).

Helps the firm to develop effective strategies and take decisions to raise their customers.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.