Financial Analysis for Managers: Project and Ratio Analysis Homework

VerifiedAdded on 2022/08/11

|10

|1870

|26

Homework Assignment

AI Summary

This financial analysis assignment evaluates two proposed expansion projects (Taxi and Travel applications) using Net Present Value (NPV) and payback period methods, considering a 14% cost of capital. The analysis determines the most financially viable project based on these metrics, with the Taxi application project being favored due to its higher NPV and a reasonable payback period. Furthermore, the assignment includes a ratio analysis of Abdullah Software, examining liquidity and profitability ratios for the years 2016 and 2017. The analysis reveals declining liquidity and profitability, highlighting the need for strategic improvements. Finally, the assignment discusses the merits and demerits of investment appraisal techniques, such as NPV and payback period, and the advantages and challenges of big data applications in the airline industry, along with challenges and solutions for database management.

Running Head: ACCOUNTING 1

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

Contents

Question 1)..................................................................................................................................................3

A)............................................................................................................................................................3

b).............................................................................................................................................................4

c).............................................................................................................................................................4

Question 2)..................................................................................................................................................5

a).............................................................................................................................................................5

b).............................................................................................................................................................6

c).............................................................................................................................................................7

Database Model Questions..........................................................................................................................8

Question 1...................................................................................................................................................8

Question 3...................................................................................................................................................9

Question 4...................................................................................................................................................9

References.................................................................................................................................................10

Contents

Question 1)..................................................................................................................................................3

A)............................................................................................................................................................3

b).............................................................................................................................................................4

c).............................................................................................................................................................4

Question 2)..................................................................................................................................................5

a).............................................................................................................................................................5

b).............................................................................................................................................................6

c).............................................................................................................................................................7

Database Model Questions..........................................................................................................................8

Question 1...................................................................................................................................................8

Question 3...................................................................................................................................................9

Question 4...................................................................................................................................................9

References.................................................................................................................................................10

ACCOUNTING

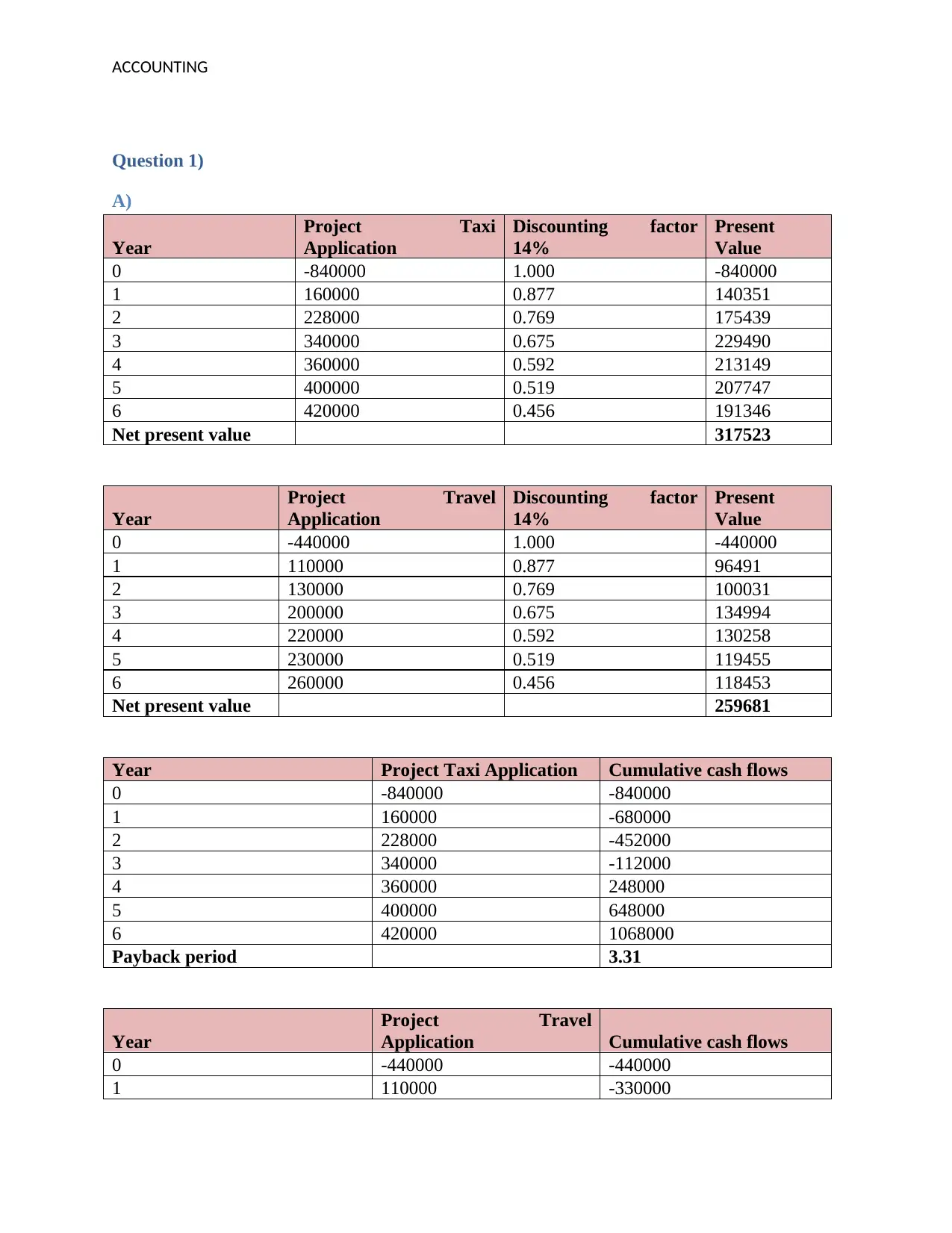

Question 1)

A)

Year

Project Taxi

Application

Discounting factor

14%

Present

Value

0 -840000 1.000 -840000

1 160000 0.877 140351

2 228000 0.769 175439

3 340000 0.675 229490

4 360000 0.592 213149

5 400000 0.519 207747

6 420000 0.456 191346

Net present value 317523

Year

Project Travel

Application

Discounting factor

14%

Present

Value

0 -440000 1.000 -440000

1 110000 0.877 96491

2 130000 0.769 100031

3 200000 0.675 134994

4 220000 0.592 130258

5 230000 0.519 119455

6 260000 0.456 118453

Net present value 259681

Year Project Taxi Application Cumulative cash flows

0 -840000 -840000

1 160000 -680000

2 228000 -452000

3 340000 -112000

4 360000 248000

5 400000 648000

6 420000 1068000

Payback period 3.31

Year

Project Travel

Application Cumulative cash flows

0 -440000 -440000

1 110000 -330000

Question 1)

A)

Year

Project Taxi

Application

Discounting factor

14%

Present

Value

0 -840000 1.000 -840000

1 160000 0.877 140351

2 228000 0.769 175439

3 340000 0.675 229490

4 360000 0.592 213149

5 400000 0.519 207747

6 420000 0.456 191346

Net present value 317523

Year

Project Travel

Application

Discounting factor

14%

Present

Value

0 -440000 1.000 -440000

1 110000 0.877 96491

2 130000 0.769 100031

3 200000 0.675 134994

4 220000 0.592 130258

5 230000 0.519 119455

6 260000 0.456 118453

Net present value 259681

Year Project Taxi Application Cumulative cash flows

0 -840000 -840000

1 160000 -680000

2 228000 -452000

3 340000 -112000

4 360000 248000

5 400000 648000

6 420000 1068000

Payback period 3.31

Year

Project Travel

Application Cumulative cash flows

0 -440000 -440000

1 110000 -330000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING

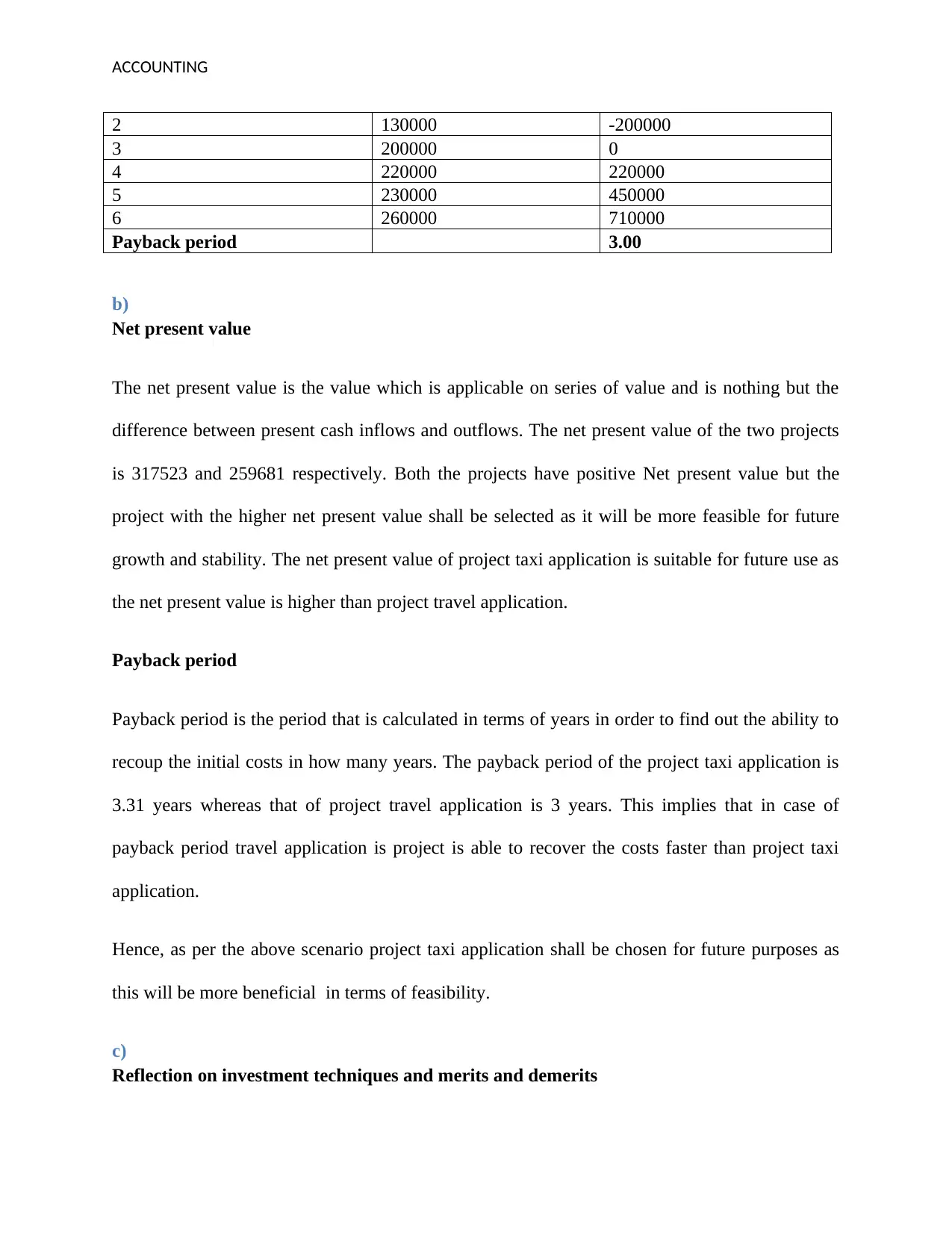

2 130000 -200000

3 200000 0

4 220000 220000

5 230000 450000

6 260000 710000

Payback period 3.00

b)

Net present value

The net present value is the value which is applicable on series of value and is nothing but the

difference between present cash inflows and outflows. The net present value of the two projects

is 317523 and 259681 respectively. Both the projects have positive Net present value but the

project with the higher net present value shall be selected as it will be more feasible for future

growth and stability. The net present value of project taxi application is suitable for future use as

the net present value is higher than project travel application.

Payback period

Payback period is the period that is calculated in terms of years in order to find out the ability to

recoup the initial costs in how many years. The payback period of the project taxi application is

3.31 years whereas that of project travel application is 3 years. This implies that in case of

payback period travel application is project is able to recover the costs faster than project taxi

application.

Hence, as per the above scenario project taxi application shall be chosen for future purposes as

this will be more beneficial in terms of feasibility.

c)

Reflection on investment techniques and merits and demerits

2 130000 -200000

3 200000 0

4 220000 220000

5 230000 450000

6 260000 710000

Payback period 3.00

b)

Net present value

The net present value is the value which is applicable on series of value and is nothing but the

difference between present cash inflows and outflows. The net present value of the two projects

is 317523 and 259681 respectively. Both the projects have positive Net present value but the

project with the higher net present value shall be selected as it will be more feasible for future

growth and stability. The net present value of project taxi application is suitable for future use as

the net present value is higher than project travel application.

Payback period

Payback period is the period that is calculated in terms of years in order to find out the ability to

recoup the initial costs in how many years. The payback period of the project taxi application is

3.31 years whereas that of project travel application is 3 years. This implies that in case of

payback period travel application is project is able to recover the costs faster than project taxi

application.

Hence, as per the above scenario project taxi application shall be chosen for future purposes as

this will be more beneficial in terms of feasibility.

c)

Reflection on investment techniques and merits and demerits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

The investment appraisal techniques as described earlier are net present value and payback

period. According to Baucells & Bodily, (2018), the net present value method takes the

assumption of the reinvestment. Further this process also accepts the conventional cash flow

pattern to implement the net present value. Since this method is a good source of measuring the

profitability it is a useful technique of the capital budgeting techniques. On the other hand there

are some cons which are associated with the net present value method such as it might not boost

the ROE or EPS of the company. This concept also ignores the sunk cost and hence there are

certain advantages and disadvantage associated with this process.

In case of payback period, it helps in revealing the period of an investment and since it is a

simple method to use, it is used by most of the companies in today’s scenario. The information

of the payback is crucial for defining the liquidity position of the company and hence, it is also

one of the important techniques. However, this methodology is not useful for long term projects

as it ignores the concept of time value of money. All the cash flows are not covered and hence,

the true results are not depicted at times.

Question 2)

a)

Calculation of ratios

Liquidity ratios 2016 2017 2016 2017

Current Ratio

Current Assets 1088 1358 1.850 1.572

Current Liabilities 588 864

Quick Ratio

Quick Assets 488 546 0.830 0.632

Current liabilities 588 864

The investment appraisal techniques as described earlier are net present value and payback

period. According to Baucells & Bodily, (2018), the net present value method takes the

assumption of the reinvestment. Further this process also accepts the conventional cash flow

pattern to implement the net present value. Since this method is a good source of measuring the

profitability it is a useful technique of the capital budgeting techniques. On the other hand there

are some cons which are associated with the net present value method such as it might not boost

the ROE or EPS of the company. This concept also ignores the sunk cost and hence there are

certain advantages and disadvantage associated with this process.

In case of payback period, it helps in revealing the period of an investment and since it is a

simple method to use, it is used by most of the companies in today’s scenario. The information

of the payback is crucial for defining the liquidity position of the company and hence, it is also

one of the important techniques. However, this methodology is not useful for long term projects

as it ignores the concept of time value of money. All the cash flows are not covered and hence,

the true results are not depicted at times.

Question 2)

a)

Calculation of ratios

Liquidity ratios 2016 2017 2016 2017

Current Ratio

Current Assets 1088 1358 1.850 1.572

Current Liabilities 588 864

Quick Ratio

Quick Assets 488 546 0.830 0.632

Current liabilities 588 864

ACCOUNTING

Profitability ratios

Net profit margin 2016 2017 2016 2017

Net Profit 330 22 7.37% 0.41%

Sales 4,480 5,362

Gross profit margin

Gross Profit 990 818 22.10% 15.26%

Net sales 4,480 5,362

Return on equity

Net profit 330 22 29.31% 2.06%

Net equity 1,126 1,068

b)

As per the above scenario it can be seen that the liquidity position of Abdullah software is

declining in comparison to the previous years. The figures state that the current ratio of the

company is 1.85 times and at the same time it decreased to 1.572 times. The current ratio is a

liquidity ratio which is used as a financial metric to define the ability of the company to pay back

the current financial obligations which are due within the period of one year. The quick ratio on

the other hand is a measure of how well the short term liabilities can be settled. Overall the

picture is not smooth as the current ratio as well as quick ratio is declining as the investment in

the current liabilities are more in comparison to the previous year such as from 588 to 864. The

company is not so liquid and it becomes difficult for the company to convert the assets into cash

to pay back the current liabilities.

The profitability ratios are the ratios that are used as a financial measurement to identify how

much profits have been earned by the company with respect to the sales generated. The

profitability of Abdullah software is judged on the basis of net profit margin, gross profit margin

and return on equity. The net profit margin is the total profits available after deducting form the

expenses. The net profit margin fell down drastically from 7.37% to 0.41% whereas the gross

Profitability ratios

Net profit margin 2016 2017 2016 2017

Net Profit 330 22 7.37% 0.41%

Sales 4,480 5,362

Gross profit margin

Gross Profit 990 818 22.10% 15.26%

Net sales 4,480 5,362

Return on equity

Net profit 330 22 29.31% 2.06%

Net equity 1,126 1,068

b)

As per the above scenario it can be seen that the liquidity position of Abdullah software is

declining in comparison to the previous years. The figures state that the current ratio of the

company is 1.85 times and at the same time it decreased to 1.572 times. The current ratio is a

liquidity ratio which is used as a financial metric to define the ability of the company to pay back

the current financial obligations which are due within the period of one year. The quick ratio on

the other hand is a measure of how well the short term liabilities can be settled. Overall the

picture is not smooth as the current ratio as well as quick ratio is declining as the investment in

the current liabilities are more in comparison to the previous year such as from 588 to 864. The

company is not so liquid and it becomes difficult for the company to convert the assets into cash

to pay back the current liabilities.

The profitability ratios are the ratios that are used as a financial measurement to identify how

much profits have been earned by the company with respect to the sales generated. The

profitability of Abdullah software is judged on the basis of net profit margin, gross profit margin

and return on equity. The net profit margin is the total profits available after deducting form the

expenses. The net profit margin fell down drastically from 7.37% to 0.41% whereas the gross

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING

profit margin has also fallen from 22.10% to 15.26%. It is necessary to assess the gross profit as

the company is also concerned with how much profits are generated out of the costs involved in

producing the products and the services. This again resulted in decline of operating profits due to

increase in operating expenses by 40%. Due to the lower profits, the return on equity ratio have

also decreased from 29.31% to 2.06% which implies the shareholders are getting only 2.06% of

what is invested by them. From the overall analysis it can be stated that profitability position is

not smooth and the necessary steps like increase in the prices, prevention of theft and taking the

cash discounts from the suppliers, reduction in labor and also it can be improve by lowering

down the taxes.

c)

Ratio analysis is a technique or term which is used in the financial management to evaluate the

performance of the companies either on the basis of the benchmark or on the basis of the past

year performance. In the above scenario, this technique is applied on Abdullah Software

company where the analysis it done for the financial year 2016-2017. The merits of the ratio

analysis starts with utilizing industry trends as a benchmark, businessman can set time-bound

execution objectives regarding explicit proportions to give financial specialists a look into the

ability of the firm. Ratios can likewise fill in to bring in the strategic change in the organization

and it also furnishes the board with applicable direction and input as proportion valuations move

in light of authoritative changes. Ratio analysis is also bound with certain disadvantages such as

it cannot be used to determine the future performance of the business. When two policies are

being in use by the company than the figures can distort and hence, the results could be different

which are not acceptable for predicting the profitability or liquidity.

profit margin has also fallen from 22.10% to 15.26%. It is necessary to assess the gross profit as

the company is also concerned with how much profits are generated out of the costs involved in

producing the products and the services. This again resulted in decline of operating profits due to

increase in operating expenses by 40%. Due to the lower profits, the return on equity ratio have

also decreased from 29.31% to 2.06% which implies the shareholders are getting only 2.06% of

what is invested by them. From the overall analysis it can be stated that profitability position is

not smooth and the necessary steps like increase in the prices, prevention of theft and taking the

cash discounts from the suppliers, reduction in labor and also it can be improve by lowering

down the taxes.

c)

Ratio analysis is a technique or term which is used in the financial management to evaluate the

performance of the companies either on the basis of the benchmark or on the basis of the past

year performance. In the above scenario, this technique is applied on Abdullah Software

company where the analysis it done for the financial year 2016-2017. The merits of the ratio

analysis starts with utilizing industry trends as a benchmark, businessman can set time-bound

execution objectives regarding explicit proportions to give financial specialists a look into the

ability of the firm. Ratios can likewise fill in to bring in the strategic change in the organization

and it also furnishes the board with applicable direction and input as proportion valuations move

in light of authoritative changes. Ratio analysis is also bound with certain disadvantages such as

it cannot be used to determine the future performance of the business. When two policies are

being in use by the company than the figures can distort and hence, the results could be different

which are not acceptable for predicting the profitability or liquidity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

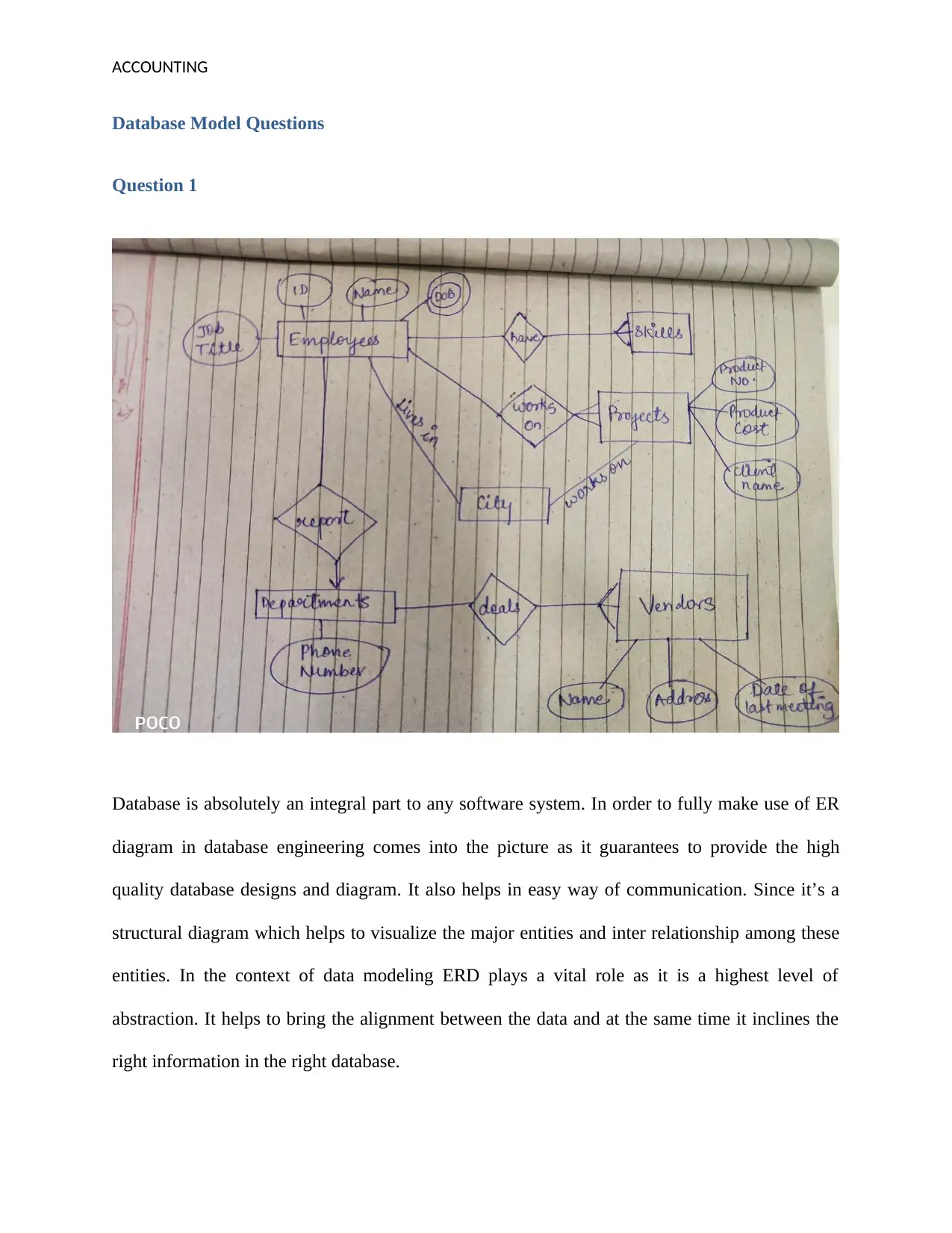

Database Model Questions

Question 1

Database is absolutely an integral part to any software system. In order to fully make use of ER

diagram in database engineering comes into the picture as it guarantees to provide the high

quality database designs and diagram. It also helps in easy way of communication. Since it’s a

structural diagram which helps to visualize the major entities and inter relationship among these

entities. In the context of data modeling ERD plays a vital role as it is a highest level of

abstraction. It helps to bring the alignment between the data and at the same time it inclines the

right information in the right database.

Database Model Questions

Question 1

Database is absolutely an integral part to any software system. In order to fully make use of ER

diagram in database engineering comes into the picture as it guarantees to provide the high

quality database designs and diagram. It also helps in easy way of communication. Since it’s a

structural diagram which helps to visualize the major entities and inter relationship among these

entities. In the context of data modeling ERD plays a vital role as it is a highest level of

abstraction. It helps to bring the alignment between the data and at the same time it inclines the

right information in the right database.

ACCOUNTING

Question 3

As per the above case study there are several advantages which are used by the airline industry

with respect to the big data and its concepts. The major advantages start with increase in the

revenue as the big data helps the skyline airlines to analyze the booking which also helps to grab

a greater customer base. With the help of big data, the data can be maintained in the easiest

manner and it helps decode predictive maintenance solutions to manage the data in a better

manner. Big data is one step solution for Sky airlines as its cost effective, however there are

certain challenges which are also welcomed once the big data is implemented.

At times airline struggles to use the big data as the IT department is small and big data in airlines

is quite huge. The process is complex and crucial and for sky airline industry which is using all

of the resources which can use of all the costs. In terms of the privacy it becomes crucial for the

companies to keep the data private as most of the structure and the unstructured data are gathered

while collecting of the data.

Question 4

There are several challenges faced by the database management are as follows. There is a

growing complexity in the landscape as there is a variety in the database management and chose

a solution and there is a wide spin with each vendor. When there is a limit of scalability it

becomes a problem for the company. Due to the increased data volumes companies are having

huge problem in keeping the data updated and accessibility. Since the databases are the hidden

workhorses of many of the IT companies are paying more than 5 million dollars to set of the data

breach costs. As per the current situation there are certain solutions which can be used for DAS

model starting with the encryption of the data. With the help of decryption a layer of protection

is created above the DBMS which can help in arranging compatibility with the software and at

Question 3

As per the above case study there are several advantages which are used by the airline industry

with respect to the big data and its concepts. The major advantages start with increase in the

revenue as the big data helps the skyline airlines to analyze the booking which also helps to grab

a greater customer base. With the help of big data, the data can be maintained in the easiest

manner and it helps decode predictive maintenance solutions to manage the data in a better

manner. Big data is one step solution for Sky airlines as its cost effective, however there are

certain challenges which are also welcomed once the big data is implemented.

At times airline struggles to use the big data as the IT department is small and big data in airlines

is quite huge. The process is complex and crucial and for sky airline industry which is using all

of the resources which can use of all the costs. In terms of the privacy it becomes crucial for the

companies to keep the data private as most of the structure and the unstructured data are gathered

while collecting of the data.

Question 4

There are several challenges faced by the database management are as follows. There is a

growing complexity in the landscape as there is a variety in the database management and chose

a solution and there is a wide spin with each vendor. When there is a limit of scalability it

becomes a problem for the company. Due to the increased data volumes companies are having

huge problem in keeping the data updated and accessibility. Since the databases are the hidden

workhorses of many of the IT companies are paying more than 5 million dollars to set of the data

breach costs. As per the current situation there are certain solutions which can be used for DAS

model starting with the encryption of the data. With the help of decryption a layer of protection

is created above the DBMS which can help in arranging compatibility with the software and at

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING

the same time creates a wall against the malicious content. Real time security monitoring is also

one of the solutions that can be adopted. Further the new method of query over encrypted data

can help in implementation of SQL queries over encrypted data efficiently.

the same time creates a wall against the malicious content. Real time security monitoring is also

one of the solutions that can be adopted. Further the new method of query over encrypted data

can help in implementation of SQL queries over encrypted data efficiently.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.