Environmental Accounting and Management

VerifiedAdded on 2020/06/06

|16

|4126

|40

AI Summary

This assignment delves into the realm of environmental management accounting, focusing on case studies of South-East Asian companies. It examines various aspects of this field, including research methodologies such as validation in interpretive accounting research and the influence of industry context on management accounting practices. The assignment also considers the advantages and disadvantages of mixed methods research approaches.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Research report on functions of management accounting.....................................................1

i) Management accounting concept and its differentiation from financial accounting..........1

ii) Importance of management accounting for taking decisions............................................2

b) Different management accounting system and its usage to improve reports.........................3

TASK 2............................................................................................................................................4

P3 Preparation of income statement by consulting absorption and marginal costing.................4

TASK 3............................................................................................................................................7

P4 Written report on planning tools............................................................................................7

a) Different types of budget and its limitation and advantages..............................................7

b) Process for preparing budget..............................................................................................7

c) Pricing strategy for Imda tech............................................................................................9

TASK 4..........................................................................................................................................10

P5 Balance scorecard and its use in Imda Tech for better decisions.........................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Research report on functions of management accounting.....................................................1

i) Management accounting concept and its differentiation from financial accounting..........1

ii) Importance of management accounting for taking decisions............................................2

b) Different management accounting system and its usage to improve reports.........................3

TASK 2............................................................................................................................................4

P3 Preparation of income statement by consulting absorption and marginal costing.................4

TASK 3............................................................................................................................................7

P4 Written report on planning tools............................................................................................7

a) Different types of budget and its limitation and advantages..............................................7

b) Process for preparing budget..............................................................................................7

c) Pricing strategy for Imda tech............................................................................................9

TASK 4..........................................................................................................................................10

P5 Balance scorecard and its use in Imda Tech for better decisions.........................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management of each and every sort of business is must. It enables an organisation to take

appropriate decision which are beneficial for an entity. Management accounting is a process

which enables a firm’s decision makers to take appropriate steps on the basis of short term

reports (Baldvinsdottir, Mitchell and Nørreklit, 2010). This present assignment is based on Imda

Tech which deals in manufacturing of special chargers and other carry on services. Managers of

cited organisation have to maintain their short term reports which aid them in taking long term

financial decisions for the company. In this report several number of concepts are discussed

which includes importance of management accounting as a decision making tool. Also it is

completely different from financial accounting process. Moreover, importance of balanced

scorecard approaches depicted which enables management to take crucial decisions and helps in

analysing the performance of a company.

TASK 1

P1 Research report on functions of management accounting

i) Management accounting concept and its differentiation from financial

accounting

Management accounting is a financial statement or advice for a company through which

management is able to take appropriate decision for an organisations’ long term benefit. It is a

process of making reports and accounts that provides accurate and financial statistical

information required by the managers to help them make day to day and short term decisions.

This process supports an entity to operate in all segments in effective and efficient manner

(Bodie, 2013). Authority can formulate strategies by taking these reports in their account.

Managers can identify all changes which are concerned with their projects to take

beneficial decision which increase the chances of sustainability of operation. It is prepared on

short term provision of business. Hence, it is completely different from financial accounting

which provides a data for whole year. Financial accounting and managerial accounting both have

different formats and managers have to take both of them in their consideration while dealing

with varying situations. A basic differentiation between financial accounting and managerial

accounting is as follow:

1

Management of each and every sort of business is must. It enables an organisation to take

appropriate decision which are beneficial for an entity. Management accounting is a process

which enables a firm’s decision makers to take appropriate steps on the basis of short term

reports (Baldvinsdottir, Mitchell and Nørreklit, 2010). This present assignment is based on Imda

Tech which deals in manufacturing of special chargers and other carry on services. Managers of

cited organisation have to maintain their short term reports which aid them in taking long term

financial decisions for the company. In this report several number of concepts are discussed

which includes importance of management accounting as a decision making tool. Also it is

completely different from financial accounting process. Moreover, importance of balanced

scorecard approaches depicted which enables management to take crucial decisions and helps in

analysing the performance of a company.

TASK 1

P1 Research report on functions of management accounting

i) Management accounting concept and its differentiation from financial

accounting

Management accounting is a financial statement or advice for a company through which

management is able to take appropriate decision for an organisations’ long term benefit. It is a

process of making reports and accounts that provides accurate and financial statistical

information required by the managers to help them make day to day and short term decisions.

This process supports an entity to operate in all segments in effective and efficient manner

(Bodie, 2013). Authority can formulate strategies by taking these reports in their account.

Managers can identify all changes which are concerned with their projects to take

beneficial decision which increase the chances of sustainability of operation. It is prepared on

short term provision of business. Hence, it is completely different from financial accounting

which provides a data for whole year. Financial accounting and managerial accounting both have

different formats and managers have to take both of them in their consideration while dealing

with varying situations. A basic differentiation between financial accounting and managerial

accounting is as follow:

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

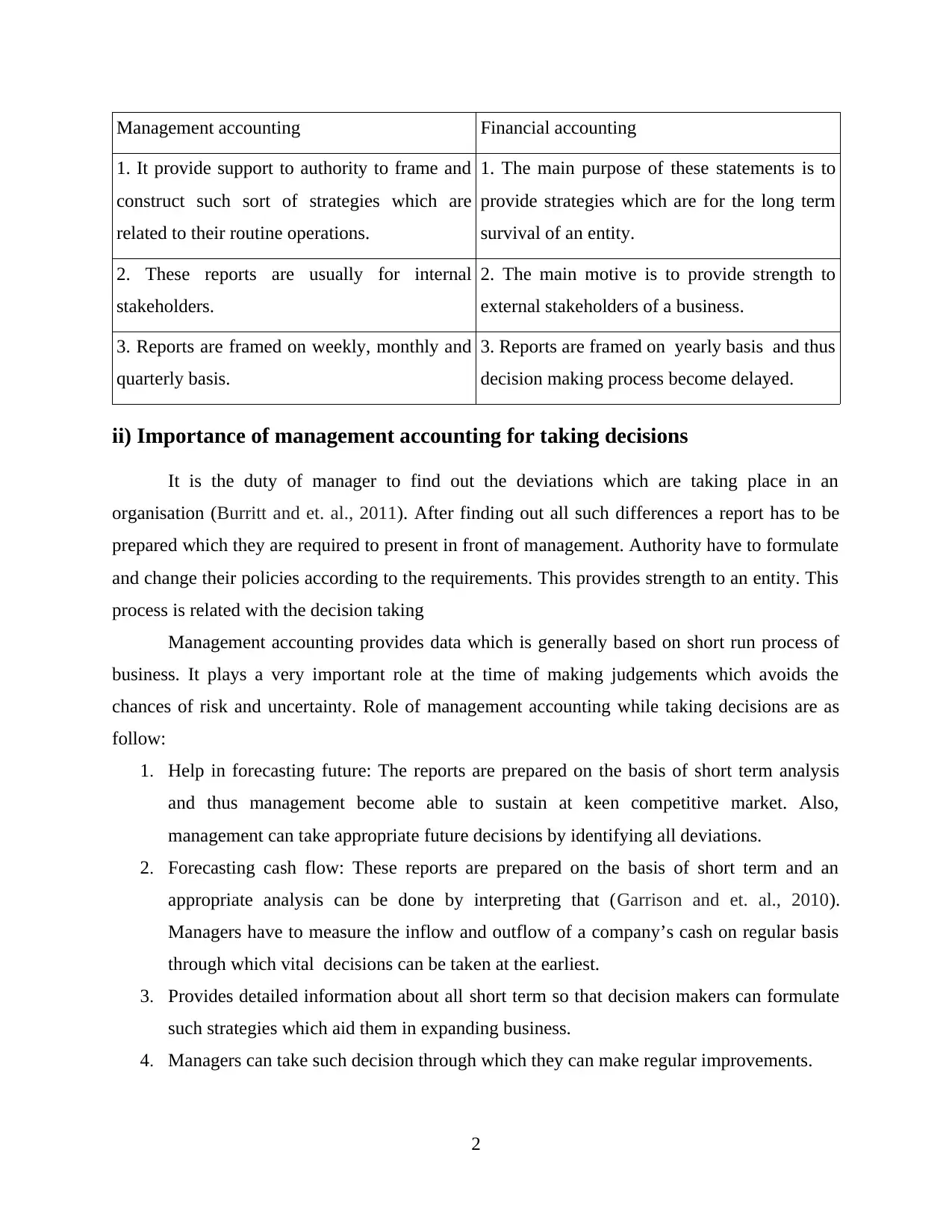

Management accounting Financial accounting

1. It provide support to authority to frame and

construct such sort of strategies which are

related to their routine operations.

1. The main purpose of these statements is to

provide strategies which are for the long term

survival of an entity.

2. These reports are usually for internal

stakeholders.

2. The main motive is to provide strength to

external stakeholders of a business.

3. Reports are framed on weekly, monthly and

quarterly basis.

3. Reports are framed on yearly basis and thus

decision making process become delayed.

ii) Importance of management accounting for taking decisions

It is the duty of manager to find out the deviations which are taking place in an

organisation (Burritt and et. al., 2011). After finding out all such differences a report has to be

prepared which they are required to present in front of management. Authority have to formulate

and change their policies according to the requirements. This provides strength to an entity. This

process is related with the decision taking

Management accounting provides data which is generally based on short run process of

business. It plays a very important role at the time of making judgements which avoids the

chances of risk and uncertainty. Role of management accounting while taking decisions are as

follow:

1. Help in forecasting future: The reports are prepared on the basis of short term analysis

and thus management become able to sustain at keen competitive market. Also,

management can take appropriate future decisions by identifying all deviations.

2. Forecasting cash flow: These reports are prepared on the basis of short term and an

appropriate analysis can be done by interpreting that (Garrison and et. al., 2010).

Managers have to measure the inflow and outflow of a company’s cash on regular basis

through which vital decisions can be taken at the earliest.

3. Provides detailed information about all short term so that decision makers can formulate

such strategies which aid them in expanding business.

4. Managers can take such decision through which they can make regular improvements.

2

1. It provide support to authority to frame and

construct such sort of strategies which are

related to their routine operations.

1. The main purpose of these statements is to

provide strategies which are for the long term

survival of an entity.

2. These reports are usually for internal

stakeholders.

2. The main motive is to provide strength to

external stakeholders of a business.

3. Reports are framed on weekly, monthly and

quarterly basis.

3. Reports are framed on yearly basis and thus

decision making process become delayed.

ii) Importance of management accounting for taking decisions

It is the duty of manager to find out the deviations which are taking place in an

organisation (Burritt and et. al., 2011). After finding out all such differences a report has to be

prepared which they are required to present in front of management. Authority have to formulate

and change their policies according to the requirements. This provides strength to an entity. This

process is related with the decision taking

Management accounting provides data which is generally based on short run process of

business. It plays a very important role at the time of making judgements which avoids the

chances of risk and uncertainty. Role of management accounting while taking decisions are as

follow:

1. Help in forecasting future: The reports are prepared on the basis of short term analysis

and thus management become able to sustain at keen competitive market. Also,

management can take appropriate future decisions by identifying all deviations.

2. Forecasting cash flow: These reports are prepared on the basis of short term and an

appropriate analysis can be done by interpreting that (Garrison and et. al., 2010).

Managers have to measure the inflow and outflow of a company’s cash on regular basis

through which vital decisions can be taken at the earliest.

3. Provides detailed information about all short term so that decision makers can formulate

such strategies which aid them in expanding business.

4. Managers can take such decision through which they can make regular improvements.

2

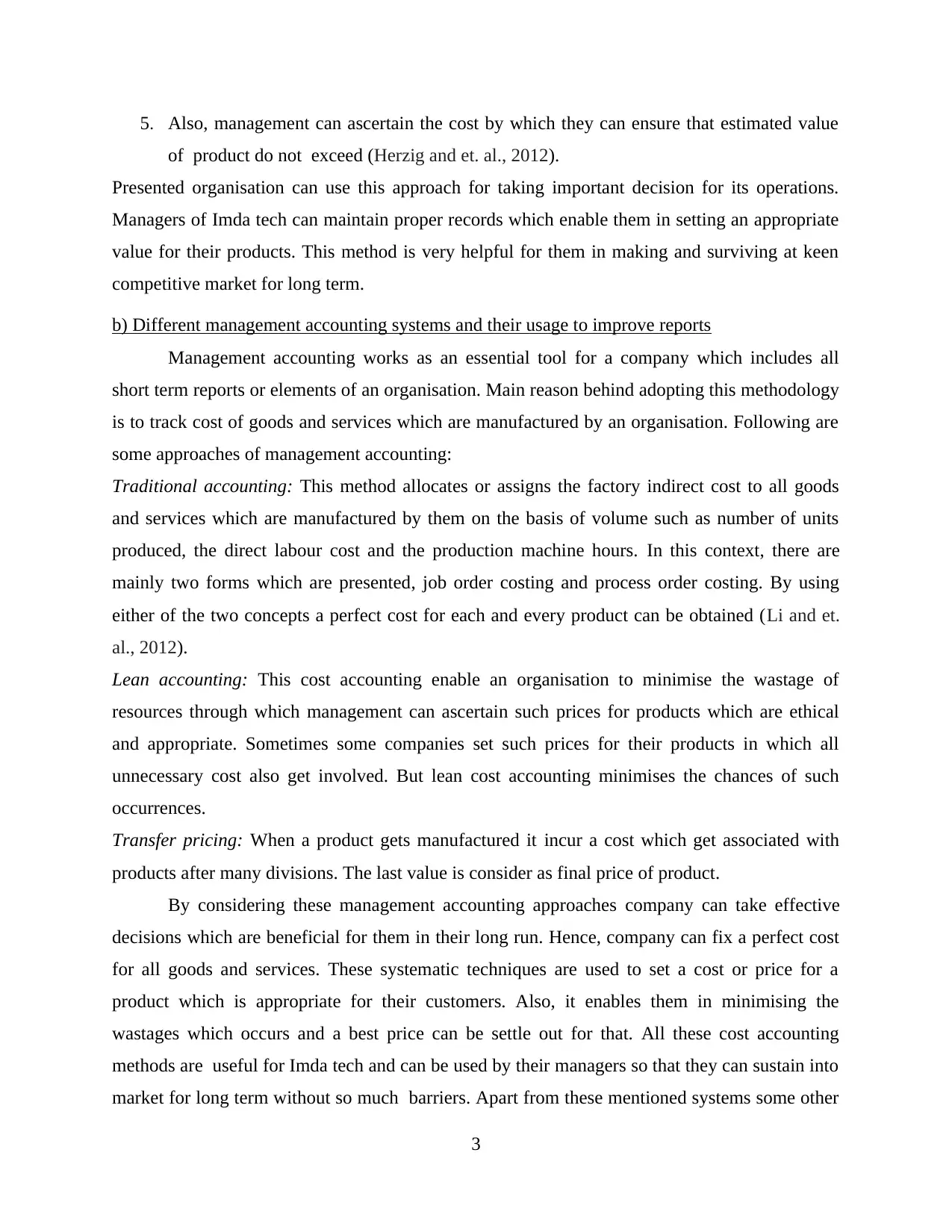

5. Also, management can ascertain the cost by which they can ensure that estimated value

of product do not exceed (Herzig and et. al., 2012).

Presented organisation can use this approach for taking important decision for its operations.

Managers of Imda tech can maintain proper records which enable them in setting an appropriate

value for their products. This method is very helpful for them in making and surviving at keen

competitive market for long term.

b) Different management accounting systems and their usage to improve reports

Management accounting works as an essential tool for a company which includes all

short term reports or elements of an organisation. Main reason behind adopting this methodology

is to track cost of goods and services which are manufactured by an organisation. Following are

some approaches of management accounting:

Traditional accounting: This method allocates or assigns the factory indirect cost to all goods

and services which are manufactured by them on the basis of volume such as number of units

produced, the direct labour cost and the production machine hours. In this context, there are

mainly two forms which are presented, job order costing and process order costing. By using

either of the two concepts a perfect cost for each and every product can be obtained (Li and et.

al., 2012).

Lean accounting: This cost accounting enable an organisation to minimise the wastage of

resources through which management can ascertain such prices for products which are ethical

and appropriate. Sometimes some companies set such prices for their products in which all

unnecessary cost also get involved. But lean cost accounting minimises the chances of such

occurrences.

Transfer pricing: When a product gets manufactured it incur a cost which get associated with

products after many divisions. The last value is consider as final price of product.

By considering these management accounting approaches company can take effective

decisions which are beneficial for them in their long run. Hence, company can fix a perfect cost

for all goods and services. These systematic techniques are used to set a cost or price for a

product which is appropriate for their customers. Also, it enables them in minimising the

wastages which occurs and a best price can be settle out for that. All these cost accounting

methods are useful for Imda tech and can be used by their managers so that they can sustain into

market for long term without so much barriers. Apart from these mentioned systems some other

3

of product do not exceed (Herzig and et. al., 2012).

Presented organisation can use this approach for taking important decision for its operations.

Managers of Imda tech can maintain proper records which enable them in setting an appropriate

value for their products. This method is very helpful for them in making and surviving at keen

competitive market for long term.

b) Different management accounting systems and their usage to improve reports

Management accounting works as an essential tool for a company which includes all

short term reports or elements of an organisation. Main reason behind adopting this methodology

is to track cost of goods and services which are manufactured by an organisation. Following are

some approaches of management accounting:

Traditional accounting: This method allocates or assigns the factory indirect cost to all goods

and services which are manufactured by them on the basis of volume such as number of units

produced, the direct labour cost and the production machine hours. In this context, there are

mainly two forms which are presented, job order costing and process order costing. By using

either of the two concepts a perfect cost for each and every product can be obtained (Li and et.

al., 2012).

Lean accounting: This cost accounting enable an organisation to minimise the wastage of

resources through which management can ascertain such prices for products which are ethical

and appropriate. Sometimes some companies set such prices for their products in which all

unnecessary cost also get involved. But lean cost accounting minimises the chances of such

occurrences.

Transfer pricing: When a product gets manufactured it incur a cost which get associated with

products after many divisions. The last value is consider as final price of product.

By considering these management accounting approaches company can take effective

decisions which are beneficial for them in their long run. Hence, company can fix a perfect cost

for all goods and services. These systematic techniques are used to set a cost or price for a

product which is appropriate for their customers. Also, it enables them in minimising the

wastages which occurs and a best price can be settle out for that. All these cost accounting

methods are useful for Imda tech and can be used by their managers so that they can sustain into

market for long term without so much barriers. Apart from these mentioned systems some other

3

methods can also be used by firm in improving their reports and they can minimise their prices

by considering them (Lukka and Modell, 2010).

1. Cost accounting: For settling up a perfect price for a product cost accounting works as a

helpful tool. Many values are incorporated at the time of manufacturing of goods and

services. Hence, management can use either of the cost accounting concept which are

actual cost, standard cost and normal cost.

2. Inventory accounting: Stock identification is an effective tool which means to measure all

the remaining unsold inventory of a company.

3. Price optimising: This concept signifies about the nature of customers and their reactions

towards different prices which are offered by producers. Also, many business entities use

this concept to set a best price which enables them in meeting their objectives (Macintosh

and Quattrone, 2010).

Imda tech can use either mentioned concept through which they can set a best

price for their gadgets. While considering one of them a perfect value for the products can be set

by decision makers which is beneficial for their customers. According to lean accounting and

price optimising techniques company can set an appropriate cost for a product. Along with that

wastages of resources can be reduced to minimum.

TASK 2

P3 Preparation of income statement by application of absorption and marginal costing

techniques

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

4

by considering them (Lukka and Modell, 2010).

1. Cost accounting: For settling up a perfect price for a product cost accounting works as a

helpful tool. Many values are incorporated at the time of manufacturing of goods and

services. Hence, management can use either of the cost accounting concept which are

actual cost, standard cost and normal cost.

2. Inventory accounting: Stock identification is an effective tool which means to measure all

the remaining unsold inventory of a company.

3. Price optimising: This concept signifies about the nature of customers and their reactions

towards different prices which are offered by producers. Also, many business entities use

this concept to set a best price which enables them in meeting their objectives (Macintosh

and Quattrone, 2010).

Imda tech can use either mentioned concept through which they can set a best

price for their gadgets. While considering one of them a perfect value for the products can be set

by decision makers which is beneficial for their customers. According to lean accounting and

price optimising techniques company can set an appropriate cost for a product. Along with that

wastages of resources can be reduced to minimum.

TASK 2

P3 Preparation of income statement by application of absorption and marginal costing

techniques

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

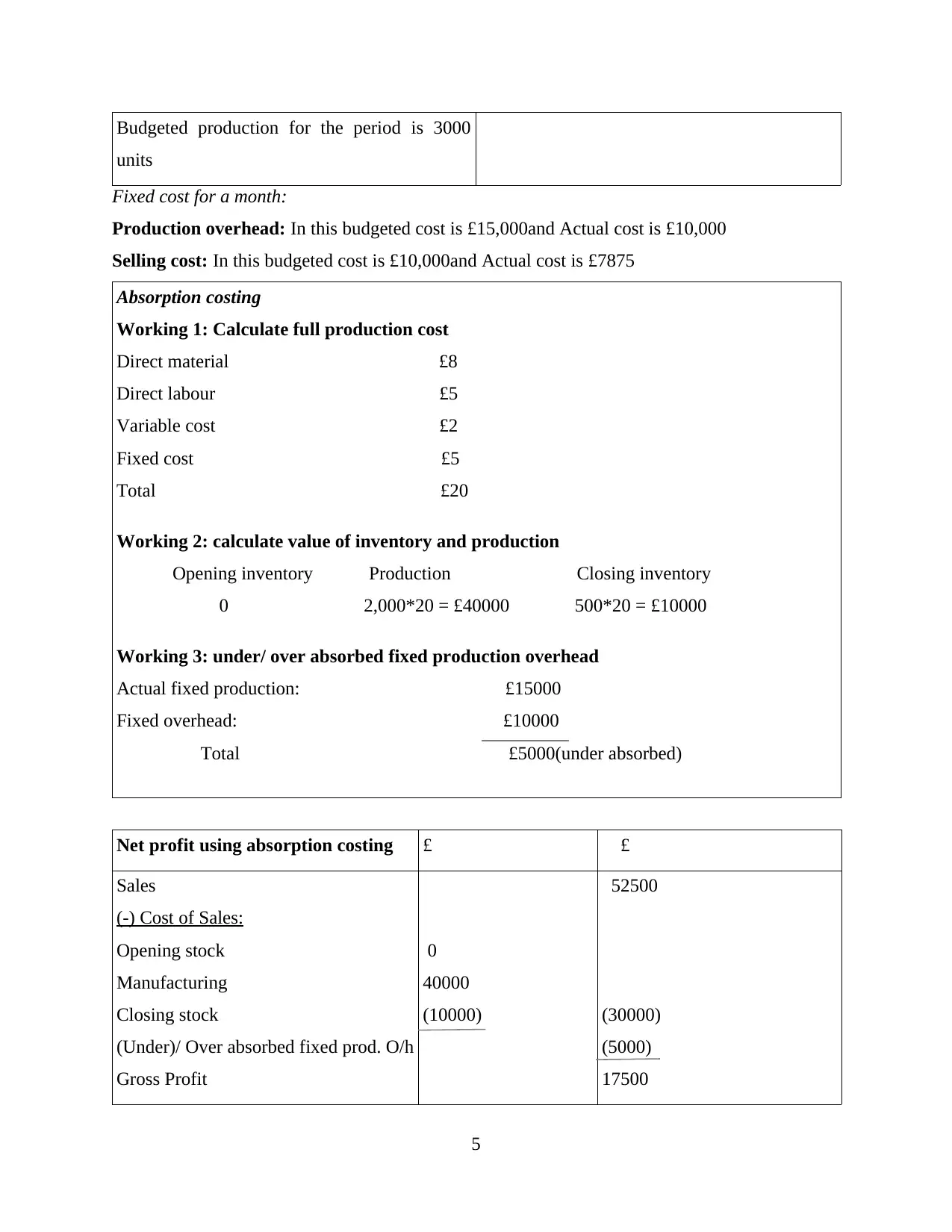

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

0

40000

(10000)

52500

(30000)

(5000)

17500

5

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

0

40000

(10000)

52500

(30000)

(5000)

17500

5

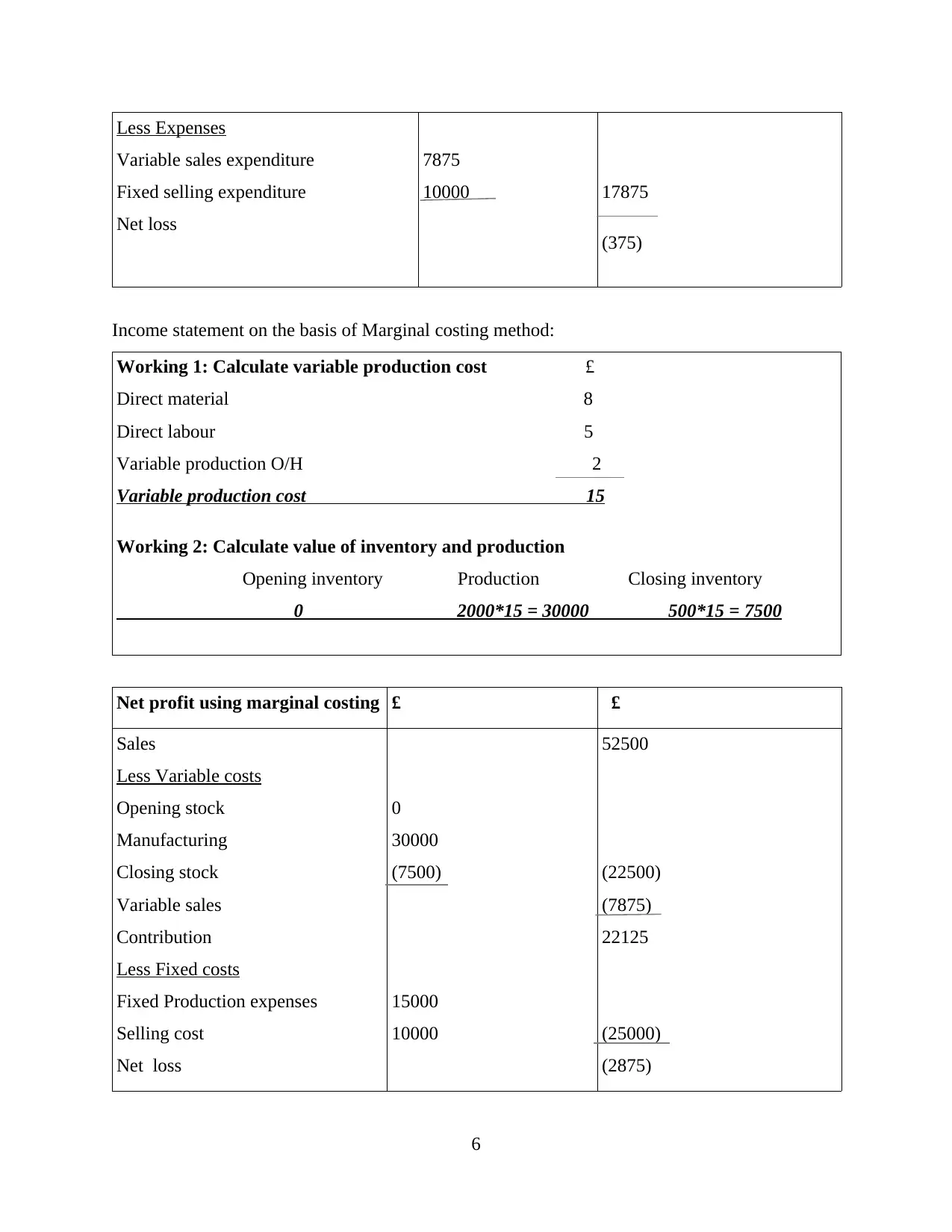

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

7875

10000 17875

(375)

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/H 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

6

Variable sales expenditure

Fixed selling expenditure

Net loss

7875

10000 17875

(375)

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/H 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

6

Absorption costing is a full costing method in which all the costs which are incurred at the time

of production are included. But according to this Imda tech income statement it is clearly get

identified that company is suffering a heavy loss of (375) which is not appropriate at all (Malina,

Nørreklit and Selto, 2011). As per the marginal costing which varies according to time,

company’s income statement again showing the loss of (2875). Hence, in both scenario,

company is bearing heavy loss which is not appropriate at all.

TASK 3

P4 Written report on planning tools

a) Different types of budget and its limitation and advantages

Budget is an essential planning tool for any organisation. It provides a framework for a

company to draw their expenses and income. All the investment related activities also come

under this technique (Messner, 2016). If an entity will not lead to formulate appropriate plan for

their near future investment and expenditure, then they have to face so much problem. Imda tech

have to prepare their budget which enables them in setting all of operations in an effective

manner. Once this work gets done then chances of sustainability increases and production of

goods becomes more quality based because all resources gets utilised in a proper manner. In this

context, there are various forms of budget which Imda tech can take into account when they are

dealing with regular operation by analysing their reports on monthly, or weekly basis. The

different kinds of budgets are as follow with their advantage and limitations:

1. Master budget: Accumulation of whole year expenses and investment by a company get done

with assistance of master budget. It enables the management or decision makers to find out the

right path for investment and arranging funds. There are numerous number of functions are

taking place in an entity which come under different departments. For looking them, these

division have managers who accumulate their whole year investment at one time (Rausch, 2011).

This budgetary format provides a shorter or capsule form of budget in which all functions

are considerd as one but a major drawback of this concept is by gathering all expenses at once, it

become difficult for management to conclude which department is more detrimental than others.

2. Operating Budget: This budgetary format provides a set of data in which management divides

all regular activities and expenses in a sequence. One of the advantage of this budgetary system

7

of production are included. But according to this Imda tech income statement it is clearly get

identified that company is suffering a heavy loss of (375) which is not appropriate at all (Malina,

Nørreklit and Selto, 2011). As per the marginal costing which varies according to time,

company’s income statement again showing the loss of (2875). Hence, in both scenario,

company is bearing heavy loss which is not appropriate at all.

TASK 3

P4 Written report on planning tools

a) Different types of budget and its limitation and advantages

Budget is an essential planning tool for any organisation. It provides a framework for a

company to draw their expenses and income. All the investment related activities also come

under this technique (Messner, 2016). If an entity will not lead to formulate appropriate plan for

their near future investment and expenditure, then they have to face so much problem. Imda tech

have to prepare their budget which enables them in setting all of operations in an effective

manner. Once this work gets done then chances of sustainability increases and production of

goods becomes more quality based because all resources gets utilised in a proper manner. In this

context, there are various forms of budget which Imda tech can take into account when they are

dealing with regular operation by analysing their reports on monthly, or weekly basis. The

different kinds of budgets are as follow with their advantage and limitations:

1. Master budget: Accumulation of whole year expenses and investment by a company get done

with assistance of master budget. It enables the management or decision makers to find out the

right path for investment and arranging funds. There are numerous number of functions are

taking place in an entity which come under different departments. For looking them, these

division have managers who accumulate their whole year investment at one time (Rausch, 2011).

This budgetary format provides a shorter or capsule form of budget in which all functions

are considerd as one but a major drawback of this concept is by gathering all expenses at once, it

become difficult for management to conclude which department is more detrimental than others.

2. Operating Budget: This budgetary format provides a set of data in which management divides

all regular activities and expenses in a sequence. One of the advantage of this budgetary system

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

is to trim all unnecessary expenditure by management so that chances of resource utilisation gets

maximised . But sometimes it increases the cost because another person is hired for maintaining

and operating.

b) Process for preparing budget

Budget helps in estimating all expenses and investments in an appropriate manner. It

enables an organisation to use all of their resources in a proper manner and reduce the wastage of

resources by sorting them in a proper way. Management have to use appropriate steps for their

budget preparation through which they can settle down all operations and activities in a proper

manner. Authorities have to analyse all thing and then prepare their budgets. This include several

number of steps which are as follow:

1. Strategic plan: An organisation should have to frame a written plan in which all of their

mission and vision are stated. Management have to prepare a strategic plan in which

organisational resources are revealed in support of strategy implementation and

development of an entity (SAEIDI, Hamidian and Rabiee, 2013).

2. Business goals: An entity have to set some goals which provide them strength.

Management have to link these goals with financial resources through which all targets

could be attained in an effective manner.

3. Revenue projection: This process is a part of analysis of historical financial performance

and projected income growth. This factor plays a crucial role.

4. Fixed cost projection: Management have to include all fixed cost in their budget through

which an organisation can ascertain all their expenses in a proper manner. By considering

this format, authority can raise fund through different resources.

5. Variable cost projection: This is such cost which fluctuates according to production.

They are not fixed in nature and it is the duty of manager to analyse them. Once all such

factors gets identified then management can raise debt in accordance with such variable

expenses.

6. Annual goal expenses: Several targets which formulate by management are for long term

purpose and do not get attain in short period of time. Management have to consider them

also.

8

maximised . But sometimes it increases the cost because another person is hired for maintaining

and operating.

b) Process for preparing budget

Budget helps in estimating all expenses and investments in an appropriate manner. It

enables an organisation to use all of their resources in a proper manner and reduce the wastage of

resources by sorting them in a proper way. Management have to use appropriate steps for their

budget preparation through which they can settle down all operations and activities in a proper

manner. Authorities have to analyse all thing and then prepare their budgets. This include several

number of steps which are as follow:

1. Strategic plan: An organisation should have to frame a written plan in which all of their

mission and vision are stated. Management have to prepare a strategic plan in which

organisational resources are revealed in support of strategy implementation and

development of an entity (SAEIDI, Hamidian and Rabiee, 2013).

2. Business goals: An entity have to set some goals which provide them strength.

Management have to link these goals with financial resources through which all targets

could be attained in an effective manner.

3. Revenue projection: This process is a part of analysis of historical financial performance

and projected income growth. This factor plays a crucial role.

4. Fixed cost projection: Management have to include all fixed cost in their budget through

which an organisation can ascertain all their expenses in a proper manner. By considering

this format, authority can raise fund through different resources.

5. Variable cost projection: This is such cost which fluctuates according to production.

They are not fixed in nature and it is the duty of manager to analyse them. Once all such

factors gets identified then management can raise debt in accordance with such variable

expenses.

6. Annual goal expenses: Several targets which formulate by management are for long term

purpose and do not get attain in short period of time. Management have to consider them

also.

8

7. Target profit margin: Business firms have to set their profit margin first. This provides

them a set target which company wants to attain. It promotes in performing all task in an

effective manner (Schaltegger and Csutora, 2012).

8. Board approval:Directors of a company have to measure the current status as well as they

must review all financial statement critically so as to minimise losses by reducing

irrelevant expenditure.

9. Budget review: As per the stage of review company measure their current performance

and goals which they achieve or the targets which management settle down. Once this

work get done all deviations lead to get measure. Hence, management can cut down the

unnecessary spendings with this assessment.

10. Dealing with budget variances: At last all variances which took place during a month

have to get analyse so that management can take beneficial steps for overcoming from

them (Senftlechner and Hiebl, 2015). The variances get measure by computing the budget

properly.

c) Pricing strategy for Imda tech

An organisation has to formulate a strategy for setting their prices. It is the duty of

management to set such prices which are easily affordable to each and every customer. Presented

company have to fix such price which have a capability to attract to every customer. In this

context, there are three major techniques which can be used by company are as follow:

1. Premium pricing: Many firms use this concept under which they set their value of

products high with appropriate quality. Such high prices lead to attract many customers

(Smith, Brännström and Jansson, 2015).

2. Penetration pricing: According to this pricing strategy in which company lowers down

their prices at initial level and after getting a greater market share they then slightly hike

up their prices.

3. Skimming pricing: This strategy is completely different from penetration pricing in which

prices are high at initial level. In this pricing strategy company lower their rates at

starting and then increase their value of products after grabbing most market share.

9

them a set target which company wants to attain. It promotes in performing all task in an

effective manner (Schaltegger and Csutora, 2012).

8. Board approval:Directors of a company have to measure the current status as well as they

must review all financial statement critically so as to minimise losses by reducing

irrelevant expenditure.

9. Budget review: As per the stage of review company measure their current performance

and goals which they achieve or the targets which management settle down. Once this

work get done all deviations lead to get measure. Hence, management can cut down the

unnecessary spendings with this assessment.

10. Dealing with budget variances: At last all variances which took place during a month

have to get analyse so that management can take beneficial steps for overcoming from

them (Senftlechner and Hiebl, 2015). The variances get measure by computing the budget

properly.

c) Pricing strategy for Imda tech

An organisation has to formulate a strategy for setting their prices. It is the duty of

management to set such prices which are easily affordable to each and every customer. Presented

company have to fix such price which have a capability to attract to every customer. In this

context, there are three major techniques which can be used by company are as follow:

1. Premium pricing: Many firms use this concept under which they set their value of

products high with appropriate quality. Such high prices lead to attract many customers

(Smith, Brännström and Jansson, 2015).

2. Penetration pricing: According to this pricing strategy in which company lowers down

their prices at initial level and after getting a greater market share they then slightly hike

up their prices.

3. Skimming pricing: This strategy is completely different from penetration pricing in which

prices are high at initial level. In this pricing strategy company lower their rates at

starting and then increase their value of products after grabbing most market share.

9

TASK 4

P5 Balance scorecard and its use in Imda Tech for better decisions

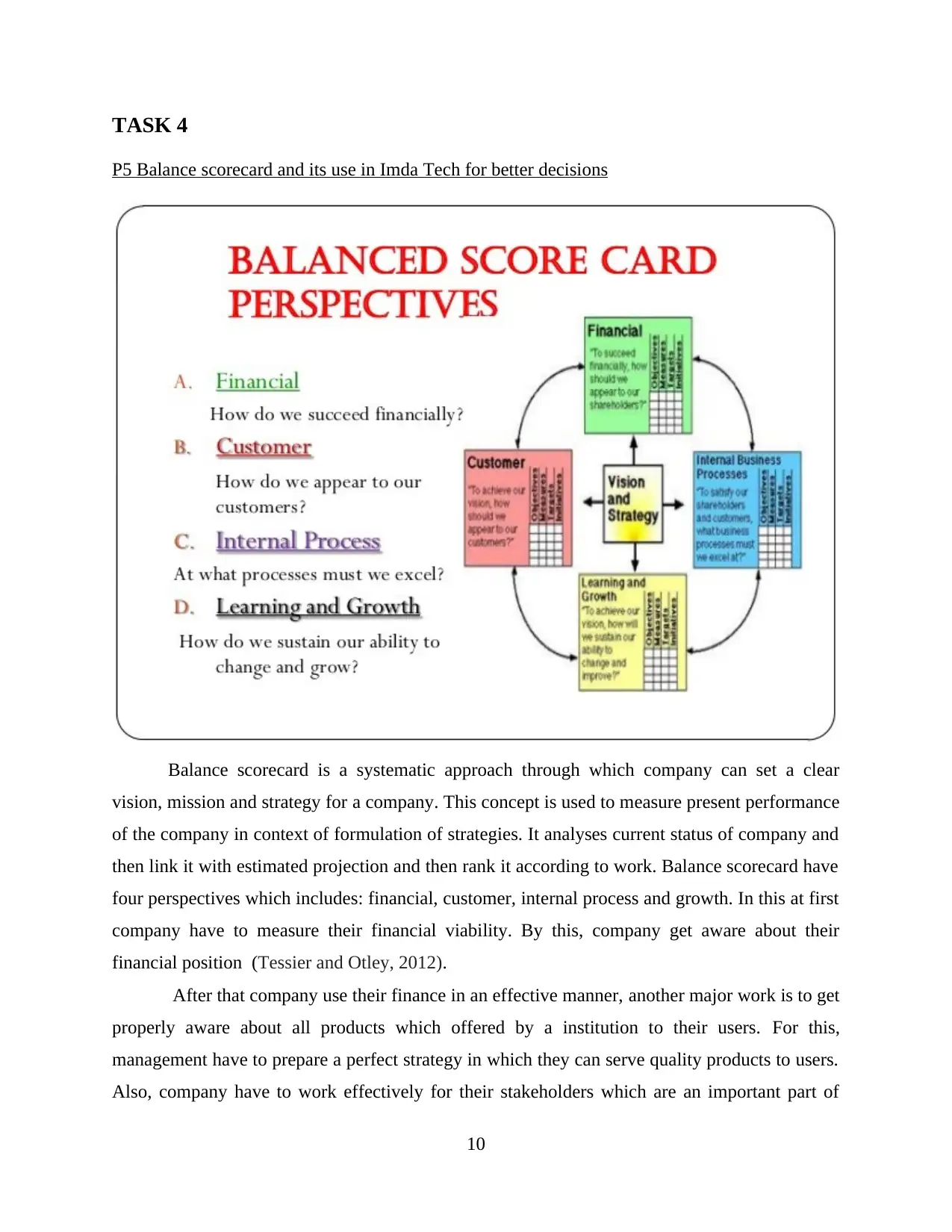

Balance scorecard is a systematic approach through which company can set a clear

vision, mission and strategy for a company. This concept is used to measure present performance

of the company in context of formulation of strategies. It analyses current status of company and

then link it with estimated projection and then rank it according to work. Balance scorecard have

four perspectives which includes: financial, customer, internal process and growth. In this at first

company have to measure their financial viability. By this, company get aware about their

financial position (Tessier and Otley, 2012).

After that company use their finance in an effective manner, another major work is to get

properly aware about all products which offered by a institution to their users. For this,

management have to prepare a perfect strategy in which they can serve quality products to users.

Also, company have to work effectively for their stakeholders which are an important part of

10

P5 Balance scorecard and its use in Imda Tech for better decisions

Balance scorecard is a systematic approach through which company can set a clear

vision, mission and strategy for a company. This concept is used to measure present performance

of the company in context of formulation of strategies. It analyses current status of company and

then link it with estimated projection and then rank it according to work. Balance scorecard have

four perspectives which includes: financial, customer, internal process and growth. In this at first

company have to measure their financial viability. By this, company get aware about their

financial position (Tessier and Otley, 2012).

After that company use their finance in an effective manner, another major work is to get

properly aware about all products which offered by a institution to their users. For this,

management have to prepare a perfect strategy in which they can serve quality products to users.

Also, company have to work effectively for their stakeholders which are an important part of

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their strategy and vision. And at last balance scorecard includes the manner through which they

can sustain in market. All these things are included in balance scorecard and management have

to identify this thing in a proper manner by analysing the outcomes at the end of week, month or

quarter (Ward, 2012).

CONCLUSION

As per the above stated report is get clearly identified that an organisation have to use

appropriate tools and techniques for an appropriate decision.. Also they have to analyse their

management accounting reports which provide them ability to ascertain the circumstances.

Hence, management have to analyse their cost by identifying their income statement in which

they can consider various costing methods. After analysing any deviations management have to

prepare a budget which provide them strength and support in setting a proper pricing strategy for

a company. At last all issues have to get match with balance scorecard and in case of more

deviations these problems have to get resolved.

11

can sustain in market. All these things are included in balance scorecard and management have

to identify this thing in a proper manner by analysing the outcomes at the end of week, month or

quarter (Ward, 2012).

CONCLUSION

As per the above stated report is get clearly identified that an organisation have to use

appropriate tools and techniques for an appropriate decision.. Also they have to analyse their

management accounting reports which provide them ability to ascertain the circumstances.

Hence, management have to analyse their cost by identifying their income statement in which

they can consider various costing methods. After analysing any deviations management have to

prepare a budget which provide them strength and support in setting a proper pricing strategy for

a company. At last all issues have to get match with balance scorecard and in case of more

deviations these problems have to get resolved.

11

REFERENCES

Baldvinsdottir, G., Mitchell, F and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Bodie, Z., 2013. Investments. McGraw-Hill.

Burritt, R.L., and et. al., 2011. Environmental management accounting and supply chain

management (Vol. 27). Springer Science & Business Media.

Garrison, R.H., and et. al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Herzig, C., and et. al., 2012. Environmental management accounting: case studies of South-East

Asian Companies. Routledge.

Li, X., and et. al., 2012. A comparative analysis of management accounting systems’ impact on

lean implementation. International Journal of Technology Management. 57(1/2/3).

pp.33-48.

Lukka, K and Modell, S., 2010. Validation in interpretive management accounting research.

Accounting, Organizations and Society. 35(4). pp.462-477.

Macintosh, N.B and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Malina, M.A., Nørreklit, H.S. and Selto, F.H., 2011. Lessons learned: advantages and

disadvantages of mixed method research. Qualitative Research in Accounting &

Management. 8(1). pp.59-71.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Rausch, A., 2011. Reconstruction of decision-making behavior in shareholder and stakeholder

theory: implications for management accounting systems. Review of Managerial

Science. 5(2-3). pp.137-169.

SAEIDI, A., Hamidian, N. and Rabiee, H., 2013. The relationship between real earnings

management activities and future performance of the listed companies in tehran stock

exchange.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Senftlechner, D. and Hiebl, M.R., 2015. Management accounting and management control in

family businesses: Past accomplishments and future opportunities. Journal of

Accounting & Organizational Change. 11(4). pp.573-606.

Smith, D., Brännström, D. and Jansson, A., 2015. Redovisningens språk. Studentlitteratur.

Tessier, S. and Otley, D., 2012. A conceptual development of Simons’ Levers of Control

framework. Management Accounting Research. 23(3). pp.171-185.

Ward, K., 2012. Strategic management accounting. Routledge.

Online

5 Types of Budgets for Businesses. 2017 [Online]. Available

through:<https://www.fool.com/knowledge-center/5-types-of-budgets-for-businesses.aspx>.

[Accessed on 11th April 2017]

12

Baldvinsdottir, G., Mitchell, F and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Bodie, Z., 2013. Investments. McGraw-Hill.

Burritt, R.L., and et. al., 2011. Environmental management accounting and supply chain

management (Vol. 27). Springer Science & Business Media.

Garrison, R.H., and et. al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Herzig, C., and et. al., 2012. Environmental management accounting: case studies of South-East

Asian Companies. Routledge.

Li, X., and et. al., 2012. A comparative analysis of management accounting systems’ impact on

lean implementation. International Journal of Technology Management. 57(1/2/3).

pp.33-48.

Lukka, K and Modell, S., 2010. Validation in interpretive management accounting research.

Accounting, Organizations and Society. 35(4). pp.462-477.

Macintosh, N.B and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Malina, M.A., Nørreklit, H.S. and Selto, F.H., 2011. Lessons learned: advantages and

disadvantages of mixed method research. Qualitative Research in Accounting &

Management. 8(1). pp.59-71.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Rausch, A., 2011. Reconstruction of decision-making behavior in shareholder and stakeholder

theory: implications for management accounting systems. Review of Managerial

Science. 5(2-3). pp.137-169.

SAEIDI, A., Hamidian, N. and Rabiee, H., 2013. The relationship between real earnings

management activities and future performance of the listed companies in tehran stock

exchange.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Senftlechner, D. and Hiebl, M.R., 2015. Management accounting and management control in

family businesses: Past accomplishments and future opportunities. Journal of

Accounting & Organizational Change. 11(4). pp.573-606.

Smith, D., Brännström, D. and Jansson, A., 2015. Redovisningens språk. Studentlitteratur.

Tessier, S. and Otley, D., 2012. A conceptual development of Simons’ Levers of Control

framework. Management Accounting Research. 23(3). pp.171-185.

Ward, K., 2012. Strategic management accounting. Routledge.

Online

5 Types of Budgets for Businesses. 2017 [Online]. Available

through:<https://www.fool.com/knowledge-center/5-types-of-budgets-for-businesses.aspx>.

[Accessed on 11th April 2017]

12

Definition of 'Pricing Strategies'. 2017 [Online]. Available

through:<http://economictimes.indiatimes.com/definition/pricing-strategies>. [Accessed on 11th

April 2017]

13

through:<http://economictimes.indiatimes.com/definition/pricing-strategies>. [Accessed on 11th

April 2017]

13

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.