Management Accounting Report: Financial Performance of EECL

VerifiedAdded on 2022/12/15

|15

|4239

|110

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, focusing on the case study of Eastern Engineering Co. Ltd (EECL). It delves into various aspects, including different types of management accounting systems, such as cost accounting, inventory management, and price optimization systems, and their essential requirements. The report explores different methods used for management accounting reporting, like aging accounts and job reports. Furthermore, it examines cost analysis techniques, specifically marginal and absorption costing, and their application in preparing financial statements. The report also discusses the benefits and disadvantages of various planning tools, such as budgeting, and how companies like EECL use management accounting to address economic difficulties. The analysis includes financial statements prepared using marginal and absorption costing, demonstrating their impact on profitability. Overall, the report offers valuable insights into the practical application of management accounting within a manufacturing context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Types of MA systems and essential need.............................................................................3

P2. Different methods used for MA reporting. ..........................................................................6

TASK 2............................................................................................................................................7

P3: Cost analysis techniques & use of absorption and marginal costing....................................7

TASK 3............................................................................................................................................9

P4: Benefits and disadvantage of various tools of planning.......................................................9

TASK 4..........................................................................................................................................11

P5: Compare how companies are prepared to deal mostly with management accounting

framework to solve different economic difficulties and issues.................................................11

Conclusion.....................................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Types of MA systems and essential need.............................................................................3

P2. Different methods used for MA reporting. ..........................................................................6

TASK 2............................................................................................................................................7

P3: Cost analysis techniques & use of absorption and marginal costing....................................7

TASK 3............................................................................................................................................9

P4: Benefits and disadvantage of various tools of planning.......................................................9

TASK 4..........................................................................................................................................11

P5: Compare how companies are prepared to deal mostly with management accounting

framework to solve different economic difficulties and issues.................................................11

Conclusion.....................................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

MA deals primarily with exchanges that are linked to finance, but there are many other

difference accounting method that emphasise all aspects of money transfers. MA is also an

accounting company that is responsible for monitoring and recording monetary and non-

monetary data (Tan, 2019). This data is used because when management teams also need

create internal reports for specific period. MA is specifically designed for critical success factors

to take additional actions relating to the use of financial and non-financial resources. Business

concern that is selected for the project is Eastern Engineering Co. Ltd (EECL) which is a

medium sized venture in manufacturing sector.

In the report, various tasks are covered. Under the Task 1, the report is categorised into

three parts which cover information pertaining to MA processes and reports. While part two

includes some risks are managed as well as about their practical implications on a given dataset.

The impact of forecasting methods and MA technologies was presented in the subsequent section

of the analysis in order to address the economic issues of the firms.

TASK 1

P1. Types of MA systems and essential need.

It is described as a financial reporting that is directed at collecting and evaluating key

transaction details that happened in a corporation throughout a monetary year (Hutaibat and

Alhatabat, 2019). In EECL, the whole act is carried out to obtain internal financial report that

managers execute to make major decisions. Within the concept, professional skills addition to

knowledge are applied to prepare accounting information so that it guides internal management

in preparing policies together with controlling organisational operations.

As per the chartered Institute of Management Accountants, the expense of London is

described as the quantity of both total outstanding and real government spending due primarily to

or accrued on a specific activity or something. In EECL, general responsibility associated with

management accounting is for assisting people in devising essential decisions for future of

business.

Distinction between MA and financial accounting:

Base for

comparison

Management accounting Financial accounting

MA deals primarily with exchanges that are linked to finance, but there are many other

difference accounting method that emphasise all aspects of money transfers. MA is also an

accounting company that is responsible for monitoring and recording monetary and non-

monetary data (Tan, 2019). This data is used because when management teams also need

create internal reports for specific period. MA is specifically designed for critical success factors

to take additional actions relating to the use of financial and non-financial resources. Business

concern that is selected for the project is Eastern Engineering Co. Ltd (EECL) which is a

medium sized venture in manufacturing sector.

In the report, various tasks are covered. Under the Task 1, the report is categorised into

three parts which cover information pertaining to MA processes and reports. While part two

includes some risks are managed as well as about their practical implications on a given dataset.

The impact of forecasting methods and MA technologies was presented in the subsequent section

of the analysis in order to address the economic issues of the firms.

TASK 1

P1. Types of MA systems and essential need.

It is described as a financial reporting that is directed at collecting and evaluating key

transaction details that happened in a corporation throughout a monetary year (Hutaibat and

Alhatabat, 2019). In EECL, the whole act is carried out to obtain internal financial report that

managers execute to make major decisions. Within the concept, professional skills addition to

knowledge are applied to prepare accounting information so that it guides internal management

in preparing policies together with controlling organisational operations.

As per the chartered Institute of Management Accountants, the expense of London is

described as the quantity of both total outstanding and real government spending due primarily to

or accrued on a specific activity or something. In EECL, general responsibility associated with

management accounting is for assisting people in devising essential decisions for future of

business.

Distinction between MA and financial accounting:

Base for

comparison

Management accounting Financial accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Users This accounting is primarily

designed for the internal customers.

This is being used by internally and

externally interested parties of EECL.

Regulations Within this financial reporting, there

have been no laws and regulations

for producing detailed reports

(Tekathen, 2019).

This accounting includes several

restrictions which accounting

professionals must recognise.

Type of

company

This can be implemented in any

enterprise. No address operating

requires such bookkeeping.

Although this bookkeeping is a

requirement for all those firms

mentioned on a renowned stock market.

The primary function of this financial reporting would be to perform a main role in

decision-making process again for key customers. This accounting leads to management teams

by supplying them with necessary time knowledge which was used as decision-

making procedures. In addition, MA it also provides a mechanism for regulating firms which

leads to better performance. With respect with the above EECL, they can implement this

accounting for their operational activities with the aim of improving performance from both

viewpoints including monetary and non-monetary viewpoints. Essential requirements that are

part of key management accounting systems are states underneath in relevance with EECL:

Cost accounting system: This structure is constituted with a procedure of monitoring and

attempting to control almost all expenditures that either takes place in a company in a financial

period. Under it the costs of each object are determined and compared to standardised costs

(Zandi, Khalid and Islam, 2019). Managers are able to find the efficiency and advancement of

various tasks throughout terms of costs. Essential requirement of the system within EECL is to

gather information regarding expenditures associated with direct material, labour etc. in

manufacturing industry. With respect to EECL Limited, manager can gain critical details from

this financial statement together with variability on the cost of various activities. This can lead to

an acceptable phase in aspects of financing need or elimination of such operations that are cost-

consuming significantly greater.

Essential requirement: It helps to control unpractised cost in order to increase

revenues because expense consumption is regularly tracked across each operating condition. This

financial reporting infrastructure is crucial in EECL. to implement for the elimination of costs of

designed for the internal customers.

This is being used by internally and

externally interested parties of EECL.

Regulations Within this financial reporting, there

have been no laws and regulations

for producing detailed reports

(Tekathen, 2019).

This accounting includes several

restrictions which accounting

professionals must recognise.

Type of

company

This can be implemented in any

enterprise. No address operating

requires such bookkeeping.

Although this bookkeeping is a

requirement for all those firms

mentioned on a renowned stock market.

The primary function of this financial reporting would be to perform a main role in

decision-making process again for key customers. This accounting leads to management teams

by supplying them with necessary time knowledge which was used as decision-

making procedures. In addition, MA it also provides a mechanism for regulating firms which

leads to better performance. With respect with the above EECL, they can implement this

accounting for their operational activities with the aim of improving performance from both

viewpoints including monetary and non-monetary viewpoints. Essential requirements that are

part of key management accounting systems are states underneath in relevance with EECL:

Cost accounting system: This structure is constituted with a procedure of monitoring and

attempting to control almost all expenditures that either takes place in a company in a financial

period. Under it the costs of each object are determined and compared to standardised costs

(Zandi, Khalid and Islam, 2019). Managers are able to find the efficiency and advancement of

various tasks throughout terms of costs. Essential requirement of the system within EECL is to

gather information regarding expenditures associated with direct material, labour etc. in

manufacturing industry. With respect to EECL Limited, manager can gain critical details from

this financial statement together with variability on the cost of various activities. This can lead to

an acceptable phase in aspects of financing need or elimination of such operations that are cost-

consuming significantly greater.

Essential requirement: It helps to control unpractised cost in order to increase

revenues because expense consumption is regularly tracked across each operating condition. This

financial reporting infrastructure is crucial in EECL. to implement for the elimination of costs of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unnecessary operation. Along with leading to the preparation of successful tactics for appropriate

activities that result in far more expenditure.

Inventory management system: This is recognised as a system connected to the

management among all aspects of company stock. This is achieved by measuring regularly based

stock report which includes data on consumption of resources, able to prepare stock, etc. In a

pattern made using various approaches called FIFO, LIFO, etc. The primary function of this

financial reporting is to keep storage costs lower by trying to make production according to the

amount of inventory formulated and demand accessible. In the above-mentioned company, their

supervisors will use this bookkeeping to better exploit the amount of possible raw resources such

that storage costs could be regulated.

Essential requirements: In EECL, it's really critical to handle raw materials such as

berries, sweetener for manufacturing and to produce new output according to the number of able

to prepare flavourings and beverages stored.

Price optimisation system: The purpose of this bookkeeping is to establish the price

point within each product according to increased competition. It is calculated in conjunction with

the response of the clients for the company or brand and also by evaluating the pricing stages of

competing companies. The key feature of such bookkeeping is that rates underneath it were also

established by effective alternatives such as demand analysis, market trend and competition

policy. Due to which a company could even charge a threshold within each targeted customers at

such a standard that will become appropriate.

Essential requirement: It is mandatory to implement for all those drinks for whom the

sale is smaller or for innovative technologies for EECL (Łada, Kozarkiewicz and Haslam, 2020).

It can be utilized to evaluate the reaction of clients over the established price level as well as

their asking value for a given product.

Job costing system: This system focuses on monitoring task or job costs aligned with the

completion procedure. Within the sense of EECL, such system is used with intent of discovering

job or task costs for each exercise alongside per unit price. Moreover, the system assigns costs

comprising depreciation on building, rent and other aspects to various cost pools. Total values of

all cost pool are further assigned to multiple open jobs that are related to certain allocation

methodology which is consistently executed.

activities that result in far more expenditure.

Inventory management system: This is recognised as a system connected to the

management among all aspects of company stock. This is achieved by measuring regularly based

stock report which includes data on consumption of resources, able to prepare stock, etc. In a

pattern made using various approaches called FIFO, LIFO, etc. The primary function of this

financial reporting is to keep storage costs lower by trying to make production according to the

amount of inventory formulated and demand accessible. In the above-mentioned company, their

supervisors will use this bookkeeping to better exploit the amount of possible raw resources such

that storage costs could be regulated.

Essential requirements: In EECL, it's really critical to handle raw materials such as

berries, sweetener for manufacturing and to produce new output according to the number of able

to prepare flavourings and beverages stored.

Price optimisation system: The purpose of this bookkeeping is to establish the price

point within each product according to increased competition. It is calculated in conjunction with

the response of the clients for the company or brand and also by evaluating the pricing stages of

competing companies. The key feature of such bookkeeping is that rates underneath it were also

established by effective alternatives such as demand analysis, market trend and competition

policy. Due to which a company could even charge a threshold within each targeted customers at

such a standard that will become appropriate.

Essential requirement: It is mandatory to implement for all those drinks for whom the

sale is smaller or for innovative technologies for EECL (Łada, Kozarkiewicz and Haslam, 2020).

It can be utilized to evaluate the reaction of clients over the established price level as well as

their asking value for a given product.

Job costing system: This system focuses on monitoring task or job costs aligned with the

completion procedure. Within the sense of EECL, such system is used with intent of discovering

job or task costs for each exercise alongside per unit price. Moreover, the system assigns costs

comprising depreciation on building, rent and other aspects to various cost pools. Total values of

all cost pool are further assigned to multiple open jobs that are related to certain allocation

methodology which is consistently executed.

Essential requirements: This accounting is critical to identifying the number of jobs

assigned to complete an activity and to evaluate the cost per unit. This accounting method can be

implemented by the management teams of EECL since they have a strong product portfolio for

different drinks. Hence, it is crucial that they discover out the expense within each drink

manufactured.

P2. Different methods used for MA reporting.

MA is a core internal reporting method that manager adapt to aid individuals in making

decisions. Management accounting reports comprises major detailed organisational accounts

which involve information about cash on hand, present state of accounts payable or receivable,

recent sales revenue generation, etc. In EECL, management accounting reports aids in managing

and control business in better ways. Additionally, appropriate arranged data are presented for

management supervision objectives as well as prevention methods are laid out. Some of these

methods of accounting reports are mentioned below:

Report on ageing accounts: This report includes description of all credit transaction such

that managers can make a complete accounts receivable assessment. It is therefore effective in

reducing bad debt as well as managing the liquid assets of EECL. In this, information are

categorised as per length of time concerned with invoice which is already outstanding.

Job report: This is related to assessment and manufacturing service delivery techniques

against such an approximate standard. The goal is to identify favourable consequences and

inconsistencies throughout the type of cash values (Messner, 2016). These are modified

documents used by internal manager in order to motivate the higher performance employee and

make proper plans to increase the weak performances. It really is a document which aims to

assess all the costs, charges and gain business productivity in a reasonable time since more focus

can be given to beneficial investments. It leads to the prevention of wasting available funds and

to controlling costs.

Inventory management report: Results on inventory checks are being used to

demonstrate stock levels. This is used to ensure value-added capital is decided to invest. There

have been different aspects like inventory book which is to track manually the stock levels in the

terms of low business. In EECL, Barcodes are being used for inventory monitoring, as well as

stock on hand has become inventory control software that is used to demonstrate the amount of

inventory particularly clear.

assigned to complete an activity and to evaluate the cost per unit. This accounting method can be

implemented by the management teams of EECL since they have a strong product portfolio for

different drinks. Hence, it is crucial that they discover out the expense within each drink

manufactured.

P2. Different methods used for MA reporting.

MA is a core internal reporting method that manager adapt to aid individuals in making

decisions. Management accounting reports comprises major detailed organisational accounts

which involve information about cash on hand, present state of accounts payable or receivable,

recent sales revenue generation, etc. In EECL, management accounting reports aids in managing

and control business in better ways. Additionally, appropriate arranged data are presented for

management supervision objectives as well as prevention methods are laid out. Some of these

methods of accounting reports are mentioned below:

Report on ageing accounts: This report includes description of all credit transaction such

that managers can make a complete accounts receivable assessment. It is therefore effective in

reducing bad debt as well as managing the liquid assets of EECL. In this, information are

categorised as per length of time concerned with invoice which is already outstanding.

Job report: This is related to assessment and manufacturing service delivery techniques

against such an approximate standard. The goal is to identify favourable consequences and

inconsistencies throughout the type of cash values (Messner, 2016). These are modified

documents used by internal manager in order to motivate the higher performance employee and

make proper plans to increase the weak performances. It really is a document which aims to

assess all the costs, charges and gain business productivity in a reasonable time since more focus

can be given to beneficial investments. It leads to the prevention of wasting available funds and

to controlling costs.

Inventory management report: Results on inventory checks are being used to

demonstrate stock levels. This is used to ensure value-added capital is decided to invest. There

have been different aspects like inventory book which is to track manually the stock levels in the

terms of low business. In EECL, Barcodes are being used for inventory monitoring, as well as

stock on hand has become inventory control software that is used to demonstrate the amount of

inventory particularly clear.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

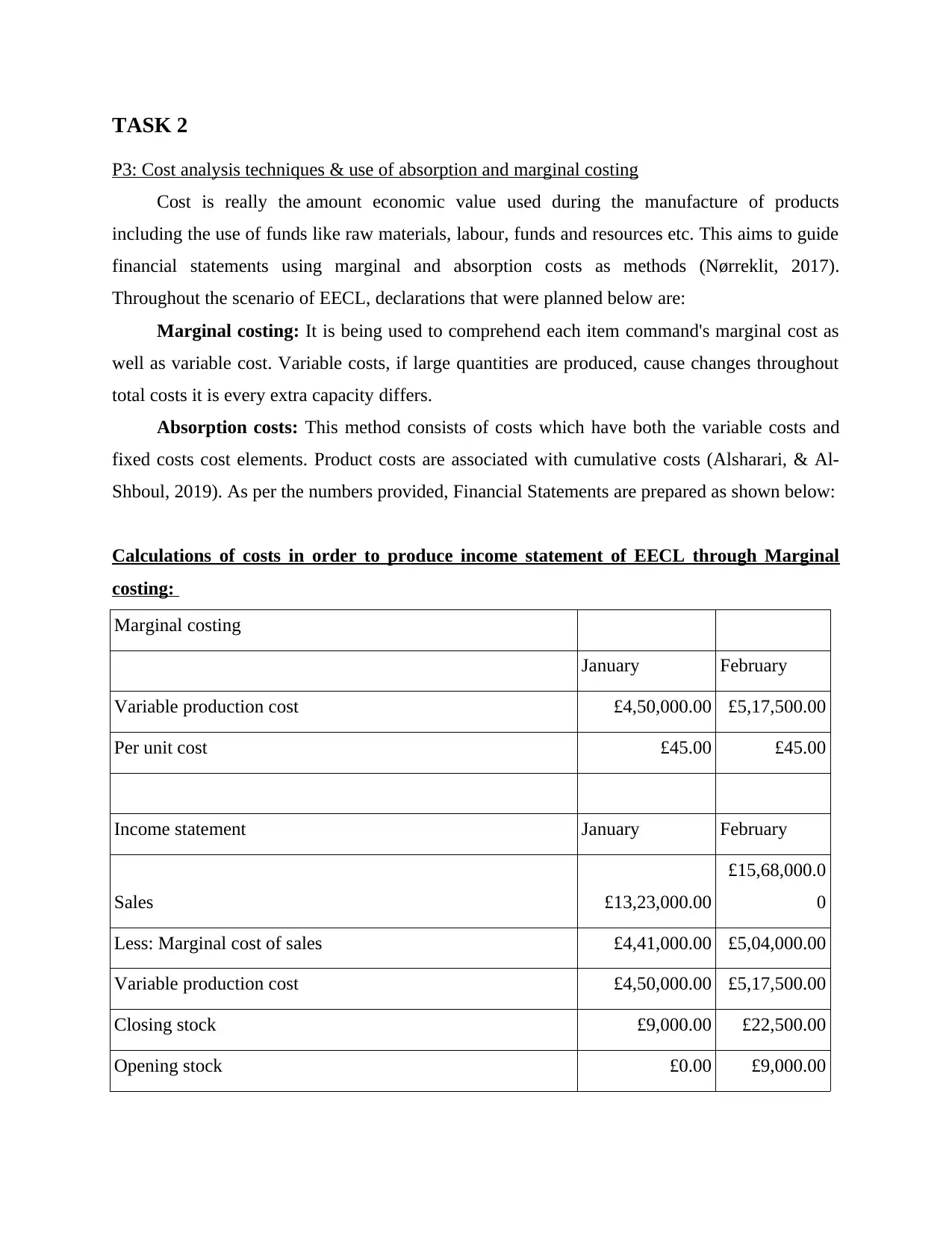

P3: Cost analysis techniques & use of absorption and marginal costing

Cost is really the amount economic value used during the manufacture of products

including the use of funds like raw materials, labour, funds and resources etc. This aims to guide

financial statements using marginal and absorption costs as methods (Nørreklit, 2017).

Throughout the scenario of EECL, declarations that were planned below are:

Marginal costing: It is being used to comprehend each item command's marginal cost as

well as variable cost. Variable costs, if large quantities are produced, cause changes throughout

total costs it is every extra capacity differs.

Absorption costs: This method consists of costs which have both the variable costs and

fixed costs cost elements. Product costs are associated with cumulative costs (Alsharari, & Al-

Shboul, 2019). As per the numbers provided, Financial Statements are prepared as shown below:

Calculations of costs in order to produce income statement of EECL through Marginal

costing:

Marginal costing

January February

Variable production cost £4,50,000.00 £5,17,500.00

Per unit cost £45.00 £45.00

Income statement January February

Sales £13,23,000.00

£15,68,000.0

0

Less: Marginal cost of sales £4,41,000.00 £5,04,000.00

Variable production cost £4,50,000.00 £5,17,500.00

Closing stock £9,000.00 £22,500.00

Opening stock £0.00 £9,000.00

P3: Cost analysis techniques & use of absorption and marginal costing

Cost is really the amount economic value used during the manufacture of products

including the use of funds like raw materials, labour, funds and resources etc. This aims to guide

financial statements using marginal and absorption costs as methods (Nørreklit, 2017).

Throughout the scenario of EECL, declarations that were planned below are:

Marginal costing: It is being used to comprehend each item command's marginal cost as

well as variable cost. Variable costs, if large quantities are produced, cause changes throughout

total costs it is every extra capacity differs.

Absorption costs: This method consists of costs which have both the variable costs and

fixed costs cost elements. Product costs are associated with cumulative costs (Alsharari, & Al-

Shboul, 2019). As per the numbers provided, Financial Statements are prepared as shown below:

Calculations of costs in order to produce income statement of EECL through Marginal

costing:

Marginal costing

January February

Variable production cost £4,50,000.00 £5,17,500.00

Per unit cost £45.00 £45.00

Income statement January February

Sales £13,23,000.00

£15,68,000.0

0

Less: Marginal cost of sales £4,41,000.00 £5,04,000.00

Variable production cost £4,50,000.00 £5,17,500.00

Closing stock £9,000.00 £22,500.00

Opening stock £0.00 £9,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contribution £8,82,000.00

£10,64,000.0

0

Less: Fixed production cost £3,50,000.00 £3,40,000.00

Net income £5,32,000.00 £7,24,000.00

Calculations of cost for producing income statement by absorption costing for EECL

Absorption costing

January February

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Total cost £7,70,000.00

£8,85,500.0

0

Per unit cost £77.00 £77.00

Income statement January February

Sales £13,23,000.00

£15,68,000.

00

Less: Cost of sales £7,54,600.00

£8,62,400.0

0

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Closing stock £15,400.00 £38,500.00

£10,64,000.0

0

Less: Fixed production cost £3,50,000.00 £3,40,000.00

Net income £5,32,000.00 £7,24,000.00

Calculations of cost for producing income statement by absorption costing for EECL

Absorption costing

January February

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Total cost £7,70,000.00

£8,85,500.0

0

Per unit cost £77.00 £77.00

Income statement January February

Sales £13,23,000.00

£15,68,000.

00

Less: Cost of sales £7,54,600.00

£8,62,400.0

0

Variable production cost £4,50,000.00

£5,17,500.0

0

Fixed production cost £3,20,000.00

£3,68,000.0

0

Closing stock £15,400.00 £38,500.00

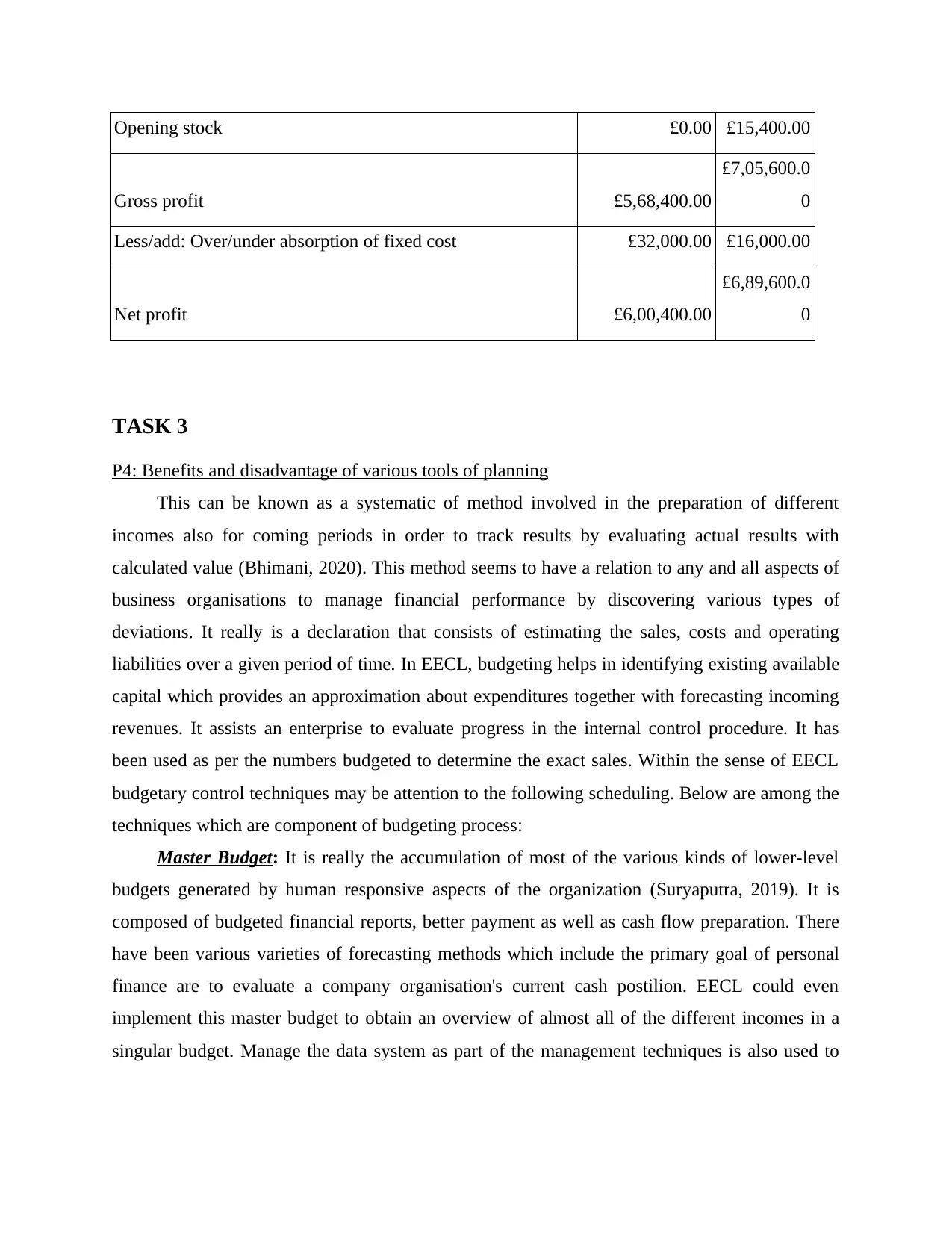

Opening stock £0.00 £15,400.00

Gross profit £5,68,400.00

£7,05,600.0

0

Less/add: Over/under absorption of fixed cost £32,000.00 £16,000.00

Net profit £6,00,400.00

£6,89,600.0

0

TASK 3

P4: Benefits and disadvantage of various tools of planning

This can be known as a systematic of method involved in the preparation of different

incomes also for coming periods in order to track results by evaluating actual results with

calculated value (Bhimani, 2020). This method seems to have a relation to any and all aspects of

business organisations to manage financial performance by discovering various types of

deviations. It really is a declaration that consists of estimating the sales, costs and operating

liabilities over a given period of time. In EECL, budgeting helps in identifying existing available

capital which provides an approximation about expenditures together with forecasting incoming

revenues. It assists an enterprise to evaluate progress in the internal control procedure. It has

been used as per the numbers budgeted to determine the exact sales. Within the sense of EECL

budgetary control techniques may be attention to the following scheduling. Below are among the

techniques which are component of budgeting process:

Master Budget: It is really the accumulation of most of the various kinds of lower-level

budgets generated by human responsive aspects of the organization (Suryaputra, 2019). It is

composed of budgeted financial reports, better payment as well as cash flow preparation. There

have been various varieties of forecasting methods which include the primary goal of personal

finance are to evaluate a company organisation's current cash postilion. EECL could even

implement this master budget to obtain an overview of almost all of the different incomes in a

singular budget. Manage the data system as part of the management techniques is also used to

Gross profit £5,68,400.00

£7,05,600.0

0

Less/add: Over/under absorption of fixed cost £32,000.00 £16,000.00

Net profit £6,00,400.00

£6,89,600.0

0

TASK 3

P4: Benefits and disadvantage of various tools of planning

This can be known as a systematic of method involved in the preparation of different

incomes also for coming periods in order to track results by evaluating actual results with

calculated value (Bhimani, 2020). This method seems to have a relation to any and all aspects of

business organisations to manage financial performance by discovering various types of

deviations. It really is a declaration that consists of estimating the sales, costs and operating

liabilities over a given period of time. In EECL, budgeting helps in identifying existing available

capital which provides an approximation about expenditures together with forecasting incoming

revenues. It assists an enterprise to evaluate progress in the internal control procedure. It has

been used as per the numbers budgeted to determine the exact sales. Within the sense of EECL

budgetary control techniques may be attention to the following scheduling. Below are among the

techniques which are component of budgeting process:

Master Budget: It is really the accumulation of most of the various kinds of lower-level

budgets generated by human responsive aspects of the organization (Suryaputra, 2019). It is

composed of budgeted financial reports, better payment as well as cash flow preparation. There

have been various varieties of forecasting methods which include the primary goal of personal

finance are to evaluate a company organisation's current cash postilion. EECL could even

implement this master budget to obtain an overview of almost all of the different incomes in a

singular budget. Manage the data system as part of the management techniques is also used to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gain the information and using that to carry out duties as well as improve product decisions. It

means avoiding any kind of inefficiency and increase efficiency when all of the features.

Benefits: Master budget assists in identifying problems and plans as well as captures the

statements budged further than department. It could be used for having complex agency's

expected expenses and total revenues. This budget is appropriate for all kinds of businesses as it

would not have to be changed over a specific accounting period. In addition, it helps companies

to assess specific goals for the company with related to specific elements.

Limitation: Timely updating of the spending plan and making minor changes might be

challenging, since there are a number of hurdles associated and need to be carried to cope to the

whole spending plan.

Flexible budget: This is used as a budgetary control planning process, where stimulation

and quantity modify as per regulations. EECL could even implement this spending plan to alter

the level of sales, the amount of manufacturing process in accordance with changes in functional

areas (Erawati and Krisnadewi, 2018). It helps in proper attempting to control & planning.

Benefits: It assists in measure the extent of manufacturing such that the rate of production

could be changed easily. Total amount of EECL may be adapted to achieve a satisfactory degree

of profit margins.

Limitation: Competent and skilled personnel are required to accommodate immediately

informed. Flexible budgets are more expensive and not always accurate which can cause the

company to be ambiguous.

Zero-based budgeting: This is really a method which can be implemented in the event that

perhaps the total revenue is comparable to proportion of the wealth estimates, this distinction is

usually zero. If there would be any percentage in surplus that needs to be adjusted, this technique

is useful in measuring the amount spent each year. This spending plan is also modelled as a set

budget that mostly, before an accounting period, is from a nature to stay unchanged. The actions

of this spending plan cannot really be altered according to the will of the corporation. This

budget has no adverse effect to volatility in specific cost numbers. The overall budget goal is to

achieve an income, cost etc. target. EECL management team use this spending plan for such

operations that are anticipated to stay unchanged like portfolio analysis, insurance.

Benefits: Zero based budgeting helps managers of EECL to provide justification of every

activity and explains revenue which all type of costs will generate for business. More oriented

means avoiding any kind of inefficiency and increase efficiency when all of the features.

Benefits: Master budget assists in identifying problems and plans as well as captures the

statements budged further than department. It could be used for having complex agency's

expected expenses and total revenues. This budget is appropriate for all kinds of businesses as it

would not have to be changed over a specific accounting period. In addition, it helps companies

to assess specific goals for the company with related to specific elements.

Limitation: Timely updating of the spending plan and making minor changes might be

challenging, since there are a number of hurdles associated and need to be carried to cope to the

whole spending plan.

Flexible budget: This is used as a budgetary control planning process, where stimulation

and quantity modify as per regulations. EECL could even implement this spending plan to alter

the level of sales, the amount of manufacturing process in accordance with changes in functional

areas (Erawati and Krisnadewi, 2018). It helps in proper attempting to control & planning.

Benefits: It assists in measure the extent of manufacturing such that the rate of production

could be changed easily. Total amount of EECL may be adapted to achieve a satisfactory degree

of profit margins.

Limitation: Competent and skilled personnel are required to accommodate immediately

informed. Flexible budgets are more expensive and not always accurate which can cause the

company to be ambiguous.

Zero-based budgeting: This is really a method which can be implemented in the event that

perhaps the total revenue is comparable to proportion of the wealth estimates, this distinction is

usually zero. If there would be any percentage in surplus that needs to be adjusted, this technique

is useful in measuring the amount spent each year. This spending plan is also modelled as a set

budget that mostly, before an accounting period, is from a nature to stay unchanged. The actions

of this spending plan cannot really be altered according to the will of the corporation. This

budget has no adverse effect to volatility in specific cost numbers. The overall budget goal is to

achieve an income, cost etc. target. EECL management team use this spending plan for such

operations that are anticipated to stay unchanged like portfolio analysis, insurance.

Benefits: Zero based budgeting helps managers of EECL to provide justification of every

activity and explains revenue which all type of costs will generate for business. More oriented

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

processes are available which assist in motivated execution. Furthermore, it guides in effective

allocation of available resources without looking at past data rather focusing on actual figures.

Disadvantages: It consists of the potential of advanced resource utilisation, misinformed

towards short-term planning as well as deception by knowledgeable managers which can impact

the genuineness of zero-based budgeting.

TASK 4

P5: Compare how companies are prepared to deal mostly with management accounting

framework to solve different economic difficulties and issues.

Financial problems are really the ones that take place whenever the supply and demand vary

greatly. There have been some prevalent problems that may arise when there is no careful

management in the institution. These appear leading to defaults, small error on the aspect of

economic accountants and company departments. Some prevalent Financial Management

problems are raised below:

High promotional expenses: large amount of expenses are needed when EECL are

building a different launch date. Only for specified subset of consumers, there is a necessity to

establish a strategy that helps increase awareness.

Inconsistency in sales revenue: This is a component of accounting problem regarding

sales revenue fluctuations due to some internal vulnerability or intense demand (Le, Tran and

Nguyen, 2020). This money problem tends to result in such a downgrade of a company'

development graph. For example, they confronted this money problems lead to inadequate

pricing sequence in EECL.

Management accounting approach is a concept that involves techniques to solve

pertaining issues in business about financial resources. In EECL, mentioned below are some

approaches with the help of which financial analysts are able to deal with problems and achieve

sustainable success:

Benchmarking: It really is a method in which the institution will have to define a few

targets or guidelines to be followed in the duration of organisational performance. In the scenario

of medium-sized organisations such as EECL, there is indeed a loss scenario that has to be

addressed with by establishing standards is that expenditure only takes place throughout the

benchmarks recognised.

allocation of available resources without looking at past data rather focusing on actual figures.

Disadvantages: It consists of the potential of advanced resource utilisation, misinformed

towards short-term planning as well as deception by knowledgeable managers which can impact

the genuineness of zero-based budgeting.

TASK 4

P5: Compare how companies are prepared to deal mostly with management accounting

framework to solve different economic difficulties and issues.

Financial problems are really the ones that take place whenever the supply and demand vary

greatly. There have been some prevalent problems that may arise when there is no careful

management in the institution. These appear leading to defaults, small error on the aspect of

economic accountants and company departments. Some prevalent Financial Management

problems are raised below:

High promotional expenses: large amount of expenses are needed when EECL are

building a different launch date. Only for specified subset of consumers, there is a necessity to

establish a strategy that helps increase awareness.

Inconsistency in sales revenue: This is a component of accounting problem regarding

sales revenue fluctuations due to some internal vulnerability or intense demand (Le, Tran and

Nguyen, 2020). This money problem tends to result in such a downgrade of a company'

development graph. For example, they confronted this money problems lead to inadequate

pricing sequence in EECL.

Management accounting approach is a concept that involves techniques to solve

pertaining issues in business about financial resources. In EECL, mentioned below are some

approaches with the help of which financial analysts are able to deal with problems and achieve

sustainable success:

Benchmarking: It really is a method in which the institution will have to define a few

targets or guidelines to be followed in the duration of organisational performance. In the scenario

of medium-sized organisations such as EECL, there is indeed a loss scenario that has to be

addressed with by establishing standards is that expenditure only takes place throughout the

benchmarks recognised.

Key performance indicator: This is classified as a type of accounting method based on

measurement of both monetary and non-monetary aspects. Information regarding profit,

expenditure, change back etc. is part of financial aspects. in addition, information relating to

profit margin, political situation etc. are part of non-financial aspects. This is useful in assessing

the causes of financial problems.

Financial governance: It really is a solution that can support a company to accumulate

timely information to meet entire financial reporting (Qian, Hörisch and Schaltegger, 2018). It

tends to make financial reports more realistic however it will be accurate to form further

programs based upon these information.

Comparison showing the ways two establishments have responded to financial problems

EECL Vita coco

Products EECL cope in juices and

soften which are sold legally in

superstore, coffee houses. It is

purchased also by brand of

coca cola 90 as s Smoothies

are Innocent's main element, as

they contain of pulverised

flavourings and berries with

specific use of turmeric and

vegetables in a few of their

beverages.

Vita coco is indeed a coconut

beverage producer, as well as a

distribution company of

healthier options. They serve

various nutrient ingredients,

which help their clients to live

a healthy life.

Financial issues Currently there seems to be

full lock-down throughout

EECL due to COVID-19 Virus

circumstances since March

2020. This has resulted in a

dramatic decline in their

selling and this scenario marks

the end of 2020 as a result of

Costs were a significant matter

in the coconut market segment.

Although sales have been

really high since 2004, there

have also been problems of

raw material accuracy and

chain management

disintegration in providing

measurement of both monetary and non-monetary aspects. Information regarding profit,

expenditure, change back etc. is part of financial aspects. in addition, information relating to

profit margin, political situation etc. are part of non-financial aspects. This is useful in assessing

the causes of financial problems.

Financial governance: It really is a solution that can support a company to accumulate

timely information to meet entire financial reporting (Qian, Hörisch and Schaltegger, 2018). It

tends to make financial reports more realistic however it will be accurate to form further

programs based upon these information.

Comparison showing the ways two establishments have responded to financial problems

EECL Vita coco

Products EECL cope in juices and

soften which are sold legally in

superstore, coffee houses. It is

purchased also by brand of

coca cola 90 as s Smoothies

are Innocent's main element, as

they contain of pulverised

flavourings and berries with

specific use of turmeric and

vegetables in a few of their

beverages.

Vita coco is indeed a coconut

beverage producer, as well as a

distribution company of

healthier options. They serve

various nutrient ingredients,

which help their clients to live

a healthy life.

Financial issues Currently there seems to be

full lock-down throughout

EECL due to COVID-19 Virus

circumstances since March

2020. This has resulted in a

dramatic decline in their

selling and this scenario marks

the end of 2020 as a result of

Costs were a significant matter

in the coconut market segment.

Although sales have been

really high since 2004, there

have also been problems of

raw material accuracy and

chain management

disintegration in providing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.