Nelson College Management Accounting Report: GSQ Limited Analysis

VerifiedAdded on 2023/01/12

|11

|698

|49

Report

AI Summary

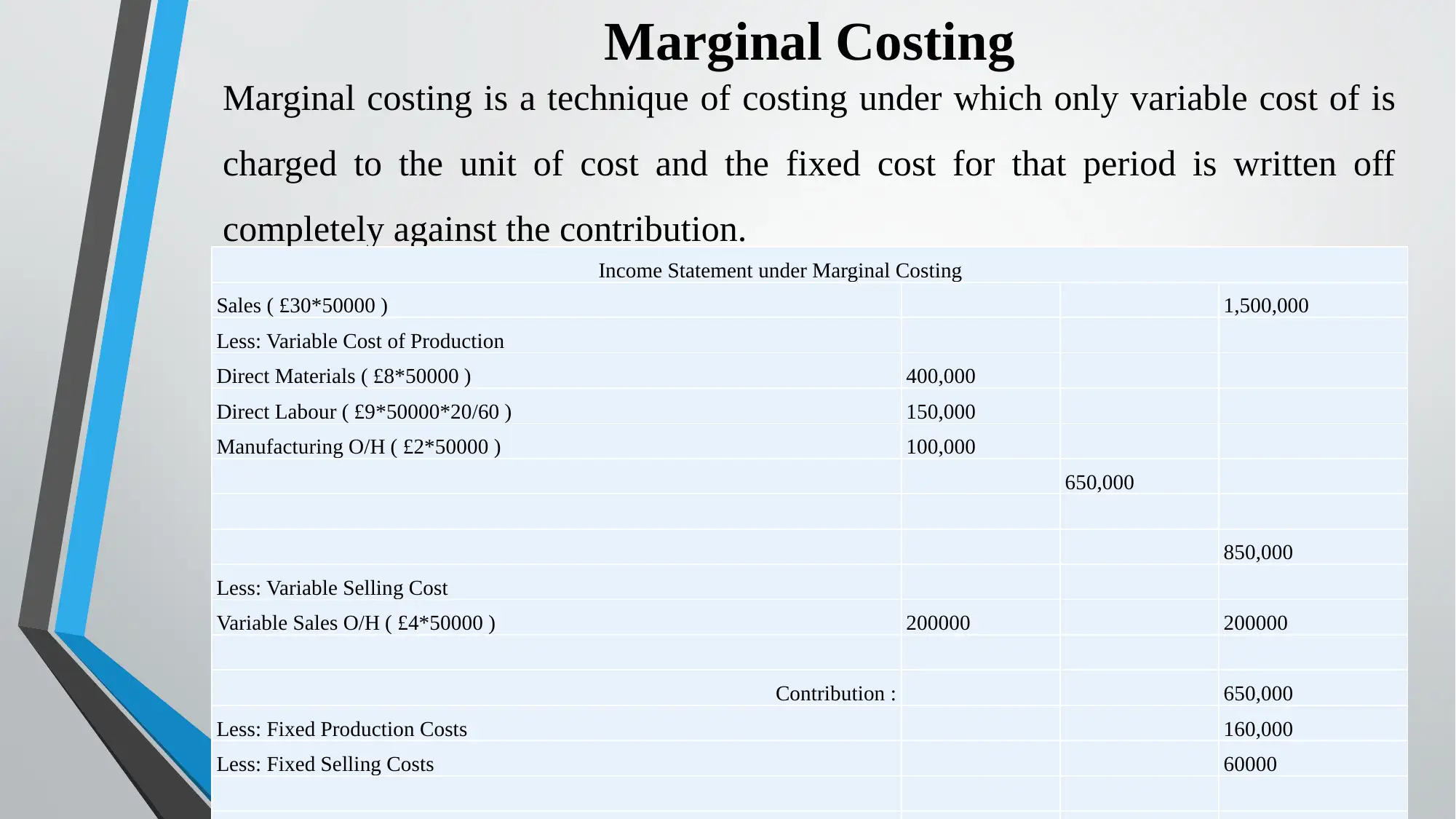

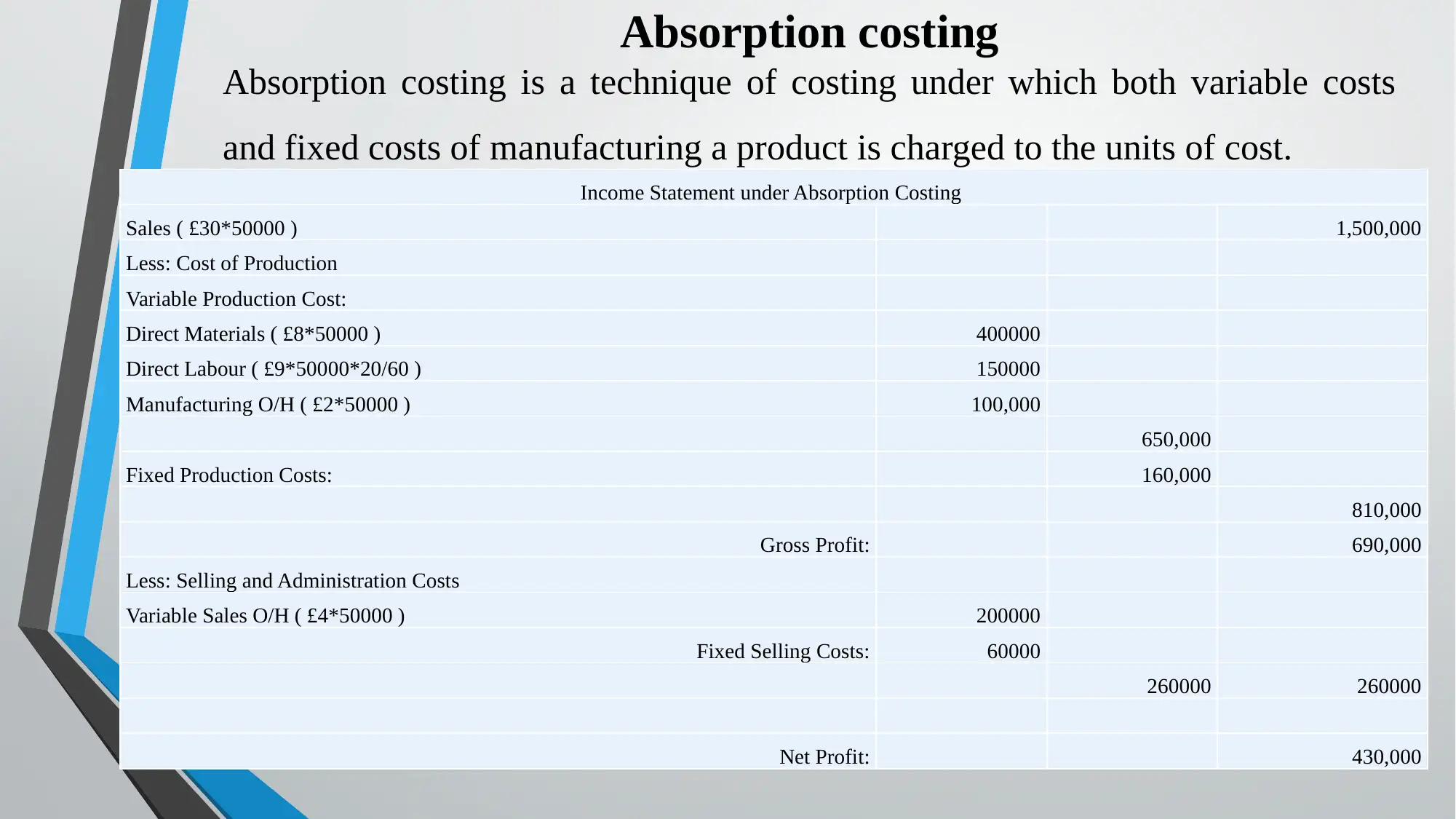

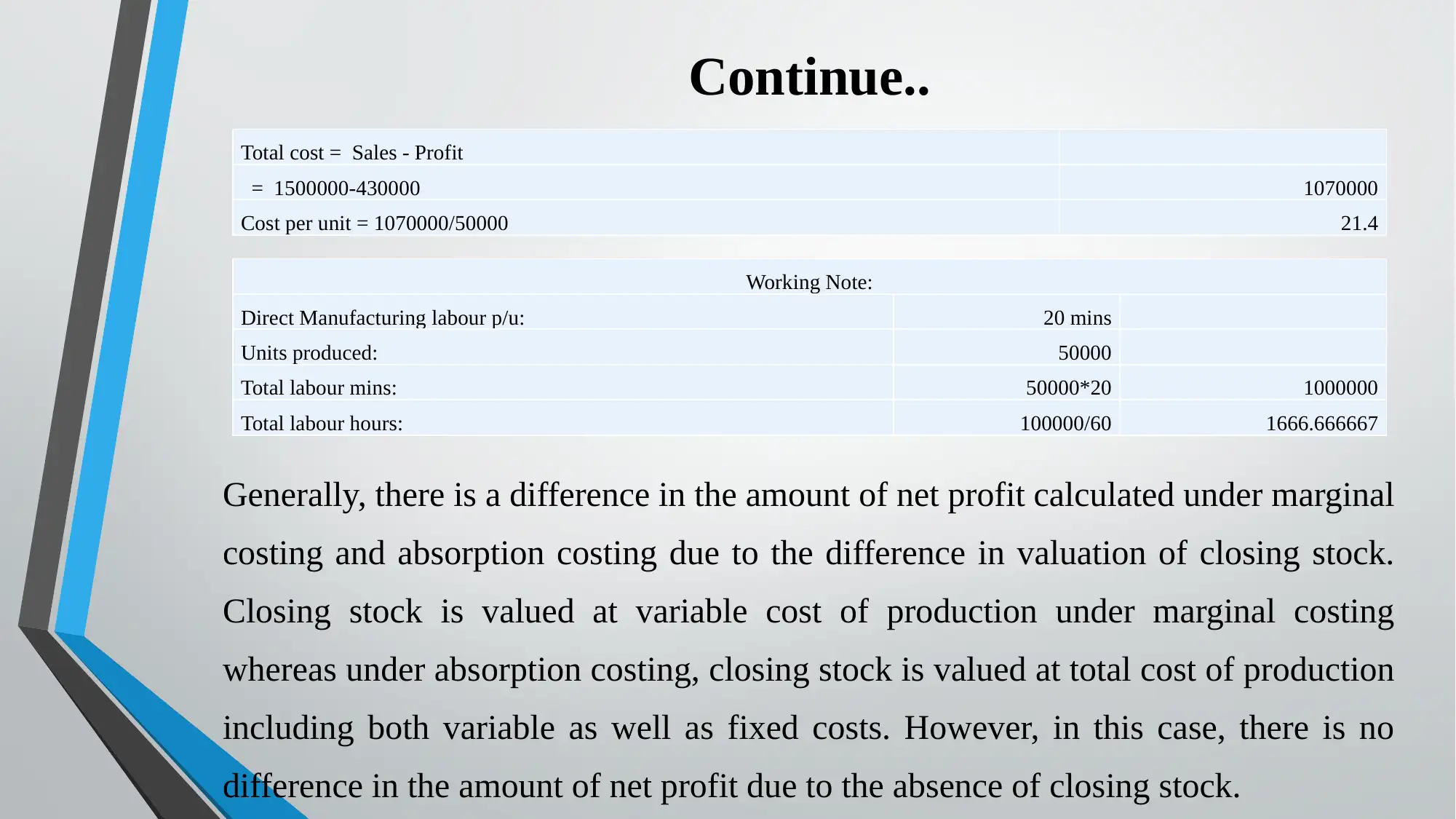

This report delves into the realm of management accounting, specifically analyzing marginal and absorption costing methods. It begins with an introduction to management accounting and then proceeds to analyze the concepts of marginal and absorption costing. The report uses GSQ Limited as a case study to illustrate the application of these costing techniques. The report includes income statements prepared under both marginal and absorption costing, allowing for a comparison of their impacts on profit calculation. The analysis includes working notes to explain the calculations. The report concludes with a recommendation for GSQ Limited on which costing approach is most suitable, and a brief conclusion summarizing the key takeaways. References are provided at the end of the report.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.