Detailed Budget Analysis: A Report on Management Accounting Practices

VerifiedAdded on 2023/06/14

|8

|896

|213

Report

AI Summary

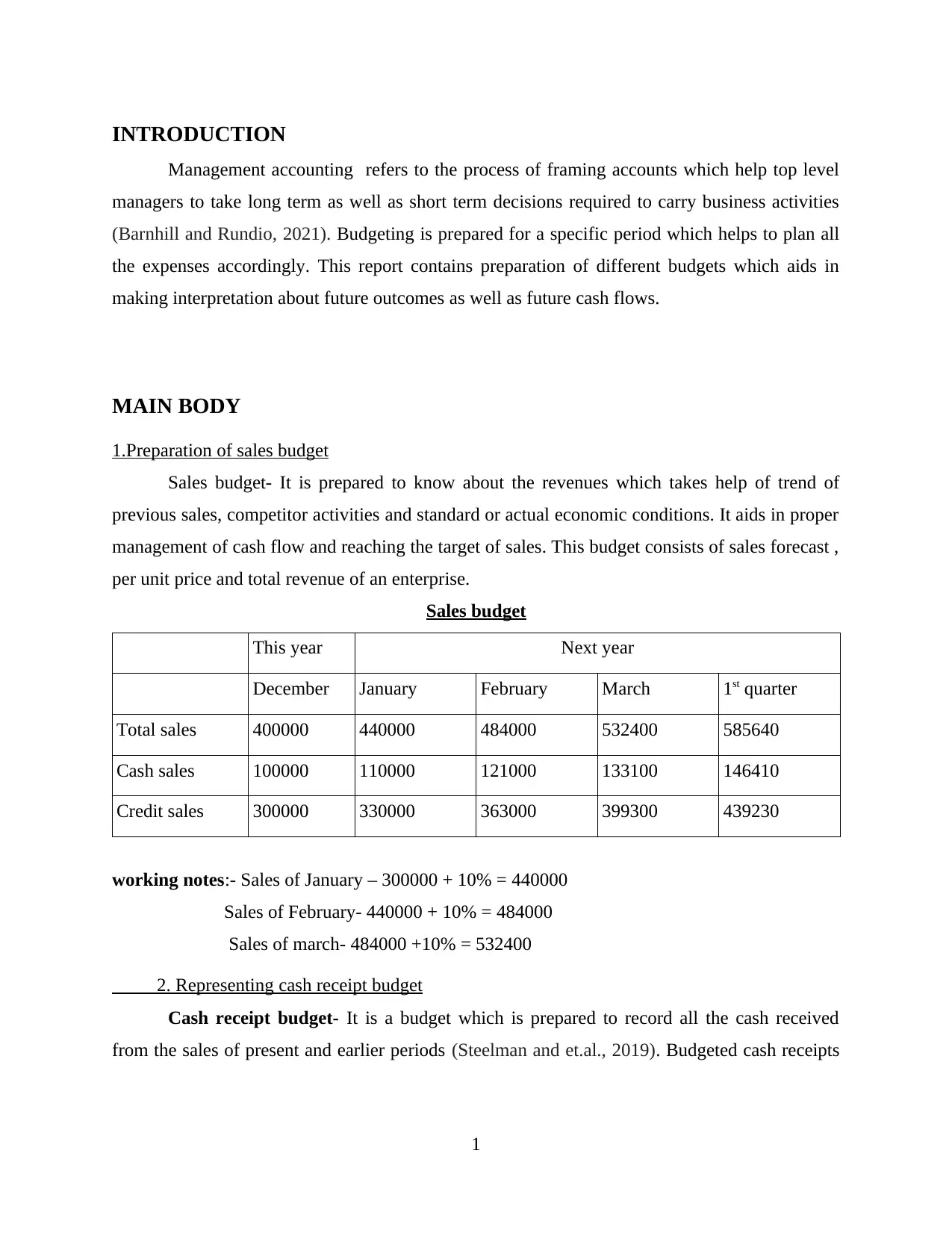

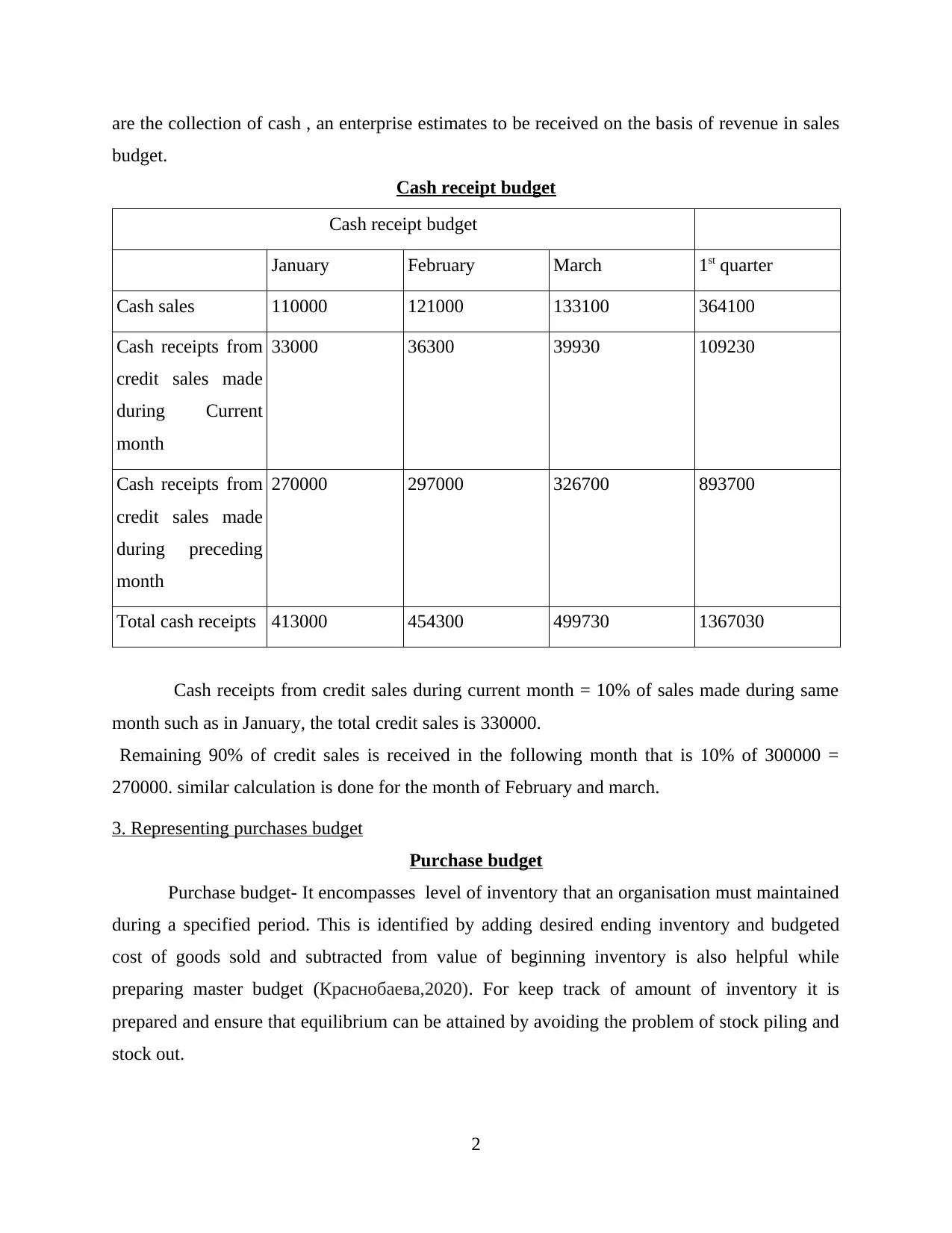

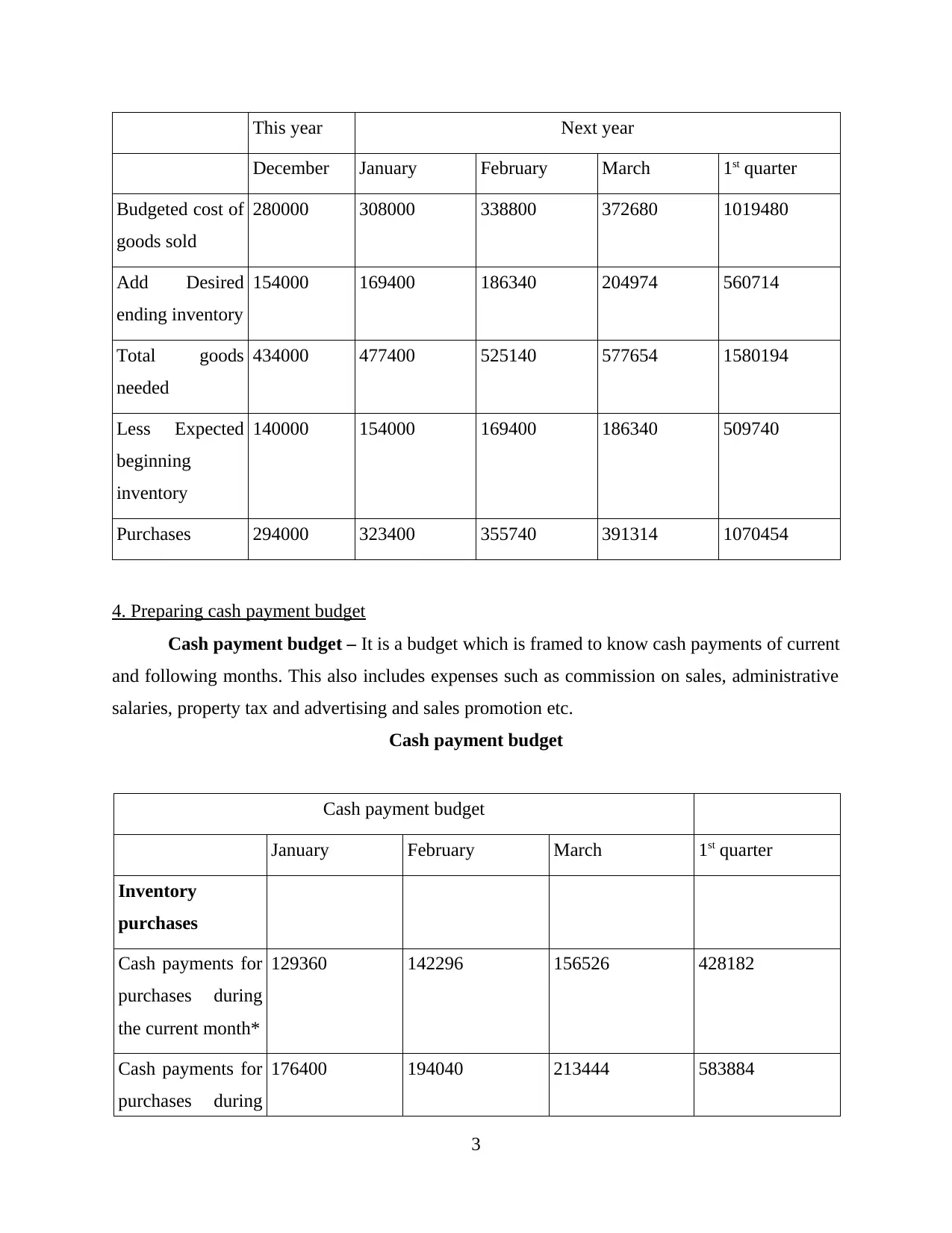

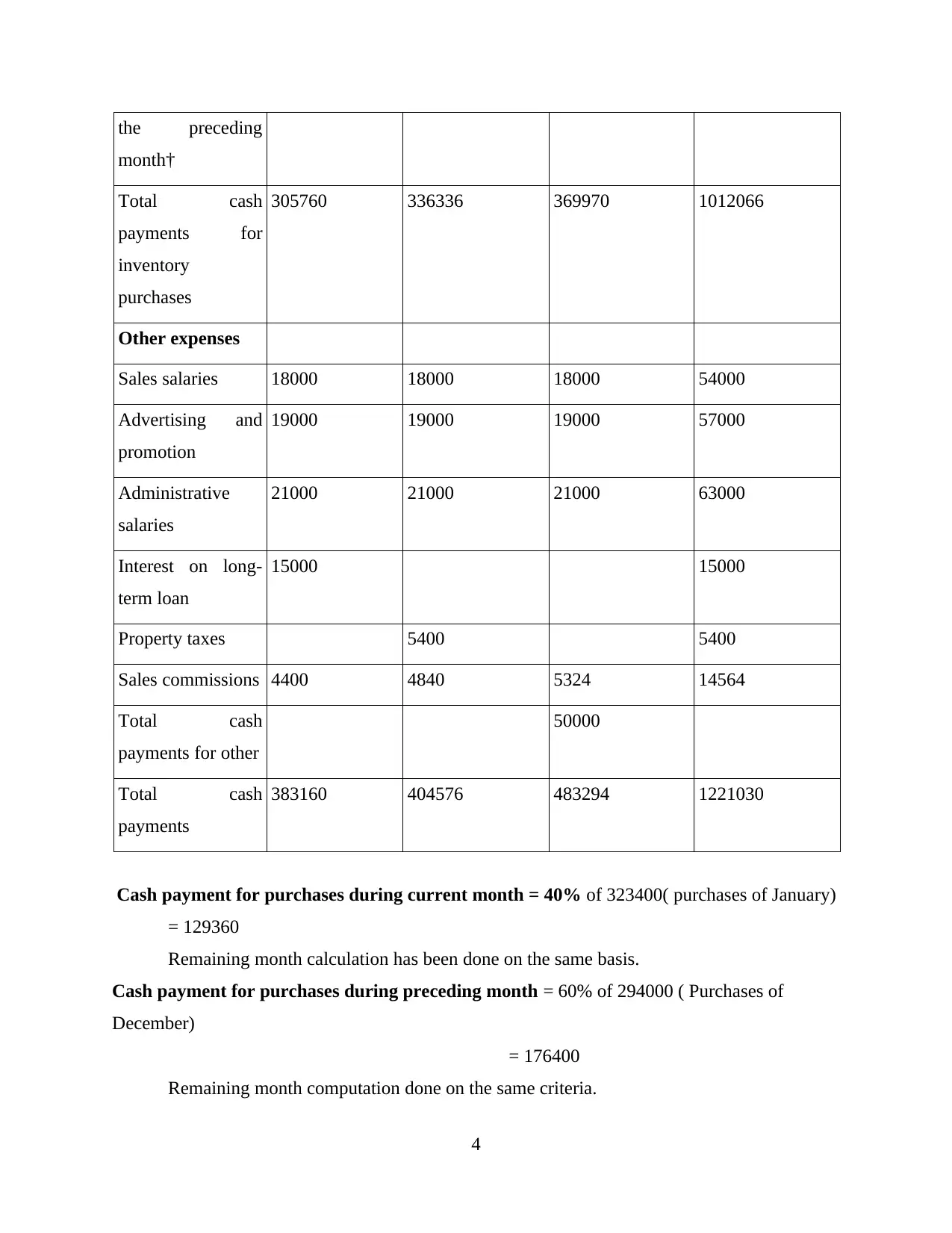

This report delves into management accounting principles, focusing on the preparation and analysis of various budgets. It begins with the construction of a sales budget, utilizing historical sales data and market trends to forecast revenues for the upcoming period. Subsequently, it presents a cash receipt budget, detailing the expected cash inflows from both cash and credit sales, considering collection patterns from previous months. The report also includes a purchases budget, which balances the budgeted cost of goods sold with desired inventory levels to ensure optimal stock management. Furthermore, a cash payment budget is developed to project cash outflows related to inventory purchases and other operational expenses, such as salaries, advertising, and taxes. The analysis provides a comprehensive overview of an organization's financial planning and control mechanisms, essential for effective decision-making and resource allocation. Desklib offers a range of similar solved assignments to aid students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.