Financial Analysis and Decision Making: Playdough Company Case Study

VerifiedAdded on 2019/10/30

|8

|1664

|183

Homework Assignment

AI Summary

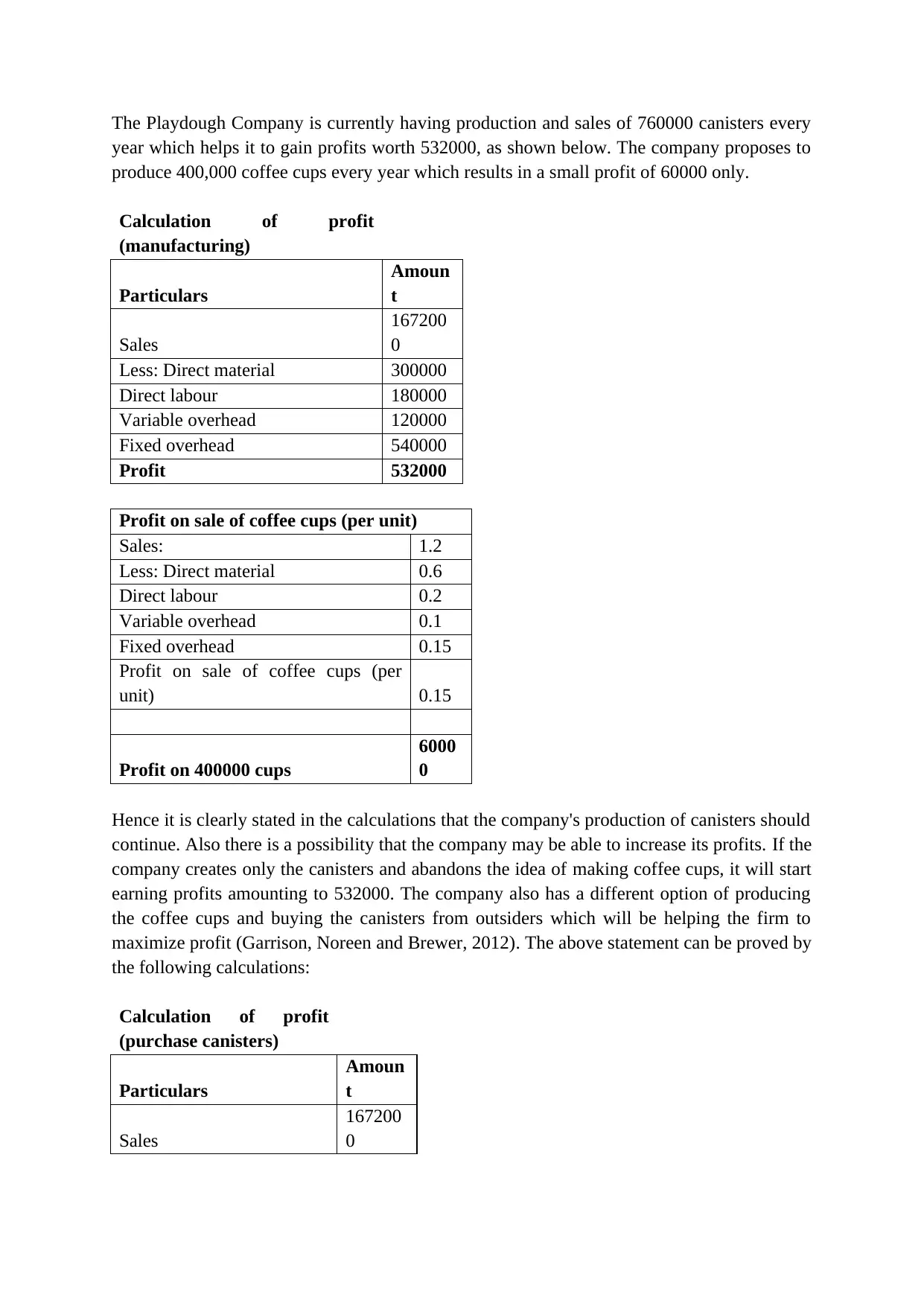

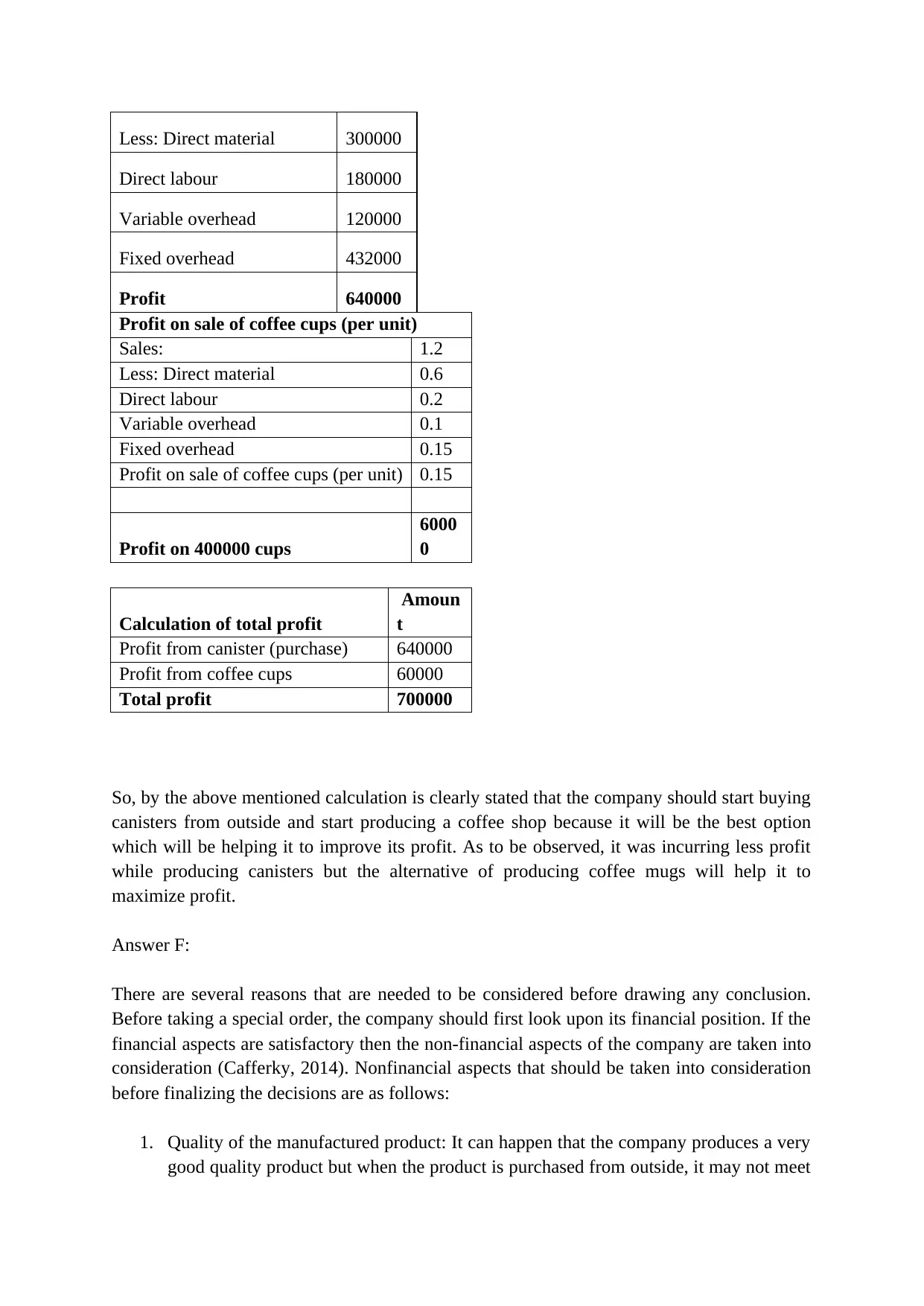

This assignment analyzes the financial decisions of the Playdough Company. It begins with a cost analysis, calculating the cost per canister and examining the impact of variable and fixed costs. The assignment then explores outsourcing, comparing the profitability of in-house manufacturing versus purchasing from an external supplier. It delves into special order decisions, evaluating whether to accept an order at a lower price, considering both financial and non-financial factors. The analysis includes calculations of profit under various scenarios, emphasizing the importance of contribution margin and the potential impact on overall profitability. Finally, the assignment considers the production of coffee cups alongside canisters, assessing the optimal production strategy to maximize profits. The analysis emphasizes that companies should consider both financial and non-financial factors, such as quality, delivery time, and reputation, when making decisions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.