Management Accounting: Calculation of Costs and Expenses with Various Methods

VerifiedAdded on 2023/06/10

|13

|1976

|250

AI Summary

The report explains the importance of Management accounting in a firm, business, company etc. It includes calculation of costs and expenses incurred with the help of various methods. It explains it as a process which states preparation of reports and statements which would be related to business activities and operations. It further is useful in achieving objectives that is laid by a specific firm and interpret the results that would be served by related company over a period of time. Main goal of every business is increase profit, revenue and minimize risk as well as loss too.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................4

QUESTION 1..................................................................................................................................4

a) Direct Method..........................................................................................................................4

b) Step Down Method:.................................................................................................................5

QUESTION 2..................................................................................................................................7

a) Determine the cost for Job MT27 by using reciprocal method...............................................7

b) Which allocation method will be preferred to allocate support department’s costs to

manufacturing departments?........................................................................................................8

QUESTION 3..................................................................................................................................8

a) Calculate the cost per unit for the assembly department........................................................8

QUESTION 4................................................................................................................................10

a) Compute the Break-even point and also calculate operating profit.......................................10

(b) Assuming sales to 17500 units.............................................................................................11

(c) What would be new Break Even Pointy and operating income...........................................11

(d) Explain the comment...........................................................................................................11

QUESTION 5................................................................................................................................12

a) Explain the ethical behaviour and how its impact on the customers and the company.........12

b) If John behaves unethically, how would his behaviour impact the company and its

customers?.................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................4

QUESTION 1..................................................................................................................................4

a) Direct Method..........................................................................................................................4

b) Step Down Method:.................................................................................................................5

QUESTION 2..................................................................................................................................7

a) Determine the cost for Job MT27 by using reciprocal method...............................................7

b) Which allocation method will be preferred to allocate support department’s costs to

manufacturing departments?........................................................................................................8

QUESTION 3..................................................................................................................................8

a) Calculate the cost per unit for the assembly department........................................................8

QUESTION 4................................................................................................................................10

a) Compute the Break-even point and also calculate operating profit.......................................10

(b) Assuming sales to 17500 units.............................................................................................11

(c) What would be new Break Even Pointy and operating income...........................................11

(d) Explain the comment...........................................................................................................11

QUESTION 5................................................................................................................................12

a) Explain the ethical behaviour and how its impact on the customers and the company.........12

b) If John behaves unethically, how would his behaviour impact the company and its

customers?.................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The report prepared below explains the importance of Management accounting in a firm,

business, company etc. It includes calculation of costs and expenses incurred with the help of

various methods. It explains it as a process which states preparation of reports and statements

which would be related to business activities and operations (Hoozée, S., & Mitchell, F. (2018)).

It further is useful in achieving objectives that is laid by a specific firm and interpret the results

that would be served by related company over a period of time. Main goal of every business is

increase profit, revenue and minimize risk as well as loss too. It also facilitates important and

necessary decision making as well. The report further provides an idea related to various

functions being performed by the organisation. Accounting is useful in undertaking various

activities such as planning, organising, directing and controlling which is being followed by the

company. It also gives an idea about various budgets that would be required for better results and

planning unusual strategies that would help to perform actions that would be helpful for better

outcomes. The user can assess which area is producing and involving more costs compared to

other areas.

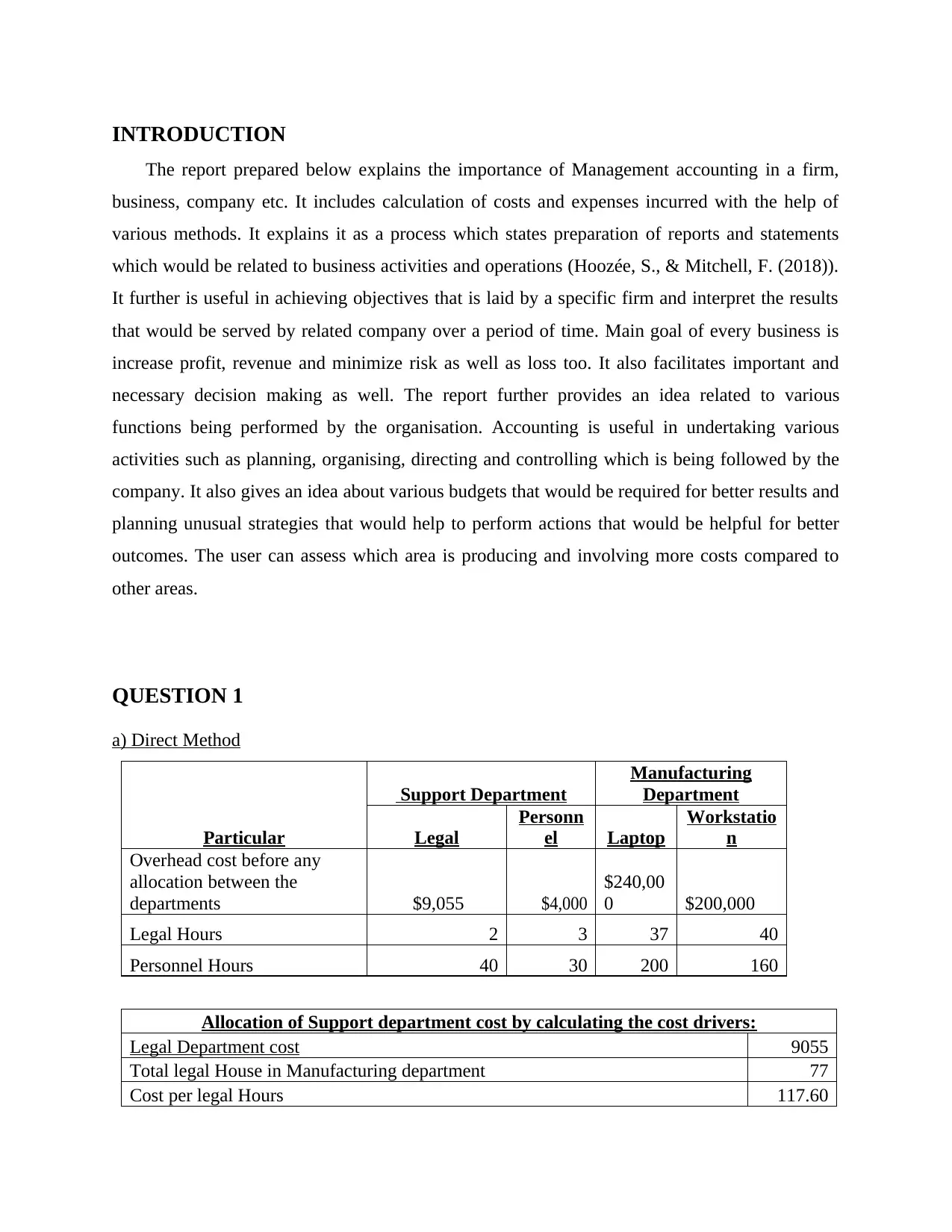

QUESTION 1

a) Direct Method

Particular

Support Department

Manufacturing

Department

Legal

Personn

el Laptop

Workstatio

n

Overhead cost before any

allocation between the

departments $9,055 $4,000

$240,00

0 $200,000

Legal Hours 2 3 37 40

Personnel Hours 40 30 200 160

Allocation of Support department cost by calculating the cost drivers:

Legal Department cost 9055

Total legal House in Manufacturing department 77

Cost per legal Hours 117.60

The report prepared below explains the importance of Management accounting in a firm,

business, company etc. It includes calculation of costs and expenses incurred with the help of

various methods. It explains it as a process which states preparation of reports and statements

which would be related to business activities and operations (Hoozée, S., & Mitchell, F. (2018)).

It further is useful in achieving objectives that is laid by a specific firm and interpret the results

that would be served by related company over a period of time. Main goal of every business is

increase profit, revenue and minimize risk as well as loss too. It also facilitates important and

necessary decision making as well. The report further provides an idea related to various

functions being performed by the organisation. Accounting is useful in undertaking various

activities such as planning, organising, directing and controlling which is being followed by the

company. It also gives an idea about various budgets that would be required for better results and

planning unusual strategies that would help to perform actions that would be helpful for better

outcomes. The user can assess which area is producing and involving more costs compared to

other areas.

QUESTION 1

a) Direct Method

Particular

Support Department

Manufacturing

Department

Legal

Personn

el Laptop

Workstatio

n

Overhead cost before any

allocation between the

departments $9,055 $4,000

$240,00

0 $200,000

Legal Hours 2 3 37 40

Personnel Hours 40 30 200 160

Allocation of Support department cost by calculating the cost drivers:

Legal Department cost 9055

Total legal House in Manufacturing department 77

Cost per legal Hours 117.60

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Personnel Department Cost 4000

Total personnel hours in manufacturing department 360

Cost per personnel hours 11.11

Allocation of Support

department cost to

manufacturing department

Particular Laptop Department Workstation Department

Legal Department 4351.10 4703.90

Personnel Department 2222.22 1777.78

Cost allocation of Manufacturing Department

Particular

Lega

l Personal Laptop

Workstatio

n

Total cost incurred 9055 4000 240000 200000

Allocation of legal -9055 4351.1 4703.9

Allocation of Personnel -4000 2222.22 1777.78

Total Cost of Manufacturing

Department Nil Nil

246573.3

2 206481.68

b) Step Down Method:

Allocation of legal department cost by calculating the cost drivers:

Legal Department cost 9055

Total legal Hours Except Legal 80

Cost per legal Hours 113.19

Allocation of Legal Department cost to other department by calculating

cost drivers

Total personnel hours in manufacturing department 360

Cost per personnel hours 11.11

Allocation of Support

department cost to

manufacturing department

Particular Laptop Department Workstation Department

Legal Department 4351.10 4703.90

Personnel Department 2222.22 1777.78

Cost allocation of Manufacturing Department

Particular

Lega

l Personal Laptop

Workstatio

n

Total cost incurred 9055 4000 240000 200000

Allocation of legal -9055 4351.1 4703.9

Allocation of Personnel -4000 2222.22 1777.78

Total Cost of Manufacturing

Department Nil Nil

246573.3

2 206481.68

b) Step Down Method:

Allocation of legal department cost by calculating the cost drivers:

Legal Department cost 9055

Total legal Hours Except Legal 80

Cost per legal Hours 113.19

Allocation of Legal Department cost to other department by calculating

cost drivers

Particular Personnel Laptop

Workstatio

n

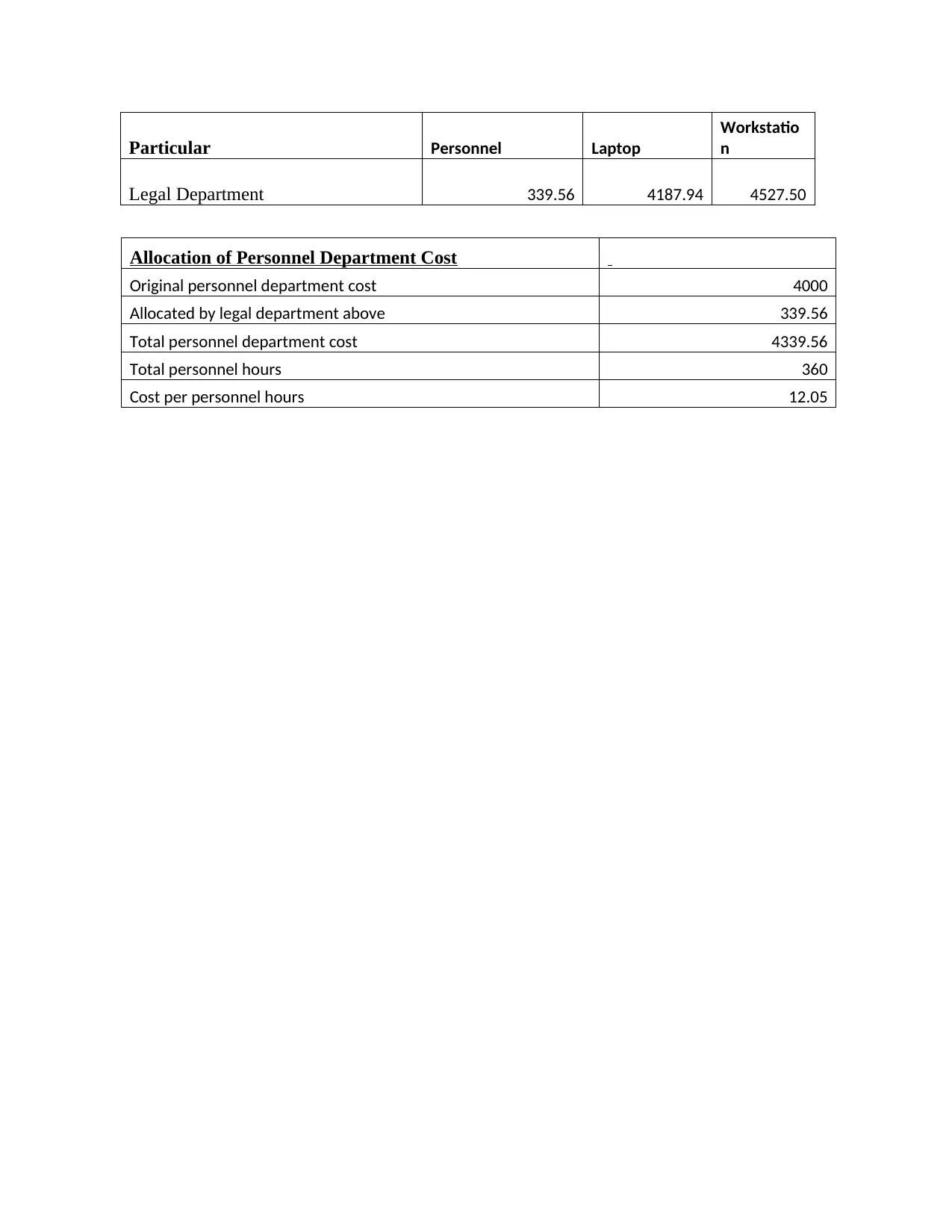

Legal Department 339.56 4187.94 4527.50

Allocation of Personnel Department Cost

Original personnel department cost 4000

Allocated by legal department above 339.56

Total personnel department cost 4339.56

Total personnel hours 360

Cost per personnel hours 12.05

Workstatio

n

Legal Department 339.56 4187.94 4527.50

Allocation of Personnel Department Cost

Original personnel department cost 4000

Allocated by legal department above 339.56

Total personnel department cost 4339.56

Total personnel hours 360

Cost per personnel hours 12.05

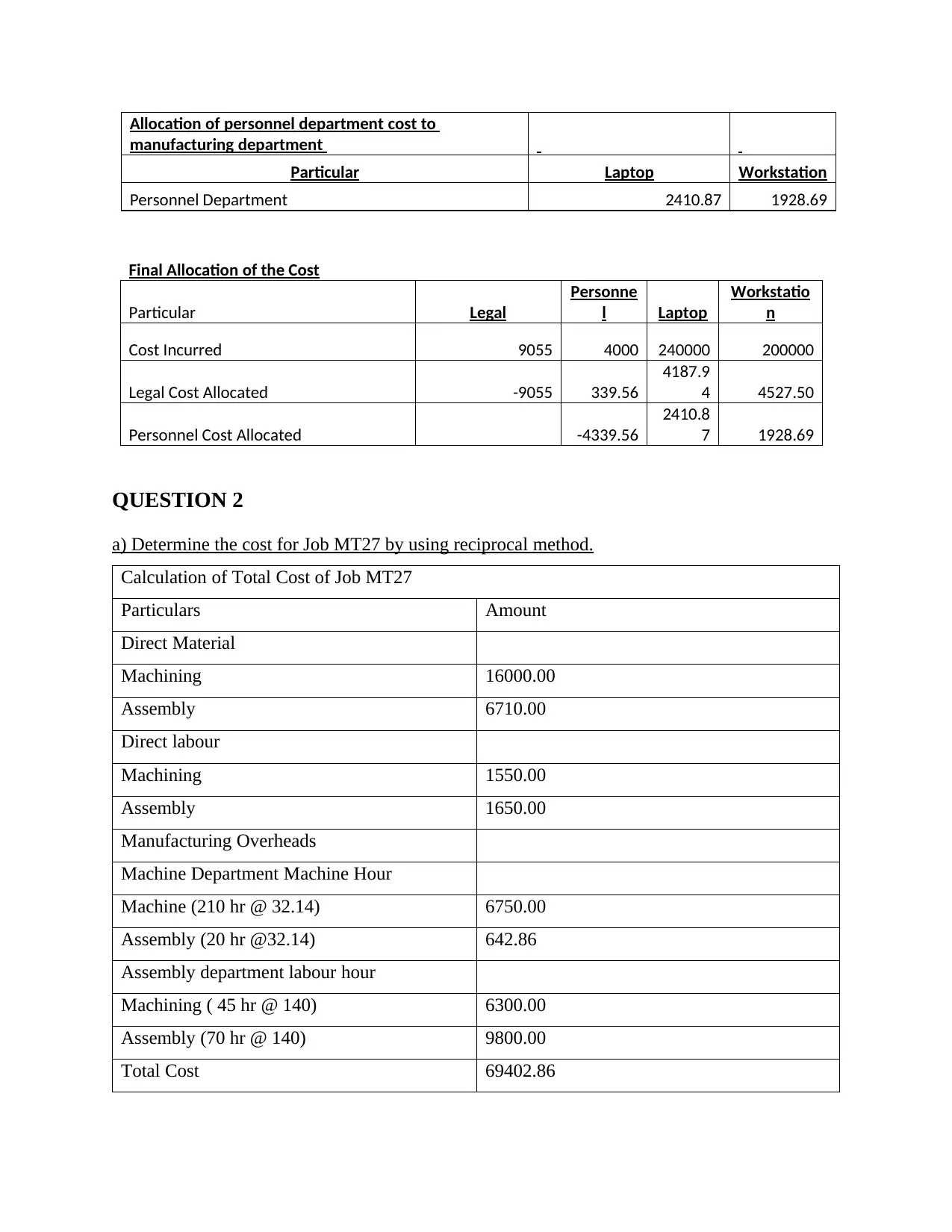

Allocation of personnel department cost to

manufacturing department

Particular Laptop Workstation

Personnel Department 2410.87 1928.69

Final Allocation of the Cost

Particular Legal

Personne

l Laptop

Workstatio

n

Cost Incurred 9055 4000 240000 200000

Legal Cost Allocated -9055 339.56

4187.9

4 4527.50

Personnel Cost Allocated -4339.56

2410.8

7 1928.69

QUESTION 2

a) Determine the cost for Job MT27 by using reciprocal method.

Calculation of Total Cost of Job MT27

Particulars Amount

Direct Material

Machining 16000.00

Assembly 6710.00

Direct labour

Machining 1550.00

Assembly 1650.00

Manufacturing Overheads

Machine Department Machine Hour

Machine (210 hr @ 32.14) 6750.00

Assembly (20 hr @32.14) 642.86

Assembly department labour hour

Machining ( 45 hr @ 140) 6300.00

Assembly (70 hr @ 140) 9800.00

Total Cost 69402.86

manufacturing department

Particular Laptop Workstation

Personnel Department 2410.87 1928.69

Final Allocation of the Cost

Particular Legal

Personne

l Laptop

Workstatio

n

Cost Incurred 9055 4000 240000 200000

Legal Cost Allocated -9055 339.56

4187.9

4 4527.50

Personnel Cost Allocated -4339.56

2410.8

7 1928.69

QUESTION 2

a) Determine the cost for Job MT27 by using reciprocal method.

Calculation of Total Cost of Job MT27

Particulars Amount

Direct Material

Machining 16000.00

Assembly 6710.00

Direct labour

Machining 1550.00

Assembly 1650.00

Manufacturing Overheads

Machine Department Machine Hour

Machine (210 hr @ 32.14) 6750.00

Assembly (20 hr @32.14) 642.86

Assembly department labour hour

Machining ( 45 hr @ 140) 6300.00

Assembly (70 hr @ 140) 9800.00

Total Cost 69402.86

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

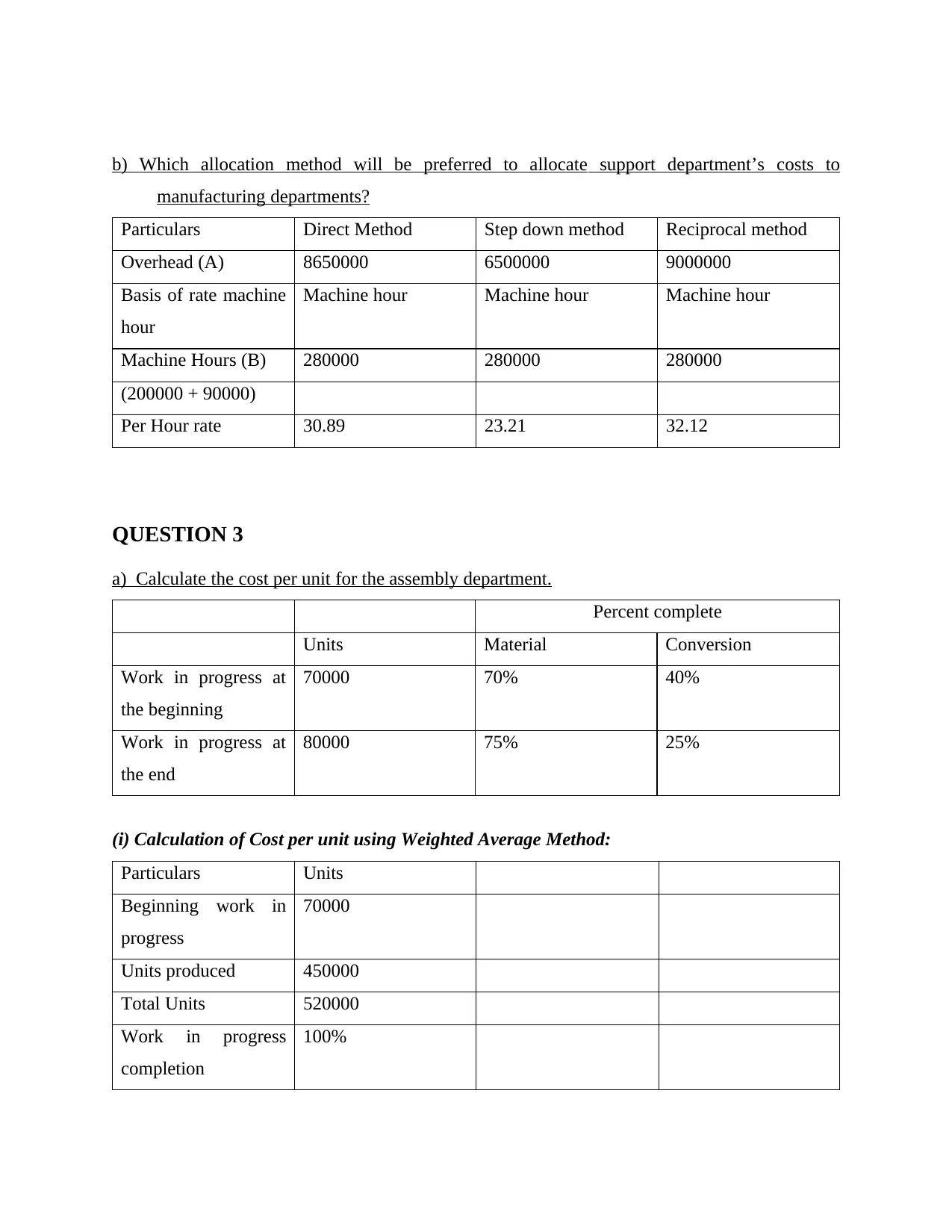

b) Which allocation method will be preferred to allocate support department’s costs to

manufacturing departments?

Particulars Direct Method Step down method Reciprocal method

Overhead (A) 8650000 6500000 9000000

Basis of rate machine

hour

Machine hour Machine hour Machine hour

Machine Hours (B) 280000 280000 280000

(200000 + 90000)

Per Hour rate 30.89 23.21 32.12

QUESTION 3

a) Calculate the cost per unit for the assembly department.

Percent complete

Units Material Conversion

Work in progress at

the beginning

70000 70% 40%

Work in progress at

the end

80000 75% 25%

(i) Calculation of Cost per unit using Weighted Average Method:

Particulars Units

Beginning work in

progress

70000

Units produced 450000

Total Units 520000

Work in progress

completion

100%

manufacturing departments?

Particulars Direct Method Step down method Reciprocal method

Overhead (A) 8650000 6500000 9000000

Basis of rate machine

hour

Machine hour Machine hour Machine hour

Machine Hours (B) 280000 280000 280000

(200000 + 90000)

Per Hour rate 30.89 23.21 32.12

QUESTION 3

a) Calculate the cost per unit for the assembly department.

Percent complete

Units Material Conversion

Work in progress at

the beginning

70000 70% 40%

Work in progress at

the end

80000 75% 25%

(i) Calculation of Cost per unit using Weighted Average Method:

Particulars Units

Beginning work in

progress

70000

Units produced 450000

Total Units 520000

Work in progress

completion

100%

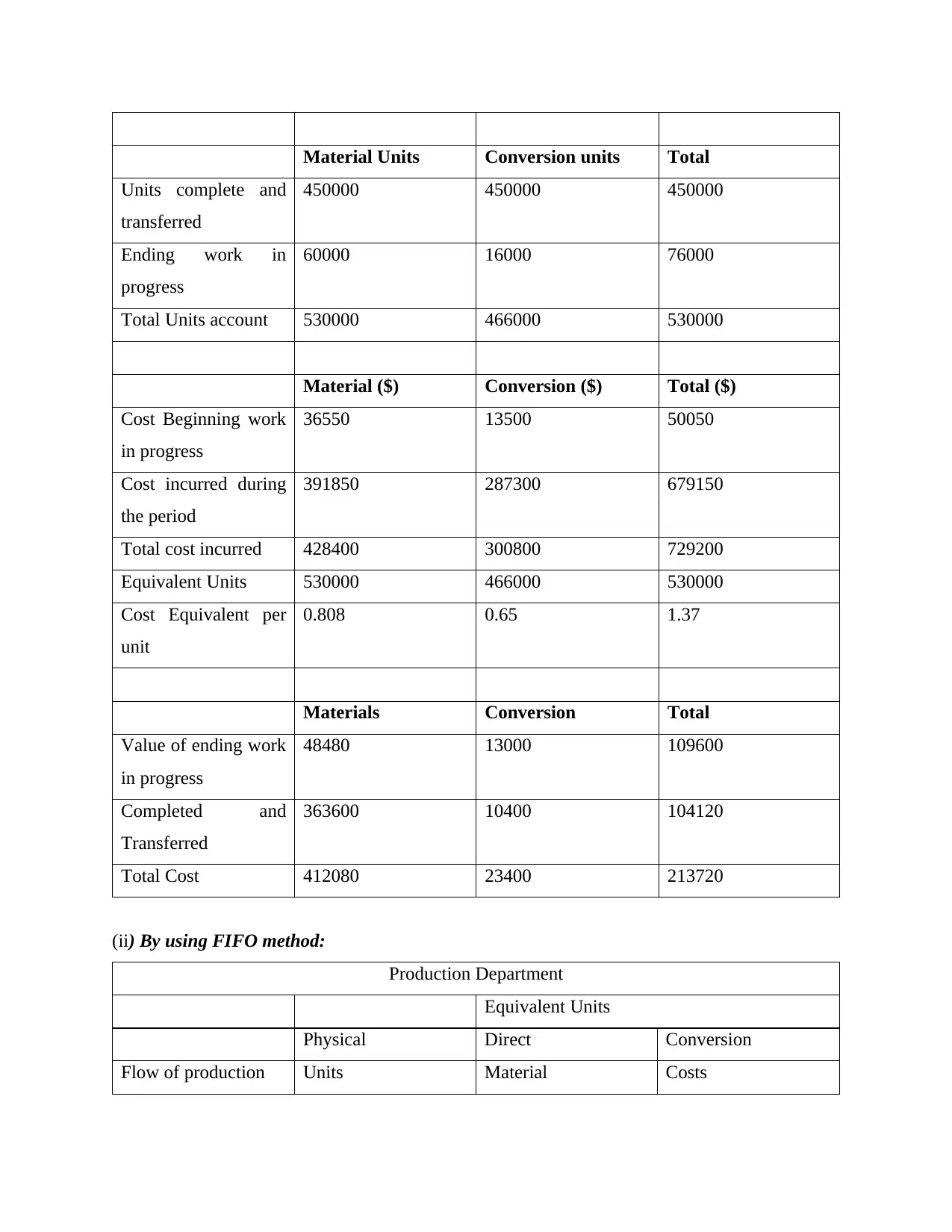

Material Units Conversion units Total

Units complete and

transferred

450000 450000 450000

Ending work in

progress

60000 16000 76000

Total Units account 530000 466000 530000

Material ($) Conversion ($) Total ($)

Cost Beginning work

in progress

36550 13500 50050

Cost incurred during

the period

391850 287300 679150

Total cost incurred 428400 300800 729200

Equivalent Units 530000 466000 530000

Cost Equivalent per

unit

0.808 0.65 1.37

Materials Conversion Total

Value of ending work

in progress

48480 13000 109600

Completed and

Transferred

363600 10400 104120

Total Cost 412080 23400 213720

(ii) By using FIFO method:

Production Department

Equivalent Units

Physical Direct Conversion

Flow of production Units Material Costs

Units complete and

transferred

450000 450000 450000

Ending work in

progress

60000 16000 76000

Total Units account 530000 466000 530000

Material ($) Conversion ($) Total ($)

Cost Beginning work

in progress

36550 13500 50050

Cost incurred during

the period

391850 287300 679150

Total cost incurred 428400 300800 729200

Equivalent Units 530000 466000 530000

Cost Equivalent per

unit

0.808 0.65 1.37

Materials Conversion Total

Value of ending work

in progress

48480 13000 109600

Completed and

Transferred

363600 10400 104120

Total Cost 412080 23400 213720

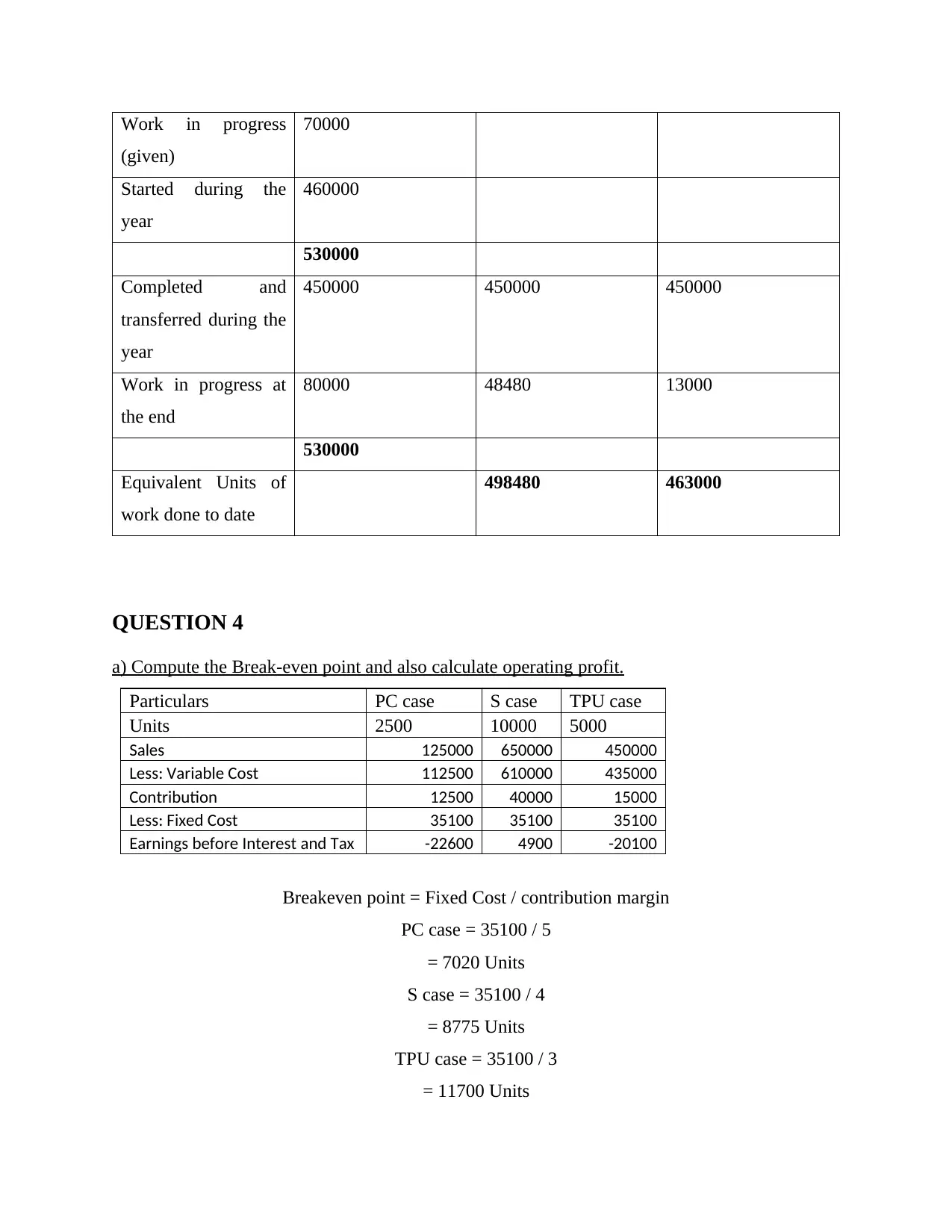

(ii) By using FIFO method:

Production Department

Equivalent Units

Physical Direct Conversion

Flow of production Units Material Costs

Work in progress

(given)

70000

Started during the

year

460000

530000

Completed and

transferred during the

year

450000 450000 450000

Work in progress at

the end

80000 48480 13000

530000

Equivalent Units of

work done to date

498480 463000

QUESTION 4

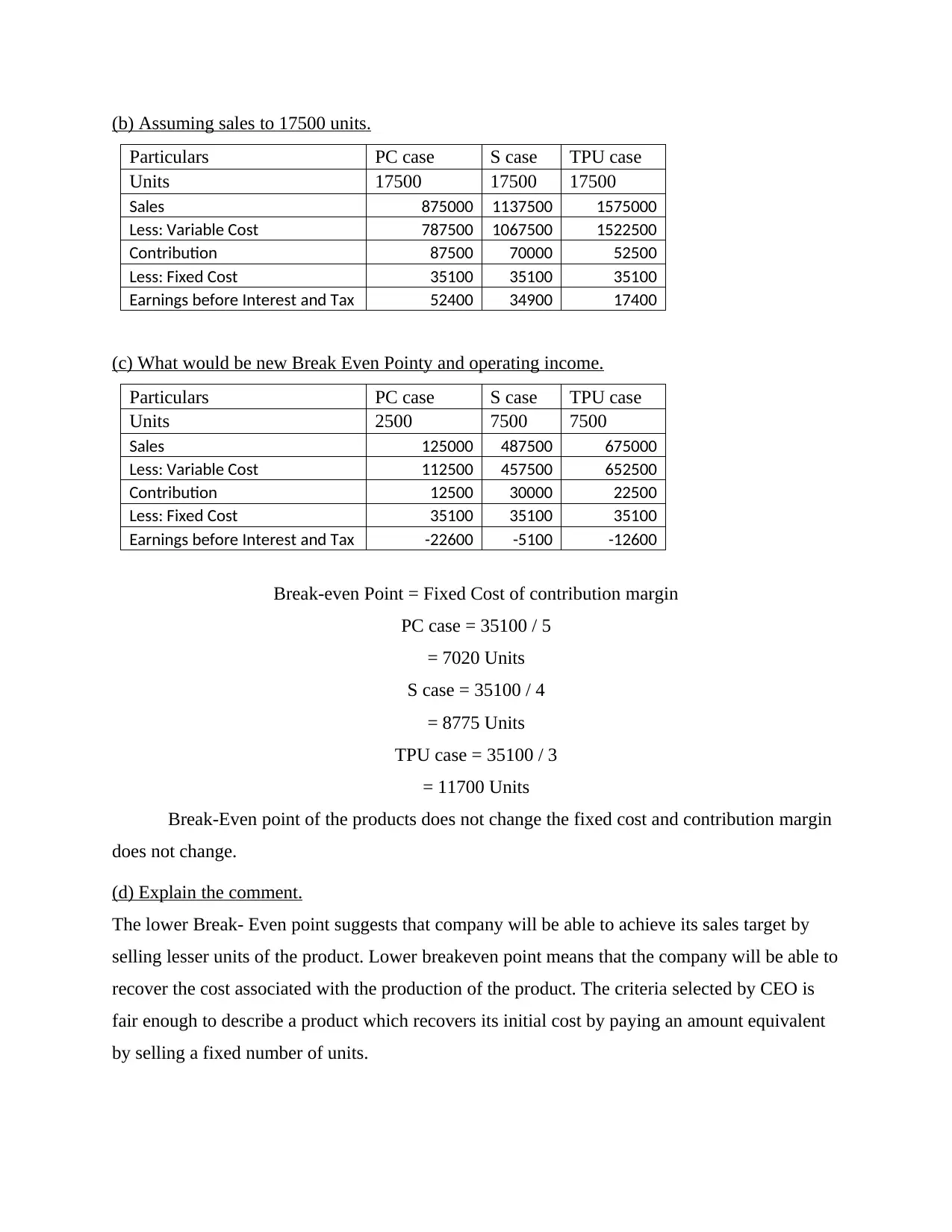

a) Compute the Break-even point and also calculate operating profit.

Particulars PC case S case TPU case

Units 2500 10000 5000

Sales 125000 650000 450000

Less: Variable Cost 112500 610000 435000

Contribution 12500 40000 15000

Less: Fixed Cost 35100 35100 35100

Earnings before Interest and Tax -22600 4900 -20100

Breakeven point = Fixed Cost / contribution margin

PC case = 35100 / 5

= 7020 Units

S case = 35100 / 4

= 8775 Units

TPU case = 35100 / 3

= 11700 Units

(given)

70000

Started during the

year

460000

530000

Completed and

transferred during the

year

450000 450000 450000

Work in progress at

the end

80000 48480 13000

530000

Equivalent Units of

work done to date

498480 463000

QUESTION 4

a) Compute the Break-even point and also calculate operating profit.

Particulars PC case S case TPU case

Units 2500 10000 5000

Sales 125000 650000 450000

Less: Variable Cost 112500 610000 435000

Contribution 12500 40000 15000

Less: Fixed Cost 35100 35100 35100

Earnings before Interest and Tax -22600 4900 -20100

Breakeven point = Fixed Cost / contribution margin

PC case = 35100 / 5

= 7020 Units

S case = 35100 / 4

= 8775 Units

TPU case = 35100 / 3

= 11700 Units

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

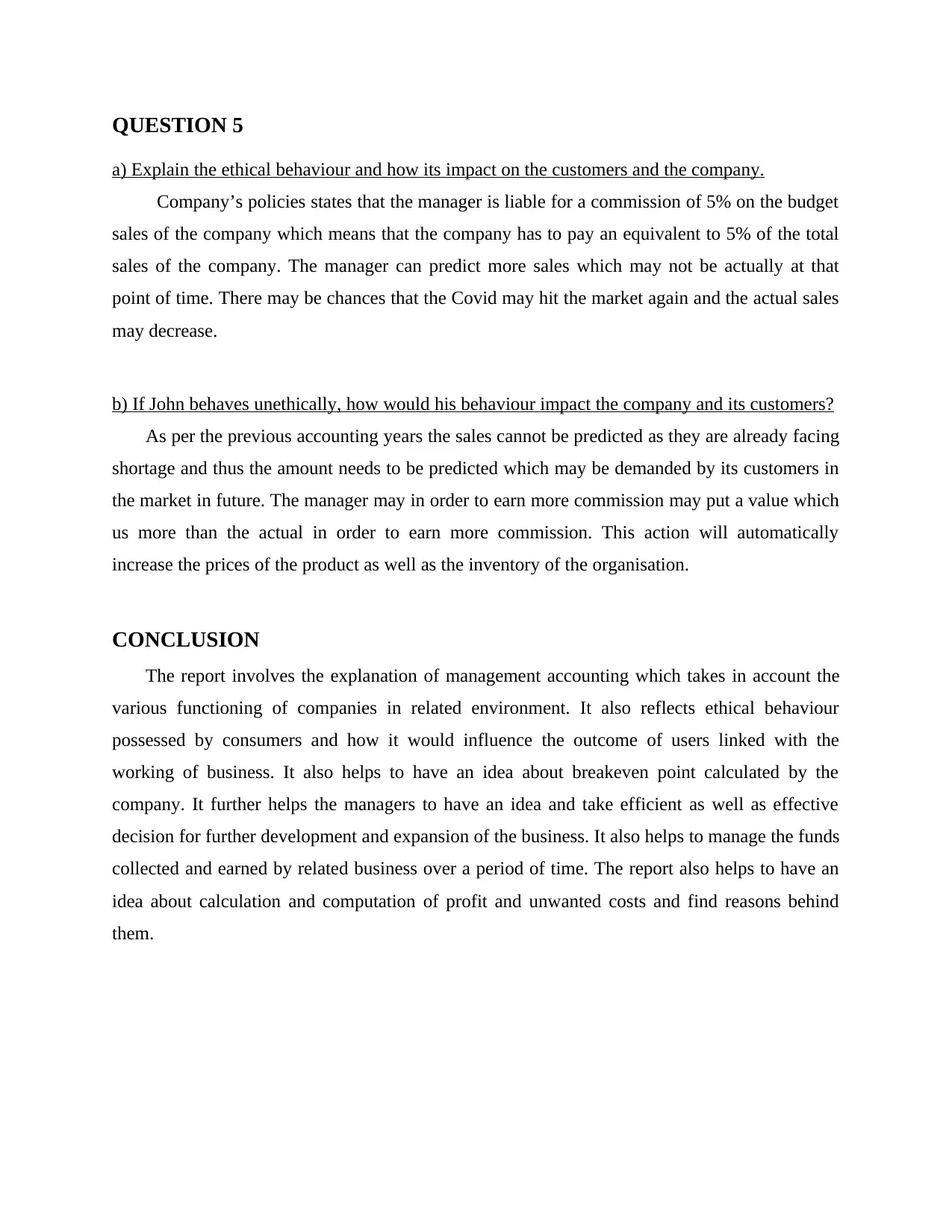

(b) Assuming sales to 17500 units.

Particulars PC case S case TPU case

Units 17500 17500 17500

Sales 875000 1137500 1575000

Less: Variable Cost 787500 1067500 1522500

Contribution 87500 70000 52500

Less: Fixed Cost 35100 35100 35100

Earnings before Interest and Tax 52400 34900 17400

(c) What would be new Break Even Pointy and operating income.

Particulars PC case S case TPU case

Units 2500 7500 7500

Sales 125000 487500 675000

Less: Variable Cost 112500 457500 652500

Contribution 12500 30000 22500

Less: Fixed Cost 35100 35100 35100

Earnings before Interest and Tax -22600 -5100 -12600

Break-even Point = Fixed Cost of contribution margin

PC case = 35100 / 5

= 7020 Units

S case = 35100 / 4

= 8775 Units

TPU case = 35100 / 3

= 11700 Units

Break-Even point of the products does not change the fixed cost and contribution margin

does not change.

(d) Explain the comment.

The lower Break- Even point suggests that company will be able to achieve its sales target by

selling lesser units of the product. Lower breakeven point means that the company will be able to

recover the cost associated with the production of the product. The criteria selected by CEO is

fair enough to describe a product which recovers its initial cost by paying an amount equivalent

by selling a fixed number of units.

Particulars PC case S case TPU case

Units 17500 17500 17500

Sales 875000 1137500 1575000

Less: Variable Cost 787500 1067500 1522500

Contribution 87500 70000 52500

Less: Fixed Cost 35100 35100 35100

Earnings before Interest and Tax 52400 34900 17400

(c) What would be new Break Even Pointy and operating income.

Particulars PC case S case TPU case

Units 2500 7500 7500

Sales 125000 487500 675000

Less: Variable Cost 112500 457500 652500

Contribution 12500 30000 22500

Less: Fixed Cost 35100 35100 35100

Earnings before Interest and Tax -22600 -5100 -12600

Break-even Point = Fixed Cost of contribution margin

PC case = 35100 / 5

= 7020 Units

S case = 35100 / 4

= 8775 Units

TPU case = 35100 / 3

= 11700 Units

Break-Even point of the products does not change the fixed cost and contribution margin

does not change.

(d) Explain the comment.

The lower Break- Even point suggests that company will be able to achieve its sales target by

selling lesser units of the product. Lower breakeven point means that the company will be able to

recover the cost associated with the production of the product. The criteria selected by CEO is

fair enough to describe a product which recovers its initial cost by paying an amount equivalent

by selling a fixed number of units.

QUESTION 5

a) Explain the ethical behaviour and how its impact on the customers and the company.

Company’s policies states that the manager is liable for a commission of 5% on the budget

sales of the company which means that the company has to pay an equivalent to 5% of the total

sales of the company. The manager can predict more sales which may not be actually at that

point of time. There may be chances that the Covid may hit the market again and the actual sales

may decrease.

b) If John behaves unethically, how would his behaviour impact the company and its customers?

As per the previous accounting years the sales cannot be predicted as they are already facing

shortage and thus the amount needs to be predicted which may be demanded by its customers in

the market in future. The manager may in order to earn more commission may put a value which

us more than the actual in order to earn more commission. This action will automatically

increase the prices of the product as well as the inventory of the organisation.

CONCLUSION

The report involves the explanation of management accounting which takes in account the

various functioning of companies in related environment. It also reflects ethical behaviour

possessed by consumers and how it would influence the outcome of users linked with the

working of business. It also helps to have an idea about breakeven point calculated by the

company. It further helps the managers to have an idea and take efficient as well as effective

decision for further development and expansion of the business. It also helps to manage the funds

collected and earned by related business over a period of time. The report also helps to have an

idea about calculation and computation of profit and unwanted costs and find reasons behind

them.

a) Explain the ethical behaviour and how its impact on the customers and the company.

Company’s policies states that the manager is liable for a commission of 5% on the budget

sales of the company which means that the company has to pay an equivalent to 5% of the total

sales of the company. The manager can predict more sales which may not be actually at that

point of time. There may be chances that the Covid may hit the market again and the actual sales

may decrease.

b) If John behaves unethically, how would his behaviour impact the company and its customers?

As per the previous accounting years the sales cannot be predicted as they are already facing

shortage and thus the amount needs to be predicted which may be demanded by its customers in

the market in future. The manager may in order to earn more commission may put a value which

us more than the actual in order to earn more commission. This action will automatically

increase the prices of the product as well as the inventory of the organisation.

CONCLUSION

The report involves the explanation of management accounting which takes in account the

various functioning of companies in related environment. It also reflects ethical behaviour

possessed by consumers and how it would influence the outcome of users linked with the

working of business. It also helps to have an idea about breakeven point calculated by the

company. It further helps the managers to have an idea and take efficient as well as effective

decision for further development and expansion of the business. It also helps to manage the funds

collected and earned by related business over a period of time. The report also helps to have an

idea about calculation and computation of profit and unwanted costs and find reasons behind

them.

REFERENCES

Books and Journals

Atrill, P., & Lindley, L. (Eds.). (2019). Issues in Accounting and Finance. Routledge.

Birnberg, J. G., & Shields, M. D. (2020). Journal of Management Accounting Research at 30

years: reflections on its context, creation, challenges, and contributions. Journal of

Management Accounting Research, 32(1), 1-10.

Holopainen, R. M., Niskanen, M., & Rissanen, S. (2019). Management accounting and

profitability in private healthcare SMEs. International Journal of Public and Private

Perspectives on Healthcare, Culture, and the Environment (IJPPPHCE), 3(1), 28-44.

Hoozée, S., & Mitchell, F. (2018). Who influences the design of management accounting

systems? An exploratory study. Australian Accounting Review, 28(3), 374-390.

Islam, M. A. (2018). Environmental accounting. In Encyclopedia of Business and Professional

Ethics. Springer International Publishing AG.

Nobakh, Y. (2018). Scientometrics of Behavioral Accounting Research in Iran. Journal of

Management Accounting and Auditing Knowledge, 7(27), 125-136.

Pelz, M. (2019). Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management Reviews, 21(2),

256-274.

Books and Journals

Atrill, P., & Lindley, L. (Eds.). (2019). Issues in Accounting and Finance. Routledge.

Birnberg, J. G., & Shields, M. D. (2020). Journal of Management Accounting Research at 30

years: reflections on its context, creation, challenges, and contributions. Journal of

Management Accounting Research, 32(1), 1-10.

Holopainen, R. M., Niskanen, M., & Rissanen, S. (2019). Management accounting and

profitability in private healthcare SMEs. International Journal of Public and Private

Perspectives on Healthcare, Culture, and the Environment (IJPPPHCE), 3(1), 28-44.

Hoozée, S., & Mitchell, F. (2018). Who influences the design of management accounting

systems? An exploratory study. Australian Accounting Review, 28(3), 374-390.

Islam, M. A. (2018). Environmental accounting. In Encyclopedia of Business and Professional

Ethics. Springer International Publishing AG.

Nobakh, Y. (2018). Scientometrics of Behavioral Accounting Research in Iran. Journal of

Management Accounting and Auditing Knowledge, 7(27), 125-136.

Pelz, M. (2019). Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management Reviews, 21(2),

256-274.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.