Management Accounting Case | Question and Answer

VerifiedAdded on 2022/08/31

|10

|1370

|18

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING

Table of Contents

Question 1......................................................................................................................2

Question 2......................................................................................................................3

Part a...........................................................................................................................3

Part b..........................................................................................................................3

Part c...........................................................................................................................4

Question 3......................................................................................................................4

Part a...........................................................................................................................4

Part b..........................................................................................................................5

Question 4......................................................................................................................6

Part a...........................................................................................................................6

Part b..........................................................................................................................7

Question 5......................................................................................................................7

Question 6......................................................................................................................8

Part a...........................................................................................................................8

Part b..........................................................................................................................9

Bibliography...................................................................................................................9

MANAGEMENT ACCOUNTING

Table of Contents

Question 1......................................................................................................................2

Question 2......................................................................................................................3

Part a...........................................................................................................................3

Part b..........................................................................................................................3

Part c...........................................................................................................................4

Question 3......................................................................................................................4

Part a...........................................................................................................................4

Part b..........................................................................................................................5

Question 4......................................................................................................................6

Part a...........................................................................................................................6

Part b..........................................................................................................................7

Question 5......................................................................................................................7

Question 6......................................................................................................................8

Part a...........................................................................................................................8

Part b..........................................................................................................................9

Bibliography...................................................................................................................9

2

MANAGEMENT ACCOUNTING

Question 1

As per the case, Anni-Frid and Benny wants to appoint a management accountant for

properly conducting the operations of the business. Anni-Frid and Benny appoints Bjorn as a

management accounting for the business. It is to be noted that Qualification of Bjorn is not

apt for the post. As per the ethical regulations which are set by Institute of Management

Accountants has been violated. The provisions of Competency standards, management

accounts need to maintain appropriate level of professional expertise by continually

developing knowledge and skills. The management accountant needs to have proper

qualification and maintain competence while conducting the duties of a management

accountant.

Question 2

Part a

Particular

Fixed

Costs

Variable

Costs

Direct

Costs

Indirect

Costs

Product

Costs

Period

Costs

Rent

Warehouse rent

Administrative Costs for

Staff

Commission

Invoicing system fees

Miscellaneous Costs

Full Time employee fee

Miscellaneous costs of

Warehouse

Delivery Costs

Fabric

Timber

Foam

Button stud

Varnish

Bolt

Woodworking costs

MANAGEMENT ACCOUNTING

Question 1

As per the case, Anni-Frid and Benny wants to appoint a management accountant for

properly conducting the operations of the business. Anni-Frid and Benny appoints Bjorn as a

management accounting for the business. It is to be noted that Qualification of Bjorn is not

apt for the post. As per the ethical regulations which are set by Institute of Management

Accountants has been violated. The provisions of Competency standards, management

accounts need to maintain appropriate level of professional expertise by continually

developing knowledge and skills. The management accountant needs to have proper

qualification and maintain competence while conducting the duties of a management

accountant.

Question 2

Part a

Particular

Fixed

Costs

Variable

Costs

Direct

Costs

Indirect

Costs

Product

Costs

Period

Costs

Rent

Warehouse rent

Administrative Costs for

Staff

Commission

Invoicing system fees

Miscellaneous Costs

Full Time employee fee

Miscellaneous costs of

Warehouse

Delivery Costs

Fabric

Timber

Foam

Button stud

Varnish

Bolt

Woodworking costs

3

MANAGEMENT ACCOUNTING

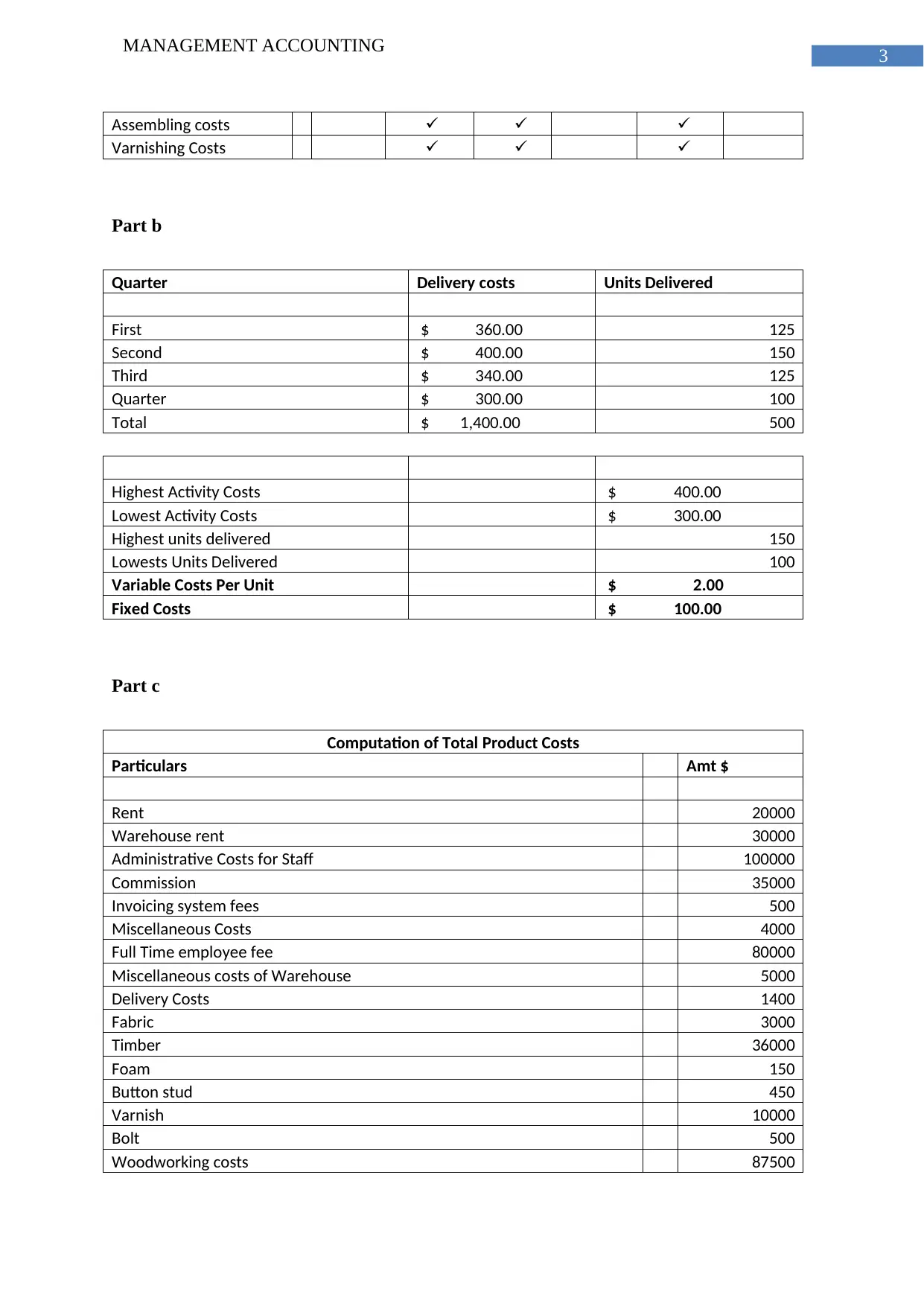

Assembling costs

Varnishing Costs

Part b

Quarter Delivery costs Units Delivered

First $ 360.00 125

Second $ 400.00 150

Third $ 340.00 125

Quarter $ 300.00 100

Total $ 1,400.00 500

Highest Activity Costs $ 400.00

Lowest Activity Costs $ 300.00

Highest units delivered 150

Lowests Units Delivered 100

Variable Costs Per Unit $ 2.00

Fixed Costs $ 100.00

Part c

Computation of Total Product Costs

Particulars Amt $

Rent 20000

Warehouse rent 30000

Administrative Costs for Staff 100000

Commission 35000

Invoicing system fees 500

Miscellaneous Costs 4000

Full Time employee fee 80000

Miscellaneous costs of Warehouse 5000

Delivery Costs 1400

Fabric 3000

Timber 36000

Foam 150

Button stud 450

Varnish 10000

Bolt 500

Woodworking costs 87500

MANAGEMENT ACCOUNTING

Assembling costs

Varnishing Costs

Part b

Quarter Delivery costs Units Delivered

First $ 360.00 125

Second $ 400.00 150

Third $ 340.00 125

Quarter $ 300.00 100

Total $ 1,400.00 500

Highest Activity Costs $ 400.00

Lowest Activity Costs $ 300.00

Highest units delivered 150

Lowests Units Delivered 100

Variable Costs Per Unit $ 2.00

Fixed Costs $ 100.00

Part c

Computation of Total Product Costs

Particulars Amt $

Rent 20000

Warehouse rent 30000

Administrative Costs for Staff 100000

Commission 35000

Invoicing system fees 500

Miscellaneous Costs 4000

Full Time employee fee 80000

Miscellaneous costs of Warehouse 5000

Delivery Costs 1400

Fabric 3000

Timber 36000

Foam 150

Button stud 450

Varnish 10000

Bolt 500

Woodworking costs 87500

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING

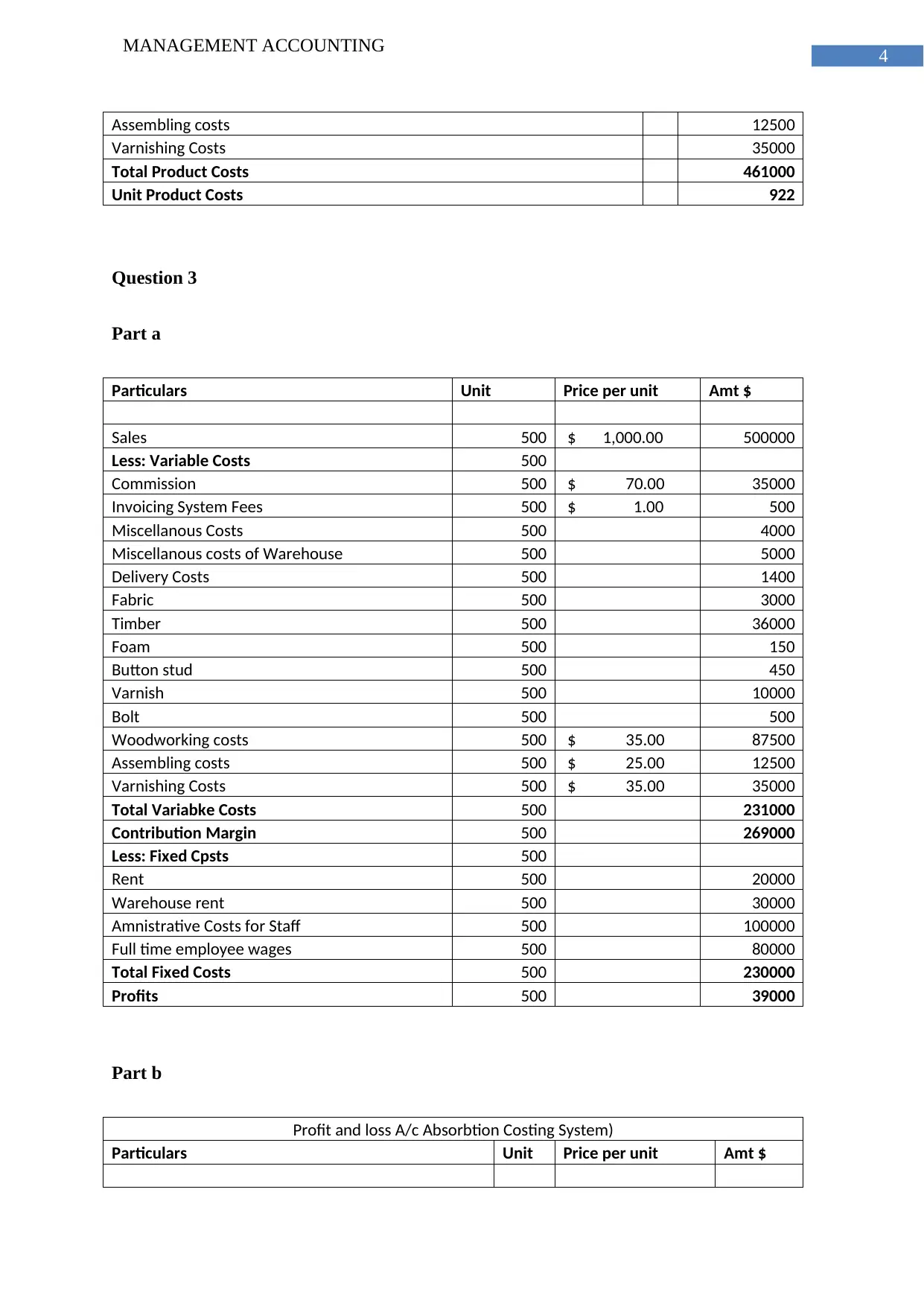

Assembling costs 12500

Varnishing Costs 35000

Total Product Costs 461000

Unit Product Costs 922

Question 3

Part a

Particulars Unit Price per unit Amt $

Sales 500 $ 1,000.00 500000

Less: Variable Costs 500

Commission 500 $ 70.00 35000

Invoicing System Fees 500 $ 1.00 500

Miscellanous Costs 500 4000

Miscellanous costs of Warehouse 500 5000

Delivery Costs 500 1400

Fabric 500 3000

Timber 500 36000

Foam 500 150

Button stud 500 450

Varnish 500 10000

Bolt 500 500

Woodworking costs 500 $ 35.00 87500

Assembling costs 500 $ 25.00 12500

Varnishing Costs 500 $ 35.00 35000

Total Variabke Costs 500 231000

Contribution Margin 500 269000

Less: Fixed Cpsts 500

Rent 500 20000

Warehouse rent 500 30000

Amnistrative Costs for Staff 500 100000

Full time employee wages 500 80000

Total Fixed Costs 500 230000

Profits 500 39000

Part b

Profit and loss A/c Absorbtion Costing System)

Particulars Unit Price per unit Amt $

MANAGEMENT ACCOUNTING

Assembling costs 12500

Varnishing Costs 35000

Total Product Costs 461000

Unit Product Costs 922

Question 3

Part a

Particulars Unit Price per unit Amt $

Sales 500 $ 1,000.00 500000

Less: Variable Costs 500

Commission 500 $ 70.00 35000

Invoicing System Fees 500 $ 1.00 500

Miscellanous Costs 500 4000

Miscellanous costs of Warehouse 500 5000

Delivery Costs 500 1400

Fabric 500 3000

Timber 500 36000

Foam 500 150

Button stud 500 450

Varnish 500 10000

Bolt 500 500

Woodworking costs 500 $ 35.00 87500

Assembling costs 500 $ 25.00 12500

Varnishing Costs 500 $ 35.00 35000

Total Variabke Costs 500 231000

Contribution Margin 500 269000

Less: Fixed Cpsts 500

Rent 500 20000

Warehouse rent 500 30000

Amnistrative Costs for Staff 500 100000

Full time employee wages 500 80000

Total Fixed Costs 500 230000

Profits 500 39000

Part b

Profit and loss A/c Absorbtion Costing System)

Particulars Unit Price per unit Amt $

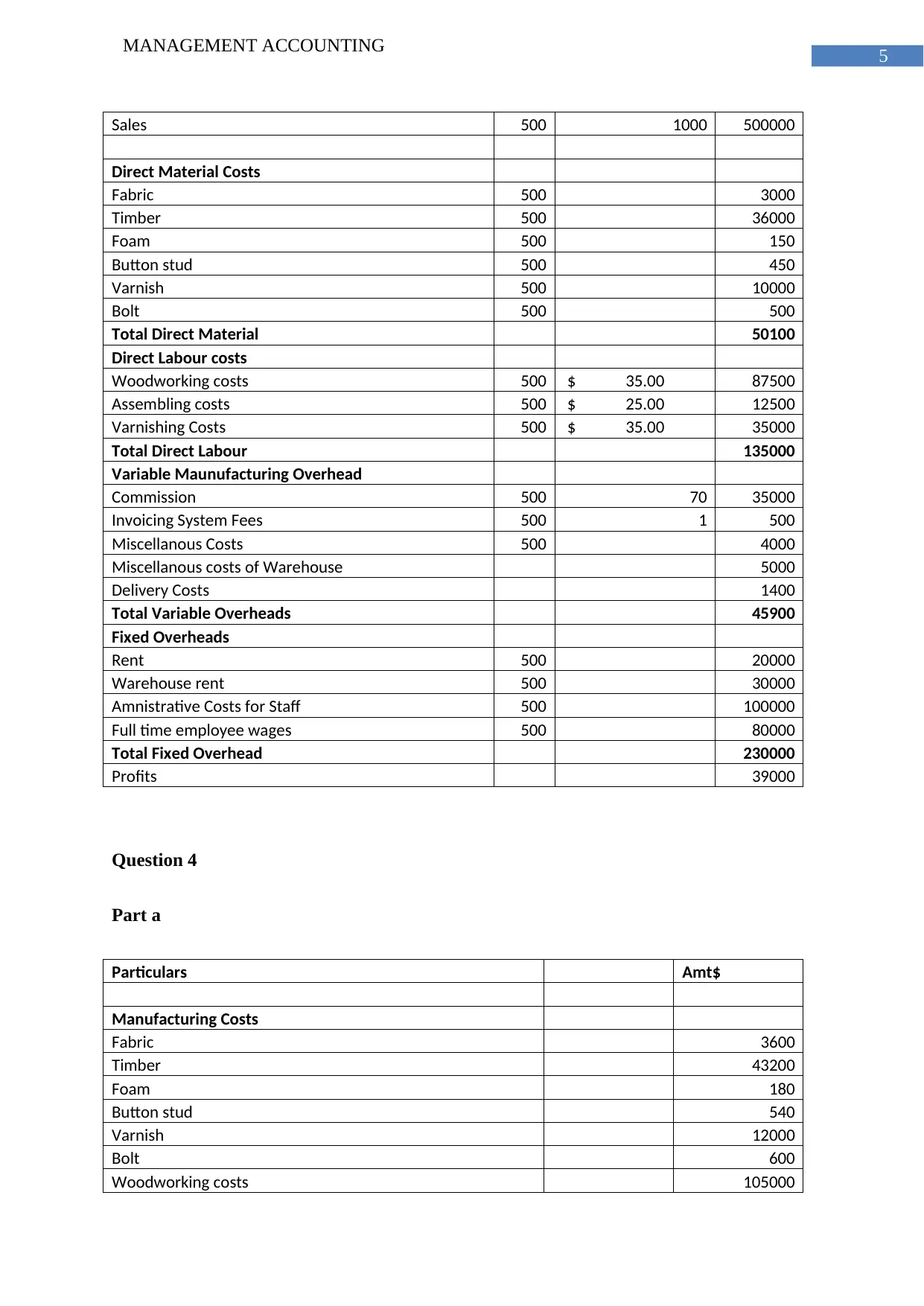

5

MANAGEMENT ACCOUNTING

Sales 500 1000 500000

Direct Material Costs

Fabric 500 3000

Timber 500 36000

Foam 500 150

Button stud 500 450

Varnish 500 10000

Bolt 500 500

Total Direct Material 50100

Direct Labour costs

Woodworking costs 500 $ 35.00 87500

Assembling costs 500 $ 25.00 12500

Varnishing Costs 500 $ 35.00 35000

Total Direct Labour 135000

Variable Maunufacturing Overhead

Commission 500 70 35000

Invoicing System Fees 500 1 500

Miscellanous Costs 500 4000

Miscellanous costs of Warehouse 5000

Delivery Costs 1400

Total Variable Overheads 45900

Fixed Overheads

Rent 500 20000

Warehouse rent 500 30000

Amnistrative Costs for Staff 500 100000

Full time employee wages 500 80000

Total Fixed Overhead 230000

Profits 39000

Question 4

Part a

Particulars Amt$

Manufacturing Costs

Fabric 3600

Timber 43200

Foam 180

Button stud 540

Varnish 12000

Bolt 600

Woodworking costs 105000

MANAGEMENT ACCOUNTING

Sales 500 1000 500000

Direct Material Costs

Fabric 500 3000

Timber 500 36000

Foam 500 150

Button stud 500 450

Varnish 500 10000

Bolt 500 500

Total Direct Material 50100

Direct Labour costs

Woodworking costs 500 $ 35.00 87500

Assembling costs 500 $ 25.00 12500

Varnishing Costs 500 $ 35.00 35000

Total Direct Labour 135000

Variable Maunufacturing Overhead

Commission 500 70 35000

Invoicing System Fees 500 1 500

Miscellanous Costs 500 4000

Miscellanous costs of Warehouse 5000

Delivery Costs 1400

Total Variable Overheads 45900

Fixed Overheads

Rent 500 20000

Warehouse rent 500 30000

Amnistrative Costs for Staff 500 100000

Full time employee wages 500 80000

Total Fixed Overhead 230000

Profits 39000

Question 4

Part a

Particulars Amt$

Manufacturing Costs

Fabric 3600

Timber 43200

Foam 180

Button stud 540

Varnish 12000

Bolt 600

Woodworking costs 105000

6

MANAGEMENT ACCOUNTING

Assembling costs 15000

Varnishing Costs 42000

Direct Manufacturing costs 222120

Rent 20000

Warehouse rent 30000

Amnistrative Costs for Staff 100000

Commission 42000

Invoicing ystem fees 600

Miscellanous Costs 4000

Full Time employee fee 80000

Miscellanous costs of Warehouse 5000

Delivery Costs 1600

Indirect Manufacturing costs 283200

Total Manufacturing costs 505320

Direct Labour hours 4800

Overhead per direct labour hours 59

Part b

The analysis of the indirect activities of the business reveals that woodwork would

have the higher allocation of the overhead costs for the business as the same forms part of the

indirect costs activities of the business considering the level of operations in the current year.

The company is looking to expand the level of their production and thereby the same would

also result in increase in the costs of operations and also increase in different overhead costs

for the business.

Question 5

Profit and loss A/c

Particulars Unit Price per unit Amt $

Variable Costs 500

Commission 500 $ 70.00 35000

Invoicing System Fees 500 $ 1.00 500

Miscellanous Costs 500 4000

Miscellanous costs of Warehouse 500 5000

Delivery Costs 500 1400

Fabric 500 3000

Timber 500 36000

MANAGEMENT ACCOUNTING

Assembling costs 15000

Varnishing Costs 42000

Direct Manufacturing costs 222120

Rent 20000

Warehouse rent 30000

Amnistrative Costs for Staff 100000

Commission 42000

Invoicing ystem fees 600

Miscellanous Costs 4000

Full Time employee fee 80000

Miscellanous costs of Warehouse 5000

Delivery Costs 1600

Indirect Manufacturing costs 283200

Total Manufacturing costs 505320

Direct Labour hours 4800

Overhead per direct labour hours 59

Part b

The analysis of the indirect activities of the business reveals that woodwork would

have the higher allocation of the overhead costs for the business as the same forms part of the

indirect costs activities of the business considering the level of operations in the current year.

The company is looking to expand the level of their production and thereby the same would

also result in increase in the costs of operations and also increase in different overhead costs

for the business.

Question 5

Profit and loss A/c

Particulars Unit Price per unit Amt $

Variable Costs 500

Commission 500 $ 70.00 35000

Invoicing System Fees 500 $ 1.00 500

Miscellanous Costs 500 4000

Miscellanous costs of Warehouse 500 5000

Delivery Costs 500 1400

Fabric 500 3000

Timber 500 36000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

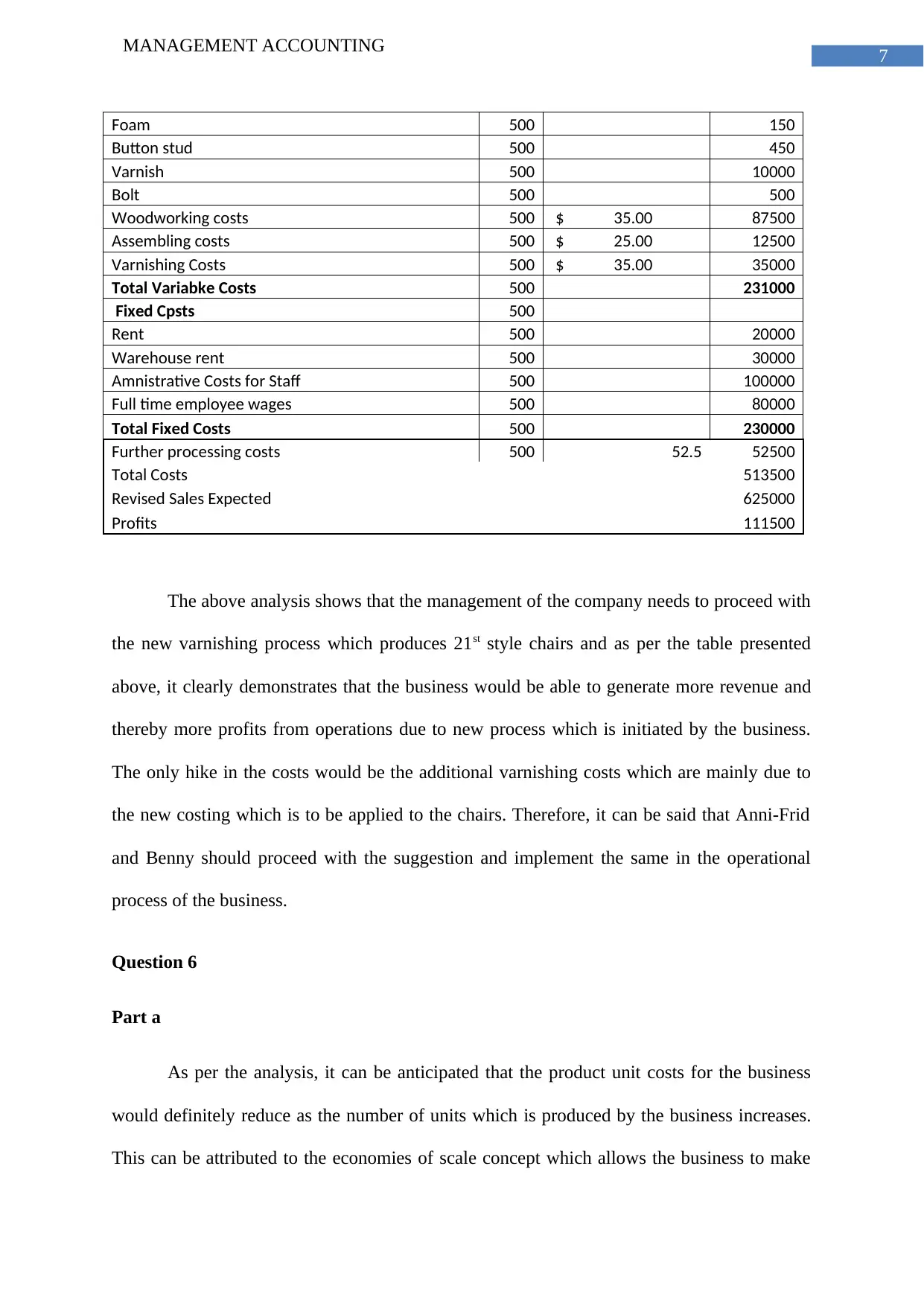

MANAGEMENT ACCOUNTING

Foam 500 150

Button stud 500 450

Varnish 500 10000

Bolt 500 500

Woodworking costs 500 $ 35.00 87500

Assembling costs 500 $ 25.00 12500

Varnishing Costs 500 $ 35.00 35000

Total Variabke Costs 500 231000

Fixed Cpsts 500

Rent 500 20000

Warehouse rent 500 30000

Amnistrative Costs for Staff 500 100000

Full time employee wages 500 80000

Total Fixed Costs 500 230000

Further processing costs 500 52.5 52500

Total Costs 513500

Revised Sales Expected 625000

Profits 111500

The above analysis shows that the management of the company needs to proceed with

the new varnishing process which produces 21st style chairs and as per the table presented

above, it clearly demonstrates that the business would be able to generate more revenue and

thereby more profits from operations due to new process which is initiated by the business.

The only hike in the costs would be the additional varnishing costs which are mainly due to

the new costing which is to be applied to the chairs. Therefore, it can be said that Anni-Frid

and Benny should proceed with the suggestion and implement the same in the operational

process of the business.

Question 6

Part a

As per the analysis, it can be anticipated that the product unit costs for the business

would definitely reduce as the number of units which is produced by the business increases.

This can be attributed to the economies of scale concept which allows the business to make

MANAGEMENT ACCOUNTING

Foam 500 150

Button stud 500 450

Varnish 500 10000

Bolt 500 500

Woodworking costs 500 $ 35.00 87500

Assembling costs 500 $ 25.00 12500

Varnishing Costs 500 $ 35.00 35000

Total Variabke Costs 500 231000

Fixed Cpsts 500

Rent 500 20000

Warehouse rent 500 30000

Amnistrative Costs for Staff 500 100000

Full time employee wages 500 80000

Total Fixed Costs 500 230000

Further processing costs 500 52.5 52500

Total Costs 513500

Revised Sales Expected 625000

Profits 111500

The above analysis shows that the management of the company needs to proceed with

the new varnishing process which produces 21st style chairs and as per the table presented

above, it clearly demonstrates that the business would be able to generate more revenue and

thereby more profits from operations due to new process which is initiated by the business.

The only hike in the costs would be the additional varnishing costs which are mainly due to

the new costing which is to be applied to the chairs. Therefore, it can be said that Anni-Frid

and Benny should proceed with the suggestion and implement the same in the operational

process of the business.

Question 6

Part a

As per the analysis, it can be anticipated that the product unit costs for the business

would definitely reduce as the number of units which is produced by the business increases.

This can be attributed to the economies of scale concept which allows the business to make

8

MANAGEMENT ACCOUNTING

appropriate uses of resources and enhance the production but also at the same time, the costs

of production for the business are also reduced. Therefore, it can be said that increase in scale

of production for the business would enhance the productivity of the business and at the same

time the costs of operations for the business would fall.

Part b

In case there is an fall in the production and the same is not as per the anticipated

production level which is set by the management of the company than the indirect costs

would be over allocated to some extent and therefore adjustments are required to the made to

the costs estimates of the business so that accurate presentation of the cost structure can be

achieved by the business.

Bibliography

Ackerman, P., Belbo, H., Eliasson, L., de Jong, A., Lazdins, A. and Lyons, J., 2014. The

COST model for calculation of forest operations costs. International Journal of Forest

Engineering, 25(1), pp.75-81.

MANAGEMENT ACCOUNTING

appropriate uses of resources and enhance the production but also at the same time, the costs

of production for the business are also reduced. Therefore, it can be said that increase in scale

of production for the business would enhance the productivity of the business and at the same

time the costs of operations for the business would fall.

Part b

In case there is an fall in the production and the same is not as per the anticipated

production level which is set by the management of the company than the indirect costs

would be over allocated to some extent and therefore adjustments are required to the made to

the costs estimates of the business so that accurate presentation of the cost structure can be

achieved by the business.

Bibliography

Ackerman, P., Belbo, H., Eliasson, L., de Jong, A., Lazdins, A. and Lyons, J., 2014. The

COST model for calculation of forest operations costs. International Journal of Forest

Engineering, 25(1), pp.75-81.

9

MANAGEMENT ACCOUNTING

Gibson, I., Rosen, D. and Stucker, B., 2015. Business opportunities and future directions.

In Additive Manufacturing Technologies (pp. 475-486). Springer, New York, NY.

Lewis, W.A., 2013. Overhead costs (Vol. 6). Routledge.

Osadchy, E.A. and Akhmetshin, E.M., 2015. Accounting and control of indirect costs of

organization as a condition of optimizing its financial and economic activities. International

Business Management, 9(7), pp.1705-1709.

MANAGEMENT ACCOUNTING

Gibson, I., Rosen, D. and Stucker, B., 2015. Business opportunities and future directions.

In Additive Manufacturing Technologies (pp. 475-486). Springer, New York, NY.

Lewis, W.A., 2013. Overhead costs (Vol. 6). Routledge.

Osadchy, E.A. and Akhmetshin, E.M., 2015. Accounting and control of indirect costs of

organization as a condition of optimizing its financial and economic activities. International

Business Management, 9(7), pp.1705-1709.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.