Case Study Analysis: Management Accounting - HI5017, T1 2019

VerifiedAdded on 2022/11/26

|10

|3315

|402

Case Study

AI Summary

This assignment presents a comprehensive analysis of a management accounting case study, focusing on cost concepts, relevant costs, and decision-making. The solution meticulously examines fixed, variable, incremental, and sunk costs within the case, differentiating between relevant and irrelevant costs for appliance purchase decisions. It then evaluates three alternatives (rental, laundromat, purchase) using detailed calculations to determine the most cost-effective option. Furthermore, the assignment employs incremental analysis to assess the financial impact of enrolling additional children in a daycare, providing a recommendation based on the incremental profit. Finally, it explores strategic management decisions regarding facility locations and enrollment, including the preparation of monthly income statements for different scenarios. Part B includes a critique of a journal article comparing Canon Inc. and Apple Computer, Inc. to analyze the practical use of accounting information to real-life companies’ decision-making and achievement of business goals.

Running head: MANAGEMENT ACCOUNTING CASE STUDIES

Management Accounting Case Studies

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting Case Studies

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING CASE STUDIES

Table of Contents

Part A: Case Study Analysis..............................................................................................2

Requirement 1:...............................................................................................................2

Requirement 2:...............................................................................................................2

Requirement 3:...............................................................................................................3

Requirement 4:...............................................................................................................3

Requirement 5:...............................................................................................................4

Part B: Journal Article Critique..........................................................................................5

Requirement 1:...............................................................................................................5

Requirement 2:...............................................................................................................6

Requirement 3:...............................................................................................................7

References and Bibliographies:.........................................................................................8

Table of Contents

Part A: Case Study Analysis..............................................................................................2

Requirement 1:...............................................................................................................2

Requirement 2:...............................................................................................................2

Requirement 3:...............................................................................................................3

Requirement 4:...............................................................................................................3

Requirement 5:...............................................................................................................4

Part B: Journal Article Critique..........................................................................................5

Requirement 1:...............................................................................................................5

Requirement 2:...............................................................................................................6

Requirement 3:...............................................................................................................7

References and Bibliographies:.........................................................................................8

2MANAGEMENT ACCOUNTING CASE STUDIES

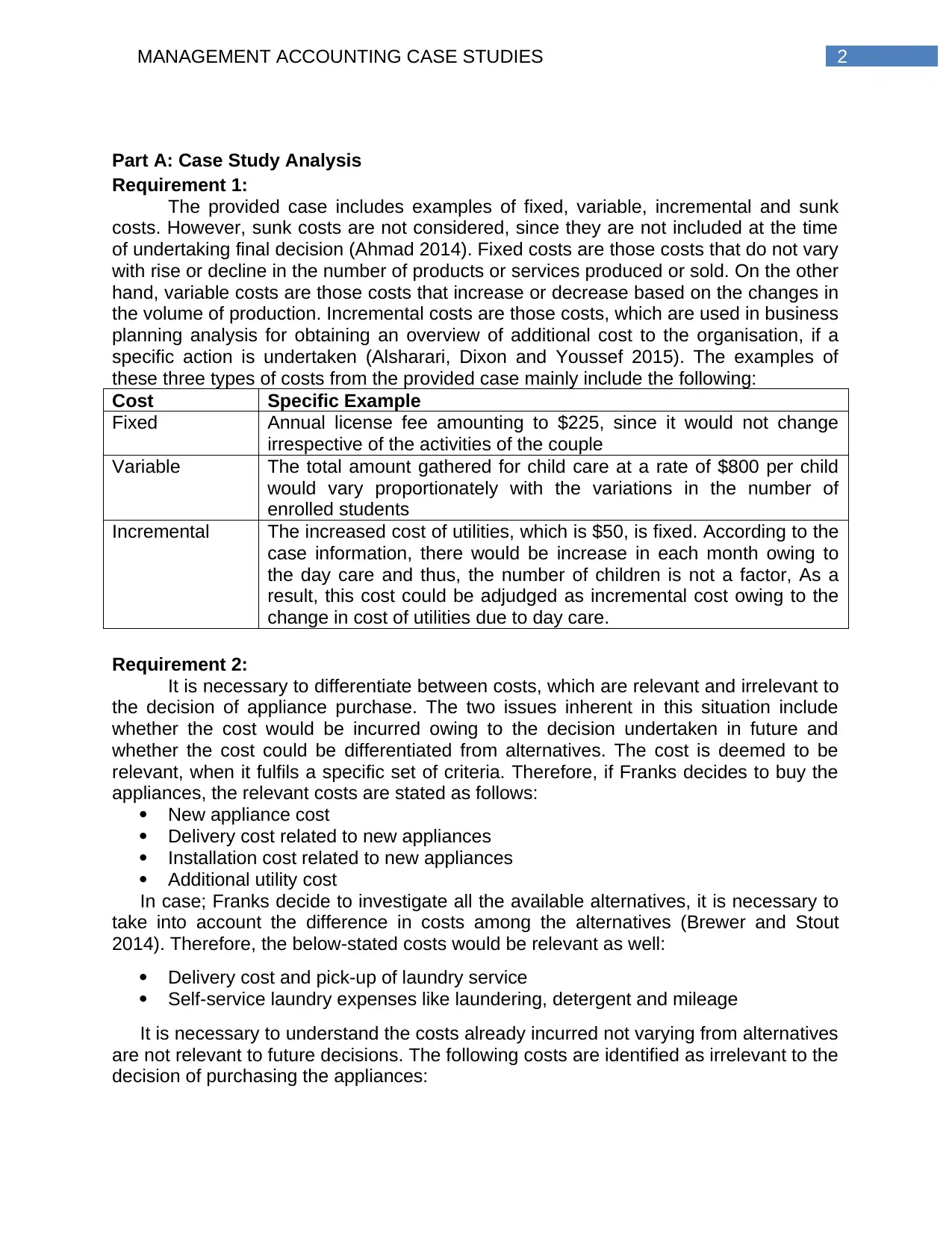

Part A: Case Study Analysis

Requirement 1:

The provided case includes examples of fixed, variable, incremental and sunk

costs. However, sunk costs are not considered, since they are not included at the time

of undertaking final decision (Ahmad 2014). Fixed costs are those costs that do not vary

with rise or decline in the number of products or services produced or sold. On the other

hand, variable costs are those costs that increase or decrease based on the changes in

the volume of production. Incremental costs are those costs, which are used in business

planning analysis for obtaining an overview of additional cost to the organisation, if a

specific action is undertaken (Alsharari, Dixon and Youssef 2015). The examples of

these three types of costs from the provided case mainly include the following:

Cost Specific Example

Fixed Annual license fee amounting to $225, since it would not change

irrespective of the activities of the couple

Variable The total amount gathered for child care at a rate of $800 per child

would vary proportionately with the variations in the number of

enrolled students

Incremental The increased cost of utilities, which is $50, is fixed. According to the

case information, there would be increase in each month owing to

the day care and thus, the number of children is not a factor, As a

result, this cost could be adjudged as incremental cost owing to the

change in cost of utilities due to day care.

Requirement 2:

It is necessary to differentiate between costs, which are relevant and irrelevant to

the decision of appliance purchase. The two issues inherent in this situation include

whether the cost would be incurred owing to the decision undertaken in future and

whether the cost could be differentiated from alternatives. The cost is deemed to be

relevant, when it fulfils a specific set of criteria. Therefore, if Franks decides to buy the

appliances, the relevant costs are stated as follows:

New appliance cost

Delivery cost related to new appliances

Installation cost related to new appliances

Additional utility cost

In case; Franks decide to investigate all the available alternatives, it is necessary to

take into account the difference in costs among the alternatives (Brewer and Stout

2014). Therefore, the below-stated costs would be relevant as well:

Delivery cost and pick-up of laundry service

Self-service laundry expenses like laundering, detergent and mileage

It is necessary to understand the costs already incurred not varying from alternatives

are not relevant to future decisions. The following costs are identified as irrelevant to the

decision of purchasing the appliances:

Part A: Case Study Analysis

Requirement 1:

The provided case includes examples of fixed, variable, incremental and sunk

costs. However, sunk costs are not considered, since they are not included at the time

of undertaking final decision (Ahmad 2014). Fixed costs are those costs that do not vary

with rise or decline in the number of products or services produced or sold. On the other

hand, variable costs are those costs that increase or decrease based on the changes in

the volume of production. Incremental costs are those costs, which are used in business

planning analysis for obtaining an overview of additional cost to the organisation, if a

specific action is undertaken (Alsharari, Dixon and Youssef 2015). The examples of

these three types of costs from the provided case mainly include the following:

Cost Specific Example

Fixed Annual license fee amounting to $225, since it would not change

irrespective of the activities of the couple

Variable The total amount gathered for child care at a rate of $800 per child

would vary proportionately with the variations in the number of

enrolled students

Incremental The increased cost of utilities, which is $50, is fixed. According to the

case information, there would be increase in each month owing to

the day care and thus, the number of children is not a factor, As a

result, this cost could be adjudged as incremental cost owing to the

change in cost of utilities due to day care.

Requirement 2:

It is necessary to differentiate between costs, which are relevant and irrelevant to

the decision of appliance purchase. The two issues inherent in this situation include

whether the cost would be incurred owing to the decision undertaken in future and

whether the cost could be differentiated from alternatives. The cost is deemed to be

relevant, when it fulfils a specific set of criteria. Therefore, if Franks decides to buy the

appliances, the relevant costs are stated as follows:

New appliance cost

Delivery cost related to new appliances

Installation cost related to new appliances

Additional utility cost

In case; Franks decide to investigate all the available alternatives, it is necessary to

take into account the difference in costs among the alternatives (Brewer and Stout

2014). Therefore, the below-stated costs would be relevant as well:

Delivery cost and pick-up of laundry service

Self-service laundry expenses like laundering, detergent and mileage

It is necessary to understand the costs already incurred not varying from alternatives

are not relevant to future decisions. The following costs are identified as irrelevant to the

decision of purchasing the appliances:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING CASE STUDIES

Old appliance cost

Detergent cost is not relevant, only if the available options do not take into

account delivery and pick-up services (Bromwich and Scapens 2016)

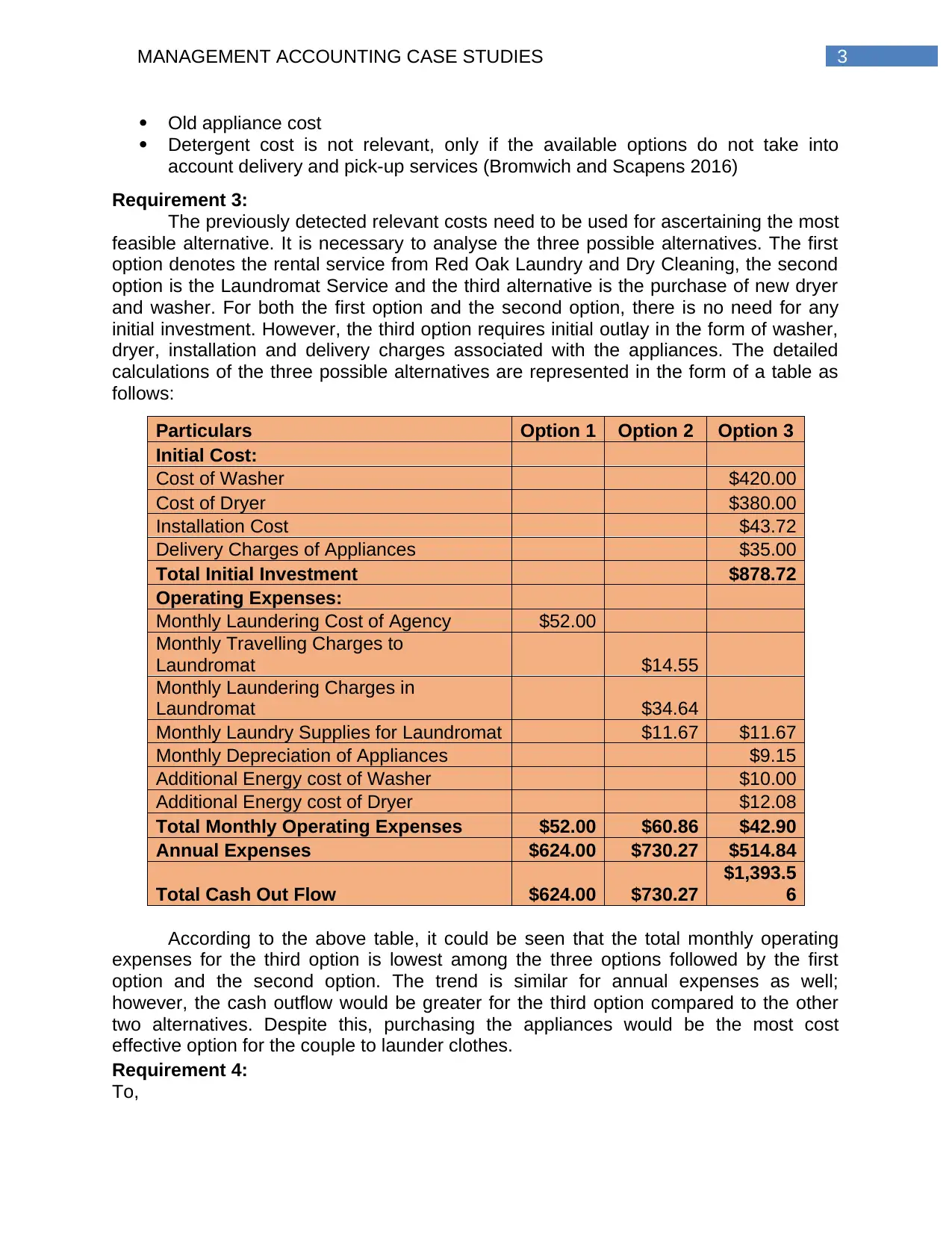

Requirement 3:

The previously detected relevant costs need to be used for ascertaining the most

feasible alternative. It is necessary to analyse the three possible alternatives. The first

option denotes the rental service from Red Oak Laundry and Dry Cleaning, the second

option is the Laundromat Service and the third alternative is the purchase of new dryer

and washer. For both the first option and the second option, there is no need for any

initial investment. However, the third option requires initial outlay in the form of washer,

dryer, installation and delivery charges associated with the appliances. The detailed

calculations of the three possible alternatives are represented in the form of a table as

follows:

Particulars Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to

Laundromat $14.55

Monthly Laundering Charges in

Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27

$1,393.5

6

According to the above table, it could be seen that the total monthly operating

expenses for the third option is lowest among the three options followed by the first

option and the second option. The trend is similar for annual expenses as well;

however, the cash outflow would be greater for the third option compared to the other

two alternatives. Despite this, purchasing the appliances would be the most cost

effective option for the couple to launder clothes.

Requirement 4:

To,

Old appliance cost

Detergent cost is not relevant, only if the available options do not take into

account delivery and pick-up services (Bromwich and Scapens 2016)

Requirement 3:

The previously detected relevant costs need to be used for ascertaining the most

feasible alternative. It is necessary to analyse the three possible alternatives. The first

option denotes the rental service from Red Oak Laundry and Dry Cleaning, the second

option is the Laundromat Service and the third alternative is the purchase of new dryer

and washer. For both the first option and the second option, there is no need for any

initial investment. However, the third option requires initial outlay in the form of washer,

dryer, installation and delivery charges associated with the appliances. The detailed

calculations of the three possible alternatives are represented in the form of a table as

follows:

Particulars Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to

Laundromat $14.55

Monthly Laundering Charges in

Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27

$1,393.5

6

According to the above table, it could be seen that the total monthly operating

expenses for the third option is lowest among the three options followed by the first

option and the second option. The trend is similar for annual expenses as well;

however, the cash outflow would be greater for the third option compared to the other

two alternatives. Despite this, purchasing the appliances would be the most cost

effective option for the couple to launder clothes.

Requirement 4:

To,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING CASE STUDIES

Franks,

Date: 25th May 2019

Subject: Letter of recommendation

The provided situation needs to be evaluated with the help of incremental

analysis. More precisely, the incremental costs of undertaking changes have to be

evaluated in this case. The change in costs needs to be considered for additional staffs

along with feeding additional children. The additional number of children would result in

rise in revenue. Hence, the change in revenue has to be taken into consideration

(Chenhall and Moers 2015). The incremental changes are represented in the form a

table as follows:

Particulars Amount

Additional Number of Children 3

Revenue per Child $800

Incremental Revenue per Month $2,400

Number of employees 1

Labour Hour per week 40

Labour Charges per hour $9

Incremental Labour Charges per month $1,559

Food cost per day for each child $ 3.20

Number of days per week 5

Incremental food cost per month $208

Total Incremental cost $1,767

Incremental Profit per month $633

The incremental revenue obtained by enrolling additional three children, which is

$2,400, has exceeded the total incremental cost of additional staff and incremental food

cost for the additional children obtained as $1,767. Therefore, Franks would have net

benefit of $633, if it decides to exercise the option.

Requirement 5:

It is necessary to gain an insight that facility locations and enrolment decisions

are management decisions that need an understanding of the strategic goals (De Loo,

Cooper and Manochin 2015). This would assist in understanding the impact of

enrolment decisions on the number of staffs needed and additional food expenses. For

the two provided options, monthly income statements are prepared. The calculations

reveal that service for nine children would need one additional staff; service for 12

children would need two additional staffs and service for 14 children would need three

additional staffs.

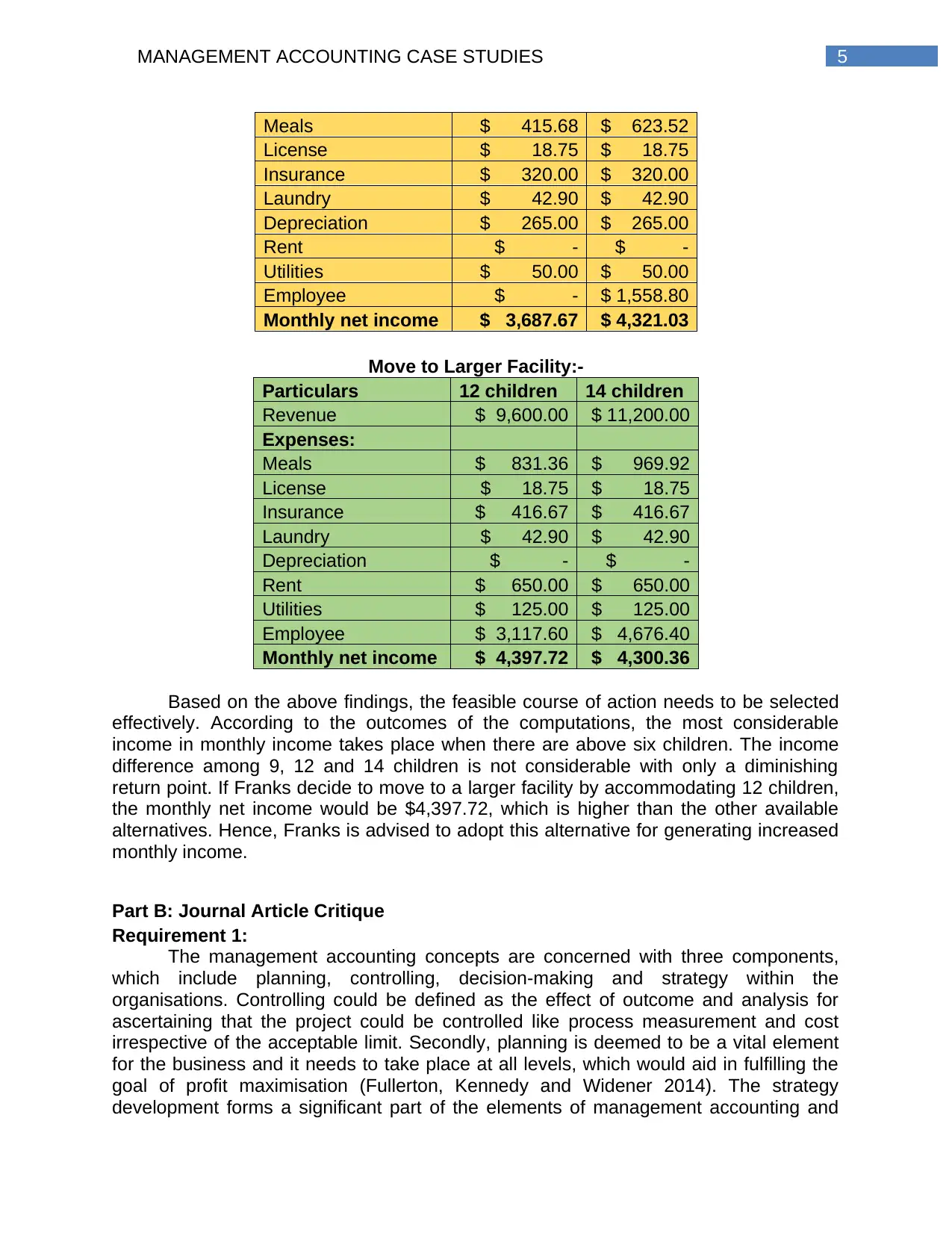

Remain in Current Location:-

Particulars 6 children 9 children

Revenue $ 4,800.00 $ 7,200.00

Expenses:

Franks,

Date: 25th May 2019

Subject: Letter of recommendation

The provided situation needs to be evaluated with the help of incremental

analysis. More precisely, the incremental costs of undertaking changes have to be

evaluated in this case. The change in costs needs to be considered for additional staffs

along with feeding additional children. The additional number of children would result in

rise in revenue. Hence, the change in revenue has to be taken into consideration

(Chenhall and Moers 2015). The incremental changes are represented in the form a

table as follows:

Particulars Amount

Additional Number of Children 3

Revenue per Child $800

Incremental Revenue per Month $2,400

Number of employees 1

Labour Hour per week 40

Labour Charges per hour $9

Incremental Labour Charges per month $1,559

Food cost per day for each child $ 3.20

Number of days per week 5

Incremental food cost per month $208

Total Incremental cost $1,767

Incremental Profit per month $633

The incremental revenue obtained by enrolling additional three children, which is

$2,400, has exceeded the total incremental cost of additional staff and incremental food

cost for the additional children obtained as $1,767. Therefore, Franks would have net

benefit of $633, if it decides to exercise the option.

Requirement 5:

It is necessary to gain an insight that facility locations and enrolment decisions

are management decisions that need an understanding of the strategic goals (De Loo,

Cooper and Manochin 2015). This would assist in understanding the impact of

enrolment decisions on the number of staffs needed and additional food expenses. For

the two provided options, monthly income statements are prepared. The calculations

reveal that service for nine children would need one additional staff; service for 12

children would need two additional staffs and service for 14 children would need three

additional staffs.

Remain in Current Location:-

Particulars 6 children 9 children

Revenue $ 4,800.00 $ 7,200.00

Expenses:

5MANAGEMENT ACCOUNTING CASE STUDIES

Meals $ 415.68 $ 623.52

License $ 18.75 $ 18.75

Insurance $ 320.00 $ 320.00

Laundry $ 42.90 $ 42.90

Depreciation $ 265.00 $ 265.00

Rent $ - $ -

Utilities $ 50.00 $ 50.00

Employee $ - $ 1,558.80

Monthly net income $ 3,687.67 $ 4,321.03

Move to Larger Facility:-

Particulars 12 children 14 children

Revenue $ 9,600.00 $ 11,200.00

Expenses:

Meals $ 831.36 $ 969.92

License $ 18.75 $ 18.75

Insurance $ 416.67 $ 416.67

Laundry $ 42.90 $ 42.90

Depreciation $ - $ -

Rent $ 650.00 $ 650.00

Utilities $ 125.00 $ 125.00

Employee $ 3,117.60 $ 4,676.40

Monthly net income $ 4,397.72 $ 4,300.36

Based on the above findings, the feasible course of action needs to be selected

effectively. According to the outcomes of the computations, the most considerable

income in monthly income takes place when there are above six children. The income

difference among 9, 12 and 14 children is not considerable with only a diminishing

return point. If Franks decide to move to a larger facility by accommodating 12 children,

the monthly net income would be $4,397.72, which is higher than the other available

alternatives. Hence, Franks is advised to adopt this alternative for generating increased

monthly income.

Part B: Journal Article Critique

Requirement 1:

The management accounting concepts are concerned with three components,

which include planning, controlling, decision-making and strategy within the

organisations. Controlling could be defined as the effect of outcome and analysis for

ascertaining that the project could be controlled like process measurement and cost

irrespective of the acceptable limit. Secondly, planning is deemed to be a vital element

for the business and it needs to take place at all levels, which would aid in fulfilling the

goal of profit maximisation (Fullerton, Kennedy and Widener 2014). The strategy

development forms a significant part of the elements of management accounting and

Meals $ 415.68 $ 623.52

License $ 18.75 $ 18.75

Insurance $ 320.00 $ 320.00

Laundry $ 42.90 $ 42.90

Depreciation $ 265.00 $ 265.00

Rent $ - $ -

Utilities $ 50.00 $ 50.00

Employee $ - $ 1,558.80

Monthly net income $ 3,687.67 $ 4,321.03

Move to Larger Facility:-

Particulars 12 children 14 children

Revenue $ 9,600.00 $ 11,200.00

Expenses:

Meals $ 831.36 $ 969.92

License $ 18.75 $ 18.75

Insurance $ 416.67 $ 416.67

Laundry $ 42.90 $ 42.90

Depreciation $ - $ -

Rent $ 650.00 $ 650.00

Utilities $ 125.00 $ 125.00

Employee $ 3,117.60 $ 4,676.40

Monthly net income $ 4,397.72 $ 4,300.36

Based on the above findings, the feasible course of action needs to be selected

effectively. According to the outcomes of the computations, the most considerable

income in monthly income takes place when there are above six children. The income

difference among 9, 12 and 14 children is not considerable with only a diminishing

return point. If Franks decide to move to a larger facility by accommodating 12 children,

the monthly net income would be $4,397.72, which is higher than the other available

alternatives. Hence, Franks is advised to adopt this alternative for generating increased

monthly income.

Part B: Journal Article Critique

Requirement 1:

The management accounting concepts are concerned with three components,

which include planning, controlling, decision-making and strategy within the

organisations. Controlling could be defined as the effect of outcome and analysis for

ascertaining that the project could be controlled like process measurement and cost

irrespective of the acceptable limit. Secondly, planning is deemed to be a vital element

for the business and it needs to take place at all levels, which would aid in fulfilling the

goal of profit maximisation (Fullerton, Kennedy and Widener 2014). The strategy

development forms a significant part of the elements of management accounting and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING CASE STUDIES

the organisations tend to develop relationship between daily business activities as well

as strategic endeavours.

Canon Inc has made internal development of Mini Copier through re-

conceptualisation of the overall plain paper copier market and owing to this, the

introduction of the mini copier would need lower or no maintenance cost. Therefore, the

actualisation of Mini Copier was needed for managing the inverse association between

reliability and cost. The management of the organisation planned to resolve the

contradiction between reliability and cost (Nonaka and Kenney 1991). This implies that

the product cost arose owing to the enhancement in reliability and rise in service need

because of the cost minimisation. Therefore, the issue related to the mini copier is to

ensure improvement in the durability of drums and cleaners. In this new method, the

drum needs to be treated in the form of a module, which has been discarded after

making different numbers of copies and the outcome would be the copier development,

which would be devoid of maintenance (Juras 2014). The product development has

been revolutionised owing to the addition of capacity of Canon Inc.

The product development process of Apple has taken into account the elements

of the management accounting concepts. The aim of the organisation in the initial

period has been to revolutionise the Mac computers owing to the introduction of high-

priced machine and there has been incorporation of developed technology at Xerox

Parc. With the aid of consequent crystallisation and issue from the end of CEO of Apple

Inc, Mac has become self-organised, as optimisation could be observed between

software and hardware individuals (Nonaka and Kenney 1991). From the provided

information, it has been found that the Mac team has made some significant innovation,

which could not be reverberated across the organisation owing to the absence of

coordination between Mac and other Apple members. The new ideas have emerged

owing to the constant interaction between the members of the Mac team.

The controlling factor that Apple has used includes producing Mac inexpensively

through the set-up of a highly automated factor by setting low target price. The role of

the CEO for product development has been critical due to the issues engaged in the

development process (Kaplan and Atkinson 2015). Moreover, the process of decision-

making within the organisation has been improved owing to the role of the final arbiter

involved in making decision. The role of the individual in terms of product visionary has

lead to positive aspects. Hence, it has been determined that controlling and decision-

making have been the significant contributors in the development process.

Requirement 2:

Management accounting is a group of procedures that the managers use for

providing useful and valuable insights in monitoring, planning and decision-making

process (Lavia López and Hiebl 2014). In case of Canon, the innovation process

includes the recapitalisation of the overall plain paper copier, which has been developed

on human activity. The new solutions associated with the contradiction of Copier have

been brainstormed by collection of the project teams, which are outside the

marketplace. By interacting with individuals, the innovation evolved has been the drum

development in the form of module, which after learning different copies, need to be

discarded and this would make the copier free of maintenance.

In case of Apple Inc, the new features and ideas in developing the Macintosh

Computers have evolved owing to the constant interactions between the members of

the organisations tend to develop relationship between daily business activities as well

as strategic endeavours.

Canon Inc has made internal development of Mini Copier through re-

conceptualisation of the overall plain paper copier market and owing to this, the

introduction of the mini copier would need lower or no maintenance cost. Therefore, the

actualisation of Mini Copier was needed for managing the inverse association between

reliability and cost. The management of the organisation planned to resolve the

contradiction between reliability and cost (Nonaka and Kenney 1991). This implies that

the product cost arose owing to the enhancement in reliability and rise in service need

because of the cost minimisation. Therefore, the issue related to the mini copier is to

ensure improvement in the durability of drums and cleaners. In this new method, the

drum needs to be treated in the form of a module, which has been discarded after

making different numbers of copies and the outcome would be the copier development,

which would be devoid of maintenance (Juras 2014). The product development has

been revolutionised owing to the addition of capacity of Canon Inc.

The product development process of Apple has taken into account the elements

of the management accounting concepts. The aim of the organisation in the initial

period has been to revolutionise the Mac computers owing to the introduction of high-

priced machine and there has been incorporation of developed technology at Xerox

Parc. With the aid of consequent crystallisation and issue from the end of CEO of Apple

Inc, Mac has become self-organised, as optimisation could be observed between

software and hardware individuals (Nonaka and Kenney 1991). From the provided

information, it has been found that the Mac team has made some significant innovation,

which could not be reverberated across the organisation owing to the absence of

coordination between Mac and other Apple members. The new ideas have emerged

owing to the constant interaction between the members of the Mac team.

The controlling factor that Apple has used includes producing Mac inexpensively

through the set-up of a highly automated factor by setting low target price. The role of

the CEO for product development has been critical due to the issues engaged in the

development process (Kaplan and Atkinson 2015). Moreover, the process of decision-

making within the organisation has been improved owing to the role of the final arbiter

involved in making decision. The role of the individual in terms of product visionary has

lead to positive aspects. Hence, it has been determined that controlling and decision-

making have been the significant contributors in the development process.

Requirement 2:

Management accounting is a group of procedures that the managers use for

providing useful and valuable insights in monitoring, planning and decision-making

process (Lavia López and Hiebl 2014). In case of Canon, the innovation process

includes the recapitalisation of the overall plain paper copier, which has been developed

on human activity. The new solutions associated with the contradiction of Copier have

been brainstormed by collection of the project teams, which are outside the

marketplace. By interacting with individuals, the innovation evolved has been the drum

development in the form of module, which after learning different copies, need to be

discarded and this would make the copier free of maintenance.

In case of Apple Inc, the new features and ideas in developing the Macintosh

Computers have evolved owing to the constant interactions between the members of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING CASE STUDIES

the Mac team. The problems that the team members have created in developing

computers have stimulated the other members of the team in forming solution and thus,

it leads to problem-solving (Maas, Schaltegger and Crutzen 2016). Hence, Mac has

obtained differentiated design along with compact look. The resources have been

funnelled into the Mac project, which are later converted into vision of the real product

and the complex part of the project has been conceptualised by using metaphor and

analogies.

Requirement 3:

The product development is not same for Apple Inc and Canon Inc and even

differences could be observed in the innovation process as well. The product

development in the big Japanese organisation has been significantly different from the

Silicon Valley chaos. Apple Inc has experienced significant growth by the continual flow

of new entrepreneurs along with development of venture capital. On the contrary, the

growth at the Japanese organisation is marked by increasingly competitive market, in

which there is use of innovation for ensuring business growth (Malmi 2016). Hence, in a

rapidly growing economy, the organisations are needed to form an environment, in

which there has been transmission of new ideas across the organisation.

After this, it is necessary for the organisations to involve the management in

developing a situation, in which chaos could lead to creation of new information. This

could be formed via merger and acquisition programs. Thirdly, raw materials are used

for the theoretical projects owing to the innovation process. Hence, stress needs to be

provided on emergence and synthesis.

In addition, it has been found by analysing the case of Canon Inc that there has

been revitalisation of different product lines owing to the spin offs for developing mini

copier. Hence, the transformative ability of the organisation is adjudged as the strong

stimulus, which assists in propelling the organisation forward. Hence, the innovating

company needs to develop an environment resulting in the creation of transmit and

information along with amplifying the newly developed information by structuring the

entities (Messner 2016).

In the current era, the management accountants are deemed to be the decision

makers as well as providers of information since they assist in smooth conduction of

business operations (Nielsen, Mitchell and Nørreklit 2015). From the findings obtained

from the journal article, the organisations are needed to develop an environment, which

aids in development and generation of new ideas, which could be transmitted through

the organisations. The organisations have to understand that the accountant functions

need to be made by incorporating chaos into the research and development decision

(Pavlatos 2015).

the Mac team. The problems that the team members have created in developing

computers have stimulated the other members of the team in forming solution and thus,

it leads to problem-solving (Maas, Schaltegger and Crutzen 2016). Hence, Mac has

obtained differentiated design along with compact look. The resources have been

funnelled into the Mac project, which are later converted into vision of the real product

and the complex part of the project has been conceptualised by using metaphor and

analogies.

Requirement 3:

The product development is not same for Apple Inc and Canon Inc and even

differences could be observed in the innovation process as well. The product

development in the big Japanese organisation has been significantly different from the

Silicon Valley chaos. Apple Inc has experienced significant growth by the continual flow

of new entrepreneurs along with development of venture capital. On the contrary, the

growth at the Japanese organisation is marked by increasingly competitive market, in

which there is use of innovation for ensuring business growth (Malmi 2016). Hence, in a

rapidly growing economy, the organisations are needed to form an environment, in

which there has been transmission of new ideas across the organisation.

After this, it is necessary for the organisations to involve the management in

developing a situation, in which chaos could lead to creation of new information. This

could be formed via merger and acquisition programs. Thirdly, raw materials are used

for the theoretical projects owing to the innovation process. Hence, stress needs to be

provided on emergence and synthesis.

In addition, it has been found by analysing the case of Canon Inc that there has

been revitalisation of different product lines owing to the spin offs for developing mini

copier. Hence, the transformative ability of the organisation is adjudged as the strong

stimulus, which assists in propelling the organisation forward. Hence, the innovating

company needs to develop an environment resulting in the creation of transmit and

information along with amplifying the newly developed information by structuring the

entities (Messner 2016).

In the current era, the management accountants are deemed to be the decision

makers as well as providers of information since they assist in smooth conduction of

business operations (Nielsen, Mitchell and Nørreklit 2015). From the findings obtained

from the journal article, the organisations are needed to develop an environment, which

aids in development and generation of new ideas, which could be transmitted through

the organisations. The organisations have to understand that the accountant functions

need to be made by incorporating chaos into the research and development decision

(Pavlatos 2015).

8MANAGEMENT ACCOUNTING CASE STUDIES

References and Bibliographies:

Ahmad, K., 2014. The adoption of management accounting practices in malaysian small

and medium-sized enterprises. Asian Social Science, 10(2), p.236.

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting

change: critical review and a new contextual framework. Journal of Accounting &

Organizational Change, 11(4), pp.476-502.

Brewer, P.C. and Stout, D.E., 2014. The future of accounting education: Addressing the

competency crisis. Strategic Finance, 96(2), p.29.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of

management accounting and its integration into management control. Accounting,

organizations and society, 47, pp.1-13.

De Loo, I., Cooper, S. and Manochin, M., 2015. Enhancing the transparency of

accounting research: the case of narrative analysis. Qualitative Research in Accounting

& Management, 12(1), pp.34-54.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Juras, A., 2014. Strategic Management Accounting-What Is the Current State of the

Concept?. Economy Transdisciplinarity Cognition, 17(2), p.76.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-

sized enterprises: current knowledge and avenues for further research. Journal of

Management Accounting Research, 27(1), pp.81-119.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–

2014. Management Accounting Research, 31, pp.31-44.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum, 39(1), pp. 66-

82.

Nonaka, I. and Kenney. M., 1991. Towards a new theory of innovation management: A

case study comparing Canon, Inc. and Apple Computer, Inc. Journal of Engineering and

Technology Management, 8, p. 67-83.

Pavlatos, O., 2015. An empirical investigation of strategic management accounting in

hotels. International Journal of Contemporary Hospitality Management, 27(5), pp.756-

767.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

References and Bibliographies:

Ahmad, K., 2014. The adoption of management accounting practices in malaysian small

and medium-sized enterprises. Asian Social Science, 10(2), p.236.

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting

change: critical review and a new contextual framework. Journal of Accounting &

Organizational Change, 11(4), pp.476-502.

Brewer, P.C. and Stout, D.E., 2014. The future of accounting education: Addressing the

competency crisis. Strategic Finance, 96(2), p.29.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of

management accounting and its integration into management control. Accounting,

organizations and society, 47, pp.1-13.

De Loo, I., Cooper, S. and Manochin, M., 2015. Enhancing the transparency of

accounting research: the case of narrative analysis. Qualitative Research in Accounting

& Management, 12(1), pp.34-54.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Juras, A., 2014. Strategic Management Accounting-What Is the Current State of the

Concept?. Economy Transdisciplinarity Cognition, 17(2), p.76.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI

Learning.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-

sized enterprises: current knowledge and avenues for further research. Journal of

Management Accounting Research, 27(1), pp.81-119.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–

2014. Management Accounting Research, 31, pp.31-44.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum, 39(1), pp. 66-

82.

Nonaka, I. and Kenney. M., 1991. Towards a new theory of innovation management: A

case study comparing Canon, Inc. and Apple Computer, Inc. Journal of Engineering and

Technology Management, 8, p. 67-83.

Pavlatos, O., 2015. An empirical investigation of strategic management accounting in

hotels. International Journal of Contemporary Hospitality Management, 27(5), pp.756-

767.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING CASE STUDIES

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A

management accounting perspective on safety. Safety science, 71, pp.151-159.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A. and Nenonen, N., 2015. A

management accounting perspective on safety. Safety science, 71, pp.151-159.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.