Management Accounting Case Studies

Added on 2022-11-26

10 Pages3315 Words402 Views

Running head: MANAGEMENT ACCOUNTING CASE STUDIES

Management Accounting Case Studies

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting Case Studies

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

1MANAGEMENT ACCOUNTING CASE STUDIES

Table of Contents

Part A: Case Study Analysis..............................................................................................2

Requirement 1:...............................................................................................................2

Requirement 2:...............................................................................................................2

Requirement 3:...............................................................................................................3

Requirement 4:...............................................................................................................3

Requirement 5:...............................................................................................................4

Part B: Journal Article Critique..........................................................................................5

Requirement 1:...............................................................................................................5

Requirement 2:...............................................................................................................6

Requirement 3:...............................................................................................................7

References and Bibliographies:.........................................................................................8

Table of Contents

Part A: Case Study Analysis..............................................................................................2

Requirement 1:...............................................................................................................2

Requirement 2:...............................................................................................................2

Requirement 3:...............................................................................................................3

Requirement 4:...............................................................................................................3

Requirement 5:...............................................................................................................4

Part B: Journal Article Critique..........................................................................................5

Requirement 1:...............................................................................................................5

Requirement 2:...............................................................................................................6

Requirement 3:...............................................................................................................7

References and Bibliographies:.........................................................................................8

2MANAGEMENT ACCOUNTING CASE STUDIES

Part A: Case Study Analysis

Requirement 1:

The provided case includes examples of fixed, variable, incremental and sunk

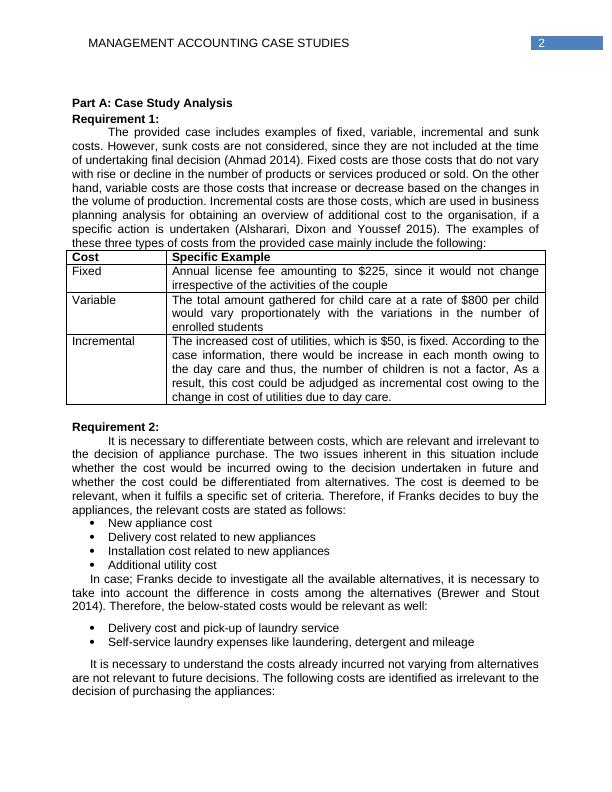

costs. However, sunk costs are not considered, since they are not included at the time

of undertaking final decision (Ahmad 2014). Fixed costs are those costs that do not vary

with rise or decline in the number of products or services produced or sold. On the other

hand, variable costs are those costs that increase or decrease based on the changes in

the volume of production. Incremental costs are those costs, which are used in business

planning analysis for obtaining an overview of additional cost to the organisation, if a

specific action is undertaken (Alsharari, Dixon and Youssef 2015). The examples of

these three types of costs from the provided case mainly include the following:

Cost Specific Example

Fixed Annual license fee amounting to $225, since it would not change

irrespective of the activities of the couple

Variable The total amount gathered for child care at a rate of $800 per child

would vary proportionately with the variations in the number of

enrolled students

Incremental The increased cost of utilities, which is $50, is fixed. According to the

case information, there would be increase in each month owing to

the day care and thus, the number of children is not a factor, As a

result, this cost could be adjudged as incremental cost owing to the

change in cost of utilities due to day care.

Requirement 2:

It is necessary to differentiate between costs, which are relevant and irrelevant to

the decision of appliance purchase. The two issues inherent in this situation include

whether the cost would be incurred owing to the decision undertaken in future and

whether the cost could be differentiated from alternatives. The cost is deemed to be

relevant, when it fulfils a specific set of criteria. Therefore, if Franks decides to buy the

appliances, the relevant costs are stated as follows:

New appliance cost

Delivery cost related to new appliances

Installation cost related to new appliances

Additional utility cost

In case; Franks decide to investigate all the available alternatives, it is necessary to

take into account the difference in costs among the alternatives (Brewer and Stout

2014). Therefore, the below-stated costs would be relevant as well:

Delivery cost and pick-up of laundry service

Self-service laundry expenses like laundering, detergent and mileage

It is necessary to understand the costs already incurred not varying from alternatives

are not relevant to future decisions. The following costs are identified as irrelevant to the

decision of purchasing the appliances:

Part A: Case Study Analysis

Requirement 1:

The provided case includes examples of fixed, variable, incremental and sunk

costs. However, sunk costs are not considered, since they are not included at the time

of undertaking final decision (Ahmad 2014). Fixed costs are those costs that do not vary

with rise or decline in the number of products or services produced or sold. On the other

hand, variable costs are those costs that increase or decrease based on the changes in

the volume of production. Incremental costs are those costs, which are used in business

planning analysis for obtaining an overview of additional cost to the organisation, if a

specific action is undertaken (Alsharari, Dixon and Youssef 2015). The examples of

these three types of costs from the provided case mainly include the following:

Cost Specific Example

Fixed Annual license fee amounting to $225, since it would not change

irrespective of the activities of the couple

Variable The total amount gathered for child care at a rate of $800 per child

would vary proportionately with the variations in the number of

enrolled students

Incremental The increased cost of utilities, which is $50, is fixed. According to the

case information, there would be increase in each month owing to

the day care and thus, the number of children is not a factor, As a

result, this cost could be adjudged as incremental cost owing to the

change in cost of utilities due to day care.

Requirement 2:

It is necessary to differentiate between costs, which are relevant and irrelevant to

the decision of appliance purchase. The two issues inherent in this situation include

whether the cost would be incurred owing to the decision undertaken in future and

whether the cost could be differentiated from alternatives. The cost is deemed to be

relevant, when it fulfils a specific set of criteria. Therefore, if Franks decides to buy the

appliances, the relevant costs are stated as follows:

New appliance cost

Delivery cost related to new appliances

Installation cost related to new appliances

Additional utility cost

In case; Franks decide to investigate all the available alternatives, it is necessary to

take into account the difference in costs among the alternatives (Brewer and Stout

2014). Therefore, the below-stated costs would be relevant as well:

Delivery cost and pick-up of laundry service

Self-service laundry expenses like laundering, detergent and mileage

It is necessary to understand the costs already incurred not varying from alternatives

are not relevant to future decisions. The following costs are identified as irrelevant to the

decision of purchasing the appliances:

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Case Studieslg...

|11

|3347

|500

Management Accounting Case Studies: Analysis, Costs, and Decisionslg...

|19

|4289

|385

Managerial Accounting Case Study and Journal Article Critiquelg...

|17

|3704

|60

Managerial Accounting, Case Studieslg...

|12

|3248

|281

Management Accounting Case Studies - Deskliblg...

|16

|3702

|370

HI5017 Managerial Accounting.lg...

|18

|2985

|274