ACC202 Management Accounting: Customer Profitability Case Study 2018

VerifiedAdded on 2023/06/07

|15

|2275

|305

Case Study

AI Summary

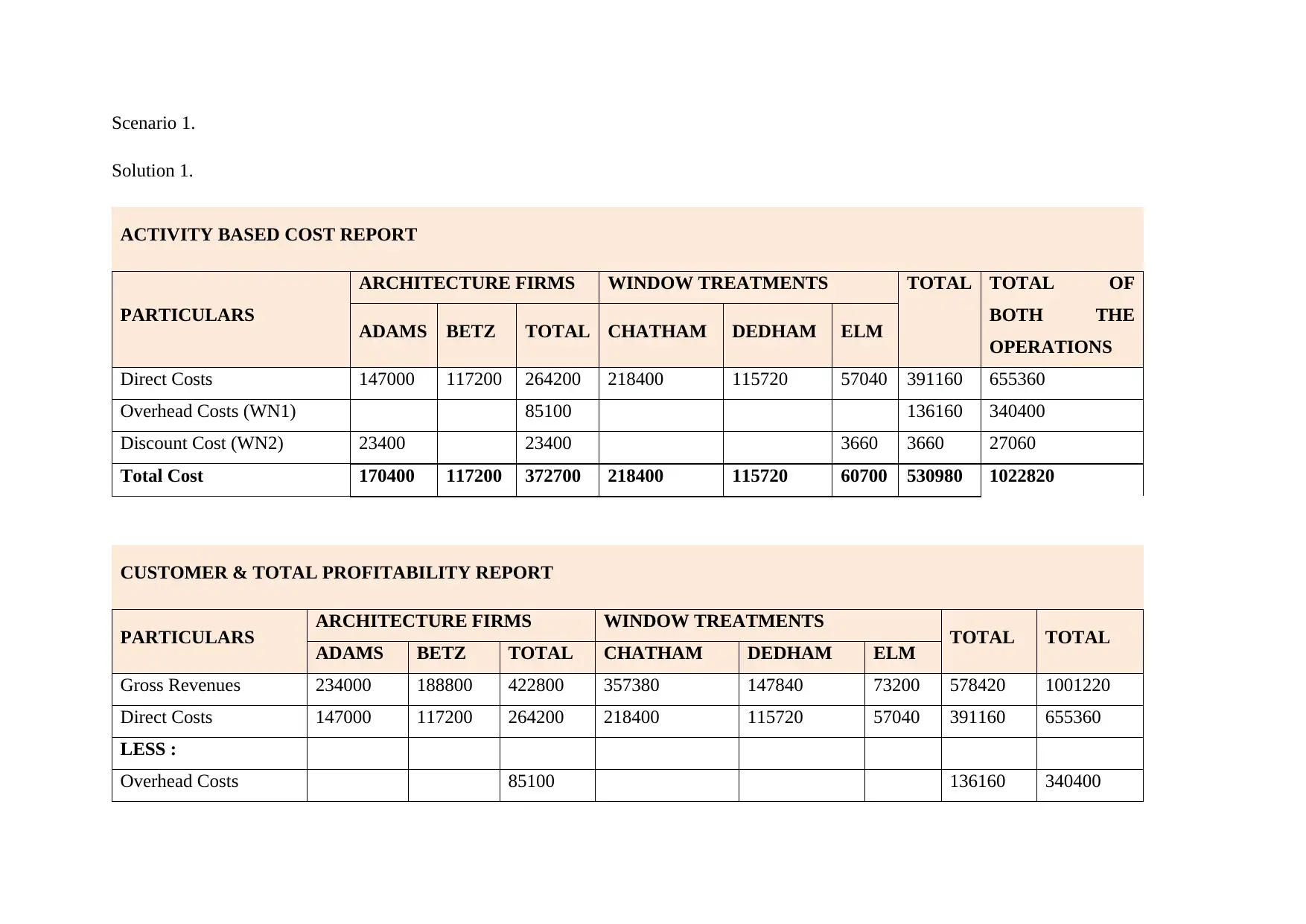

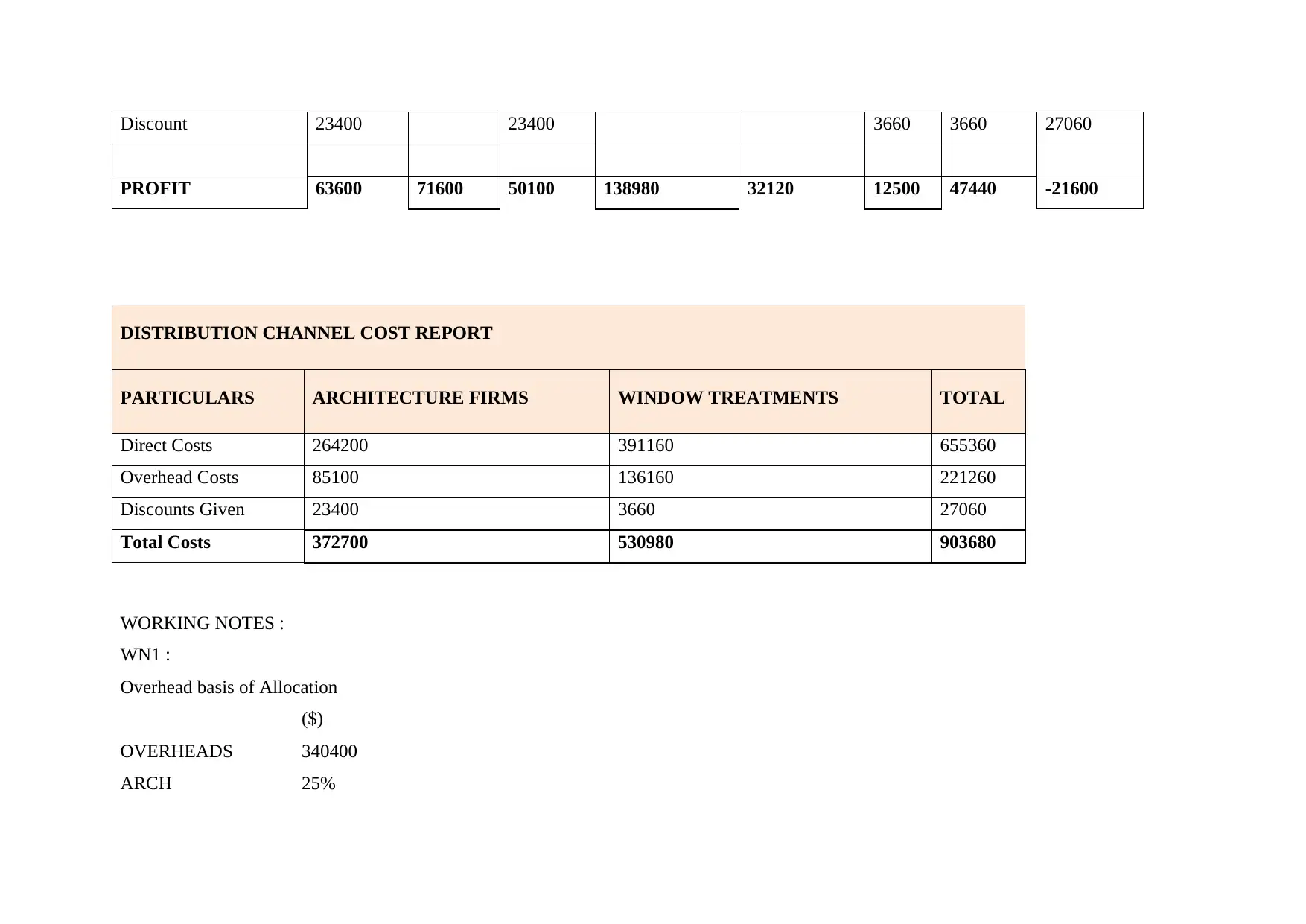

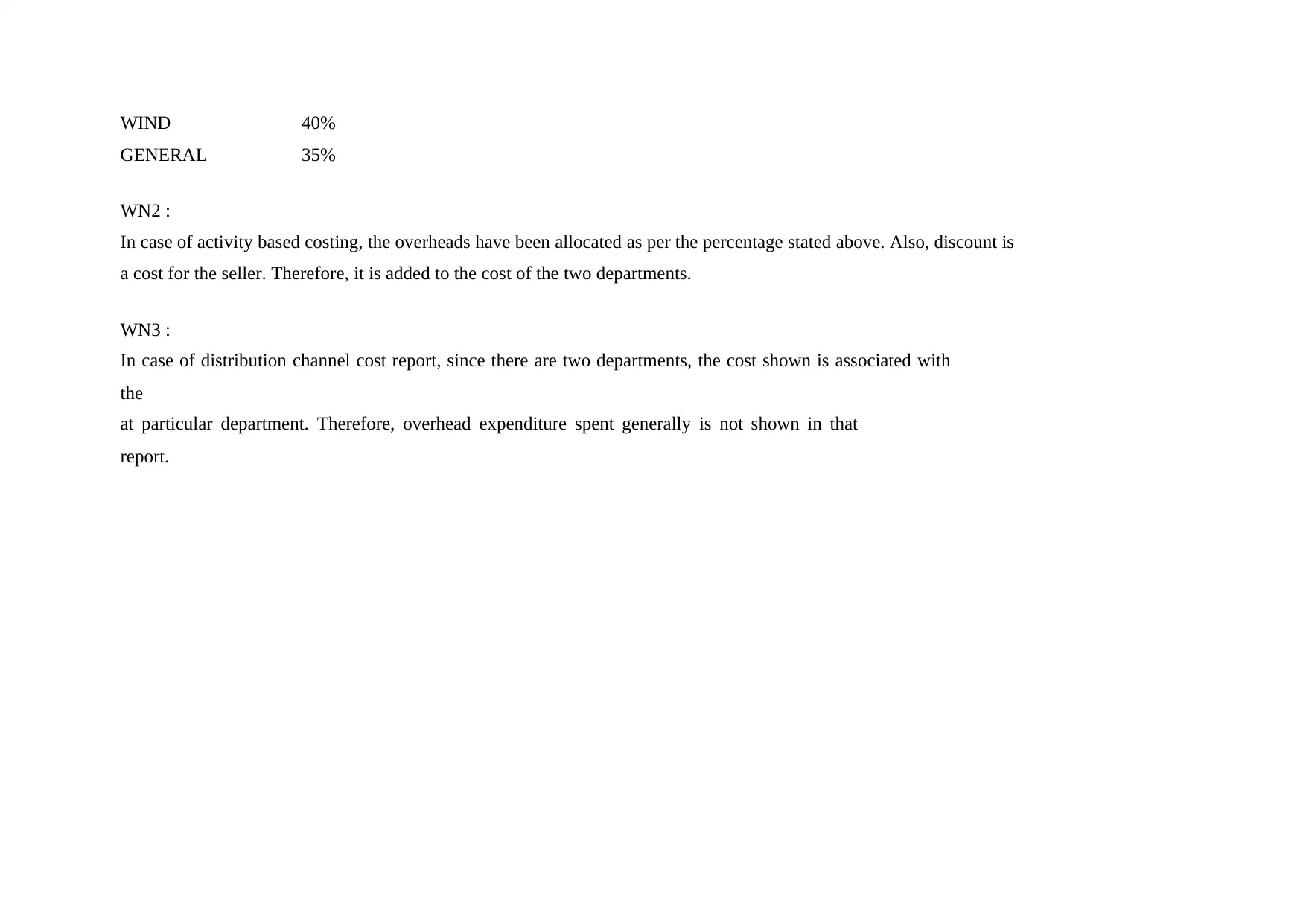

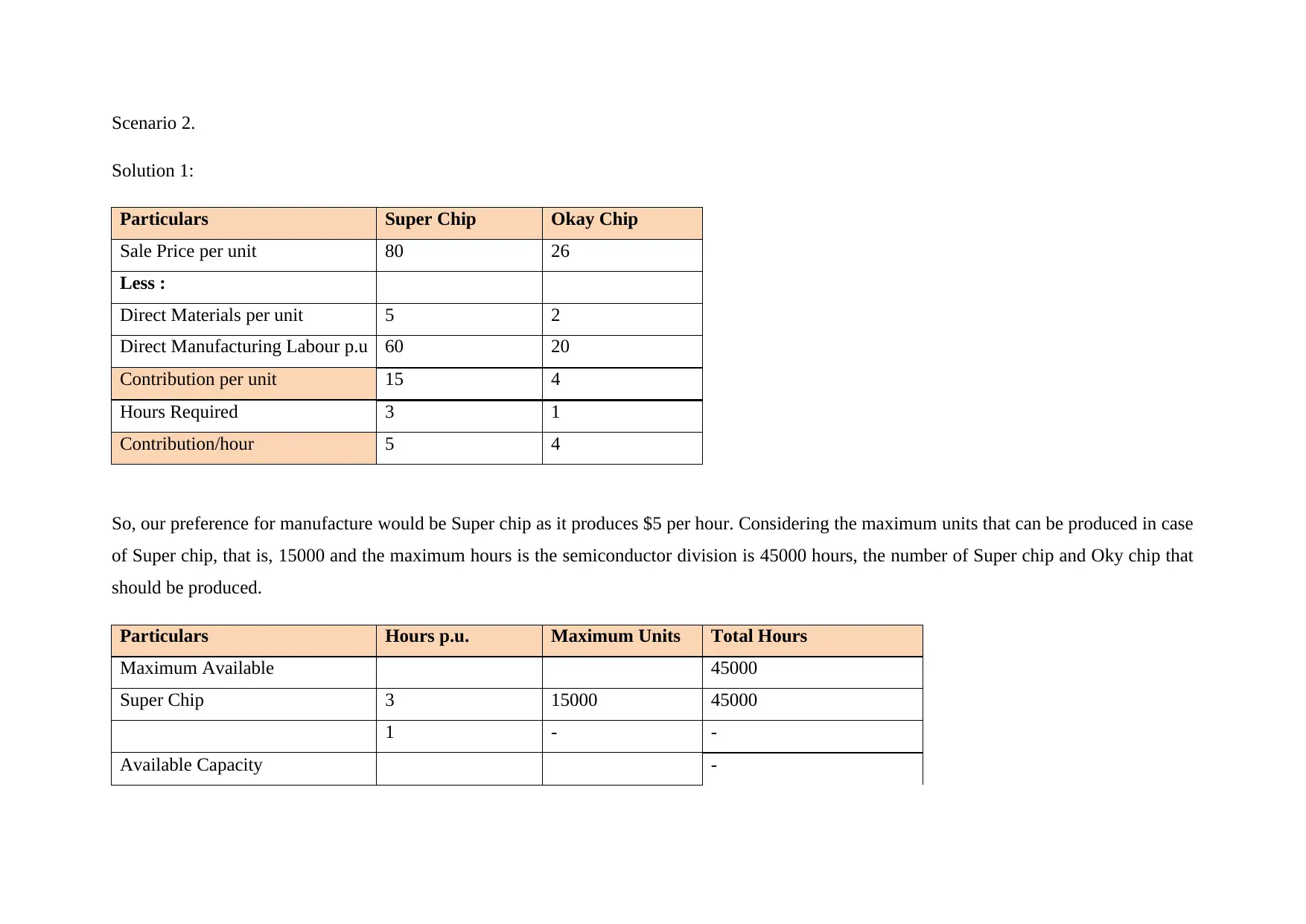

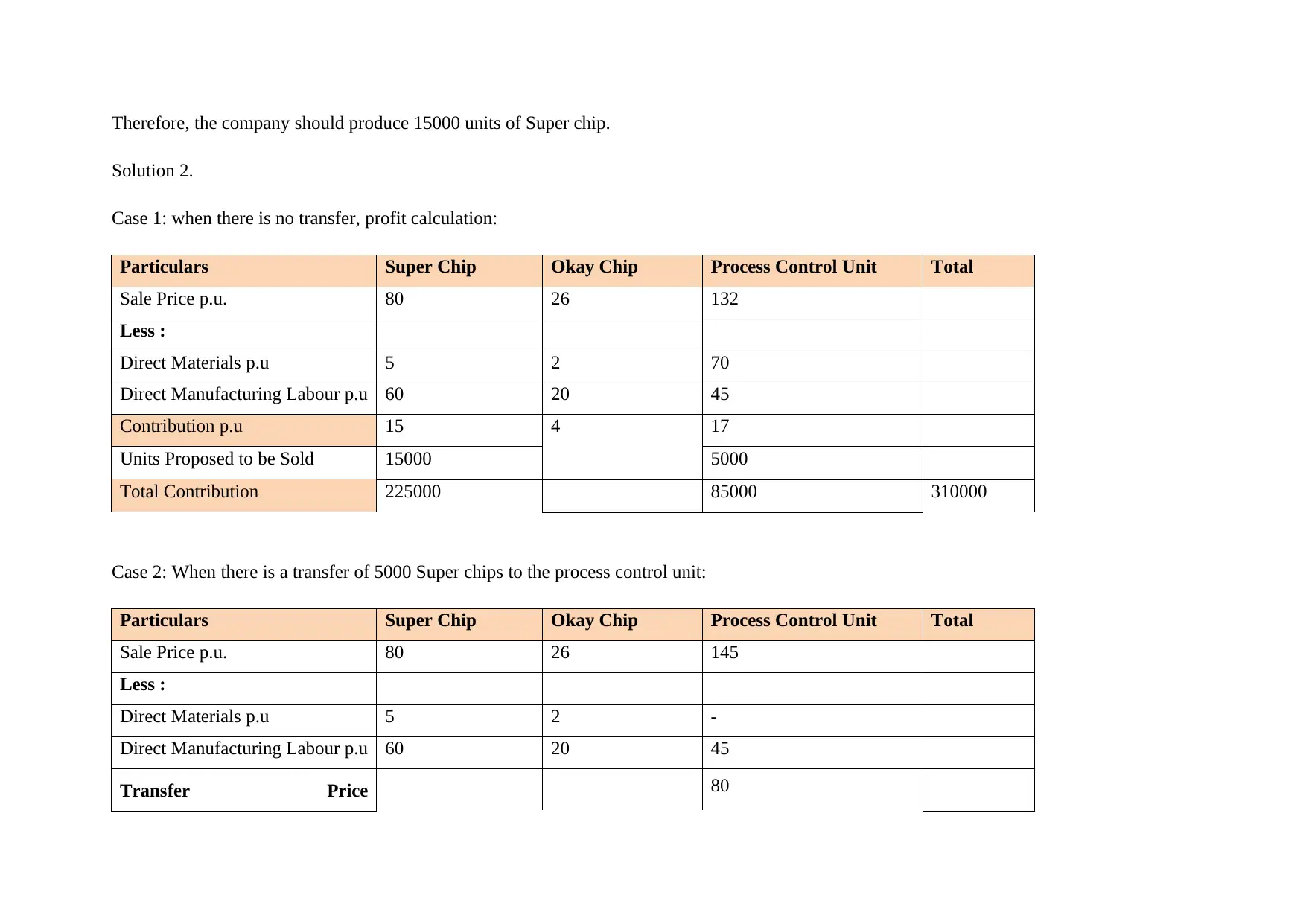

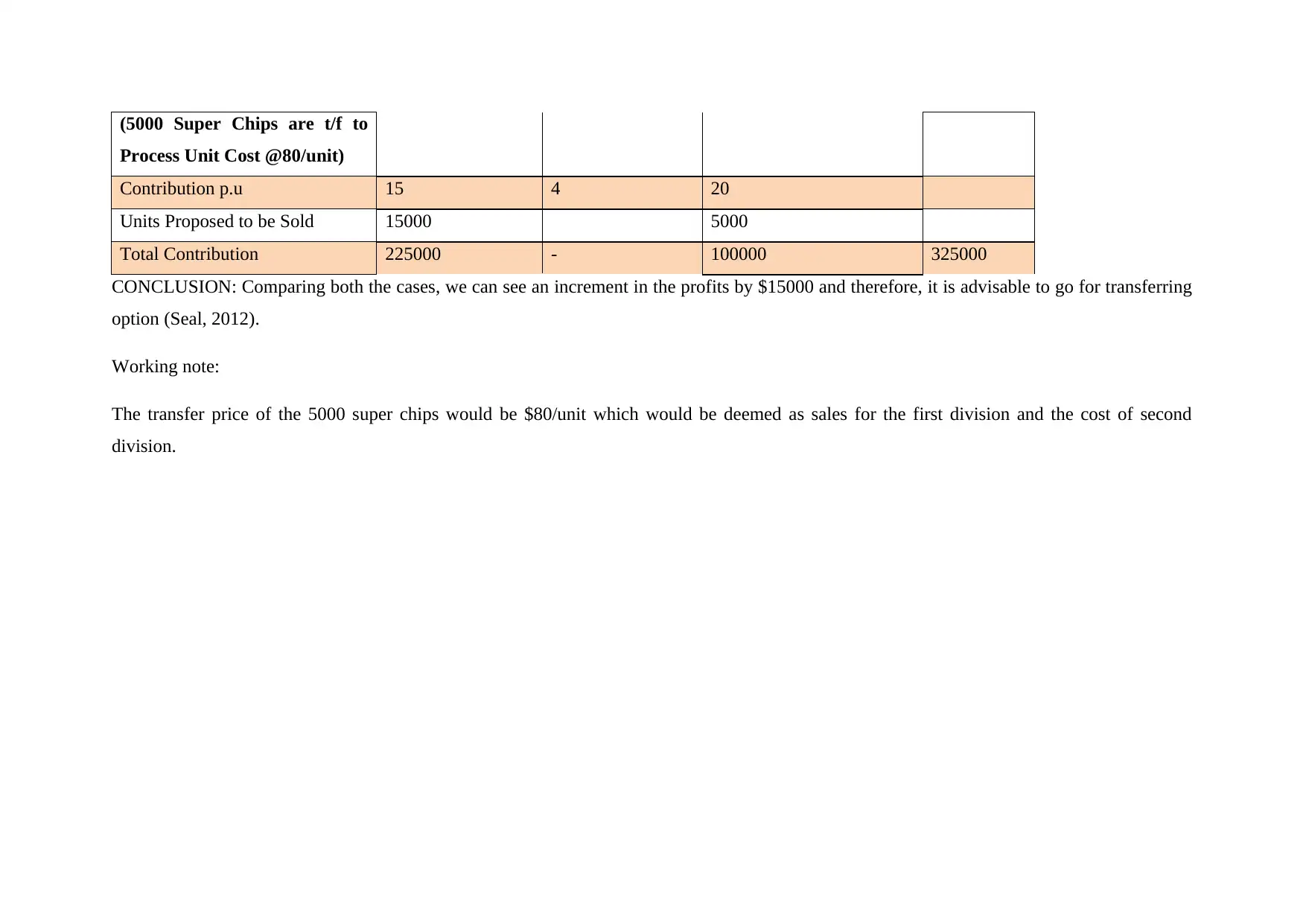

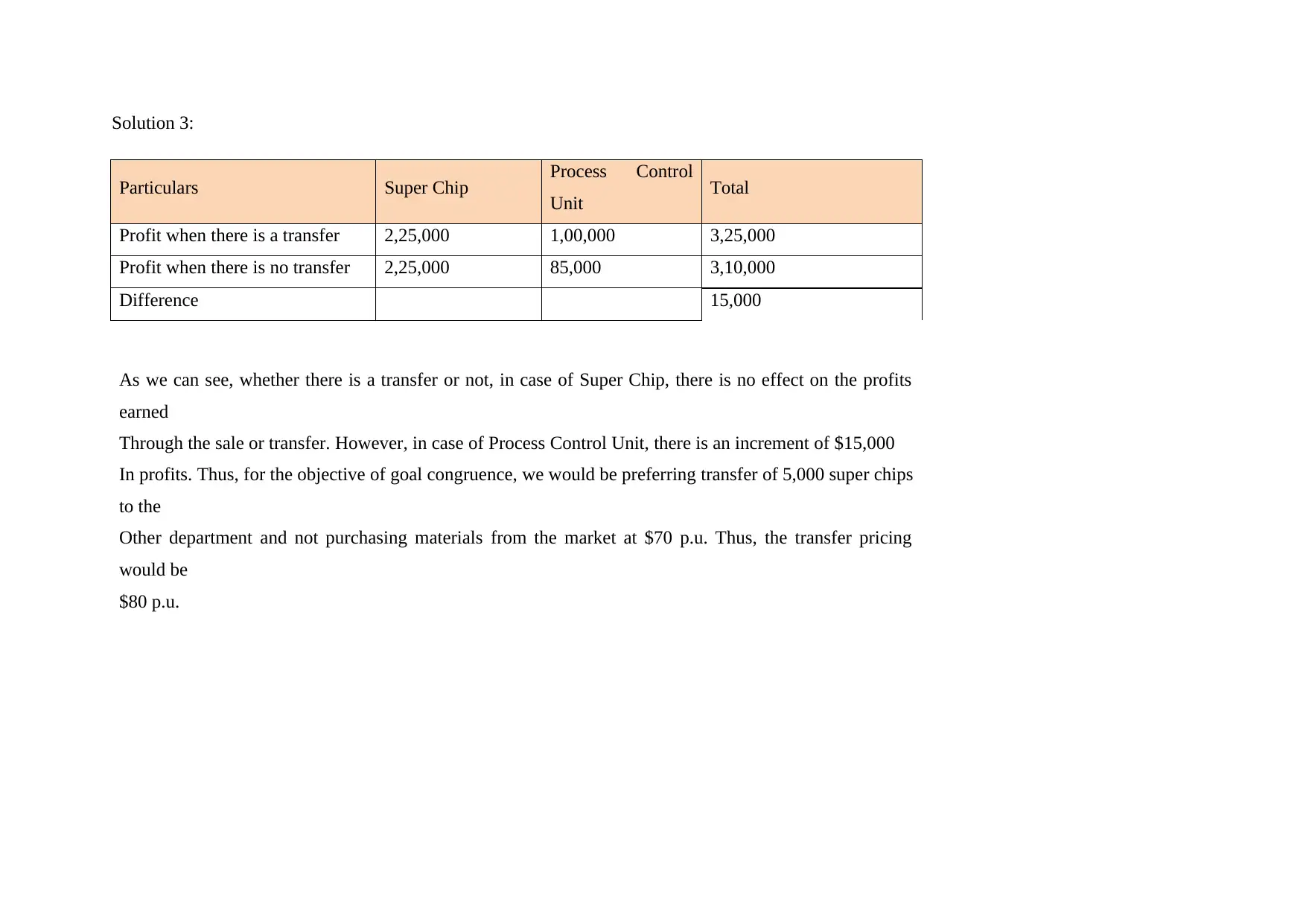

This assignment presents a comprehensive case study on management accounting, focusing on customer profitability, distribution channel costs, and transfer pricing. It involves analyzing Louise Fairbern's interior design consulting and window treatment business across two distribution channels. The solution includes an activity-based cost report, a customer profitability report, and a distribution channel cost report, with recommendations based on the analysis. The case study also explores transfer pricing decisions within a semiconductor division, evaluating the impact of internal transfers on overall profitability. The analysis highlights the importance of accurate cost allocation, strategic discounting, and informed transfer pricing for maximizing profitability and achieving goal congruence. Desklib offers a wealth of similar solved assignments and resources for students.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.