Management Accounting: Comparative Analysis and Strategic Application

VerifiedAdded on 2023/06/18

|18

|5054

|198

Report

AI Summary

This report provides a comprehensive analysis of managerial accounting, comparing it to financial accounting and bookkeeping, with a focus on its various components and applications within a business context. It evaluates commonly utilized budgetary control and reporting methodologies, emphasizing the applicability and long-term advantages of managerial accounting programs. The report includes an assessment of the convergence of managerial accounting systems and documentation, alongside a compilation of income statements using cost analytical methods like absorption and marginal pricing. It further assesses budgeting management planning instruments, highlighting their benefits and drawbacks, and examines the use of prediction methods for budgeting and projection. The study also assesses how companies adjust to the accounting information framework to address diverse accounting challenges, with managerial accounting research assisting in maintaining competitiveness by logically handling economic difficulties. The report concludes by emphasizing the development and assessment of bases for predicting, aiding a company in resolving fiscal issues for long-term benefits, using Capital Joinery Limited as a case study.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

P1. Examining managerial accountancy comparing it to finance bookkeeping and assessing

multiple components....................................................................................................................1

P2. Thorough evaluation among the most generally utilised budgetary control reporting

methodologies in the business market.........................................................................................4

M1. Recognition of the managerial accountancy program's applicability and its long-term

advantages....................................................................................................................................5

D1. An assessment of the convergence of both managerial accountancy systems and managing

accountancy documentation.........................................................................................................5

TASK 2............................................................................................................................................6

P3. Compilation of income statements and other essential phrases utilising cost analytical

methods such as absorption and marginal pricing.......................................................................6

M2. Using managerial accountancy approaches which are applicable and acceptable for

presenting financial information..................................................................................................9

D2. Assessment of the preceding presentation and analysis of information relating to company

activity.......................................................................................................................................10

TASK 3..........................................................................................................................................10

P4. A thorough evaluation of the budgeting management planning instruments, including their

benefits and drawbacks..............................................................................................................10

M3. Assessment and examination of the use of prediction methods for budgeting process and

projection...................................................................................................................................11

TASK 4..........................................................................................................................................12

P5. Assessment of multiple companies which adjust to the accounting information framework

in order to react effectively to diverse accounting challenges...................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

P1. Examining managerial accountancy comparing it to finance bookkeeping and assessing

multiple components....................................................................................................................1

P2. Thorough evaluation among the most generally utilised budgetary control reporting

methodologies in the business market.........................................................................................4

M1. Recognition of the managerial accountancy program's applicability and its long-term

advantages....................................................................................................................................5

D1. An assessment of the convergence of both managerial accountancy systems and managing

accountancy documentation.........................................................................................................5

TASK 2............................................................................................................................................6

P3. Compilation of income statements and other essential phrases utilising cost analytical

methods such as absorption and marginal pricing.......................................................................6

M2. Using managerial accountancy approaches which are applicable and acceptable for

presenting financial information..................................................................................................9

D2. Assessment of the preceding presentation and analysis of information relating to company

activity.......................................................................................................................................10

TASK 3..........................................................................................................................................10

P4. A thorough evaluation of the budgeting management planning instruments, including their

benefits and drawbacks..............................................................................................................10

M3. Assessment and examination of the use of prediction methods for budgeting process and

projection...................................................................................................................................11

TASK 4..........................................................................................................................................12

P5. Assessment of multiple companies which adjust to the accounting information framework

in order to react effectively to diverse accounting challenges...................................................12

M4. Managerial accounting research which assists businesses in remaining competitive by

handling economic difficulties in a logical manner...................................................................13

D3. Development and assessment of basis for predicting which assist a company in resolving

fiscal issues so that it can be beneficial in the longer haul........................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

handling economic difficulties in a logical manner...................................................................13

D3. Development and assessment of basis for predicting which assist a company in resolving

fiscal issues so that it can be beneficial in the longer haul........................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Administrative accountancy for all organisations functioning in the economy, regardless

of the sector in where it operates is among the most significant as well as crucial (Bufoni,

Ferreira and Oliveira, 2018). It is described as a procedure for identifying all the elements

affecting a company's operations such that the necessary steps are implemented following a

complete monitoring and interpretation of all the issues affecting it. Capital Joinery Limited is a

company founded in 2008 and operating in the United Kingdom that supplies numerous items /

solutions which have a huge amount of potential on current economy. This study provides a

thorough analysis of accounting information and the words that are associated with it. Aside

from that, the paper discusses various accounting methods, financial accounting, benefits and

disadvantages, expenses, and so on. This research also shows a review and assessment of the

aforementioned business and its rival.

P1. Examining managerial accountancy comparing it to finance bookkeeping and assessing

multiple components

Managerial control is a method which includes identifying and analysing every aspect that

influence the environment, whether explicitly or implicitly, so that requisite measures can be

made in a timely manner to contribute to the company's worth in the longer term. These choices

are of high significance to any company since they are able to enhance revenues and,

consequently, the profitability of the company, and they can harm and disorder the operation and

marketplace profitability of the organization if they are not properly used. Capital joinery

Limited is a corporation that largely offers solutions to its clients, however the organization was

created just in 2008 however, related to high quality of product it delivers to its targeted clients,

has acquired a greater chunk in the marketplace within a specific window. As a result, it is

critical for the firm to make suitable strategic decisions in order to sustain the organization's

companies focused while also allowing the company to expand and flourish in the sector and

take advantage of its competition in the market (CSCA, 2018). Both accrual analysis and

managerial accounting are very important and are necessary for organisations, but there are

significant distinctions between them which are detailed in detail below with respect to the

corporate Capital joinery Limited-

Management accounting Financial accounting

Administrative accountancy for all organisations functioning in the economy, regardless

of the sector in where it operates is among the most significant as well as crucial (Bufoni,

Ferreira and Oliveira, 2018). It is described as a procedure for identifying all the elements

affecting a company's operations such that the necessary steps are implemented following a

complete monitoring and interpretation of all the issues affecting it. Capital Joinery Limited is a

company founded in 2008 and operating in the United Kingdom that supplies numerous items /

solutions which have a huge amount of potential on current economy. This study provides a

thorough analysis of accounting information and the words that are associated with it. Aside

from that, the paper discusses various accounting methods, financial accounting, benefits and

disadvantages, expenses, and so on. This research also shows a review and assessment of the

aforementioned business and its rival.

P1. Examining managerial accountancy comparing it to finance bookkeeping and assessing

multiple components

Managerial control is a method which includes identifying and analysing every aspect that

influence the environment, whether explicitly or implicitly, so that requisite measures can be

made in a timely manner to contribute to the company's worth in the longer term. These choices

are of high significance to any company since they are able to enhance revenues and,

consequently, the profitability of the company, and they can harm and disorder the operation and

marketplace profitability of the organization if they are not properly used. Capital joinery

Limited is a corporation that largely offers solutions to its clients, however the organization was

created just in 2008 however, related to high quality of product it delivers to its targeted clients,

has acquired a greater chunk in the marketplace within a specific window. As a result, it is

critical for the firm to make suitable strategic decisions in order to sustain the organization's

companies focused while also allowing the company to expand and flourish in the sector and

take advantage of its competition in the market (CSCA, 2018). Both accrual analysis and

managerial accounting are very important and are necessary for organisations, but there are

significant distinctions between them which are detailed in detail below with respect to the

corporate Capital joinery Limited-

Management accounting Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This sort of accountancy is not required

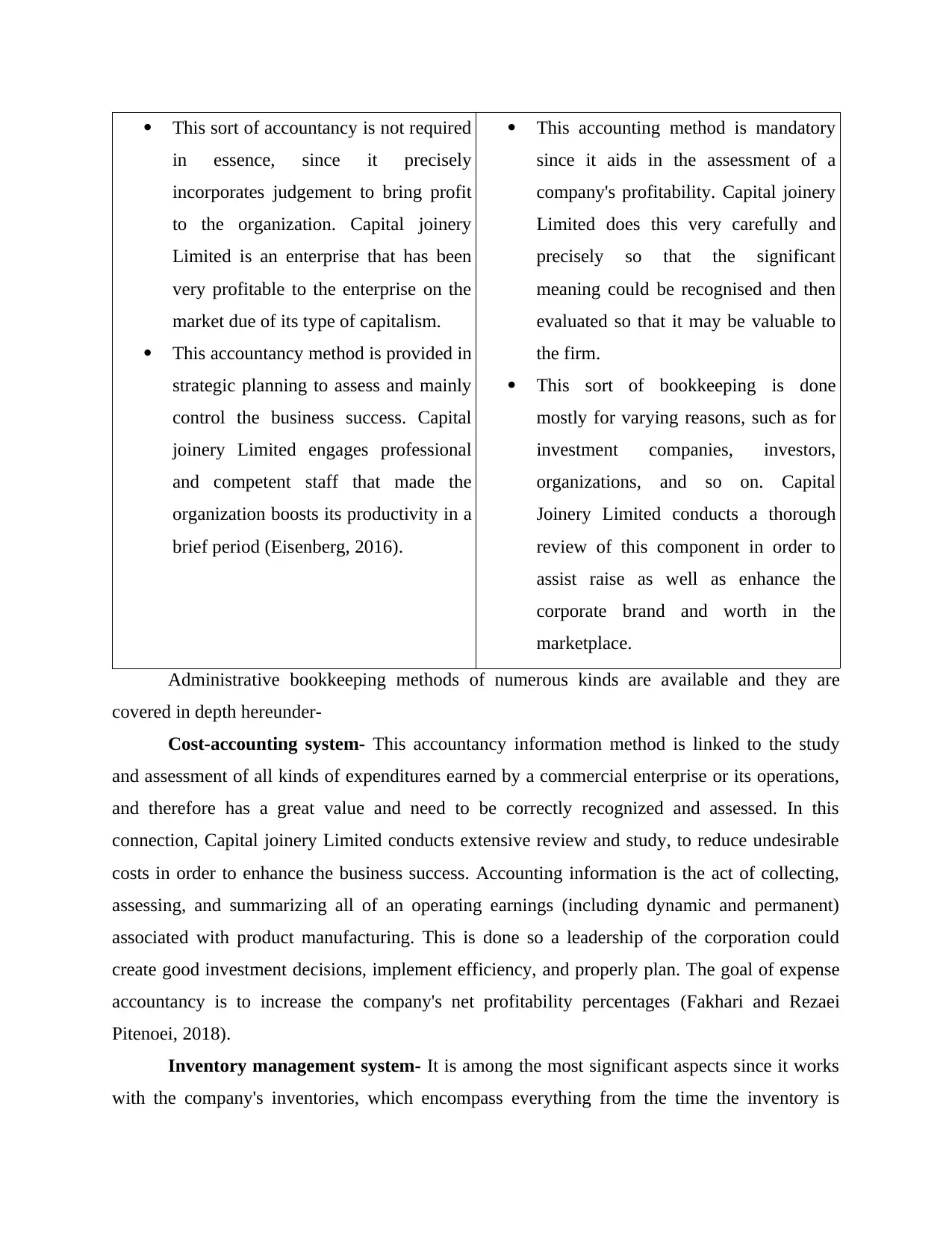

in essence, since it precisely

incorporates judgement to bring profit

to the organization. Capital joinery

Limited is an enterprise that has been

very profitable to the enterprise on the

market due of its type of capitalism.

This accountancy method is provided in

strategic planning to assess and mainly

control the business success. Capital

joinery Limited engages professional

and competent staff that made the

organization boosts its productivity in a

brief period (Eisenberg, 2016).

This accounting method is mandatory

since it aids in the assessment of a

company's profitability. Capital joinery

Limited does this very carefully and

precisely so that the significant

meaning could be recognised and then

evaluated so that it may be valuable to

the firm.

This sort of bookkeeping is done

mostly for varying reasons, such as for

investment companies, investors,

organizations, and so on. Capital

Joinery Limited conducts a thorough

review of this component in order to

assist raise as well as enhance the

corporate brand and worth in the

marketplace.

Administrative bookkeeping methods of numerous kinds are available and they are

covered in depth hereunder-

Cost-accounting system- This accountancy information method is linked to the study

and assessment of all kinds of expenditures earned by a commercial enterprise or its operations,

and therefore has a great value and need to be correctly recognized and assessed. In this

connection, Capital joinery Limited conducts extensive review and study, to reduce undesirable

costs in order to enhance the business success. Accounting information is the act of collecting,

assessing, and summarizing all of an operating earnings (including dynamic and permanent)

associated with product manufacturing. This is done so a leadership of the corporation could

create good investment decisions, implement efficiency, and properly plan. The goal of expense

accountancy is to increase the company's net profitability percentages (Fakhari and Rezaei

Pitenoei, 2018).

Inventory management system- It is among the most significant aspects since it works

with the company's inventories, which encompass everything from the time the inventory is

in essence, since it precisely

incorporates judgement to bring profit

to the organization. Capital joinery

Limited is an enterprise that has been

very profitable to the enterprise on the

market due of its type of capitalism.

This accountancy method is provided in

strategic planning to assess and mainly

control the business success. Capital

joinery Limited engages professional

and competent staff that made the

organization boosts its productivity in a

brief period (Eisenberg, 2016).

This accounting method is mandatory

since it aids in the assessment of a

company's profitability. Capital joinery

Limited does this very carefully and

precisely so that the significant

meaning could be recognised and then

evaluated so that it may be valuable to

the firm.

This sort of bookkeeping is done

mostly for varying reasons, such as for

investment companies, investors,

organizations, and so on. Capital

Joinery Limited conducts a thorough

review of this component in order to

assist raise as well as enhance the

corporate brand and worth in the

marketplace.

Administrative bookkeeping methods of numerous kinds are available and they are

covered in depth hereunder-

Cost-accounting system- This accountancy information method is linked to the study

and assessment of all kinds of expenditures earned by a commercial enterprise or its operations,

and therefore has a great value and need to be correctly recognized and assessed. In this

connection, Capital joinery Limited conducts extensive review and study, to reduce undesirable

costs in order to enhance the business success. Accounting information is the act of collecting,

assessing, and summarizing all of an operating earnings (including dynamic and permanent)

associated with product manufacturing. This is done so a leadership of the corporation could

create good investment decisions, implement efficiency, and properly plan. The goal of expense

accountancy is to increase the company's net profitability percentages (Fakhari and Rezaei

Pitenoei, 2018).

Inventory management system- It is among the most significant aspects since it works

with the company's inventories, which encompass everything from the time the inventory is

purchased until it is delivered. Stock administration is concerned with the operations of

purchasing, keeping, and benefiting from items as they go down the line between makers to

client. This may appear to be an easy operation; however there are numerous key regular

activities which must be followed in order to sustain ordered and effective inventories. It is hard

to maintain a proper stability between all the variables involved of a storage solution. Inventory

management assists businesses in determining which as well as how much merchandise to

purchase at what moment. It keeps a record of merchandise from acquisition to disposal. The

technique analyzes and reacts to patterns in order to make sure that there will always be

sufficient stock to satisfy order placement and that there is adequate notification of a shortfall.

Capital Joinery Limited has a well-established production process, which enables it to meet all

requirements precisely.

Job-costing system- Job order costing is a mechanism which occurs whenever clients

purchase tiny, one-of-a-kind quantities of things. This method recognizes the pricing of each

additional object and guarantees that the cost is fair enough for every buyer to buy whilst yet

enabling the corporation to earn. This could acquire and monitor obtained from multiple

elements such as manufacturing costs, financial documents, vendor bills, and administrative

allowances. Those materials will be used by an auditor to collect tabulate or record this using a

task cost sheet. They could also utilise a job order system containing every item by assigning a

unique identifier to each one. Whenever things are created associated with individual customer

requests, the job - order costing system is employed. Every object created is regarded as a job.

Expenses are monitored on a job-by-job basis. A job can also be defined as beneficial owners. In

a technological sense, the work order costing method should record and monitor the associated

with creating each task, that mainly contains, labour, and administration. This method is

concerned with the optimal scheduling and distribution of duties so that they can be executed

correctly. Capital Joinery Limited assesses the capability of each of its employees and then

assigns work based on that assessment in order to complete projects on schedule and with the

higher precision (Georgiev, 2016).

Price-optimising system- The choice of a reasonable price and profits in the business are

all about it. Capital joinery Limited carries out a careful examination of all elements in order to

make a proper conclusion.

purchasing, keeping, and benefiting from items as they go down the line between makers to

client. This may appear to be an easy operation; however there are numerous key regular

activities which must be followed in order to sustain ordered and effective inventories. It is hard

to maintain a proper stability between all the variables involved of a storage solution. Inventory

management assists businesses in determining which as well as how much merchandise to

purchase at what moment. It keeps a record of merchandise from acquisition to disposal. The

technique analyzes and reacts to patterns in order to make sure that there will always be

sufficient stock to satisfy order placement and that there is adequate notification of a shortfall.

Capital Joinery Limited has a well-established production process, which enables it to meet all

requirements precisely.

Job-costing system- Job order costing is a mechanism which occurs whenever clients

purchase tiny, one-of-a-kind quantities of things. This method recognizes the pricing of each

additional object and guarantees that the cost is fair enough for every buyer to buy whilst yet

enabling the corporation to earn. This could acquire and monitor obtained from multiple

elements such as manufacturing costs, financial documents, vendor bills, and administrative

allowances. Those materials will be used by an auditor to collect tabulate or record this using a

task cost sheet. They could also utilise a job order system containing every item by assigning a

unique identifier to each one. Whenever things are created associated with individual customer

requests, the job - order costing system is employed. Every object created is regarded as a job.

Expenses are monitored on a job-by-job basis. A job can also be defined as beneficial owners. In

a technological sense, the work order costing method should record and monitor the associated

with creating each task, that mainly contains, labour, and administration. This method is

concerned with the optimal scheduling and distribution of duties so that they can be executed

correctly. Capital Joinery Limited assesses the capability of each of its employees and then

assigns work based on that assessment in order to complete projects on schedule and with the

higher precision (Georgiev, 2016).

Price-optimising system- The choice of a reasonable price and profits in the business are

all about it. Capital joinery Limited carries out a careful examination of all elements in order to

make a proper conclusion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition, there are several corporate accountancy systems needs, which have tremendous

value in the present condition of the economy and are all discussed in depth hereunder-

Management style- There is a great deal of importance in adopting an appropriate

leadership style, because it helps the industry to expand by boosting productivity and

revenue, and therefore can harm and destroy a reputation of an organisation if not

carefully considered.

Organisation structure- It is critical to design an organizational design in a functional

and timely way so that it would help improve the business's success in the longer term.

Information requirements- All company actions must be centred on gathering pertinent

data that will contribute to the company’s profitability in the sector in wherein it operates

(Hemmer and Labro, 2017).

P2. Thorough evaluation among the most generally utilised budgetary control reporting

methodologies in the business market

Managerial financial statements are those provided by administrators to authorized

officials following a complete study of all the aspects that exact way the operation of the

organisation in order to assist the company in growing in the marketplace. Capital joinery

Limited utilizes a variety of ways of accounting in its functioning, all of which are detailed here-

Budget report- It is a kind of reporting which produces plans for the prospective and

serves as a basis to identify and immediately rectify with no wastage if variances occur in the

overall results. While producing the strategy, Capital joinery Limited conducts numerous kinds

of analyses to ensure that it is ideal for the business to thrive in the challenging marketplace.

Accounts receivable ageing report- This sort of analysis is concerned with the operation

of the corporation's working capital, or borrowers, as it is among the most significant areas of the

industry. Capital joinery Limited had employed a trained staff that conducts all proper work on

its account in order to be valuable to the firm in the lengthy period.

Performance report- As the name implies, the analysis is concerned with studying and

assessing the company’s financial success over a specific time period in order to determine

whether or not resources are being used appropriately. In its accounting records Capital joinery

Limited displays its summary sheet so that it may enable its staff to reach their targets within a

limited time period.

value in the present condition of the economy and are all discussed in depth hereunder-

Management style- There is a great deal of importance in adopting an appropriate

leadership style, because it helps the industry to expand by boosting productivity and

revenue, and therefore can harm and destroy a reputation of an organisation if not

carefully considered.

Organisation structure- It is critical to design an organizational design in a functional

and timely way so that it would help improve the business's success in the longer term.

Information requirements- All company actions must be centred on gathering pertinent

data that will contribute to the company’s profitability in the sector in wherein it operates

(Hemmer and Labro, 2017).

P2. Thorough evaluation among the most generally utilised budgetary control reporting

methodologies in the business market

Managerial financial statements are those provided by administrators to authorized

officials following a complete study of all the aspects that exact way the operation of the

organisation in order to assist the company in growing in the marketplace. Capital joinery

Limited utilizes a variety of ways of accounting in its functioning, all of which are detailed here-

Budget report- It is a kind of reporting which produces plans for the prospective and

serves as a basis to identify and immediately rectify with no wastage if variances occur in the

overall results. While producing the strategy, Capital joinery Limited conducts numerous kinds

of analyses to ensure that it is ideal for the business to thrive in the challenging marketplace.

Accounts receivable ageing report- This sort of analysis is concerned with the operation

of the corporation's working capital, or borrowers, as it is among the most significant areas of the

industry. Capital joinery Limited had employed a trained staff that conducts all proper work on

its account in order to be valuable to the firm in the lengthy period.

Performance report- As the name implies, the analysis is concerned with studying and

assessing the company’s financial success over a specific time period in order to determine

whether or not resources are being used appropriately. In its accounting records Capital joinery

Limited displays its summary sheet so that it may enable its staff to reach their targets within a

limited time period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory and manufacturing report- This analysis is linked to stocks that a company

has and works with all its associated features so that detection may be made if waste products

occur. Capital Joinery Limited employs people who are both knowledgeable and qualified in this

field so that their know-how will be useful for the company (Khemakhem and Fontaine, 2020).

M1. Recognition of the managerial accountancy program's applicability and its long-term

advantages

The advantages and implementation of managerial accountancy systems in the analysis of

the organisation are briefly discussed below-

Cost-accounting system- It is particularly beneficial since it gives necessary details on

budgeting, and after reviewing this data, expenses from unproductive operations could be

lowered in order to raise the profitability of the stock by utilising the amount in those other

operations that really can yield a higher returns. Capital joinery Limited analyses it using

multiple ways in order to assist the company expand as a total in a highly dynamic market.

Inventory management system- This technology helps ease the processes of the

company and the company called Capital Joinery Limited utilizes it to streamline the dynamic

business procedure.

Job-costing system- The success of the person is quite beneficial in gauging the

corporation's long term growth. In this respect Capital joinery Limited utilises all its resource

accessible to come in handy to the company.

Price-optimising system- This approach is really valuable as it increases the chances

required to make choices more concise and Capital joinery Limited utilises it to shorten the costs

required to take strategic decisions. That's very beneficial (King, 2016).

D1. An assessment of the convergence of both managerial accountancy systems and managing

accountancy documentation

The financial mechanism and its documentation are interlinked and interconnected and

assist the business to operate efficiently and effectively, and are explored in greater detail

hereunder-

Budget report- The organization Capital joinery Limited's profits depend heavily on this

aspect and has been using this rather appropriately and shown thus extremely essential for the

organisation. It is also extremely useable in all environment of a commercial enterprise.

has and works with all its associated features so that detection may be made if waste products

occur. Capital Joinery Limited employs people who are both knowledgeable and qualified in this

field so that their know-how will be useful for the company (Khemakhem and Fontaine, 2020).

M1. Recognition of the managerial accountancy program's applicability and its long-term

advantages

The advantages and implementation of managerial accountancy systems in the analysis of

the organisation are briefly discussed below-

Cost-accounting system- It is particularly beneficial since it gives necessary details on

budgeting, and after reviewing this data, expenses from unproductive operations could be

lowered in order to raise the profitability of the stock by utilising the amount in those other

operations that really can yield a higher returns. Capital joinery Limited analyses it using

multiple ways in order to assist the company expand as a total in a highly dynamic market.

Inventory management system- This technology helps ease the processes of the

company and the company called Capital Joinery Limited utilizes it to streamline the dynamic

business procedure.

Job-costing system- The success of the person is quite beneficial in gauging the

corporation's long term growth. In this respect Capital joinery Limited utilises all its resource

accessible to come in handy to the company.

Price-optimising system- This approach is really valuable as it increases the chances

required to make choices more concise and Capital joinery Limited utilises it to shorten the costs

required to take strategic decisions. That's very beneficial (King, 2016).

D1. An assessment of the convergence of both managerial accountancy systems and managing

accountancy documentation

The financial mechanism and its documentation are interlinked and interconnected and

assist the business to operate efficiently and effectively, and are explored in greater detail

hereunder-

Budget report- The organization Capital joinery Limited's profits depend heavily on this

aspect and has been using this rather appropriately and shown thus extremely essential for the

organisation. It is also extremely useable in all environment of a commercial enterprise.

Cost-accounting system- It is both a very important service since it tends to decrease

expenses in order to make the business economically solid, also with complete conductivity

Capital joinery Limited is doing the similar so that it can enable the business to develop and

thrive over time (Lestari, Sofianty and Sukarmanto, 2018).

TASK 2

P3. Compilation of income statements and other essential phrases utilising cost analytical

methods such as absorption and marginal pricing

Expenses are a crucial issue, because there are various kinds of expenses which are

experienced by each and every company, all of which are detailed in detail below-

Fixed cost- It is a form of expense which does not alter with manufacturing whereas the

firm is running in the sector. It is an expense which will be incurred whether the firm is running

or otherwise, and the corporate Capital joinery Limited has very few fixed expenses, which

enables the corporation to achieve significant earnings in the marketplace and that too in a short

span of time.

Variable cost- The expenses are those which fluctuate with the corporation's changing

capacity of productivity and could be described as the expenditure involved in creating an

additional manufacturing unit. This cuts the amount per cohesive block and becomes profitable

for the enterprise in the long-term. Capital joinery Limited generates significant outputs.

Semi-variable cost- It is an expense category which contains the above two costs, which

is permanent in some way while others are of a varying size. Capital joinery Limited maintains

its semi-variable price minimal so that it would last further than its rivals in the industry.

Cost analysis- It is a form of study wherein numerous expenses are examined and

reviewed so that extra expenditures can be minimised with quick consequence, increasing as well

as improving the corporation's situation. Capital Joinery Limited employs a particular group of

expert’s employees who are knowledgeable in this respect so that this element may be properly

analysed.

Absorption costing- It is an accounting method which encompasses all forms of

expenditures incurred by the firm whilst carrying out its regular operations, such as rental,

salaries, and so on (Namazi and Rezaei, 2017).

expenses in order to make the business economically solid, also with complete conductivity

Capital joinery Limited is doing the similar so that it can enable the business to develop and

thrive over time (Lestari, Sofianty and Sukarmanto, 2018).

TASK 2

P3. Compilation of income statements and other essential phrases utilising cost analytical

methods such as absorption and marginal pricing

Expenses are a crucial issue, because there are various kinds of expenses which are

experienced by each and every company, all of which are detailed in detail below-

Fixed cost- It is a form of expense which does not alter with manufacturing whereas the

firm is running in the sector. It is an expense which will be incurred whether the firm is running

or otherwise, and the corporate Capital joinery Limited has very few fixed expenses, which

enables the corporation to achieve significant earnings in the marketplace and that too in a short

span of time.

Variable cost- The expenses are those which fluctuate with the corporation's changing

capacity of productivity and could be described as the expenditure involved in creating an

additional manufacturing unit. This cuts the amount per cohesive block and becomes profitable

for the enterprise in the long-term. Capital joinery Limited generates significant outputs.

Semi-variable cost- It is an expense category which contains the above two costs, which

is permanent in some way while others are of a varying size. Capital joinery Limited maintains

its semi-variable price minimal so that it would last further than its rivals in the industry.

Cost analysis- It is a form of study wherein numerous expenses are examined and

reviewed so that extra expenditures can be minimised with quick consequence, increasing as well

as improving the corporation's situation. Capital Joinery Limited employs a particular group of

expert’s employees who are knowledgeable in this respect so that this element may be properly

analysed.

Absorption costing- It is an accounting method which encompasses all forms of

expenditures incurred by the firm whilst carrying out its regular operations, such as rental,

salaries, and so on (Namazi and Rezaei, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

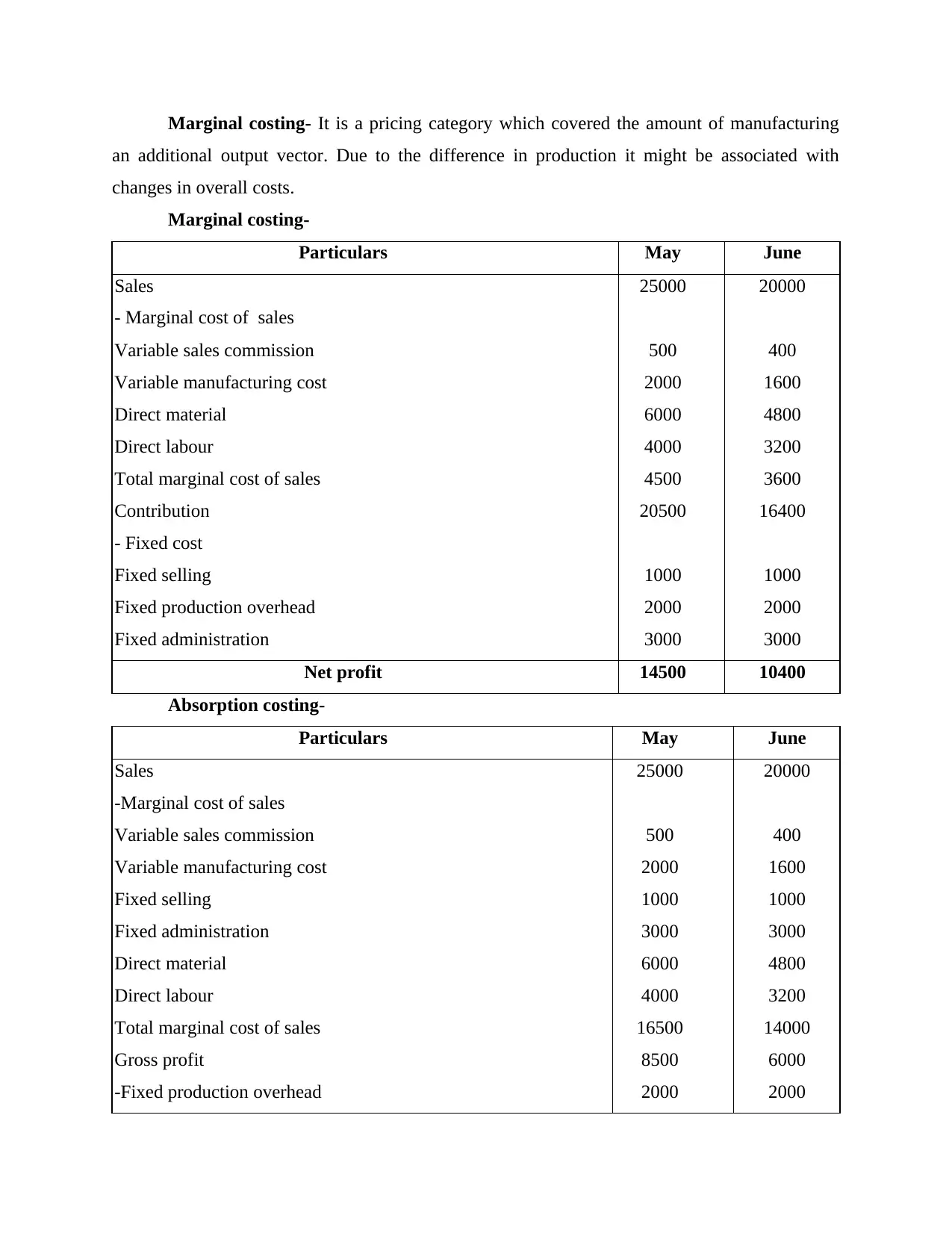

Marginal costing- It is a pricing category which covered the amount of manufacturing

an additional output vector. Due to the difference in production it might be associated with

changes in overall costs.

Marginal costing-

Particulars May June

Sales 25000 20000

- Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Direct material 6000 4800

Direct labour 4000 3200

Total marginal cost of sales 4500 3600

Contribution 20500 16400

- Fixed cost

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 14500 10400

Absorption costing-

Particulars May June

Sales 25000 20000

-Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Fixed selling 1000 1000

Fixed administration 3000 3000

Direct material 6000 4800

Direct labour 4000 3200

Total marginal cost of sales 16500 14000

Gross profit 8500 6000

-Fixed production overhead 2000 2000

an additional output vector. Due to the difference in production it might be associated with

changes in overall costs.

Marginal costing-

Particulars May June

Sales 25000 20000

- Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Direct material 6000 4800

Direct labour 4000 3200

Total marginal cost of sales 4500 3600

Contribution 20500 16400

- Fixed cost

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 14500 10400

Absorption costing-

Particulars May June

Sales 25000 20000

-Marginal cost of sales

Variable sales commission 500 400

Variable manufacturing cost 2000 1600

Fixed selling 1000 1000

Fixed administration 3000 3000

Direct material 6000 4800

Direct labour 4000 3200

Total marginal cost of sales 16500 14000

Gross profit 8500 6000

-Fixed production overhead 2000 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

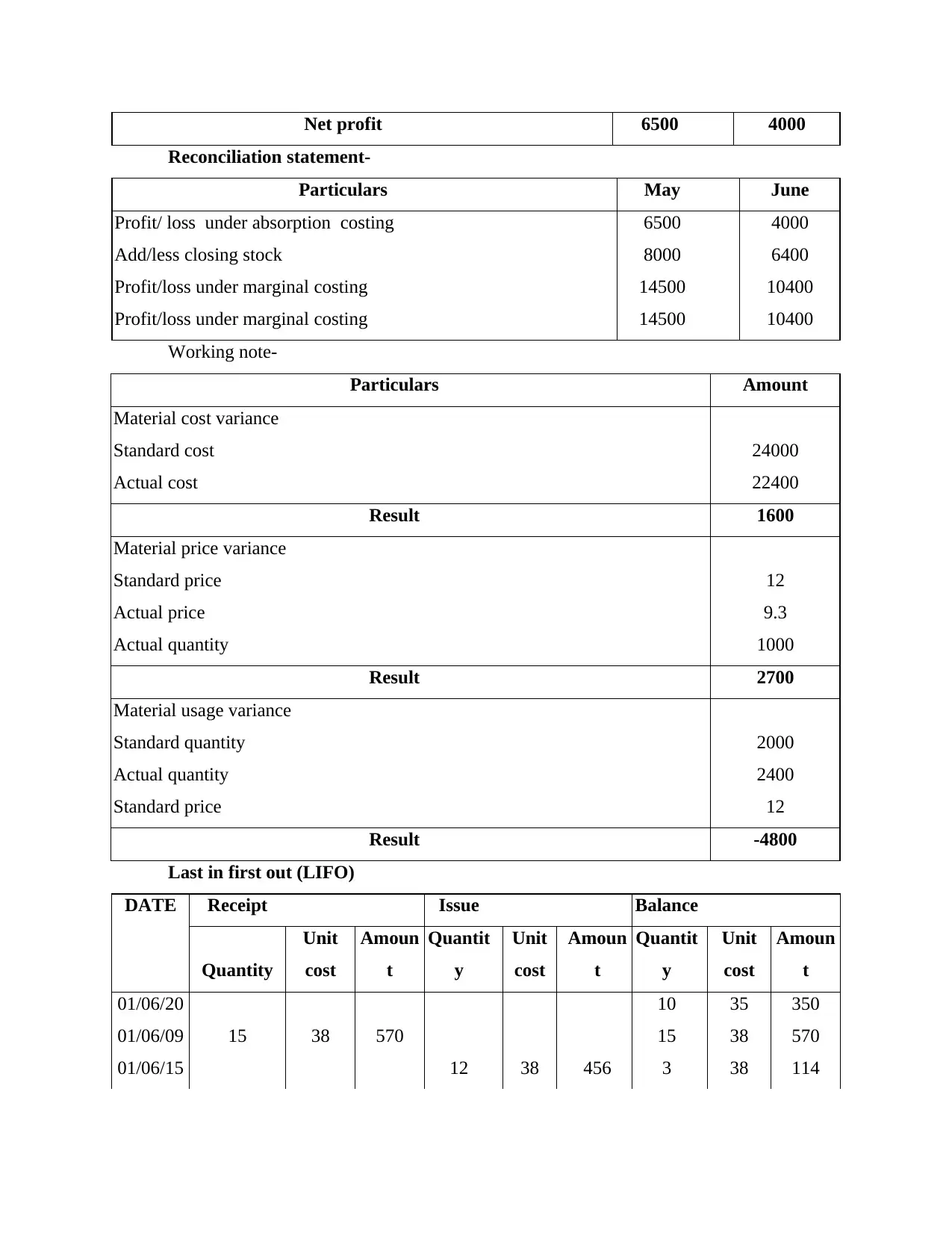

Net profit 6500 4000

Reconciliation statement-

Particulars May June

Profit/ loss under absorption costing 6500 4000

Add/less closing stock 8000 6400

Profit/loss under marginal costing 14500 10400

Profit/loss under marginal costing 14500 10400

Working note-

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

Result 2700

Material usage variance

Standard quantity 2000

Actual quantity 2400

Standard price 12

Result -4800

Last in first out (LIFO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

Reconciliation statement-

Particulars May June

Profit/ loss under absorption costing 6500 4000

Add/less closing stock 8000 6400

Profit/loss under marginal costing 14500 10400

Profit/loss under marginal costing 14500 10400

Working note-

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

Result 2700

Material usage variance

Standard quantity 2000

Actual quantity 2400

Standard price 12

Result -4800

Last in first out (LIFO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

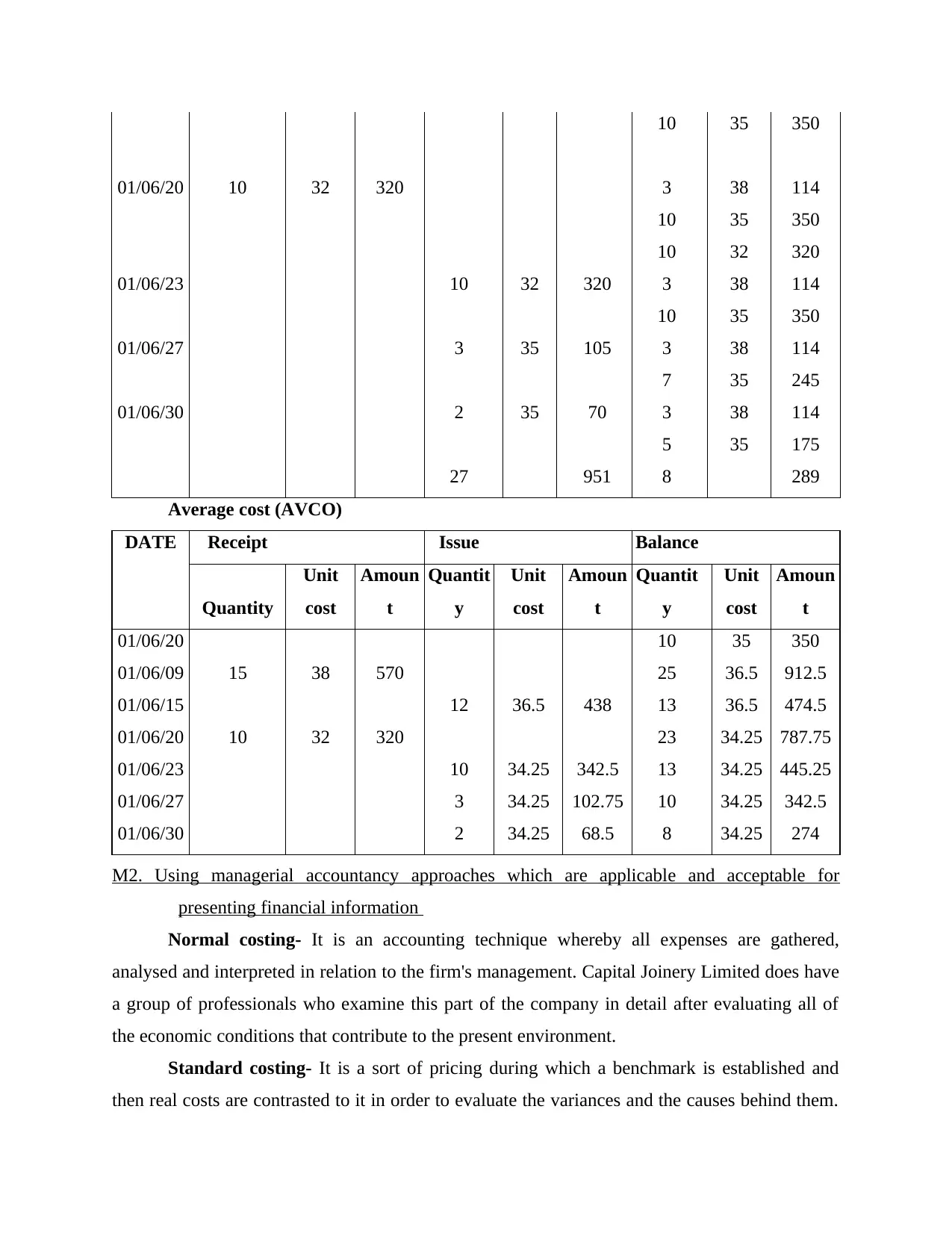

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

27 951 8 289

Average cost (AVCO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 25 36.5 912.5

01/06/15 12 36.5 438 13 36.5 474.5

01/06/20 10 32 320 23 34.25 787.75

01/06/23 10 34.25 342.5 13 34.25 445.25

01/06/27 3 34.25 102.75 10 34.25 342.5

01/06/30 2 34.25 68.5 8 34.25 274

M2. Using managerial accountancy approaches which are applicable and acceptable for

presenting financial information

Normal costing- It is an accounting technique whereby all expenses are gathered,

analysed and interpreted in relation to the firm's management. Capital Joinery Limited does have

a group of professionals who examine this part of the company in detail after evaluating all of

the economic conditions that contribute to the present environment.

Standard costing- It is a sort of pricing during which a benchmark is established and

then real costs are contrasted to it in order to evaluate the variances and the causes behind them.

01/06/20 10 32 320 3 38 114

10 35 350

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

27 951 8 289

Average cost (AVCO)

DATE Receipt Issue Balance

Quantity

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

Quantit

y

Unit

cost

Amoun

t

01/06/20 10 35 350

01/06/09 15 38 570 25 36.5 912.5

01/06/15 12 36.5 438 13 36.5 474.5

01/06/20 10 32 320 23 34.25 787.75

01/06/23 10 34.25 342.5 13 34.25 445.25

01/06/27 3 34.25 102.75 10 34.25 342.5

01/06/30 2 34.25 68.5 8 34.25 274

M2. Using managerial accountancy approaches which are applicable and acceptable for

presenting financial information

Normal costing- It is an accounting technique whereby all expenses are gathered,

analysed and interpreted in relation to the firm's management. Capital Joinery Limited does have

a group of professionals who examine this part of the company in detail after evaluating all of

the economic conditions that contribute to the present environment.

Standard costing- It is a sort of pricing during which a benchmark is established and

then real costs are contrasted to it in order to evaluate the variances and the causes behind them.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.