Management Accounting Concepts and Techniques in Decision Making

VerifiedAdded on 2023/01/09

|14

|2891

|29

AI Summary

This document discusses the benefits of adopting a management accounting system, provides income statements for different costing methods, explores various planning tools and their advantages and disadvantages, and compares organizations based on their use of management accounting to respond to financial issues.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting Concepts

and Techniques in

Decision Making

Accounting Concepts

and Techniques in

Decision Making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

TASK 1............................................................................................................................................3

M1. Benefits of adopting management accounting system....................................................3

TASK 2............................................................................................................................................3

P3 Income statements for both the costing methods..............................................................3

M2 Apply a range of management accounting techniques....................................................7

TASK 3............................................................................................................................................8

P4. Different planning tools with its advantages and disadvantages.....................................8

M3 Importance of planning tools for budgeting and forecasting process............................10

TASK 4..........................................................................................................................................11

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues......................................................................................................................11

M4 Respond to financial problems, MA lead to sustainable development..........................13

REFERENCES..............................................................................................................................14

TASK 1............................................................................................................................................3

M1. Benefits of adopting management accounting system....................................................3

TASK 2............................................................................................................................................3

P3 Income statements for both the costing methods..............................................................3

M2 Apply a range of management accounting techniques....................................................7

TASK 3............................................................................................................................................8

P4. Different planning tools with its advantages and disadvantages.....................................8

M3 Importance of planning tools for budgeting and forecasting process............................10

TASK 4..........................................................................................................................................11

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues......................................................................................................................11

M4 Respond to financial problems, MA lead to sustainable development..........................13

REFERENCES..............................................................................................................................14

TASK 1

M1. Benefits of adopting management accounting system

System Benefits

Cost accounting system It method allows managers to analyse the Creams

Ltd biggest branded goods in a way that suits them.

This also allows precise pricing for the goods to be

calculated by providing the right cost information.

Inventory management

system

Through maintaining sufficient stocks, this help

manager can boost the performance and profitability of

Creams Ltd.

Supported by this method, the company has the details

and accurate inventory level understanding.

Job costing system Managers evaluate the performance of a company's

individual jobs.

It provides full billing specifics such as salaries, services

and other running costs which are extended in different

occupations throughout the enterprise.

Price optimisation system It program facilitates the application of the most

favourable sales policy inside the business so as to

preserve a profitable return.

It also allows the correct costs of products to be set so as

to maximize the loyal consumer base.

TASK 2

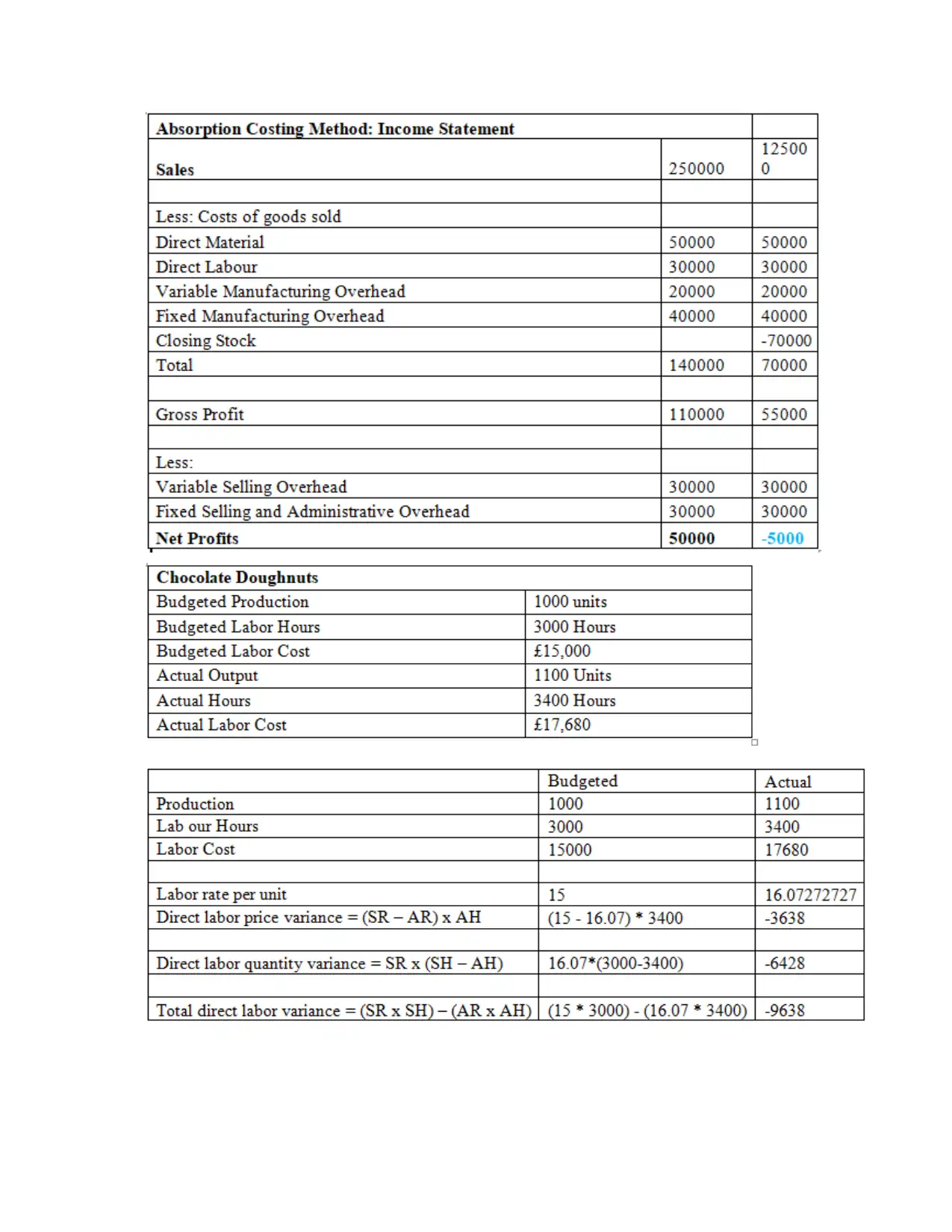

P3 Income statements for both the costing methods

Marginal costs: This was also recognised as indirect expenses were used in the method for

calculating profit only operating costs so that will help to describe break even, minimum safety

process for the business. It can also be described as a cost analysis which recognises overhead

M1. Benefits of adopting management accounting system

System Benefits

Cost accounting system It method allows managers to analyse the Creams

Ltd biggest branded goods in a way that suits them.

This also allows precise pricing for the goods to be

calculated by providing the right cost information.

Inventory management

system

Through maintaining sufficient stocks, this help

manager can boost the performance and profitability of

Creams Ltd.

Supported by this method, the company has the details

and accurate inventory level understanding.

Job costing system Managers evaluate the performance of a company's

individual jobs.

It provides full billing specifics such as salaries, services

and other running costs which are extended in different

occupations throughout the enterprise.

Price optimisation system It program facilitates the application of the most

favourable sales policy inside the business so as to

preserve a profitable return.

It also allows the correct costs of products to be set so as

to maximize the loyal consumer base.

TASK 2

P3 Income statements for both the costing methods

Marginal costs: This was also recognised as indirect expenses were used in the method for

calculating profit only operating costs so that will help to describe break even, minimum safety

process for the business. It can also be described as a cost analysis which recognises overhead

costs as production cost whilst also fixed operational expenses are handled also as cost of the

period.

Absorption Costing: This costing approach involves deduction from the sale of the finished

goods in the main expenditure. The administrators of Creams Limited ensure that their income

cover all expenses incurred in the manufacture of various products (Malmi, 2016). This costing

method recognizes both constant and variable expense of production as expense of the

commodity.

period.

Absorption Costing: This costing approach involves deduction from the sale of the finished

goods in the main expenditure. The administrators of Creams Limited ensure that their income

cover all expenses incurred in the manufacture of various products (Malmi, 2016). This costing

method recognizes both constant and variable expense of production as expense of the

commodity.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

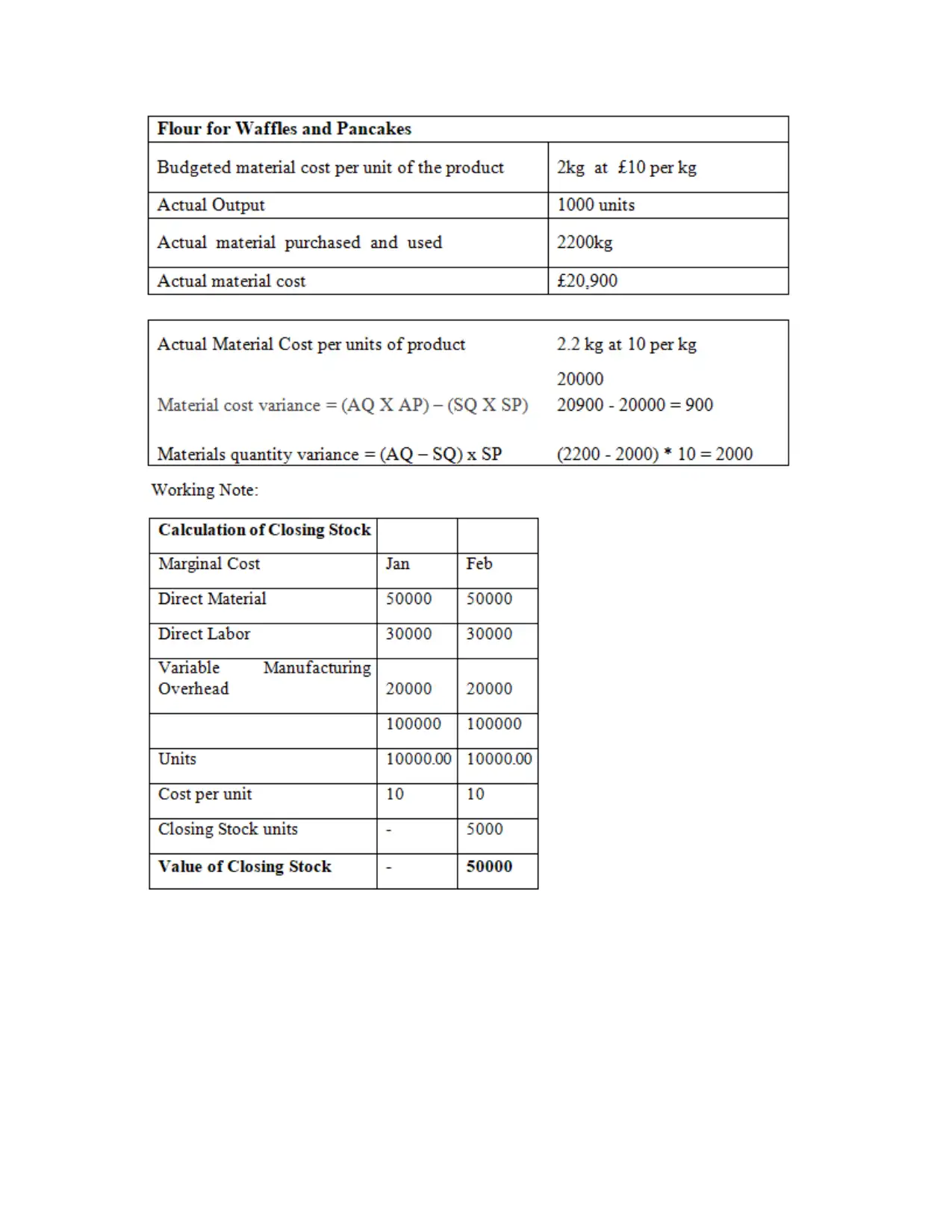

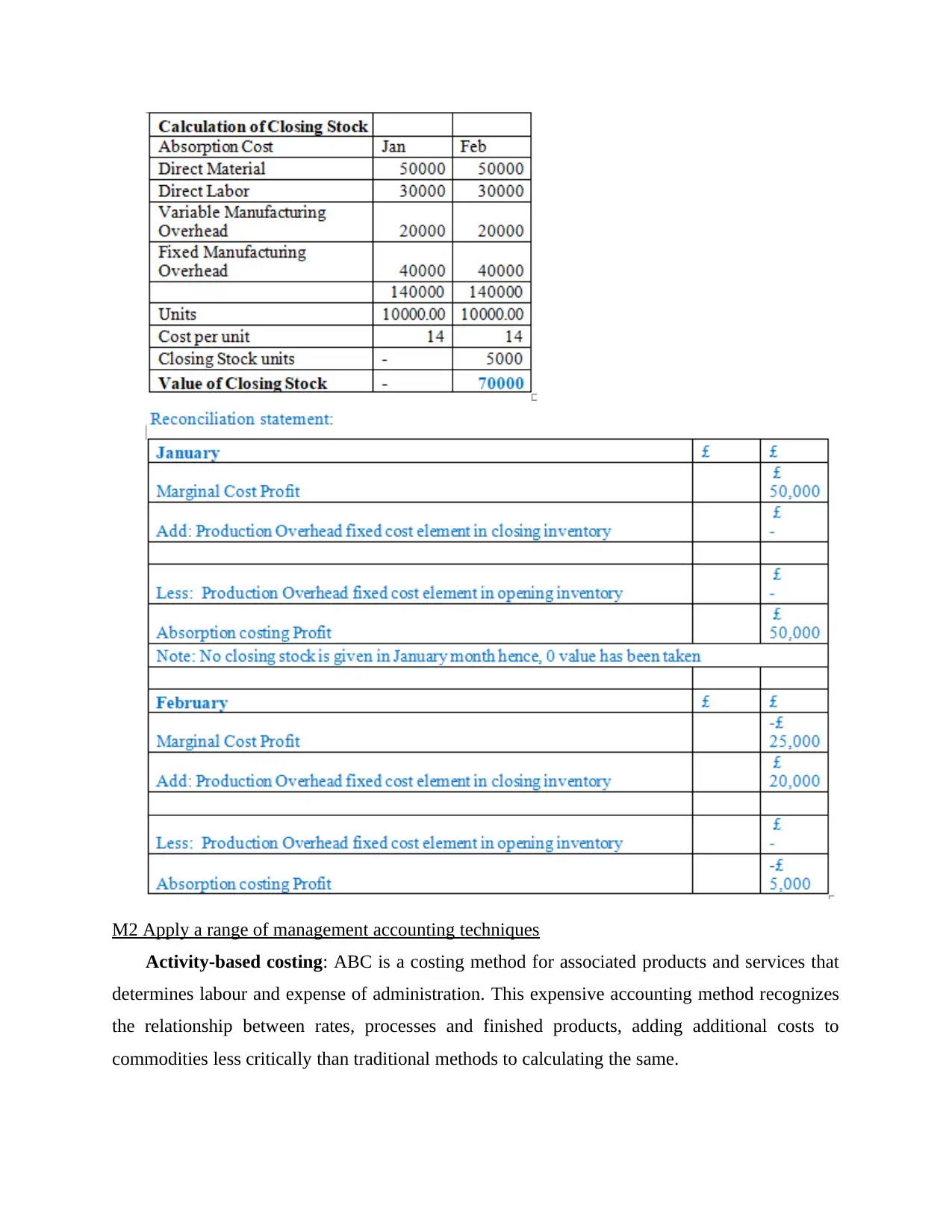

M2 Apply a range of management accounting techniques

Activity-based costing: ABC is a costing method for associated products and services that

determines labour and expense of administration. This expensive accounting method recognizes

the relationship between rates, processes and finished products, adding additional costs to

commodities less critically than traditional methods to calculating the same.

Activity-based costing: ABC is a costing method for associated products and services that

determines labour and expense of administration. This expensive accounting method recognizes

the relationship between rates, processes and finished products, adding additional costs to

commodities less critically than traditional methods to calculating the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost-volume profit analysis: CVP analysis is basically a cost-accounting method that

examines the impact of varying expense and volume levels in similar period on net sales. The

CVP model, which is often commonly accepted as a break-even model, aims to measure the

break-even point under varying rates of sales and cost systems and can be beneficial to

management when creating short-term economic choices.

TASK 3

P4. Different planning tools with its advantages and disadvantages.

Budgetary control is described as the process by which businesses prepare expenditure for

the future term and compare it again with actual performance such that the discrepancy can be

measured. A company's executives will easily detect inconsistencies and suggest suitable

corrections when matching the predictions to the actual figures. This process guarantees that

Creams Ltd management knows, within a time period, the budget constraints of various

operations. Such regulation is critical since unnecessary spending adversely affects company

revenues.

In utilizing the budgetary monitor, Creams Ltd key objective is to assess the difference

between the real and budgeted estimates that is crucial to the organization's progress. This leads

to increased business productivity and production in a timely manner. Budgeting plays a critical

function in preparation and management, because it facilitates the allocation of money that is

allocated for the most productive purpose, thus ensuring business stability (Quattrone, 2016). A

successful budgetary control mechanism facilitates the coordination of the different operations

and guarantees the company's efficient and organized operation. It often incorporates suggestions

from increasing layers of management to plan the program and also promoting divisional

collaboration. In the sense of Creams Ltd a few of the primary planning methods are described

below:

Cost budget: It is a budgetary plan for the forthcoming year, covering specified company

spending. This specifies all of the risks involved with the business activities and accidents. This

is the estimated possible cost that a business will potentially experience in future when carrying

out different operations. It became the most successful approach for adequately managing

development and cash flows of Creams Ltd over various operational and non-operating

expenditures. Here are the strengths and pitfalls of expense budgeting:

examines the impact of varying expense and volume levels in similar period on net sales. The

CVP model, which is often commonly accepted as a break-even model, aims to measure the

break-even point under varying rates of sales and cost systems and can be beneficial to

management when creating short-term economic choices.

TASK 3

P4. Different planning tools with its advantages and disadvantages.

Budgetary control is described as the process by which businesses prepare expenditure for

the future term and compare it again with actual performance such that the discrepancy can be

measured. A company's executives will easily detect inconsistencies and suggest suitable

corrections when matching the predictions to the actual figures. This process guarantees that

Creams Ltd management knows, within a time period, the budget constraints of various

operations. Such regulation is critical since unnecessary spending adversely affects company

revenues.

In utilizing the budgetary monitor, Creams Ltd key objective is to assess the difference

between the real and budgeted estimates that is crucial to the organization's progress. This leads

to increased business productivity and production in a timely manner. Budgeting plays a critical

function in preparation and management, because it facilitates the allocation of money that is

allocated for the most productive purpose, thus ensuring business stability (Quattrone, 2016). A

successful budgetary control mechanism facilitates the coordination of the different operations

and guarantees the company's efficient and organized operation. It often incorporates suggestions

from increasing layers of management to plan the program and also promoting divisional

collaboration. In the sense of Creams Ltd a few of the primary planning methods are described

below:

Cost budget: It is a budgetary plan for the forthcoming year, covering specified company

spending. This specifies all of the risks involved with the business activities and accidents. This

is the estimated possible cost that a business will potentially experience in future when carrying

out different operations. It became the most successful approach for adequately managing

development and cash flows of Creams Ltd over various operational and non-operating

expenditures. Here are the strengths and pitfalls of expense budgeting:

Advantages:

Cost forecast is an easy means for the Creams Ltd budget planner to plan potential

company expenditures. This therefore facilitates the recognition of the disparity between the

budgeted expense and real spending on a single operation. Therefore, this expenditure allows it

possible to determine whether to allow a change to any project in the next year in order to reduce

costs. Moreover, incorporating these strategies by Creams Ltd increases risk understanding,

encourages adequate resource use as well as allows the employee to function in the right manner

to minimize expenses and maximize performance (Otley, 2016).

Disadvantages:

This expenditure plan takes some extra time to determine the total cost of the elements

conducted, thereby delaying the business operations many times. Leadership also demanded very

much from the expenditure and the administration should be liable if such expectations were not

met. The main downside to this strategy is that it relies on the estimates of the prior year owing

to which management chooses at times to reduce operations that require large expenses however

such practices will be competitive in the future based on the circumstances of the sector.

Zero-based budgeting: This process of analysis will clarify new cycles of expenditure for

each new phase. The process starts at a point nil, deciding the requirements and expenditures of

increasing organizational operation (Nitzl, 2016). The main goal of this budgeting strategy is to

reduce extra spending, taking into consideration the situations in which spending will be

reduced. It is necessary to verify any bill to manage Creams Ltd before it is integrated into the

current expenses. Here are a few of Creams Ltd's positives and disadvantages to zero-based

budgeting:

Advantages:

ZBB is a creative financial planning to enable Creams Ltd handle money efficiently, since

it provides fresh projections for increasing operation from 0 and does not take into consideration

any previous details. This budgeting approach promotes greater operational management and

cooperation and allows workers to accept responsibilities (Lachmann, Trapp and Trapp, 2017).

The key benefit of this expenditure plan is the removal of unhealthy activities which further

allow cost-effective solutions to be found and the optimum usage of available resources in order

to achieve the massive profit.

Cost forecast is an easy means for the Creams Ltd budget planner to plan potential

company expenditures. This therefore facilitates the recognition of the disparity between the

budgeted expense and real spending on a single operation. Therefore, this expenditure allows it

possible to determine whether to allow a change to any project in the next year in order to reduce

costs. Moreover, incorporating these strategies by Creams Ltd increases risk understanding,

encourages adequate resource use as well as allows the employee to function in the right manner

to minimize expenses and maximize performance (Otley, 2016).

Disadvantages:

This expenditure plan takes some extra time to determine the total cost of the elements

conducted, thereby delaying the business operations many times. Leadership also demanded very

much from the expenditure and the administration should be liable if such expectations were not

met. The main downside to this strategy is that it relies on the estimates of the prior year owing

to which management chooses at times to reduce operations that require large expenses however

such practices will be competitive in the future based on the circumstances of the sector.

Zero-based budgeting: This process of analysis will clarify new cycles of expenditure for

each new phase. The process starts at a point nil, deciding the requirements and expenditures of

increasing organizational operation (Nitzl, 2016). The main goal of this budgeting strategy is to

reduce extra spending, taking into consideration the situations in which spending will be

reduced. It is necessary to verify any bill to manage Creams Ltd before it is integrated into the

current expenses. Here are a few of Creams Ltd's positives and disadvantages to zero-based

budgeting:

Advantages:

ZBB is a creative financial planning to enable Creams Ltd handle money efficiently, since

it provides fresh projections for increasing operation from 0 and does not take into consideration

any previous details. This budgeting approach promotes greater operational management and

cooperation and allows workers to accept responsibilities (Lachmann, Trapp and Trapp, 2017).

The key benefit of this expenditure plan is the removal of unhealthy activities which further

allow cost-effective solutions to be found and the optimum usage of available resources in order

to achieve the massive profit.

Disadvantages:

This budgeting phase is highly time-consuming for creams Ltd but is far more

complicated to tolerate any adjustment to the budget for each year. Therefore assessment of all

Creams Ltd products is becoming a daunting job for boss again and again. In planning ZBB

budgets Creams Ltd requires a trained and skilled representative leader that increase the overall

employees’ turnover.

Capital budgeting: It is described as the manner wherein the firm determines what

fixed-resource investments it will allow and reduce (Weetman, 2019). Capital budgeting has

been used to create a practical framework to determine the potential investments of fixed assets

and to establish a strategic perspective. Through handling Creams LTd it helps in evaluating

future big deals or ventures.

Advantages:

The key advantage of this strategy is to support Creams Ltd in determining the most

desirable return on expenditure within a defined time period. This added assistance to make wise

investment choices that will continue to develop resources which could be used to fund the

activity of the business according to the structure needed. It helps internal team to take rational

financial choices, keeping the potential options present on the markets into account.

Disadvantage

The key downside of this expenditure plan is that it is focused on speculation and does

not show any investments decision-related risks so more time contributes to a greater disaster of

Creams Ltd money. Bad investment appraisal forecasts may have an influence on Creams Ltd's

long-term survival and several times have an effect on actual market performance because

managers are waiting to make the correct decision (Wagenhofer, 2016).

M3 Importance of planning tools for budgeting and forecasting process

The forecasting strategy mentioned above helps business managers to provide an

knowledge of the organization's costs over different operational operations. As a consequence, it

also facilitates the creation of successful strategies for the duration because administrators may

effectively assign funds to the tasks that they feel can bring in better returns in the future.

Therefore, various preparation methods provide a similar potential of managing funds correctly

or allowing good use of existing capital in order to better discuss annual budgets. Such methods

also support useful modelling of required resources use in a way that allows the expected results

This budgeting phase is highly time-consuming for creams Ltd but is far more

complicated to tolerate any adjustment to the budget for each year. Therefore assessment of all

Creams Ltd products is becoming a daunting job for boss again and again. In planning ZBB

budgets Creams Ltd requires a trained and skilled representative leader that increase the overall

employees’ turnover.

Capital budgeting: It is described as the manner wherein the firm determines what

fixed-resource investments it will allow and reduce (Weetman, 2019). Capital budgeting has

been used to create a practical framework to determine the potential investments of fixed assets

and to establish a strategic perspective. Through handling Creams LTd it helps in evaluating

future big deals or ventures.

Advantages:

The key advantage of this strategy is to support Creams Ltd in determining the most

desirable return on expenditure within a defined time period. This added assistance to make wise

investment choices that will continue to develop resources which could be used to fund the

activity of the business according to the structure needed. It helps internal team to take rational

financial choices, keeping the potential options present on the markets into account.

Disadvantage

The key downside of this expenditure plan is that it is focused on speculation and does

not show any investments decision-related risks so more time contributes to a greater disaster of

Creams Ltd money. Bad investment appraisal forecasts may have an influence on Creams Ltd's

long-term survival and several times have an effect on actual market performance because

managers are waiting to make the correct decision (Wagenhofer, 2016).

M3 Importance of planning tools for budgeting and forecasting process

The forecasting strategy mentioned above helps business managers to provide an

knowledge of the organization's costs over different operational operations. As a consequence, it

also facilitates the creation of successful strategies for the duration because administrators may

effectively assign funds to the tasks that they feel can bring in better returns in the future.

Therefore, various preparation methods provide a similar potential of managing funds correctly

or allowing good use of existing capital in order to better discuss annual budgets. Such methods

also support useful modelling of required resources use in a way that allows the expected results

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

to be accomplished in real time. Cost budget as well as ZBB is a creative financial forecasting

resource that facilitates improved collaboration and cooperation between organisations and

fosters workplace accountability.

TASK 4

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues

Companies are facing numerous growing financial challenges and issues overall economy

owing to a dynamic global climate. There are many reasons why these situations happen inside

the company, like missed payments from customers, increased debt, unclearance of inventory,

etc. Some of the huge problems that big companies like Tesla as well as General Motors are

facing while functioning is discussed below:

Basis Tesla General Motors

Problems and tool

used to detect.

Tesla confronts the main financial

problem linked to cash flow transfer.

Thus managers use KPI to identify

the cause for the inadequate cash

flow across multiple activities.

Reviews are compared to their

forecasts with the aid of this method

result stated by Tesla, implying the

expectations of the business are not at

least relevant to its performance, but

instead to its own missed or

surpassed projection in the past. The

performances of Tesla are tailored to

their own expectations.

The organization faces problems

relating to inadequate stock

utilization due to which

profitability is rising. General

Motors would then take into

account revenue innovation and

market role as the important

indicators of achievement in the

balance sheet’s economic

measures department. Such

initiatives will serve to determine

how well the business proceeds

to achieve higher profits, as its

primary goal.

Implementation of

MAS

By incorporating cost accounting

method administrators can effectively

monitor and calculate the overall

costs involved with different

To address the above-mentioned

financial problem manager use to

conduct stock accounting

program such that correct stock

resource that facilitates improved collaboration and cooperation between organisations and

fosters workplace accountability.

TASK 4

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues

Companies are facing numerous growing financial challenges and issues overall economy

owing to a dynamic global climate. There are many reasons why these situations happen inside

the company, like missed payments from customers, increased debt, unclearance of inventory,

etc. Some of the huge problems that big companies like Tesla as well as General Motors are

facing while functioning is discussed below:

Basis Tesla General Motors

Problems and tool

used to detect.

Tesla confronts the main financial

problem linked to cash flow transfer.

Thus managers use KPI to identify

the cause for the inadequate cash

flow across multiple activities.

Reviews are compared to their

forecasts with the aid of this method

result stated by Tesla, implying the

expectations of the business are not at

least relevant to its performance, but

instead to its own missed or

surpassed projection in the past. The

performances of Tesla are tailored to

their own expectations.

The organization faces problems

relating to inadequate stock

utilization due to which

profitability is rising. General

Motors would then take into

account revenue innovation and

market role as the important

indicators of achievement in the

balance sheet’s economic

measures department. Such

initiatives will serve to determine

how well the business proceeds

to achieve higher profits, as its

primary goal.

Implementation of

MAS

By incorporating cost accounting

method administrators can effectively

monitor and calculate the overall

costs involved with different

To address the above-mentioned

financial problem manager use to

conduct stock accounting

program such that correct stock

operations and properly distribute

cash capital to address the above-

mentioned issue (Tucker and

Schaltegger, 2016).

records can be preserved at each

point of manufacturing stage

because the product accessible is

completely managed (Hall,

2016).

MA Technique Using the Financial

Governance respective firm can make

it is possible to effectively document

total inflows and outflows of cash

and also to correlate with the original

estimate to determine overall

profitability.

By utilizing the Financial

Governance Management

method, it is simple to figure out

the least amount of efficiency

intervention and avoid this

process that contributes to these

big financial problems.

From the above discussion it can be determined that Creams ltd can make use of various

tools and techniques of Management accounting to determine the financial issues and easily

removed the reasons. Some of these are discussed underneath:

Benchmarking: It is the process by which the performance of organizations is calculated

at a certain level. With this method, Creams Ltd would use it to assess the causes for poor stock

use and reduced performance. Furthermore, this MA resource planner contrasts stock usage with

other competition companies by establishing a target standard.

KPI's Metrics: This seems to be a valuable method that is used throughout a period to

quantify the company's current achievement. In utilizing this method, the Creams Ltd utilizes

various forms of indicators to assess how effectively they achieve their expectations and targets.

By enforcing this tool manager of Creams Ltd are easily able to detect the major issue in

working capital by setting metrics at various operational activities.

Financial governance: This is how the organization conducts accounts documents and

compiles them in accurate statement. The company does that to include useful information on the

company's monetary situation. The financial problem may be resolved in a certain manner by

introducing this task manager of Creams Ltd can explicitly reflects the rise in total efficiency.

Ratio analysis: Within Creams Ltd, ratio analysis may be used to determine the financial

problem for accounting year. That is because correct measurement of various rations facilitates

cash capital to address the above-

mentioned issue (Tucker and

Schaltegger, 2016).

records can be preserved at each

point of manufacturing stage

because the product accessible is

completely managed (Hall,

2016).

MA Technique Using the Financial

Governance respective firm can make

it is possible to effectively document

total inflows and outflows of cash

and also to correlate with the original

estimate to determine overall

profitability.

By utilizing the Financial

Governance Management

method, it is simple to figure out

the least amount of efficiency

intervention and avoid this

process that contributes to these

big financial problems.

From the above discussion it can be determined that Creams ltd can make use of various

tools and techniques of Management accounting to determine the financial issues and easily

removed the reasons. Some of these are discussed underneath:

Benchmarking: It is the process by which the performance of organizations is calculated

at a certain level. With this method, Creams Ltd would use it to assess the causes for poor stock

use and reduced performance. Furthermore, this MA resource planner contrasts stock usage with

other competition companies by establishing a target standard.

KPI's Metrics: This seems to be a valuable method that is used throughout a period to

quantify the company's current achievement. In utilizing this method, the Creams Ltd utilizes

various forms of indicators to assess how effectively they achieve their expectations and targets.

By enforcing this tool manager of Creams Ltd are easily able to detect the major issue in

working capital by setting metrics at various operational activities.

Financial governance: This is how the organization conducts accounts documents and

compiles them in accurate statement. The company does that to include useful information on the

company's monetary situation. The financial problem may be resolved in a certain manner by

introducing this task manager of Creams Ltd can explicitly reflects the rise in total efficiency.

Ratio analysis: Within Creams Ltd, ratio analysis may be used to determine the financial

problem for accounting year. That is because correct measurement of various rations facilitates

determining the overall adjustments that occur in specific market aspects. As opposed to the

previous year, like net income ratio tends to include the percentage shift in profit figures. Then

any drop in the ratio helps enterprise to identify the cause for this drop and careful consideration

of such reasons encourages management to take drastic action to minimize the financial problem.

Cash budget: Creams ltd should use this kind of strategy to tackle the current financial

issue because it helps to manage the necessary cash capital efficiently and to achieve the precise

amount within the target period. Moreover, this proposal further encourages the implementation

of strategies for the usage of cash only for operations that produce immense profits and the

creation of new ones to minimize the financial problem.

M4 Respond to financial problems, MA lead to sustainable development

Cream Ltd internal management team use benchmarking for inventory poor management,

will help encourage workers to increase sales and efficiency, obtain additional incentives and

enforce financial regulatory laws to work effectively and track illegal offences and can often

utilize KPI approaches for cash flow problems, in which they must raise funds within a specified

period to reinstate capital. In comparison, the implementation of MA structures was also

analysed for a significantly shortened timeframe to accomplish economic growth. In addition, the

issues mentioned here may be addressed through the cost management and accounting method.

The Creams ltd seeks numerous approaches, such as resource management, organized schedules

etc. It is important for them to analyse differences within solving problems each of these goals.

previous year, like net income ratio tends to include the percentage shift in profit figures. Then

any drop in the ratio helps enterprise to identify the cause for this drop and careful consideration

of such reasons encourages management to take drastic action to minimize the financial problem.

Cash budget: Creams ltd should use this kind of strategy to tackle the current financial

issue because it helps to manage the necessary cash capital efficiently and to achieve the precise

amount within the target period. Moreover, this proposal further encourages the implementation

of strategies for the usage of cash only for operations that produce immense profits and the

creation of new ones to minimize the financial problem.

M4 Respond to financial problems, MA lead to sustainable development

Cream Ltd internal management team use benchmarking for inventory poor management,

will help encourage workers to increase sales and efficiency, obtain additional incentives and

enforce financial regulatory laws to work effectively and track illegal offences and can often

utilize KPI approaches for cash flow problems, in which they must raise funds within a specified

period to reinstate capital. In comparison, the implementation of MA structures was also

analysed for a significantly shortened timeframe to accomplish economic growth. In addition, the

issues mentioned here may be addressed through the cost management and accounting method.

The Creams ltd seeks numerous approaches, such as resource management, organized schedules

etc. It is important for them to analyse differences within solving problems each of these goals.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research. 31. pp.31-44.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Ricks, M., 2016. The money problem: rethinking financial regulation. University of Chicago

Press.

Šiška, L., 2016. The contingency factors affecting management accounting in Czech

companies. Acta Universitatis Agriculturae et Silviculturae Mendelianae

Brunensis, 64(4), pp.1383-1392.

van Helden, J. and Uddin, S., 2016. Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting. 41. pp.34-62.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research, 31, pp.112-117.

Books and Journals

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research. 31. pp.31-44.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Nitzl, C., 2016. The use of partial least squares structural equation modelling (PLS-SEM) in

management accounting research: Directions for future theory development. Journal of

Accounting Literature. 37. pp.19-35.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Ricks, M., 2016. The money problem: rethinking financial regulation. University of Chicago

Press.

Šiška, L., 2016. The contingency factors affecting management accounting in Czech

companies. Acta Universitatis Agriculturae et Silviculturae Mendelianae

Brunensis, 64(4), pp.1383-1392.

van Helden, J. and Uddin, S., 2016. Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting. 41. pp.34-62.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in management

accounting. Management Accounting Research, 31, pp.112-117.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.