Management accounting concepts and techniques in decision making

VerifiedAdded on 2023/01/12

|13

|3124

|25

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

Management Accounting and different types of management accounting systems...................1

Different methods used on the management accounting reporting.............................................2

Evaluation of the benefits and application of the management accounting techniques..............3

Integration of the management accounting systems with the reporting......................................4

LO2..................................................................................................................................................4

Calculating costs using different cost accounting techniques.....................................................4

LO3..................................................................................................................................................7

Application of different planning tools with their advantages and disadvantages......................7

LO4..................................................................................................................................................9

Organisations adapting management accounting systems for resolving the financial problems.9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

Management Accounting and different types of management accounting systems...................1

Different methods used on the management accounting reporting.............................................2

Evaluation of the benefits and application of the management accounting techniques..............3

Integration of the management accounting systems with the reporting......................................4

LO2..................................................................................................................................................4

Calculating costs using different cost accounting techniques.....................................................4

LO3..................................................................................................................................................7

Application of different planning tools with their advantages and disadvantages......................7

LO4..................................................................................................................................................9

Organisations adapting management accounting systems for resolving the financial problems.9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting refers to the process involving gathering, analysing, interpreting

and preparing the financial records and reports. Management accounting involves the preparation

of financial reports that provide the management with important decision making. This helps the

management in improving and enhancing the productivity of the organisation.MA aims at

achieving the goals and objectives of the organisation using various management accounting

tools and techniques. Present report is based over PQR Ltd that is a manufacturing concern

dealing in the production of furniture. Report will provide about the concepts and methods used

by management for effective decision making.

LO1

Management Accounting and different types of management accounting systems.

Management accounting refers to presentation of the financial information for the

formulation of policies that are required to be adapted by management and for assisting them in

meeting their day-to-day operations and activities. Management accounting involves function

such as planning, collecting, organising, directing & controlling.

Management accounting systems.

Management accounting systems are the internal management system used by

organisation.

Inventory management systems.

Inventory management refers to the system that involves keeping record of each and

inventory of the organisation. Inventory management is the combination of software and the

hardware for effectively managing the inventory of the organisation. This helps the management

in making informed decisions related with the inventory (Hopper and Bui, 2016). Different

inventory management methods include.

LIFO – In this method inventory that comes in last is sold out at first. The goods are sold

at the prices at which they are purchased in by entity.

FIFO –This refers to the method in which goods that are purchased first are sold first.

This helps in learning their older stocks of inventory.

WAC – In this approach the prices of the inventory are calculated on the weighted

average basis on all the goods purchased first and last at different prices.

1

Management accounting refers to the process involving gathering, analysing, interpreting

and preparing the financial records and reports. Management accounting involves the preparation

of financial reports that provide the management with important decision making. This helps the

management in improving and enhancing the productivity of the organisation.MA aims at

achieving the goals and objectives of the organisation using various management accounting

tools and techniques. Present report is based over PQR Ltd that is a manufacturing concern

dealing in the production of furniture. Report will provide about the concepts and methods used

by management for effective decision making.

LO1

Management Accounting and different types of management accounting systems.

Management accounting refers to presentation of the financial information for the

formulation of policies that are required to be adapted by management and for assisting them in

meeting their day-to-day operations and activities. Management accounting involves function

such as planning, collecting, organising, directing & controlling.

Management accounting systems.

Management accounting systems are the internal management system used by

organisation.

Inventory management systems.

Inventory management refers to the system that involves keeping record of each and

inventory of the organisation. Inventory management is the combination of software and the

hardware for effectively managing the inventory of the organisation. This helps the management

in making informed decisions related with the inventory (Hopper and Bui, 2016). Different

inventory management methods include.

LIFO – In this method inventory that comes in last is sold out at first. The goods are sold

at the prices at which they are purchased in by entity.

FIFO –This refers to the method in which goods that are purchased first are sold first.

This helps in learning their older stocks of inventory.

WAC – In this approach the prices of the inventory are calculated on the weighted

average basis on all the goods purchased first and last at different prices.

1

Cost Accounting System

This a method used for recording all the cost information of the business. it involves

accounting for all the costs such as raw materials, labour and production overheads. This helps

the management in controlling its costs and expenditures related with the business and in taking

effective decision. Job costing is used by organisation for making decision related with cost of

manufacturing and profit margins.

Direct Costing – This system accounts only variable costs associated with the production of the

units and not the fixed cost.

Standard Costing – This costing methods involves carrying out the production as per the set

standards and measuring variances ate the year with the actual output for taking the corrective

measures.

Job Costing

It could be defines as the for recording of costs related to the manufacturing of job, instead

of the process. This helps in identifying the costs related with the specific jobs carried out for

manufacturing particular product. Costing method is used by the companies involved in

manufacturing or construction that involve more than one process.

Different methods used on the management accounting reporting.

Management accounting reporting contains all the information related with the business

operations.

Budgeting Report

Budget report are the report prepared by the organisation for keeping its costs and

expenditures under control and preventing overspending. Budget reports are one of the most

important reports that are prepared by the management after analysing the records of previous

years (Weetman, 2019). For the preparation of current budget information of previous budgets

are used and other adjustments related are made related with inflation and market conditions.

Performance Report

Performance report is prepared for evaluating the performance of the business operations.

Performance report contains all the information related with the effectiveness of management in

achieving the targeted objectives. This is essential for analysing the strengths and weaknesses of

the company in achieving its benchmarks. This also helps the management in taking effective

improvement steps for increasing the efficiency and productivity.

2

This a method used for recording all the cost information of the business. it involves

accounting for all the costs such as raw materials, labour and production overheads. This helps

the management in controlling its costs and expenditures related with the business and in taking

effective decision. Job costing is used by organisation for making decision related with cost of

manufacturing and profit margins.

Direct Costing – This system accounts only variable costs associated with the production of the

units and not the fixed cost.

Standard Costing – This costing methods involves carrying out the production as per the set

standards and measuring variances ate the year with the actual output for taking the corrective

measures.

Job Costing

It could be defines as the for recording of costs related to the manufacturing of job, instead

of the process. This helps in identifying the costs related with the specific jobs carried out for

manufacturing particular product. Costing method is used by the companies involved in

manufacturing or construction that involve more than one process.

Different methods used on the management accounting reporting.

Management accounting reporting contains all the information related with the business

operations.

Budgeting Report

Budget report are the report prepared by the organisation for keeping its costs and

expenditures under control and preventing overspending. Budget reports are one of the most

important reports that are prepared by the management after analysing the records of previous

years (Weetman, 2019). For the preparation of current budget information of previous budgets

are used and other adjustments related are made related with inflation and market conditions.

Performance Report

Performance report is prepared for evaluating the performance of the business operations.

Performance report contains all the information related with the effectiveness of management in

achieving the targeted objectives. This is essential for analysing the strengths and weaknesses of

the company in achieving its benchmarks. This also helps the management in taking effective

improvement steps for increasing the efficiency and productivity.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

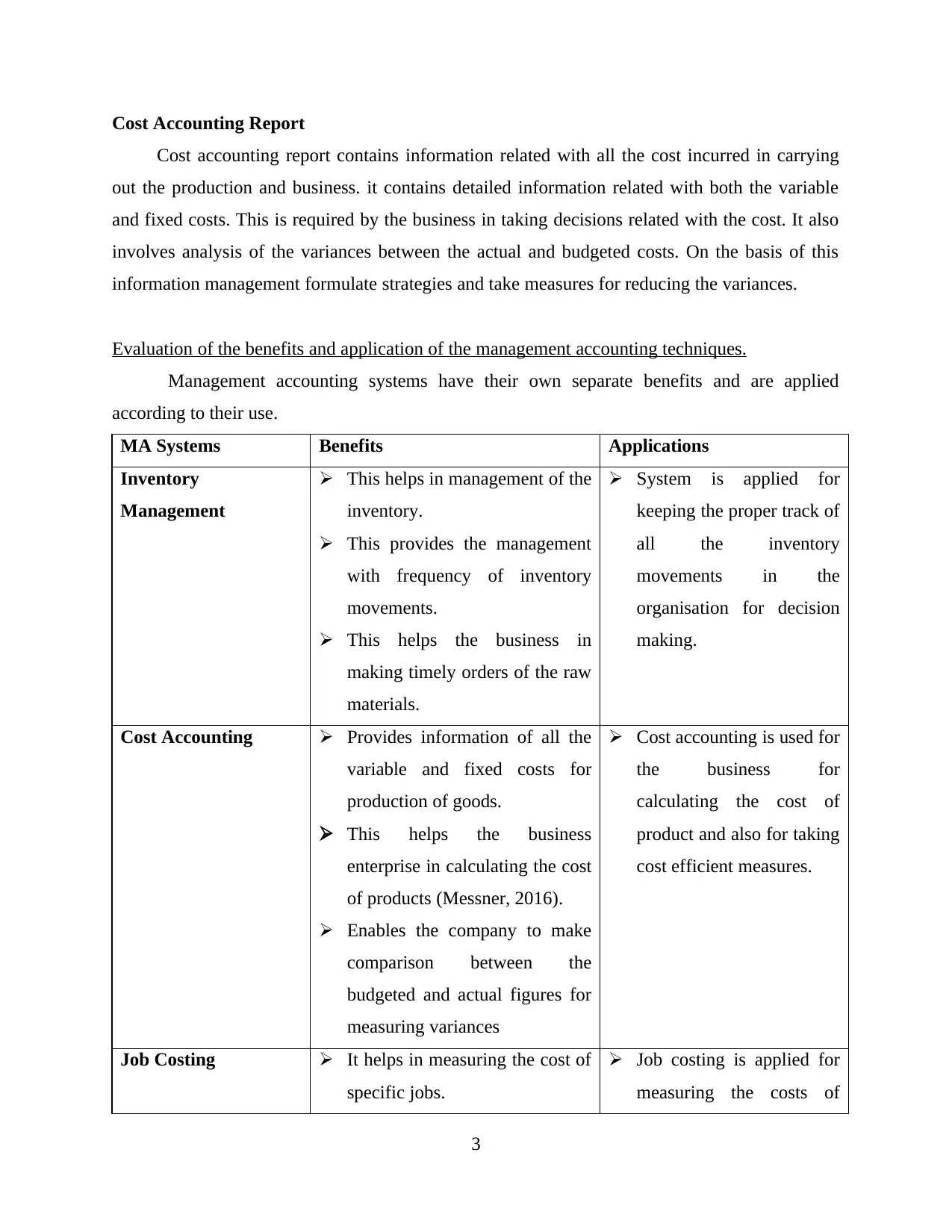

Cost Accounting Report

Cost accounting report contains information related with all the cost incurred in carrying

out the production and business. it contains detailed information related with both the variable

and fixed costs. This is required by the business in taking decisions related with the cost. It also

involves analysis of the variances between the actual and budgeted costs. On the basis of this

information management formulate strategies and take measures for reducing the variances.

Evaluation of the benefits and application of the management accounting techniques.

Management accounting systems have their own separate benefits and are applied

according to their use.

MA Systems Benefits Applications

Inventory

Management

This helps in management of the

inventory.

This provides the management

with frequency of inventory

movements.

This helps the business in

making timely orders of the raw

materials.

System is applied for

keeping the proper track of

all the inventory

movements in the

organisation for decision

making.

Cost Accounting Provides information of all the

variable and fixed costs for

production of goods.

This helps the business

enterprise in calculating the cost

of products (Messner, 2016).

Enables the company to make

comparison between the

budgeted and actual figures for

measuring variances

Cost accounting is used for

the business for

calculating the cost of

product and also for taking

cost efficient measures.

Job Costing It helps in measuring the cost of

specific jobs.

Job costing is applied for

measuring the costs of

3

Cost accounting report contains information related with all the cost incurred in carrying

out the production and business. it contains detailed information related with both the variable

and fixed costs. This is required by the business in taking decisions related with the cost. It also

involves analysis of the variances between the actual and budgeted costs. On the basis of this

information management formulate strategies and take measures for reducing the variances.

Evaluation of the benefits and application of the management accounting techniques.

Management accounting systems have their own separate benefits and are applied

according to their use.

MA Systems Benefits Applications

Inventory

Management

This helps in management of the

inventory.

This provides the management

with frequency of inventory

movements.

This helps the business in

making timely orders of the raw

materials.

System is applied for

keeping the proper track of

all the inventory

movements in the

organisation for decision

making.

Cost Accounting Provides information of all the

variable and fixed costs for

production of goods.

This helps the business

enterprise in calculating the cost

of products (Messner, 2016).

Enables the company to make

comparison between the

budgeted and actual figures for

measuring variances

Cost accounting is used for

the business for

calculating the cost of

product and also for taking

cost efficient measures.

Job Costing It helps in measuring the cost of

specific jobs.

Job costing is applied for

measuring the costs of

3

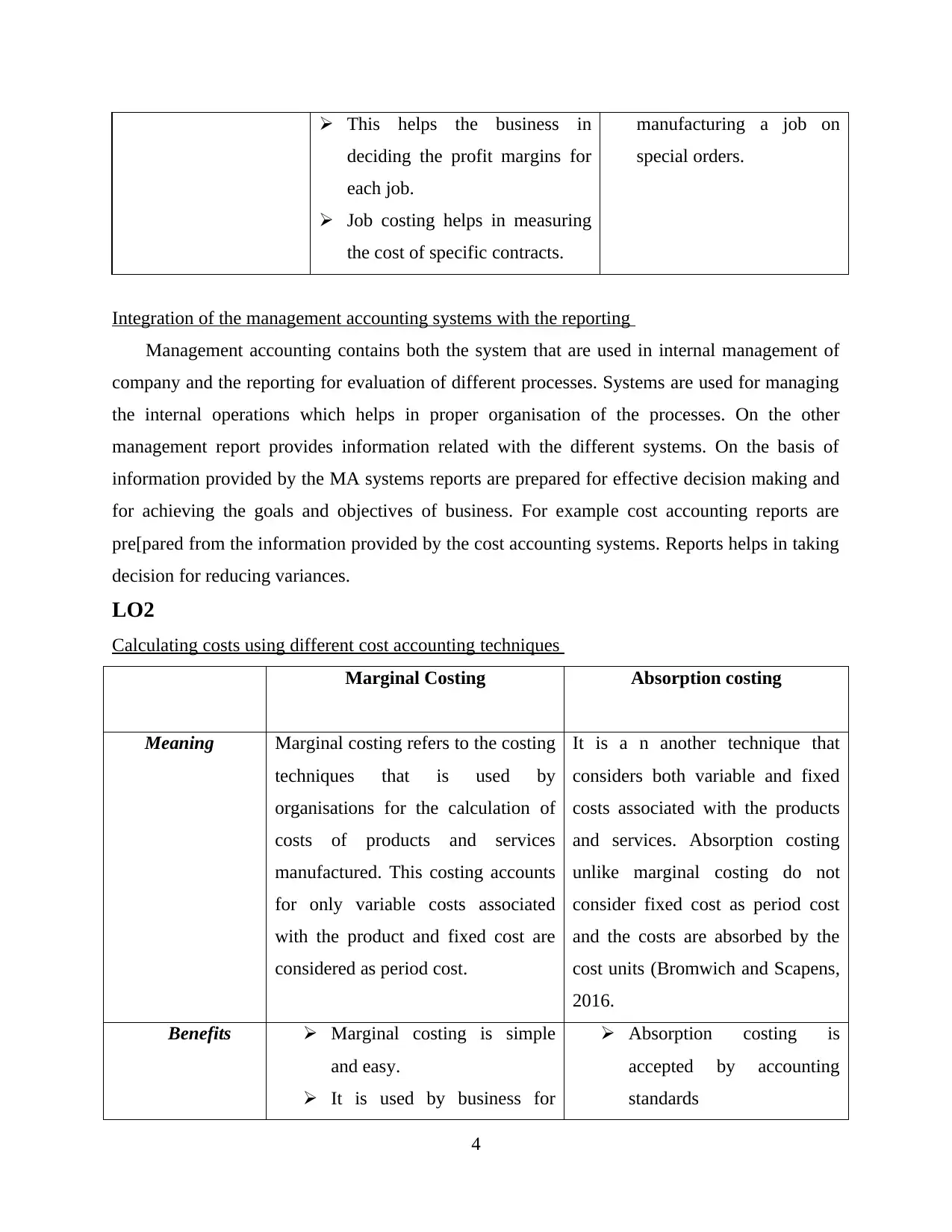

This helps the business in

deciding the profit margins for

each job.

Job costing helps in measuring

the cost of specific contracts.

manufacturing a job on

special orders.

Integration of the management accounting systems with the reporting

Management accounting contains both the system that are used in internal management of

company and the reporting for evaluation of different processes. Systems are used for managing

the internal operations which helps in proper organisation of the processes. On the other

management report provides information related with the different systems. On the basis of

information provided by the MA systems reports are prepared for effective decision making and

for achieving the goals and objectives of business. For example cost accounting reports are

pre[pared from the information provided by the cost accounting systems. Reports helps in taking

decision for reducing variances.

LO2

Calculating costs using different cost accounting techniques

Marginal Costing Absorption costing

Meaning Marginal costing refers to the costing

techniques that is used by

organisations for the calculation of

costs of products and services

manufactured. This costing accounts

for only variable costs associated

with the product and fixed cost are

considered as period cost.

It is a n another technique that

considers both variable and fixed

costs associated with the products

and services. Absorption costing

unlike marginal costing do not

consider fixed cost as period cost

and the costs are absorbed by the

cost units (Bromwich and Scapens,

2016.

Benefits Marginal costing is simple

and easy.

It is used by business for

Absorption costing is

accepted by accounting

standards

4

deciding the profit margins for

each job.

Job costing helps in measuring

the cost of specific contracts.

manufacturing a job on

special orders.

Integration of the management accounting systems with the reporting

Management accounting contains both the system that are used in internal management of

company and the reporting for evaluation of different processes. Systems are used for managing

the internal operations which helps in proper organisation of the processes. On the other

management report provides information related with the different systems. On the basis of

information provided by the MA systems reports are prepared for effective decision making and

for achieving the goals and objectives of business. For example cost accounting reports are

pre[pared from the information provided by the cost accounting systems. Reports helps in taking

decision for reducing variances.

LO2

Calculating costs using different cost accounting techniques

Marginal Costing Absorption costing

Meaning Marginal costing refers to the costing

techniques that is used by

organisations for the calculation of

costs of products and services

manufactured. This costing accounts

for only variable costs associated

with the product and fixed cost are

considered as period cost.

It is a n another technique that

considers both variable and fixed

costs associated with the products

and services. Absorption costing

unlike marginal costing do not

consider fixed cost as period cost

and the costs are absorbed by the

cost units (Bromwich and Scapens,

2016.

Benefits Marginal costing is simple

and easy.

It is used by business for

Absorption costing is

accepted by accounting

standards

4

decision making.

No calculation of under or

over absorption of overhead

cost

It helps in identifying the

overhead costs separately.

Method covers both fixed

and variable costs.

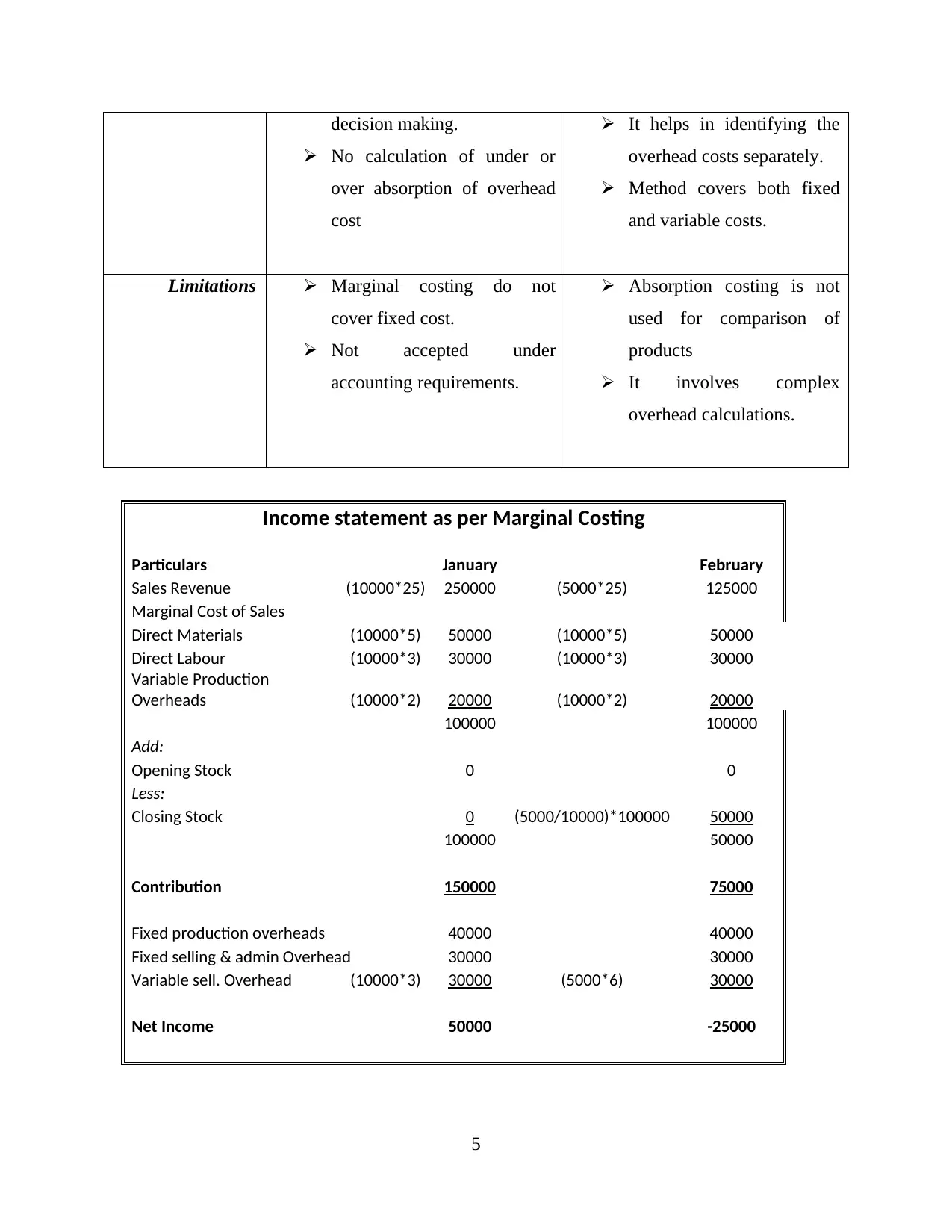

Limitations Marginal costing do not

cover fixed cost.

Not accepted under

accounting requirements.

Absorption costing is not

used for comparison of

products

It involves complex

overhead calculations.

Income statement as per Marginal Costing

Particulars January February

Sales Revenue (10000*25) 250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production

Overheads (10000*2) 20000 (10000*2) 20000

100000 100000

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5000/10000)*100000 50000

100000 50000

Contribution 150000 75000

Fixed production overheads 40000 40000

Fixed selling & admin Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000 -25000

5

No calculation of under or

over absorption of overhead

cost

It helps in identifying the

overhead costs separately.

Method covers both fixed

and variable costs.

Limitations Marginal costing do not

cover fixed cost.

Not accepted under

accounting requirements.

Absorption costing is not

used for comparison of

products

It involves complex

overhead calculations.

Income statement as per Marginal Costing

Particulars January February

Sales Revenue (10000*25) 250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production

Overheads (10000*2) 20000 (10000*2) 20000

100000 100000

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5000/10000)*100000 50000

100000 50000

Contribution 150000 75000

Fixed production overheads 40000 40000

Fixed selling & admin Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000 -25000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

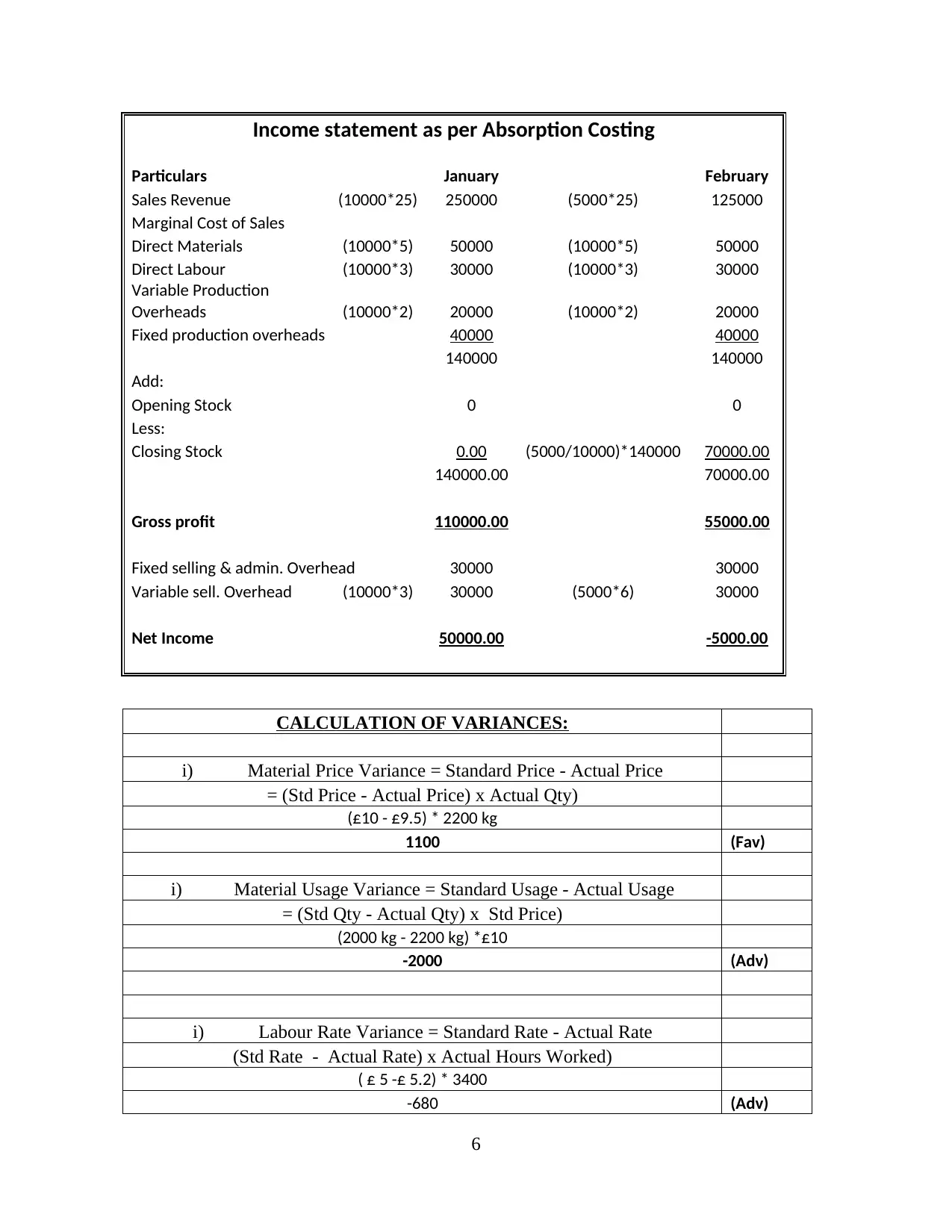

Income statement as per Absorption Costing

Particulars January February

Sales Revenue (10000*25) 250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production

Overheads (10000*2) 20000 (10000*2) 20000

Fixed production overheads 40000 40000

140000 140000

Add:

Opening Stock 0 0

Less:

Closing Stock 0.00 (5000/10000)*140000 70000.00

140000.00 70000.00

Gross profit 110000.00 55000.00

Fixed selling & admin. Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000.00 -5000.00

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£10 - £9.5) * 2200 kg

1100 (Fav)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2200 kg) *£10

-2000 (Adv)

i) Labour Rate Variance = Standard Rate - Actual Rate

(Std Rate - Actual Rate) x Actual Hours Worked)

( £ 5 -£ 5.2) * 3400

-680 (Adv)

6

Particulars January February

Sales Revenue (10000*25) 250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production

Overheads (10000*2) 20000 (10000*2) 20000

Fixed production overheads 40000 40000

140000 140000

Add:

Opening Stock 0 0

Less:

Closing Stock 0.00 (5000/10000)*140000 70000.00

140000.00 70000.00

Gross profit 110000.00 55000.00

Fixed selling & admin. Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000.00 -5000.00

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£10 - £9.5) * 2200 kg

1100 (Fav)

i) Material Usage Variance = Standard Usage - Actual Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2200 kg) *£10

-2000 (Adv)

i) Labour Rate Variance = Standard Rate - Actual Rate

(Std Rate - Actual Rate) x Actual Hours Worked)

( £ 5 -£ 5.2) * 3400

-680 (Adv)

6

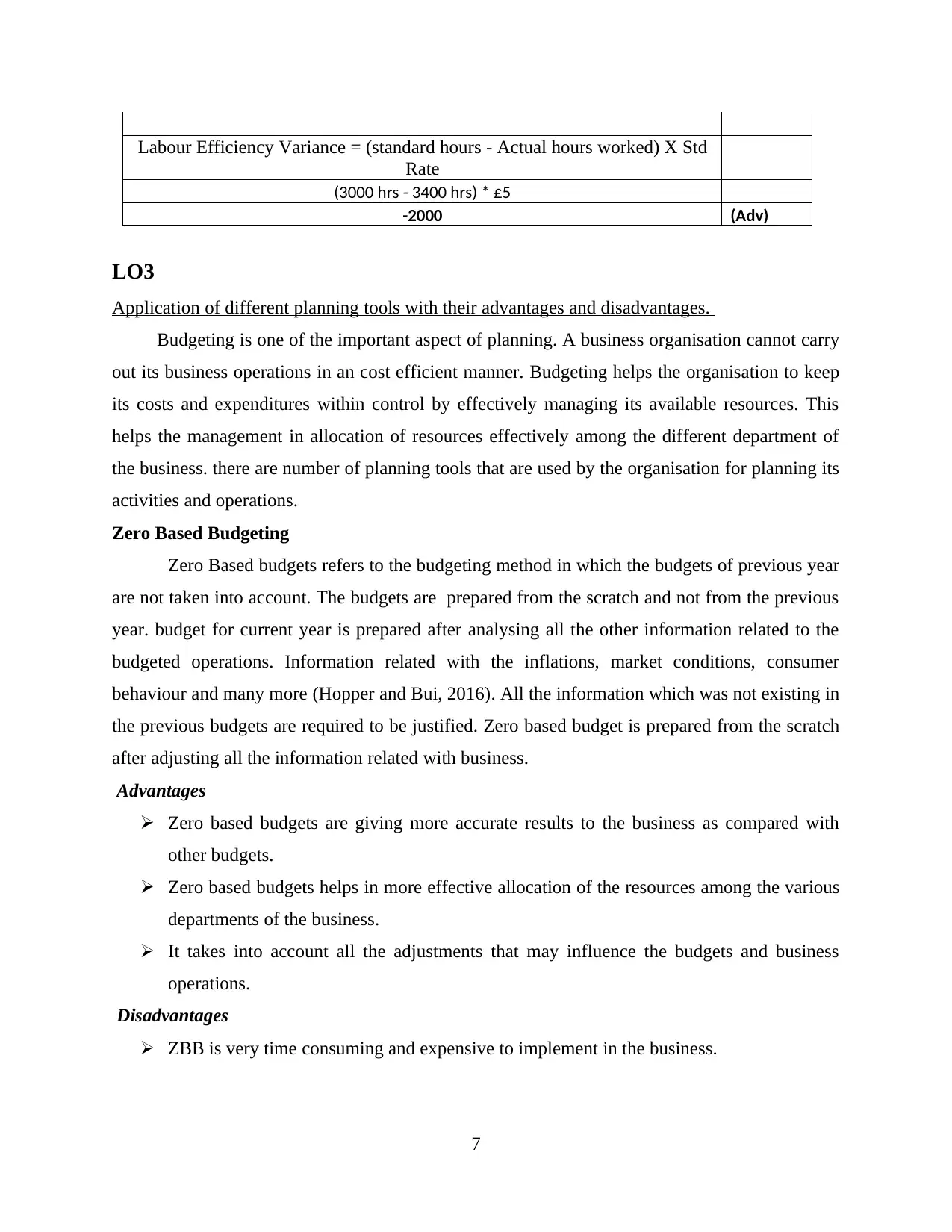

Labour Efficiency Variance = (standard hours - Actual hours worked) X Std

Rate

(3000 hrs - 3400 hrs) * £5

-2000 (Adv)

LO3

Application of different planning tools with their advantages and disadvantages.

Budgeting is one of the important aspect of planning. A business organisation cannot carry

out its business operations in an cost efficient manner. Budgeting helps the organisation to keep

its costs and expenditures within control by effectively managing its available resources. This

helps the management in allocation of resources effectively among the different department of

the business. there are number of planning tools that are used by the organisation for planning its

activities and operations.

Zero Based Budgeting

Zero Based budgets refers to the budgeting method in which the budgets of previous year

are not taken into account. The budgets are prepared from the scratch and not from the previous

year. budget for current year is prepared after analysing all the other information related to the

budgeted operations. Information related with the inflations, market conditions, consumer

behaviour and many more (Hopper and Bui, 2016). All the information which was not existing in

the previous budgets are required to be justified. Zero based budget is prepared from the scratch

after adjusting all the information related with business.

Advantages

Zero based budgets are giving more accurate results to the business as compared with

other budgets.

Zero based budgets helps in more effective allocation of the resources among the various

departments of the business.

It takes into account all the adjustments that may influence the budgets and business

operations.

Disadvantages

ZBB is very time consuming and expensive to implement in the business.

7

Rate

(3000 hrs - 3400 hrs) * £5

-2000 (Adv)

LO3

Application of different planning tools with their advantages and disadvantages.

Budgeting is one of the important aspect of planning. A business organisation cannot carry

out its business operations in an cost efficient manner. Budgeting helps the organisation to keep

its costs and expenditures within control by effectively managing its available resources. This

helps the management in allocation of resources effectively among the different department of

the business. there are number of planning tools that are used by the organisation for planning its

activities and operations.

Zero Based Budgeting

Zero Based budgets refers to the budgeting method in which the budgets of previous year

are not taken into account. The budgets are prepared from the scratch and not from the previous

year. budget for current year is prepared after analysing all the other information related to the

budgeted operations. Information related with the inflations, market conditions, consumer

behaviour and many more (Hopper and Bui, 2016). All the information which was not existing in

the previous budgets are required to be justified. Zero based budget is prepared from the scratch

after adjusting all the information related with business.

Advantages

Zero based budgets are giving more accurate results to the business as compared with

other budgets.

Zero based budgets helps in more effective allocation of the resources among the various

departments of the business.

It takes into account all the adjustments that may influence the budgets and business

operations.

Disadvantages

ZBB is very time consuming and expensive to implement in the business.

7

Budgets are prepared from the fresh that consumes more management time that could e

used in other business operations.

It is focused over the short tem goals and objectives of the business.

Activity Based Budgeting

Activity based budget refers to the system of recording, researching and analysing the

activities which leads costs for company. every activity that is incurred in the organisation are

analysed for identifying the potential efficiencies associated with the every activity. Activity

based budgets are prepared on the basis of different activities that are carried out by the

organisation. The budgets are also prepared from the fresh. The method do not considers the

previous budgets for the preparation of current budgets. These are prepared mainly on the basis

of activities that are carried out by the organisations for manufacturing of different products and

services.

Advantages

Activity based budgeting gives more accurate results as compared with the other budgets.

This helps in analysing the costs associated with the different activities instead of the

whole process.

This helps the business enterprise in reducing the cost by accurate allocation of the

resources among different activities.

Disadvantages

Budgets do not consider the budgets of previous year which makes them time consuming.

Number assumptions are required to be taken for the preparation of activity based

budgets.

The budgets are prepared on the basis of activities which may not provide accurate

results.

Operational Budgets

Operational budget are also known as the annual budget. They are similar to traditional

method of budgeting where the budget is prepared by the business on the basis of previous

budgets. Operational budget contains information related with the classification, functional and

the cost accounts. The budget is prepared by forecasting about the future revenues and

expenditures of the business. The forecasts are made on the basis of previous trends and the

8

used in other business operations.

It is focused over the short tem goals and objectives of the business.

Activity Based Budgeting

Activity based budget refers to the system of recording, researching and analysing the

activities which leads costs for company. every activity that is incurred in the organisation are

analysed for identifying the potential efficiencies associated with the every activity. Activity

based budgets are prepared on the basis of different activities that are carried out by the

organisation. The budgets are also prepared from the fresh. The method do not considers the

previous budgets for the preparation of current budgets. These are prepared mainly on the basis

of activities that are carried out by the organisations for manufacturing of different products and

services.

Advantages

Activity based budgeting gives more accurate results as compared with the other budgets.

This helps in analysing the costs associated with the different activities instead of the

whole process.

This helps the business enterprise in reducing the cost by accurate allocation of the

resources among different activities.

Disadvantages

Budgets do not consider the budgets of previous year which makes them time consuming.

Number assumptions are required to be taken for the preparation of activity based

budgets.

The budgets are prepared on the basis of activities which may not provide accurate

results.

Operational Budgets

Operational budget are also known as the annual budget. They are similar to traditional

method of budgeting where the budget is prepared by the business on the basis of previous

budgets. Operational budget contains information related with the classification, functional and

the cost accounts. The budget is prepared by forecasting about the future revenues and

expenditures of the business. The forecasts are made on the basis of previous trends and the

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

adjustments with the other information (Weetman, 2019). The budget is prepared for effectively

managing the resources by keeping the costs and expenditures under control.

Advantages

It is easy to prepare the operational budgets and easy to implement in the organisation.

Operational budget allows comparison of the budgeted figures with the actual figures of

production for identifying the variances.

This helps in effective allocation of the resources among the different business operations

for increasing the efficiency.

Disadvantages

It is difficult to accurately forecast the future income and expenses which may cause

variations.

Operational budgets do not provide the information related with the current trends.

The budgets are not flexible and do not allow the company o make adjustments

afterwards.

LO4

Organisations adapting management accounting systems for resolving the financial problems.

A business organisation operates in a highly dynamic business environment. It is important

for the business to deal with the business changes accurately. There are various financial issues

that are faced by the companies in operating the business such as scarcity of resources,

increasing cost, inventory storage costs and such other issues.

Benchmarking - It refers to a tool that is used for identifying the issues related with the

business. Benchmarking refers to setting goals to be achieved and assessing the level of success

of achieved during the given time.

KPI – Key performance indicators is also a tool used by the business for identifying the

performance of business. KPI identifies the areas due to which the required results are not

achieved.

MA Systems in resolving issues

Inventory management system is used for identifying the frequency of inventory

movements in the organisation. PQR furniture using the inventory management reduced its

increased carrying costs of storing the inventory. Company adopted the just in time approach of

9

managing the resources by keeping the costs and expenditures under control.

Advantages

It is easy to prepare the operational budgets and easy to implement in the organisation.

Operational budget allows comparison of the budgeted figures with the actual figures of

production for identifying the variances.

This helps in effective allocation of the resources among the different business operations

for increasing the efficiency.

Disadvantages

It is difficult to accurately forecast the future income and expenses which may cause

variations.

Operational budgets do not provide the information related with the current trends.

The budgets are not flexible and do not allow the company o make adjustments

afterwards.

LO4

Organisations adapting management accounting systems for resolving the financial problems.

A business organisation operates in a highly dynamic business environment. It is important

for the business to deal with the business changes accurately. There are various financial issues

that are faced by the companies in operating the business such as scarcity of resources,

increasing cost, inventory storage costs and such other issues.

Benchmarking - It refers to a tool that is used for identifying the issues related with the

business. Benchmarking refers to setting goals to be achieved and assessing the level of success

of achieved during the given time.

KPI – Key performance indicators is also a tool used by the business for identifying the

performance of business. KPI identifies the areas due to which the required results are not

achieved.

MA Systems in resolving issues

Inventory management system is used for identifying the frequency of inventory

movements in the organisation. PQR furniture using the inventory management reduced its

increased carrying costs of storing the inventory. Company adopted the just in time approach of

9

inventory management that made inventory available on demand urgently reducing the storage

cost.

Cost accounting system is used by the GLS ltd for managing the financial issue of

increasing costs. Adoption of cost accounting system helped the company in having proper

record of all the cost information and conducting variance analysis for identifying the areas

consuming costs. It took corrective measures for reducing the variances which helped in

reducing costs.

Planning tools in resolving issues

Zero based budget is adopted by the PQR for preparation of the budgets related after

analysing all the information related with the business activities (Cooper, Ezzamel and Qu,

2017). Using the budget errors and budgets of the previous years are not carried in the current

budget that helped in overcoming the mistakes of previous year.

Activities based budget used by the GLS ltd for making proper allocation of resources

among different activities. Company carries out number of operations and activity based budget

helped the organisation to allocate the resources over the activities instead of whole process that

do not allow the company to control its costs.

CONCLUSION

From the above report it could be concluded that management accounting plays critical role

in an organisation. This helps the business to manage its business operations appropriately using

MA systems. MA techniques help in accurately valuing the inventories and assessing the profit

margins. MA planning tools and systems are used by management to resolve their financial

issues and achieve sustainable success.

10

cost.

Cost accounting system is used by the GLS ltd for managing the financial issue of

increasing costs. Adoption of cost accounting system helped the company in having proper

record of all the cost information and conducting variance analysis for identifying the areas

consuming costs. It took corrective measures for reducing the variances which helped in

reducing costs.

Planning tools in resolving issues

Zero based budget is adopted by the PQR for preparation of the budgets related after

analysing all the information related with the business activities (Cooper, Ezzamel and Qu,

2017). Using the budget errors and budgets of the previous years are not carried in the current

budget that helped in overcoming the mistakes of previous year.

Activities based budget used by the GLS ltd for making proper allocation of resources

among different activities. Company carries out number of operations and activity based budget

helped the organisation to allocate the resources over the activities instead of whole process that

do not allow the company to control its costs.

CONCLUSION

From the above report it could be concluded that management accounting plays critical role

in an organisation. This helps the business to manage its business operations appropriately using

MA systems. MA techniques help in accurately valuing the inventories and assessing the profit

margins. MA planning tools and systems are used by management to resolve their financial

issues and achieve sustainable success.

10

REFERENCES

Books and Journals

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.34(2). pp.991-1025.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research.31.pp.10-30.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research.31. pp.1-9.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31.pp.103-111.

11

Books and Journals

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.34(2). pp.991-1025.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research.31.pp.10-30.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research.31. pp.1-9.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31.pp.103-111.

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.