Analysis of Management Accounting and Control at Lazy King Ltd

VerifiedAdded on 2021/02/22

|15

|4796

|175

Report

AI Summary

This report focuses on management accounting and control systems, using Lazy King Ltd., a plastic chair manufacturer, as a case study. Task 1 analyzes production plans to maximize weekly profit and evaluates cost reduction strategies using Economic Order Quantity (EOQ), Margin of Safety, and Just-in-Time methods. It includes a profit statement and recommendations for increasing production. Task 2 examines different investment options, analyzing Net Present Value (NPV) and discussing the benefits, limitations, and dysfunctional consequences of financial performance measures. The report also explores the Balance Scorecard (BSC) to reduce short-term orientation, providing a comprehensive overview of management accounting principles and their application in real-world business scenarios.

Management

Accounting &

Control Assessment

Accounting &

Control Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................4

Task 1- ............................................................................................................................................4

a. determine the production plan which will maximize the weekly profit of Lazy King Ltd and

prepare a profit statement showing the profit your plan will yield .............................................4

b. applying a response drawn from a relevant academic research, critically analyse how could

Lazy King Ltd adopt Economic order quantity (EOQ) , Margin of safety and Just-in-time in

cost reduction...............................................................................................................................6

c. critically evaluate and discuss by use of the balance score card (BSC)...................................7

Task 2...............................................................................................................................................9

(a)- Analysis of different investment options..............................................................................9

Net present value (NPV): ............................................................................................................9

(b) Benefits and limitation of each financial performance measures .......................................10

(c) Dysfunctional consequences of short-term financial performance measures and critically

discuss the adoption of balance score card (BSC) in reducing short-term orientation..............13

Conclusion ....................................................................................................................................14

References......................................................................................................................................14

Introduction......................................................................................................................................4

Task 1- ............................................................................................................................................4

a. determine the production plan which will maximize the weekly profit of Lazy King Ltd and

prepare a profit statement showing the profit your plan will yield .............................................4

b. applying a response drawn from a relevant academic research, critically analyse how could

Lazy King Ltd adopt Economic order quantity (EOQ) , Margin of safety and Just-in-time in

cost reduction...............................................................................................................................6

c. critically evaluate and discuss by use of the balance score card (BSC)...................................7

Task 2...............................................................................................................................................9

(a)- Analysis of different investment options..............................................................................9

Net present value (NPV): ............................................................................................................9

(b) Benefits and limitation of each financial performance measures .......................................10

(c) Dysfunctional consequences of short-term financial performance measures and critically

discuss the adoption of balance score card (BSC) in reducing short-term orientation..............13

Conclusion ....................................................................................................................................14

References......................................................................................................................................14

Introduction

Management accounting plays a vital role in the development of a business. It enables

the coping mechanism of an organisation by providing a range of qualitative and quantitative

solutions to the chronic problems (Bresser and Bishop, 2019). This report is dedicated on the

locus of management accounting control systems and their assessment. This study will introduce

various tools and techniques used by the organisations in modern world to reduce cost and

maximise profits. For the purpose of emancipating management accounting principles in real

scenario, Lazy king limited is chosen which is engaged in plastic chair manufacturing business.

The firm is searching for alternatives to reduce costs and increase profits. And in scenario two,

KADlex consultancy PLC is engaging in three investments options and the possible solution to

enhance performance of each investment option. The final estimation of financial performance

of proposed investment venues will heavily be based on the inferences from strategic

management accounting techniques and principles, quantitative models and advance theories

practised by the managers all over the globe. The generous attempt would seek to derive

important aspects of management accounting in dealing with real business scenarios.

Task 1-

a. determine the production plan which will maximize the weekly profit of Lazy King Ltd and

prepare a profit statement showing the profit your plan will yield

Production plan : Production plan is a planning schedule which is used to manage

production and operations activities as per the manufacturing capacity of the plant and clients

demand. This plan is made to ensure that all factors of production like raw materials, labour,

machinery, tools and equipments etc. are available at all times during the production process to

ensure smooth flow of processes (Bromwich and Walker, 2018). This planning method focuses

on estimating future demand of the products through trends, fads, customer preferences, plant

capacity etc. There are a number of production plans which can be devised by the organisation.

Some of them are as introduced :

Job method : As per this method, the manufacturing task is either handled by a worker

alone or in a group of workers. This method suffices for a small scale manufacturing firm where

the tasks are not much skilled. Chefs, saloons, tailoring etc. are the businesses which primarily

Management accounting plays a vital role in the development of a business. It enables

the coping mechanism of an organisation by providing a range of qualitative and quantitative

solutions to the chronic problems (Bresser and Bishop, 2019). This report is dedicated on the

locus of management accounting control systems and their assessment. This study will introduce

various tools and techniques used by the organisations in modern world to reduce cost and

maximise profits. For the purpose of emancipating management accounting principles in real

scenario, Lazy king limited is chosen which is engaged in plastic chair manufacturing business.

The firm is searching for alternatives to reduce costs and increase profits. And in scenario two,

KADlex consultancy PLC is engaging in three investments options and the possible solution to

enhance performance of each investment option. The final estimation of financial performance

of proposed investment venues will heavily be based on the inferences from strategic

management accounting techniques and principles, quantitative models and advance theories

practised by the managers all over the globe. The generous attempt would seek to derive

important aspects of management accounting in dealing with real business scenarios.

Task 1-

a. determine the production plan which will maximize the weekly profit of Lazy King Ltd and

prepare a profit statement showing the profit your plan will yield

Production plan : Production plan is a planning schedule which is used to manage

production and operations activities as per the manufacturing capacity of the plant and clients

demand. This plan is made to ensure that all factors of production like raw materials, labour,

machinery, tools and equipments etc. are available at all times during the production process to

ensure smooth flow of processes (Bromwich and Walker, 2018). This planning method focuses

on estimating future demand of the products through trends, fads, customer preferences, plant

capacity etc. There are a number of production plans which can be devised by the organisation.

Some of them are as introduced :

Job method : As per this method, the manufacturing task is either handled by a worker

alone or in a group of workers. This method suffices for a small scale manufacturing firm where

the tasks are not much skilled. Chefs, saloons, tailoring etc. are the businesses which primarily

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

use job method. This method is customer centric where the work is to performed as per the needs

of a customer.

Batch method : Under this method, the goods are produced in batches. It suffices the

division of labour into parts. Goods are produced in equally divided time schedules which is

based on the labour-hour relationship. A batch contains a number of bundles of products. Once a

batch is produced, the production of next batch starts. It is most commonly used by electronic

goods manufacturing firms.(Chastek and McGregor, 2012)

Flow method : This method is focused on the continuous flow of goods from one stage

of production to another stage without much interference from the labour. This method reduces

the time lag, labour costs and raw material wastage. With the help of advance infrastructure and

modern technology the work flow is automated to full capacity where all the processes happens

in a simultaneous chain.

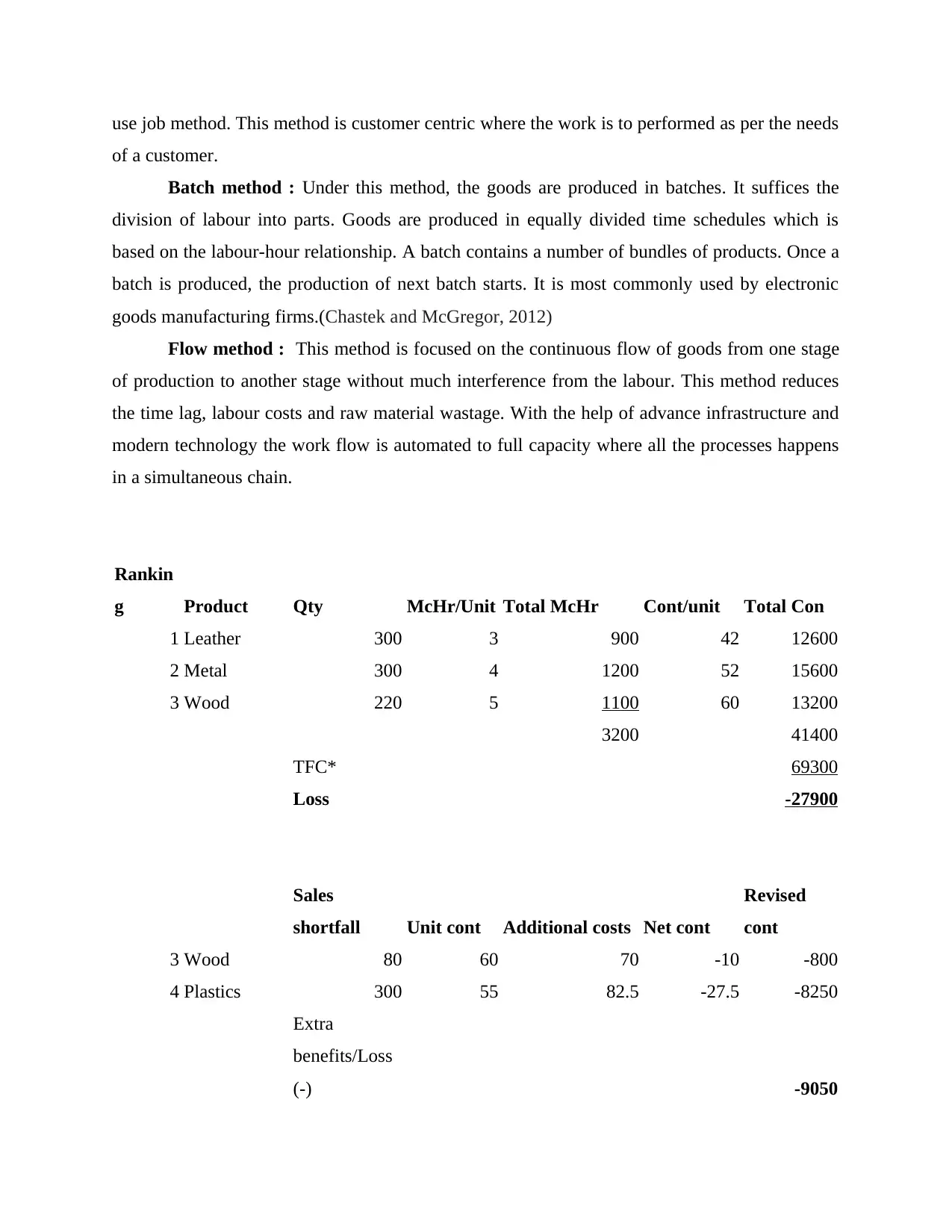

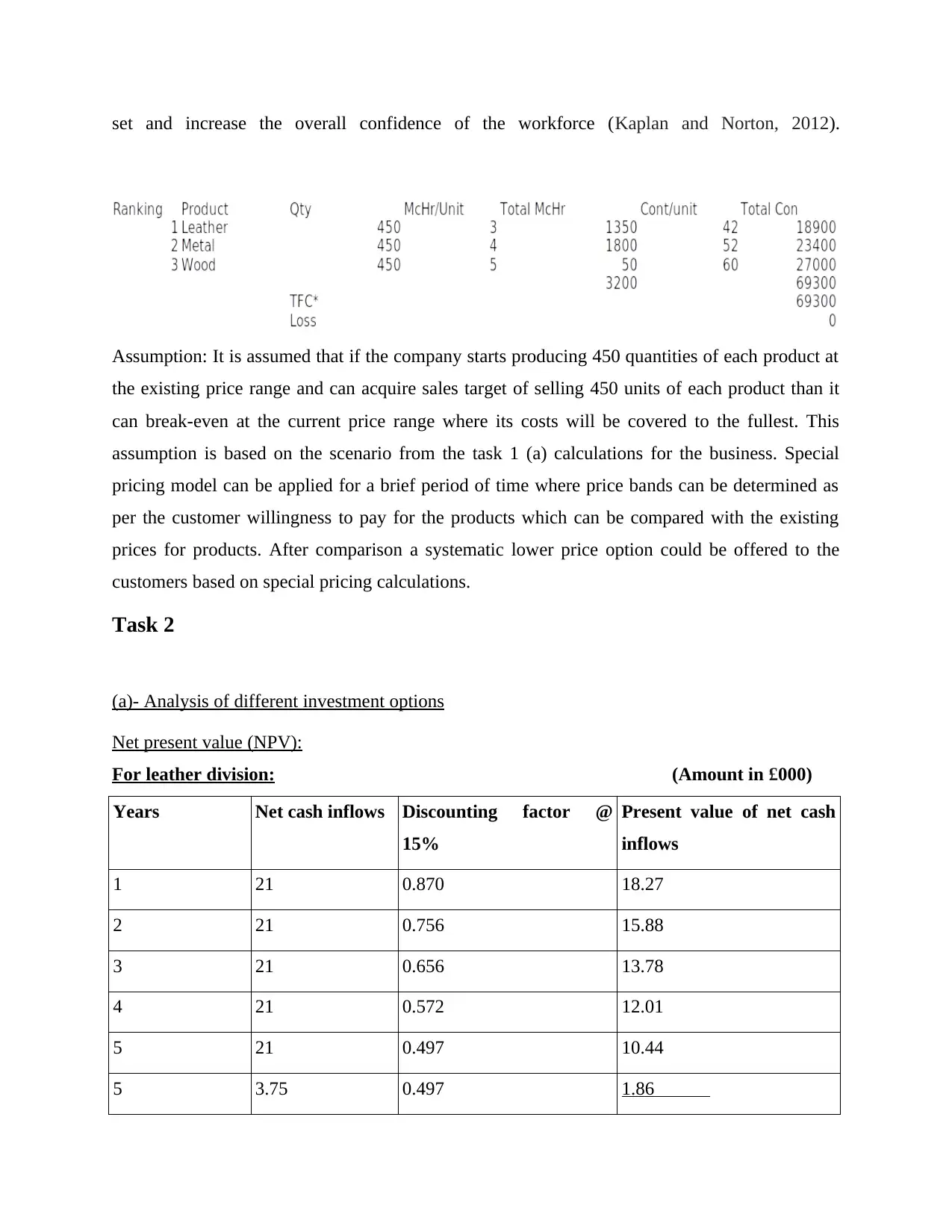

Rankin

g Product Qty McHr/Unit Total McHr Cont/unit Total Con

1 Leather 300 3 900 42 12600

2 Metal 300 4 1200 52 15600

3 Wood 220 5 1100 60 13200

3200 41400

TFC* 69300

Loss -27900

Sales

shortfall Unit cont Additional costs Net cont

Revised

cont

3 Wood 80 60 70 -10 -800

4 Plastics 300 55 82.5 -27.5 -8250

Extra

benefits/Loss

(-) -9050

of a customer.

Batch method : Under this method, the goods are produced in batches. It suffices the

division of labour into parts. Goods are produced in equally divided time schedules which is

based on the labour-hour relationship. A batch contains a number of bundles of products. Once a

batch is produced, the production of next batch starts. It is most commonly used by electronic

goods manufacturing firms.(Chastek and McGregor, 2012)

Flow method : This method is focused on the continuous flow of goods from one stage

of production to another stage without much interference from the labour. This method reduces

the time lag, labour costs and raw material wastage. With the help of advance infrastructure and

modern technology the work flow is automated to full capacity where all the processes happens

in a simultaneous chain.

Rankin

g Product Qty McHr/Unit Total McHr Cont/unit Total Con

1 Leather 300 3 900 42 12600

2 Metal 300 4 1200 52 15600

3 Wood 220 5 1100 60 13200

3200 41400

TFC* 69300

Loss -27900

Sales

shortfall Unit cont Additional costs Net cont

Revised

cont

3 Wood 80 60 70 -10 -800

4 Plastics 300 55 82.5 -27.5 -8250

Extra

benefits/Loss

(-) -9050

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

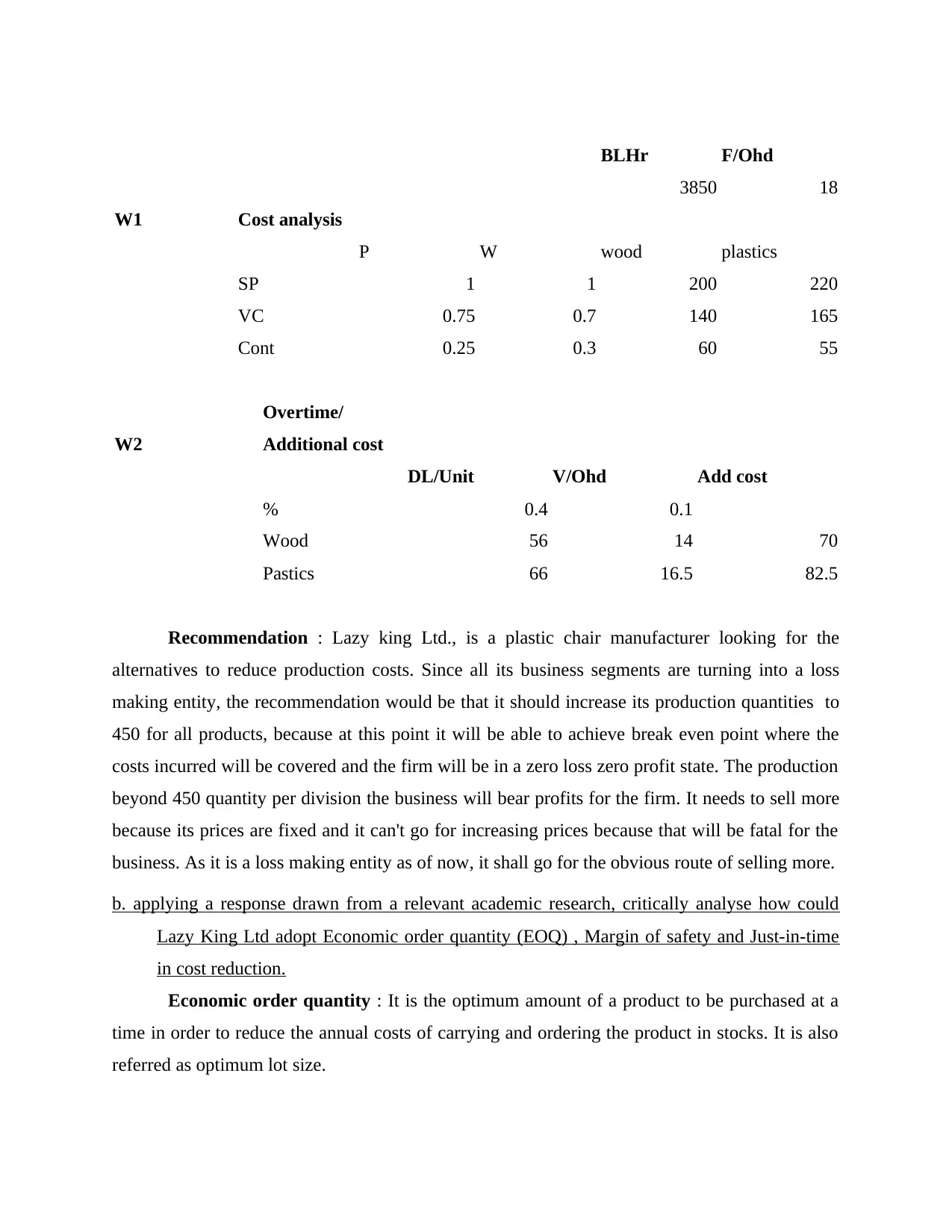

BLHr F/Ohd

3850 18

W1 Cost analysis

P W wood plastics

SP 1 1 200 220

VC 0.75 0.7 140 165

Cont 0.25 0.3 60 55

W2

Overtime/

Additional cost

DL/Unit V/Ohd Add cost

% 0.4 0.1

Wood 56 14 70

Pastics 66 16.5 82.5

Recommendation : Lazy king Ltd., is a plastic chair manufacturer looking for the

alternatives to reduce production costs. Since all its business segments are turning into a loss

making entity, the recommendation would be that it should increase its production quantities to

450 for all products, because at this point it will be able to achieve break even point where the

costs incurred will be covered and the firm will be in a zero loss zero profit state. The production

beyond 450 quantity per division the business will bear profits for the firm. It needs to sell more

because its prices are fixed and it can't go for increasing prices because that will be fatal for the

business. As it is a loss making entity as of now, it shall go for the obvious route of selling more.

b. applying a response drawn from a relevant academic research, critically analyse how could

Lazy King Ltd adopt Economic order quantity (EOQ) , Margin of safety and Just-in-time

in cost reduction.

Economic order quantity : It is the optimum amount of a product to be purchased at a

time in order to reduce the annual costs of carrying and ordering the product in stocks. It is also

referred as optimum lot size.

3850 18

W1 Cost analysis

P W wood plastics

SP 1 1 200 220

VC 0.75 0.7 140 165

Cont 0.25 0.3 60 55

W2

Overtime/

Additional cost

DL/Unit V/Ohd Add cost

% 0.4 0.1

Wood 56 14 70

Pastics 66 16.5 82.5

Recommendation : Lazy king Ltd., is a plastic chair manufacturer looking for the

alternatives to reduce production costs. Since all its business segments are turning into a loss

making entity, the recommendation would be that it should increase its production quantities to

450 for all products, because at this point it will be able to achieve break even point where the

costs incurred will be covered and the firm will be in a zero loss zero profit state. The production

beyond 450 quantity per division the business will bear profits for the firm. It needs to sell more

because its prices are fixed and it can't go for increasing prices because that will be fatal for the

business. As it is a loss making entity as of now, it shall go for the obvious route of selling more.

b. applying a response drawn from a relevant academic research, critically analyse how could

Lazy King Ltd adopt Economic order quantity (EOQ) , Margin of safety and Just-in-time

in cost reduction.

Economic order quantity : It is the optimum amount of a product to be purchased at a

time in order to reduce the annual costs of carrying and ordering the product in stocks. It is also

referred as optimum lot size.

Use in cost reduction : EOQ technique can help Lazy King Limited in reducing the

ordering and carrying costs for the inventory at a time. This method provides a model for

evaluating the most feasible reorder point and the optimum reorder quantity which ensures

optimum availability of inventory. This method reviews the level of stocks at all times and

ensures a fixed reorder quantity every time a product reaches to a specific point.

Margin of safety : It is the ratio that is used to measure the amount of sales exceeding

beyond the break even point. It is the margin of profit earned by the firm after meeting all the

fixed and variable costs associated with the production of goods. This represents the amount of

sales which a company may start to loose before it actually starts loosing the money.

Use in cost reduction : This technique can help Lazy king limited by ensuring the

minimum level of safety above the break even point of the operations. If margin of safety is

assisted by higher fixed costs and higher contribution margin , actions shall be called for

reducing the fixed cost or enhance sales, however, if the margin of safety and the contribution

are low, the situation demands decrease in variable costs or an increase in sales price will be

effected.

Just-in-time : It is an inventory management technique in which the raw material order

of the company is aligned with the suppliers directly in a production schedule. This technique

aligns ordering and supplies in such way that the raw materials will be delivered to the firm only

when it needs them. It reduces the inventory handling costs of the firm, reduces wastage and

increases efficiency (Govindarajan and Gupta, 2015).

Use in reduction of costs : This technique will be very beneficial to Lazy king limited as

this method reduces the gap between the ordering of raw material and the delivery. The extra

costs which a business usually bears to manage inventory, warehousing, care taking, scrap easily

gets eliminated to zilch, which in turn leads to cost saving for the business.

Life cycle costing: As opposed to the principle of traditional costing, the life cycle

costing approach allocates costs to full production cycle of the product right from the planning

phase to the decline stage, from its pre production phase to its post manufacturing phase. This

technique results in better planning as cost containment can be done better at the planning stage

itself rather than the initiation of manufacturing stage.

Activity based management: As per this method, costs are assigned to each activity that

form the part of business scenario. All activities are allocated costs and cost drivers which mark

ordering and carrying costs for the inventory at a time. This method provides a model for

evaluating the most feasible reorder point and the optimum reorder quantity which ensures

optimum availability of inventory. This method reviews the level of stocks at all times and

ensures a fixed reorder quantity every time a product reaches to a specific point.

Margin of safety : It is the ratio that is used to measure the amount of sales exceeding

beyond the break even point. It is the margin of profit earned by the firm after meeting all the

fixed and variable costs associated with the production of goods. This represents the amount of

sales which a company may start to loose before it actually starts loosing the money.

Use in cost reduction : This technique can help Lazy king limited by ensuring the

minimum level of safety above the break even point of the operations. If margin of safety is

assisted by higher fixed costs and higher contribution margin , actions shall be called for

reducing the fixed cost or enhance sales, however, if the margin of safety and the contribution

are low, the situation demands decrease in variable costs or an increase in sales price will be

effected.

Just-in-time : It is an inventory management technique in which the raw material order

of the company is aligned with the suppliers directly in a production schedule. This technique

aligns ordering and supplies in such way that the raw materials will be delivered to the firm only

when it needs them. It reduces the inventory handling costs of the firm, reduces wastage and

increases efficiency (Govindarajan and Gupta, 2015).

Use in reduction of costs : This technique will be very beneficial to Lazy king limited as

this method reduces the gap between the ordering of raw material and the delivery. The extra

costs which a business usually bears to manage inventory, warehousing, care taking, scrap easily

gets eliminated to zilch, which in turn leads to cost saving for the business.

Life cycle costing: As opposed to the principle of traditional costing, the life cycle

costing approach allocates costs to full production cycle of the product right from the planning

phase to the decline stage, from its pre production phase to its post manufacturing phase. This

technique results in better planning as cost containment can be done better at the planning stage

itself rather than the initiation of manufacturing stage.

Activity based management: As per this method, costs are assigned to each activity that

form the part of business scenario. All activities are allocated costs and cost drivers which mark

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

up to the cost levels for the organisation. Through this technique costs can easily be identified

which helps in total cost allocation and management of costs.

Benchmarking: It is technique under which organisational important activities and

processes are matched up with the worlds best renowned management practices. This technique

helps the business in evaluating its performance based on standards and motivate employees to

strive for the set targets as offered through benchmarked positions.

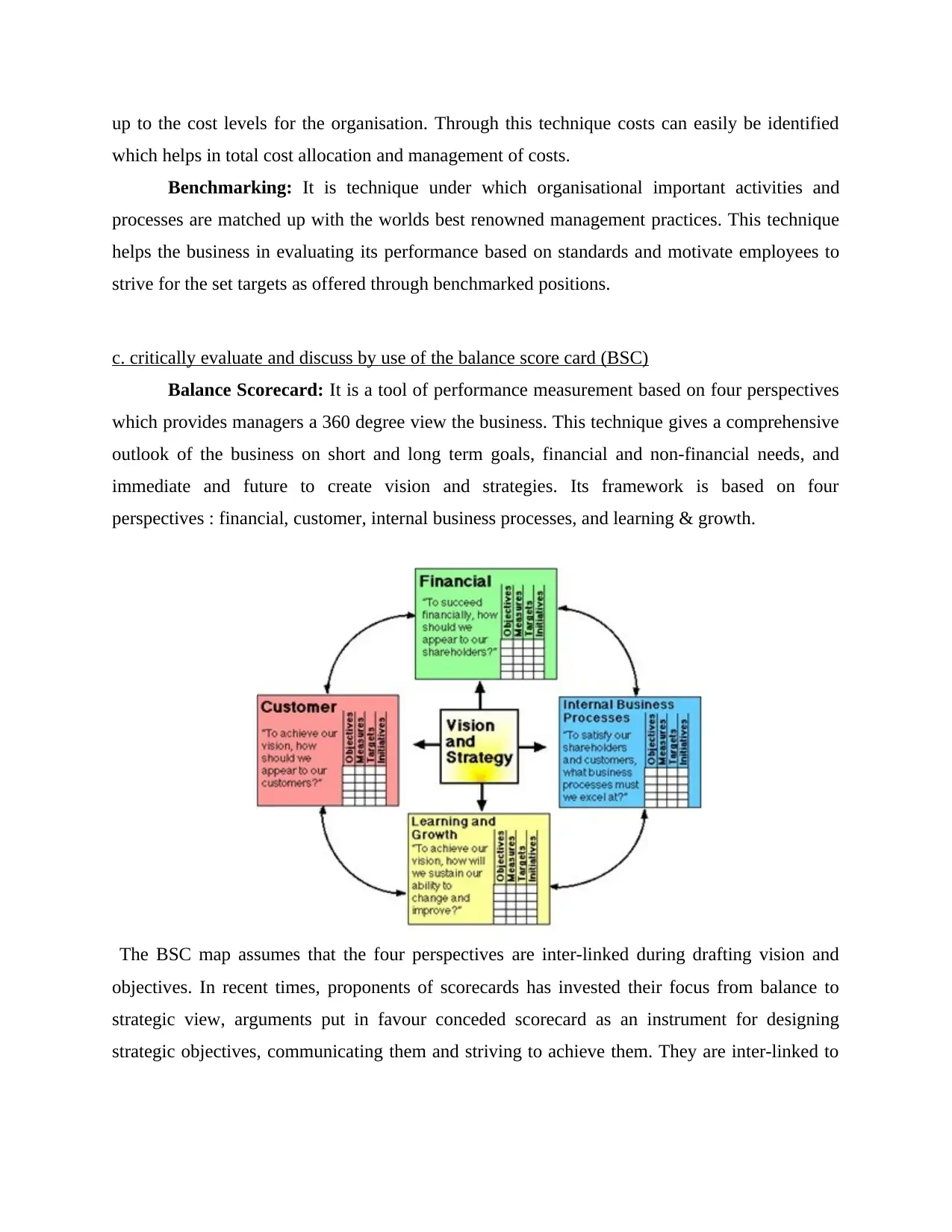

c. critically evaluate and discuss by use of the balance score card (BSC)

Balance Scorecard: It is a tool of performance measurement based on four perspectives

which provides managers a 360 degree view the business. This technique gives a comprehensive

outlook of the business on short and long term goals, financial and non-financial needs, and

immediate and future to create vision and strategies. Its framework is based on four

perspectives : financial, customer, internal business processes, and learning & growth.

The BSC map assumes that the four perspectives are inter-linked during drafting vision and

objectives. In recent times, proponents of scorecards has invested their focus from balance to

strategic view, arguments put in favour conceded scorecard as an instrument for designing

strategic objectives, communicating them and striving to achieve them. They are inter-linked to

which helps in total cost allocation and management of costs.

Benchmarking: It is technique under which organisational important activities and

processes are matched up with the worlds best renowned management practices. This technique

helps the business in evaluating its performance based on standards and motivate employees to

strive for the set targets as offered through benchmarked positions.

c. critically evaluate and discuss by use of the balance score card (BSC)

Balance Scorecard: It is a tool of performance measurement based on four perspectives

which provides managers a 360 degree view the business. This technique gives a comprehensive

outlook of the business on short and long term goals, financial and non-financial needs, and

immediate and future to create vision and strategies. Its framework is based on four

perspectives : financial, customer, internal business processes, and learning & growth.

The BSC map assumes that the four perspectives are inter-linked during drafting vision and

objectives. In recent times, proponents of scorecards has invested their focus from balance to

strategic view, arguments put in favour conceded scorecard as an instrument for designing

strategic objectives, communicating them and striving to achieve them. They are inter-linked to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

strategy through ''strategy map'' as referred as “value driver map”. Maps translate the vision into

examinable hypotheses to increase “strategic learning”.

BSC model for Lazy king Limited

Financial perspective : The company is seeking to increase its profits/net cash inflows in

short term. But is lagging behind in labour hours utilisation to the full. The company wishes to

increase its net revenue as indicated in the statements prepared. The indication is to appreciate

shareholder value as to the satisfaction of the customers. But due to uncertainties that arose due

to non profitability of labour , non availability of labour hours, external restrictions like

Malaysian government ultimatum & US climate change treaty has played critical role in

declining profits of the firm (Grant, 2013). The idea is to increase the profits by focusing on

manufacturing single type plastic chairs only for which initiatives has been taken.

Customer perspective : The problem with lazy king is that it could not manufacture up to

the demands of clients. The problem could be addressed only through increasing production with

full plant capacity. The variable and fixed costs are also varying at a high rate and labour rates

are steeper as compared to the normal labour rates. The company identifies customer value

through the orders per lot received. To increase the customer satisfaction, company has planned

to increase production overtime to satisfy clients and decrease product line to single plastic chair

line.

Internal process perspective : Lazy king limited strives to increase its customer

satisfaction value by increasing efficiency of its production. To achieve the targets of the firm, it

should strive for new production plan technique and a set of statistical tools like EOQ, Just in

time etc. shall be integrated with the total production plan to increase the efficiency of the

business processes.

Learning and growth perspective : The major problem faced by the organisation in

terms of labour is that of non productivity of the labour and the non-utilisation of full labour

hours assigned to each unit of production. To overcome this problem, the organisation needs to

design new training and development programmes for the workers to be relevant with the skill

examinable hypotheses to increase “strategic learning”.

BSC model for Lazy king Limited

Financial perspective : The company is seeking to increase its profits/net cash inflows in

short term. But is lagging behind in labour hours utilisation to the full. The company wishes to

increase its net revenue as indicated in the statements prepared. The indication is to appreciate

shareholder value as to the satisfaction of the customers. But due to uncertainties that arose due

to non profitability of labour , non availability of labour hours, external restrictions like

Malaysian government ultimatum & US climate change treaty has played critical role in

declining profits of the firm (Grant, 2013). The idea is to increase the profits by focusing on

manufacturing single type plastic chairs only for which initiatives has been taken.

Customer perspective : The problem with lazy king is that it could not manufacture up to

the demands of clients. The problem could be addressed only through increasing production with

full plant capacity. The variable and fixed costs are also varying at a high rate and labour rates

are steeper as compared to the normal labour rates. The company identifies customer value

through the orders per lot received. To increase the customer satisfaction, company has planned

to increase production overtime to satisfy clients and decrease product line to single plastic chair

line.

Internal process perspective : Lazy king limited strives to increase its customer

satisfaction value by increasing efficiency of its production. To achieve the targets of the firm, it

should strive for new production plan technique and a set of statistical tools like EOQ, Just in

time etc. shall be integrated with the total production plan to increase the efficiency of the

business processes.

Learning and growth perspective : The major problem faced by the organisation in

terms of labour is that of non productivity of the labour and the non-utilisation of full labour

hours assigned to each unit of production. To overcome this problem, the organisation needs to

design new training and development programmes for the workers to be relevant with the skill

set and increase the overall confidence of the workforce (Kaplan and Norton, 2012).

Assumption: It is assumed that if the company starts producing 450 quantities of each product at

the existing price range and can acquire sales target of selling 450 units of each product than it

can break-even at the current price range where its costs will be covered to the fullest. This

assumption is based on the scenario from the task 1 (a) calculations for the business. Special

pricing model can be applied for a brief period of time where price bands can be determined as

per the customer willingness to pay for the products which can be compared with the existing

prices for products. After comparison a systematic lower price option could be offered to the

customers based on special pricing calculations.

Task 2

(a)- Analysis of different investment options

Net present value (NPV):

For leather division: (Amount in £000)

Years Net cash inflows Discounting factor @

15%

Present value of net cash

inflows

1 21 0.870 18.27

2 21 0.756 15.88

3 21 0.656 13.78

4 21 0.572 12.01

5 21 0.497 10.44

5 3.75 0.497 1.86

Assumption: It is assumed that if the company starts producing 450 quantities of each product at

the existing price range and can acquire sales target of selling 450 units of each product than it

can break-even at the current price range where its costs will be covered to the fullest. This

assumption is based on the scenario from the task 1 (a) calculations for the business. Special

pricing model can be applied for a brief period of time where price bands can be determined as

per the customer willingness to pay for the products which can be compared with the existing

prices for products. After comparison a systematic lower price option could be offered to the

customers based on special pricing calculations.

Task 2

(a)- Analysis of different investment options

Net present value (NPV):

For leather division: (Amount in £000)

Years Net cash inflows Discounting factor @

15%

Present value of net cash

inflows

1 21 0.870 18.27

2 21 0.756 15.88

3 21 0.656 13.78

4 21 0.572 12.01

5 21 0.497 10.44

5 3.75 0.497 1.86

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

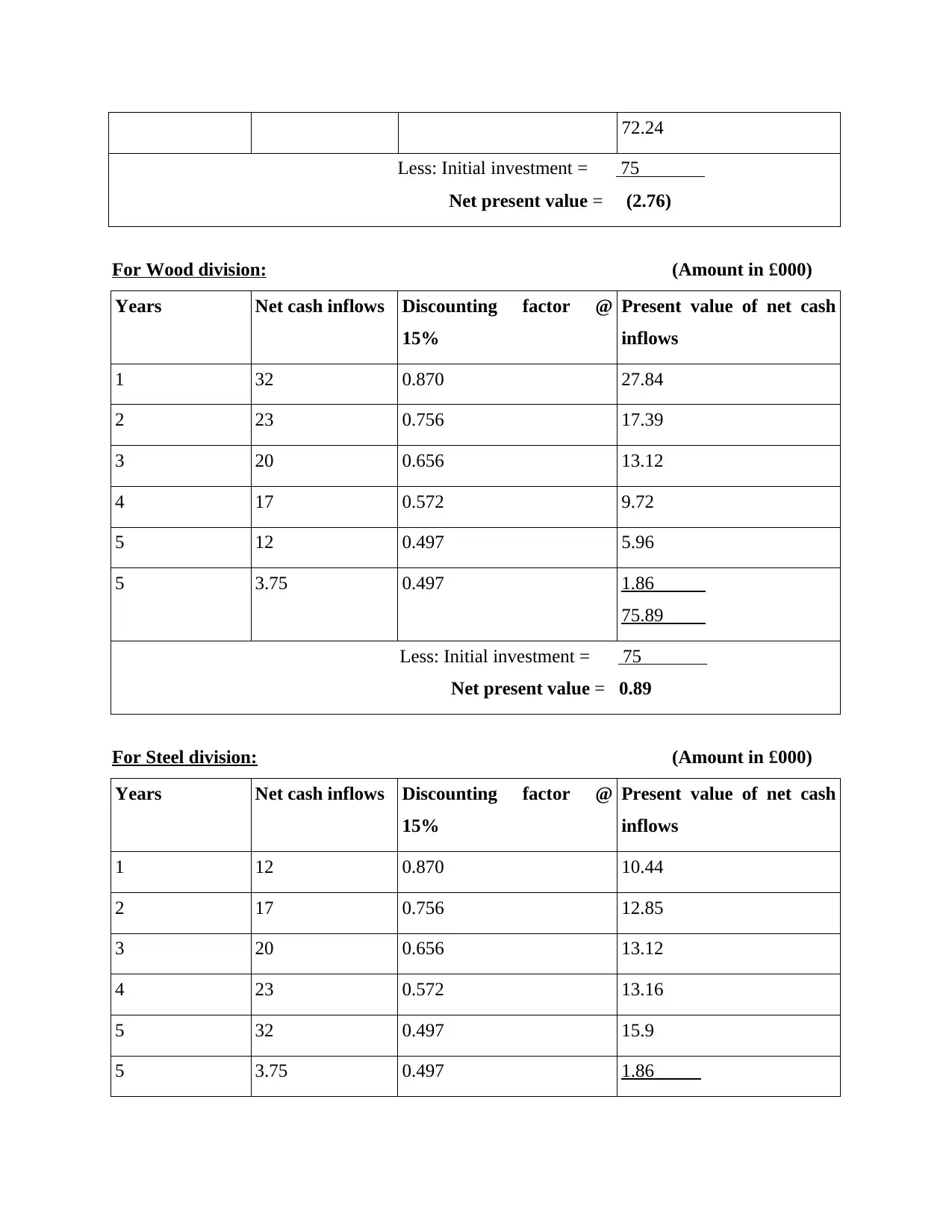

72.24

Less: Initial investment = 75

Net present value = (2.76)

For Wood division: (Amount in £000)

Years Net cash inflows Discounting factor @

15%

Present value of net cash

inflows

1 32 0.870 27.84

2 23 0.756 17.39

3 20 0.656 13.12

4 17 0.572 9.72

5 12 0.497 5.96

5 3.75 0.497 1.86

75.89

Less: Initial investment = 75

Net present value = 0.89

For Steel division: (Amount in £000)

Years Net cash inflows Discounting factor @

15%

Present value of net cash

inflows

1 12 0.870 10.44

2 17 0.756 12.85

3 20 0.656 13.12

4 23 0.572 13.16

5 32 0.497 15.9

5 3.75 0.497 1.86

Less: Initial investment = 75

Net present value = (2.76)

For Wood division: (Amount in £000)

Years Net cash inflows Discounting factor @

15%

Present value of net cash

inflows

1 32 0.870 27.84

2 23 0.756 17.39

3 20 0.656 13.12

4 17 0.572 9.72

5 12 0.497 5.96

5 3.75 0.497 1.86

75.89

Less: Initial investment = 75

Net present value = 0.89

For Steel division: (Amount in £000)

Years Net cash inflows Discounting factor @

15%

Present value of net cash

inflows

1 12 0.870 10.44

2 17 0.756 12.85

3 20 0.656 13.12

4 23 0.572 13.16

5 32 0.497 15.9

5 3.75 0.497 1.86

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

67.33

Less: Initial investment = 75

Net present value = (7.67)

Note: Residual value of fixed assets is 5% of original cost, therefore, it is £ 3750 (i.e. 5% of 75 )

Recommendation : On the basis of the above analysis, it could be comprehended that the

Kadlex consultancy should invest in wood division as it has the positive net present value as

compared to other two options.

(b) Benefits and limitation of each financial performance measures

Kadlex consultancy has after the acquisition of LK Ltd. Has changed the orientation of

business from the functional structure to a divisional structure. The organisation has given

substantial autonomy to each divisional manager with the power to select Investment project.

The financial performance measure inter linked with remuneration of managers as devised by the

organisation are return on investment (ROI), residual income (RI) and economic value added

(EVA). To understand the benefits and limitation of each financial performance measure a

critical analysis of each measure has been carried out as follows :

Return on investment : It is a quantitative ratio used to evaluate the benefits the

organisation will receive on the investment in relationship with the investment cost. It is

calculated as net income divided by the capital cost of investment proposed. Higher the ratio,

higher will be the profit. ROI has been a very fancy metric for the firms because of the versatility

and the efficiency (Maas, Schaltegger and Crutzen, 2016). The simple interpretation of ROI is

that if it is positive go for the investment and if it negative devoid investment idea. Kapex

consultancy has introduced this method after the fall of earlier production plans of LK ltd. Which

could have possibly fell down. This method is used to ensure that the financial performance is

intact.

Merits

The primary benefit it offers is that investor can most easily and quickly can check the

prospects of the investment and the feasibility of it. This results in saving of time and

funds of the firm (Silk, 2018).

Less: Initial investment = 75

Net present value = (7.67)

Note: Residual value of fixed assets is 5% of original cost, therefore, it is £ 3750 (i.e. 5% of 75 )

Recommendation : On the basis of the above analysis, it could be comprehended that the

Kadlex consultancy should invest in wood division as it has the positive net present value as

compared to other two options.

(b) Benefits and limitation of each financial performance measures

Kadlex consultancy has after the acquisition of LK Ltd. Has changed the orientation of

business from the functional structure to a divisional structure. The organisation has given

substantial autonomy to each divisional manager with the power to select Investment project.

The financial performance measure inter linked with remuneration of managers as devised by the

organisation are return on investment (ROI), residual income (RI) and economic value added

(EVA). To understand the benefits and limitation of each financial performance measure a

critical analysis of each measure has been carried out as follows :

Return on investment : It is a quantitative ratio used to evaluate the benefits the

organisation will receive on the investment in relationship with the investment cost. It is

calculated as net income divided by the capital cost of investment proposed. Higher the ratio,

higher will be the profit. ROI has been a very fancy metric for the firms because of the versatility

and the efficiency (Maas, Schaltegger and Crutzen, 2016). The simple interpretation of ROI is

that if it is positive go for the investment and if it negative devoid investment idea. Kapex

consultancy has introduced this method after the fall of earlier production plans of LK ltd. Which

could have possibly fell down. This method is used to ensure that the financial performance is

intact.

Merits

The primary benefit it offers is that investor can most easily and quickly can check the

prospects of the investment and the feasibility of it. This results in saving of time and

funds of the firm (Silk, 2018).

It is very easy to comprehend and measure the investment easily, It also helps in

identifying the potential competition engaged around.

Demerits

It is hard to determine the true connotation of profit and investment because there is no

single precursor to define the two elements precisely. The valuation itself sometimes a

vague system.

It is not easy to compare ROI of two different entities until and unless they both have

divulged same methods and techniques to calculate various ratios.

Residual income (RI) : It is the net income amount achieved in excess to the minimum

rate of return. This technique has been very instrumental in measuring corporate performance

where the locus is on the returns earned in relation to the minimum desired return. Alternatively,

it is the amount of income left after meeting all the debts and expenses. It is measured by

considering all costs to capital required in generation of the income. It basically for the Kapex

consultancy is the excess income over opportunity cost of the total capital employed in the

business. It is quite useful in allocating funds to the projects. A positive RI would certainly mean

that the organisation has met the minimum returns required condition meanwhile a negative RI

would mean that the organisation has failed in meeting the criteria (Marginson, McAulay, Roush

and Van Zijl, 2010).

Merits

The primary benefit of it is that if once the organisation has achieved the feat of residual

income, It is easy to maintain throughout. Income keeps on generating beyond the point,

because the firm gets an idea as to how much it has to work in order to maintain the ratio. It encourages the investment managers to indulge in new investments if they increase in

more RI. A new RI may reduce the ROI but wouldn't be counted as dysfunctional

behaviour as it considered to be a best decision for the firm (Ross, 2015).

Demerits

It doesn't help in facilitating comparison between several divisions because it is driven by

the structure and relative size and their investments.

It is characterised by the accounting measures employed in profits and capital which

could be manipulated subject to pilferage or illicit behaviour of the user.

identifying the potential competition engaged around.

Demerits

It is hard to determine the true connotation of profit and investment because there is no

single precursor to define the two elements precisely. The valuation itself sometimes a

vague system.

It is not easy to compare ROI of two different entities until and unless they both have

divulged same methods and techniques to calculate various ratios.

Residual income (RI) : It is the net income amount achieved in excess to the minimum

rate of return. This technique has been very instrumental in measuring corporate performance

where the locus is on the returns earned in relation to the minimum desired return. Alternatively,

it is the amount of income left after meeting all the debts and expenses. It is measured by

considering all costs to capital required in generation of the income. It basically for the Kapex

consultancy is the excess income over opportunity cost of the total capital employed in the

business. It is quite useful in allocating funds to the projects. A positive RI would certainly mean

that the organisation has met the minimum returns required condition meanwhile a negative RI

would mean that the organisation has failed in meeting the criteria (Marginson, McAulay, Roush

and Van Zijl, 2010).

Merits

The primary benefit of it is that if once the organisation has achieved the feat of residual

income, It is easy to maintain throughout. Income keeps on generating beyond the point,

because the firm gets an idea as to how much it has to work in order to maintain the ratio. It encourages the investment managers to indulge in new investments if they increase in

more RI. A new RI may reduce the ROI but wouldn't be counted as dysfunctional

behaviour as it considered to be a best decision for the firm (Ross, 2015).

Demerits

It doesn't help in facilitating comparison between several divisions because it is driven by

the structure and relative size and their investments.

It is characterised by the accounting measures employed in profits and capital which

could be manipulated subject to pilferage or illicit behaviour of the user.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.